Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

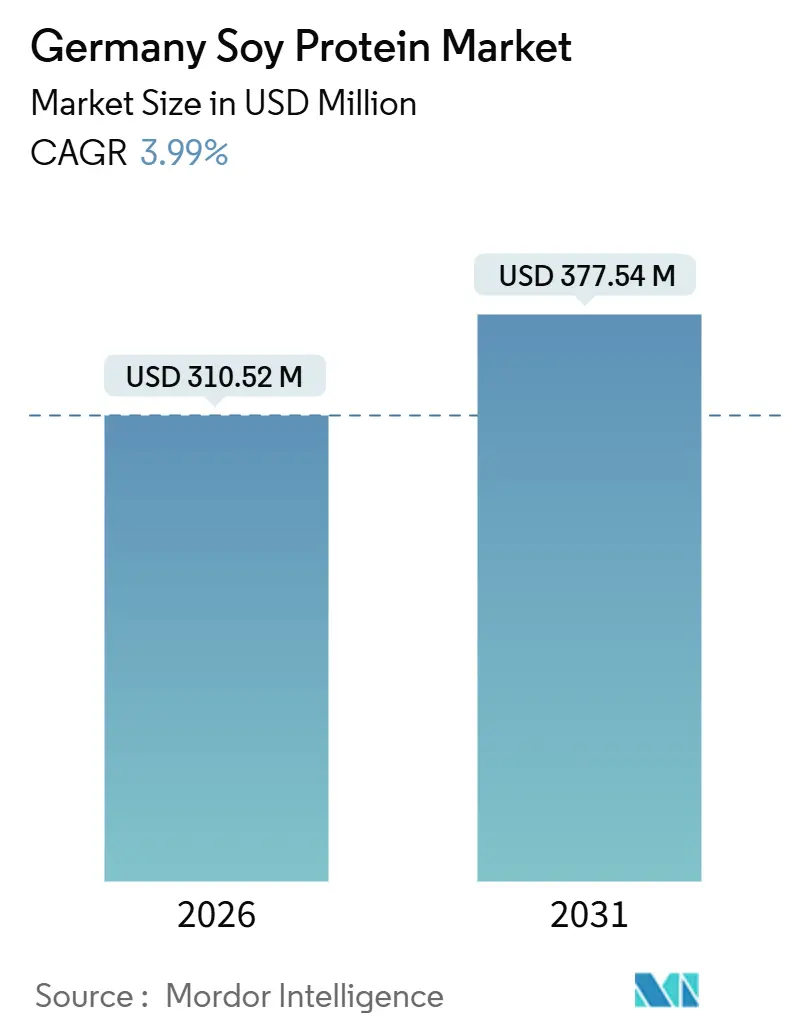

| Market Size (2026) | USD 310.52 Million |

| Market Size (2031) | USD 377.54 Million |

| Growth Rate (2026 - 2031) | 3.99% CAGR |

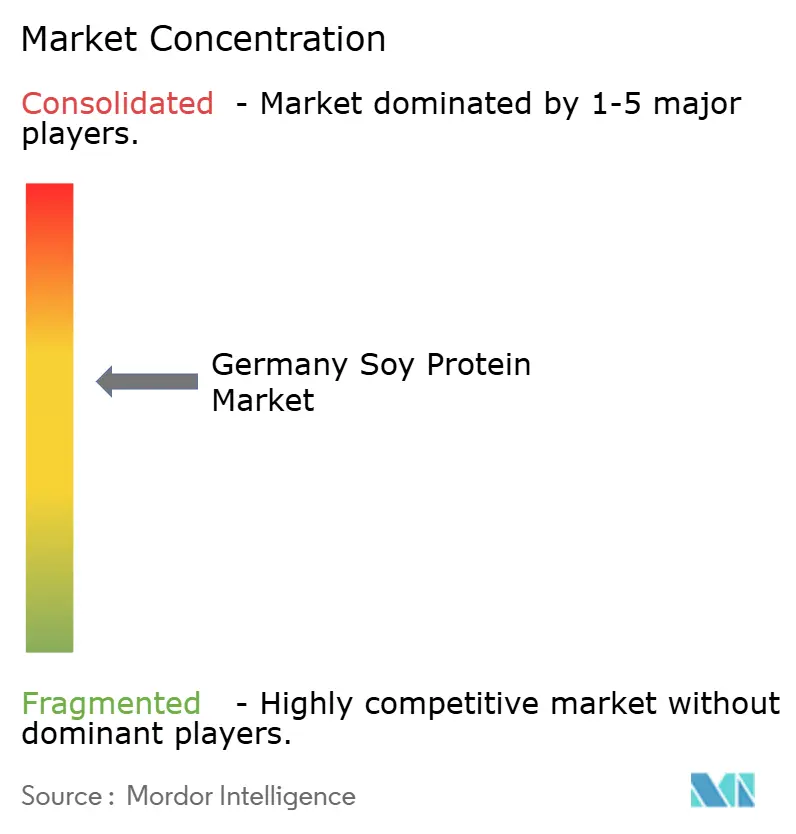

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Soy Protein Market Analysis by Mordor Intelligence

The Germany soy protein market size stood at USD 310.52 million in 2026 and is forecast to reach USD 377.54 million by 2031, advancing at a 3.99% CAGR through the period. This growth is driven by rising flexitarian demand, the cost-effectiveness of soy concentrates, and ongoing research and development in high-moisture extrusion technology. However, processors face challenges, including allergen concerns, fluctuations in raw material prices, and new traceability requirements from the EU Deforestation Regulation set for December 2024[1]Source: European Commission, “Regulation on Deforestation-Free Products,” ec.europa.eu. While competitive intensity is moderate, multinationals with crushing assets in Hamburg and the Ruhr Valley dominate, and mid-tier specialists focus on organic, non-GMO, and high-moisture texturates. Additionally, the Federal Ministry of Food and Agriculture’s National Protein Strategy bolsters the market's prospects, co-funding soybean and pulse cultivation and supporting extrusion pilot lines.

Key Report Takeaways

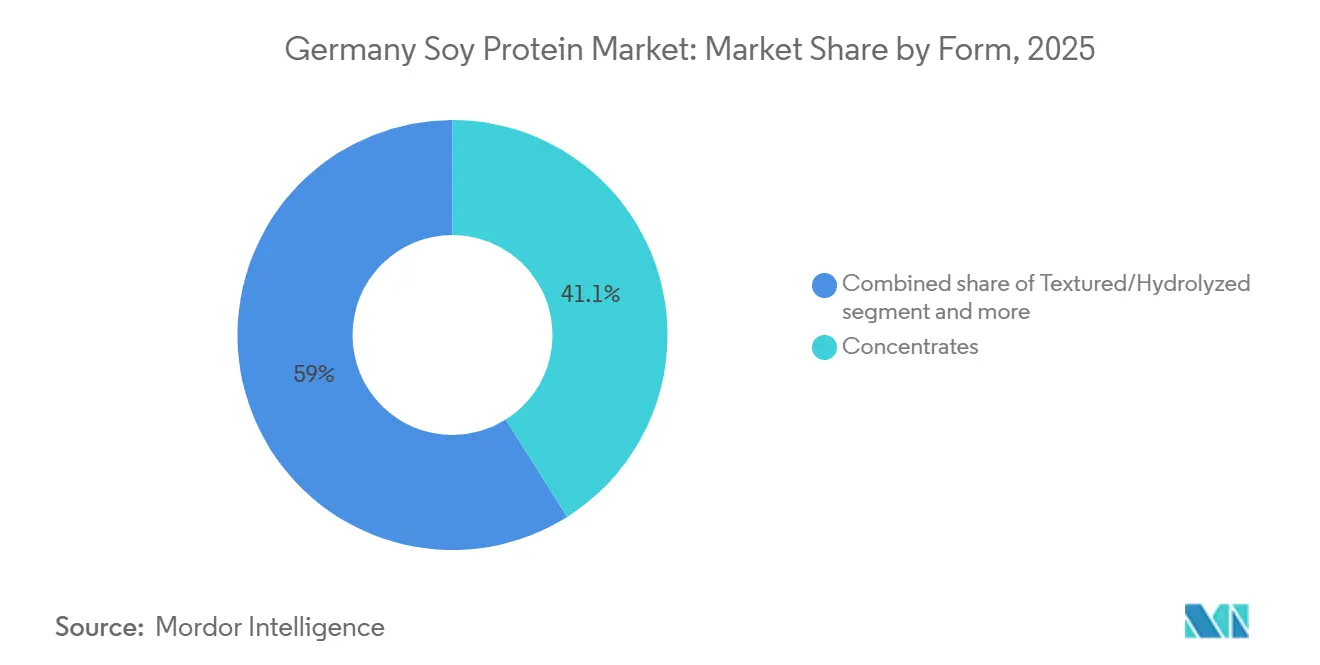

- By form, concentrates captured 41.05% of the Germany soy protein market share in 2025, whereas textured and hydrolyzed variants are projected to grow at a 4.80% CAGR through 2031.

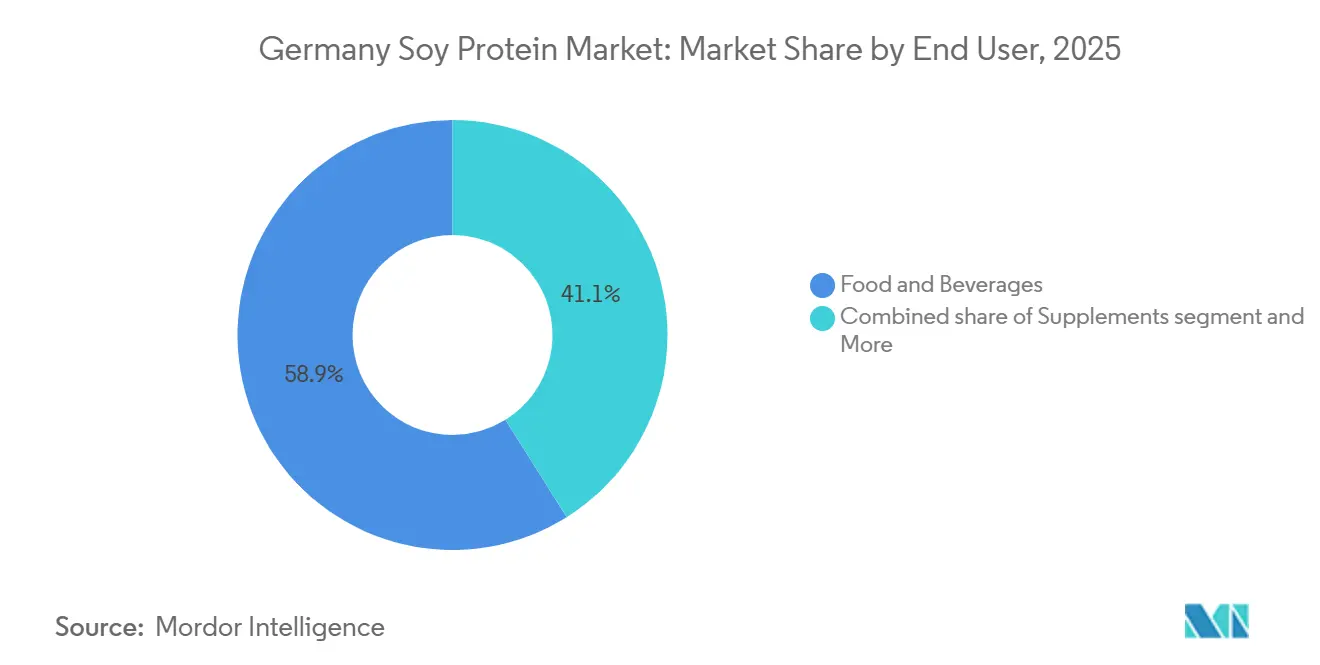

- By end user, food and beverages accounted for 58.91% of the Germany soy protein market size in 2025, while the supplements category is poised to expand at a 4.60% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Soy Protein Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Flexitarian and vegan population surge | +1.2% | National, with urban concentration in Berlin, Hamburg, Munich | Short term (≤ 2 years) |

| Proven functionality and cost-effectiveness of soy protein | +0.9% | National, spillover to neighboring EU markets | Medium term (2-4 years) |

| EU and German sustainability policies favouring plant proteins | +0.8% | National, aligned with the broader EU Green Deal framework | Long term (≥ 4 years) |

| Expansion of domestic soybean/legume cultivation (National Protein Strategy) | +0.5% | National, early gains in Bavaria, North Rhine-Westphalia | Medium term (2-4 years) |

| Rapid adoption of high-moisture extrusion and other texturizing tech | +0.7% | National, technology transfer from the Netherlands, Denmark | Short term (≤ 2 years) |

| University - industry research collaborations are accelerating innovation | +0.4% | National, concentrated in technical university hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Flexitarian and vegan population surge

The flexitarian demographic in Germany, those who are reducing meat consumption without fully eliminating it, has become the primary driver of the country's soy protein market, surpassing strict vegans in both volume and purchasing frequency. This shift is significant: flexitarians are less sensitive to price than their budget-conscious omnivore counterparts, yet they prioritize cleaner labels more than the early-adopter vegans. This creates a lucrative opportunity for soy concentrates in hybrid products, like blended burgers and dairy-alternative yogurts. According to the Federal Statistical Office, plant-based food sales in Germany saw double-digit growth in 2024[2]Source: Federal Statistical Office, “Food Retail Turnover 2024,” destasis.de. While soy-based products continued to dominate, they faced stiff competition from pea and oat proteins. In response, formulators are blending soy isolates with pea protein. This strategy not only masks any residual beany notes but also maintains a cost advantage, aligning with the flexitarian's preference for neutral taste profiles.

Proven functionality and cost-effectiveness of soy protein

The growing demand for soy protein as a cost-effective and versatile ingredient is driving the Germany soy protein market. Manufacturers in Germany are increasingly relying on soy protein to simplify formulations without compromising texture or shelf life. With its ability to emulsify, gel, and bind water at concentrations of 65-90%, soy protein has become a preferred choice. By 2025, soy isolates are projected to achieve cost parity with dairy proteins. Currently, soy isolates in Germany are trading at about 60-70% of the price of whey protein isolate on a per-kilogram basis. This competitive pricing has accelerated the adoption of soy protein in bakery and confectionery applications, particularly where taste neutrality is less critical. ADM's product portfolio highlights this versatility, offering textured soy concentrates that replicate ground meat for dishes like tacos and bolognese sauces, along with isolates designed for high-protein beverages that remain stable under UHT processing. The economic benefits of soy protein are further amplified when considering yield. Its water-holding capacity can increase the weight of finished products by 15-20%, effectively reducing the cost-per-serving in ready-to-eat meal kits, a growing segment in Germany.

EU and German sustainability policies favouring plant proteins

The European Commission's Farm to Fork Strategy, which aims for 25% of farmland to be organic by 2030, is a key driver of the Germany soy protein market. This initiative has elevated plant proteins from a niche focus to a strategic priority. In alignment with this, Germany's Federal Ministry of Food and Agriculture has allocated research grants specifically for legume breeding and agronomic trials. This policy framework is crucial as it reduces risks for long-term investments in domestic crushing capacity, signaling to processors that the supportive regulatory environment is likely to persist beyond election cycles. Additionally, reforms to the EU's Common Agricultural Policy in 2023 have shifted the focus by offering coupled support for cultivating protein crops, moving away from decades of cereal-centric subsidies. This change enables farmers to incorporate soybeans into their maize-heavy rotations without compromising income. Moreover, Germany's 2030 Organic Strategy, released in 2024, identifies soy and faba beans as priority crops. It links organic certification to preferential procurement in public cafeterias and schools, establishing a demand channel that ingredient suppliers can confidently contract for, supported by multi-year visibility.

Expansion of domestic soybean/legume cultivation (national protein strategy)

Germany's National Protein Strategy, first launched in 2012 and expanded in 2024, has emerged as a key driver of the Germany Soy Protein Market. The strategy has successfully boosted field-pea acreage by 7.6% and faba-bean plantings by 21.2% year-over-year in 2025. However, soybean cultivation faces challenges due to climate unsuitability and shorter growing seasons compared to the Danube basin. This has led to a split in sourcing strategies: processors targeting premium organic markets are directly contracting with farmers in Bavaria and Brandenburg for non-GMO soybeans, even paying a 10-15% cost premium for EUDR-compliant traceability. In contrast, mainstream players still rely on imports from Brazil and Argentina, but are mitigating deforestation risks through third-party certifications. Additionally, co-funding from the Federal Ministry for on-farm storage and drying infrastructure has curbed post-harvest losses, bolstering the economics of domestic cultivation. Yet, in 2025, domestic soybean output met less than 5% of Germany's national crushing demand, highlighting the sector's heavy dependence on imports.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Allergen and GMO perception concerns | -0.6% | National, heightened in urban centers with high organic-food penetration | Short term (≤ 2 years) |

| Import-price volatility for soybeans | -0.5% | National, linked to global commodity markets | Medium term (2-4 years) |

| EU Deforestation Regulation compliance costs | -0.4% | National, affecting importers of South American soybeans | Short term (≤ 2 years) |

| Taste fatigue/beany notes shifting demand to other proteins | -0.3% | National, accelerating in premium plant-based segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Allergen and GMO perception concerns

The Germany soy protein market faces significant restraints due to soy's classification as one of the EU's 14 major allergens, which necessitates mandatory labeling. This regulatory requirement limits soy's incorporation in products aimed at allergy-sensitive groups, including infant formulas and school meal programs. Germany's Federal Institute for Risk Assessment has noted a consistent rise in reported soy allergies among children under five[3]Source: Federal Institute for Risk Assessment, “Allergen Monitoring Report 2025,” bfr.bund.de. In response, pediatricians are advocating for alternatives like pea or rice, directly shrinking soy protein's market share in the lucrative baby-food sector. In 2025, consumer surveys indicated that 38% of German consumers link soy with genetic modification. This perception persists even with the widespread availability of non-GMO certified ingredients. To bridge this perception gap, brands are prominently labeling products as "GMO-free" on the front, albeit at the expense of higher raw material costs. Furthermore, the allergenic nature of soy restricts its tolerance for cross-contamination on shared production lines. As a result, co-packers are compelled to run soy batches separately, leading to cleaning downtimes and an increased per-unit cost of 8-12%.

Import-price volatility for soybeans

The Germany soy protein market faces significant restraints due to its reliance on soybean imports, which total approximately 3.5 million metric tons annually. Brazil and Argentina are the primary suppliers, exposing the market to challenges such as currency fluctuations, South American weather patterns, and changes in export-tax policies. These factors can cause landed costs to vary by 15-20% within a single quarter. This volatility is critical, as ingredient contracts are typically negotiated for 6-12 month periods, leaving processors unable to pass on sudden spot-price increases to food manufacturers, who operate on thinner margins. In 2024, a drought in Argentina's Pampas region reduced soybean yields by 30%, triggering a global price rally that extended into early 2025. This situation forced several mid-sized German crushers to either reduce production or source higher-cost European-grown soybeans to meet contractual obligations. Although hedging through futures markets could mitigate such risks, smaller players often avoid it due to basis risk and margin requirements. This reluctance creates a structural disadvantage for them compared to multinational traders with in-house risk-management capabilities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Texturization Drives Premiumization

High-moisture extrusion and enzymatic hydrolysis are reshaping the form-based segmentation. Textured and hydrolyzed variants are forecast to grow at a 4.80% CAGR through 2031, outpacing concentrates and isolates. This shift occurs as food manufacturers prioritize meat-analog authenticity over cost minimization. In 2025, concentrates held 41.05% of the market. Their dominance stems from a 65-70% protein content, meeting functional needs in bakery, snacks, and dairy alternatives without the premium price of isolates. Bakery applications utilize concentrates' water-binding ability to prolong dough shelf life. Condiment producers employ them as emulsifiers in mayonnaise and salad dressings, realizing 15-20% cost savings compared to egg-based stabilizers. Isolates, boasting over 90% protein purity, grapple with challenges from allergen-sensitive segments. Additionally, the emergence of pea-protein isolates, which deliver similar functionality with reduced allergen concerns, further complicates their position.

Textured soy protein's 4.80% CAGR underscores the category's shift towards high-moisture extrusion. This technology crafts fibrous, whole-muscle structures that command 30-40% premiums over conventional textured vegetable protein. In a move democratizing premium meat-analog production, German equipment suppliers have set up pilot extrusion lines at contract manufacturers in the Netherlands and Denmark. This allows mid-sized brands to harness the technology without hefty capital investments. Hydrolyzed variants are carving a niche in sports nutrition and products for the elderly, where the premium on rapid amino-acid absorption is justified. The Federal Ministry's 2024 expansion of the National Protein Strategy, which includes co-funding for extrusion research and development, underscores policy backing for bolstering domestic texturization. This initiative aims to curtail dependence on imported textured soy from Asia.

By End User: Supplements Outpace Food Applications

The supplements market is projected to grow at a 4.60% CAGR by 2031, surpassing the food-and-beverages segment's 58.91% share in 2025. Growth is driven by infant formula reformulations, aging-population nutrition, and sports-performance products prioritizing protein bioavailability. Infant formula manufacturers are blending soy isolates with hydrolyzed whey for hypoallergenic formulations, a category that grew 12% in Germany in 2025 due to pediatric recommendations for plant-based colic management. Elderly nutrition products, such as ready-to-drink shakes and fortified soups, use soy protein's neutral taste and solubility to deliver 20-25 grams of protein per serving without the chalky texture of dairy proteins. Sports nutrition brands combine soy isolates with pea protein to target the 35% of German gym-goers identifying as flexitarian and preferring plant-based recovery products.

In 2025, the food and beverages sector held a 58.91% market share, driven by nine sub-segments like meat alternatives and breakfast cereals. Meat and poultry alternatives are growing rapidly as retailers expand shelf space for plant-based SKUs, with soy-based patties and sausages maintaining cost advantages over pea-protein competitors. Dairy alternatives, such as soy milk and yogurt, face competition from oat and almond products, prompting soy suppliers to emphasize higher protein content (8-10 grams per serving vs. 1-2 grams in oat milk) to attract health-conscious consumers. Ready-to-cook meal kits are emerging as a growth area, with soy protein enabling 15-20% protein content in pasta sauces and stir-fry bases without refrigeration, simplifying distribution. The animal feed segment remains mature and low-margin, with soy meal competing on price against rapeseed and sunflower meals.

Geography Analysis

Germany, bolstered by the Federal Ministry's National Protein Strategy and a concentration of technical universities specializing in extrusion and fermentation research, plays a pivotal role in Europe's plant-protein landscape. Despite domestic soybean cultivation meeting less than 5% of its 2025 crushing demand, Germany's reliance on imports from Brazil and Argentina exposes processors to EUDR compliance costs and currency fluctuations. In Bavaria and Brandenburg, farmers are integrating soybeans into their maize-heavy rotations, spurred by subsidies from the 2023 Common Agricultural Policy reforms. However, shorter growing seasons and yields lagging behind the Danube basin limit their expansion. As a net exporter of processed soy ingredients to EU neighbors like France, the Netherlands, and Poland, Germany's domestic policy shifts reverberate across Europe, with the EUDR's December 2024 enforcement setting a compliance benchmark for intra-EU trade.

Berlin, Hamburg, and Munich are at the forefront of the plant-based product surge, boasting flexitarian rates over 40%, outpacing the national average of 25-30%. This concentration offers ingredient suppliers a unique chance to collaborate with local food startups on novel formulations before introducing them to national retail chains. The Ruhr region's established food-processing facilities, such as crushing mills and fractionation plants, grant cost benefits for large-scale concentrate production. Meanwhile, southern Germany's dense organic farming scene nurtures niche markets for non-GMO isolates, fetching 20-30% price premiums. Additionally, Germany's closeness to the Netherlands, which has rapidly expanded its high-moisture extrusion capacity, facilitates toll-manufacturing deals. This arrangement helps German brands introduce premium meat analogs without the hefty investment in dedicated production lines.

With a nod to EU sustainability goals, Germany is ramping up domestic legume cultivation. The Federal Ministry's 2024 budget earmarks EUR 50 million for protein-crop research and bolstering on-farm infrastructure. The 2030 Organic Strategy mandates public cafeterias and schools to source 30% of their ingredients from organic suppliers by 2030. This creates a steady demand for domestically grown, certified-organic soybeans, offering processors a buffer against import volatility, albeit at tighter margins. Yet, the strategy's triumph relies on breeding programs crafting soybean varieties suited to Germany's cooler, shorter growing seasons. This is a lengthy endeavor, and any significant reduction in import dependency isn't expected before 2028-2029. Meanwhile, processors are adopting a dual-sourcing strategy: securing domestic organic soybeans for premium products while continuing to import mainstream concentrates from Brazil. This approach maintains flexibility but introduces added complexity to the supply chain.

Competitive Landscape

In Germany's soy protein market, multinational ingredient giants dominate crushing and fractionation assets, leveraging scale advantages. Meanwhile, mid-tier specialists focus on carving out niches, emphasizing organic, non-GMO, and high-moisture extruded products. Here, brand premiums justify their smaller production runs. The industry's titans, employing vertical integration, run oilseed-crushing facilities in Hamburg and the Ruhr region. This strategic positioning allows them to profit at every stage, from importing commodity soybeans to producing finished isolates and texturates. Technology plays a pivotal role, especially in high-moisture extrusion and enzyme-assisted hydrolysis. Equipment suppliers like Bühler and Clextral collaborate with ingredient houses, co-developing formulations that tackle specific challenges, notably off-flavor masking and enhanced water retention. Meanwhile, fermentation-derived soy proteins present a burgeoning opportunity. Microbial platforms can craft peptide fractions with better solubility or fewer allergens. This frontier is drawing interest from several venture-backed German biotech startups.

Smaller players are turning the EUDR's traceability mandates into a competitive edge. By directly contracting with European farmers, they're securing certified deforestation-free soybeans. These beans, prized in the organic and premium plant-based markets, come at a premium. This direct approach circumvents the multinational-controlled commodity-trading system. As a result, regional processors can promise brands shorter lead times and enhanced supply-chain transparency, a boon for those emphasizing sustainability.

Patent activity underscores the sector's innovative spirit. A 2025 review of European Patent Office filings highlighted a 22% surge in applications centered on plant-protein texturization. Notably, German applicants made up 18% of the total, trailing only the Netherlands. As the EUDR tightens its grip with due diligence mandates, firms boasting geolocation systems and adept legal teams for supplier audits find themselves at an advantage. This regulatory compliance prowess is inadvertently consolidating market share, favoring those with the financial muscle to invest in compliance technologies.

Germany Soy Protein Industry Leaders

Archer Daniels Midland Company

CHS Inc.

International Flavors & Fragrances Inc.

Kerry Group PLC

Wilmar International Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Roquette launched a new line of high-moisture extruded soy protein texturates at its pilot facility in Lestrem, France, targeting the German meat-alternative market with products that replicate whole-muscle chicken and beef structures. The launch followed 18 months of co-development with German food startups and leverages enzyme-treated soy isolates to reduce beany off-notes.

- March 2025: Cargill entered a multi-year supply partnership with a consortium of Bavarian organic farmers to source non-GMO soybeans for its plant-protein division, guaranteeing minimum purchase volumes of 8,000 metric tons per year and providing agronomic support to improve yields. The arrangement enables Cargill to offer fully traceable, European-grown soy isolates to premium plant-based brands navigating EUDR compliance.

- January 2025: ADM announced the expansion of its soy protein isolate production capacity at its Straubing facility in Bavaria, investing EUR 18 million to install a new fractionation line capable of producing 12,000 metric tons annually of non-GMO isolates for the European market. The investment responds to growing demand from dairy-alternative and sports-nutrition brands seeking EUDR-compliant ingredients with shorter lead times than imports from Asia.

Germany Soy Protein Market Report Scope

Soy protein is a high-quality, plant-derived protein that comes from soybeans (soya beans). Germany soy protein market is segmented by form and end user. By form, the market is segmented into Concentrates, Isolates, and Textured/Hydrolyzed. By end user, the market is segmented into animal feed, food and beverages, and supplements. The food and beverages segment is further sub-segmented into bakery, beverages, breakfast cereals, condiments/sauces, confectionery, dairy and dairy alternative products, meat/poultry/seafood and meat alternative products, RTE/RTC food products, and snacks. Similarly, the supplements segment is further sub-segmented into Baby Food and infant formula, elderly nutrition and medical nutrition, and sport/performance nutrition. The Market forecasts are provided in terms of value (USD) and volume (Tons).

Form

| Concentrates |

| Isolates |

| Textured/Hydrolyzed |

End User

| Animal Feed | |

| Food and Beverages | Bakery |

| Beverages | |

| Breakfast Cereals | |

| Condiments/Sauces | |

| Dairy and Dairy Alternative Products | |

| Meat/Poultry/Seafood and Meat Alternative Products | |

| RTE/RTC Food Products | |

| Snacks | |

| Supplements | Baby Food and Infant Formula |

| Elderly Nutrition and Medical Nutrition | |

| Sport/Performance Nutrition |

| Form | Concentrates | |

| Isolates | ||

| Textured/Hydrolyzed | ||

| End User | Animal Feed | |

| Food and Beverages | Bakery | |

| Beverages | ||

| Breakfast Cereals | ||

| Condiments/Sauces | ||

| Dairy and Dairy Alternative Products | ||

| Meat/Poultry/Seafood and Meat Alternative Products | ||

| RTE/RTC Food Products | ||

| Snacks | ||

| Supplements | Baby Food and Infant Formula | |

| Elderly Nutrition and Medical Nutrition | ||

| Sport/Performance Nutrition | ||

Market Definition

- End User - The Protein Ingredients Market operates on a B2B basis. Food, Beverages, Supplements, Animal Feed, and Personal Care & Cosmetic manufacturers are considered to be end-consumers in the market studied. The scope excludes manufacturers buying liquid/dry whey to be used for application as a binding agent or thickener or other non-protein applications.

- Penetration Rate - Penetration Rate is defined as the percentage of Protein-Fortified End User Market Volume in the Overall End User Market Volume.

- Average Protein Content - Average protein content is the average protein content present per 100 g of product manufactured by all end-user companies considered under the scope of this report.

- End User Market Volume - End-user market volume is the consolidated volume of all types and forms of end-user products in the country or region.

| Keyword | Definition |

|---|---|

| Alpha-lactalbumin (α-Lactalbumin) | It is a protein that regulates the production of lactose in the milk of almost all mammalian species. |

| Amino acid | It is an organic compound that contains both amino and carboxylic acid functional groups, which are required for the synthesis of body protein and other important nitrogen-containing compounds, such as creatine, peptide hormones, and some neurotransmitters. |

| Blanching | It is the process of briefly heating vegetables with steam or boiling water. |

| BRC | British Retail Consortium |

| Bread improver | It is a flour-based blend of several components with specific functional properties designed to modify dough characteristics and give quality attributes to bread. |

| BSF | Black Soldier Fly |

| Caseinate | It is a substance produced by adding an alkali to acid casein, a derivative of casein. |

| Celiac disease | Celiac disease is an immune reaction to eating gluten, a protein found in wheat, barley, and rye. |

| Colostrum | It is a milky fluid that’s released by mammals that have recently given birth before breast milk production begins. |

| Concentrate | It is the least processed form of protein and has a protein content ranging from 40-90% by weight. |

| Dry protein basis | It refers to the percentage of "pure protein" present in a supplement after the water in it is completely removed through heat. |

| Dry whey | It is the product resulting from drying fresh whey which has been pasteurized and to which nothing has been added as a preservative. |

| Egg protein | It is a mixture of individual proteins, including ovalbumin, ovomucoid, ovoglobulin, conalbumin, vitellin, and vitellenin. |

| Emulsifier | It is a food additive that facilitates the blending of foods that are immiscible with one another, such as oil and water. |

| Enrichment | It is the process of addition of micronutrients that are lost during the processing of the product. |

| ERS | Economic Research Service of the USDA |

| Extrusion | It is the process of forcing soft mixed ingredients through an opening in a perforated plate or die designed to produce the required shape. The extruded food is then cut to a specific size by blades. |

| Fava | Also known as Faba, it is another word for yellow split beans. |

| FDA | Food and Drug Administration |

| Flaking | It is a process in which typically a cereal grain (like corn, wheat, or rice) is broken down into grits, cooked with flavors and syrups, and then pressed into flakes between cooled rollers. |

| Foaming agent | It is a food ingredient that makes it possible to form or maintain a uniform dispersion of a gaseous phase in a liquid or solid food. |

| Foodservice | It refers to the part of the food industry which includes businesses, institutions, and companies which prepare meals outside the home. It includes restaurants, school and hospital cafeterias, catering operations, and many other formats. |

| Fortification | It is the deliberate addition of micronutrients that are not found in them naturally or which are lost during processing, to improve a food product's nutritional value. |

| FSANZ | Food Standards Australia New Zealand |

| FSIS | Food Safety and Inspection Service |

| FSSAI | Food Safety and Standards Authority of India |

| Gelling agent | It is an ingredient that functions as a stabilizer and thickener to provide thickening without stiffness through the formation of gel. |

| GHG | Greenhouse Gas |

| Gluten | It is a family of proteins found in grains, including wheat, rye, spelt, and barley. |

| Hemp | It is a botanical class of Cannabis sativa cultivars grown specifically for industrial or medicinal use. |

| Hydrolysate | It is a form of protein manufactured by exposing the protein to enzymes that can partially break the bonds between the protein's amino acids and break down large, complicated proteins into smaller pieces. Its processing makes it easier and quicker to digest. |

| Hypoallergenic | It refers to a substance that causes fewer allergic reactions. |

| Isolate | It is the purest and most processed form of protein which has undergone separation to obtain a pure protein fraction. It typically contains ≥ 90% of protein by weight. |

| Keratin | It is a protein that helps form hair, nails, and the outer layer of skin. |

| Lactalbumin | It is the albumin contained in milk and obtained from whey. |

| Lactoferrin | It is an iron‑binding glycoprotein that is present in the milk of most mammals. |

| Lupin | It is the yellow legume seeds of the genus Lupinus. |

| Millenial | Also known as Generation Y or Gen Y, it refers to the people born from 1981 to 1996. |

| Monogastric | It refers to an animal with a single-compartmented stomach. Examples of monogastric include humans, poultry, pigs, horses, rabbits, dogs, and cats. Most monogastric are generally unable to digest much cellulose food materials such as grasses. |

| MPC | Milk protein concentrate |

| MPI | Milk protein isolate |

| MSPI | Methylated soy protein isolate |

| Mycoprotein | Mycoprotein is a form of single-cell protein, also known as fungal protein, derived from fungi for human consumption. |

| Nutricosmetics | It is a category of products and ingredients that act as nutritional supplements to care for skin, nails, and hair natural beauty. |

| Osteoporosis | It is a medical condition in which the bones become brittle and fragile from loss of tissue, typically as a result of hormonal changes, or deficiency of calcium or vitamin D. |

| PDCAAS | Protein digestibility-corrected amino acid score (PDCAAS) is a method of evaluating the quality of a protein based on both the amino acid requirements of humans and their ability to digest it. |

| Per-capita consumption of animal protein | It is the average amount of animal protein (such as milk, whey, gelatin, collagen, and egg proteins) that is readily available for consumption by each person in an actual population. |

| Per-capita consumption of plant protein | It is the average amount of plant protein (such as soy, wheat, pea, oat, and hemp proteins) that is readily available for consumption by each person in an actual population. |

| Quorn | It is a microbial protein manufactured using mycoprotein as an ingredient, in which the fungus culture is dried and mixed with egg albumen or potato protein, which acts as a binder, and then is adjusted in texture and pressed into various forms. |

| Ready-to-Cook (RTC) | It refers to food products that include all of the ingredients, where some preparation or cooking is required through a process that is given on the package. |

| Ready-to-Eat (RTE) | It refers to a food product prepared or cooked in advance, with no further cooking or preparation required before being eaten. |

| RTD | Ready-to-Drink |

| RTS | Ready-to-Serve |

| Saturated fat | It is a type of fat in which the fatty acid chains have all single bonds. It is generally considered unhealthy. |

| Sausage | It is a meat product made of finely chopped and seasoned meat, which may be fresh, smoked, or pickled and which is then usually stuffed into a casing. |

| Seitan | It is a plant-based meat substitute made out of wheat gluten. |

| Softgel | It is a gelatin-based capsule with a liquid fill. |

| SPC | Soy protein concentrate |

| SPI | Soy protein isolate |

| Spirulina | It is a biomass of cyanobacteria that can be consumed by humans and animals. |

| Stabilizer | It is an ingredient added to food products to help maintain or enhance their original texture, and physical and chemical characteristics. |

| Supplementation | It is the consumption or provision of concentrated sources of nutrients or other substances that are intended to supplement nutrients in the diet and is intended to correct nutritional deficiencies. |

| Texturant | It is a specific type of food ingredient that is used to control and alter the mouthfeel and texture of food and beverage products. |

| Thickener | It is an ingredient that is used to increase the viscosity of a liquid or dough and make it thicker, without substantially changing its other properties. |

| Trans fat | Also called trans-unsaturated fatty acids or trans fatty acids, it is a type of unsaturated fat that naturally occurs in small amounts in meat. |

| TSP | Textured soy protein |

| TVP | Textured vegetable protein |

| WPC | Whey protein concentrate |

| WPI | Whey protein isolate |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms