Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

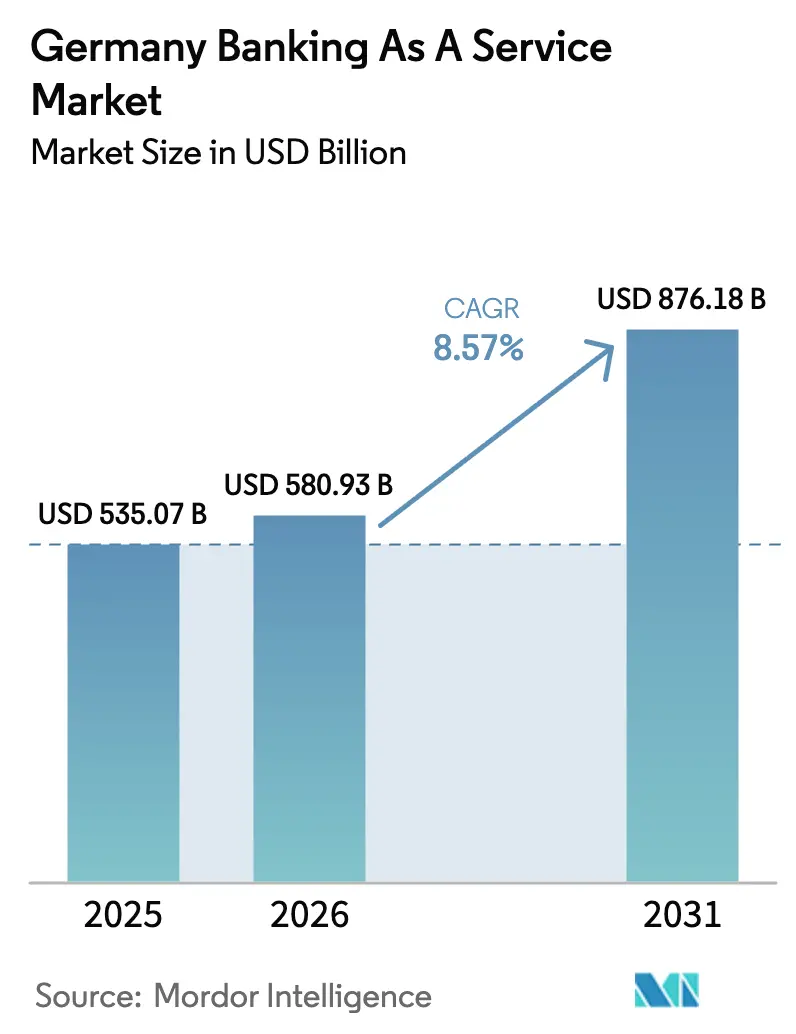

| Base Year Market Size (2025) | USD 535.07 Billion |

| Market Size (2026) | USD 580.93 Billion |

| Market Size (2031) | USD 876.18 Billion |

| Growth Rate (2026 - 2031) | 8.57% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Banking As A Service Market Analysis by Mordor Intelligence

The Germany Banking As A Service Market size is projected to be USD 535.07 billion in 2025, USD 580.93 billion in 2026, and reach USD 876.18 billion by 2031, growing at a CAGR of 8.57% from 2026 to 2031.

The uptrend aligns with policy-led openness under PSD2, broader enterprise migration to cloud infrastructure, and rapid adoption of embedded finance across non-bank platforms that distribute payments, lending, cards, and wallets via APIs. Operational scrutiny is rising as BaFin flags concentration and outsourcing risks as a supervisory priority for 2026 to 2029, elevating resilience requirements for BaaS providers at scale. The EU Instant Payments Regulation mandates 10-second settlement for euro credit transfers from October 9, 2025, which compresses processing windows and reshapes platform designs for real-time liquidity, reconciliation, and verification of payee checks. MiCAR is fully applicable since December 30, 2024, and expands custody and compliance obligations, pushing BaaS platforms to support crypto-asset services with rigorous operational, IT, and investor-protection controls.

Germany’s BaaS trajectory benefits from high digital adoption, strong bank-FinTech collaboration, and deep SME demand for modular financial services. FinTech adoption among German consumers sits above the EU average, supported by active e-commerce and SaaS ecosystems that embed payments, card issuing, and lending for conversion and retention gains.

Key Report Takeaways

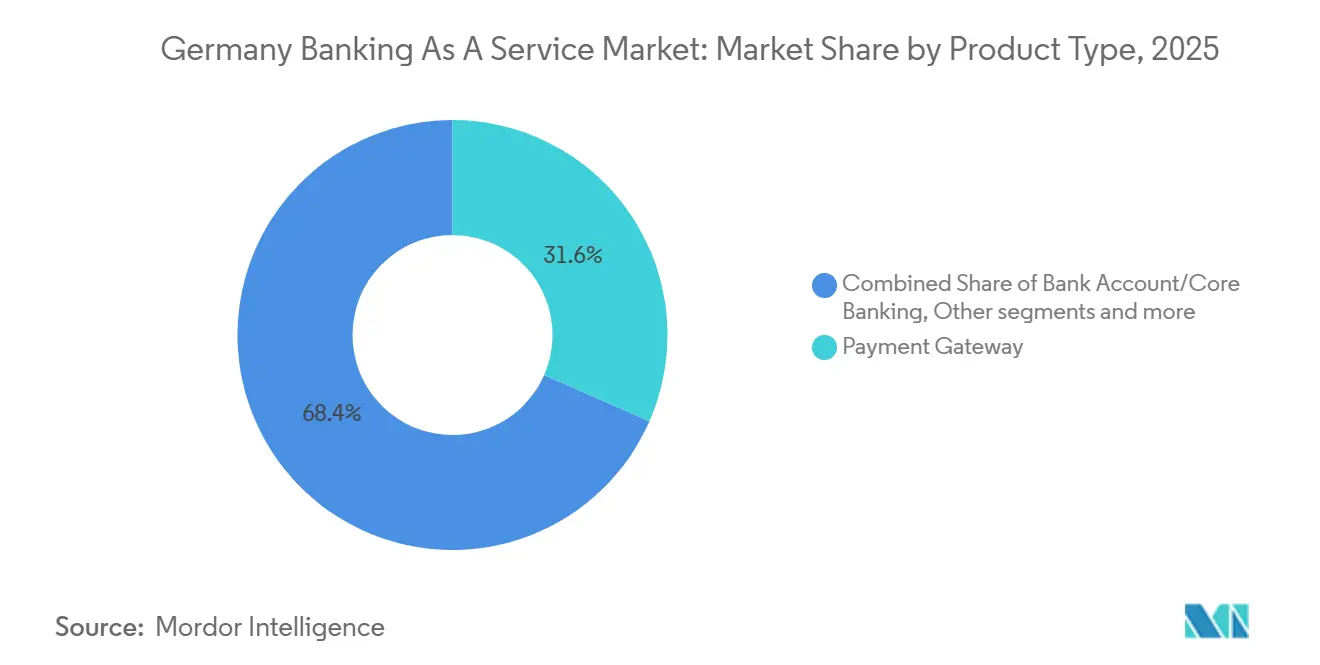

- By product type, payment gateways led the Germany Banking as a Service market with a 31.56% revenue share in 2025, while embedded finance software is forecast to expand at a 12.34% CAGR through 2031, the fastest pace in this segmentation.

- By enterprise size, large enterprises held a 60.07% share of the Germany Banking as a Service market in 2025, while small and medium enterprises are projected to record a 10.95% CAGR through 2031.

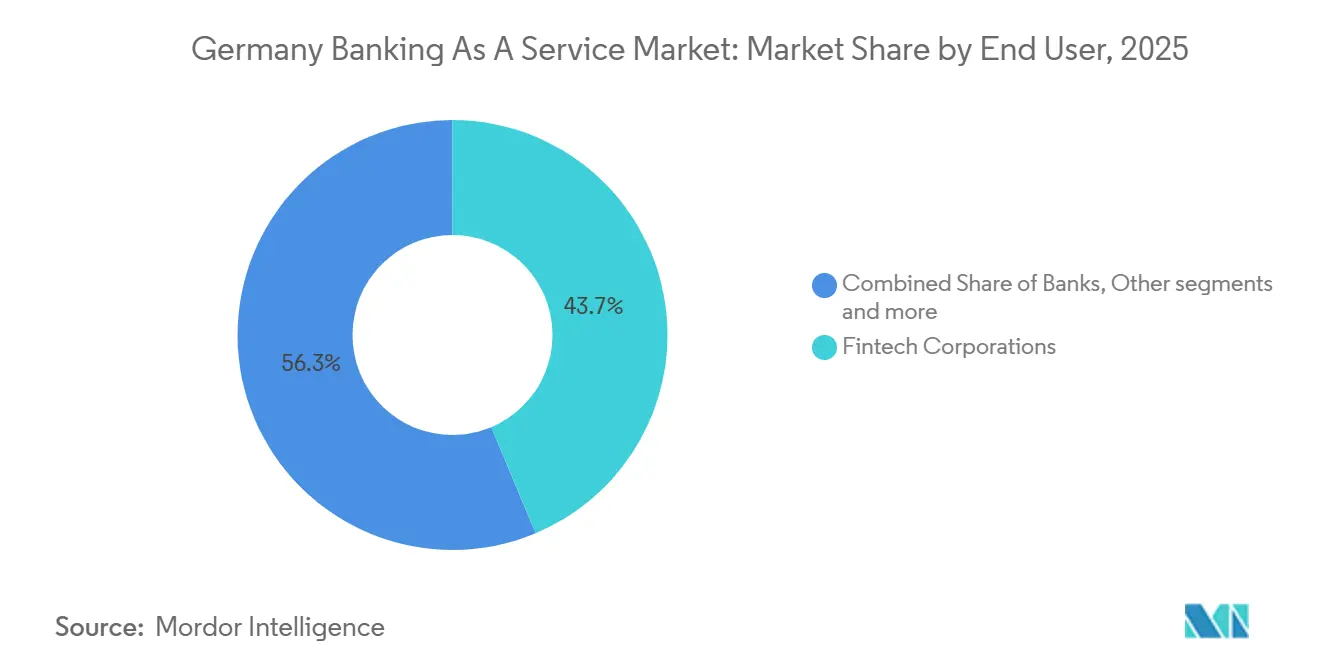

- By end user, FinTech corporations accounted for a 43.67% share of the Germany Banking as a Service market in 2025 and are expected to grow at a 13.83% CAGR through 2031.

- By component, platform and infrastructure solutions commanded 53.46% of the Germany Banking as a Service market in 2025, while services are set to advance at a 14.86% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Banking As A Service Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for digital banking and seamless online financial services | +1.8% | National, concentrated in urban hubs (Berlin, Munich, Frankfurt) | Short term (≤ 2 years) |

| Expansion of FinTechs and embedded finance models | +2.1% | Global, with spillover from German e‑commerce and SaaS ecosystems | Medium term (2-4 years) |

| Open banking momentum under PSD2 enabling API innovation | +1.5% | EU‑wide, amplified in Germany due to strong regulatory enforcement | Medium term (2-4 years) |

| Growing adoption of cloud‑based infrastructure | +1.9% | National, with higher traction in the Mittelstand segments | Medium term (2-4 years) |

| Advanced digital infrastructure and strong technology adoption | +0.7% | National, concentrated in major financial centers | Short term (≤ 2 years) |

| Emphasis on personalized, data‑driven customer experiences | +0.6% | National, with higher adoption in retail and e‑commerce | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Digital Banking Services

FinTech service usage in Germany reached an adoption level of 75%, surpassing the European average of 64%, while legacy banks retain deposit primacy and FinTechs dominate transactional interfaces, which together create fertile ground for modular BaaS integrations that improve time to market and unit economics[1]Germany Trade & Invest, “FinTech in Germany,” GTAI, gtai.de. The EU Instant Payments Regulation requires all payment service providers to offer euro credit transfers settling within 10 seconds on a 24/7 basis from October 9, 2025, which compels BaaS platforms to implement real-time liquidity, verification of payee, and continuous risk monitoring. The new regime also enables payment and e-money institutions to compete more directly in instant settlement, narrowing the historic advantage held by banks on clearing and reconciliation windows. Online banking usage in the EU reached 72% of internet users in 2024, up from 56% in 2014, creating a stable behavioral base for end-to-end digital services that BaaS providers can modularize and scale. The German Banking as a Service market internalizes these adoption curves as companies re-platform payments and accounts to meet real-time commitments and higher UX standards.

Expansion of FinTechs and Embedded Finance Models

Germany counts 3.6 million SMEs, representing 99% of all enterprises, which widens the addressable base for embedded payments, invoicing, and working capital delivered through partner platforms that do not seek banking licenses. Only 35% of businesses completed digitalization projects in recent years, indicating untapped demand for BaaS-enabled solutions that compress onboarding and lower integration barriers for resource-constrained firms. Aggregate digitalization expenditure by German SMEs reached EUR 31.9 billion in 2023 and grew 54% versus 2019, which aligns with higher investment in APIs, data, and cloud architectures that often bundle embedded finance modules[2]KfW Research, “KfW SME Digitalisation Report 2024,” KfW, kfw.de. Two-thirds of FinTech revenue in Germany stems from B2B business models, reinforcing the shift from direct to consumer plays toward infrastructure and enablement services. The Germany Banking as a Service market is the operating layer behind this shift, enabling software providers, marketplaces, and merchants to embed compliant financial workflows without full-stack rebuilds.

Open Banking Momentum Under PSD2

PSD2 continues to shape collaboration patterns between incumbent banks and FinTechs, yet the quality of APIs and bank responsiveness varies across markets, which affects innovation throughput and consistency of data access. Germany maintained a high density of licensed institutions within the EU, with broad availability of credit institutions and payment service providers enabling a mix of partnership-led and competitive models for BaaS adoption. Deutsche Bank launched Wero on December 17, 2025, integrating a European Payments Initiative digital wallet into its mobile app to provide a sovereign alternative to non-European wallet ecosystems and to add P2P functionality. ClearBank secured an EU banking license in July 2024 and onboarded German FinTech Raisin by year's end, showing how regulatory passports channel cross-border infrastructure competition into Germany. The Eurosystem’s near-term plan to link DLT platforms with TARGET services by the end of Q3 2026 through a bridging model known as Pontes creates central bank money settlement pathways that could decrease reliance on private stablecoins for institutional flows.

Growing Adoption of Cloud-Based Infrastructure

BaFin highlights the risks arising from IT outsourcing concentration as a supervisory focus, indicating that cloud reliance will be scrutinized across resilience, continuity, and multi-client dependencies in BaaS arrangements. Three U.S. providers account for nearly 70% of the European cloud market, and German providers have small shares, which raises concerns over sovereignty and operational dependencies as BaaS transaction volumes scale. Germany’s cloud computing performance rose sharply, with 2025 metrics signaling a strong step-up versus 2024 and long-term gains since 2018, which supports migration to cloud-native core and payments stacks. Solaris selected ACI Connetic in September 2025 to consolidate SEPA Instant payments onto a cloud-native architecture, an example of horizontal scaling to meet the incoming instant payments load. SME credit constraints remain elevated, which underpins demand for BaaS-enabled underwriting that uses transactional data for faster decisions while maintaining compliance and controls.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory environment and PSD2 compliance | -1.2% | National, with spillover across EU passporting | Long term (≥ 4 years) |

| GDPR-led data protection and privacy requirements | -0.9% | EU-wide, amplified in Germany | Medium term (2-4 years) |

| System integration complexity with legacy IT | -0.6% | National, older technology stacks | Medium term (2-4 years) |

| Intense competition from banks and well-funded FinTechs | -0.5% | National and cross‑border within EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Environment, Including BaFin Supervision and PSD2 Compliance

BaFin shortened the formal authorization timeline to six months from a complete application, yet applicants must still present a viable business model, a minimum initial capital of at least EUR 5 million for deposit and lending institutions, and fit and proper management, which raises entry thresholds for new providers. MiCAR applies fully since December 30, 2024, requiring crypto-asset service providers to demonstrate robust governance, IT resilience aligned with DORA, and investor protection standards, resulting in parallel authorizations for BaaS platforms that add digital asset modules. Supervisors face tight statutory deadlines for MiCAR applications, and incomplete or inconsistent submissions must be rejected, which elevates legal and technical preparation costs[3]BaFin, “Banking business,” BaFin, bafin.de. BaFin’s focus on operational resilience, including concentration risks and cross-border interdependencies across service providers, expands mapping and monitoring requirements for BaaS operators with multi-client footprints. The Instant Payments Regulation requires verification of payee services at no extra charge from October 9, 2025, so platforms must absorb implementation costs into their operating models.

Heightened Data Protection and Privacy Requirements Under GDPR

Fraudulent payment transactions in the EEA reached EUR 4.2 billion in 2024, a 17% rise over 2023, even as overall fraud rates stayed near 0.002% of transaction value, which forces BaaS providers to balance frictionless UX with strong authentication mandates. Credit transfer fraud accounted for EUR 2.5 billion in losses in 2024, with payment service users bearing 85% due to social engineering, elevating expectations for identity verification and behavioral analytics. BaFin intensified AML supervision in 2025 and increased on-site inspections, which translates into higher compliance and technology spending for platforms conducting high-volume onboarding and monitoring. Card payment fraud was 17 times higher when the counterpart was outside the EEA, adding cross-border complexities for BaaS providers serving international customers. The instant payments shift reduces monitoring windows from days to seconds, pushing investments in streaming analytics, model retraining, and real-time alerting so that BaaS platforms can mitigate loss while preserving user experience.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Embedded Finance Software Captures Fastest Expansion

Payment gateways held a 31.56% share in 2025 within the product-type segmentation, while embedded finance software is projected to expand at a 12.34% CAGR through 2031, signaling a sustained mix shift as merchants and SaaS platforms fold payments and credit into user journeys. Payment processing faces margin compression as instant settlement becomes a baseline requirement, which lifts the appeal of higher value modules across lending, insurance, and wealth features that can be orchestrated through APIs. Bank account and core banking solutions continue as the foundational ledger and compliance layer for account issuance and reporting, although their growth is tempered by strong competition and strict prudential expectations around capital and governance. The German Banking as a Service market benefits from the scale of card and account transactions, which allows providers to upsell analytics, reconciliation, and fraud modules on top of base rails.

Comparing digitalization momentum among German businesses with the 2026-2031 outlook suggests stronger embedded finance adoption as liability frameworks mature and API standards harmonize, making integration more predictable for enterprise teams. Distribution channels broaden as EPI’s Wero rollout places a bank-owned wallet into consumer flows, which can be white labeled or integrated with merchant experiences over time. Euro area card transactions reached 44.3 billion in H2 2024, up 11.3% year on year, reinforcing the scale case for modular card issuance and tokenized credentials. MiCAR’s full applicability increases demand for compliant custody and token transaction monitoring within gateway and wallet stacks, extending the functional scope of product categories in the German Banking as a Service market.

By Enterprise Size: SME Segment Growth Outpaces Large-Enterprise Adoption

Large enterprises held a 60.07% share in 2025 due to larger budgets and bespoke integration capacity, while SMEs are projected to grow at a 10.95% CAGR through 2031, reflecting both falling integration costs and a sharper need for automated onboarding that compresses time to cash. The German Banking as a Service market size allocated to SME targeted solutions is set to expand as credit constraints and real-time payment mandates steer businesses toward pre-integrated payment, invoicing, and working capital APIs. Germany’s 3.6 million SMEs represent 99% of enterprises, yet only 35% report recent digitalization completion, which implies sizeable white space for turnkey BaaS suites that are lighter to adopt.

Large enterprises emphasize treasury, cross-border flows, and corporate card programs, with early pilots for blockchain-based settlement complementing traditional rails[4]European Central Bank, “Payments statistics: second half of 2024,” European Central Bank, ecb.europa.eu. SMEs value single API coverage of payment acceptance, invoicing, and cash cycle financing, lowering the burden on thin IT teams while raising integration velocity. Investor attention in 2025 favored infrastructure and enablement categories over consumer brands, consistent with Germany attracting USD 1.0 billion in FinTech investment across 149 deals and ranking third in Europe. As adoption leaves the early adopter cohort, the Germany Banking as a Service industry will likely standardize integration and compliance pathways to lower SME switching costs while fulfilling BaFin’s resilience expectations.

By End User: FinTech Corporations Drive Adoption Velocity

FinTech corporations held a 43.67% share in 2025 and are expected to expand at a 13.83% CAGR through 2031, reflecting their reliance on modular banking components to accelerate rollouts across payments, accounts, cards, and wallets. Banks increasingly use BaaS for non-core outsourcing such as card issuance and FX settlement, though legacy architectures and change-management constraints can slow programs relative to FinTech timelines. Non-bank end users, including e-commerce and SaaS platforms, embed financial features to monetize customer touchpoints and create recurring revenue streams.

Germany attracted USD 1.0 billion in FinTech investment across 149 deals in 2025, with a greater share directed to infrastructure and enablement, which validates the BaaS platform thesis. Solaris raised EUR 140 million in February 2025 to support operational transformation and onboarding, underscoring continued capital access for regulated platform providers serving FinTech demand. ClearBank onboarded multiple EU clients after securing an EU license in July 2024, demonstrating that cross-border BaaS can scale quickly once authorization is complete. Two-thirds of German FinTech revenue is B2B, which reinforces the role of BaaS APIs in enabling faster pivots and product extensions for clients. The Germany Banking as a Service market share held by banks remains important in specialized services such as liquidity and regulatory reporting, but FinTechs absorb platform changes faster due to agile delivery cultures.

By Component: Services Layer Emerges as Faster-Growing Revenue Stream

Platform and infrastructure solutions commanded 53.46% of the Germany Banking as a Service market share in 2025 across account provisioning, payment rails, and ledgers, while services spanning compliance, KYC, and fraud detection are projected to expand at a 14.86% CAGR through 2031, outpacing platforms as regulatory complexity deepens. This gap reflects the growing monetization of compliance modules, as enforcement actions and AML inspections raise the bar for conduct, disclosures, and operational controls. The German Banking as a Service market size tied to services should benefit from real-time fraud controls and verification mandates that carry low latency requirements under instant payments.

Platform providers continue bundling services to protect margins and reduce churn, as shown by Solaris selecting ACI Connetic for SEPA Instant on a cloud-native stack in September 2025. Fraud prevention services command premium pricing because manipulation of payers accounted for 74% of credit transfer fraud losses in 2024, which raises demand for behavioral analytics and real-time scoring. MiCAR compliance expands the scope of standard service modules to cover digital asset custody, wallet management, and token transaction monitoring for regulated products. Providers face higher resilience expectations on multi-client footprints, which require enterprise-grade uptime, incident response, and third-party oversight.

Geography Analysis

Germany anchors the European BaaS landscape with a dense institutional base, active FinTech ecosystems, and high digital adoption, even as conservative bank cultures and heterogeneous APIs slow some integrations relative to Nordic and UK counterparts. Multiple hubs, including Berlin, Munich, and Frankfurt, host platform providers that extend core banking and payments rails to FinTechs, merchants, and software providers. The Germany Banking as a Service market benefits from an ICT base that contributes strongly to national output and supports system integration capacity for complex enterprise deployments.

Public programs and regulatory initiatives increasingly focus on digital sovereignty and resilience, shaping data and infrastructure choices for BaaS scaling. SME digitalization continues to expand with higher spending and broader tool adoption among larger SMEs, while micro enterprises remain less served, creating scope for low-friction BaaS bundles that cover payments, invoicing, and credit. The German Banking as a Service market is further catalyzed by instant payments rules that standardize settlement speeds and verification obligations, aligning merchant and consumer expectations with real-time service design.

Innovation performance remains strong on a European scale, although digitalization metrics trail the EU leaders, which positions Germany as a scale market where pre-integrated BaaS suites can accelerate adoption. Venture capital funding patterns in 2025 skew to later stage infrastructure and enablement providers with revenue traction, which supports BaaS platforms that can evidence compliance and reliability at scale. The Germany Banking as a Service market continues to draw cross-border competitors through EU passporting, which raises the standard for uptime, support, and integration tooling for domestic suppliers.

Competitive Landscape

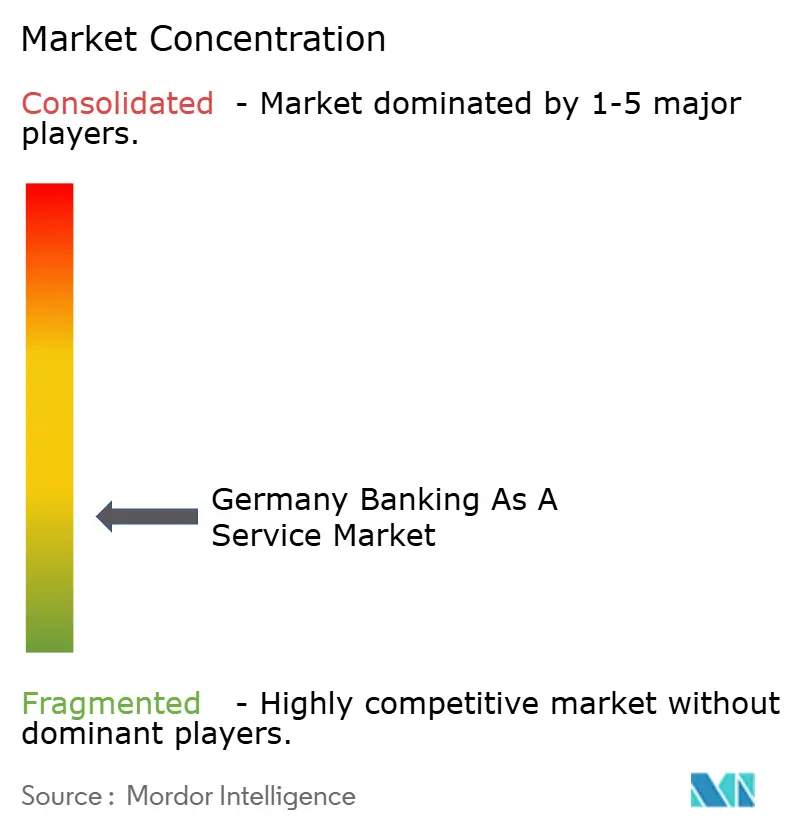

The Germany Banking as a Service market shows moderate fragmentation, with no single platform holding a dominant share and a crowded field of banks, licensed payment institutions, and non-bank platforms competing across overlapping modules. Competitive intensity is rising as MiCAR clarifies boundaries for digital asset services and as BaFin sharpens priorities on authorization quality, outsourcing oversight, and operational resilience for multi-client service providers. Solaris secured EUR 140 million in February 2025 and completed a leadership transition by December 2025 after restructuring, signaling investors’ continued interest in regulated platform providers that can harden operations. Mambu continues to expand an API-first core banking footprint with European partners, reflecting demand for cloud-native cores that can power fast product cycles and regulated reporting.

Banks broaden white-label offerings and collaborate on sovereign payment stacks, as shown by Deutsche Bank’s Wero wallet launch and its first euro-denominated cross-border blockchain transaction with DBS, which illustrates multi-rail settlement strategies for institutions. ClearBank uses EU passporting to add clients, including Raisin, bringing new competition in real-time clearing, safeguarding, and accounts for German FinTechs. Banking Circle expands cross-border payment, FX, and collection rails for marketplaces and PSPs, with company updates in 2025 highlighting broader access and connectivity into Europe and Asia.

Strategic patterns are split between pure-play BaaS platforms that standardize horizontal APIs and incumbent banks that monetize existing licenses through vertical white-label offers. The former can scale faster but face price and compliance pressure as components commoditize, while the latter often secure higher revenue per client but are constrained by legacy systems and longer change cycles. Digital bond issuance and DLT settlement pilots by leading institutions like KfW and Deutsche Bank show how capital markets digitalization creates adjacency for custody, tokenized deposits, and programmable payments. AI adoption among German businesses rose to 19.8% in 2024, a 71% annual increase, underscoring the competitive value of machine learning for credit decisioning, fraud detection, and reconciliation services in the German Banking as a Service market.

Germany Banking As A Service Industry Leaders

Deutsche Bank

Commerz Bank

KFW Bankgruppe

DZ Bank

HypoVereinsbank

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: DZ BANK received MiCAR authorization from BaFin for its meinKrypto cryptocurrency platform, enabling Volksbanken and Raiffeisenbanken to offer Bitcoin, Ethereum, Litecoin, and Cardano trading through the VR Banking App, marking a significant push by Germany's cooperative banking network into digital assets.

- December 2025: Deutsche Bank and Postbank launched Wero, a European Payments Initiative digital wallet, integrating person-to-person payment functionality into their mobile banking apps as a sovereign alternative to non-European providers, with future expansion planned for person-to-business payments and QR-code-based in-store transactions.

- November 2025: Banking Circle announced a collaboration with JD Fintech to provide real-time payments, foreign exchange, and marketplace collection infrastructure for global merchants, extending its German branch operations to serve Asian payment service providers expanding into European markets.

- August 2025: KfW issued a EUR 50 million digital bond as a crypto security under the German Electronic Securities Act, utilizing the Deutsche Bundesbank's Trigger Solution to achieve delivery-versus-payment settlement in central bank money within one day, advancing the digitalization of capital market infrastructure.

Germany Banking As A Service Market Report Scope

Banking-as-a-service (baas) describes an ecosystem in which licensed financial institutions provide non-banking businesses access to their services, generally through APIs. This growing market relies on baas to deliver its products. The report offers a complete background analysis of the German baas market, including an assessment of the emerging market trends by segments, significant changes in the market dynamics, key players in the market, market insights, and the market overview.

The German banking as A service market is segmented by component, type, enterprise size, and end-user. By component, the market is sub-segmented into platform service. By type, the market is sub-segmented into an API-based bank as an A service and a cloud-based bank as an A service. By enterprise size, the market is sub-segmented into large enterprises small & medium size enterprises. By end-user, the market is sub-segmented into banks, fintech corporations/NBFC, and other end-users. The report offers market size and forecasts for the German banking as A service market in value (USD) for all the above segments.

.

By Product Type

| Payment Gateway |

| Bank Account/Core Banking |

| Lending and Credit Services |

| Embedded Finance Software |

| Other Product Types |

By Enterprise Size

| Large Enterprises |

| Small & Medium Enterprises (SMEs) |

By End User

| Banks |

| FinTech Corporations |

| Other End Users |

By Component

| Platform / Infrastructure |

| Services (Compliance, KYC, Fraud, etc.) |

| By Product Type | Payment Gateway |

| Bank Account/Core Banking | |

| Lending and Credit Services | |

| Embedded Finance Software | |

| Other Product Types | |

| By Enterprise Size | Large Enterprises |

| Small & Medium Enterprises (SMEs) | |

| By End User | Banks |

| FinTech Corporations | |

| Other End Users | |

| By Component | Platform / Infrastructure |

| Services (Compliance, KYC, Fraud, etc.) |

Key Questions Answered in the Report

What is the projected size and growth rate for the Germany Banking as a Service market by 2031?

The Germany Banking as a Service market size is USD 580.93 billion in 2026 and is projected to reach USD 876.18 billion by 2031 at an 8.57% CAGR.

Which product category will grow fastest in Germany between 2026 and 2031?

Embedded finance software is forecast to grow at a 12.34% CAGR, outpacing payment gateways and core banking components.

Which end user segment leads adoption in Germany?

FinTech corporations lead with a 43.67% share in 2025 and the fastest growth at a 13.83% CAGR through 2031.

How do instant payments rules affect BaaS platforms in Germany?

The EU Instant Payments Regulation requires 10-second settlement and free verification of payee, which drives real-time infrastructure upgrades and compliance investments.

Where is the fastest enterprise growth within Germany's BaaS landscape?

SMEs are expected to grow at a 10.95% CAGR as integration costs fall and embedded services address financing and workflow gaps.

What is driving the services component to outgrow platform/infrastructure?

Heightened regulatory complexity, AML expectations, and fraud pressures are pushing demand for compliance, KYC, and transaction monitoring services, which are forecast to grow at 14.86% CAGR.

Page last updated on: