Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

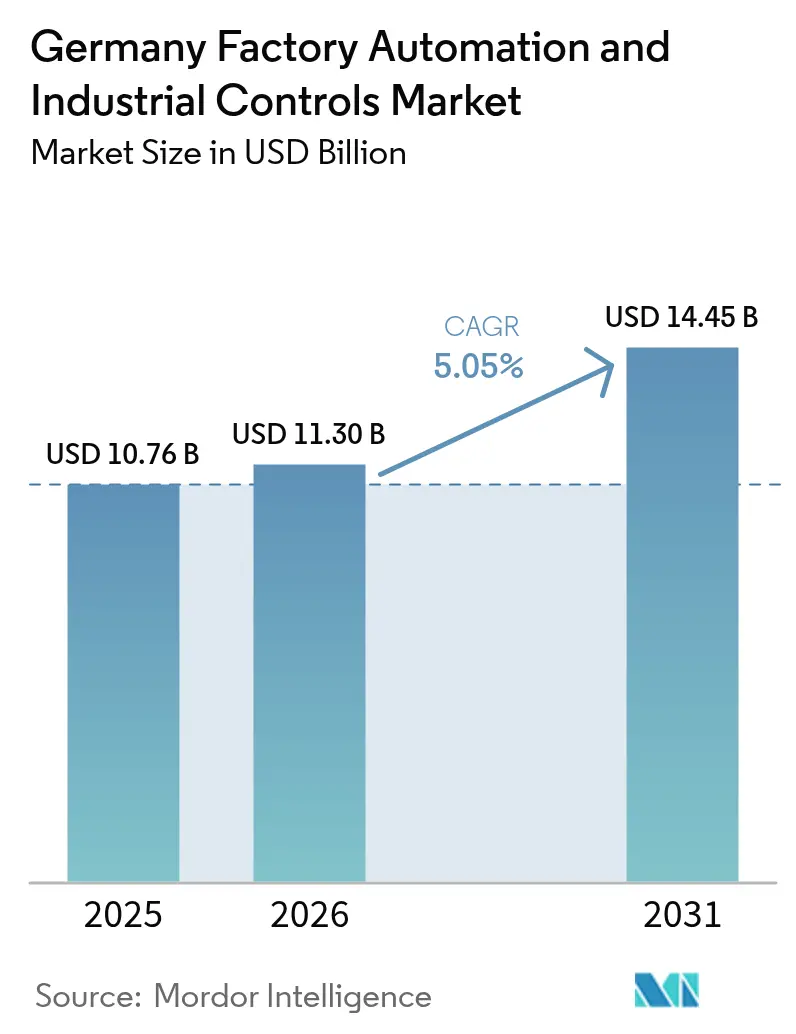

| Base Year Market Size (2025) | USD 10.76 Billion |

| Market Size (2026) | USD 11.3 Billion |

| Market Size (2031) | USD 14.45 Billion |

| Growth Rate (2026 - 2031) | 5.05% CAGR |

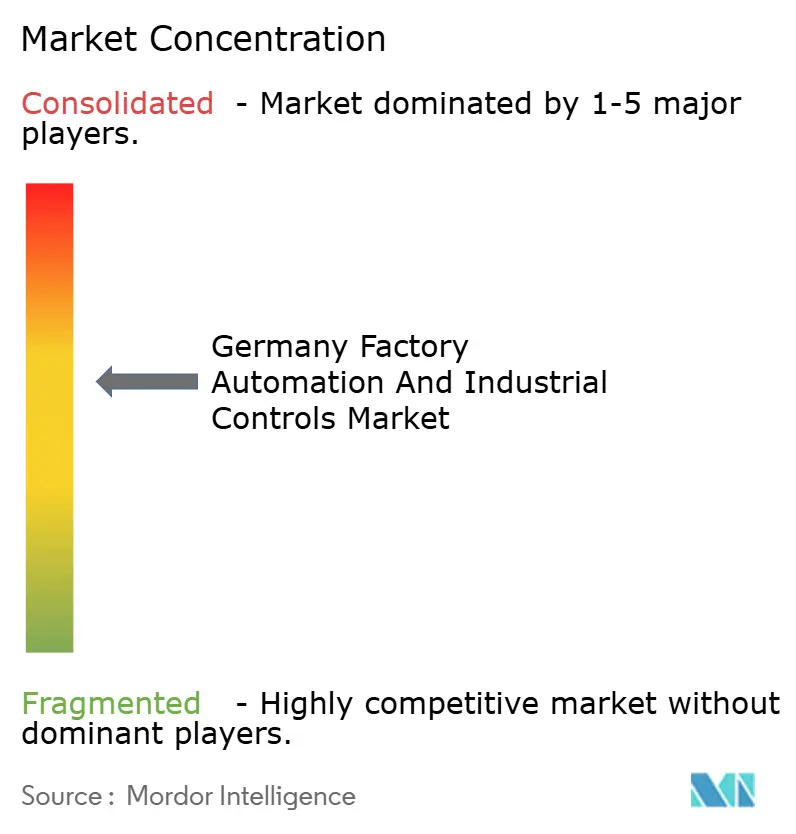

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Factory Automation And Industrial Controls Market Analysis by Mordor Intelligence

The Germany factory automation and industrial controls market size is expected to grow from USD 10.76 billion in 2025 to USD 11.3 billion in 2026 and is forecast to reach USD 14.45 billion by 2031 at 5.05% CAGR over 2026-2031. Demand growth reflects a structural shift toward resilient, data-centric production as labor scarcity, energy efficiency mandates, and supply chain reshoring converge. Automotive, machinery, and electronics producers are rolling out digitally networked equipment to mitigate skilled-worker deficits, while government incentives for low-carbon operations accelerate upgrades to IEC 62443-compliant platforms. Suppliers that own the full stack, from sensor to cloud, win market share by shortening the time to value. Yet, modular, open-protocol offerings from mid-tier specialists continue to penetrate greenfield micro-factories. Semiconductor component shortages, which had previously lifted controller lead times to 18 weeks in mid-2025, catalyzed the development of higher inventory buffers and design-for-substitution strategies that favor software-defined control architectures.

Key Report Takeaways

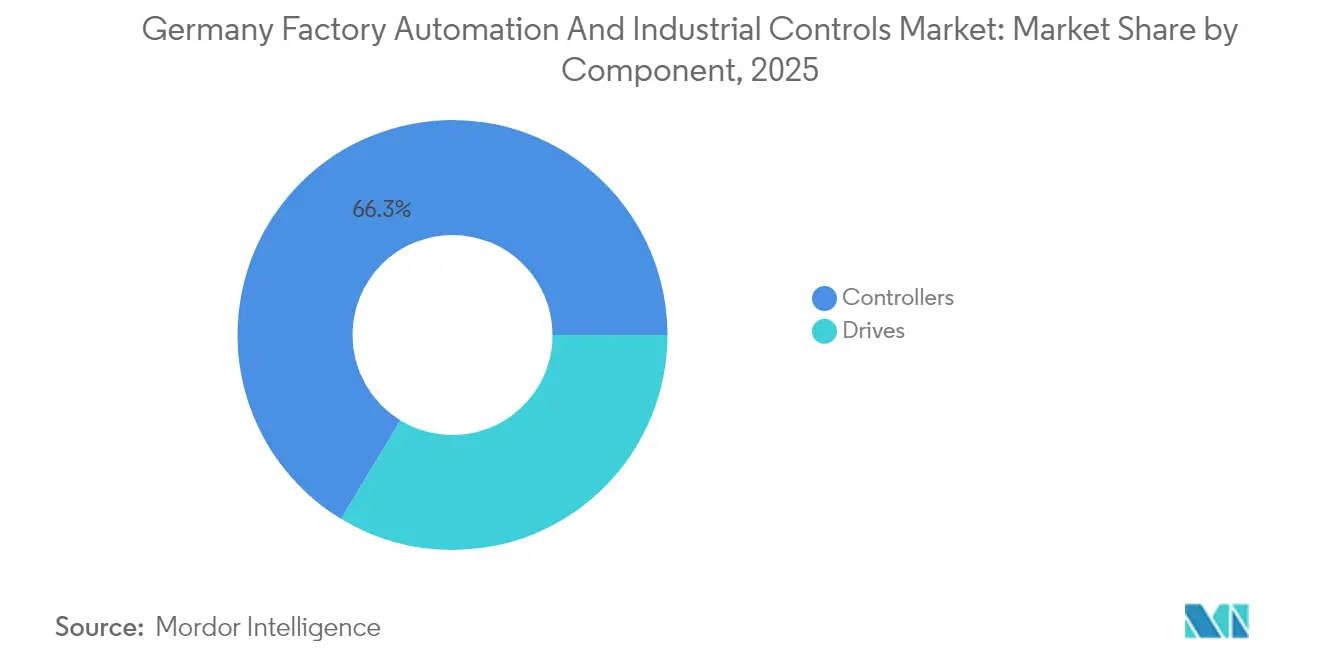

- By component, controllers led with a 66.31% share of the Germany factory automation and industrial controls market in 2025 and are expected to advance at a 5.55% CAGR through 2031.

- By control system type, discrete control systems led with a 39.46% share of the Germany factory automation and industrial controls market in 2025; IoT-enabled edge control platforms are forecast to expand at a 5.9% CAGR to 2031, outpacing supervisory control and data acquisition (SCADA).

- By end-user industry, the automotive sector accounted for 25.35% of the Germany factory automation and industrial controls market size in 2025, while electronics and semiconductors are projected to register the highest CAGR at 6.25% through 2031.

- By deployment model, on-premises systems retained a 64.72% share of the Germany factory automation and industrial controls market in 2025, while cloud-based platforms recorded the fastest growth at a 5.65% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Factory Automation And Industrial Controls Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Industry 4.0 adoption across German manufacturing | +1.2% | National, concentrated in Baden-Württemberg, Bavaria, North Rhine-Westphalia | Medium term (2-4 years) |

| Rising labor costs and skilled labor shortage driving automation | +1.5% | National, acute in automotive and machinery clusters | Short term (≤ 2 years) |

| Government incentives for energy-efficient smart factories | +0.8% | National, prioritizing industrial zones with renewable-energy access | Medium term (2-4 years) |

| Increasing demand for mass customization and flexible production | +0.9% | National, led by automotive, machinery, consumer electronics | Long term (≥ 4 years) |

| Emphasis on cyber-physical security standards boosting control upgrades | +0.7% | National, export-oriented manufacturers | Short term (≤ 2 years) |

| Reshoring of critical supply chains stimulating domestic capex | +0.6% | National, semiconductors, pharmaceuticals, battery production | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Industry 4.0 Adoption Across German Manufacturing

Plattform Industrie 4.0 reported that by end-2024, 78% of large plants and 54% of SMEs had implemented at least one digital use case, up from 41% in 2020.[1]Federal Ministry for Economic Affairs and Climate Action, “Plattform Industrie 4.0 Progress Report,” bmwk.de Asset Administration Shell and OPC UA standards now underpin machine-to-machine data exchange, letting heterogeneous fleets interoperate without vendor lock-in. Tier-one automotive suppliers embed digital twins inside programmable logic controller code to test changeovers virtually, shrinking downtime from days to hours. Machinery builders have standardized on plug-and-produce modules that reduce engineering effort by up to 40%, enabling line re-configuration within a single shift. Demand for industrial PCs with multi-core processors and FPGAs is rising as manufacturers run machine-learning inference at the edge, bypassing latency and safeguarding intellectual property on-premises.

Rising Labor Costs and Skilled Labor Shortage Driving Automation

Median hourly manufacturing wages climbed to EUR 47.30 (USD 53.45) in 2024, the highest in the European Union. Germany faces a projected 1.2 million technical-worker shortfall by 2030. Collaborative robots without safety cages shipped 22% more units in 2024, especially to food and beverage packagers that handle variable-size products. Pharmaceutical contractors integrated automated guided vehicles with warehouse-management software, boosting throughput 18% and cutting injuries 35%.[2]KUKA AG, “Industrial Robotics and Automation,” kuka.com Automation offsets spiraling onboarding costs as apprenticeship completion rates declined 9% since 2020 and operator turnover averages 14% annually.

Government Incentives for Energy-Efficient Smart Factories

The Energy Efficiency and Process Heat program earmarked EUR 1.8 billion (USD 2.03 billion) through 2025, covering up to 55% of automation spend that yields at least 15% energy savings. Variable-frequency drives paired with SCADA-based energy dashboards qualify for accelerated depreciation. Chemical processors that retrofitted advanced process control cut natural-gas use 12% and generate EUR 3.2 million (USD 3.62 million) in annual carbon-credit revenue.[3]ABB Ltd, “Industrial Automation Solutions,” abb.com ISO 50001-certified energy-management software earns a 10% grant top-up, spurring demand for controllers with embedded metering and real-time visualization.

Increasing Demand for Mass Customization and Flexible Production

Automakers shift from fixed lines to matrix layouts where battery-electric, hybrid and ICE vehicles share conveyors, requiring controllers that sequence mixed models without manual programming. Average machinery batch sizes fell from 500 units in 2020 to 150 in 2024 as customers expect four-week delivery VDMA. Software-defined control lets operators swap product recipes on touchscreens in under five minutes, while machine-vision systems auto-identify components and adjust pick-and-place trajectories, cutting changeover costs 40%.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial capital expenditure for SMEs | -0.9% | National, regions with lower SME digitalization rates | Short term (≤ 2 years) |

| Integration complexity with legacy brownfield equipment | -0.7% | National, automotive, metals, chemicals | Medium term (2-4 years) |

| Semiconductor supply-chain volatility | -0.6% | National, ripple effects across industries | Short term (≤ 2 years) |

| Stringent data-sovereignty regulations | -0.5% | National, multinationals | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Initial Capital Expenditure for SMEs

SMEs employ 60% of Germany’s manufacturing workforce yet face upfront retrofit costs of EUR 800,000 to 1.5 million (USD 904,000 to 1.70 million) per plant, extending payback to five years in low-margin segments. The Digital Now subsidy covers half the spend, but applicants must supply energy audits and cybersecurity plans that small firms often outsource, delaying disbursements six to nine months. Leasing and automation-as-a-service models spread expenses over monthly fees, though concerns about data ownership and vendor lock-in temper adoption VDMA.

Integration Complexity With Legacy Brownfield Equipment

About 40% of installed machinery exceeds 15 years in age and lacks digital interfaces. Retrofitting costs EUR 20,000 to 80,000 (USD 22,600 to 90,400) per asset, and custom middleware is required to translate proprietary protocols into OPC UA for modern SCADA systems. Automotive suppliers running 1990s-era transfer lines must choose between brownfield upgrades that add five to seven years of life or greenfield cells delivering 20% higher overall equipment effectiveness. In chemicals, integrating new distributed control modules with safety-instrumented systems triggers 12- to 18-month re-validation cycles and EUR 200,000 to 500,000 (USD 226,000 to 565,000) in compliance costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Controllers Sustain Dominance Through Retrofit Cycles

Controllers held the largest slice of the Germany factory automation and industrial controls market size at 66.31% in 2025 and will grow at a 5.55% CAGR to 2031. Programmable logic controllers remain indispensable for discrete tasks, while distributed control systems lead in process environments that demand validated audit trails. Industrial PCs are seizing high-speed vision and AI workloads, particularly in electronics assembly, where shipments jumped 19% in 2024.

Drives, motors, sensors and robotics comprise the balance of spending and track controller growth. Servo motors with integrated encoders replace steppers in packaging, offering 0.01 millimeter precision. IO-Link sensors reduce commissioning by 25%, and embedded deep-learning cameras deliver 99.5% defect detection in automotive final inspection. Collaborative robots with wash-down ratings are gaining share in beverage palletizing lines.

By Control System Type: IoT Edge Platforms Reshape Architecture

Discrete control systems secured 39.46% of 2025 revenue as automotive and machinery customers prioritize high-speed logic. Process control dominates chemicals and pharmaceuticals by regulating temperature, pressure and flow.

SCADA provides historian and visualization functions but lags at 4.05% CAGR. IoT-enabled edge platforms, integrating PLCs, PCs and gateways, advance at 5.9%, establishing a responsive layer for predictive maintenance without exposing proprietary data to public clouds. Demand for time-sensitive networking switches that guarantee sub-1 millisecond latency underscores the architectural transition.

By End-User Industry: Electronics Outpaces Automotive Growth

Automotive maintained a 25.35% spending share in 2025, yet its 4.95% CAGR is eclipsed by electronics and semiconductors at 6.25% as the European Chips Act mobilizes local wafer and packaging capacity. Mega-fabs in Saxony require ultra-clean robot handling and sub-micron vibration isolation.

Machinery builders embed predictive maintenance modules to differentiate exports, while pharmaceuticals deploy single-use bioreactors with wireless sensors to shorten cleaning cycles. Food processors adopt hygienic-design robots, and metals firms retrofit furnaces with condition-monitoring sensors to extend asset life.

By Deployment Model: Hybrid Architectures Reconcile Sovereignty and Scale

On-premises platforms captured 64.72% of 2025 value, reflecting Germany’s strict data-sovereignty rules under GDPR and the IT Security Act 2.0. Cloud-based control grows fastest at 5.65% CAGR as SMEs embrace SaaS MES and planning tools.

Hybrid edge-plus-cloud designs balance latency and scalability, closed-loop motion remains on-site, while anonymized metrics stream to hyperscale clouds for AI training. Compliance with the Network and Information Security Directive 2, effective October 2024, motivates manufacturers to offload non-critical workloads to managed cloud platforms.

Geography Analysis

Germany accounts for the European Union’s largest manufacturing value add at EUR 650 billion (USD 734 billion) in 2024. Baden-Württemberg, Bavaria and North Rhine-Westphalia drive roughly 60% of automation capex, anchored by automotive OEMs, tier-one suppliers and machine builders. Proximity to institutes such as Fraunhofer IPA expedites the commercialization of adaptive robotics and digital twins. Saxony and Thuringia emerge as semiconductor and battery hubs under Important Projects of Common European Interest, attracting EUR 15 billion (USD 16.95 billion) in commitments by 2025.

Integration inside the European single market eases equipment flow and labor mobility, but German firms’ preference for open-architecture systems distinguishes them from peers. Adoption of PC-based control from Beckhoff Automation and B and R Industrial Automation exceeds the regional average, reflecting concerns about vendor lock-in. Regulatory rigor, Machinery Directive, Low Voltage Directive and Electromagnetic Compatibility Directive creates high entry barriers yet guarantees reliability that underpins export success. CE marking and IEC 62443 certification are essential credentials for German machinery shipped to North America and Asia-Pacific, where cybersecurity scrutiny intensifies.

Regulatory Landscape

Germany's factory automation and industrial controls market operates under a dense EU and national compliance stack covering machinery safety, functional safety, and cybersecurity. A key change is the Maschinenverordnung-Durchfuehrungsgesetz (MaschinenDG), enacted on December 2, 2025, which implements EU Regulation 2023/1230 and tightens expectations around digital documentation and conformity processes for machinery placed on the market.

Cybersecurity requirements are also moving closer to product-level obligations. The Federal Office for Information Security (BSI) issued TR-03183 (including version 1.1.0 guidance for Module H) to help manufacturers interpret cyber resilience expectations in preparation for the EU Cyber Resilience Act, with phased enforcement referenced from June 11, 2026, and a transition toward full implementation by December 11, 2027. For safety-relevant measurement, control, and regulation equipment in industrial plants, TRBS 1115 Part 1 continues to concretize cybersecurity expectations under the Betriebssicherheitsverordnung, supporting demand for hardened control platforms and documented security-by-design practices.

Value Chain Analysis

The value chain runs from component suppliers (semiconductors, sensors, drives, industrial PCs) to automation OEMs and software providers (controllers, SCADA, edge platforms, engineering tools), then through system integrators to end users across automotive, machinery, electronics, and process industries. Interoperability and data-exchange standards increasingly shape supplier selection and integration effort, with Industry 4.0 reference architectures such as Asset Administration Shell (AAS) and OPC UA influencing how brownfield assets connect to modern SCADA and IoT-enabled edge control platforms.

Germany's industrial data layer is also being organized through Manufacturing-X, including the Factory-X lighthouse project led by Siemens and SAP with a multi-partner ecosystem. This supports federated data sharing and common semantics as an enabler for multi-vendor automation rollouts. Supply constraints remain a recurring operating reality as well: in December 2025, 27.6% of German manufacturing companies reported bottlenecks for intermediate products, which reinforces procurement strategies such as multi-sourcing, higher buffers, and design-for-substitution that favor modular control architectures and software-defined capabilities.

Competitive Landscape

The Germany factory automation and industrial controls market is moderately concentrated: Siemens, Bosch Rexroth, ABB, Schneider Electric and Mitsubishi Electric collectively hold most of the share. Vertical integration delivers bundled hardware, software and lifecycle services that lower total cost of ownership, positioning incumbents strongly in automotive and electronics programs where single-vendor accountability is paramount. Siemens leverages its Digital Industries suite, while ABB packages motion, robotics, and cloud analytics in ABB Ability.

Mid-tier specialists such as Beckhoff Automation and WAGO address machinery builders’ need for flexibility through open-protocol, PC-based platforms that reduce software royalties. White space exists in software-defined automation, which decouples logic from proprietary hardware; vendors targeting this niche rely on commercial off-the-shelf computers and containerized runtimes. Collaborative robotics remains a growth pocket: newcomers like Franka Emika and Yuanda Robotics market force-sensitive arms priced 30-40% below established brands to penetrate SME cells.

The competitive frontier shifts toward ecosystem orchestration rather than product specs alone. Siemens acquired Mendix to embed low-code application development, and Schneider Electric partnered with Microsoft Azure to integrate cloud IoT services. Patent filings tied to predictive maintenance and digital twins jumped significantly in 2024, with German assignees emphasizing hybrid architectures that satisfy sovereignty while leveraging cloud scale.

Germany Factory Automation And Industrial Controls Industry Leaders

Siemens AG

Bosch Rexroth AG

ABB Ltd

Schneider Electric SE

Mitsubishi Electric Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Software-defined automation and standardized data exchange remain a clear whitespace in Germany, particularly for manufacturers modernizing brownfield lines while avoiding vendor lock-in and meeting sovereignty constraints. Manufacturing-X (including the Factory-X lighthouse project led by Siemens and SAP) provides an active framework for federated, interoperable industrial data sharing, which supports demand for edge platforms, gateways, and engineering tools aligned to Industry 4.0 constructs such as Asset Administration Shell and OPC UA.

Budget allocation is also being pulled toward compliance-driven digitization. Germany's MaschinenDG (December 2025) strengthens digital documentation expectations for machinery, while the BSI has published TR-03183 guidance to help manufacturers prepare for EU Cyber Resilience Act obligations, driving suppliers to incorporate cybersecurity and lifecycle documentation into controllers, IPCs, and software toolchains. On the execution side, announced investments signal continued scaling of smart manufacturing infrastructure, including Siemens' March 2026 announcement of a EUR 200 million intelligent factory investment in Amberg focused on smart infrastructure and AI-enabled manufacturing.

Recent Industry Developments

- July 2026: Siemens announced a EUR 300 million investment in Germany to expand production capacity for power distribution systems, including upgrades at its Frankfurt switchgear factory and a new supplier facility in Offenbach. The investment increases domestic manufacturing depth for electrification hardware that underpins automated plants, data centers, and e-mobility supply chains in Germany.

- June 2026: Siemens expanded Simatic AX Logic Control Engineering to add XLad ladder programming and support for Simatic S7-1200 G2 controllers. Broadening the engineering workflow across controller families supports adoption of unified, software-centric development in German factories standardizing on Siemens PLC and edge toolchains.

- October 2025: ABB commissioned Germany's first IEC 62443-certified, hydrogen-ready process control system at a Saxony chemical park, integrating 3,000 I/O points and native cybersecurity monitoring. The deployment shows how cyber-certified control architectures are being paired with fuel-flexible operations, supporting modernization of process automation under energy-transition programs.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of factory automation and industrial control hardware and related software used inside German industrial sites to monitor, control, and automate production processes, lines, and machines. The sizing is done in revenue terms for products and solutions delivered into Germany during the study period.

Scope exclusions: We exclude general-purpose IT hardware, pure building automation, and standalone consumer IoT devices that are not designed for industrial production environments.

Segmentation Overview

- By Component

- Controllers

- Programmable Logic Controllers (PLCs)

- Distributed Control Systems (DCS)

- Industrial PCs (IPCs)

- Drives

- Motors

- Sensors

- Machine Vision

- Robotics

- Other Drives

- Controllers

- By Control System Type

- Discrete Control Systems

- Process Control Systems

- Supervisory Control and Data Acquisition (SCADA)

- IoT-Enabled Edge Control Platforms

- By End-User Industry

- Automotive

- Machinery and Equipment

- Electronics and Semiconductors

- Food and Beverage

- Pharmaceuticals and Chemicals

- Metals and Mining

- Other End-User Industries

- By Deployment Model

- On-Premises Control Systems

- Cloud-Based Control Platforms

- Hybrid (Edge + Cloud) Architectures

Data Sources, Market Sizing, and Validation

Desk Research

Desk work was used to build the model structure for Germany and set realistic guardrails before primary inputs were applied. We mainly relied on public references such as Destatis releases, Eurostat industry output series, VDMA Robotics + Automation publications, and selected IEA and OECD manufacturing indicators to understand production cycles and where investment is being directed.

To keep assumptions grounded, we also reviewed company annual reports, German plant investment announcements covered by reputed press, and association websites that track automation adoption themes. Where needed, a paid subscription for company financials and news was used to cross-check revenue exposure statements, and an import and export shipment-level database was referenced selectively to validate directional movement for relevant control and automation categories. The desk research sources listed above are illustrative only, and other references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary discussions were used to test scope and to understand whether customers treat pricing changes and adjacent spend as part of factory automation. We spoke with automation suppliers, system integrators, distributors, plant engineering teams, and end-user maintenance leaders across Germany, and we rechecked the same inputs across multiple end-use industries so one sector did not drive the result.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 13% | |

| Mid tier: 56% | Functional/Unit leaders: 33% | |

| Smaller Players: 16% | Managers: 54% |

Market-Sizing & Forecasting

The core sizing starts with a top-down build where Germany manufacturing activity and capex signals are translated into an automation spend pool, then allocated across factory automation and control categories using validated adoption splits. To avoid relying on one direction only, results were corroborated with selective bottom-up checks, such as sampled ASP x shipment volumes for common device groups and reasonableness checks against supplier revenue exposure to Germany.

Inputs used in the model include German industrial production trends, order intake and lead-time direction for key control equipment, typical replacement and retrofit cycles in plants, plant-level automation intensity by end-use industry, and price progression for controllers, drives, and key sensing and interface devices. When a bottom-up datapoint was missing, gaps were handled by applying conservative penetration ranges agreed during interviews, which were then tightened through cross-checks with known installation and upgrade patterns.

For forecasting, scenario analysis was used because industrial demand in Germany can swing quickly with export orders, energy costs, and investment timing. The forward view is built by adjusting the demand pool under a base case and then applying expert-validated ranges for automation intensity and pricing, so the curve stays consistent with how projects are approved and delivered in practice.

Data Validation & Update Cycle

Findings are checked in more than one way so obvious overstatements do not pass through. We compare the modeled totals against independent signals, such as association turnover direction, industrial production movement, and visible investment cycles, and then any large variances are reviewed again before final sign-off.

If a key assumption shifts, such as a change in lead times, project deferrals, or unexpected price drops, the related inputs are re-contacted and the model is recalculated. Reports are refreshed annually, and interim updates are made when material events affect Germany industrial investment. Before delivery, a final analyst pass is performed so clients receive the latest updated view.

Mordor Intelligence's Germany Factory Automation and Industrial Controls Market Market Size Measured Against Other Published Estimates

Published market values for this space can look far apart, even when studies use similar labels, because the scope boundary is not consistent and the assumed demand pool differs. Differences also show up when some studies use broader industrial automation umbrellas, apply aggressive adoption curves, or mix turnover style figures with product revenue sizing.

In Germany, the biggest gap drivers are usually whether robotics and machine vision are counted as part of the same market, whether system integration services are included as a major line item, and how pricing is treated when lead times ease and discounts return. Currency timing and the update cycle also matter, since Germany industrial capex sentiment can change within a year and older estimates may not reflect that shift.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 10.76 B (2025) | |

| Industry Publisher A | USD 5.06 B (2024) | Uses a different base year and can reflect a narrower counted revenue pool, with less explicit reconciliation to Germany-wide automation intensity by end-use industry and less consistent treatment of price progression across the cycle. |

| Trade Body B | USD 17.30 B (2024) | Represents turnover for a broader robotics and automation basket, which can include robotics and machine vision bundles that sit outside factory automation and industrial controls when the market is defined as product and solution revenue for industrial control and automation in plants. |

The table shows a wide spread mainly because the measured basket is different, and then the base year and pricing logic compound the gap. In Mordor Intelligence's model, the Germany total is built from manufacturing output and capex linked demand signals and then constrained by validated adoption splits for industrial controls and factory automation, rather than using robotics and automation turnover as a direct proxy. With clear inputs and repeatable checks, the estimate remains easy to follow and practical for planning discussions.

Key Questions Answered in the Report

How large is the Germany factory automation and industrial controls market in 2026?

The market is valued at USD 11.3 billion in 2026 and is forecast to grow at a 5.05% CAGR to USD 14.45 billion by 2031.

Which component category commands the highest spending?

Controllers dominate with 66.31% of 2025 revenue and continue to expand due to mandatory cybersecurity upgrades.

Which end-user segment is growing fastest?

Electronics and semiconductors exhibit a 6.25% CAGR as Germany localizes chip production under the European Chips Act.

What deployment model is gaining momentum despite data-sovereignty rules?

Cloud-based control platforms show the highest growth at a 5.65% CAGR, although on-premises systems still prevail.

How are SMEs financing automation projects?

Many SMEs combine Digital Now grants with KfW development loans or opt for leasing and automation-as-a-service contracts to lower upfront costs.

What is driving the shift toward IoT edge platforms?

Manufacturers want real-time analytics without sending proprietary data to public clouds, leading to a 5.9% CAGR for IoT-enabled edge control solutions.

Page last updated on: