Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

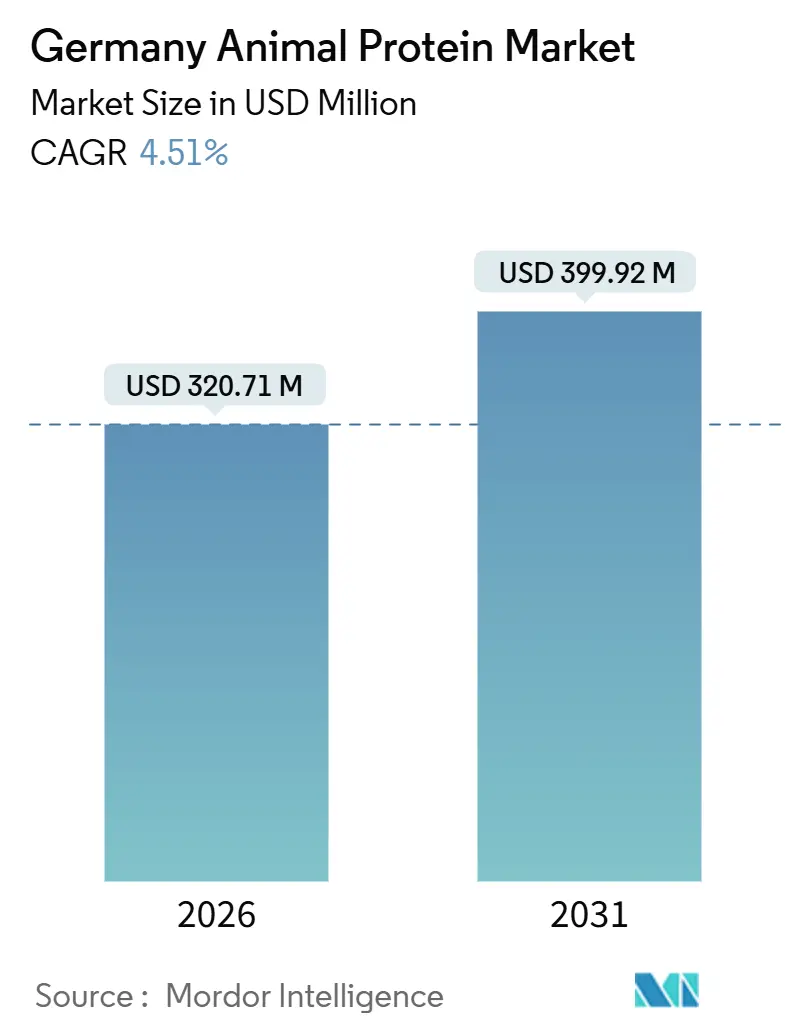

| Market Size (2026) | USD 320.71 Million |

| Market Size (2031) | USD 399.92 Million |

| Growth Rate (2026 - 2031) | 4.51% CAGR |

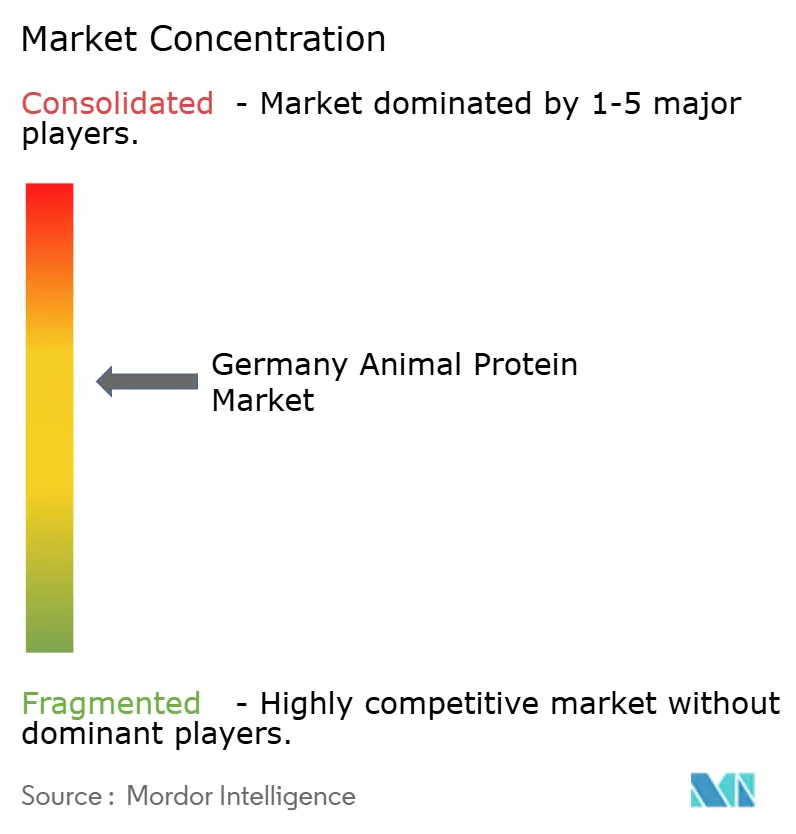

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Animal Protein Market Analysis by Mordor Intelligence

The Germany animal protein market is projected to grow significantly, with its size valued at USD 320.71 million in 2026 and expected to reach USD 399.92 million by 2031, reflecting a 4.51% CAGR. The market's growth is driven by a shift from traditional commodity powders to value-added ingredients. These include collagen peptides for beauty supplements, whey isolates for sports nutrition, and insect proteins designed for premium pet food. In 2024, African Swine Fever and 15,372 bluetongue outbreaks caused persistent price volatility in pork and beef[1]Source: Friedrich-Loeffler-Institut, “Bluetongue Situation in Germany 2024,” fli.de. This has prompted formulators to adopt dairy-derived proteins and alternative feedstocks, stabilizing margins against raw material disruptions, as noted by the Friedrich-Loeffler-Institut. Clean-label and non-GMO standards, already well-established in sports nutrition and infant formulas, are further fueling demand for traceable ingredients. These ingredients are supplied by vertically integrated cooperatives capable of certifying feed, processing aids, and allergen controls. Technological advancements, such as precision filtration and enzymatic hydrolysis, are enabling the production of whey isolates with 95% protein purity and collagen peptides with clinically proven bioactivity. These innovations support premium pricing, even as competition from precision fermentation intensifies.

Key Report Takeaways

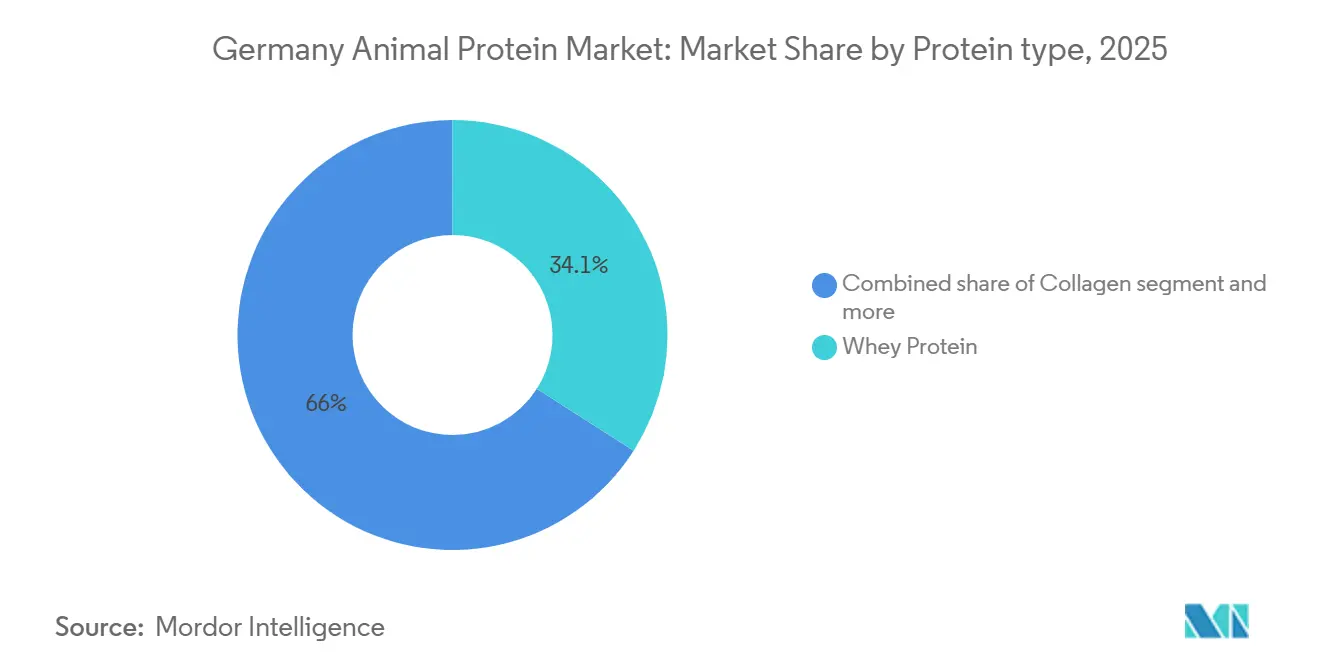

- By protein type, whey led with 34.05% of the Germany animal protein market share in 2025, while collagen peptides are forecast to expand at a 5.30% CAGR through 2031.

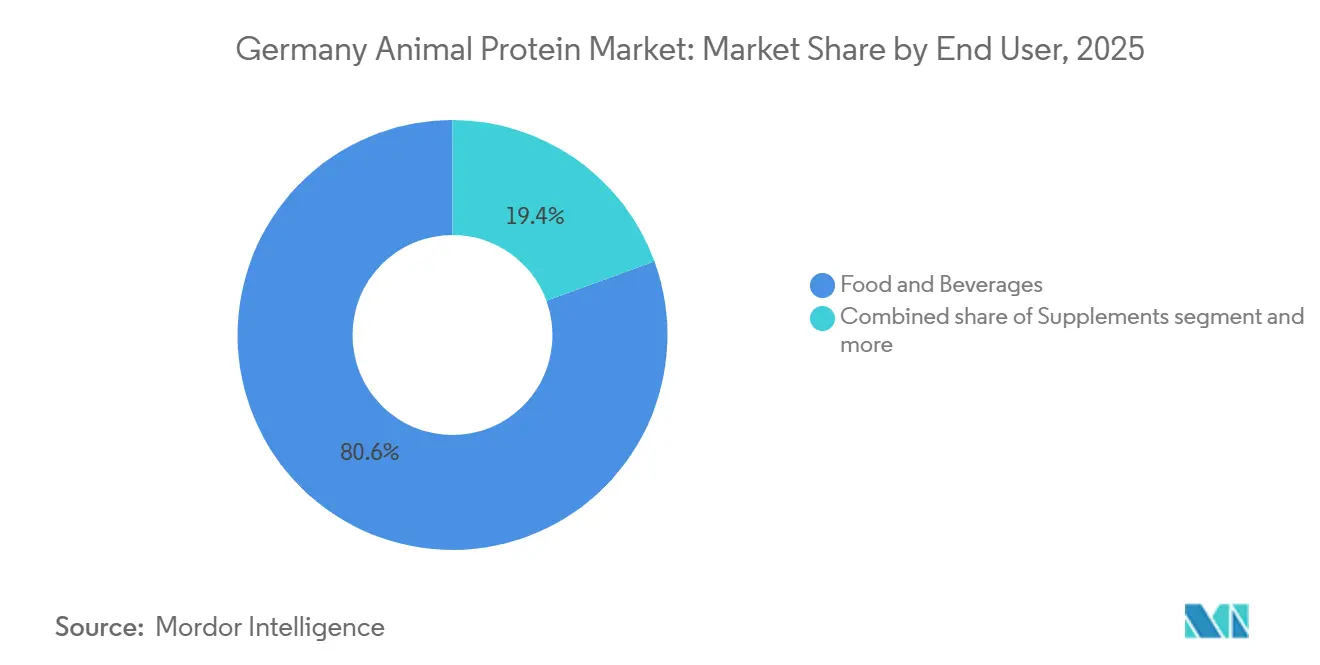

- By end user, food and beverages accounted for 72.51% of the Germany animal protein market size in 2025 and supplements are advancing at a 5.81% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Animal Protein Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Structural pork-to-beef price gap widens post-African Swine Fever | +0.7% | Germany, with spillover to the EU gelatin/collagen supply chains | Medium term (2-4 years) |

| Regulatory approval of insect proteins | +0.6% | Germany and EU-wide, concentrated in aquaculture and pet feed | Long term (≥ 4 years) |

| Clean label and non-GMO standards | +0.9% | Germany, Netherlands, Scandinavia, premium ingredient markets | Short term (≤ 2 years) |

| Premiumization of pet nutrition | +0.8% | Germany, urban centers with high pet ownership | Medium term (2-4 years) |

| Technological breakthroughs in solubility | +0.7% | Germany, early adoption by sports nutrition brands | Short term (≤ 2 years) |

| Surge in "beauty-from-within" demand | +0.9% | Germany, France, UK, mature ingestible beauty markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Structural pork-to-beef price gap widens post-African swine fever

The ongoing circulation of African Swine Fever in Eastern Europe, along with sporadic detections near the German border, has emerged as a significant driver of the German animal protein market. These disruptions in pork slaughter volumes have created a structural price premium for pork over beef, prompting processors to shift their focus toward poultry and cattle. This shift has tightened the availability of porcine hides and bones, key feedstocks for pharmaceutical-grade gelatin and Type I collagen, forcing ingredient buyers to diversify into bovine, fish-skin, and poultry-bone sources. Additionally, Germany's bluetongue virus outbreaks, which recorded 15,372 confirmed cases nationwide in 2024, have further constrained cattle throughput and driven spot prices for bovine-derived gelatin up by 8 to 12% in late 2024, according to disclosures from GELITA's raw-material procurement and the Friedrich-Loeffler-Institut. These factors have accelerated research and development efforts, particularly in recombinant collagen and fish-skin peptides. GELITA, for example, is investing in enzymatic hydrolysis processes to extract collagen from previously discarded poultry cartilage, targeting a 15 to 20% yield improvement by 2027. Regulatory oversight by the Friedrich-Loeffler-Institut remains critical, ensuring effective disease surveillance and timely vaccine approvals. In 2024, three bluetongue vaccines were authorized, aiming to mitigate cattle losses and stabilize the gelatin feedstock supply, further influencing the German animal protein market.

Regulatory approval of insect proteins

The European Food Safety Authority's novel-food approvals for Hermetia illucens (black soldier fly) larvae in 2024 and 2025 are driving innovation in Germany's animal protein market. These approvals enable applications in aquaculture feed and pet nutrition, where insect protein's amino-acid profile and digestibility rival fishmeal at 30 to 40% lower carbon intensity. German companies are at the forefront of this shift. Infinite Roots secured a EUR 2.6 million EU grant to up-cycle mycoprotein from brewer's yeast, while Mushlabs partnered with Bitburger brewery to convert spent yeast into protein ingredients. These companies are positioning insect and fungal proteins as premium alternatives to soy and whey in pet food formulations. Enifer's EUR 36 million Series A funding in 2024 and YeastUp's pilot-scale fermentation facility in Bavaria further highlight the growing momentum in Germany's novel protein sector. However, regulatory timelines remain a bottleneck; each novel-food dossier requires 18 to 36 months of toxicology, allergenicity, and stability data before EFSA authorization. The approval process favors larger ingredient suppliers with regulatory affairs teams and co-development partnerships with feed compounders, creating a first-mover advantage for companies that filed dossiers in 2023 and secured approvals in 2025. Smaller startups, however, face capital constraints that could delay their market entry until 2027 or beyond, underscoring the challenges within Germany's animal protein market.

Clean label and non-GMO standards

The growing emphasis on clean-label and non-GMO requirements is driving the Germany animal protein market. Sports nutrition brands and infant formula manufacturers are increasingly embedding these requirements into their ingredient specifications. They are now demanding certificates of analysis to confirm the absence of genetically modified organisms, antibiotic residues, and undeclared processing aids. This shift is benefiting vertically integrated dairy cooperatives. For instance, DMK Deutsches Milchkontor, with control over an annual intake of 5.1 billion kilograms of milk, can ensure non-GMO feed sourcing from its contracted farms. Similarly, Müller Group provides whey powder to infant formula manufacturers throughout Europe, boasting full traceability from cow to can. In Dresden, Sachsenmilch Leppersdorf operates a cutting-edge spray-drying facility. This facility produces whey protein concentrates and isolates, certified under Regulation (EU) 2016/355. This regulation standardizes raw-material sourcing, production processes, and residue limits for dairy proteins. While clean-label positioning can command a 15 to 25% price premium over conventional ingredients, it also necessitates ongoing investments in analytical testing. Techniques like liquid chromatography-mass spectrometry for pesticide residues and polymerase chain reaction for GMO detection are essential. However, these costs are burdensome for smaller ingredient suppliers, leading to a swift consolidation trend favoring larger cooperatives that can leverage scale economies in quality assurance.

Premiumization of pet nutrition

The growing preference for premium pet food formulations is emerging as a significant driver of the German animal protein market. Pet owners in Germany are increasingly opting for human-grade ingredients, fueling demand for hydrolyzed proteins, collagen peptides, and novel sources like insect meal. MEGGLE Group's Feed Ingredients division plays a pivotal role in this market, supplying high-quality milk protein concentrates and whey permeate to pet food manufacturers. By leveraging advanced spray-drying and agglomeration techniques, the company delivers instant-dispersible powders that enhance kibble palatability and digestibility. Additionally, pet food brands are embedding joint-health claims substantiated by GELITA's FORTIGEL collagen peptides. These peptides, clinically validated for cartilage regeneration in canine osteoarthritis trials, enable brands to position their products at a 40 to 60% price premium over conventional formulations. The premiumization trend is particularly pronounced in urban centers like Berlin, Munich, and Hamburg, where pet ownership exceeds 40% of households and higher disposable incomes support spending on functional ingredients. Regulatory compliance with European Pet Food Industry Federation guidelines on ingredient labeling and nutritional adequacy further shapes the market. Manufacturers must balance protein bioavailability, cost constraints, and shelf-life stability to meet these stringent requirements.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Longer regulatory approval for novel proteins | -0.5% | Germany and EU-wide, affecting the insect and mycoprotein market entry | Long term (≥ 4 years) |

| Competition from precision fermentation | -0.8% | Germany, the Netherlands, and Denmark, venture-capital-rich ecosystems | Medium term (2-4 years) |

| Ethical concerns over gelatin | -0.4% | Germany, UK, Scandinavia, high vegan/vegetarian penetration | Short term (≤ 2 years) |

| Allergen labeling burdens | -0.6% | Germany and EU-wide, affecting co-manufacturing flexibility | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Longer regulatory approval for novel proteins

Under the EU Novel Food Regulation, the European Food Safety Authority mandates a 18 to 36 month process for safety dossiers, toxicology assessments, allergenicity checks, stability tests, and production-process validations. This is a prerequisite for market entry of insect, mycoprotein, and algae-derived proteins. As a result, companies that submitted their dossiers in 2023, like suppliers of Hermetia illucens larvae, gained approvals in 2025, enjoying a first-mover advantage. In contrast, those in the second wave face delays, pushing their market entry to 2027 or later. While Infinite Roots secured a EUR 2.6 million EU grant for mycoprotein up-cycling and Enifer raised a notable EUR 36 million in Series A funding in 2024, highlighting venture capital's faith in novel proteins, these startups grapple with regulatory hurdles. Such bottlenecks stall revenue generation until approvals are granted, leading these companies to deplete cash reserves on pilot-scale productions and clinical trials, all without any commercial sales. Smaller ingredient suppliers, often without dedicated regulatory affairs teams, feel the brunt of this regulatory burden. In contrast, larger entities like GELITA and DMK can spread out and absorb these regulatory costs across their diverse protein portfolios. Consequently, this dynamic acts as a restraint on the German animal protein market, slowing down the pace of innovation and diminishing competitive intensity in the novel protein sector, favoring only those with substantial capital to maneuver through the approval maze.

Ethical concerns over gelatin

In Germany, consumer skepticism regarding the sourcing of animal-based gelatin, particularly from bovine and porcine origins, has emerged as a significant restraint in the animal protein market. Major food manufacturers like Unilever and Nestlé are increasingly turning to plant-based gelling agents such as pectin, agar, and carrageenan, which are gradually reducing gelatin's presence in products like gummies, marshmallows, and desserts. Meanwhile, GELITA is diversifying its approach by investing in fish-skin and poultry-bone collagen, moving away from traditional mammalian sources. This shift not only targets halal and kosher certifications, broadening their market reach, but also includes the development of MEDELLAPRO. This ultra-low-endotoxin gelatin is tailored for pharmaceutical capsules and bioprinting, areas where its functional performance and adherence to regulatory standards pose challenges for plant-based substitutes. The push against traditional gelatin sourcing is particularly strong in Germany, where over 10% of the population identifies as vegan or vegetarian, emphasizing transparency in ingredient sourcing. While Regulation (EU) 2016/355 sets standards for the sourcing, production, and residue limits of gelatin and collagen, ensuring quality and safety, it falls short of addressing the ethical concerns. This oversight leaves ingredient suppliers to navigate the complex landscape of consumer sentiment, often relying on voluntary certifications and thorough supply-chain audits.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Protein Type: Collagen Peptides Capture Beauty and Joint-Health Premiums

In 2025, whey protein held 34.05% of the ingredient market, supported by DMK Deutsches Milchkontor's 5.1 billion kilograms of annual milk throughput and Sachsenmilch Leppersdorf's advanced spray-drying facility producing whey concentrates and isolates for sports nutrition and infant formula. Collagen peptides are projected to grow at a 5.30% CAGR through 2031, driven by GELITA's VERISOL for skin elasticity and FORTIGEL for joint cartilage. Clinical trials show VERISOL reduces wrinkle depth by 20% after 8 weeks, enabling premium pricing. Casein and caseinates, supplied by Lactoprot Deutschland and DMK, cater to niche markets requiring sustained amino-acid release or emulsification. Milk protein concentrates and isolates, produced by Müller Group and MEGGLE, are used in functional foods, protein-fortified yogurt, bakery emulsions, and ready-to-eat meals.

Gelatin's gelling and film-forming properties make it vital for pharmaceutical capsules, gummies, and wound-care products. GELITA's MEDELLAPRO ultra-low-endotoxin gelatin targets bioprinting and parenteral applications, where regulatory compliance and consistency command premiums. Egg protein dominates bakery and confectionery emulsions due to ovalbumin's foaming and binding properties but faces growth constraints from allergen-labeling under EU Regulation 1169/2011[2]Source: EUR-Lex, “Regulation 1169/2011 on Food Information,” eur-lex.europa.eu. Research into hydrolyzed egg protein aims to reduce allergenicity. Insect protein, under 1% of current volume, is gaining traction with European Food Safety Authority approvals for Hermetia illucens larvae in 2024 and 2025. Companies like Infinite Roots and Mushlabs target aquaculture feed and premium pet nutrition, where insect protein rivals fishmeal with lower carbon intensity. Other animal proteins, such as mycoprotein from brewer's yeast and colostrum for immune-health supplements, occupy niches supported by functional claims and clinical validation.

By End User: Supplements Surge on Beauty-from-Within and Sarcopenia Prevention

In 2025, food and beverage manufacturers held 72.51% of ingredient demand, using egg protein in bakery emulsions, whey isolates in protein beverages, and milk protein concentrates in dairy alternatives. The supplements segment is projected to grow fastest at a 5.81% CAGR through 2031, driven by beauty-from-within formulations, sarcopenia prevention, and sports performance. GELITA's VERISOL collagen peptides, marketed in tablets and gummies, target skin hydration and elasticity, leveraging clinical validation for premium positioning. Sports nutrition is shifting to clean-label whey isolates and hydrolysates, highlighted by DMK's acquisition of the DV Nutrition joint venture. Infant formula and baby food demand whey protein concentrates and hydrolysates for digestibility, with Müller Group ensuring full traceability.

Elderly and medical nutrition focus on protein fortification to combat sarcopenia, with collagen peptides and milk protein isolates offering superior bioavailability. The personal care sector is growing, incorporating collagen peptides into ingestible supplements and topical products targeting skin hydration. GELITA's VERISOL peptides are used in serums and creams, supported by clinical evidence. Animal feed, though minor in value, is vital for by-product valorization. MEGGLE Group produces milk protein concentrates and whey permeate for premium pet food, tapping into demand for human-grade claims. Food and beverages' 72.51% share reflects diverse applications like gelatin in gummies and whey in yogurt, though growth is slowing as categories saturate and plant-based alternatives gain traction. Supplements' 5.81% CAGR is driven by aging populations, millennials adopting ingestible beauty routines, and innovations in delivery formats like tablets and gummies enhancing appeal.

Geography Analysis

Bavaria and Lower Saxony dominate Germany's animal protein ingredient market, jointly holding over 50% of the nation's dairy processing capacity. These regions supply essential raw materials, milk, whey, hides, and bones, crucial for producing whey protein, casein, gelatin, and collagen. MEGGLE operates its headquarters in Wasserburg am Inn and cheese operations in Altusried, Bavaria, where they produce whey permeate and milk protein concentrates for both feed and food applications. Meanwhile, Lower Saxony is home to DMK Deutsches Milchkontor, a cooperative network comprising 5,800 dairy farms that collectively supply an impressive 5.1 billion kilograms of milk annually. North Rhine-Westphalia and Thuringia also play a role, contributing to the processing capacity for dairy proteins. Notably, Müller Group's Leppersdorf site near Dresden stands out as one of Europe's most modern milk-processing plants, specializing in whey derivatives for both industrial clients and infant formula producers. In a strategic move, MEGGLE bolstered cheese production and whey by-product recovery in northern Germany's milk-rich coastal regions by acquiring Aurich and Wismar sites through the Rücker dairy takeover, a decision greenlit by the Bundeskartellamt in October 2025[3]Source: Bundeskartellamt, “Decision B2-88/25: MEGGLE / Rücker,” bundeskartellamt.de.

Eastern German states, notably Saxony and Thuringia, are witnessing a steady uptick in activity. Attracting greenfield investments in dairy and protein processing, these regions benefit from lower land costs and EU structural funds. However, challenges loom large: labor shortages and infrastructural gaps hinder their expansion. GELITA, with its headquarters in Eberbach, Baden-Württemberg, spearheads collagen and gelatin production. Their enzymatic hydrolysis facilities adeptly extract bioactive peptides from bovine, porcine, and fish-skin sources, catering to diverse applications ranging from pharmaceutical capsules and bioprinting to ingestible beauty products. Major urban centers like Berlin, Hamburg, Munich, and Frankfurt are fueling a surge in demand for sports nutrition and beauty supplements. Brands are keenly attuning their formulations to resonate with regional preferences, emphasizing clean-label and non-GMO attributes.

This geographic segmentation reveals a clear trend: while traditional dairy regions are consolidating processing capacities for economies of scale in whey and casein production, urban hubs are adeptly capturing value through premium supplements and functional ingredients. The cross-border dynamics are becoming increasingly pronounced. German ingredient suppliers are exporting high-value proteins, ranging from whey isolates and collagen peptides to pharmaceutical-grade gelatin, to markets in Asia, the Middle East, and North America. They are leveraging the strategic advantages of Hamburg and Bremen ports for container shipments, all while capitalizing on Germany's esteemed reputation for quality and stringent regulatory compliance.

Competitive Landscape

In Germany's animal protein ingredient market, dairy proteins dominate, with DMK Deutsches Milchkontor, Müller Group, and MEGGLE holding a significant share of whey and casein production. Meanwhile, GELITA, operating enzymatic hydrolysis facilities in Eberbach, leads in collagen and gelatin. Strategies focus on vertical integration, clean-label certification, and research and development in bioactive peptides. GELITA's backing of VERISOL and FORTIGEL clinical trials, which validate claims on skin elasticity and joint cartilage, not only fortifies its market position but also allows it to price products 40 to 60% above standard commodity gelatin. Opportunities abound in areas like novel proteins, insect meal for aquaculture and pet food, up-cycled mycoprotein from brewer's yeast, and fish-skin collagen targeting halal and kosher markets. Here, approvals from the European Food Safety Authority and clinical validations act as barriers, benefiting established players with regulatory expertise and partnerships with feed compounders and supplement brands.

Disruptors are emerging: Infinite Roots, awarded a EUR 2.6 million EU grant, collaborates with Bitburger brewery to transform spent yeast into protein ingredients. Enifer, having raised EUR 36 million in Series A funding in 2024, aims to scale mycoprotein fermentation in Finland, eyeing the German market in 2026. Technology is evolving: suppliers in sports nutrition are increasingly adopting cross-flow microfiltration for neutral-tasting whey protein isolates, enzymatic hydrolysis for rapidly absorbable di- and tri-peptides from casein, and agglomeration for better dispersibility. Compliance with EU regulations on gelatin, collagen, food hygiene, and allergen labeling mandates ongoing investments in quality assurance and analytical testing.

The market is splitting: larger players use vertical integration and clean-label certifications to maintain their positions in whey and casein, while niche innovators focus on bioactive peptides, novel proteins, and hypoallergenic formulations. As precision fermentation and ethical concerns rise, consolidation seems inevitable, especially for mid-tier suppliers struggling to differentiate.

Germany Animal Protein Industry Leaders

Arla Foods Ingredients Group P/S

GELITA AG

DMK Deutsches Milchkontor GmbH

MEGGLE Group GmbH

Fonterra Co-operative Group Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: The Bundeskartellamt cleared MEGGLE Holding SE to acquire 100% of Rücker GmbH and Ostsee-Molkerei Wismar GmbH, finding that the parties' market shares in cream, cheese, butter, and milk powder are small and do not raise competition concerns. The authority noted no overlap in raw-milk procurement, as the companies source from different German regions, and consultations with market participants across dairy categories yielded no competition issues.

- September 2025: MEGGLE Holding SE announced its acquisition of Rücker dairy, pending competition authority approval, to strengthen its cheese segment and create one of Germany's largest private dairies. Rücker, with over 135 years of history and known as a quality leader in Hirtenkäse, operates state-of-the-art facilities in Aurich and Wismar and recorded 2024 revenue of approximately EUR 500 million, with whey by-product streams targeted for protein ingredient recovery.

- August 2024: Arla Foods Ingredients has shifted its focus to high-value protein innovations, repurposing facilities to prioritize premium milk and whey proteins over early-life nutrition. In Germany, it has strengthened its partnership with Novozymes to explore precision fermentation, aiming to produce "animal-free" dairy proteins by 2026 to complement its traditional portfolio.

Germany Animal Protein Market Report Scope

Animal protein is defined both scientifically and industrially as high-quality protein derived from animal tissues and fluids. Germany animal protein market is segmented by protein type and end user. By protein type, the market is segmented into casein and caseinates, collagen, egg protein, gelatin, insect protein, milk protein, whey protein, and other animal protein. By end user, the market is segmented into animal feed, food and beverages, personal care and cosmetics, and supplements. The food and beverages segment is further sub-segmented into bakery, beverages, breakfast cereals, condiments/sauces, confectionery, dairy and dairy alternative products, RTE/RTC food products, and snacks. Similarly, the supplements segment is further sub-segmented into Baby Food and infant formula, elderly nutrition and medical nutrition, and sport/performance nutrition. The Market forecasts are provided in terms of value (USD) and volume (Tons).

Protein Type

| Casein and Caseinates |

| Collagen |

| Egg Protein |

| Gelatin |

| Insect Protein |

| Milk Protein |

| Whey Protein |

| Other Animal Protein |

End User

| Animal Feed | |

| Food and Beverages | Bakery |

| Beverages | |

| Breakfast Cereals | |

| Condiments/Sauces | |

| Confectionery | |

| Dairy and Dairy Alternative Products | |

| RTE/RTC Food Products | |

| Snacks | |

| Personal Care and Cosmetics | |

| Supplements | Baby Food and Infant Formula |

| Elderly Nutrition and Medical Nutrition | |

| Sport/Performance Nutrition |

| Protein Type | Casein and Caseinates | |

| Collagen | ||

| Egg Protein | ||

| Gelatin | ||

| Insect Protein | ||

| Milk Protein | ||

| Whey Protein | ||

| Other Animal Protein | ||

| End User | Animal Feed | |

| Food and Beverages | Bakery | |

| Beverages | ||

| Breakfast Cereals | ||

| Condiments/Sauces | ||

| Confectionery | ||

| Dairy and Dairy Alternative Products | ||

| RTE/RTC Food Products | ||

| Snacks | ||

| Personal Care and Cosmetics | ||

| Supplements | Baby Food and Infant Formula | |

| Elderly Nutrition and Medical Nutrition | ||

| Sport/Performance Nutrition | ||

Market Definition

- End User - The Protein Ingredients Market operates on a B2B basis. Food, Beverages, Supplements, Animal Feed, and Personal Care & Cosmetic manufacturers are considered to be end-consumers in the market studied. The scope excludes manufacturers buying liquid/dry whey to be used for application as a binding agent or thickener or other non-protein applications.

- Penetration Rate - Penetration Rate is defined as the percentage of Protein-Fortified End User Market Volume in the Overall End User Market Volume.

- Average Protein Content - Average protein content is the average protein content present per 100 g of product manufactured by all end-user companies considered under the scope of this report.

- End User Market Volume - End-user market volume is the consolidated volume of all types and forms of end-user products in the country or region.

| Keyword | Definition |

|---|---|

| Alpha-lactalbumin (α-Lactalbumin) | It is a protein that regulates the production of lactose in the milk of almost all mammalian species. |

| Amino acid | It is an organic compound that contains both amino and carboxylic acid functional groups, which are required for the synthesis of body protein and other important nitrogen-containing compounds, such as creatine, peptide hormones, and some neurotransmitters. |

| Blanching | It is the process of briefly heating vegetables with steam or boiling water. |

| BRC | British Retail Consortium |

| Bread improver | It is a flour-based blend of several components with specific functional properties designed to modify dough characteristics and give quality attributes to bread. |

| BSF | Black Soldier Fly |

| Caseinate | It is a substance produced by adding an alkali to acid casein, a derivative of casein. |

| Celiac disease | Celiac disease is an immune reaction to eating gluten, a protein found in wheat, barley, and rye. |

| Colostrum | It is a milky fluid that’s released by mammals that have recently given birth before breast milk production begins. |

| Concentrate | It is the least processed form of protein and has a protein content ranging from 40-90% by weight. |

| Dry protein basis | It refers to the percentage of "pure protein" present in a supplement after the water in it is completely removed through heat. |

| Dry whey | It is the product resulting from drying fresh whey which has been pasteurized and to which nothing has been added as a preservative. |

| Egg protein | It is a mixture of individual proteins, including ovalbumin, ovomucoid, ovoglobulin, conalbumin, vitellin, and vitellenin. |

| Emulsifier | It is a food additive that facilitates the blending of foods that are immiscible with one another, such as oil and water. |

| Enrichment | It is the process of addition of micronutrients that are lost during the processing of the product. |

| ERS | Economic Research Service of the USDA |

| Extrusion | It is the process of forcing soft mixed ingredients through an opening in a perforated plate or die designed to produce the required shape. The extruded food is then cut to a specific size by blades. |

| Fava | Also known as Faba, it is another word for yellow split beans. |

| FDA | Food and Drug Administration |

| Flaking | It is a process in which typically a cereal grain (like corn, wheat, or rice) is broken down into grits, cooked with flavors and syrups, and then pressed into flakes between cooled rollers. |

| Foaming agent | It is a food ingredient that makes it possible to form or maintain a uniform dispersion of a gaseous phase in a liquid or solid food. |

| Foodservice | It refers to the part of the food industry which includes businesses, institutions, and companies which prepare meals outside the home. It includes restaurants, school and hospital cafeterias, catering operations, and many other formats. |

| Fortification | It is the deliberate addition of micronutrients that are not found in them naturally or which are lost during processing, to improve a food product's nutritional value. |

| FSANZ | Food Standards Australia New Zealand |

| FSIS | Food Safety and Inspection Service |

| FSSAI | Food Safety and Standards Authority of India |

| Gelling agent | It is an ingredient that functions as a stabilizer and thickener to provide thickening without stiffness through the formation of gel. |

| GHG | Greenhouse Gas |

| Gluten | It is a family of proteins found in grains, including wheat, rye, spelt, and barley. |

| Hemp | It is a botanical class of Cannabis sativa cultivars grown specifically for industrial or medicinal use. |

| Hydrolysate | It is a form of protein manufactured by exposing the protein to enzymes that can partially break the bonds between the protein's amino acids and break down large, complicated proteins into smaller pieces. Its processing makes it easier and quicker to digest. |

| Hypoallergenic | It refers to a substance that causes fewer allergic reactions. |

| Isolate | It is the purest and most processed form of protein which has undergone separation to obtain a pure protein fraction. It typically contains ≥ 90% of protein by weight. |

| Keratin | It is a protein that helps form hair, nails, and the outer layer of skin. |

| Lactalbumin | It is the albumin contained in milk and obtained from whey. |

| Lactoferrin | It is an iron‑binding glycoprotein that is present in the milk of most mammals. |

| Lupin | It is the yellow legume seeds of the genus Lupinus. |

| Millenial | Also known as Generation Y or Gen Y, it refers to the people born from 1981 to 1996. |

| Monogastric | It refers to an animal with a single-compartmented stomach. Examples of monogastric include humans, poultry, pigs, horses, rabbits, dogs, and cats. Most monogastric are generally unable to digest much cellulose food materials such as grasses. |

| MPC | Milk protein concentrate |

| MPI | Milk protein isolate |

| MSPI | Methylated soy protein isolate |

| Mycoprotein | Mycoprotein is a form of single-cell protein, also known as fungal protein, derived from fungi for human consumption. |

| Nutricosmetics | It is a category of products and ingredients that act as nutritional supplements to care for skin, nails, and hair natural beauty. |

| Osteoporosis | It is a medical condition in which the bones become brittle and fragile from loss of tissue, typically as a result of hormonal changes, or deficiency of calcium or vitamin D. |

| PDCAAS | Protein digestibility-corrected amino acid score (PDCAAS) is a method of evaluating the quality of a protein based on both the amino acid requirements of humans and their ability to digest it. |

| Per-capita consumption of animal protein | It is the average amount of animal protein (such as milk, whey, gelatin, collagen, and egg proteins) that is readily available for consumption by each person in an actual population. |

| Per-capita consumption of plant protein | It is the average amount of plant protein (such as soy, wheat, pea, oat, and hemp proteins) that is readily available for consumption by each person in an actual population. |

| Quorn | It is a microbial protein manufactured using mycoprotein as an ingredient, in which the fungus culture is dried and mixed with egg albumen or potato protein, which acts as a binder, and then is adjusted in texture and pressed into various forms. |

| Ready-to-Cook (RTC) | It refers to food products that include all of the ingredients, where some preparation or cooking is required through a process that is given on the package. |

| Ready-to-Eat (RTE) | It refers to a food product prepared or cooked in advance, with no further cooking or preparation required before being eaten. |

| RTD | Ready-to-Drink |

| RTS | Ready-to-Serve |

| Saturated fat | It is a type of fat in which the fatty acid chains have all single bonds. It is generally considered unhealthy. |

| Sausage | It is a meat product made of finely chopped and seasoned meat, which may be fresh, smoked, or pickled and which is then usually stuffed into a casing. |

| Seitan | It is a plant-based meat substitute made out of wheat gluten. |

| Softgel | It is a gelatin-based capsule with a liquid fill. |

| SPC | Soy protein concentrate |

| SPI | Soy protein isolate |

| Spirulina | It is a biomass of cyanobacteria that can be consumed by humans and animals. |

| Stabilizer | It is an ingredient added to food products to help maintain or enhance their original texture, and physical and chemical characteristics. |

| Supplementation | It is the consumption or provision of concentrated sources of nutrients or other substances that are intended to supplement nutrients in the diet and is intended to correct nutritional deficiencies. |

| Texturant | It is a specific type of food ingredient that is used to control and alter the mouthfeel and texture of food and beverage products. |

| Thickener | It is an ingredient that is used to increase the viscosity of a liquid or dough and make it thicker, without substantially changing its other properties. |

| Trans fat | Also called trans-unsaturated fatty acids or trans fatty acids, it is a type of unsaturated fat that naturally occurs in small amounts in meat. |

| TSP | Textured soy protein |

| TVP | Textured vegetable protein |

| WPC | Whey protein concentrate |

| WPI | Whey protein isolate |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms