Craniomaxillofacial Fixation Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.08 Billion |

| Market Size (2031) | USD 2.69 Billion |

| Growth Rate (2026 - 2031) | 5.35% CAGR |

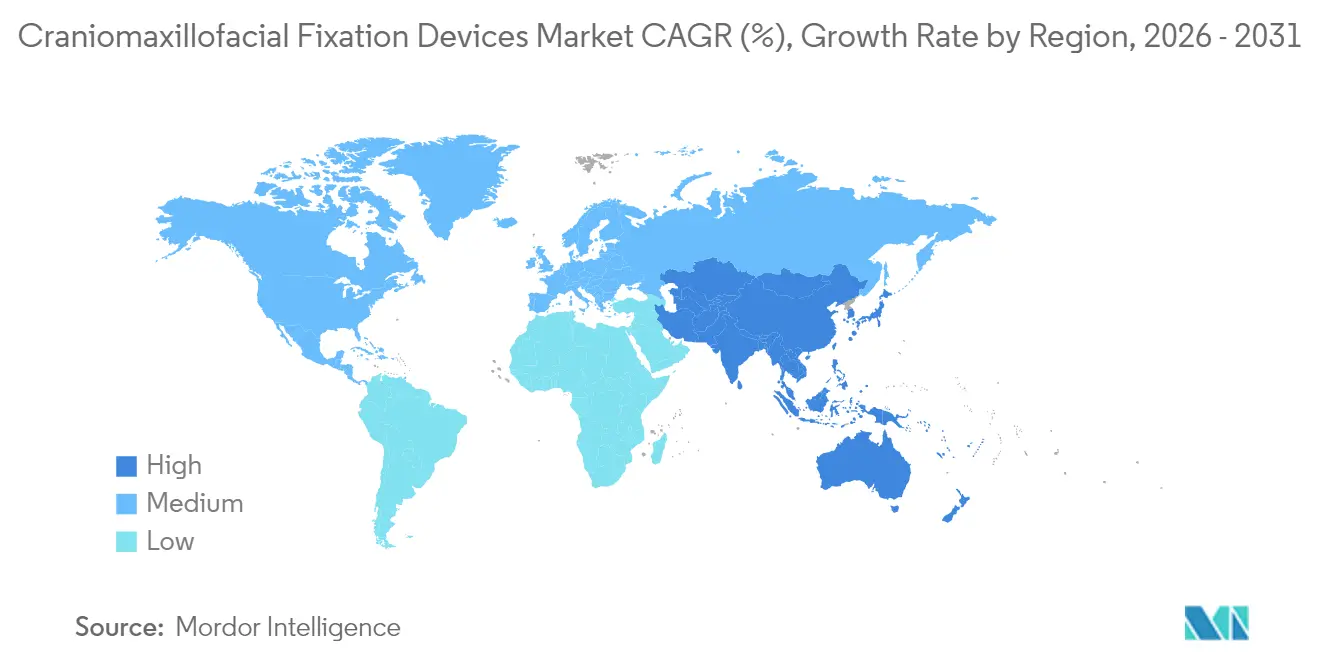

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Craniomaxillofacial Fixation Devices Market Analysis by Mordor Intelligence

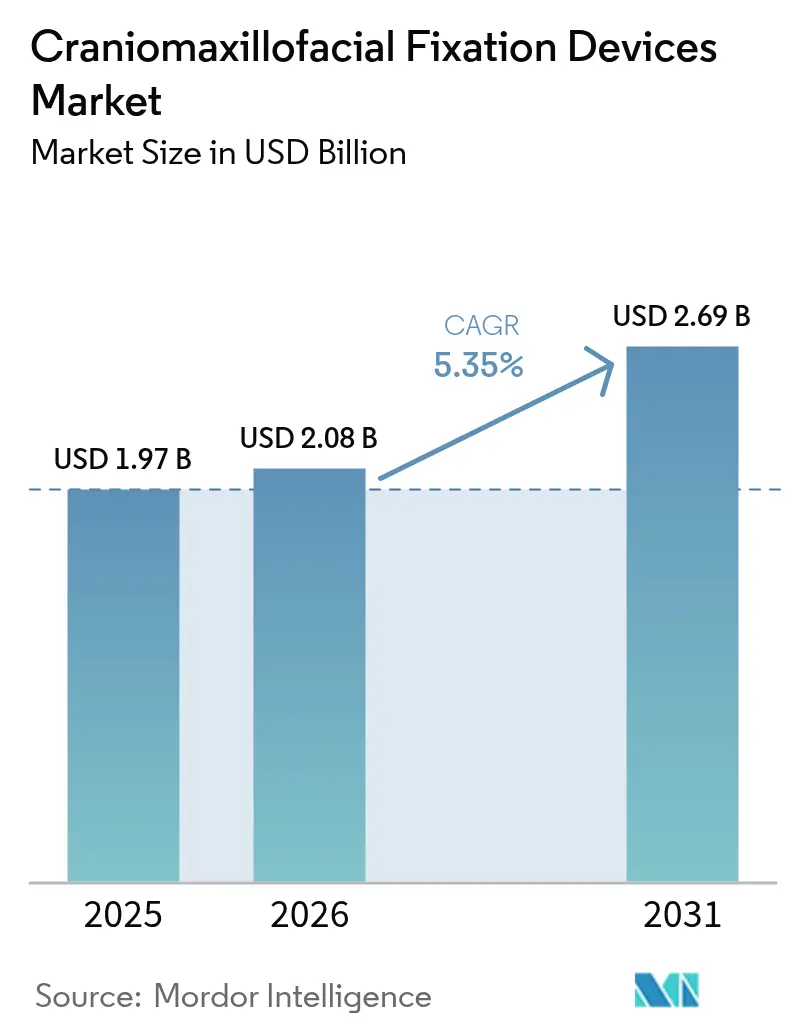

The craniomaxillofacial fixation devices market size was valued at USD 1.97 billion in 2025 and estimated to grow from USD 2.08 billion in 2026 to reach USD 2.69 billion by 2031, at a CAGR of 5.35% during the forecast period (2026-2031). Demand remains healthy as rising trauma incidence, steady orthognathic surgery volumes and new bio-resorbable materials widen clinical adoption, while 3D-printed patient-specific solutions create premium price tiers that underpin revenue growth. Integration of additive manufacturing with bio-polymers shifts the competitive focus from commodity titanium sets to customized implants that shorten operating room time and reduce secondary procedures. Regulatory tightening, notably the Quality Management System Regulation that mandates ISO 13485:2016 compliance from February 2026, pushes manufacturers toward harmonized global quality systems and favors firms with robust compliance infrastructure. At the same time, hospital buyers expect evidence of cost savings under value-based care, prompting suppliers to link implant choice to reduced re-operation risk and shorter lengths of stay.

Key Report Takeaways

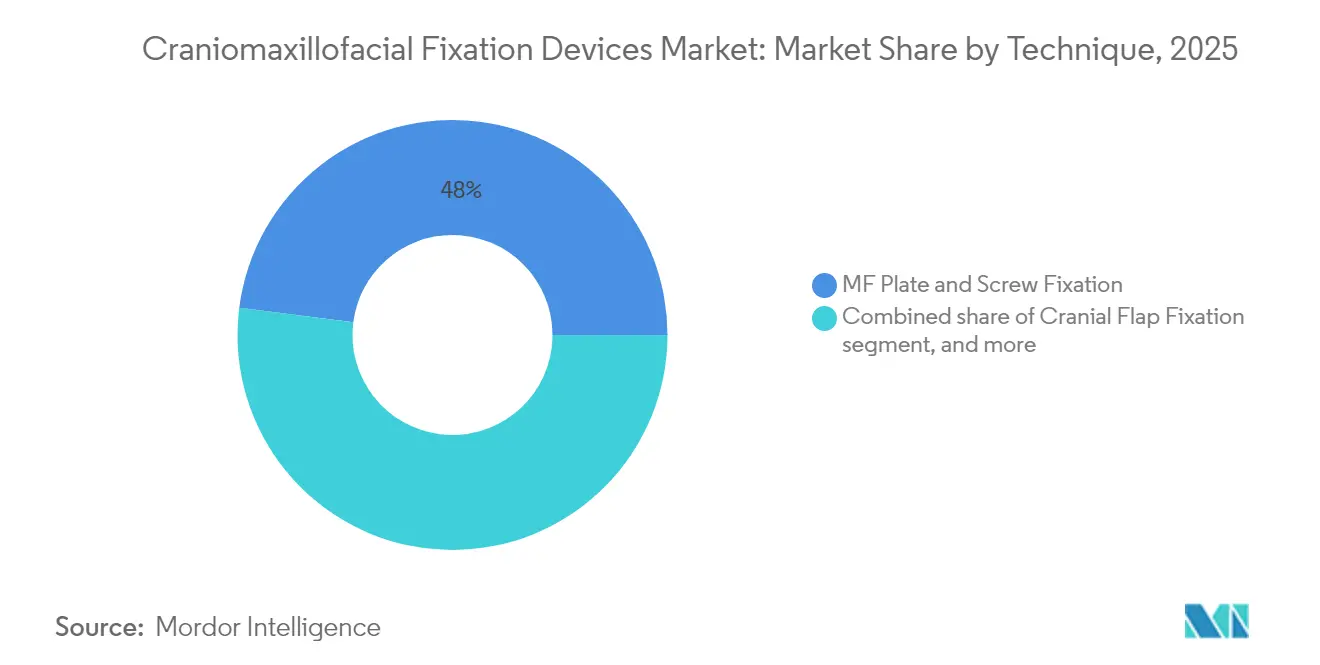

- By technique, MF plate & screw fixation held 47.98% of the craniomaxillofacial fixation devices market share in 2025; CMF distraction is predicted to post a 7.25% CAGR through 2031.

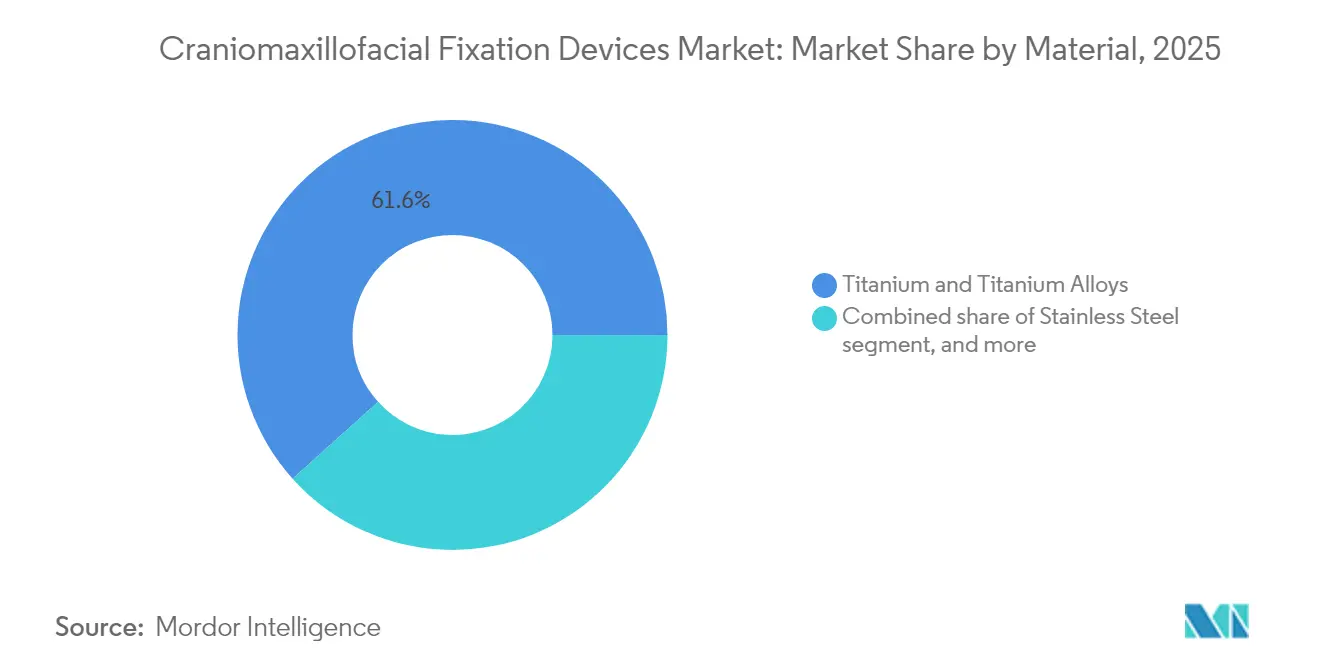

- By material, titanium & titanium alloys accounted for 61.65% of the craniomaxillofacial fixation devices market size in 2025, whereas bio-resorbable polymers are set to expand at an 8.12% CAGR to 2031.

- By application, orthognathic & dental surgery captured 33.92% share of the craniomaxillofacial fixation devices market size in 2025; pediatric craniosynostosis repair is advancing at an 7.88% CAGR over the same period.

- By geography, North America commanded 40.02% share of the craniomaxillofacial fixation devices market; Asia-Pacific is advancing at an 6.21% CAGR over the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Craniomaxillofacial Fixation Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing incidence of craniofacial trauma | +1.8% | Global, concentrated in North America & Europe | Medium term (2-4 years) |

| Rising adoption of minimally invasive surgical techniques | +1.2% | North America & EU, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Continuous technological advancements in fixation devices | +1.5% | Global, led by North America & Europe | Long term (≥ 4 years) |

| Growing utilization of patient-specific and 3D-printed implants | +1.0% | North America & EU, selective Asia-Pacific adoption | Medium term (2-4 years) |

| Expansion of healthcare infrastructure and procurement initiatives in emerging markets | +0.8% | Asia-Pacific core, spill-over to MEA & South America | Long term (≥ 4 years) |

| Integration of navigation and augmented-reality systems | +0.6% | North America & EU, limited Asia-Pacific penetration | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Incidence of Craniofacial Trauma

Urbanization, higher road traffic density and contact-sport participation continue to elevate facial injury rates, making mandibular fractures the most frequent indication for fixation plates. Aging in developed economies adds fall-related injuries, while polytrauma cases demand multi-site fixation, thus requiring broad system portfolios rather than single configurations. Surgeons increasingly adopt modular sets that cover midface, mandible and cranial repairs in one sterile tray, which raises average selling prices. Hospitals value complete kits that shorten turnover time, reinforcing manufacturer preference for players able to bundle screws, plates and resorbables under unified compatibility guarantees. The trend sustains steady baseline procedure volume even in mature regions, protecting the craniomaxillofacial fixation devices market from cyclical capital-equipment swings.

Rising Adoption of Minimally Invasive Surgical Techniques

Intraoral distraction devices and concealed maxillary distractors avoid visible scarring while preserving bone blood supply, improving cosmetic outcomes that matter strongly to pediatric and adult patients alike. Rapid-prototype guide plates generated from CT data enable precise osteotomies, cutting operating room time and reducing radiation exposure from intra-operative imaging. As surgeons gain confidence, minimally invasive protocols become first-line choice rather than alternative, prompting redesigns toward slimmer plate profiles and low-head screws that fit through smaller incisions. Device makers differentiate through ergonomic instrumentation that permits placement without wide exposure, and through color-coded kits that streamline workflow. This shift favors suppliers able to align mechanical strength with smaller footprint hardware.

Continuous Technological Advancements in Fixation Devices

Bio-resorbable PLA and PGA blends now reach tensile strengths sufficient for many midface and pediatric cranial procedures, eliminating follow-up hardware removal surgeries that add cost and risk. Surface-treated titanium plates coated with calcium-phosphate accelerate osseointegration, enabling earlier load-bearing and shorter splinting durations. Embedded micro-sensors that relay stability data remain in pilot use, but point toward postoperative monitoring without repeated radiographs. Additive manufacturing merges these material gains with geometry freedom, letting engineers thicken high-stress regions while thinning others for weight reduction. Overall, technology lifts clinician expectations for devices that actively support healing rather than merely anchor bone segments.

Growing Utilization of Patient-Specific and 3D-Printed Implants

Customized implants address anatomical deficits after tumor resection or complex trauma in ways stock plates cannot, reducing intra-operative bending and contouring time. Implant production at hospital-based 3D labs trims lead times from weeks to days and allows plate-hole patterns aligned to osteotomy plans, improving screw purchase. Porous hydroxyapatite-ceramic prints foster vascular ingrowth and bone replacement, making implants part of the regenerative process instead of inert supports. Because units are built on demand, inventory carrying costs drop, empowering smaller vendors with design software to compete against large catalog-based incumbents. Regulators streamline patient-matched submissions under existing device codes, further leveling market entry barriers.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Unfavorable reimbursement and coverage policies | -1.4% | Global, most severe in North America | Short term (≤ 2 years) |

| High procedural costs and price pressure | -1.1% | Global, with regional variations | Medium term (2-4 years) |

| Stringent regulatory compliance and certification requirements | -0.9% | Global, particularly U.S. & EU | Medium term (2-4 years) |

| Limited access to specialized CMF surgeons in rural regions | -0.6% | Emerging markets & rural areas worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Unfavorable Reimbursement and Coverage Policies

Medicare fee-cuts of up to 20% on selected CPT codes erode hospital margins, pushing purchasing departments to cap implant spend per procedure[1]Centers for Medicare & Medicaid Services, “2025 Physician Fee Schedule Final Rule,” medicare.gov. Private insurers request extensive pre-authorization, delaying surgeries and forcing surgeons to document functional necessity beyond aesthetic benefit. In single-payer systems, formularies often prefer generic plates over branded innovations, limiting uptake of premium resorbables despite superior outcomes. Manufacturers respond by publishing cost-utility studies that show savings from avoiding removal surgeries, yet payers demand longitudinal evidence. Near-term, this restraint tempers the craniomaxillofacial fixation devices market growth until value-based data accumulate.

High Procedural Costs and Price Pressure

Multicomponent fixation procedures involve implants, specialized drills and plating tools that can push supply cost near USD 9,000 per trauma case according to purchasing audits. Group purchasing organizations leverage aggregated volume to demand rebates, compressing unit margins. International reference pricing highlights discrepancies, prompting hospitals in Latin America and Africa to request parity with Asia-Pacific quotes. Device makers streamline SKUs and convert instrument sets to modular designs that serve several plate families, cutting sterilization overhead but also reducing perceived differentiation. Persistent price erosion compels companies to focus R&D on features that create measurable value, such as reduced OR time or elimination of follow-up surgery.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technique: Distraction Leads Innovation Wave

CMF distraction devices are forecast to log a 7.25% CAGR through 2031, well above the overall craniomaxillofacial fixation devices market growth rate. The method is now standard for mandibular lengthening in neonates with airway obstruction, achieving 91.3% success in averting tracheostomy according to multicenter data. MF plate & screw fixation remains the workhorse, holding 47.98% market share in 2025 as surgeons rely on its familiarity and immediate load-bearing strength. Technique selection increasingly turns on patient age and defect complexity rather than surgeon preference, with bio-resorbable distraction systems gaining pediatric favor for eliminating secondary hardware removal. The craniomaxillofacial fixation devices market size for distraction systems is projected to reach USD 696 million by 2031, implying a widening revenue gap over cranial flap-only sets.

Surgeons demand hybrid solutions that pair distraction with navigation guidance, creating opportunities for firms that integrate threaded distractors with pre-bent patient-matched guides. External devices lose ground to internal systems that avoid pin-site infections, furthering procedure acceptance among caregivers. Meanwhile, temporomandibular joint replacement grows steadily, supported by custom alloplastic components but remains a smaller share of the craniomaxillofacial fixation devices market. As payers acknowledge long-term airway and facial symmetry benefits, adoption barriers lessen, reinforcing the segment’s outperformance.

By Material: Bio-Resorbables Challenge Titanium Dominance

Titanium & titanium alloys retained 61.65% share in 2025, reflecting decades-long surgeon trust in their mechanical endurance. Yet bio-resorbable polymers, expanding at 8.12% CAGR, chip away at this lead, particularly in pediatric cranial vault and midface procedures where growth plates mandate temporary fixation. Early formulations suffered unpredictable absorption, but next-generation PLLA-PGA blends deliver consistent modulus retention for 20-24 weeks, matching critical bone healing windows. As a result, the craniomaxillofacial fixation devices market size attributable to bio-resorbables is estimated to double by 2030. Stainless steel holds marginal share in cost-sensitive regions due to corrosion concerns, whereas carbon-fiber-reinforced PEEK enters select trauma indications where radiolucency aids postoperative imaging.

Three-material composite plates that combine titanium skeletons with resorbable arms illustrate innovation momentum. Such designs give immediate strength while leaving only low-profile titanium after polymer absorption, minimizing palpability in thin-tissue regions. Additive manufacturing accelerates iteration cycles; vendors now launch updated compositions within 12 months versus 36 months under conventional casting. The material landscape is thus dynamic, fostering competition not on alloy grade alone but on tailored degradation and imaging compatibility attributes.

By Application: Pediatric Segment Drives Premium Growth

Orthognathic & dental surgery represented 33.92% of 2025 revenue, reflecting stable demand for malocclusion correction and dental implant support across affluent populations. Pediatric craniosynostosis repair, however, registers the fastest 7.88% CAGR, propelled by spring-assisted cranioplasty that reduces operative blood loss and shorter hospital stays. Device kits designed for infants incorporate low-torque screws and color coding to match bone thickness, enabling safer procedures. Hospitals willingly pay a premium because avoiding hardware removal cuts anesthesia exposure risks in children. Consequently, the craniomaxillofacial fixation devices market share of pediatric indications is forecast to exceed 18.60% by 2031, up from 13.42% in 2025.

Neurosurgery and ENT remain steady contributors, relying on cranial flap fixation plates that seldom change design, yet volume persists due to consistent tumor and trauma caseload. Plastic & aesthetic surgery shows moderate growth through orbital floor and zygomatic reconstructions following high-energy injuries. Procedure mix variation underscores supplier need for broad catalogs that span cranial mesh to micro plates, an advantage held by top three vendors.

Geography Analysis

North America generated 40.02% of global 2025 revenue, anchored by well-reimbursed trauma care and high awareness of pediatric craniofacial conditions. Procedure growth plateaus near population growth, but ASPs remain the highest worldwide thanks to rapid uptake of resorbables and patient-specific implants. Europe follows with subdued but stable expansion; strict MDR documentation raises cost of market entry, tilting competitive balance toward established firms with mature clinical evidence dossiers. Hospitals there increasingly request environmental impact statements, prompting early trials of recyclable instrument trays.

Asia-Pacific exhibits the most momentum at a 6.21% CAGR, led by China’s fast build-out of tier-III trauma centers and India’s expansion of medical insurance coverage. Domestic companies gain share in standard trauma plates, yet imported bio-resorbables dominate premium pediatric cases. Governments encourage local 3D-printing initiatives, but surgeons still rely on U.S. or German planning software for complex reconstructions, maintaining cross-border supply chains. The craniomaxillofacial fixation devices market size in Asia-Pacific could surpass that of Europe by 2028 if current volume trends hold.

Latin America and the Middle East & Africa grow from a small base, driven mainly by private hospital chains positioning as medical-tourism hubs. Exchange-rate volatility, however, dampens large capital purchases and favors consignment stocking over outright ownership. Vendors must offer flexible payment models such as pay-per-use for patient-specific implants to penetrate these regions. Overall, geographic diversification mitigates exposure to reimbursement cuts in mature markets.

Regulatory Landscape

Craniomaxillofacial (CMF) fixation systems are regulated as implantable surgical devices in major markets, with the United States commonly requiring 510(k) clearance for Class II CMF fixation products such as external mandibular fixators (FDA product code MQN, under 21 CFR 872.4760). Submissions typically center on standardized bench and safety evidence, including biocompatibility (ISO 10993 series), mechanical performance (for example, ASTM F382 for plate bending fatigue and ASTM F543 for bone screw torque), and sterilization validation (for example, ISO 17665-1 and ISO 14937), shaping design controls and verification plans for both titanium and bio-resorbable systems.

Regulatory compliance obligations are tightening and shifting toward harmonized quality frameworks, highlighted by the FDA Quality System Regulation amendments finalized in February 2024 that transition quality expectations toward a QMS model aligned with ISO 13485:2016, consistent with the report context noting ISO 13485:2016 compliance requirements taking effect in February 2026. In Europe, the EU Medical Device Regulation (MDR) continues to raise the documentation bar for implantables and custom-made pathways; at the same time, activity around patient-matched workflows is advancing, illustrated by the January 2026 FDA clearance for Materialise Personalized Guides and Models for craniomaxillofacial surgery and 2026 clinical work demonstrating an EU MDR Article 5(5)-compliant point-of-care manufacturing framework for patient-matched 3D-printed PEEK CMF implants at University Hospital of Basel.

Competitive Landscape

The market remains moderately concentrated; Stryker, DePuy Synthes and Zimmer Biomet collectively control close to 55% of global revenue through expansive catalogs and sales networks. Stryker’s Pangea Plating System launch in 2024 broadened its variable-angle offering, winning early adoption for complex trauma cases. DePuy Synthes leverages its power-tool ecosystem to lock hospitals into integrated solutions, while Zimmer Biomet bundles patient-specific planning software with cranial plates, adding digital stickiness. KLS Martin and Medartis succeed in specialist niches such as micro-plates for orbital repair, relying on surgeon-faculty relationships and responsive custom fabrication.

Disruptors capitalize on in-hospital 3D-printing labs, selling design services and titanium powder rather than finished plates. They avoid inventory costs and undercut lead times, appealing to academic centers. Regulatory change is a double-edged sword: ISO 13485:2016 alignment raises entry costs, yet patient-matched device pathways lower evidence hurdles for one-off implants. Larger incumbents use M&A, evidenced by Enovis acquiring LimaCorporate in January 2025 to access European craniofacial lines and additive capabilities. Recent FDA workforce reductions could elongate 510(k) review times, inadvertently benefiting firms with dedicated regulatory affairs teams able to navigate complex queries.

Overall, competition pivots on offering full ecosystems—hardware, software and service—rather than stand-alone plates. Companies that demonstrate reduced operating room minutes or avoided second surgeries gain pricing leeway even under cost-containment pressure.

Craniomaxillofacial Fixation Devices Industry Leaders

Stryker Corporation

Johnson and Johnson

Acumed LLC

Zimmer Biomet Holdings Inc.

Medtronic Plc

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Patient-specific and point-of-care manufacturing is expanding the addressable premium tier in CMF fixation by reducing intra-operative contouring and compressing lead times for complex reconstructions. In 2026, Materialise launched custom-made PEEK implants for its craniomaxillofacial portfolio in Europe (excluding Switzerland), and point-of-care deployment models are being productized, with Meticuly demonstrating a modular Factory-in-a-Box concept positioned for on-site production of patient-specific implants in under 24 hours. These developments create whitespace for suppliers that bundle virtual surgical planning, guides/models, and implant manufacturing services alongside conventional plate-and-screw sets, particularly in tumor resection, complex trauma, and revision cases where stock components underperform.

Portfolio adjacency with regenerative solutions is becoming a practical route to differentiation under cost pressure, as hospitals increasingly ask for outcomes evidence beyond hardware performance. In May 2026, DePuy Synthes entered an exclusive distribution agreement with CGBIO to commercialize NOVOSIS (a growth-factor bone graft substitute) in the United States, Canada, and Australia, indicating a go-to-market pattern where fixation vendors complement implants with biologics to support fusion and defect fill in CMF indications. In parallel, incremental instrumentation innovations in bio-resorbables (for example, Inion announcing an UltraPress Inserter for bioabsorbable cranial surgery in 2026) highlight opportunities in workflow reliability and ease-of-use, especially for pediatric cranial procedures where resorbables can remove the need for secondary hardware-removal surgeries.

Recent Industry Developments

- June 2026: Stryker launched the TPX HD small bone power tool, positioned to support oral maxillofacial procedures with improved visibility and control in confined surgical spaces. The launch strengthens Stryker's procedural ecosystem around CMF fixation by pairing hardware sets with enabling instrumentation that can reduce handling friction in complex cases.

- May 2026: DePuy Synthes (Johnson and Johnson) entered an exclusive distribution agreement with CGBIO to commercialize NOVOSIS in the United States, Canada, and Australia, including use across orthopaedic applications that span craniomaxillofacial surgery. This aligns fixation offerings with biologics to support fusion and defect fill in CMF indications.

- November 2025: Acumed completes acquisition of TECHFIT Digital Surgery assets to broaden patient-specific planning and reconstruction platforms, reinforcing competition around integrated digital-to-device workflows in craniomaxillofacial procedures. The move accelerates adoption of digital planning and planning-to-implant workflows.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers devices used to fix, stabilize, and support bones in cranial and facial procedures, including plates, screws, meshes, distraction systems, and TMJ replacement components used during surgery.

Scope exclusions: Non-fixation surgical tools, imaging equipment, and general dental consumables are excluded from the market values.

Segmentation Overview

- By Technique

- Cranial Flap Fixation

- CMF Distraction

- Temporomandibular Joint (TMJ) Replacement

- MF Plate & Screw Fixation

- Bio-Resorbable Fixation

- Others

- By Material

- Titanium & Titanium Alloys

- Stainless Steel

- Bio-Resorbable Polymers (PLA, PGA, PDO)

- Bio-Ceramics (Hydroxyapatite, Tricalcium Phosphate)

- Patient-Specific 3-D Printed Composites

- By Application

- Neurosurgery & ENT

- Orthognathic & Dental Surgery

- Plastic & Aesthetic Surgery

- Paediatric Craniosynostosis Repair

- Others

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to build the fact base for procedure volumes, clinical adoption, and country-level context before any modeling is finalized. We reviewed public sources such as the US FDA device databases, the US National Library of Medicine for clinical literature, the OECD health statistics, the World Bank indicators, and trade and customs statistics where implants and medical devices are reported.

On the supply side, we also relied on company annual reports, investor presentations, product catalogs, regulatory disclosures, and reputable medical society publications to understand device positioning and typical pricing ranges. Where it helped close gaps, we used paid subscriptions for company financials and intelligence, patent databases, and shipment-level import and export data to cross-check directionally. These examples are not exhaustive, and we reviewed other public documents and data sources for collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on structured interviews and surveys with manufacturers, distributors, hospital procurement teams, and clinicians who regularly use CMF systems across major regions. Respondent input was used to confirm the technique mix in routine practice, typical replacement cycles, and how pricing varies by material choice and case complexity. We then followed up where points were unclear to make sure the model assumptions matched observed buying and usage patterns.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 18% | APAC: 48% |

| Mid tier: 45% | Functional/Unit leaders: 29% | EMEA: 33% |

| Smaller Players: 21% | Managers: 53% | Americas: 19% |

Market-Sizing & Forecasting

Market sizing uses a top-down and bottom-up flow in a practical way. First, demand pools are rebuilt using procedure-based logic, where country-level volumes for trauma, orthognathic, craniosynostosis repair, and neurosurgery-related cranial flap fixation are combined with typical fixation utilization per procedure. Those outputs are then converted into value using realistic price bands by material and technique.

To keep the model grounded, we track a few inputs closely, such as facial trauma incidence and surgery volumes, adoption of bioresorbable polymers versus metal systems, mix shift toward patient-specific 3D printed implants, hospital purchasing constraints, and the relative share of TMJ replacement within CMF case loads. Where public data is thin, we use interview ranges to fill missing pieces and document the assumption so it can be stress tested.

For forecasting, scenario analysis is applied around procedure growth and adoption curves, and the final trajectory is checked against expert consensus on pricing pressure and technology uptake. Bottom-up checks are used selectively, such as sampled supplier and channel checks for ASPs and approximate volume roll-ups by major technique, which helps flag over-counting before totals are finalized.

Data Validation & Update Cycle

Outputs are triangulated against independent signals, including regional shares, procedure growth expectations, and observed pricing movements by material class. When variances are large, we review the contributing inputs step by step and run sensitivity checks on the factors that typically move the result most, then the figures are peer reviewed before sign-off.

The study is refreshed annually, and interim updates are triggered when material events occur, such as regulatory changes, reimbursement shifts, or notable technology adoption changes. Before delivery, a final pass is done to ensure the latest public updates and primary feedback are reflected consistently across the model.

Mordor Intelligence's Cranio Maxillofacial Fixation Devices Market Size Measured Against Other Published Estimates

Published market sizes for CMF fixation devices can vary because groups do not always count the same device set, the same procedure pool, or the same year for currency conversion and inflation handling. Differences also show up when one estimate leans more on shipment assumptions and another leans more on procedure demand.

Bone graft substitutes are frequently bundled into some third-party totals, but that item sits outside Mordor Intelligence's scope here, which keeps the value tied to fixation and stabilization systems rather than the wider reconstruction basket. The remaining spread typically comes from how TMJ replacement is treated, how fast bioresorbable adoption is assumed to rise, and whether patient-specific implant pricing is modeled as a premium across all regions or only where reimbursement supports it.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.97 B (2025) | |

| Industry Publisher A | USD 2.13 B (2024) | Uses an earlier base year and a broader segmentation basket, and the device definition appears to be wider by end-use and product group, which can lift the starting value versus a fixation-only cut. |

| Global Consultancy B | USD 1.40 B (2024) | Likely applies a narrower demand pool or lower utilization per procedure and may understate premium pricing for patient-specific implants, which can pull down the 2024 total even if the growth rate is higher. |

Across the three figures, the main takeaway is that scope and pricing logic drive most of the gap, not the direction of growth itself. By tying value to procedure volumes, technique mix, and realistic price bands that can be checked with interviews and public signals, the model stays traceable and easier to replicate when assumptions need updating.

Key Questions Answered in the Report

What is the forecast revenue for craniomaxillofacial fixation devices by 2031?

The market is projected to generate USD 2.69 billion by 2031, reflecting a 5.35% CAGR.

Which technique segment is expanding fastest?

CMF distraction devices lead with a 7.25% CAGR to 2031.

Why are bio-resorbable polymers gaining popularity?

They eliminate hardware removal surgeries and show 8.12% CAGR growth, especially in pediatric procedures.

Which region shows the strongest growth momentum?

Asia-Pacific advances at a 6.21% CAGR, fueled by trauma center expansion and insurance coverage gains.

How will the 2026 FDA quality regulation affect suppliers?

All manufacturers must meet ISO 13485:2016, favoring companies with established compliance systems and potentially lengthening approval timelines.

Page last updated on: