Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 20.13 Billion |

| Market Size (2026) | USD 20.82 Billion |

| Market Size (2031) | USD 24.16 Billion |

| Growth Rate (2026 - 2031) | 3.02% CAGR |

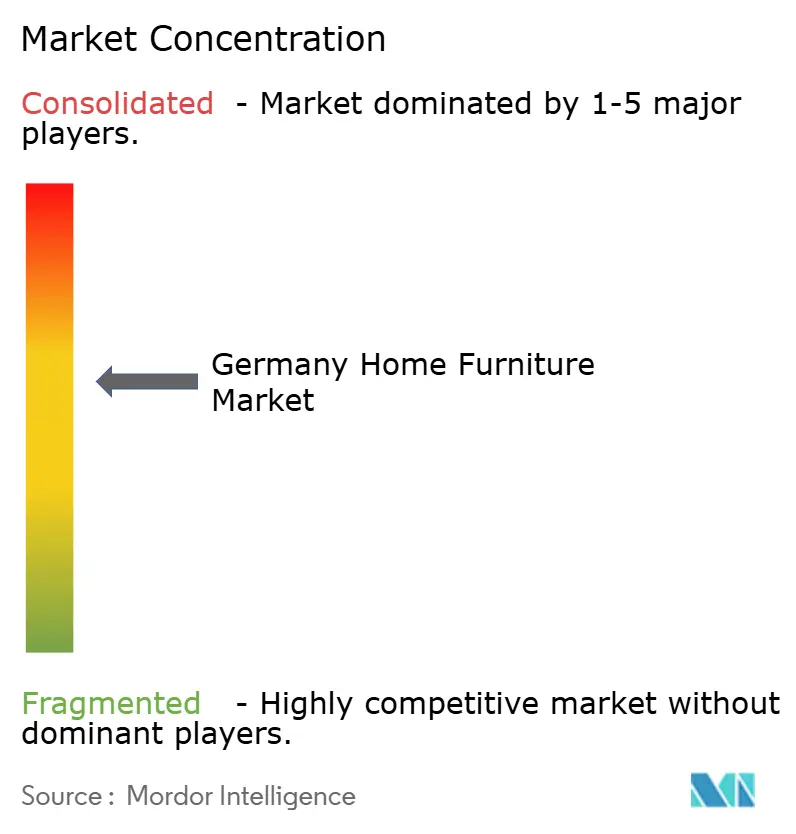

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Home Furniture Market Analysis by Mordor Intelligence

The Germany Home Furniture Market size is projected to be USD 20.13 billion in 2025, USD 20.82 billion in 2026, and reach USD 24.16 billion by 2031, growing at a CAGR of 3.02% from 2026 to 2031.

First-half 2025 sales fell 5.1% to USD 9.29 billion (EUR 7.9 billion) compared with H1 2024; however, the export ratio rose to 34.1%, as domestic channels softened, signaling a tactical mix shift toward external demand among manufacturers. Demand is being reshaped by hybrid work, renovation-led spending, and the need for space optimization in compact urban dwellings, while sustainability has become a deciding factor embedded in purchase decisions rather than a niche differentiator. Regulation provides a durable tailwind, with the EU Ecodesign for Sustainable Products Regulation now in force and a Digital Product Passport requirement scheduled by July 2026 that standardizes durability, repairability, and traceability expectations across the German home furniture market.

Key Report Takeaways

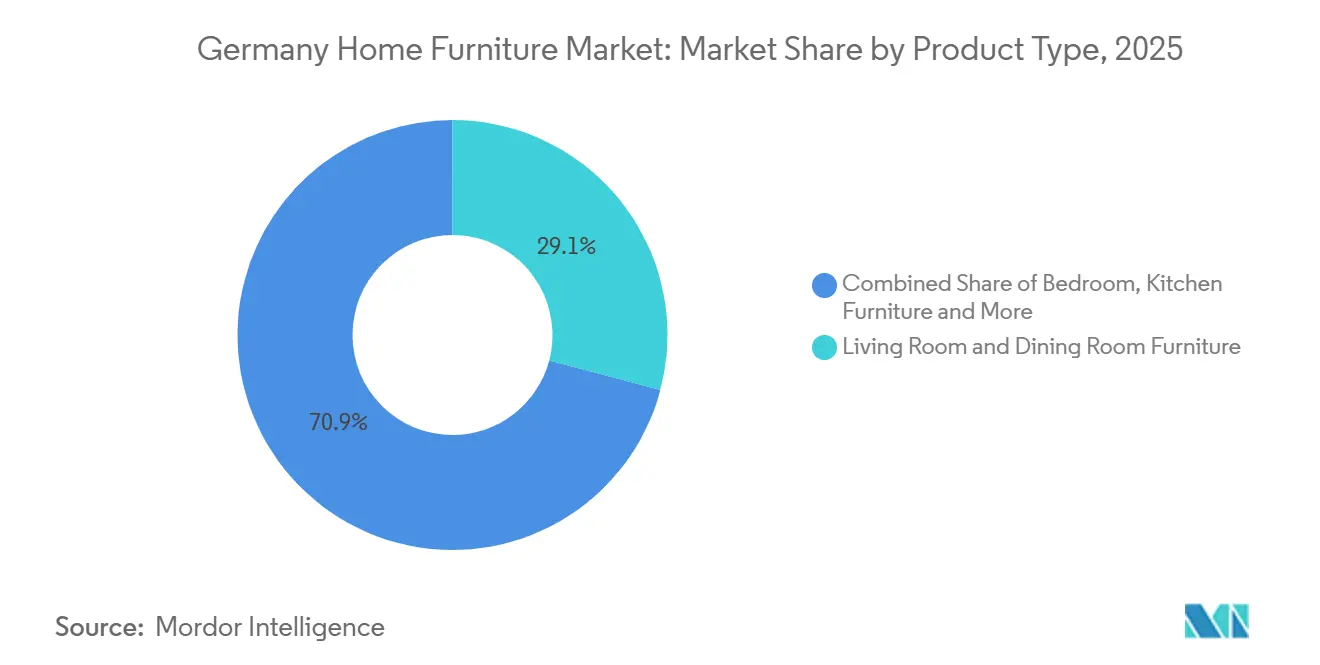

- By product type, living room and dining room furniture held 29.12% of the Germany home furniture market share in 2025, while kitchen furniture is forecast to expand at a 3.97% CAGR through 2031.

- By material, wood contributed 48.34% of the Germany home furniture market share in 2025, while plastic and polymer are set to rise at a 3.56% CAGR through 2031.

- By price range, the economy tier accounted for 54.83% of the Germany home furniture market share in 2025, while premium is projected to grow at a 3.84% CAGR through 2031.

- By distribution channel, specialty furniture stores captured 43.63% of the Germany home furniture market share in 2025, while online is anticipated to advance at a 4.75% CAGR through 2031.

- By geography, southern Germany held 38.21% of the Germany home furniture market share in 2025, while eastern Germany is expected to record the fastest growth at a 5.2% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Home Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Disposable Income Among German Households | +0.6% | Strongest in Western and Southern Germany, gradually extending to Eastern states | Medium term (2-4 years) |

| Eco-conscious Consumerism Driving Sustainable Wood Furniture Demand | +0.5% | Nationwide, led by major urban centers where FSC/PEFC labels are standard | Long term (≥ 4 years) |

| Boom in Home Renovation From Ageing Housing Stock | +0.6% | National impact, with early momentum in Southern metros and select Eastern cities | Medium term (2-4 years) |

| Demand for Multifunctional Space-saving Furniture in Urban Apartments | +0.4% | Concentrated in Berlin, Munich, and Hamburg due to smaller urban dwellings | Short term (≤ 2 years) |

| Surge in Remote Work Catalysing Home-office Furniture Sales | +0.8% | Nationwide, with highest spending in Berlin, Frankfurt, and Munich | Short term (≤ 2 years) |

| Digital Mass Customization via Online Configurators | +0.3% | National trend, strongest in modular kitchens and bespoke furniture | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Disposable Income Among German Households

Real income recovery supports upgrades that were deferred during the inflation spike in 2024, and it enables selective trade-up behavior in premium and custom categories across the Germany home furniture market. The mix of easing inflation and improving real wages reduces precautionary savings and releases pent-up replacement cycles in kitchens and living spaces that often run on 12 to 15-year timelines, supporting steady orders rather than one-off surges. Premium demand concentrates in Southern Germany, where affluent cohorts commission bespoke finishes and prioritize durability, a trend that contrasts with still-elevated price sensitivity among mass-market shoppers. Retailers and manufacturers that align assortments to value tiers while signaling provenance and quality capture this divergence without relying on heavy discounting that can erode brand equity in the Germany home furniture market. Portfolio strategies that straddle mid and premium price bands, supported by energy-efficient production upgrades and material traceability, allow companies to sustain margins as normalization unfolds[1]SCHUELLER.DE https://www.schueller.de/fileadmin/user_upload/Unternehmen/Nachhaltigkeit/Schueller_Nachhaltigkeitsbericht_2025_EN.pdf. .

Eco-conscious Consumerism Driving Sustainable Wood Furniture Demand

Sustainability signals have shifted from optional to essential, with high recognition of the Blue Angel eco-label and rising willingness to prefer certified timber that aligns with FSC (Forest Stewardship Council) and PEFC (Programme for the Endorsement of Forest Certification) expectations for responsible sourcing[2]BLAUER-ENGEL.DE https://www.blauer-engel.de/en/press/detail/germans-seek-orientation-when-making-environmentally-friendly-purchases. . Manufacturers translate these requirements into product development and marketing, highlighting low-emission materials, documentation of origin, and circular solutions such as take-back or refurbishment to strengthen the Germany home furniture market’s credibility. The regulatory path is clear, as the Ecodesign for Sustainable Products Regulation (ESPR) framework mandates design for durability, repairability, and recyclability, with a Digital Product Passport due by July 2026 that further codifies data-sharing and traceability across the value chain. Eco-labels and emissions standards work in tandem to move the market toward lower formaldehyde content and reduced VOCs, creating consistent expectations for indoor air quality and long-lived furniture in German homes. Companies that document compliance and invest in greener inputs are positioned to win share as these criteria become routine in category selection across the Germany home furniture market.

Boom in Home Renovation From Ageing Housing Stock

Renovation projects continue to outpace new-build activity and are visible in 2025 retail indicators that show stabilization in home improvement demand after a weak 2024, an environment that favors kitchen and bath upgrades, where functionality lifts daily utility[3]DIYSUMMIT.ORG https://diysummit.org/german-diy-and-home-improvement-recovery-early-2025/.. Limited housing permits combined with modest GDP improvement early in 2024 reinforce the pivot to upgrading existing dwellings rather than expanding new supply, a pattern that aligns with the sustained need for efficient layouts in German apartments. Kitchen systems benefit most in this cycle given their ticket size, role in energy and space efficiency, and integration with built-in appliances and storage that support multifunctional living. Suppliers that provide modular options, durable surfaces, and verified low-emission materials have an edge as consumers invest in solutions that endure and support resale value in tight urban markets. These features position the Germany home furniture market to benefit from planned projects, as households improve livability while meeting regulatory and environmental expectations that now define quality.

Surge in Remote Work Catalyzing Home-office Furniture Sales

Hybrid work has become structural in major metros and continues to support sustained demand for ergonomic seating, height-adjustable desks, and compact storage that fits smaller footprints common in German cities. The installed base from early pandemic purchases is now maturing into refresh cycles as buyers upgrade to longer-lasting surfaces, quieter mechanisms, and components with documented emissions performance. Companies that offer modular systems, spare parts availability, and repair options can capture repeat purchases from customers who favor responsible consumption patterns and require proof of longevity[4]VITRA.COM https://www.vitra.com/en-un/about-vitra/sustainability.. Digital planning tools and visualization features help resolve space constraints, and they shorten decision cycles when paired with white-glove delivery and assembly services that reduce friction in dense urban settings. The effect on the German home furniture market is an ongoing floor of demand for compact, ergonomic, and certifiably low-emission products that are compatible with hybrid work routines.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Wood and Raw-material Costs | -0.4% | National, with acute pressure in Bavaria and Baden-Württemberg, where wood-based production clusters dominate | Short term (≤ 2 years) |

| Global Supply-chain Disruptions and Freight Inflation | -0.3% | Nationwide exposure to import cost volatility, with a higher risk given the elevated import share in early 2025 | Medium term (2-4 years) |

| Shortage of Skilled Craftsmanship in the Premium Segment | -0.2% | National, most severe in the East Westphalia cluster in North Rhine-Westphalia | Long term (≥ 4 years) |

| Stringent VOC and Formaldehyde Emission Standards Raising Compliance Costs | -0.2% | EU-wide, with Germany as an early adopter and alignment to REACH by August 2026 | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Wood and Raw-material Costs

Wood input prices follow cyclical swings, and recent figures for wood and products of wood and cork show year-on-year increases that compress margins where pass-through is constrained by price sensitivity. The Germany home furniture market feels this pressure most in wood-heavy segments that rely on certified European hardwoods, since certification is non-negotiable for many buyers, and it adds cost that cannot be easily offset when inflation compresses discretionary budgets. Companies respond with material efficiency, lightweighting, and selective substitution of higher-cost resins or coatings where performance is maintained, and they tighten procurement to reduce waste and handling losses in the value chain. Emissions compliance adds further cost, especially with formaldehyde limits tightening in line with REACH Annex XVII, which raises testing and certification workloads for panels and upholstered components. Over time, producers that invest in compliant chemistries and process control can better stabilize costs, but the near-term drag is visible across supply-constrained categories in the Germany home furniture market.

Global Supply-chain Disruptions and Freight Inflation

Elevated import dependence during early 2025 raised sensitivity to freight rate moves and timing mismatches that complicate just-in-time inventory strategies at retailers. When container costs and port delays increase, landed cost inflation and longer lead times squeeze promotions, strain working capital, and force compromises on breadth or depth of assortments. Retailers investing in last-mile logistics, EV-enabled depot operations, and automation are better positioned to cushion volatility and maintain service levels that improve conversion in high-consideration categories. Domestic producers with regional supplier networks and transparent traceability gain resilience from shorter flows and more predictable lead times, a factor that strengthens their position in the Germany home furniture market during periods of global disruption. These offsets reduce, but do not eliminate, the medium-term drag on growth from shipping cost volatility and logistics bottlenecks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Kitchen Furniture Ascends While Living Room Dominates

Living room and dining room furniture held a 29.12% share in 2025, while kitchen furniture is the fastest-growing product category with a 3.97% CAGR projected through 2031, indicating a continued shift toward layout optimization during renovations across the Germany home furniture market. Market structure also supports kitchen leadership, since only a small share of the nearly 1,000 sector companies manufacture kitchen systems, enabling specialization and premium pricing where certifications and climate-neutral production are verifiable differentiators. These conditions reinforce a steady upgrade cadence that keeps kitchen demand above broader traffic trends in the Germany home furniture market.

Kitchen producers use quality signaling and process investments to protect margins, which is important as input costs and compliance timelines tighten. Schüller Möbelwerk manufactures about 170,000 fitted kitchens annually and pairs mid-market and premium lines to address distinct buyer needs, while operational improvements like energy-efficient compressors reduce electricity consumption to bolster resilience during cost spikes. Office furniture softened in H1 2025 as corporate fit-outs slowed, but hybrid work continues to support the home-office segment with ergonomic and compact solutions that optimize limited space. The Germany home furniture market share lead for Living Room and Dining Room remains intact, and the Germany home furniture market size for Kitchen furniture is on a firmer multi-year trajectory due to the renovation lens and durable value-per-use case among owners.

By Material Type: Wood Heritage Meets Polymer Innovation

Wood-based products contributed 48.34% of category revenue in 2025, maintaining the lead on material choice, while plastic and polymer products are projected to post a 3.56% CAGR through 2031 as manufacturers leverage recycling and bio-based input strategies. The Germany home furniture market retains a strong wood heritage supported by certified forestry, with PEFC and FSC labels serving as baseline trust markers for consumers and trade partners. Producers mitigate input volatility through greater material efficiency and modular design, and they integrate emissions testing regimes to ensure compliance with evolving formaldehyde limits and VOC thresholds. Blue Angel criteria complement these requirements, and recognition of the eco-label underpins mainstream acceptance of sustainable materials in finished goods. These conditions guide material selection where endurance, indoor air quality, and recyclability are increasingly non-negotiable in the Germany home furniture market.

On the polymer side, circular inputs and durable performance allow designers to meet emissions goals and cost targets without compromising use-life. Producer price movements for wood and derived products show recent year-on-year increases, reminding industry buyers that diversified material strategies are necessary to stabilize landed costs. Standards alignment under REACH and the ESPR framework increases transparency on inputs and expected durability, providing a clearer compliance roadmap for procurement teams in mid-sized and larger enterprises. Upholstery and surface finishes also move toward certified low-emission solutions with spare parts policies that extend product life, which enhances both brand value and customer retention in a fragmented field. In this context, the Germany home furniture market share lead for wood reflects authentic consumer preference and certified supply, while the Germany home furniture market size growth in polymers reflects practical advances in circular design and compliance-driven innovation.

By Price Range: Economy Dominates Yet Premium Grows Faster

The Economy price tier accounted for 54.83% of sales in 2025, underscoring the persistence of value-driven shopping, while premium is projected to grow at a 3.84% CAGR through 2031 as affluent buyers prioritize longevity and provenance in the Germany home furniture market. The mix reflects uneven recovery across household cohorts, with Southern states showing a stronger appetite for bespoke solutions and craftsmanship where brand narratives emphasize durability and verified sourcing. Retailers adapt by calibrating private labels and promotions around entry-level price points while preserving premium displays that highlight material quality and design heritage for higher-income shoppers. Companies that maintain service levels for delivery, assembly, and post-sale support improve conversion without steep discounting, a tactic that helps sustain mid-market margins even when consumer confidence is uneven. These tactics align with the Germany home furniture market’s dual-speed dynamics and enable stable category performance despite pockets of price sensitivity.

Premium dynamics benefit from credentials that are difficult to replicate, such as design collaborations, circular take-back programs, and long-term spare parts availability that extend product life. Energy-efficient production and logistics upgrades provide cost relief and support corporate sustainability goals, which are increasingly visible to customers and contract buyers in full-lifecycle assessments. Specialty stores can stage these narratives with tactile demonstrations, while online marketplaces leverage visualization and service integration to reduce friction for bigger-ticket orders. As growth normalizes, price-tier positioning and verified sustainability will be key to retaining loyalty and repeat purchase in the Germany home furniture market. The Germany home furniture market share lead of the Economy tier is clear, and the Germany home furniture market size expansion led by premium will continue to rely on craftsmanship and proof of durability.

By Distribution Channel: Specialty Stores Lead While Online Accelerates

Specialty furniture stores held a 43.63% share in 2025, affirming the value of in-store consultation and touch, while online is projected to record the fastest growth at a 4.75% CAGR through 2031 as augmented reality (AR) and 3D planning become mainstream across the Germany home furniture market. The channel mix reflects a durable need for experience-led selling in complex categories like kitchen and upholstered, balanced by digital tools that shorten the path from inspiration to purchase. Retailers with omnichannel integration, including delivery and assembly services, continue to gain traction as they simplify last-mile execution for bulky items. Home improvement chains show signs of recovery in early 2025 that support DIY furniture and self-assembly categories as renovation activity stabilizes from the 2024 low. These blended approaches build share in a fragmented market by meeting buyers where they want to browse and transact in the Germany home furniture market.

Digital configurators and visualization tools add momentum to online growth by reducing uncertainty on fit and finish, and they enable manageable customization without the complexity of fully bespoke projects. Large-format retailers complement this with showroom experiences that let customers test comfort and materials before finalizing online or in-app, blending the best of both environments. Logistics investments in automation, storage density, and route electrification enhance reliability and sustainability, which boosts customer satisfaction and reduces returns for higher-value orders. Over time, the balance will favor an omnichannel default, with specialty-led selling supported by online planning and fulfillment that fits modern shopping behavior in the Germany home furniture market. The Germany home furniture market share edge for specialty stores is intact, and the Germany home furniture market size growth advantage for online will remain tied to smooth planning and last-mile services.

Geography Analysis

Southern Germany accounted for 38.21% of the market value in 2025 and is projected to grow further, leveraging affluent bases around Munich and Stuttgart, as well as a dense supplier network that enables reliable fulfillment in the Germany home furniture market. The region’s focus on high-quality manufacturing and design helps it maintain pricing power even when broader demand is uneven, with kitchen and bathroom upgrades remaining attractive anchor projects in renovation cycles. Category leaders emphasize verified sourcing and long-life designs supported by repair and spare parts commitments, which align with EU-wide expectations for traceability and durability. Tourism inflows and corporate spending around trade fairs also support premium retail traffic and contract opportunities in the region, reinforcing its weight within the Germany home furniture market. These attributes sustain Southern Germany’s lead and contribute to steadier order books among mid-sized and premium-focused companies.

Eastern Germany is projected to grow at a 5.2% CAGR through 2031, the fastest rate among regions, as rising disposable income and EU-supported refurbishment programs lift residential upgrades and unlock replacement demand in previously underinvested stock. Retail expansion into secondary cities demonstrates confidence in demand convergence, supported by improving logistics links to Polish suppliers and distribution hubs. The region’s price sensitivity tends to skew toward economy and mid-range, yet above-average growth suggests multi-year normalization that benefits value-focused assortments with credible sustainability credentials. Supply chains that integrate cross-border routes with automated consolidation points can serve the region efficiently while maintaining delivery standards for bulkier goods. These patterns strengthen the case for omnichannel coverage and localized services in a region with the highest growth prospects within the Germany home furniture market.

Western and Northern Germany display mixed conditions shaped by mature retail footprints and dense urban centers that favor space-efficient designs and digital planning tools. North Rhine-Westphalia’s furniture cluster benefits from vocational investments such as the Furniture Industry Training Factory in Löhne, which expands the pipeline of skilled labor that premium producers rely on. Northern Germany gains from e-commerce infrastructure anchored by the Otto Group, including headquarters expansion, robotics pilots at logistics centers, and depot electrification initiatives that improve reliability and lower emissions. Berlin and Hamburg remain centers for design and planning services that specify home and contract furniture, and they amplify online discovery when paired with high-quality last-mile execution. Collectively, these dynamics support steady contributions from Western and Northern Germany to the Germany home furniture market while Southern and Eastern regions set the pace on share and growth.

Regulatory Landscape

The Germany home furniture market operates under a predominantly EU-led compliance framework covering product safety, chemicals, and sustainability. Since 13 December 2024, the EU General Product Safety Regulation (GPSR) has applied to non-harmonised consumer products, reducing reliance on Germany's Product Safety Act (ProdSG) where GPSR directly governs. Chemicals restrictions and indoor air quality requirements remain central for furniture placed on the market, with formaldehyde and VOC compliance commonly handled through REACH-aligned testing and documentation.

Sustainability and traceability obligations intensify through late 2026. Commission Regulation (EU) 2023/1464 applies a formaldehyde release limit of 0.062 mg/m3 for furniture and wood-based articles from 6 August 2026, increasing the importance of panel, coating, and upholstery material selection and verification. For wood-based furniture, the EU Deforestation Regulation (EUDR) requires due diligence for medium and large operators from 30 December 2026 (with later timing for many micro and small operators), pushing importers and manufacturers to implement chain-of-custody data systems alongside supplier onboarding and risk screening. Product Contact Points in Germany, including the BLE Product Contact Point, provide guidance on applicable technical rules for products that are not fully harmonised at EU level.

Value Chain Analysis

The value chain spans raw materials and components (wood-based panels, certified timber, metal fittings, upholstery foams, adhesives and coatings) through manufacturing (case goods, upholstered, and fitted kitchens), then wholesale and retail distribution across specialty furniture stores, large-format retailers, home centers, and online platforms offering delivery and assembly services. The industry ecosystem is supported by sector bodies such as the Verband der Deutschen Moebelindustrie (VDM) and the Deutsche Guetegemeinschaft Moebel (DGM), which issues RAL quality certification across a large member base, reinforcing product quality, testing routines, and buyer confidence.

Cross-border sourcing and logistics are increasingly structural in Germany, with import dependence described as rising from roughly 55% (2018) to nearly 68% by 2025, and key supplying countries including Poland, China, and the Czech Republic. Landed cost, lead times, and compliance documentation (materials disclosures, emissions testing, and emerging traceability requirements) become key control points for retailers and manufacturers. Downstream, service-heavy fulfillment for bulky goods (two-person delivery, returns handling, and assembly) has become a differentiator, while the shift toward Ecodesign-driven durability and data readiness increases the importance of supplier integration, SKU-level material transparency, and standardized product information flows across brands and marketplaces.

Competitive Landscape

Competitive intensity remains high, with a broad base of producers and retailers competing across price tiers and channels in the Germany home furniture market. Industry employment among larger enterprises remains sizable despite a challenging 2024, and fragmentation is most visible in the mid-market, where many companies operate at limited scale. Scale advantages in logistics, procurement, and omnichannel execution are reshaping retail after a year of consolidation moves that brought larger showroom networks under unified operations. These assets help national chains expand services like 3D visualization, AR-enabled home planning, and coordinated delivery and assembly, which are now embedded in the customer journey for higher-value categories. The result is a more demanding operating environment where brand trust and fulfillment quality drive differentiation across the Germany home furniture market.

Premium manufacturers lean on design collaborations, circular programs, and parts availability to reinforce longevity and value retention for customers in both residential and contract use. Kitchen leaders maintain dual-brand strategies to address mid and premium buyers while investing in energy efficiency and logistics that reduce operating costs and emissions profiles. Retail marketplaces add marketplace breadth while improving assembly and connection services that remove friction in categories that have traditionally required in-store visits. The Germany home furniture market rewards players that pair transparent sustainability practices with convenience and reliable service, and this alignment is now a baseline expectation for retaining share in core categories.

Strategic moves in 2024 and 2025 centered on footprint optimization, digital planning features, and logistics modernization. Examples include showroom network consolidation at large-format chains, logistics automation rollouts to speed picking and reduce handling strain, and investments in EV charging capacity that improve route efficiency and reduce operating emissions. Brands also invested in training and skills development to address workforce shortages in precision joinery and upholstery, reinforcing the transfer of artisanal know-how to the next generation. These steps help stabilize operations while differentiating customer experience, which is essential for sustained performance in the Germany home furniture market.

Germany Home Furniture Industry Leaders

IKEA Germany

XXX Lutz

Höffner

Roller

Poco

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Circularity and compliance-readiness create immediate whitespace for manufacturers and retailers that can document materials, durability, and repair options in a scalable way. Germany's Circular Economy Act (KrWG) supports a policy environment that favors reuse and waste prevention, while the EU Ecodesign for Sustainable Products Regulation (ESPR) has moved furniture up the agenda for delegated acts following the Commission's 2025-2030 working plan. As Digital Product Passport requirements approach, opportunities concentrate around data services and operating models that translate compliance into shopper-facing proof (traceable wood sourcing, low-emission claims, spare parts availability, and refurbishment or take-back programs) across both specialty and online channels.

Operational investment and format innovation also point to where capacity and capability are being built. Rotpunkt completed a EUR 50 million growth package including a 10,000 sq m warehousing and logistics facility at its Bunde headquarters, reflecting a push toward automation and production flexibility aligned with kitchen-oriented demand tied to renovation cycles. Februe expanded commercial coverage and flagged equipment investments at its Herford site, while other firms have pursued energy-efficient facility upgrades, reflecting continued focus on productivity, service levels, and cost control under tighter materials and emissions constraints. These moves support opportunities in modular kitchens, space-optimized home-office solutions, and omnichannel delivery-and-assembly propositions, particularly where providers can combine configuration tools with reliable lead times and verified sustainability credentials.

Recent Industry Developments

- July 2026: The European Commission opened a formal investigation into potential gun-jumping linked to XXXLutz's acquisition of the Porta Group. The action raises the compliance bar for large-scale retail consolidation in Germany, increasing the need for transaction planning that addresses standstill obligations and integration sequencing.

- June 2026: IKEA opened a new compact-format store in Ingolstadt (about 2,950 sq m), expanding access to planning-led shopping in a smaller footprint. The move underscores continued experimentation with format diversification and service-forward retail to complement large-box stores and online ordering.

- October 2025: Ingka Group (IKEA) acquired Locus, an AI-powered logistics software company, to strengthen home delivery operations across its markets, including Germany. The acquisition supports optimization of routing and fulfillment capacity, which is increasingly decisive for bulky home furniture where delivery quality and cost-to-serve drive conversion and loyalty.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Germany home furniture market covers the value of furniture bought for residential use in Germany, including items sold through physical retail and online channels, and priced at the point of sale.

Scope exclusions: Items mainly bought for non-residential use, along with installation-only services and home decor that is not furniture, are not counted in this market size.

Segmentation Overview

- By Product

- Living Room & Dining Room Furniture

- Bedroom Furniture

- Kitchen Furniture

- Home Office Furniture

- Bathroom Furniture

- Outdoor Furniture

- Other Furniture

- By Material

- Wood

- Metal

- Plastic & Polymer

- Others

- By Price Range

- Economy

- Mid-Range

- Premium

- By Distribution Channel

- Home Centers

- Specialty Furniture Stores

- Online

- Other Distribution Channels

- By Geography

- Northern Germany

- Southern Germany

- Western Germany

- Eastern Germany

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts by building a clean view of household demand signals and supply flows that are visible in public data. We reviewed sources such as Destatis household expenditure and retail series, Eurostat consumption categories for furniture, and German trade and production statistics where available. Trade flows were also checked using international customs datasets like UN Comtrade to understand import reliance and price movements over time.

To keep the model grounded in what is sold and how it is sold, we also used channel and company disclosures such as annual reports, investor presentations, and reputable business press coverage of store networks and online growth. Where needed, paid subscriptions for company financials and intelligence, along with shipment-level import and export records and patent databases, were used to validate product and pricing direction. The sources mentioned are illustrative, and we also used other public documents and data tables for cross-checking and clarification where discrepancies appeared.

Primary Interviews and Surveys

Primary work was used to confirm what secondary data cannot show clearly in Germany, mainly pricing bands, channel mix, and how often furniture replacement cycles translate into purchases. We spoke with a mix of manufacturers, distributors, retailers, and online-led sellers across Germany so assumptions could be tested against current buying patterns and promotional behavior.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 13% | |

| Mid tier: 61% | Functional/Unit leaders: 31% | |

| Smaller Players: 14% | Managers: 56% |

Market-Sizing & Forecasting

Market sizing is built using a top-down approach where household demand is reconstructed from consumption and retail signals, and then adjusted using trade and production indicators to stay aligned with what is actually available and sold in Germany. After that, selective bottom-up checks are used to keep totals realistic, such as sampled average selling price by category multiplied by estimated unit volumes, along with channel checks for online versus store-based sales.

Key inputs that shaped the model include household consumption on furniture, housing turnover and renovation activity, online furniture penetration, import share and unit values for common furniture groupings, and observed price-range shifts between economy, mid-range, and premium. When specific category gaps appear, they are handled using ratios from interviewed experts and cross-validated against public retail and trade direction, before totals are rolled back up.

Forecasts rely mainly on scenario analysis supported by smoothing of historical demand indicators, because furniture spending reacts quickly to housing activity, consumer confidence, and price inflation. The forward view is then stress-tested with interview feedback on promotional intensity, lead times, and expected mix shifts toward home office and space-saving items.

Data Validation & Update Cycle

Outputs are validated through multiple checks so results do not depend on one data stream. We compare the modeled total with independent signals like household spending direction, import value trends, and channel expansion or contraction, and then investigate any unusual swings before sign-off.

The final numbers pass through step-by-step analyst review, where assumptions are rechecked and any large variances trigger follow-up outreach to confirm what changed in the market. Reports are refreshed annually, with interim updates when material events occur that can alter demand, pricing, or supply availability. Before delivery, a fresh review pass is completed so clients receive the most current view.

Mordor Intelligence's Germany Home Furniture Market Size Versus Other Published Estimates

Published market values for Germany home furniture often differ because the boundary can shift between consumer spending, retail sales, and broader furniture categories, and because price and channel assumptions are not always handled in the same way. The table below shows how scope choices and timing of price updates can move the final number even when the same country is being discussed.

The table points to a spread that is largely explained by what gets counted as home furniture and how it is valued. In Mordor Intelligence's model, only residential furniture sold through defined retail and online channels is counted, and adjacent categories like broader furnishings and floor coverings are left out, which can keep the value lower than consumer-expenditure based totals that bundle those items together.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 20.13 B (2025) | |

| Industry Data Platform A | USD 41.06 B (2025) | Often aligned to household consumption groupings that can include furnishings and related items beyond furniture, and values may be reported in EUR then converted at a different average exchange rate. |

| Trade Journal B | USD 17.87 B (2024) | Typically tracks manufacturer industry revenue for larger registered producers, which can undercount retail margins, smaller firms, and some imported finished goods sold through retail and online channels. |

Reading across the table, one estimate looks closer to consumer-demand value and another looks closer to producer revenue, so it is expected that the totals sit apart. By tying the size to a clear residential furniture scope and then checking it against trade, pricing, and channel signals, the market value stays traceable to repeatable steps and practical inputs.

Key Questions Answered in the Report

What is the current Germany home furniture market size and growth outlook to 2031?

The Germany home furniture market size is USD 20.82 billion in 2026 and is forecast to reach USD 24.16 billion by 2031 at a 3.02% CAGR, supported by renovation activity, hybrid work needs, and sustainability-led purchasing.

Which product categories lead in share and growth in Germany?

Living Room and Dining Room furniture lead with 29.12% share in 2025, while Kitchen furniture is the fastest-growing category at a 3.97% CAGR to 2031 due to renovation cycles and space optimization priorities.

Which distribution channel performs best and how fast is online growing?

Specialty Furniture Stores lead with a 43.63% share as in-store consultation remains decisive, while online is the fastest-growing channel at a projected 4.75% CAGR through 2031, with AR and 3D configurators improving conversion.

Which regions contribute most to demand, and where is growth strongest?

Southern Germany holds the largest share at 38.21% in 2025 and maintains steady growth, while Eastern Germany shows the fastest trajectory at a projected 5.2% CAGR as disposable incomes and refurbishment programs lift demand.

Page last updated on: