Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.03 Billion |

| Market Size (2026) | USD 2.08 Billion |

| Market Size (2031) | USD 2.5 Billion |

| Growth Rate (2026 - 2031) | 3.70% CAGR |

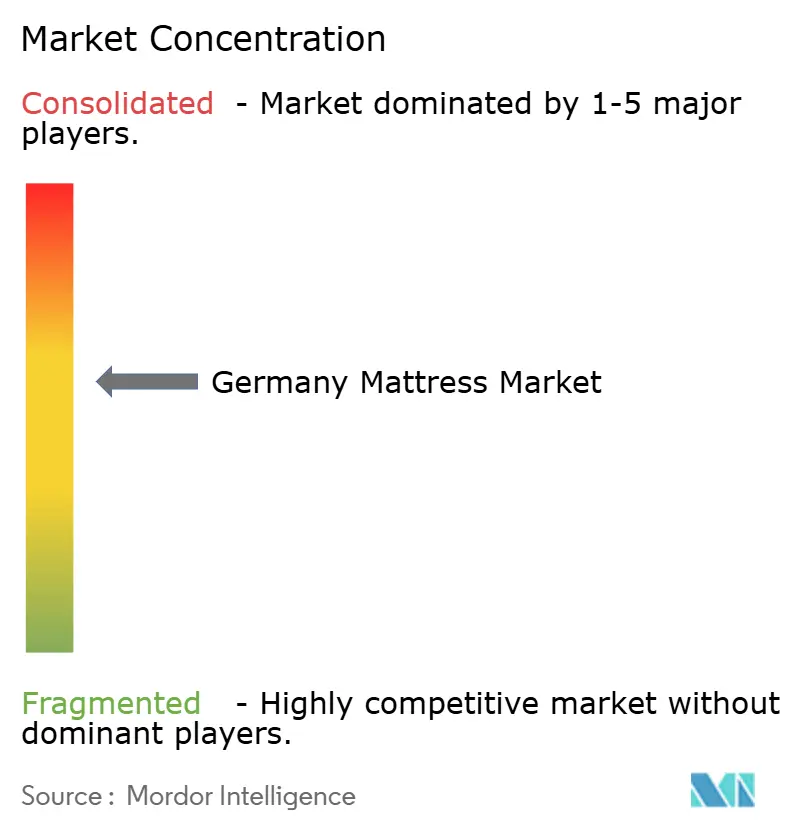

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Mattress Market Analysis by Mordor Intelligence

The Germany mattress market size is expected to increase from USD 2.03 billion in 2025 to USD 2.08 billion in 2026 and reach USD 2.5 billion by 2031, growing at a CAGR of 3.70% over 2026-2031. Manufacturing depth, consumer affluence, and policies that reward sustainable production together sustain this momentum, while heightened public awareness links quality sleep to holistic wellness and thereby elevates purchase intent across demographics. Traditional retail formats still dominate, yet omnichannel playbooks that merge physical trial zones with digital ease are gradually reshaping shopper journeys and compressing price dispersion. Technology-enabled fulfillment networks now ensure two-day deliveries across the German mattress market, a service level that reinforces consumer faith in bed-in-a-box propositions even in historically cautious regions. Alongside demand-side strength, the country’s position as an export platform for adjoining EU members helps smooth cyclical swings, keeping plant utilization rates high and justifying continuous capital upgrades. Lastly, sustainability credentials ranging from Green Button certification to carbon-neutral logistics are emerging as non-negotiable differentiators that widen brand equity gaps and command premium margins in the German mattress market.

Key Report Takeaways

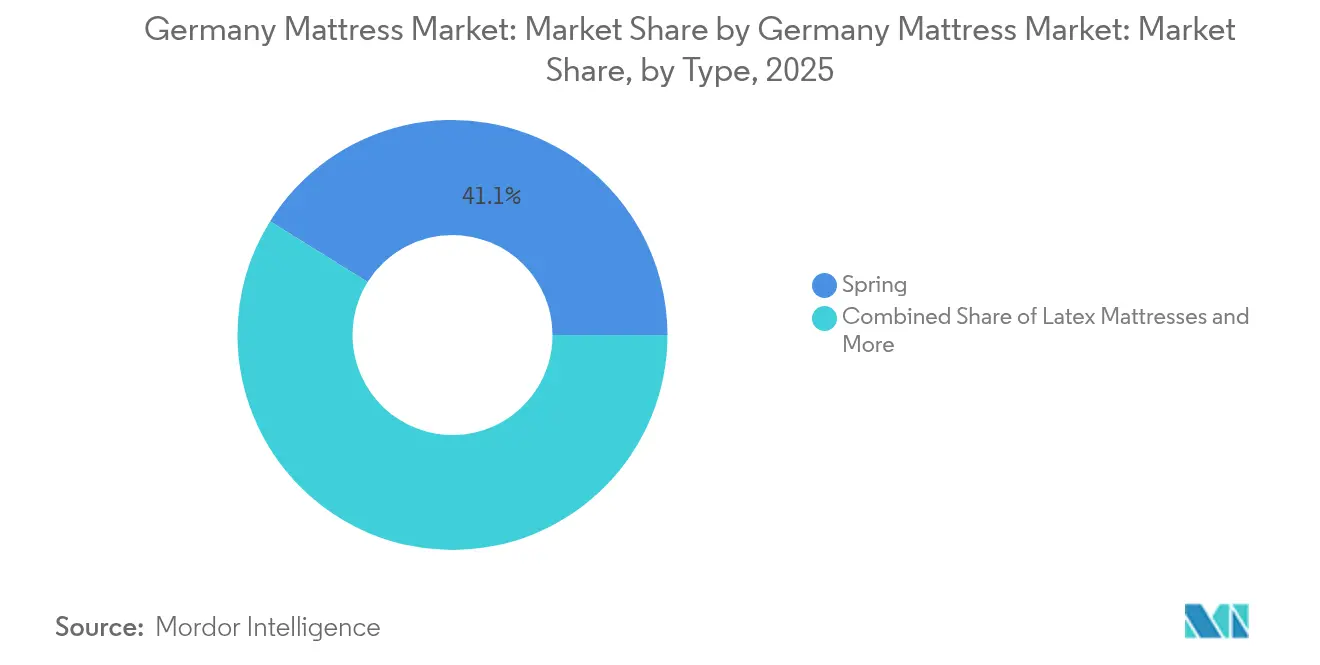

- By product type, spring mattresses led the German mattress market with 41.12% market share in 2025; memory foam mattresses are forecast to expand at a 7.84% CAGR through 2031.

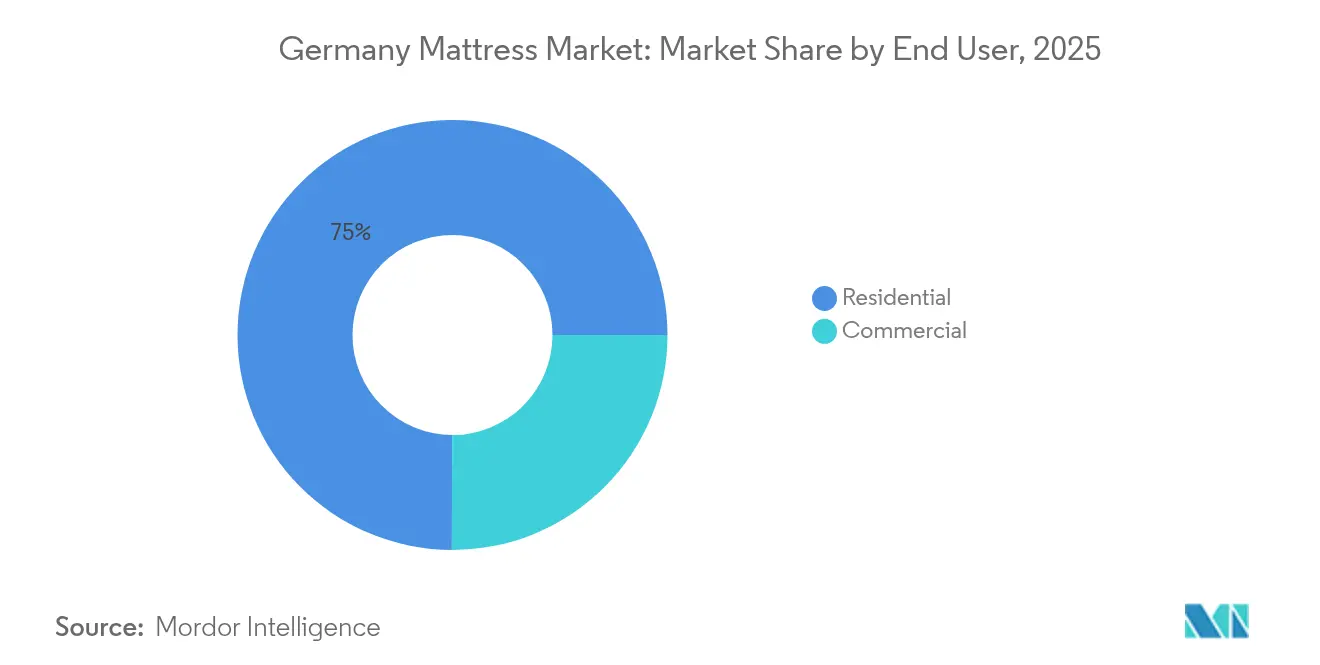

- By end user, residential demand accounted for 74.95% of the German mattress market share in 2025, while the commercial segment is projected to grow at a 5.07% CAGR during 2026–2031.

- By distribution channel, offline retail accounted for 62.74% of the German mattress market share in 2025; online channels are anticipated to grow at a 10.31% CAGR during 2026–2031.

- By geography, North Rhine-Westphalia captured 71.69% of the German mattress market share in 2025; Berlin is anticipated to be the fastest-growing region, registering a 7.01% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Mattress Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer focus on sleep-health & premium comfort | +1.8% | Germany-wide, strongest in urban centers | Medium term (2-4 years) |

| E-commerce expansion lowers go-to-market costs | +2.1% | National, with early gains in Berlin, Hamburg, Munich | Short term (≤ 2 years) |

| Higher disposable income & renovation cycles | +1.4% | Germany-wide, concentrated in high-income regions | Long term (≥ 4 years) |

| Sustainability regulations are pushing climate-neutral mattresses | +1.2% | National, with regulatory influence from EU frameworks | Medium term (2-4 years) |

| Corporate incentives for ergonomic nap areas in offices | +0.7% | Major business districts nationwide | Medium term (2-4 years) |

| German Supply-Chain Act favors local sourcing | +0.8% | National, benefiting domestic manufacturers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising consumer focus on sleep-health & premium comfort

Urban professionals increasingly treat restorative sleep as a core pillar of preventive healthcare, prompting a pivot toward mattresses that advertise orthopedic alignment and certified low-VOC materials. Stiftung Warentest’s detailed scoring rubrics make performance data widely accessible, accelerating informed decision-making that favors high-spec products. Direct-to-consumer pioneer Bett1.de leveraged this scrutiny by positioning its BODYGUARD line as “anti-cartel” value, a message that resonated across age cohorts and helped shift perceptions about fair pricing. As affluent buyers gravitate to multilayer memory foam systems that modulate micro-climate and relieve pressure points, premium units proliferate in the Germany mattress market. Marketing narratives now foreground quantified benefits such as reduced tossing frequency and improved spinal curvature, translating abstract comfort claims into actionable metrics. This convergence of objective testing, health literacy, and brand storytelling reinforces willingness to pay and sustains the driver’s medium-term uplift on market growth.

E-commerce expansion lowers go-to-market costs

Bed-in-box pioneers demonstrated that compressible foam could be shipped safely, thereby removing the showroom bottleneck that long limited category e-commerce penetration. The Germany mattress market benefited from postal codes that receive next-day deliveries and statutory 14-day return rights, both of which shrink perceived risk and fuel repeat purchases. Brands deploy data analytics to refine advertising spend, achieving customer-acquisition costs materially below traditional retail margins and redirecting savings into R&D. Pandemic-era digital habits linger, so even older cohorts now shop for big-ticket items online, elevating basket sizes on web and app interfaces. Brick-and-mortar incumbents responded by launching click-and-collect services and virtual consultation widgets, which reposition floor space as experiential rather than transactional. Consequently, omnichannel frameworks are no longer optional; they are central to defending share as pure online specialists scale. With last-mile carbon footprints under scrutiny, several operators introduced electric-van fleets, combining speed with sustainability to reinforce brand promises.

Higher disposable income & renovation cycles

Macro indicators reveal wage gains outpacing consumer-price inflation, enlarging discretionary budgets that funnel into home-improvement categories such as bedding. Deutsche Bank’s 2024 outlook notes nominal housing prices turning positive after a brief correction, unlocking equity effects that spur refurbishment[1]Deutsche Bank Research, “Outlook for the German Housing Market 2024/2025,” dbresearch.com.. Mattress replacement, therefore, rides a dual trigger: periodic renovation windows and newfound felt prosperity, each amplifying average selling prices in the Germany mattress market. Luxury layers—think gel-infused foams and natural latex cores—benefit disproportionately because households treat them as long-cycle investments rather than sunk costs. Marketing that frames mattresses as durable capital goods dovetails with this mindset and softens sticker shock. Builders and interior designers increasingly bundle premium mattresses into turnkey packages, especially in high-income states such as Bavaria, reinforcing demand at the point of property handover. The driver’s longer timeline reflects the staggered nature of renovation events across Germany’s 41.3 million dwellings.

Sustainability regulations are pushing climate-neutral mattresses

Germany enforces stringent eco-design and due diligence norms, and the Green Button seal now functions as a shorthand for ethically produced textile goods. To comply, suppliers audit upstream emissions and pivot to recycled steel coils, bio-based foams, and solvent-free adhesives. The European Commission’s life-cycle analysis of mattresses gives additional weight to end-of-life recyclability, influencing not only raw-material choices but also disassembly-friendly designs[2]European Commission, “Final LCA Report on Bed Mattresses,” ec.europa.eu. . Producers that meet or exceed these stipulations secure access to institutional procurement frameworks that prioritize green criteria, including public tender contracts for hospitals and dormitories. Carbon-neutral logistics solutions, such as rail-first freight, further strengthen corporate bids. As awareness filters down to households, survey data indicate that more than half of first-time parents now research product sustainability before purchasing a crib mattress, signaling future-proof demand. Given regulatory tightness and consumer activism, compliance ceases to be overhead and instead becomes a priced asset that commands margin uplift.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Market saturation & long replacement cycle | -1.5% | Germany-wide, particularly in established markets | Long term (≥ 4 years) |

| Escalating EU foam/latex input costs | -0.9% | National, affecting all manufacturers | Short term (≤ 2 years) |

| Strict fire-safety / recyclability compliance costs | -0.6% | National, with regulatory influence from DIN/EN standards | Medium term (2-4 years) |

| Urban switch to sofa-beds, reducing mattress purchases | -0.4% | Metropolitan areas, particularly Berlin, Hamburg, and Munich | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Market saturation & long replacement cycle

Penetration in mature regions approaches 1 mattress per adult, limiting upside from first-time buyers and shifting competitive focus to replacement frequency. German sleepers traditionally keep mattresses for 8-12 years, a tenure that tempers annual turnover despite population growth. Extended warranties offered by premium brands, while attractive to consumers, also elongate replacement intent and thus drag on volume. Aggressive promotional tactics aimed at accelerating upgrade decisions sometimes erode category value by conditioning shoppers to wait for discounts. Additionally, smaller urban dwellings increasingly opt for convertible sofa-beds, shrinking the addressable unit base in dense metros. The restraint’s long-term effect reflects the structural nature of demographic density and cultural frugality, both of which resist quick remediation.

Escalating EU foam/latex input costs

Natural-latex tapping disruptions in Southeast Asia and volatile TDI prices in European chemical hubs jointly inflate the bill of materials, squeezing gross margins across foam-heavy SKUs. EUROPUR notes that flexible polyurethane cost increases of even 4% translate almost directly into a 3-4 percentage-point decline in mattress profit contribution unless offset by retail price hikes. Passing through costs proves tricky in segments where price transparency online has trained consumers to cherry-pick deals. Smaller independents lacking scale purchase contracts face sharper shocks, intensifying consolidation risk that may further alter the structure of the Germany mattress market. Manufacturers explore substitutes such as coconut fiber cores, yet these materials seldom deliver an identical feel or durability, limiting adoption. Over the short term, cost pressures catalyze efficiency drives ranging from foam-nest optimization to digital twin modeling to minimize scrap rates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Memory Foam Innovation Drives Premium Shift

Spring units continue to dominate with a 41.12% share of the German mattress market in 2025, underscoring consumer comfort with established coil technology. Nevertheless, the memory-foam segment is forecast at a 7.84% CAGR, signaling a premium pivot fuelled by thermal-management gels and zoned support foams that visibly differentiate performance. Latex formats enjoy a loyal following among allergy-sensitive buyers and eco-conscious households, though their higher ticket price constrains mass uptake. Hybrid models that marry pocket springs with viscoelastic layers blur categorical boundaries, allowing legacy manufacturers to defend relevance against foam specialists. Testing frameworks from EUROPUR calibrate resilience and indentation parameters, creating a level field where quality claims can be audited and thus trusted by German shoppers. Marketing narratives now revolve around sleep-stage analytics, presenting memory foam as conducive to prolonged deep-sleep intervals, which enhances daily cognitive performance. Because these health benefits withstand third-party validation, they increasingly command higher average selling prices and lift total revenue despite modest unit share gains in the Germany mattress market.

Memory-foam advancements resonate with e-commerce’s box-shipping format, giving digital-native labels cost advantages that play well in Germany’s tightly regulated logistics arena. Compression technology permits container densification, lowering per-unit freight emissions, an attribute highlighted in sustainability scorecards. Spring-oriented incumbents respond with micro-coil layers that simulate foam contouring while retaining their legacy know-how, protecting their base amid technological disruption. Meanwhile, latex producers bundle cradle-to-cradle certifications to reinforce green leadership, winning niche yet profitable contracts with boutique hotels that brand themselves eco-neutral. Collectively, the type segmentation showcases how innovation breadth—not just absolute market share—drives brand elevation and margin capture within the Germany mattress market.

By Distribution Channel: Digital Transformation Accelerates

Physical stores retained a 62.74% share of the Germany mattress market in 2025, but online sales trajectories at 10.31% CAGR signify enduring channel reallocation that erodes legacy markups. Showrooms still matter because German buyers value tactile assessment of firmness, yet many now use in-store trials only to place final orders via lower-priced web shops. Retail chains integrate QR-based product tags that link to manufacturer videos, bridging information asymmetry and capturing leads before shoppers exit to competitor platforms. Courier networks offering carbon-offset delivery certificates add reputational sheen, dovetailing with legal pressures to document sustainability metrics. Returns handling remains a sticking point; nonetheless, algorithmic restocking systems cut reverse-logistics costs and shorten refund cycles, bolstering online satisfaction scores.

For incumbents, omnichannel investment reallocates capex from new store builds toward platform enhancements such as 3D room-visualization tools that help consumers gauge mattress height under diverse bed frames. Meanwhile, pure-play e-commerce brands like Emma Sleep augment credibility through pop-up test lounges in Tier-1 cities, validating a phygital thesis that blends low overhead with selective experiential touchpoints. The channel landscape thus converges toward a hybrid equilibrium, making agility in inventory orchestration and customer service the key determinant of durable share in the Germany mattress market.

By End User: Commercial Segment Gains Corporate Wellness Traction

Residential households continue to anchor 74.95% of the Germany mattress market size in 2025, underpinned by cyclic replacement and family formation trends. Public discourse around ergonomic sleep gains momentum, prompting families to upgrade across age cohorts—crib, junior, and adult—during single shopping occasions, thereby raising basket values. Housebuilders partner with mattress suppliers for fully furnished offers, adding convenience that locks in volume and provides a predictable pipeline for manufacturers. In addition, regulatory encouragement for energy-positive homes indirectly benefits mattress sales because whole-house refurbishments usually include bedding overhauls.

Commercial demand, though smaller in base, is set for a 5.07% CAGR thanks to office wellness zones, boutique hotel refurbishments, and an aging-patient boom in healthcare facilities. Hospital groups procure pressure-redistribution mattresses compliant with infection-control norms, a specification niche commanding up to 20% price premiums over consumer equivalents. Corporate nap pods require compact yet durable foam cores that withstand intensive daily cycles, spurring specialized R&D investment. Student housing operators contract standardized SKUs for rapid turnover, favoring suppliers that keep buffer stock regionally for emergency replacements. Altogether, the commercial pathway injects diversification and counters household replacement cyclicality, offering a strategic hedge and incremental growth within the Germany mattress market.

Geography Analysis

North Rhine-Westphalia captured 71.69% of the Germany mattress market in 2025, reflecting its dense population, automotive-grade manufacturing clusters, and multimodal freight corridors that facilitate both inbound materials and outbound finished goods. Co-location of foam formulators and spring manufacturers shortens lead times and supports just-in-sequence production models attractive to large retailers. Bavaria and Baden-Württemberg follow as high-income catchments where premium SKUs command disproportionate revenue, aided by retail footprints that showcase luxury bedding side by side with high-end furniture.

Berlin stands out with a 7.01% CAGR through 2031, propelled by a tech workforce comfortable with online shopping and flexible living arrangements that necessitate frequent furnishing updates. Co-working operators and startup campuses there often integrate sleep pods, directly boosting commercial demand. Hamburg and Munich witness similar urban dynamics, though smaller dwelling sizes encourage sofa-bed uptake, partially cannibalizing traditional mattress needs. Nonetheless, rising per-square-meter rents push tenants toward mattress toppers that upgrade comfort without replacing frames, creating accessory upsell avenues.

Eastern German states remain volume-relevant through value-priced offerings and long-established brick-and-mortar chains. Logistics improvements along the A14 and planned rail expansions promise wider reach for omnichannel deliveries, potentially lifting future share. Overall, state-level heterogeneity obliges suppliers to tailor assortment, promotional cadence, and logistics strategies to local economic structures and cultural buying behaviours, ensuring the Germany mattress market maintains broad-based expansion.

Competitive Landscape

The German mattress market reflects moderate concentration, with leading players holding a significant share. Bett1.de stands out through its single hero SKU approach, simplifying inventory and marketing operations. Emma Sleep closely follows, fueled by aggressive international expansion and data-driven optimization of its digital sales channels. Tempur Sealy International continues to leverage its strong brand heritage and cross-border distribution efficiencies. Hilding Anders and Badenia Bettcomfort complete the top tier, benefiting from regional dealer partnerships and white-label manufacturing, respectively.

Mattress Market growth strategies are increasingly shaped by sustainability, omnichannel integration, and innovations in materials science. Emma Sleep’s pledge to become carbon-neutral by 2030 strengthens its appeal among environmentally conscious consumers, particularly millennials. Tempur Sealy’s proposed merger with Mattress Firm signals deeper consolidation, potentially shifting supply chain dynamics and supplier leverage. Private equity remains active, shown by recent investments in niche latex manufacturers that cater to both consumer and healthcare markets. Compliance with Germany’s Supply Chain Act is also influencing competitive advantage, favoring domestic foam producers that already meet due diligence standards.

As competition intensifies, rising digital advertising costs are pressuring brands to refine their customer experience and differentiate more clearly through product quality and service. Strong branding and operational efficiency will be key to maintaining profitability in an increasingly crowded space. Players with vertically integrated operations or unique propositions are better positioned to defend margins. Meanwhile, regulatory shifts and sustainability expectations are forcing traditional manufacturers to evolve quickly. The coming years are likely to test both the agility and resilience of incumbents and new entrants alike.

Germany Mattress Industry Leaders

Bett1.de GmbH

Emma Sleep GmbH

Tempur Sealy International Inc.

Hilding Anders International AB

Recticel NV (Schlaraffia)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: EUROPUR released an updated analysis on flexible polyurethane foam properties, guiding manufacturers on performance optimization for high-density memory foams.

- February 2024: Tempur Sealy International posted USD 4.93 billion in 2023 net sales and announced plans to debut Tempur-Pedic Adapt mattresses across Europe, including Germany.

- August 2024: Vonovia SE confirmed stewardship of 480,000 apartments, integrating energy-efficient refurbishments that precipitate mattress turnover cycles.

- September 2024: T-Online published Stiftung Warentest results highlighting Breckle Weida Flex Air as top-rated spring mattress and f.a.n. Medisan Plus KS is the leading foam mattress.

Germany Mattress Market Report Scope

The German mattress market report provides an overview of the market with an exhaustive analysis of current market advancements. The report also focuses on the trends in production and consumption data of the product, policies and plans, cost structures, and manufacturing processes. Moreover, the company profile of the key competitors, along with a thorough analysis, is also provided.

By Type

| Spring Mattresses |

| Memory Foam Mattresses |

| Latex Mattresses |

| Other Mattresses |

By Distribution Channel

| Online |

| Offline |

By End User

| Residential |

| Commercial |

By Region

| Baden-Württemberg |

| Bavaria |

| Berlin |

| Brandenburg |

| Bremen |

| Hamburg |

| North Rhine-Westphalia |

| Rest of Germany |

| By Type | Spring Mattresses |

| Memory Foam Mattresses | |

| Latex Mattresses | |

| Other Mattresses | |

| By Distribution Channel | Online |

| Offline | |

| By End User | Residential |

| Commercial | |

| By Region | Baden-Württemberg |

| Bavaria | |

| Berlin | |

| Brandenburg | |

| Bremen | |

| Hamburg | |

| North Rhine-Westphalia | |

| Rest of Germany |

Key Questions Answered in the Report

How fast is the Germany mattress market expected to grow through 2031?

It is projected to expand from USD 2.08 billion in 2026 to USD 2.507 billion by 2031, translating into a 3.7% CAGR.

Which mattress type is gaining the most traction among German consumers?

Memory-foam models lead in growth, forecast at a 7.84% CAGR as shoppers prioritize pressure relief and thermal regulation.

What share do online channels hold within German mattress sales?

Online platforms represented 37.26% of 2025 value and are accelerating at a 10.31% CAGR as omnichannel convenience resonates.

Why is Berlin considered a hotspot for mattress demand?

The capital shows the fastest regional CAGR at 7.01% due to its tech-savvy population, furnished-apartment turnover, and openness to direct-to-consumer brands.

How are sustainability rules shaping product development?

Compliance with the Green Button and EU life-cycle standards is driving adoption of recycled coils, bio-based foams, and carbon-neutral freight solutions.

What is the main restraint limiting future sales growth?

High household penetration and 8–12-year replacement cycles dampen incremental unit demand, pressing firms to innovate and shorten upgrade intervals.

Page last updated on: