Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

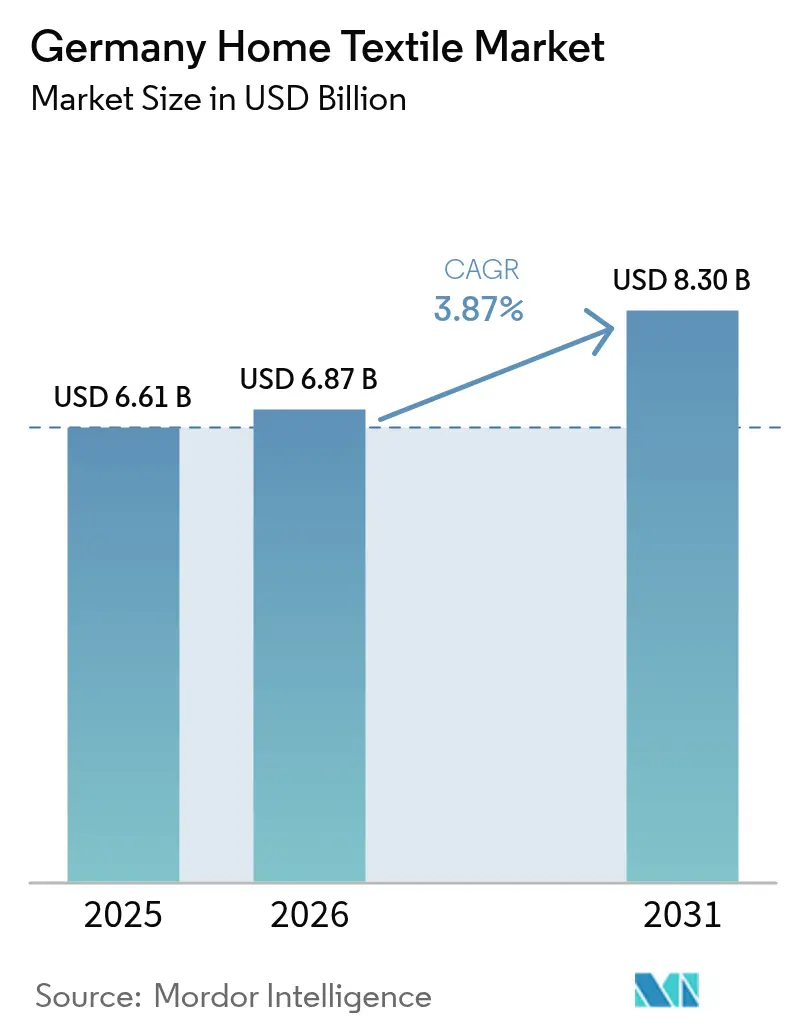

| Base Year Market Size (2025) | USD 6.61 Billion |

| Market Size (2026) | USD 6.87 Billion |

| Market Size (2031) | USD 8.3 Billion |

| Growth Rate (2026 - 2031) | 3.87% CAGR |

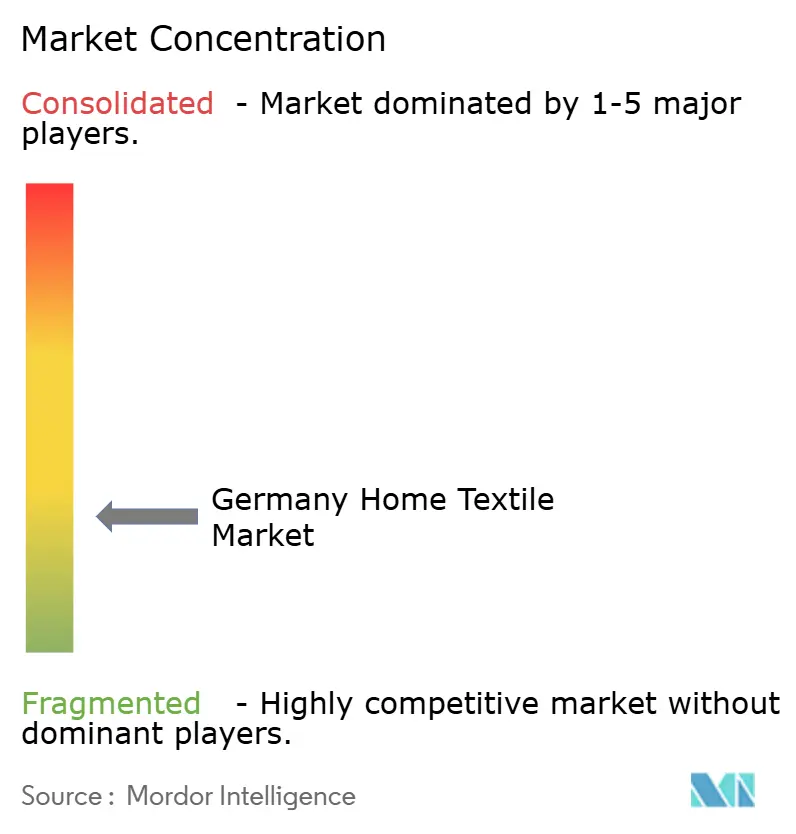

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Home Textile Market Analysis by Mordor Intelligence

The Germany home textile market size is expected to grow from USD 6.61 billion in 2025 to USD 6.87 billion in 2026 and is forecast to reach USD 8.3 billion by 2031 at 3.87% CAGR over 2026-2031. Strong online buying habits, premiumization in household goods, and regulatory support for energy-efficient refurbishment keep the Germany home textile market on a firm upward path even as discretionary spending stays under pressure. E-commerce has effectively removed regional barriers, letting brands court 99% of connected German adults and turning digital storefronts into the main showcase for sustainable bed, bath, and window products. Consumer loyalty, however, now hinges on clear proof of origin; retailers that track fiber inputs through GOTS certification or Digital Product Passport pilots win repeat sales and soften inflation-related price fears. At the same time, commercial buyers, from hotels to senior-living operators, return to multi-year linen contracts in response to tourism recovery, ensuring the Germany home textile market captures gains on both the B2C and B2B sides.

Key Report Takeaways

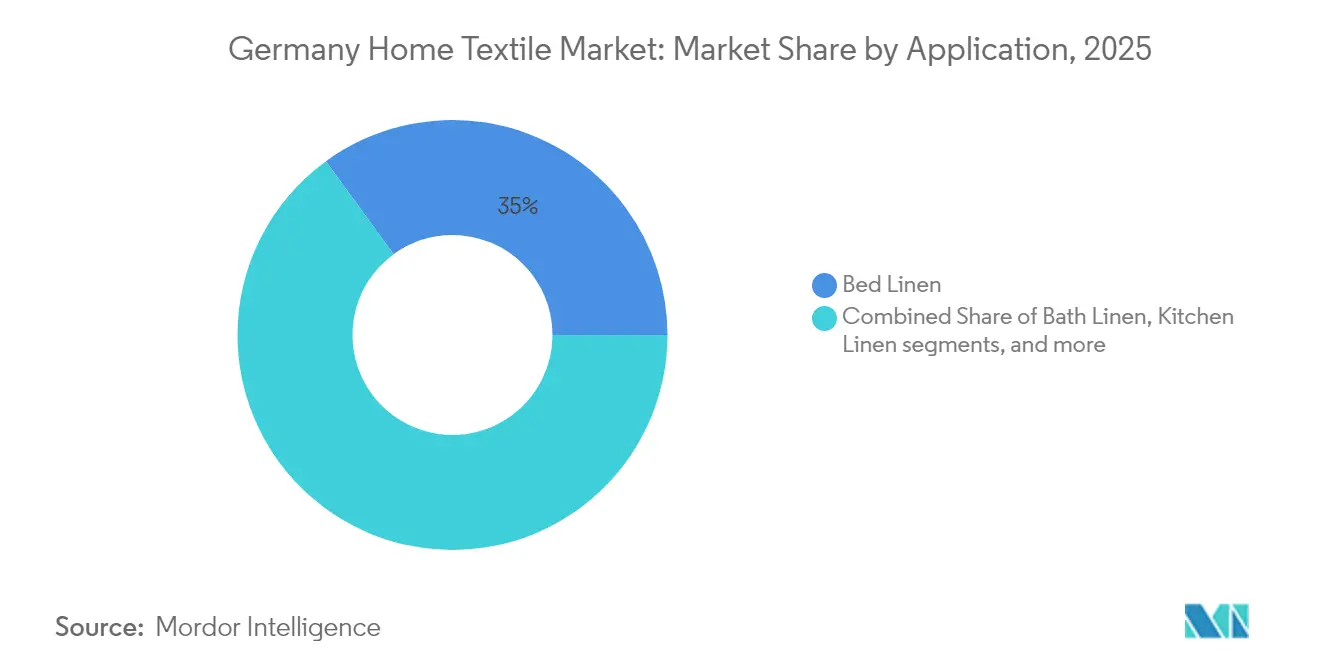

- By application, bed linen commanded 35.02% of Germany home textile market share in 2025; bath linen is projected to grow at a 4.48% CAGR through 2031.

- By material, cotton held 52.12% of the Germany home textile market size in 2025, while alternative fibers are forecast to advance at a 4.29% CAGR.

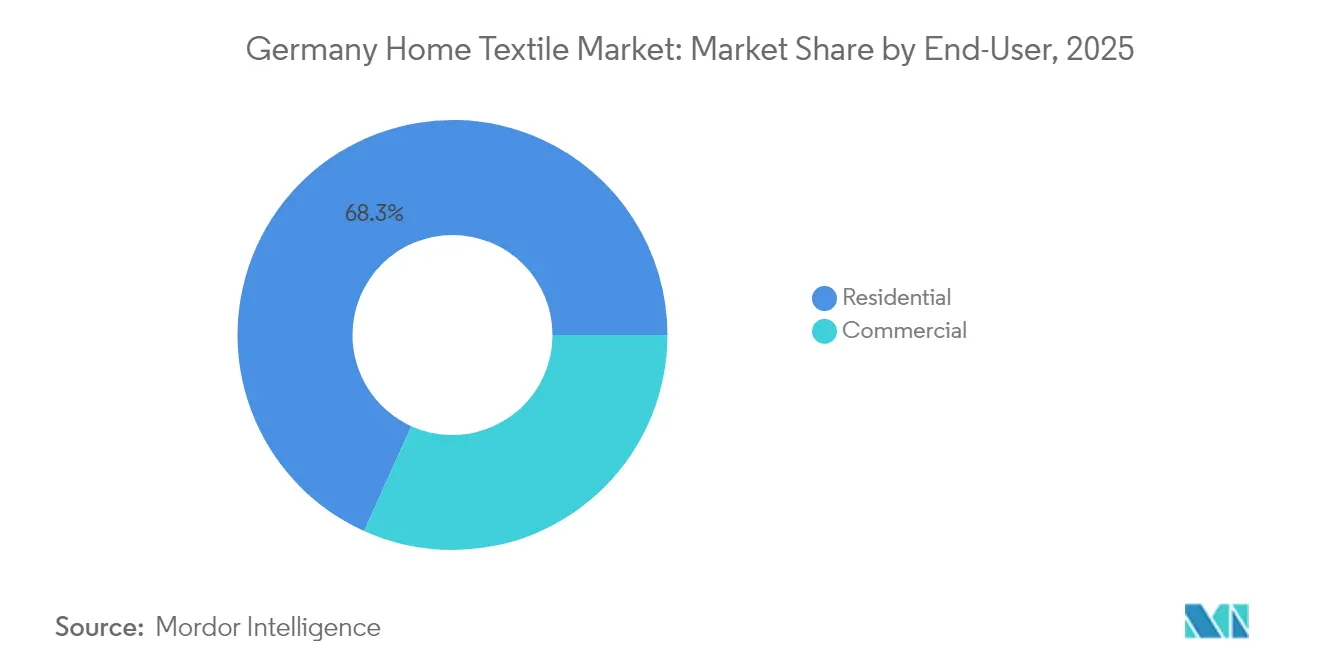

- By end-user, residential demand represented 68.25% of 2025 revenue, yet the commercial segment is on track for a 4.1% CAGR to 2031.

- By distribution channel, B2C retail retained 71.65% revenue share in 2025; direct B2B sales are poised for a 4.66% CAGR expansion.

- By region, South Germany led with a 30.88% 2025 share, but East Germany is primed for the fastest 5.05% CAGR over the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Home Textile Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce penetration & omnichannel retail acceleration | +0.8% | National, strongest in urban centers | Medium term (2-4 years) |

| Government-backed energy-saving subsidies for smart/shading textiles | +0.3% | National, focused on building efficient programs | Long term (≥ 4 years) |

| Hospitality & serviced-apartment pipeline rebound | +0.4% | Major metropolitan areas, tourism hubs | Short term (≤ 2 years) |

| Sustainability-driven demand for certified organic & recycled fibers | +0.6% | National premium segments | Medium term (2-4 years) |

| Ageing-in-place renovations boosting functional/anti-allergen bedding | +0.5% | National, aging demographics | Long term (≥ 4 years) |

| Adoption of smart/IoT-enabled blinds & curtains | +0.2% | Urban areas, new construction | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-commerce Penetration & Omnichannel Retail Acceleration

Germany’s high-speed connectivity and mature logistics network allow retailers to serve almost every household within two days, a capability that underpins the Germany home textile market’s rising online conversion ratio. Weekly online shopping now involves 39% of adults, and furniture-focused portals report double-digit traffic spikes after livestream product launches [1]Eurostat, “Digital Economy and Society Statistics on E-commerce,” ec.europa.eu. Brick-and-click formats prove effective because shoppers prefer to compare textile hand-feel in stores yet check colorways or stock online, pushing chains to fund RFID-enabled showrooms that sync inventories in real time. Larger players absorb the tech outlay; small manufacturers without fulfillment software face visibility setbacks. As digital engagement broadens, differentiated storytelling around sustainable sourcing and smart-home integration keeps margins from eroding in a competitive pricing climate.

Government-backed Energy-saving Subsidies for Smart/Shading Textiles

Building regulations that mandate tighter energy envelopes encourage homeowners to add motorized blinds and thermally efficient draperies eligible for BEG rebates. BAFA reports that applications for shading system subsidies climbed 18% year over year, a trend that diverts spending toward value-added window coverings [2]BAFA, “Guidelines for Energy-Efficient Building Subsidies,” bafa.deSource: BAFA, “Guidelines for Energy-Efficient Building Subsidies,” bafa.de. Textile mills partner with motor drives and sensor firms, embedding conductive yarns to enable automatic daylight adjustment. Because these products qualify for both energy and ESG labels, retailers can justify premiums even during broader cost-of-living strains. The alignment with Germany’s 2045 carbon-neutrality target assures long-running support, creating a structural lift for the Germany home textile market beyond normal replacement cycles.

Hospitality & Serviced-apartment Pipeline Rebound

RevPAR in Berlin and Munich surpassed 2019 levels in early 2025, fueling linen replenishment orders from hotel groups restoring occupancy thresholds [STR-GLOBAL] [3]STR Global, “Germany Hotel Performance Review 2025,” str.com. Serviced-apartment operators extend demand by insisting on higher thread-count sheets and quick-dry towels that cut laundry cycles. Commercial laundry, under cost pressure from energy tariffs, favors textiles engineered for more than 250 wash turns, granting suppliers of reinforced cotton-poly blends an edge. As events such as Oktoberfest 2025 re-draw global travelers, procurement teams sign two-year bulk contracts to lock in unit prices, stabilizing revenue visibility. This commercial surge partially insulates the Germany home textile market from softer residential outlays.

Sustainability-driven Demand for Certified Organic & Recycled Fibres

German consumers increasingly equate textile quality with environmental credentials; 59% consult sustainability labels before clicking “buy now”. Retailers react by expanding shelf space for GOTS-certified organic cotton, TENCEL™ lyocell, hemp, and bamboo blends. Mills invests in blockchain traceability to pass EU Digital Product Passport audits, transforming compliance into a marketing asset. Certifications translate into a 12–15% unit price premium that shoppers accept, particularly in baby bedding and premium towel sets. In turn, supplier order books for undyed and low-water-print fabrics lengthen, underpinning the German home textile market’s value trajectory.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile cotton & energy prices are pressuring manufacturer margins | -0.9% | National, manufacturing regions | Short term (≤ 2 years) |

| Weak consumer furniture spend amid cost-of-living squeeze | -0.7% | National, middle-income households | Medium term (2-4 years) |

| Stricter EU traceability/DPP rules are raising compliance costs for SMEs | -0.4% | EU-wide, German SME manufacturers | Medium term (2-4 years) |

| Hotel sector’s below-EU ADR dampening short-term linen CAPEX | -0.3% | Tourism-dependent regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Cotton & Energy Prices Pressuring Manufacturer Margins

Spot cotton quotations swung 28% within six months of 2024, forcing mills to juggle hedging and surcharges that retailers often resist [4]Deutscher Textilreinigungs-Verband, “Cost Index for Textile Services 2024,” dtv-deutschland.org. Germany’s electricity tariffs, still among Europe’s highest, add another squeeze, especially for energy-heavy weaving and finishing lines. Producers accelerate photovoltaic rooftop projects and heat-recovery systems to blunt cost spikes, yet payback stretches beyond SME cash tolerances. Some resort to near-shoring in Czechia or Türkiye, altering supply chain geography and diluting domestic value capture for the Germany home textile market. Until input volatility stabilizes, mid-tier brands may trim SKU diversity to conserve working capital.

Weak Consumer Furniture Spend Amid Cost-of-living Squeeze

Real wages rose only 0.3% in 2024, and households trimmed non-essential décor budgets, delaying curtain or cushion refresh cycles. Promotion-led sales events still trigger volume lifts, but margins narrow as retailers absorb part of shipping surcharges. Top-line softness is most evident in mid-priced assortments, whereas discount stores and luxury boutiques maintain footfall, polarizing the Germany home textile industry. Firms respond with multi-pack pricing and loyalty-card points rather than blanket markdowns to protect perceived quality. Recovery hinges on broader macro stabilization expected post-2026.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Bed Linen Leads, Bath Linen Accelerates

Bed linen retained leadership with 35.02% of Germany home textile market share in 2025, underpinning category stability through its essential-purchase status and wide price ladder. High-thread-count cotton and linen blends dominate premium tiers, while private-label microfiber sets cater to budget shoppers. Seasonal color refreshes and bundled pillowcase promotions sustain repeat sales, yet competitive saturation limits price hikes, prompting brands to upsell coordinated comforters and protectors.

Bath linen, meanwhile, is projected to expand at a 4.48% CAGR through 2031, the fastest among applications. German consumers equate plush towels and robes with wellness, and antimicrobial, quick-dry technologies justify double-digit price premiums. Online searches for “bamboo bath towel” climbed 23% between Q4 2024 and Q2 2025, signifying substitution potential. Hotels adopt heavier-grammage robes that endure 250 wash cycles, broadening commercial volume. Together, these dynamics keep both leading and fastest-growing segments pivotal to the Germany home textile market size trajectory.

By Material: Alternative Fibers Challenge Cotton Dominance

Cotton supplied 52.12% of the Germany home textile market size in 2025, yet modal, hemp, and recycled polyester fabrics collectively register greater momentum. Fiber innovators promote TENCEL™ Lyocell bedding that repels bacteria better than conventional cotton, winning favor among allergy-prone households. GOTS-certified organic cotton still outperforms conventional cotton in value terms because traceability justifies a premium, cushioning producers from raw-cotton volatility. Smart-textile research institutes, including TITV Greiz, embed conductive yarns into wool blends, expanding use into climate-adaptive curtains. Altogether, material choice becomes a key brand differentiator rather than a behind-the-label detail.

Cotton mills respond by adopting regenerative agriculture contracts to maintain relevance, integrating rain-fed farming claims into marketing narratives. Blended fabrics exploiting hemp’s tensile strength and bamboo’s softness appear in bathrobes and nursery textiles, widening the eco-luxury offering. European Commission draft rules promoting recycled content lend further weight to synthetics that incorporate post-consumer PET bottles. The Germany home textile market thus evolves from single-fiber dominance to a portfolio of specialized materials, each mapped to health or environmental gains.

By End-User: Commercial Segment Accelerates Despite Residential Dominance

Residential demand captured 68.25% of 2025 revenue, anchored in routine bedding and window coverings that households replace every three to five years. Commercial orders, however, are on a 4.1% CAGR trajectory as hotels, healthcare, and corporate offices prioritize antimicrobial and durable textiles.. Hospitals gravitate toward antimicrobial sheets certified under DIN EN 13795, recognizing infection-control dividends. Corporate offices, redesigning workspaces for hybrid schedules, installing acoustic textile panels and blackout roller blinds, and broadening the Germany home textile market beyond traditional décor. Although residential replacement cycles slow in inflationary periods, commercial tenders contract on three-year horizons, smoothing revenue curves.

Specialized distributors invest in digital portals that let hotel managers model lifetime cost per wash, an approach that converts on sustainability and budget criteria simultaneously. Residential retailers, conversely, emphasize narrative, carbon-neutral shipping, artisan-made stories, to differentiate. The parallel trajectories ensure the Germany home textile market enjoys both volume resilience and value upside.

By Distribution Channel: B2B Direct Sales Gain Momentum

B2C retail still channels 71.65% of turnover, spanning supermarkets, décor chains, department stores, and online marketplaces. Yet direct B2B commerce climbs by a CAGR of 4.66% because institutional buyers value bespoke specifications and immediate factory contact. Manufacturers integrate ERP systems with client dashboards, enabling just-in-sequence deliveries and predictive reorder notices. Energy-cost volatility motivates laundries to negotiate directly with mills for long-life towel specs, bypassing wholesalers. Digital showrooms, featuring 3D fabric drape simulations, help exporters court overseas clients without trade-fair travel, boosting the Germany home textile market’s international profile.

In B2C, discount grocers expand premium private labels after seeing Stiftung Warentest awards lift foot traffic; ALDI’s eco-detergent-paired towel bundles sold out within days. Pure-play e-tailers deploy AI-powered fit advisors to cut return rates on sheets and mattress protectors. The omnichannel reality means brands must sync inventory across store aisles, web carts, and B2B order portals, an operational complexity that favors scale players.

Geography Analysis

South Germany retained a 30.88% stake of the Germany home textile market in 2025. South Germany’s dominance traces to Bavaria and Baden-Württemberg, where gross household earnings surpass USD 60,000 per year and sustain an appetite for premium décor. Cross-border shopping from Austria and Switzerland bolsters weekend footfall, while robust automotive job security maintains consumer confidence. Retailers curate alpine-inspired bedding lines and climate-adaptive draperies suited to the region’s continental weather shifts. Still, elevated property prices compress living spaces, nudging consumers toward minimalist textile collections and pushing sales volumes into higher value, not wider quantity.

East Germany, by contrast, posts a 5.05% CAGR thanks to factory expansions in Saxony and Brandenburg backed by regional grants. The East’s trajectory reflects its reinvention from legacy textile hub to innovation corridor. Public-private clusters around Chemnitz and Greiz funnel EU funds into smart-fabric prototyping, drawing OEM contracts from automotive seat-cover suppliers. Rising wages raise regional purchasing capacity, and the Germany home textile market benefits as first-time homeowners invest in full bedroom and bath setups. Smaller city centers deploy pop-up “fabric experience” stores to test demand before permanent lease commitments, a low-risk format that large chains now replicate.

North, West, and Central regions preserve mid-single-digit growth on the back of logistics prowess and demographic diversity. Ports in Hamburg ease import of Asian fabric inputs, lowering landed cost for discount retailers headquartered nearby. Ruhr-area urban renewal grants fuel rental-apartment renovations that require blackout curtains and allergy-safe mattress encasements. Frankfurt’s expatriate population lifts demand for internationally sized bedding, prompting retailers to stock both EU and U.S. dimensions. Collectively, these metropolitan nodes keep the Germany home textile market balanced against regional slowdowns.

Competitive Landscape

Competition sits at a fragmented level. IKEA Deutschland maintains traffic by trimming starting price points on staple textiles while upselling coordinated accessory lines. Otto Group leans on data-driven inventory planning that lifted EBITDA margins even when topline inched down, proving that digital prowess now rivals square footage as a scale lever. Westwing’s curated collections clocked 6% year-over-year revenue growth in Q1 2024, illustrating how lifestyle storytelling converts premium shoppers. Pure-play D2C labels use micro-influencer campaigns to nibble at category niches such as linen pillowcases or thermo-regulating duvets.

M&A continues as a route to functional depth: Freudenberg’s September 2024 acquisition of Heytex augments its portfolio with coated fabrics for architecture and industry, signaling convergence between home and technical segments. Start-ups leverage crowdfunding to pre-sell recycled-polyester sheet sets, thereby funding initial production runs without bank loans. Yet scale challenges loom; compliance with Digital Product Passports favors capital-rich incumbents. Overall, the Germany home textile market rewards companies that pair transparent sourcing with digital customer engagement, a dual capability still scarce among smaller regional mills.

Technological differentiation intensifies. Mills adopts digital pigment printing to reduce water use by 95%, an eco-claim that resonates with local ordinances restricting wastewater discharge. IoT integration arrives via Bluetooth-enabled curtain rails that sync with apartment management systems, a feature that wins bids in build-to-rent developments. Players that lag on either environmental or tech criteria risk margin erosion as procurement scorecards become stricter.

Germany Home Textile Industry Leaders

IKEA Deutschland

Otto Group

ALDI (Süd & Nord)

Westwing Group SE

Jysk Germany

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: German Partnership for Sustainable Textiles released organic-cotton sourcing guidelines that anchor industry efforts to meet EU traceability mandates, offering SMEs sample audit templates and preferred-fiber scorecards.

- January 2025: Trident Group unveiled expanded EU-focused bed and bath collections at Heimtextil 2025, underscoring its commitment to recycled and organic inputs and signaling intent to localize warehousing for faster German delivery.

- November 2024: Outlast debuted NASA-inspired phase-change microcapsule fill for duvets, bringing advanced thermal regulation to premium bedding lines.

- September 2024: Freudenberg Performance Materials completed the purchase of major Heytex units, gaining architectural fabric know-how and broadening high-performance textile capacity.

Germany Home Textile Market Report Scope

This report aims to provide a detailed analysis of the home textile industry in Germany. It focuses on market dynamics, technological trends, and insights into various types, applications, and process types. Also, it analyses the major players and the competitive landscape in the home textile industry. The German home Textile Market is Segmented by Product (Bed Linen, Bath Linen, Kitchen Linen, Upholstery, and Floor), and by Distribution Channel (Specialty Stores, Supermarkets and Hypermarkets, Online, and Others), and End Users (Residential and Commercial). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Application

| Bed Linen |

| Bath Linen |

| Kitchen Linen |

| Upholstery |

| Carpets & Area Rugs |

By Material

| Cotton |

| Linen |

| Synthetic Fibres |

| Other Materials (Wool, Hemp, Silk, Jute, Bamboo) |

By End-User

| Residential |

| Commercial |

By Distribution Channel

| B2C/Retail Channels | Mass Merchandisers (Hypermarkets/Supermarkets) |

| Home Centers | |

| Specialty Stores | |

| Local Mom and Pop Stores | |

| Online | |

| Other Distribution Channels | |

| B2B/Direct from the Manufacturers |

By Region

| North Germany |

| South Germany |

| East Germany |

| West Germany |

| Central Germany |

| By Application | Bed Linen | |

| Bath Linen | ||

| Kitchen Linen | ||

| Upholstery | ||

| Carpets & Area Rugs | ||

| By Material | Cotton | |

| Linen | ||

| Synthetic Fibres | ||

| Other Materials (Wool, Hemp, Silk, Jute, Bamboo) | ||

| By End-User | Residential | |

| Commercial | ||

| By Distribution Channel | B2C/Retail Channels | Mass Merchandisers (Hypermarkets/Supermarkets) |

| Home Centers | ||

| Specialty Stores | ||

| Local Mom and Pop Stores | ||

| Online | ||

| Other Distribution Channels | ||

| B2B/Direct from the Manufacturers | ||

| By Region | North Germany | |

| South Germany | ||

| East Germany | ||

| West Germany | ||

| Central Germany | ||

Key Questions Answered in the Report

What is the current value of the Germany home textile market?

The Germany home textile market stands at USD 6.87 billion in 2026 and is projected to reach USD 8.3 billion by 2031.

Which application is growing the fastest in German home textiles?

Bath linen leads growth with a forecast 4.48% CAGR, benefiting from wellness-oriented consumer spending.

How dominant is cotton in German home textiles?

Cotton accounts for 52.12% of 2025 revenue, yet alternative fibers such as hemp and recycled polyester are closing the gap.

Why are B2B channels expanding in GermanyÕs home textile sector?

Institutional buyers prefer direct sourcing to secure tailored specifications and mitigate supply-chain volatility, driving B2B sales to a 4.66% CAGR outlook.

Which German region shows the highest growth potential?

East Germany posts the fastest 5.05% CAGR through 2031, supported by new manufacturing investments and rising household incomes.

What major regulation will affect German textile suppliers after 2026?

EU Digital Product Passports will obligate each textile item to carry a detailed traceability QR code, raising compliance stakes for SMEs.

Page last updated on: