Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

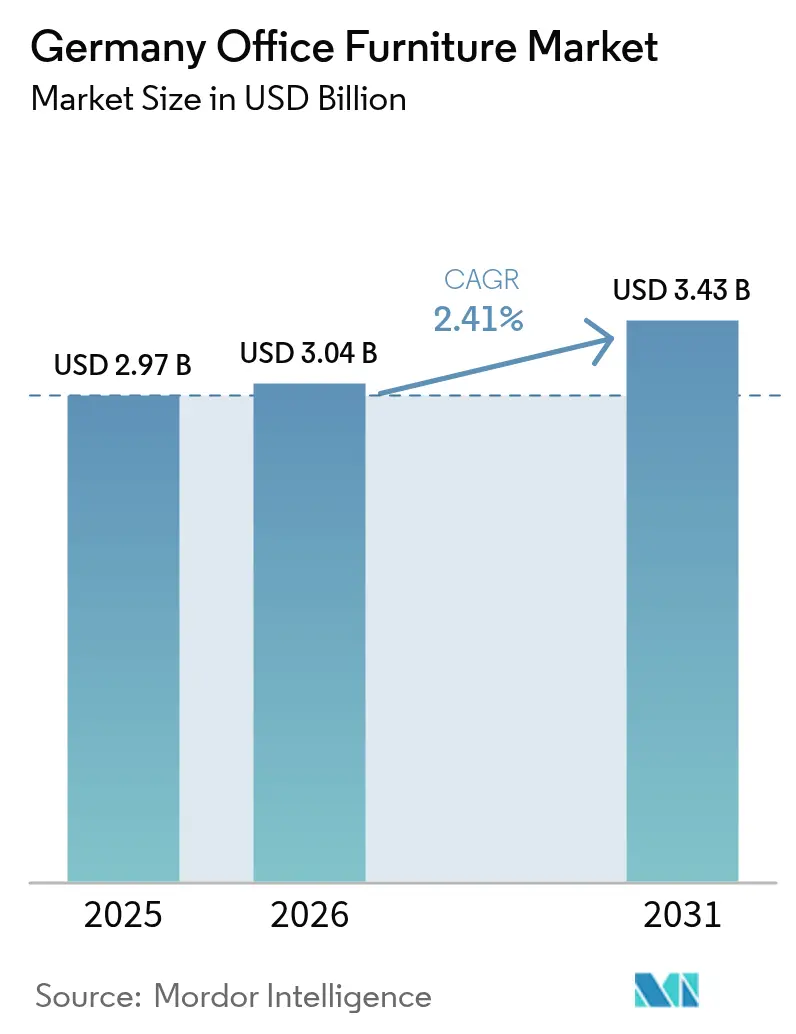

| Base Year Market Size (2025) | USD 2.97 Billion |

| Market Size (2026) | USD 3.04 Billion |

| Market Size (2031) | USD 3.43 Billion |

| Growth Rate (2026 - 2031) | 2.41% CAGR |

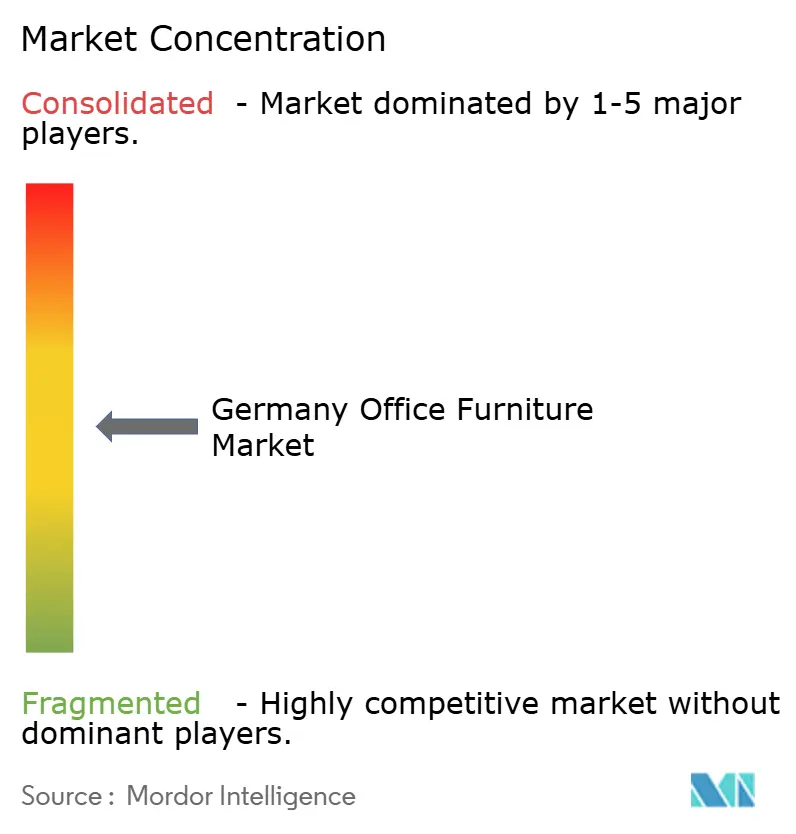

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Office Furniture Market Analysis by Mordor Intelligence

The Germany office furniture market size is expected to grow from USD 2.97 billion in 2025 to USD 3.04 billion in 2026 and is forecast to reach USD 3.43 billion by 2031 at 2.41% CAGR over 2026-2031. The market grows steadily because employers are re-planning spaces for hybrid work, investing in certified ergonomic seating, and favoring circular-economy procurement that supports corporate sustainability targets[1]“Toward a Circular Economy in the Furniture Industry,” Fraunhofer IPK, ipk.frahofer.de. Large redevelopment schemes in Munich, Berlin, and Frankfurt continue to open high-specification fit-out contracts, while mid-range products dominate corporate buying as firms reconcile quality expectations with cost controls. At the same time, recycled plastic and polymer innovations win share from traditional materials due to weight, design flexibility, and verified carbon reductions. Direct manufacturer sales flourish because professional buyers demand customization, project logistics, and long-term service agreements that retail formats seldom replicate.

Key Report Takeaways

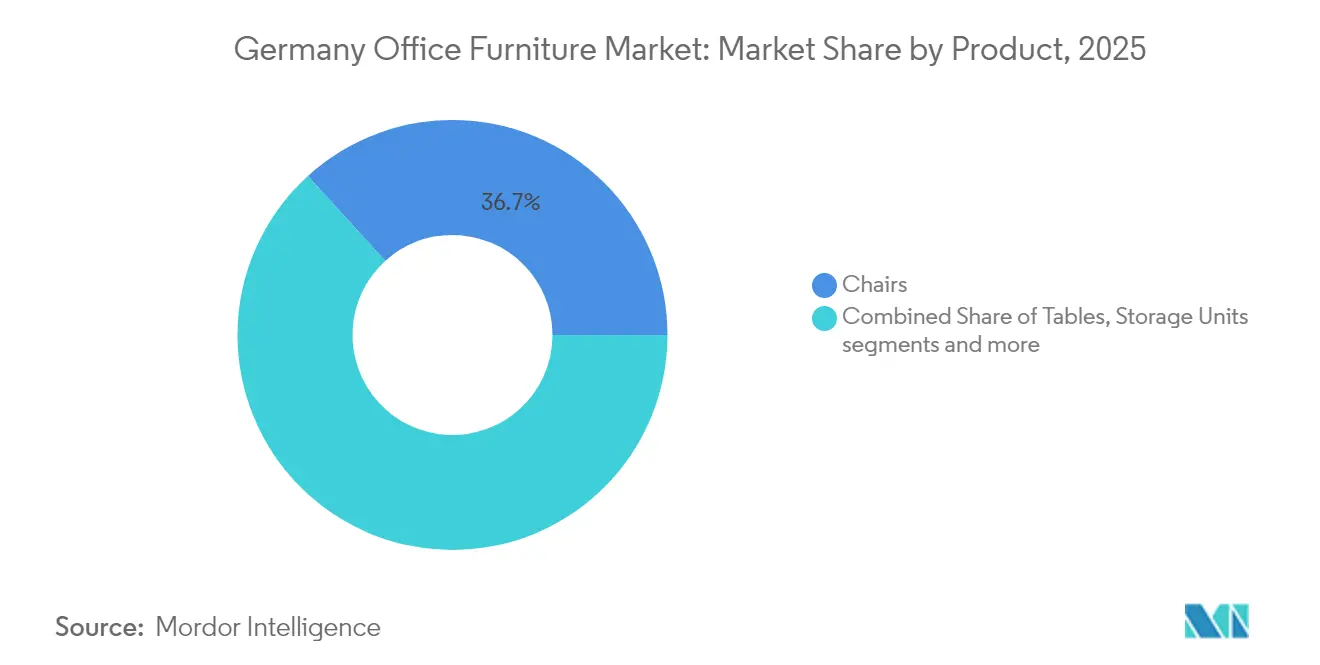

- By product category, chairs captured 36.74% revenue in 2025, while booths and office dividers are projected to register the fastest 3.69% CAGR through 2031.

- By material, wood represented 46.15% of total sales in 2025, but plastic and polymer materials will expand at a 3.59% CAGR to 2031.

- By price range, the mid-range segment controlled 58.22% revenue in 2025 and is set to grow at a 3.93% CAGR, outpacing both economy and premium tiers.

- By end-user, corporate offices commanded 42.31% of spending in 2025 and are forecast to advance at a 3.82% CAGR through 2031.

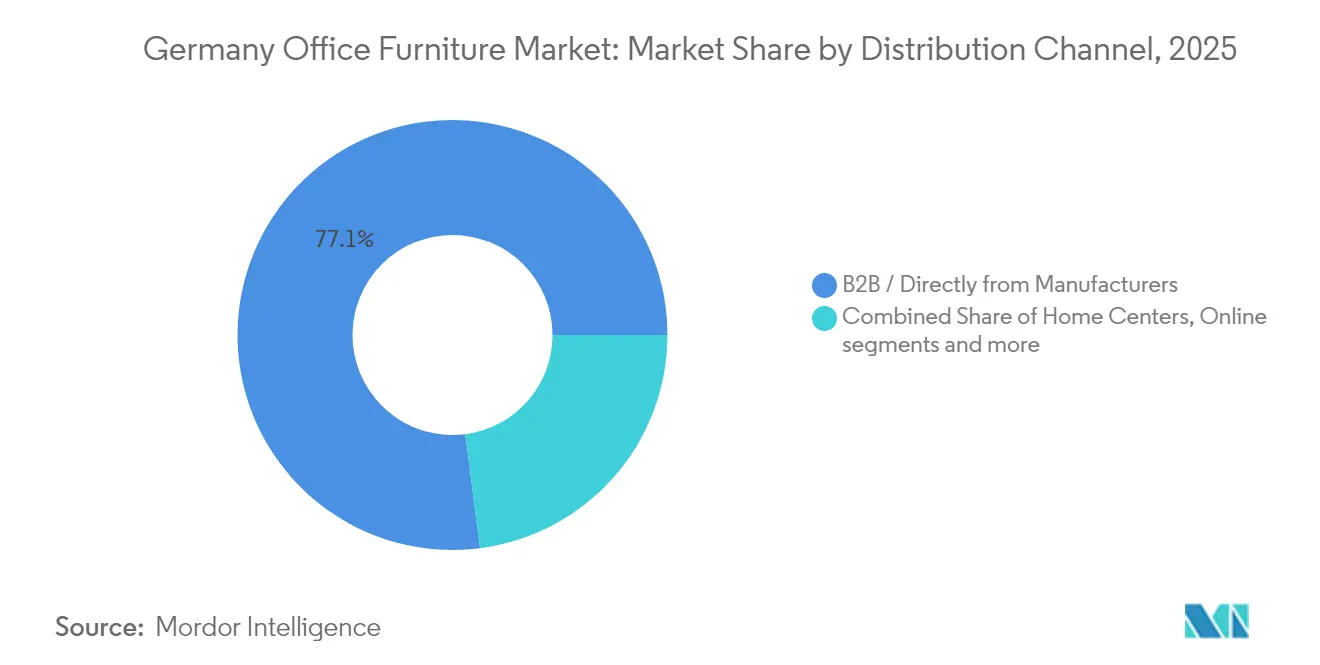

- By distribution channel, direct B2B sales from manufacturers constituted 77.05% of demand in 2025 and will rise at a 4.18% CAGR during the outlook period.

- By geography, Central Germany led with 25.11% value contribution in 2025, while Eastern Germany is set to record the fastest 3.44% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Office Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ergonomic & health-focused seating boom | +0.8% | Munich and Frankfurt tech corridors | Medium term (2-4 years) |

| Workspace redesign for hybrid models | +0.7% | Berlin, Hamburg, Düsseldorf | Short term (≤2 years) |

| Commercial construction in tech hubs | +0.5% | Munich Parkstadt Schwabing, Berlin Mitte, Frankfurt CBD | Long term (≥4 years) |

| Sustainable procurement incentives | +0.4% | Baden-Württemberg, North Rhine-Westphalia | Medium term (2-4 years) |

| DIN-driven demand for acoustic micro-pods | +0.3% | Corporate headquarters nationwide | Short term (≤2 years) |

| Circular-economy leasing models | +0.2% | Startup ecosystems in Berlin and Munich | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Ergonomic & Health-Focused Seating Boom

German employers now treat seating as a risk-mitigation and talent-retention tool rather than a commodity purchase. DIN EN 1335 compliance underpins specification lists, and brands such as Sedus embed life-cycle analyses in early design to prove low environmental impact. Meanwhile, innovators like Aeris market “active-sitting” chairs that exceed DIN requirements by encouraging micro-movement, a feature popular with wellness-oriented firms[2]“Standards vs. health: Why innovative office chairs beyond the DIN standard are so important,” Aeris, aeris.de. Corporate buyers also weigh return-to-office targets; providing comfortable, height-adjustable seating is viewed as a tangible incentive that makes on-site work more appealing. Because occupational-health statutes require suitable equipment, even cost-conscious companies continue to refresh chair fleets on predictable cycles, ensuring baseline demand stability within the Germany office furniture market.

Workspace Redesign for Hybrid Models

Office utilization has fallen to 40-50% of pre-pandemic norms, prompting facilities managers to slash dedicated desks and introduce flexible “activity-based” zones[3]Spotlight: Die Hybridarbeitswelt und ihre Konsequenzen für die Büromärkte,” Savills, savills.co.uk. Hot-desking ratios of 1:1.25 become viable when paired with modular furniture that employees can roll, stack, or fold within minutes, reducing wasted floor area and trimming rental costs by as much as USD 750 per workstation each year. Vendors able to ship coordinated suites—tables with locking casters, stackable storage, lounge modules with integrated power—win the new-build tenders. IoT-ready desks that feed occupancy data into smart-building dashboards also enter shortlists, signaling a blend of furniture and prop-tech that is reshaping procurement criteria across the Germany office furniture market.

Commercial Construction in Tech Hubs

Munich’s Parkstadt Schwabing, Berlin Mitte, and Frankfurt’s banking district continue to attract global headquarters and R&D centers, each new lease triggering turnkey fit-out projects that demand complete furniture packages. Architects on these schemes specify recycled materials, cradle-to-cradle certificates, and acoustic solutions capable of achieving DGNB Platinum ratings. Because tenant mixes skew toward software and life-science firms, requests often include hacking rooms, maker spaces, and project zones furnished with mobile whiteboards and sit-stand benches. Suppliers that master project-coordination—aligning delivery windows with tight construction schedules—secure repeat contracts in these high-growth clusters, reinforcing regional revenue streams for the Germany office furniture market.

Sustainable Procurement Incentives

Blue Angel labels and FSC or PEFC chain-of-custody proofs have become standard bid requirements. Clients weigh carbon data down to kilogram-per-seat level, and furniture-as-a-service offerings such as NORNORM’s subscription model resonate because they cut embodied emissions and free cash flow for core investments. Manufacturers with domestic supply chains gain credibility as low-transport contenders, while those lacking verifiable traceability risk exclusion from public tenders. As ESG disclosures tighten, circularity metrics like repairability and take-back rates now influence corporate purchasing just as strongly as styling or price, steering revenue toward brands that embrace closed-loop design within the Germany office furniture market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shrinking leased office footprints | -0.6% | Secondary business districts across Germany | Medium term (2-4 years) |

| Raw-material price volatility | -0.4% | Global sourcing hubs | Short term (≤2 years) |

| EU/German EPR compliance costs | -0.3% | Nationwide, with EU spill-over | Medium term (2-4 years) |

| Skilled upholsterer shortage | -0.2% | Highest in Eastern manufacturing clusters | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Shrinking Leased Office Footprints

Hybrid work cuts demand for rows of identical workstations and erodes order volumes tied to pure seat counts. While flagship downtown towers remain desirable, landlords in peripheral zones struggle with double-digit vacancy, and tenants opt for smaller, higher-quality suites. Furniture producers reliant on large-plateau projects, therefore, see bid lists shrink or fragment into phased-purchase tranches. Vendors who pivot toward leasing, refurbishment, or quick-turnaround retrofit packages cushion revenue shortfalls and continue to meet the evolving space needs of the Germany office furniture market.

Raw-Material Price Volatility

Oscillating prices for timber, metals, and engineered substrates complicate costing and quotation validity. Smaller workshops without hedging tools face margin compression, forcing them to raise list prices mid-year or accept lower profitability. To protect order pipelines, many now pre-quote alternate material specifications—offering solid beech, veneer, or recycled polymer options—so clients can adjust selections when spot prices spike. The turbulence accelerates R&D into bio-composites and post-consumer plastics, both viewed as buffers against commodity swings in the Germany office furniture market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Chairs Lead, Pods Accelerate

Chairs remain the cornerstone of the Germany office furniture market and hold 36.74% of total sales. Employers view ergonomically certified task seating as compulsory for compliance, and hot-desking pushes demand for models with intuitive adjustments that suit multiple users in a single day. Meeting and guest chairs experience renewal as companies convert static conference rooms into dynamic collaboration hubs outfitted with lightweight seating that can be rearranged at will.

A new center of gravity is emerging around acoustic booths and dividers, the fastest-growing niche at 3.69% CAGR. Open-plan offices and video meetings strain acoustics, driving interest in pods that temper noise and supply visual privacy. Brands like Mute-Labs package LED lighting, ventilation, and integrated power in turnkey modules, making pods a quick upgrade for landlords seeking to attract tenants without structural alterations. As work modes fragment, even small firms allocate budget for at least one phone booth to ensure distraction-free calls, reinforcing long-term momentum within the Germany office furniture market.

By Material: Wood Dominates, Plastics Rise

Wood furniture accounts for 46.15% of spending because German buyers equate natural surfaces with quality, and domestic forests supply certified inputs at scale. Vendors tout regional sourcing to lower transport emissions and emphasize repairability that extends product life. Oak and beech veneers remain mainstream, complemented by sustainable finishes free of formaldehyde and solvents.

Plastics and advanced polymers, however, post the quickest 3.59% CAGR. Manufacturers inject recycled content and color-through resins that reduce paint steps, thereby shrinking carbon footprints. Lightweight shells also lower shipping costs and simplify end-of-life separation for recycling. Composite hybrids—polymer skins over metal or wood cores—gain favor in chairs and pods where complex geometries enhance ergonomics or acoustics. This shift signals a gradual, innovation-led diversification of materials in the Germany office furniture market.

By Price Range: Mid-Range Strikes the Balance

Mid-range lines capture 58.22% of revenue because they deliver the sweet spot of robust engineering, DIN compliance, and competitive warranties at attainable price points. Procurement teams tasked with cost savings feel safe choosing brands that combine steel frames, melamine tops, and modest design flair. Bulk orders often bundle mid-range desks and storage with a select number of premium statement pieces for reception or executive areas.

Economy products serve startups and public agencies on tight budgets but face durability skepticism that limits large-enterprise uptake. Premium collections cater to law firms, consultancies, and tech unicorns where brand prestige justifies higher spend. Some premium demand now migrates into subscription models that offer high-spec items with lower upfront cash outlay, further blurring traditional tier boundaries inside the Germany office furniture market.

By End-User: Corporate Offices at the Core

Corporate offices generate 42.31% of overall demand because Germany hosts global automakers, banks, and software firms that constantly refresh work environments to attract talent. These buyers require synchronized installations across multiple floors or campuses and demand precise scheduling around move-in dates. Sustainability reporting has become a staple clause, compelling suppliers to deliver product passports and circularity metrics alongside CAD drawings.

Healthcare, education, and government place steady, specification-heavy orders that prioritize hygiene, robustness, and safety certifications. Growth in outpatient clinics and university research centers brings specialized needs such as antimicrobial surfaces and height-adjustable lab benches. Retail and hospitality back offices buy smaller volumes yet lean toward stylish, quick-ship collections that match front-of-house aesthetics. Each segment’s nuanced criteria enrich the solution landscape for the Germany office furniture market.

By Distribution Channel: B2B Direct Rules

Direct manufacturer relationships handle 77.05% of value because corporate clients need layout planning, customized finishes, and staged deliveries impossible to achieve through standard retail. Dealers integrated into these networks provide local measurement, installation, and service, ensuring that warranty terms are preserved. As a result, brands that invest in digital configurators and dealer training secure a higher share of wallet.

Retail remains relevant for SMEs and growing home-office demand, with showrooms allowing buyers to test ergonomics firsthand. Online platforms succeed at accessories and repeatable SKUs but rarely close six-figure fit-out contracts. Furniture-as-a-service operators occupy a middle ground, bundling products, logistics, and financing into subscriptions that lessen capex and appeal to agile companies—a model poised to expand within the Germany office furniture market.

Geography Analysis

Central Germany retains leadership thanks to Frankfurt’s finance cluster, where global banks fit out landmark towers with premium reception suites, executive boardrooms, and advanced trading-desk setups. Interior standards emphasize acoustic performance and secure cable management, pushing orders toward specialized suppliers able to integrate AV and compliance hardware seamlessly. The German office furniture market size attributable to Central Germany is reinforced by dense subcontractor networks that handle installation without cross-border logistics delays.

Eastern Germany delivers the fastest growth as Berlin’s startup ecosystem spawns co-working campuses and innovation labs needing modular, brand-worthy interiors. Medium-sized leases provide steady furniture orders spread across multiple project phases, allowing suppliers to refine agile manufacturing processes. Cities such as Leipzig and Dresden attract semiconductor and logistics investments, each new facility requiring administrative offices and training centers that expand regional demand within the German office furniture market.

Southern Germany benefits from Munich’s technology corridor and Stuttgart’s engineering excellence. Premium rents make space efficiency critical, so buyers favor compact sit-stand desks, stackable lounge modules, and integrated storage to maximize rentable area. Western Germany leverages dense population centers and an industrial heritage to sustain base-load demand, while Northern Germany’s Hamburg builds on media and maritime clusters and prefers coastal aesthetic finishes and recycled ocean plastics in furniture lines.

Competitive Landscape

Germany’s office furniture arena is best described as competitively balanced, with a handful of large industrial manufacturers sharing the stage with nimble specialists and strong retail chains. Retail consolidation—illustrated by XXXLutz absorbing Porta—has shifted bargaining power, yet many mid-sized producers counter by emphasizing design originality, bespoke finishes, and intimate dealer relationships that big-box operators cannot easily duplicate. Regional heritage brands also leverage “Made in Germany” cachet, which resonates with domestic buyers who value local employment and craftsmanship continuity.

Manufacturers increasingly differentiate on sustainability rather than pure aesthetics. Firms such as Sedus publish transparent supply-chain data and guarantee spare-part availability for over a decade, an assurance prized by facility managers aligning with circularity benchmarks. Acoustic-pod makers like Mute-Labs carve out profitable niches by coupling refined engineering with evidence-based productivity claims; their products appear in showrooms alongside classic desks and chairs, demonstrating how ancillary categories can evolve into primary purchase drivers. Meanwhile, component suppliers—hinge, glide, and lifting-column producers—shape downstream innovation by releasing lower-carbon alloys and smart actuators that enable sleek new furniture silhouettes.

The digital layer is the newest competitive frontier. Forward-looking brands equip desks with occupancy sensors and cloud dashboards, selling subscription software that reveals underused zones and guides space rightsizing. This advisory capability moves suppliers closer to consultancy territory, fostering long-term client intimacy and recurring revenue. Companies reluctant to embrace digitalization risk relegation to commodity status as the German office furniture market rewards holistic solutions that blend product, data, and service.

Germany Office Furniture Industry Leaders

Sedus

Steelcase Inc.

Haworth Inc.

MillerKnoll Inc.

König + Neurath AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Hettich Group reported solid turnover growth: Despite a macro-level sales dip in finished furniture, demand for precision hinges, drawer slides, and height-adjustable columns stayed robust. Hettich attributes performance to co-development projects that embed its fittings into new product families from leading desk and storage manufacturers.

- February 2025: Häfele Group confirmed record investments: The company broke ground on a combined logistics and office hub at Nagold Wolfsberg, designed to accelerate just-in-time deliveries and showcase a live “smart workplace” fitted exclusively with its own hardware. The site doubles as a demonstration lab, reinforcing Häfele’s evolution from component vendor to solution architect.

- January 2025: XXXLutz Group completed Porta Group acquisition: The deal folded roughly 140 showrooms into XXXLutz’s retail network, triggering a realignment of supplier agreements and sparking debate among mid-tier manufacturers about potential margin pressures. Industry observers expect the enlarged chain to wield greater influence over product assortments, thereby compelling producers to bolster branding or seek alternative distribution routes.

- January 2025: Porta Group acquired Möbel Letz GmbH: By adding the e-commerce specialist, Porta gains a well-established logistics backbone and an online catalog topping 30,000 SKUs. The integration broadens omnichannel reach, helping Porta hedge against foot-traffic volatility while offering suppliers a streamlined digital shelf for rapid product launches.

Germany Office Furniture Market Report Scope

Office furniture means any free-standing furnishing that does not require installation with parts. Examples are desks, chairs, file cabinets, tables, lounge seating, and computer desks. Germany Office Furniture Market is Segmented by Material (Wood, Metal, Plastic, and Other Materials), Product (Meeting Chairs, Lounge Chairs, Swivel Chairs, Office Tables, Storage Cabinets, and Desks), and Distribution Channel (Offline and Online). The Report Offers Market Sizes and Forecasts for the Germany Office Furniture Market in Value (USD) for all the Above Segments.

By Product

| Chairs | Employee Chairs |

| Meeting Chairs | |

| Guest Chairs | |

| Tables | Conference Tables |

| Desks | |

| Other Tables | |

| Storage Units | Filing Cabinets |

| Bookcases & Shelving | |

| Sofas / Soft Seating | |

| Booths & Office Dividers | |

| Other Office Furniture (Stools, Reception Furniture, Accessories, Others) |

By Material

| Wood |

| Metal |

| Plastic & Polymer |

| Other Materials |

By Price Range

| Economy |

| Mid-range |

| Premium |

By End-user

| Corporate Offices |

| Healthcare Offices |

| Educational Institutions |

| Government & Public Offices |

| Hospitality & Retail Back-office |

| Others |

By Distribution Channel

| B2C / Retail | Home Centers |

| Specialty Furniture Stores | |

| Online | |

| Other Distribution Channels | |

| B2B / Direct from Manufacturers |

By Geography

| Northern Germany |

| Western Germany |

| Central Germany |

| Eastern Germany |

| Southern Germany |

| By Product | Chairs | Employee Chairs |

| Meeting Chairs | ||

| Guest Chairs | ||

| Tables | Conference Tables | |

| Desks | ||

| Other Tables | ||

| Storage Units | Filing Cabinets | |

| Bookcases & Shelving | ||

| Sofas / Soft Seating | ||

| Booths & Office Dividers | ||

| Other Office Furniture (Stools, Reception Furniture, Accessories, Others) | ||

| By Material | Wood | |

| Metal | ||

| Plastic & Polymer | ||

| Other Materials | ||

| By Price Range | Economy | |

| Mid-range | ||

| Premium | ||

| By End-user | Corporate Offices | |

| Healthcare Offices | ||

| Educational Institutions | ||

| Government & Public Offices | ||

| Hospitality & Retail Back-office | ||

| Others | ||

| By Distribution Channel | B2C / Retail | Home Centers |

| Specialty Furniture Stores | ||

| Online | ||

| Other Distribution Channels | ||

| B2B / Direct from Manufacturers | ||

| By Geography | Northern Germany | |

| Western Germany | ||

| Central Germany | ||

| Eastern Germany | ||

| Southern Germany | ||

Key Questions Answered in the Report

What is the current value of the Germany office furniture market?

It stands at USD 3.04 billion in 2026 and should reach USD 3.43 billion by 2031.

Which product category dominates spending?

Ergonomic chairs lead, representing 36.74% of 2025 revenue thanks to DIN-driven compliance needs.

Which region is growing fastest?

Eastern Germany, anchored by Berlin’s tech sector, is projected to expand at 3.44% CAGR.

How are firms adapting to hybrid work?

They spec modular desks, mobile storage, and acoustic pods that let teams reconfigure layouts in real time.

Why is sustainability a key purchase driver?

Buyers increasingly demand FSC-certified wood, recycled plastics, and subscription models that cut CO? emissions by up to 70%.

Who controls distribution?

Direct B2B channels dominate because corporate clients need customized design, staged deliveries, and long-term service.

Page last updated on: