North America FMCG B2B E-commerce Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

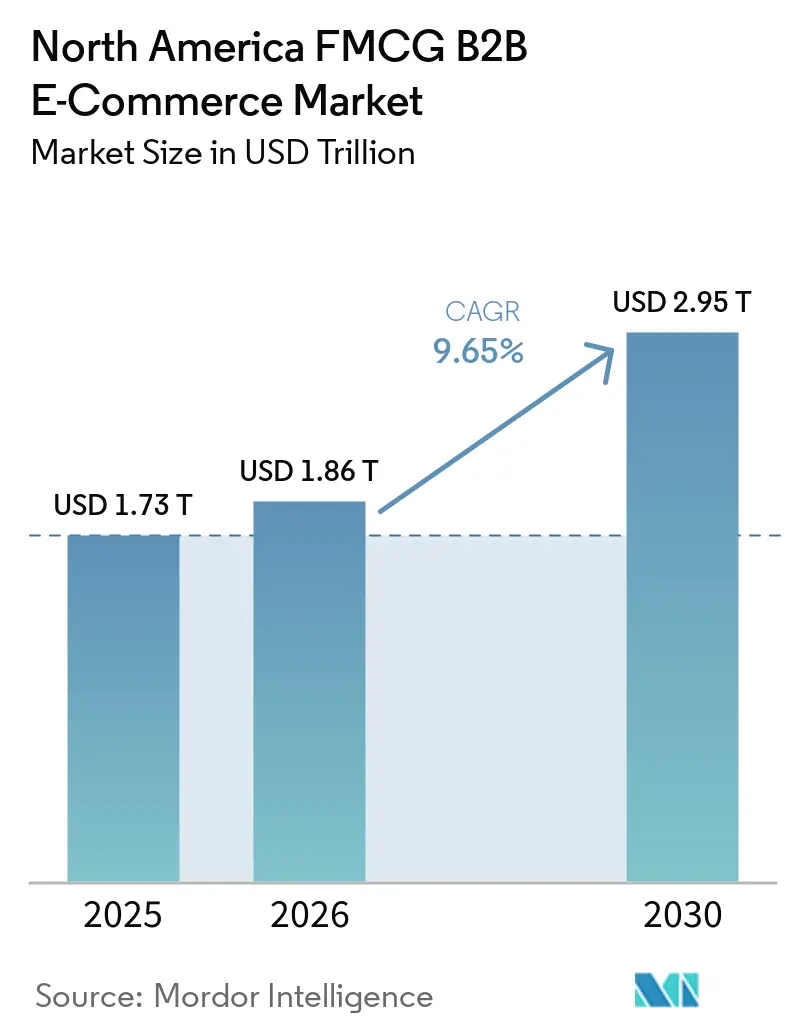

| Base Year Market Size (2025) | USD 1.73 Trillion |

| Market Size (2026) | USD 1.86 Trillion |

| Market Size (2030) | USD 2.95 Trillion |

| Growth Rate (2026 - 2031) | 9.65% CAGR |

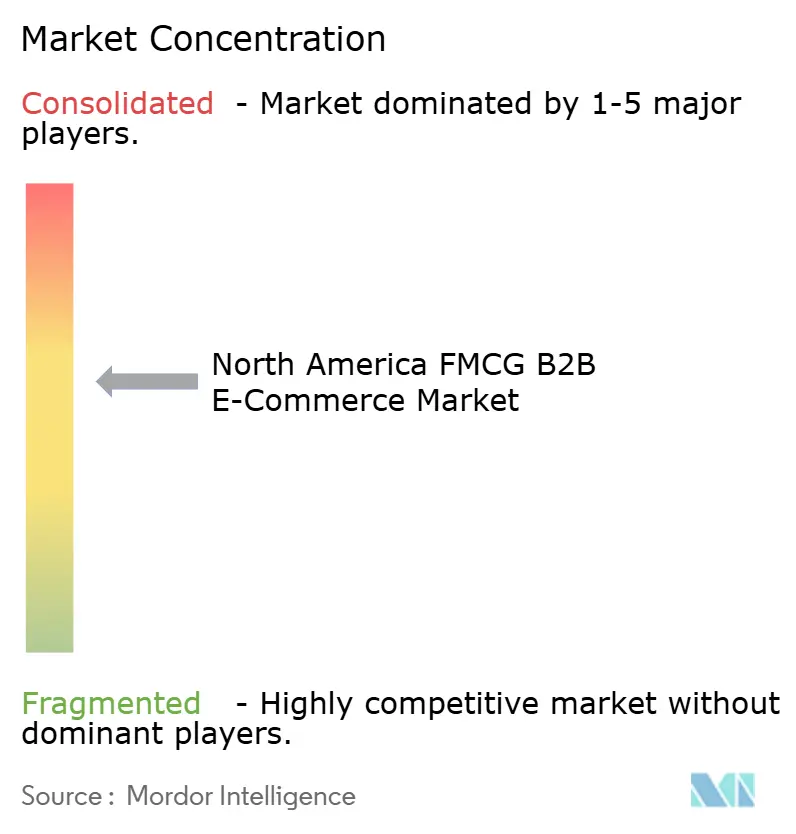

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America FMCG B2B E-commerce Market Analysis by Mordor Intelligence

The North America FMCG B2B E-commerce Market size is projected to expand from USD 1.73 trillion in 2025 and USD 1.86 trillion in 2026 to USD 2.95 trillion by 2030, registering a CAGR of 9.65% between 2026 to 2030.

Adoption of integrated EDI, API, and e-procurement workflows is scaling across large buyers as they centralize spend, standardize purchase-to-pay processes, and reduce manual order-entry costs. Regulatory traceability and serialization rules are pushing investments in EPCIS 2.0 event data, case-level visibility, and 24-hour records retrieval, which are now table stakes for distributors and suppliers handling regulated products. Embedded retail media offerings within B2B portals are generating high-margin revenue streams, improving closed-loop attribution at the point of order, supporting platform monetization, and differentiating the buyer experience. Platform incumbents are consolidating share as buyers migrate to self-service portals with contract pricing and integrated invoicing, while marketplaces continue to expand selection where legacy distributors lack breadth or digital depth. The North American FMCG B2B e-commerce market is also shaped by nearshoring and USMCA-aligned fulfillment, which tightens cross-border supply cycles and encourages bilingual, compliance-ready catalogs at scale.

Key Report Takeaways

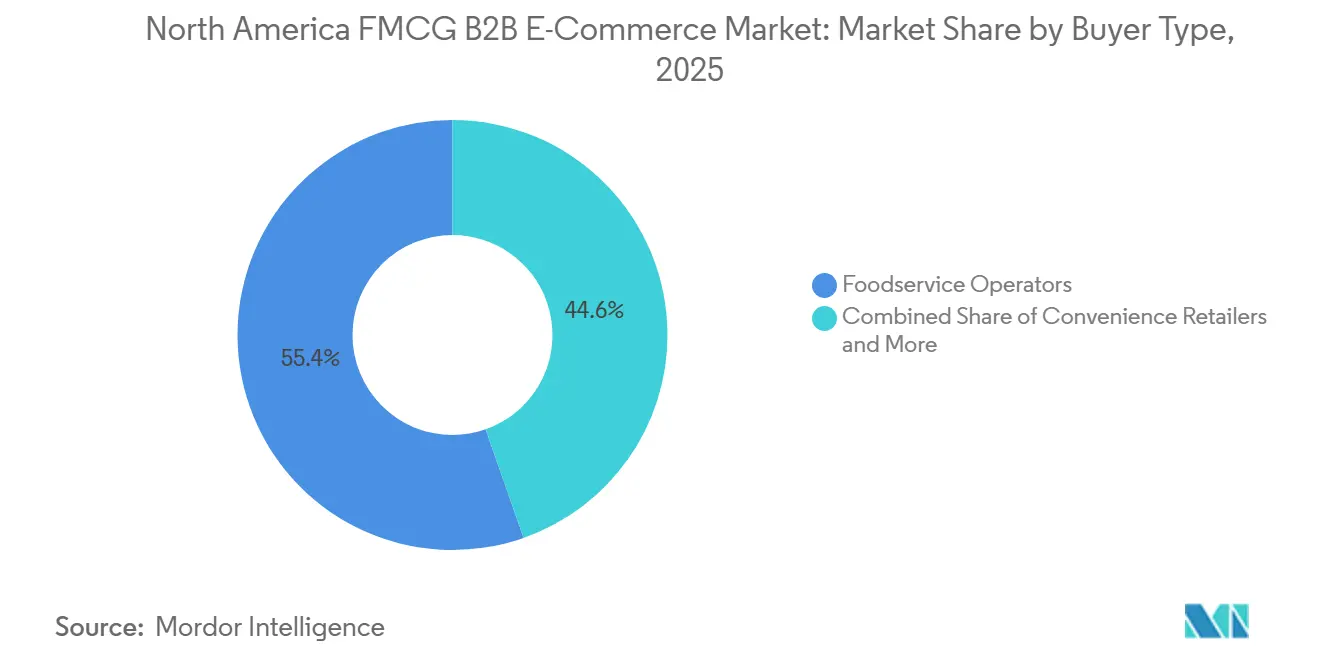

- By buyer type, foodservice operators led the North American FMCG B2B e-commerce market with 55.37% market share in 2025, and convenience retailers are projected to expand at a 12.76% CAGR through 2031.

- By product category, food and beverage accounted for 81.25% of the market share in 2025, while janitorial and sanitation supplies are forecast to grow at a 11.39% CAGR to 2031.

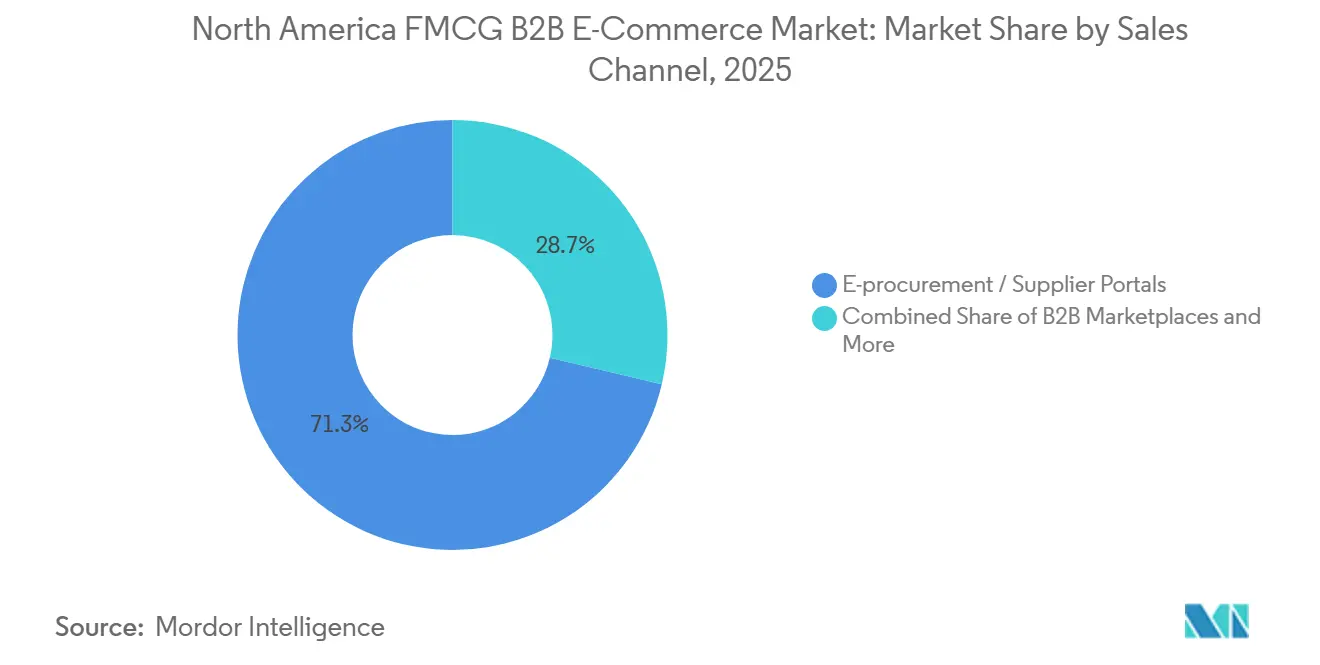

- By sales channel, e-procurement and supplier portals captured 71.33% share in 2025, and third-party B2B marketplaces are poised to grow at 18.53% CAGR through 2031.

- By geography, the United States held 91.62% of regional volume in 2025, and Mexico is projected to grow at a 13.29% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America FMCG B2B E-commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Automated replenishment via distributor EDI/API and e-procurement | +2.1% | United States core markets, expanding to Canada, early adopters in Mexico, tier-1 cities | Medium term (2-4 years) |

| Traceability and serialization mandates are speeding digital procurement | +1.8% | United States (FSMA, DSCSA), Canada (SFCR), with cross-border spillover effects | Short term (≤ 2 years) |

| Convenience and independent retail shift to distributor portals | +1.6% | United States independent grocers and convenience chains, Canada specialty retail | Medium term (2-4 years) |

| Retail media and trade-promo activation embedded in B2B checkout | +1.3% | United States broadline distributors, emerging in Canada and Mexico via platform rollouts | Medium term (2-4 years) |

| GS1/EPCIS 2.0 product data sharing for case-level visibility | +1.0% | Global standard, North America, early adopters in pharmaceuticals and fresh produce | Long term (≥ 4 years) |

| Automated tax-exemption and resale-certificate workflows | +0.7% | United States multi-state operations, Canada provincial tax harmonization zones | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Automated Replenishment via Distributor EDI/API and E-procurement Integrations

Broadline distributors scaled digital order capture as customers replaced phone and fax with portal, EDI, and API flows, which now sustain higher on-time order rates and fewer invoice disputes. Sysco completed its SHOP rollout and reports that 80% of orders now flow through the platform, strengthening contract-price enforcement and boosting purchase frequency through order guides [1]Sysco Corporation, “Investor Day 2024 Presentation,” Sysco Investor Relations, investors.sysco.com . Procurement suites expanded Punch-in and Punchout features so buyers can discover items in external catalogs and return cart data to native approval and PO creation, reducing rogue spend without shrinking SKU access. API-native EDI accelerates partner onboarding and improves real-time validation, reducing mapping errors before transmission and enabling event-driven updates for PO, ASN, and invoice milestones. These integrations reduce labor time, stabilize procurement controls, and increase reorder adherence at the point of need, supporting the North America FMCG B2B E-commerce Market as chain and independent buyers scale digital routines across locations.

Traceability/Serialization Mandates Speeding Digital Procurement (FSMA 204, DSCSA, CFIA)Traceability/Serialization Mandates Speeding Digital Procurement (FSMA 204, DSCSA, CFIA)

The FDA’s Food Traceability Rule requires electronic records of critical tracking events and key data elements for foods on the traceability list, with 24-hour retrieval, which is driving EPCIS-compliant capture, case-level identifiers, and searchable audit trails for high-risk items [2]United States Food and Drug Administration, “FSMA Final Rule on Requirements for Additional Traceability Records for Certain Foods,” United States Food and Drug Administration, fda.gov . EPCIS 2.0 improves standardized data exchange across suppliers, distributors, and retailers, and market-leading buyers are aligning serialization events with inbound receiving and outbound proof of delivery. Walmart’s EPCIS Events API processes and publishes serialization events, enabling suppliers to transmit packing, shipping, and transformation events into a tamper-evident ledger that supports faster recalls and root-cause analysis. The DSCSA enhanced dispenser and wholesaler deadlines in 2025 pushed package-level verification and authorized trading partner checks, while recent industry datasets and notices show uneven readiness among tracked entities. Heightened enforcement activity, including published warning letters in early 2026 for lack of serialization and slow verification response, is accelerating EPCIS adoption and transaction-data readiness across drug supply chains. Canada’s SFCR licensing and traceability requirements for food importers reinforce electronic documentation readiness and early license planning, which in turn influence how cross-border distributors plan renewals and compliance reviews.

Convenience and Independent Retail Shift to Distributor Portals for SKU Breadth and Labor Savings

Convenience retailers are projected to grow through 2031 as operators consolidate fragmented purchasing into distributor portals and e-procurement links that centralize spend and expand product access beyond cash-and-carry assortments. Punchout and punch-in integrations let buyers discover items in external catalogs and return carts to approval workflows and purchase-order creation, reducing manual ordering and invoice handling for small teams. Performance Food Group reports progress in specialty and convenience-oriented channels supported by digital capabilities through subsidiaries, reinforcing unified replenishment across food and facility items within a single ordering experience. Richer product data practices and standardized sharing improve B2B search and self-serve order creation, reducing sales-rep intervention during ordering and increasing conversion in long-tail categories. These digital workflows also align with traceability expectations and EPCIS 2.0 event exchange, thereby strengthening case-level visibility for regulated items and enabling faster audit retrievals. Together, these factors sustain category breadth for small-format retailers while keeping distributors' cost-to-serve in line in the North American FMCG B2B e-commerce market.

Retail Media and Trade-Promo Activation Embedded in B2B Checkout

Walmart reported USD 4.4 billion in global advertising revenue for fiscal 2025, up 27% year over year, with Walmart Connect in the United States up 24%, underscoring the rise of retail media economics that can be embedded in B2B portals targeting procurement managers at the moment of cart creation. The company highlighted Walmart Connect's 33% growth in Q3 fiscal 2026, signaling strong advertiser demand for promoted search results, category placements, and order-confirmation upsells within business-facing storefronts. Advertisers are shifting budgets toward retail media for closed-loop attribution, with 52% reporting a reallocation from open-web DSPs to retail media DSPs in 2026, which aligns promotion exposure with verified purchase outcomes. Direct-to-retailer platforms such as Pepperi support front-of-order activation with tiered volume discounts, bundles, gifts with purchase, and real-time shipping calculations, which reduces reliance on post-invoice rebates and manual claim reconciliation. These capabilities transform portals into activation channels that complement field sales, boosting conversion and average order value in the North American FMCG B2B e-commerce market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cold-chain MOQs and handling fees constrain small-basket economics | -0.9% | United States cold-chain corridors and Canada perishables distribution | Short term (≤ 2 years) |

| Fragmented EDI/API standards across wholesalers slow integrations | -0.7% | United States multi-distributor buyers and cross-border Canada-Mexico integrations | Medium term (2-4 years) |

| SKU data quality and item-master inconsistencies reduce B2B search and conversion | -0.6% | United States independent retail and Canada bilingual cataloging | Short term (≤ 2 years) |

| Tight net terms and credit underwriting slow SMB buyer conversion | -0.5% | United States convenience chains and Mexico SMB grocers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cold-Chain MOQs and Handling Fees Constrain Small-Basket Economics

Cold-chain distribution imposes minimum order quantities and accessorial fees that limit the viability of small baskets, which discourages digital replenishment for low-volume buyers. Common surcharges for multi-stop routes include layover, detention, truck-order-not-used, and extra stop fees that quickly add to landed costs for perishable shipments. Warehouse storage rates vary by temperature band and service level, with premium pricing for the frozen and ultra-low temperature ranges that put pressure on margins for sensitive categories. Reefer rates fluctuate with seasonality and equipment availability, and summer harvest windows tend to raise per-mile costs relative to winter baselines, narrowing the ROI on long-tail SKUs. Dock appointment bottlenecks compound the risk of temperature excursions during high-volume periods, potentially shortening shelf life and increasing spoilage claims for buyers and distributors. Pilots that automate appointment booking with AI agents show improved slot coverage and material time savings, which lowers dwell time and improves cold-chain reliability for order cycles.

Fragmented EDI/API Standards Across Wholesalers Slow Integrations

Integration patterns differ by supplier portal and procurement platform, which forces buyers to support multiple protocols and partner-specific mappings across their distributor network. Many high-volume transactions remain EDI-based to leverage reliability at scale, while APIs now deliver real-time agility for inventory and order-status updates at the customer edge. Modern providers emphasize API-first or API-hybrid approaches that shorten onboarding and improve automated validation, yet complex partner logic and protocol variance can extend deployment timelines. Middleware and managed services absorb translation and security differences, though buyers still manage rate limits, payload caps, and authentication requirements that vary by endpoint. The net effect is a slower time-to-value for multi-distributor rollouts, which tempers digital penetration among smaller buyers who lack IT support and funding. As API maturity improves and standards converge, these obstacles should ease, but near-term friction remains a headwind for the North America FMCG B2B E-commerce Market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Buyer Type: Independents Force Shifts as Chains Deploy Self-Serve

Foodservice operators accounted for 55.37% of buyer-type share in 2025 as digital adoption by independent restaurants and multi-location chains drove higher order cadence and fuller baskets, while convenience retailers are projected to grow at 12.76% CAGR to 2031 as mobile ordering and portal access expand assortments beyond core staples. Sysco, which completed its SHOP rollout, reports that 80% of orders are now placed through its digital platform. This level reinforces contract governance and simplifies repeat purchasing for operators that manage rotating menus and seasonality. Dispensers and pharmacies continue to align with DSCSA milestones, which sustains investments in EPCIS-based verification and ATP checks across wholesale and dispenser networks [3]Healthcare Distribution Alliance, “The Distribution Industry at the Nexus of DSCSA Implementation,” Healthcare Distribution Alliance, hda.org . Large institutions consolidate food, beverage, and facility needs into unified orders to reduce receiving windows and simplify accounts payable, which encourages more buyers to adopt e-procurement punchout and approval flows that keep purchases within policy. These shifts support stability in repeat categories and better long-tail access for independent retailers that rely on distributor portals to substitute for in-person cash-and-carry trips in the North America FMCG B2B E-commerce Market.

Independent retail and foodservice buyers value full-catalog visibility, real-time pricing, and tighter receivables workflows, which bring control and speed without reducing selection. Pharmacy and healthcare buyers increasingly rely on item-level serialization, which heightens the need for secure data exchange and compliant audit trails across trading partners. Institutional purchasers pull facility and pantry items into the same carts used for fresh, frozen, and ambient food procurement. This pattern pushes platforms to standardize master data across categories and improve unified category navigation. These account patterns amplify network effects for platforms that serve chains and independents across foodservice, convenience, and specialty retail, which strengthens the North America FMCG B2B e-commerce industry’s baseline of recurring digital spend.

By Product Category: Janitorial Gains Defy Food Dominance

Food and beverage held 81.25% of product-category share in 2025, while janitorial and sanitation supplies are projected to grow at 11.39% CAGR through 2031 as institutional buyers centralize facility-supply procurement on the same systems used for food orders. Specialty distributors and redistributors broadened adjacent categories such as vending, theater, and office coffee service, which add scale even with lower per-case margins than fresh or frozen food. Household, paper, and cleaning supplies benefit from repeat-purchase patterns and predictable par levels, which increase the value of automated replenishment and SKU-level recommendation engines. OTC health and wellness, personal care, and pet continue to benefit from cross-selling at checkout, where portals prompt logical complements that raise average basket values. Baby and family care require careful handling for select items, which rewards platforms with temperature-controlled logistics and reliable appointment scheduling in the North American FMCG B2B e-commerce market.

Broader category coverage requires consistent taxonomy and attribute data so buyers can filter by compliance needs and packaging constraints, thereby improving search relevance and increasing conversion. Janitorial and sanitation growth aligns with accounts that prefer fewer inbound deliveries and easier AP matching, so facility supplies migrate into existing food orders and replace stand-alone vendors. This shift also encourages suppliers of facility consumables to integrate via EDI and API connections, reducing catalog maintenance costs and improving invoice accuracy. Food’s anchor role continues, but adjacent categories now ride the same digital rails and benefit from unified order guides and saved lists that span locations across the North American FMCG B2B e-commerce industry.

By Sales Channel: Marketplaces, Chip at Portal Dominance

E-procurement and supplier portals captured 71.33% of channel share in 2025, while third-party B2B marketplaces are forecast to grow at a 18.53% CAGR through 2031, as independent retailers source emerging brands not carried by every broadline distributor. Punch-in and punchout integrations support enterprise control of tail spend while retaining selection, keeping carts within approval chains, and producing clean POs and matched invoices. Retail media monetization within portals supports sponsored listings and targeted promotions at the point of order, helping lift advertising revenue growth as e-commerce expands rapidly. Distributor portals strengthen switching costs through order guides, contract pricing, and ERP integrations, which makes marketplaces more complementary than substitutive for many established accounts. Direct supplier portals add value for promotional or limited-release SKUs. At the same time, daily replenishment tends to remain with distributors that aggregate orders and manage temperature-controlled logistics at scale in the North America FMCG B2B E-commerce Market.

Marketplaces continue to expand services with credit options and discovery features for new brands, which can raise first-order conversion for long-tail assortments. Enterprise buyers blend marketplace discovery with tight e-procurement control as integrations capture carts, enforce policies, and reconcile AP at speed. Platforms that deliver both a broad selection and high data quality improve search-to-purchase efficiency, which is increasingly a competitive differentiator across channels. As marketplace curation strengthens and portal UX continues to improve, buyers benefit from stable pricing, faster reorders, and real-time visibility into inventory constraints. These channel dynamics, reinforced by retail media and data-driven merchandising, support sustained growth in the North America FMCG B2B E-commerce Market.

Geography Analysis

The United States accounted for 91.62% of regional volume in 2025, supported by broadline distributor scale and rapid digital adoption, which increased the share of orders flowing through portals and integrated procurement links. Sysco’s digital execution through SHOP underscores the importance of customer-specific order guides and contract enforcement for repeat categories, which are central to United States account retention and SKU penetration. Retail media momentum, faster e-commerce delivery expectations, and growing AI-enabled procurement experiences have also set new baselines for platform engagement and monetization. FSMA 204 and DSCSA readiness pressures are higher in the United States due to strict timelines and active enforcement, so suppliers and distributors are building EPCIS event capture into standard receiving and shipping processes. These forces reinforce digital migration and solidify the North America FMCG B2B E-commerce Market’s United States anchor as buyers scale standardized purchase flows across banners and locations.

Canada’s share is smaller but is building on cross-border procurement links that benefit from USMCA frameworks and clearer importer licensing requirements under the SFCR. Bilingual labeling and Quebec’s French prominence rules add catalog governance costs, thereby increasing the value of centralized master-data stewardship across distributors serving multiple provinces. Enterprise buyers blend United States and Canadian procurement through approved supplier programs and tax-exemption workflows that simplify onboarding across jurisdictions, benefiting platforms with strong certificate management and API validation features. Category expansion into facility supplies and OTC items also encourages Canadian buyers to use unified carts and consolidated approvals, which keeps adoption rising within accounts already using portals for food and beverage. As platform vendors invest in localized compliance and content, Canada contributes incremental growth and supports the broader stability of the North American FMCG B2B e-commerce market.

Mexico is projected to grow at 13.29% CAGR through 2031 as nearshoring compresses transit timelines and cross-border flows support replenishment demand inside Mexico and for United States-bound goods. Digital procurement adoption in tier-1 cities and selected corridors is gaining traction as bilingual platforms and localized tax workflows reduce onboarding friction for SMB buyers. Partnerships that enable flexible payment options reduce cash-flow barriers and bring more small retailers into compliant digital channels. As buyer familiarity with portals grows and distributors localize their assortments, Mexico’s contribution to the North America FMCG B2B E-commerce Market should increase, led by convenience and small-format retail, which benefit most from digital order guides and curated discovery. Over time, improvements in data quality, credit tools, and logistics will continue to reduce the gap with the United States and Canada and support long-run growth in the region.

Competitive Landscape

The competitive core includes broadline distributors that aggregate tens of thousands of SKUs across ambient, chilled, frozen, and facility supplies and that embed contract pricing, order guides, and EDI/API connections into buyer workflows. The top five distributors held a significant share in 2025, while regional specialists remain important for independents, natural and organic channels, and selected geographies that demand localized service and assortment. Strategy focus spans digital order penetration, retail media monetization, and data-driven recommendations at checkout, which are now central to share defense. Sysco’s digital execution illustrates how embedded order guides and account-specific curation insulate relationships from marketplace substitution in the North America FMCG B2B E-commerce Market.

Retailers with business divisions and at-scale marketplaces expand the competitive set by leveraging consumer-grade search and last-mile networks to target procurement managers and SMB buyers. Walmart’s recent performance highlights strong e-commerce growth and expanding retail media revenue, and its acquisition of VIZIO strengthens its connected-TV ad inventory, linking promotion to conversion. Amazon Business partnerships with leading procurement suites integrate discovery into formal approval and PO creation, which channels tail spend into compliant flows while retaining selection and speed. These moves reinforce a dual-front competitive dynamic in the North American FMCG B2B e-commerce market, in which portals defend core accounts and marketplaces capture emerging brand discovery and long-tail demand.

M&A and category expansion continue as distributors strengthen regional density and add adjacent categories to deepen wallet share. Performance Food Group’s acquisition strategy broadened specialty channels and extended geographic reach, which supports scale economics and incremental category penetration. Platforms are also rolling out AI-enabled scheduling, route optimization, and anomaly detection to improve logistics efficiency and working capital, while serialized data capture supports recall readiness and customer trust. The net effect is a market where technology maturity, compliance readiness, and retail media capabilities are now decisive for share gain and customer retention across the North America FMCG B2B E-commerce Market.

North America FMCG B2B E-commerce Industry Leaders

Amazon Business

Walmart Business

Sysco Shop

US Foods

United Natural Foods (UNFI)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Avalara launched AI-powered exemption-certificate management that uses OCR and large language models to review certificate accuracy, track expirations, and validate tax IDs across common forms.

- September 2025: United States Cold Storage piloted an AI booking agent with FourKites that achieved 87% automation success and high accuracy for requested delivery dates, saving dozens of hours during an eight-week test.

- June 2025: Amazon Business expanded Business Prime benefits, including spend anomaly monitoring and higher user limits across membership tiers, to extend procurement control and visibility for enterprise accounts.

- October 2024: Performance Food Group completed the acquisition of Cheney Brothers, adding regional scale and strengthening specialty distribution capabilities.

North America FMCG B2B E-commerce Market Report Scope

| Independent grocery & specialty retailers |

| Chain supermarkets & mass merchandisers |

| Convenience stores & gas stations |

| Foodservice/HoReCa (restaurants, cafes, catering) |

| Pharmacies & drugstores |

| Online-only and quick-commerce resellers |

| Institutional, office & janitorial buyers |

| Other Buyers |

| Food & beverage |

| Household & cleaning |

| Personal care & beauty |

| OTC health & wellness |

| Pet care |

| Baby & family care |

| Other Products |

| Distributor-managed portals |

| CPG/supplier-direct portals |

| Third-party B2B marketplaces |

| E-procurement/API/EDI-integrated |

| United States |

| Canada |

| Mexico |

| By Buyer Type | Independent grocery & specialty retailers |

| Chain supermarkets & mass merchandisers | |

| Convenience stores & gas stations | |

| Foodservice/HoReCa (restaurants, cafes, catering) | |

| Pharmacies & drugstores | |

| Online-only and quick-commerce resellers | |

| Institutional, office & janitorial buyers | |

| Other Buyers | |

| By Product Category | Food & beverage |

| Household & cleaning | |

| Personal care & beauty | |

| OTC health & wellness | |

| Pet care | |

| Baby & family care | |

| Other Products | |

| By Sales Channel/Platform Type | Distributor-managed portals |

| CPG/supplier-direct portals | |

| Third-party B2B marketplaces | |

| E-procurement/API/EDI-integrated | |

| By Geography (North America) | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the North America FMCG B2B E-commerce Market growth outlook through 2031?

The market is set to reach USD 2.95 trillion by 2031, growing at a 9.65% CAGR over 2026-2031, supported by procurement integrations, compliance mandates, and retail media monetization.

Which buyer segments are leading digital adoption in North America FMCG B2B e-commerce?

Foodservice operators lead in 2025 share, while convenience retailers are the fastest growing through 2031 as portals and mobile ordering expand selection and reduce labor time.

How are regulations influencing platform investments in this space?

FSMA 204 and DSCSA are accelerating EPCIS 2.0 adoption, electronic records readiness, and package-level verification, which raise baseline compliance and data standards for trading partners.

Which channels are gaining share in the North America FMCG B2B E-commerce Market?

E-procurement and supplier portals hold the largest share, while third-party B2B marketplaces are the fastest growing as they bring emerging brands and net terms to SMB buyers.

What capabilities differentiate leading platforms in North America FMCG B2B e-commerce?

Strong EDI/API integrations, retail media activation, EPCIS traceability, AI-enabled search, and automated tax-exemption management are the most cited differentiators for conversion and retention.

How does retail media influence B2B procurement outcomes?

Retail media networks inside portals let brands target procurement managers at order creation, which lifts promoted item visibility and drives closed-loop attribution alongside growing ad revenue.

Page last updated on: