Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

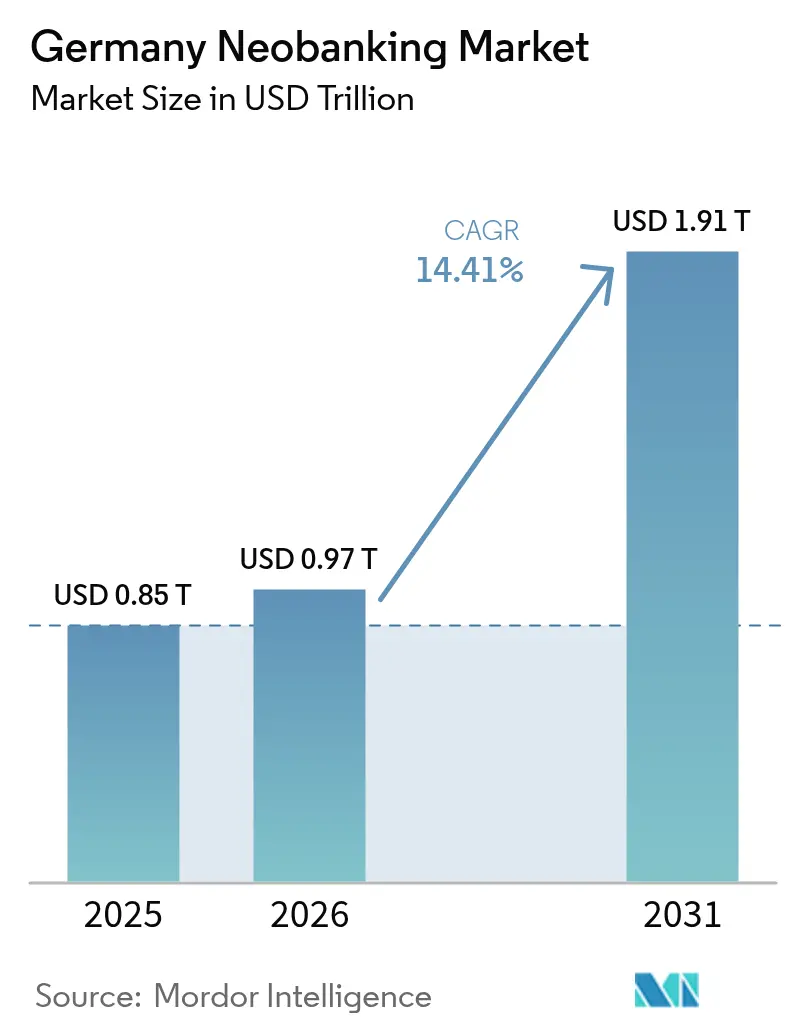

| Base Year Market Size (2025) | USD 0.85 Trillion |

| Market Size (2026) | USD 0.97 Trillion |

| Market Size (2031) | USD 1.91 Trillion |

| Growth Rate (2026 - 2031) | 14.41% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Neobanking Market Analysis by Mordor Intelligence

The Germany neobanking market size was valued at USD 0.85 trillion in 2025 and estimated to grow from USD 0.97 trillion in 2026 to reach USD 1.91 trillion by 2031, at a CAGR of 14.41% during the forecast period (2026-2031). Smartphone penetration above 85%, the maturing Payment Services Directive 2 (PSD2) framework, and BaFin’s adaptive supervisory stance together stimulate early-stage and established players to introduce mobile-first savings, lending, and cross-border payment solutions at scale. Germany’s export-oriented small and medium enterprises increasingly demand real-time, low-cost international settlement services that traditional banks deliver slowly, giving neobanks a structural advantage. Moreover, cash usage fell from 74% to 58% of point-of-sale transactions between 2020 and 2024, signaling a durable behavioral shift toward digital payments that further expands the Germany neobanking market[1]East Germany is expected to advance at an 11.27% CAGR as improved digital infrastructure and startup activity unlock previously underserved populations.. Finally, embedded-finance partnerships with software-as-a-service (SaaS) providers open new fee streams just as interchange caps compress revenue in payment processing.

Key Report Takeaways

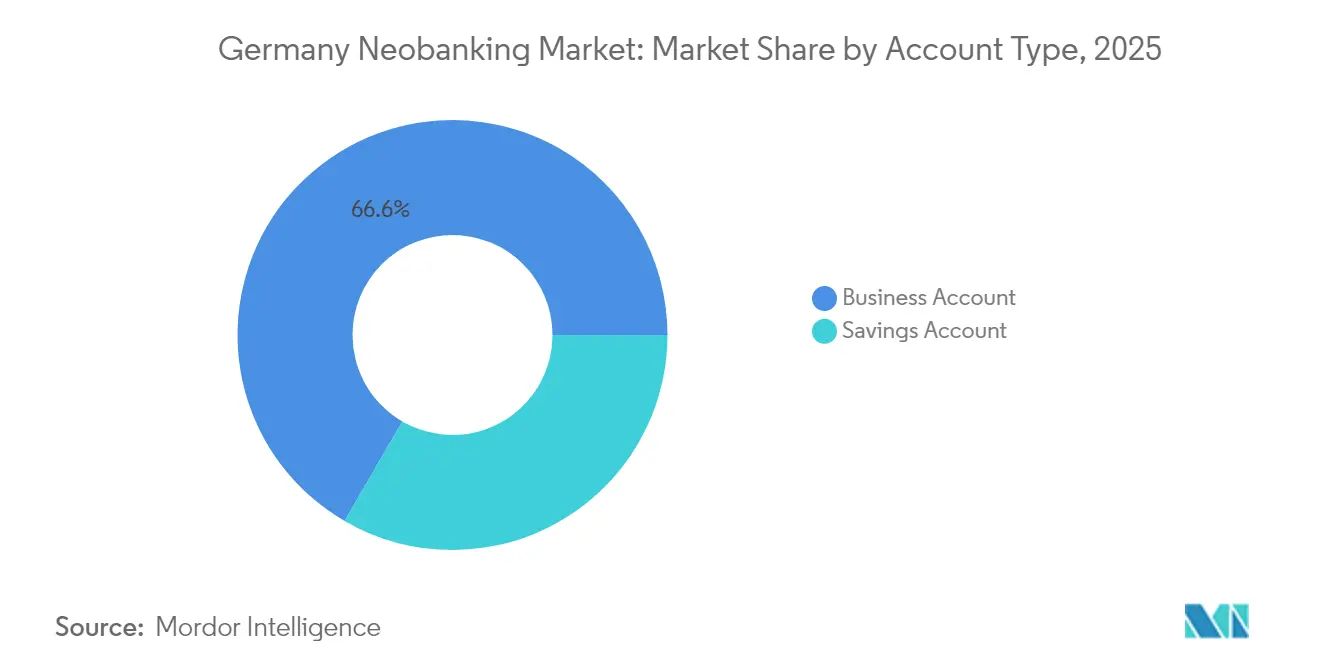

- By account type, business accounts led with a 66.63% share of the Germany neobanking market revenue in 2025; savings accounts are forecast to expand at a 33.82% CAGR through 2031.

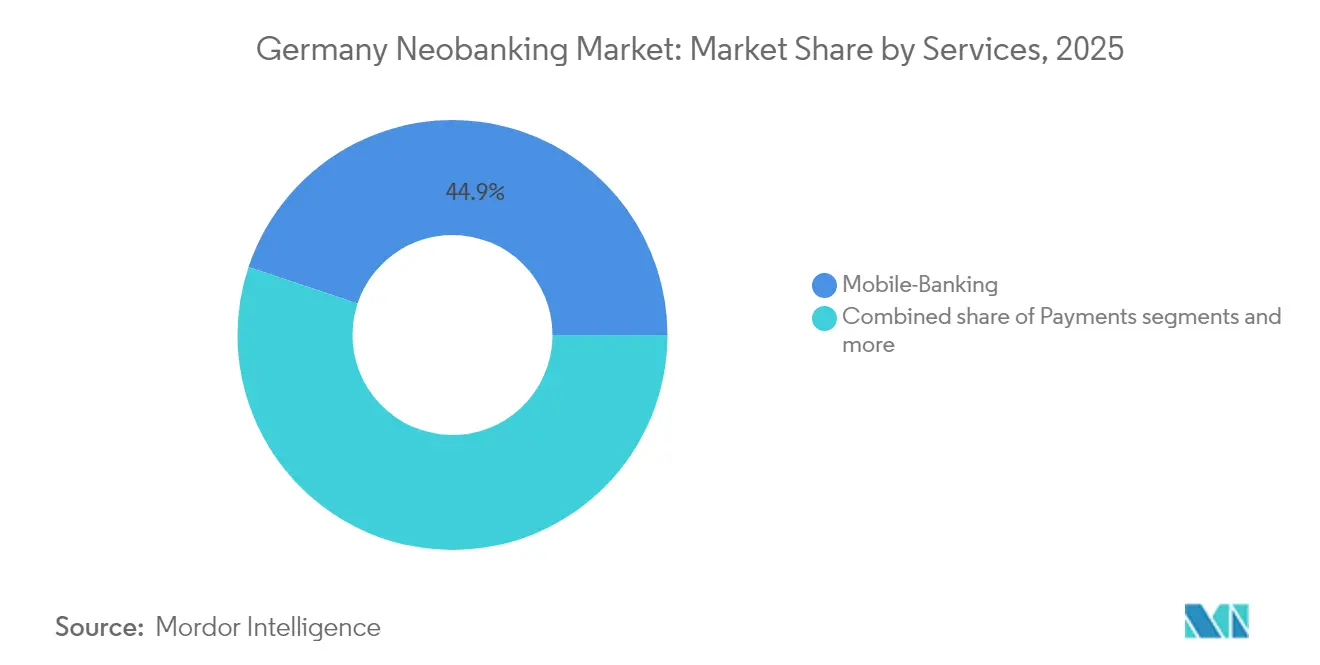

- By services, mobile banking held 44.88% of the Germany neobanking market share in 2025, while loans are projected to accelerate at a 37.28% CAGR through 2031.

- By application, enterprise solutions accounted for 62.15% of the Germany neobanking market size in 2025, and personal banking applications are poised to grow at a 30.94% CAGR through 2031.

- By geography, South Germany contributed 26.12% of 2025 revenue, whereas East Germany is expected to register the fastest 10.98% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Neobanking Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High smartphone & internet penetration | +2.3% | National, with urban concentration in Berlin, Munich, Hamburg | Short term (≤ 2 years) |

| PSD2/Open-Banking regulation support | +3.1% | EU-wide, with German implementation advantages | Medium term (2-4 years) |

| Incumbent–neobank partnership momentum | +2.8% | National, concentrated in financial centers | Medium term (2-4 years) |

| Export-oriented SME cross-border payment demand | +1.9% | National, with strength in industrial regions | Long term (≥ 4 years) |

| Embedded-finance demand from B2B SaaS platforms | +2.4% | Global, with German SaaS hub concentration | Long term (≥ 4 years) |

| Gen-Z preference for ESG-aligned banking | +1.8% | National, with urban demographic concentration | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Smartphone & Internet Penetration Accelerates Mobile-First Adoption

More than 85% of German residents own a smartphone, creating a vast addressable base for mobile-centric banking services. Pandemic-driven shifts pushed contactless payments into daily routines, compressing nearly a decade of adoption into two years. The rapid expansion of 5G coverage and intuitive app design reduces friction for older users and encourages household-level switching to digital-only providers. As younger consumers influence family financial decisions, viral network effects amplify account openings in the Germany neobanking market. Telecom operators’ joint venture to extend rural 5G coverage by 2027 further widens the potential customer pool.

PSD2/Open-Banking Regulation Creates Data-Driven Competitive Moats

PSD2 legally obliges incumbents to share account data with licensed third parties, allowing neobanks to generate unified customer profiles and superior risk analytics. German regulators require strict consent tracking and encryption, so firms that invest early in compliance gain long-term reputational credibility. Access to real-time transactional data enables more accurate underwriting for unsecured SME loans, a segment ignored by legacy lenders due to high manual costs. Open-banking interfaces also permit neobanks to embed white-label accounts inside SaaS platforms, expanding reach beyond their proprietary apps. Over the medium term, regulatory alignment across the European Economic Area simplifies cross-border expansion for German-licensed providers.

Incumbent–Neobank Partnership Momentum Reshapes Traditional Hierarchies

Large lenders increasingly cooperate with digital challengers to avoid multi-year core-system rebuilds; Deutsche Bank’s API partnership with a leading fintech payments firm illustrates this pragmatism. Such alliances give neobanks access to established clearing systems and capital markets while incumbents gain rapid innovation cycles. Joint offerings, like integrated FX wallets bundled with traditional trade-finance credit lines, blur competitive lines and accelerate customer acquisition on both sides. The partnership wave shortens time-to-market for new features, deepening service density within the Germany neobanking market. Over time, hybrid distribution models emerge wherein legacy brands front regulatory oversight and balance-sheet strength while neobanks supply customer-facing technology.

Export-Oriented SME Cross-Border Payment Demand Drives B2B Innovation

Germany’s 3.5 million SMEs generate more than 60% of national export revenue and increasingly require instant settlement, transparent FX spreads, and automated reconciliation[2]Federal Ministry for Economic Affairs and Climate Action, “SME Export Statistics 2025,” bmwk.de. . Neobanks leverage cloud-native infrastructures to price transfers well below correspondent-banking fees, reducing working-capital lockups for mid-cap exporters. Treasury modules integrated into enterprise resource planning software let finance teams track multi-currency positions in real time. Regulatory simplification that raised foreign-trade reporting thresholds from EUR 12,500 (USD 13,019.5) to EUR 50,000 (USD 52,078) in 2024 lowers compliance friction and magnifies addressable volumes. Consequently, SME cross-border flows are projected to remain a cornerstone growth driver for the Germany neobanking market over the next decade.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Interchange-fee caps squeeze revenues | -2.1% | EU-wide, with German implementation | Medium term (2-4 years) |

| BaFin AML/KYC scrutiny raises compliance costs | -1.7% | National, with regulatory focus on major players | Short term (≤ 2 years) |

| Consumer trust issues after service outages | -1.4% | National, affecting market leaders | Short term (≤ 2 years) |

| Profitability drag of low-yield deposit base | -1.9% | National, with ECB monetary policy influence | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Interchange-Fee Caps Force Revenue Model Evolution Beyond Payment Processing

European law limits debit-card interchange to 0.2% and credit-card fees to 0.3%, curbing transaction-based income for mobile-only banks[3]European Commission, “Interchange Fee Regulation Overview,” europa.eu.. German providers respond by bundling premium subscriptions that offer travel insurance, higher ATM limits, and carbon-offset debit cards. Fee capping accelerates the pivot into higher-margin segments such as consumer lending, wealth products, and revenue-sharing embedded-finance agreements with SaaS vendors. The Germany neobanking market, therefore, evolves from a free-checking paradigm toward diversified fee baskets. While larger platforms absorb the margin shock by cross-selling, niche challengers must scale rapidly or shift to specialized services to remain viable.

BaFin AML/KYC Scrutiny Raises Compliance Costs and Operational Complexity

BaFin intensified anti-money-laundering oversight after several high-profile system outages and onboarding lapses [4]BaFin, “Supervisory Priorities 2025,” bafin.de.. In 2024, the regulator ordered process audits across digital banks that collectively serve over 10 million German residents, compelling firms to deploy risk-scoring engines and dual-layer biometric verification. Compliance upgrades increase per-customer onboarding costs, eroding the low-cost advantage against branch networks. However, strong governance improves brand trust, which remains essential after public skepticism toward purely app-based finance. Over the short term, rigorous supervision may trigger consolidation as under-capitalized entrants exit, but the long-run outcome is a more resilient Germany neobanking market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Account Type: Corporate Demand Sustains Dominance

Business accounts represented 66.63% of the Germany neobanking market size in 2025, reflecting enterprises’ move toward automated reconciliation and API-enabled treasury dashboards. High export intensity and multi-currency payables drive adoption because digital banks settle FX at real-time rates instead of end-of-day averages. CFOs value single-pane cash visibility across domestic and foreign subsidiaries, reinforcing stickiness within the Germany neobanking market. Savings accounts, although currently smaller, are forecast to grow at a robust 33.82% CAGR through 2031 on the back of attractive digital-only interest rates and instant micro-saving features. As deposit protection clarity improves, retail customers funnel excess liquidity from low-yield checking into regulated savings schemes.

Lower overheads allow neobanks to pass on European Central Bank rate increases more quickly than legacy peers, deepening competitiveness. Automated goal-based saving rules appeal to Gen Z households wary of inflation and climate risk. Meanwhile, SMEs benefit from multi-user permissions and two-factor approvals that streamline invoice settlement without compromising security. Competitive bundling of savings vaults inside business accounts further blurs the line between transactional and reserve products. Consequently, corporate and retail balances together strengthen liquidity ratios that support future lending expansion.

By Services: Mobile Banking Dominance Faces Lending Upswing

Mobile-first checking captured 44.88% of Germany's neobanking market share in 2025, confirming the strategic value of streamlined onboarding that completes in minutes via electronic ID verification. Rich app interfaces that integrate budgeting analytics, push-notification spend alerts, and contactless wallet provisioning anchor daily engagement. Yet loans are the fastest-growing service line, advancing at a 37.28% CAGR to 2031 as credit algorithms harness PSD2 transaction feeds and e-commerce data for near-instant scoring. The Germany neobanking market size for unsecured personal loans is poised to expand further once providers link alternative data with BaFin-approved risk frameworks. Over the forecast horizon, revenue mix is expected to tilt toward consumer and SME credit, diversifying away from margin-compressed payment flows.

Competitive pressure encourages bundling of fixed-rate installment plans, buy-now-pay-later widgets, and micro-credit lines inside the same mobile environment. Interest-rate transparency, amortization calculators, and dynamic repayment options reduce borrower friction and dampen delinquency rates. Partnerships with insurance carriers allow instant credit-life coverage, enhancing regulatory capital efficiency. Meanwhile, money-transfer features retain relevance among immigrant communities by offering euro-to-non-euro corridors at sub-1% spreads. Cross-selling into robo-advisory and carbon-footprint dashboards positions leading apps as full-spectrum financial hubs.

By Application: Enterprise Focus Spurs Consumer Growth

Enterprise solutions contributed 62.15% to overall revenue in 2025 as businesses sought real-time integration with enterprise resource planning and payroll systems. Companies prize automated expense categorization and API endpoints that feed live transaction data into accounting ledgers, thus lowering month-end closing effort. Deep linkages with procurement and inventory modules also reduce manual reconciliations. As a result, the Germany neobanking market maintains high retention in B2B segments where switching costs rise in line with process automation depth. Personal banking applications, however, are projected to grow at a 30.94% CAGR through 2031 as younger cohorts, attracted by no-fee cards and ESG-linked spending insights, take their first salary payments into digital accounts.

Mass-market uptake accelerates once neobanks add features traditionally reserved for wealth managers, such as fractional share dealing and green bond portfolios, inside the same mobile context. Gamified saving streaks and community challenges are designed to build daily engagement without incurring high marketing spend. Personal applications increasingly share infrastructure with enterprise modules, enabling economies of scale on compliance and cloud hosting. Moreover, salary-linked overdraft protection and instant partial payouts create strong value propositions for gig-economy workers. Altogether, B2C momentum complements the enterprise franchise and widens total addressable demand, reinforcing growth in the Germany neobanking market.

Geography Analysis

South Germany led regional revenue with a 26.12% contribution in 2025, fueled by Bavaria’s EUR 716.8 (USD 746.59) billion economy and Munich’s vibrant fintech cluster that attracts both venture capital and seasoned banking talent. High GDP per capita and dense industrial supply chains create sizable fee pools for cross-border treasury and payroll processing. The region’s universities partner with incubators to funnel engineering graduates into scale-ups, further propelling the Germany neobanking market. Established insurance and banking headquarters supply a sophisticated customer base for white-label embedded-finance deployments. Local government grants that subsidize AI and cybersecurity research also foster product innovation.

East Germany posted the fastest 10.98% CAGR outlook through 2031 as fiber-optic rollouts and 5G expansion close historical connectivity gaps. Rising startup density in Leipzig and Dresden diversifies economic activity beyond manufacturing, increasing demand for digital payment accounts and SME credit lines. Federal programs that co-finance digital-skills training support household adoption of app-based banking in previously underserved districts. Lower legacy-branch density offers challengers a cost-efficient path to first-time account holders, enlarging the Germany neobanking market. As regional e-commerce exports grow, neobanks will capture incremental FX and logistics-financing volumes.

North Germany, anchored by Hamburg’s maritime complex, maintains stable demand for multi-currency solutions that track global freight payments in real time. Port operators and logistics firms rely on embedded accounts to streamline customs fees and duty advances, reinforcing stickiness. West Germany remains a core industrial heartland where automotive and chemical conglomerates integrate neobank APIs to manage supplier payments across dozens of countries. Central Germany’s technology parks nurture fintech joint ventures with regional banks, helping neobanks access legacy clearing networks while introducing agile front-end layers. Together, these dynamics ensure broad national diffusion and resilient long-run growth for the Germany neobanking market.

Competitive Landscape

The Germany neobanking market exhibits moderate concentration, with the five largest platforms estimated to control roughly 55% of active accounts. Market leaders leverage cost-efficient digital onboarding, PSD2 data aggregation, and BaFin-compliant bank-as-a-service models to scale quickly. Product roadmaps converge around fee-generating credit, investment, and insurance integrations, reducing reliance on capped interchange. Traditional banks increasingly license front-end technology or embed digital wallets under partnership frameworks, mitigating disruption risk while accelerating innovation cycles. These alliances blend incumbents’ balance-sheet depth with fintech agility, reshaping competitive boundaries.

Green-finance differentiation emerges as a key positioning axis as Gen Z consumers prefer providers that publish carbon-offset metrics and ESG-screened investment baskets. Specialist players target freelancers and content creators with instant VAT reserve accounts and cash-flow analytics. Corporate challengers concentrate on export-oriented SMEs, bundling real-time FX hedging and invoice-financing inside unified dashboards. Technology stacks emphasize micro-services architectures hosted on European cloud regions to comply with General Data Protection Regulation requirements. As BaFin tightens AML norms, scale advantages in compliance investment favor well-capitalized players, potentially driving consolidation that raises barriers to entry.

Intellectual-property acquisition in artificial-intelligence fraud detection, biometric authentication, and context-aware credit scoring remains an active battleground. Venture funding increasingly favors later-stage rounds that back established unit economics rather than customer-acquisition blitzes. Revenue per customer rises as mature platforms monetize savings, credit, and wealth modules, supporting cross-segment subsidization strategies. Market entrants lacking diversified income streams face margin pressure from fee caps and rising Regulation Technology costs. Overall, high product velocity and partnership depth continue to define sustainable advantage in the Germany neobanking market.

Germany Neobanking Industry Leaders

N26 GmbH

Deutsche Kreditbank AG (DKB)

Vivid Money GmbH

Fidor Bank AG

solaris SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Vivid Money partnered with Adyen to provide instant merchant payouts across Europe at fees of 0.29-0.39%, strengthening its SME proposition.

- February 2025: Solaris SE secured EUR 140 (USD 145.818) million in Series G funding led by SBI Group to bolster capital ratios and extend its banking-as-a-service platform.

- January 2025: Finom launched an AI-powered accountant service that auto-reconciles invoices and bank transactions for German SMEs, expanding its embedded-finance suite.

Germany Neobanking Market Report Scope

Neobanks is a bank that operates online without having a physical presence; it is part of fintech that provides digital and mobile-first services like payments, debit cards, money transfers, lending, and more. A complete background analysis of the market, which includes emerging trends, significant changes in market dynamics, and a market overview, is covered in the report. The report also features a qualitative and quantitative assessment by analyzing data gathered from industry analysts. Germany Neobanking Market is segmented by account type (Business Account and Savings Account), by service (Mobile Banking, Payments & money transfer, Savings account, Loans, and others), and by application (Enterprise, Personal, and others). The report offers market size and forecasts for Germany Neobanking Market in value (USD Million) for all the above segments.

By Account Type

| Business Account |

| Savings Account |

By Services

| Mobile-Banking |

| Payments |

| Money-Transfers |

| Savings Account |

| Loans |

| Others |

By Application

| Personal |

| Enterprise |

| Other Application |

By Geography

| North Germany |

| South Germany |

| East Germany |

| West Germany |

| Central Germany |

| By Account Type | Business Account |

| Savings Account | |

| By Services | Mobile-Banking |

| Payments | |

| Money-Transfers | |

| Savings Account | |

| Loans | |

| Others | |

| By Application | Personal |

| Enterprise | |

| Other Application | |

| By Geography | North Germany |

| South Germany | |

| East Germany | |

| West Germany | |

| Central Germany |

Key Questions Answered in the Report

How large is Germany’s neobanking sector in 2026 and what is its growth outlook through 2031?

The Germany neobanking market is valued at USD 970 billion in 2026 and is projected to reach USD 1,910 billion by 2031, reflecting a 14.41% CAGR.

Which account type currently generates the most revenue for German digital banks?

Business accounts lead with a 66.63% share in 2025, driven by strong SME demand for API-enabled treasury and cross-border services.

Which product line is expected to expand fastest for German neobanks over the forecast period?

Lending products show the highest momentum, with the loans segment projected to grow at a 37.28% CAGR through 2031.

Why are cross-border payment capabilities so critical for German providers?

Germany’s 3.5 million export-oriented SMEs demand real-time FX settlement and automated reconciliation, giving neobanks a structural edge over legacy correspondent networks.

What regulatory factor is compressing transaction margins for digital banks?

EU interchange-fee caps of 0.2% on debit and 0.3% on credit card transactions curb payment-related revenues, pushing providers toward subscription and lending income.

Which German region is forecast to register the highest growth rate to 2031?

East Germany is expected to advance at an 10.98% CAGR as improved digital infrastructure and startup activity unlock previously underserved populations.

Page last updated on: