Germany EV Battery Pack Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

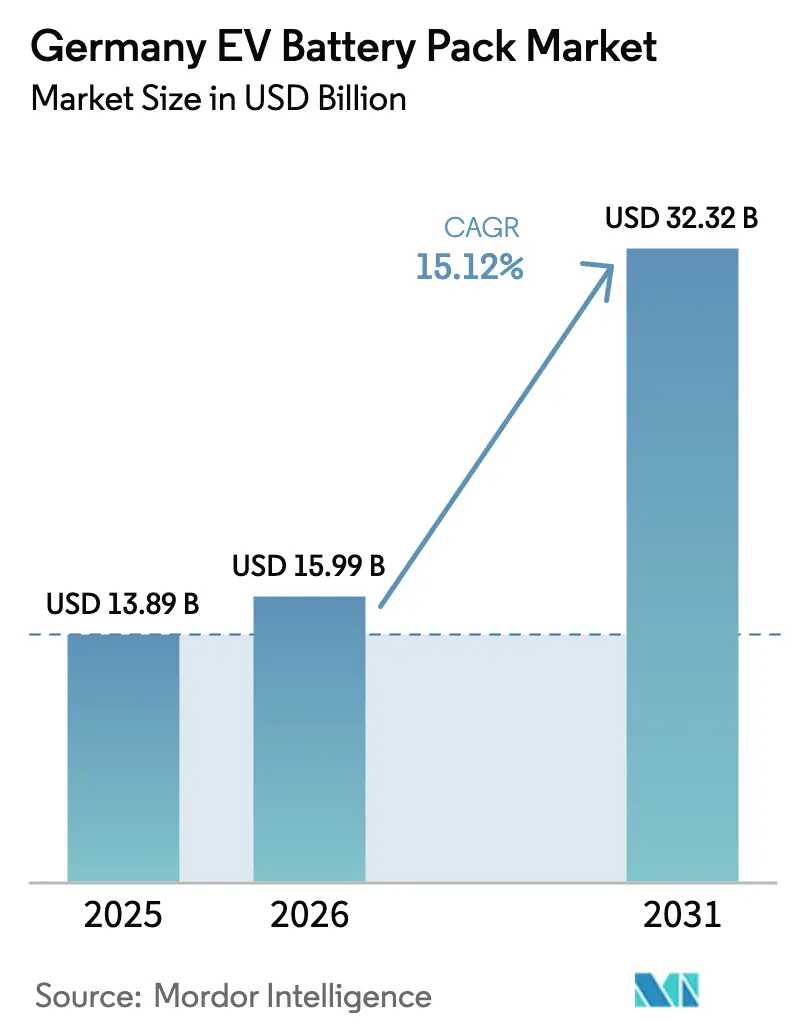

| Base Year Market Size (2025) | USD 13.89 Billion |

| Market Size (2026) | USD 15.99 Billion |

| Market Size (2031) | USD 32.32 Billion |

| Growth Rate (2026 - 2031) | 15.12% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany EV Battery Pack Market Analysis by Mordor Intelligence

The German EV battery pack market size was valued at USD 13.89 billion in 2025 and estimated to grow from USD 15.99 billion in 2026 to reach USD 32.32 billion by 2031, at a CAGR of 15.12% during the forecast period (2026-2031). Regulatory pressure from the EU Fit-for-55 package, rapid domestic gigafactory construction, and gains in lithium iron phosphate (LFP) chemistry underpin this expansion. Automakers are boosting their production of battery-electric vehicles (BEVs) to sidestep regulatory penalties linked to fleet emissions. This surge in production is steering them towards long-term supply chain strategies. In Germany, the rise of large-scale gigafactories is transforming the continent's battery landscape. Meanwhile, advanced LMFP battery technologies are gaining traction as budget-friendly substitutes for nickel-rich chemistries, especially among premium segments. A widespread fast-charging network alleviates range anxiety, paving the way for adopting high-capacity battery packs. Furthermore, supportive fiscal measures, like generous depreciation benefits for commercial BEVs, broaden market access for business fleets.

Key Report Takeaways

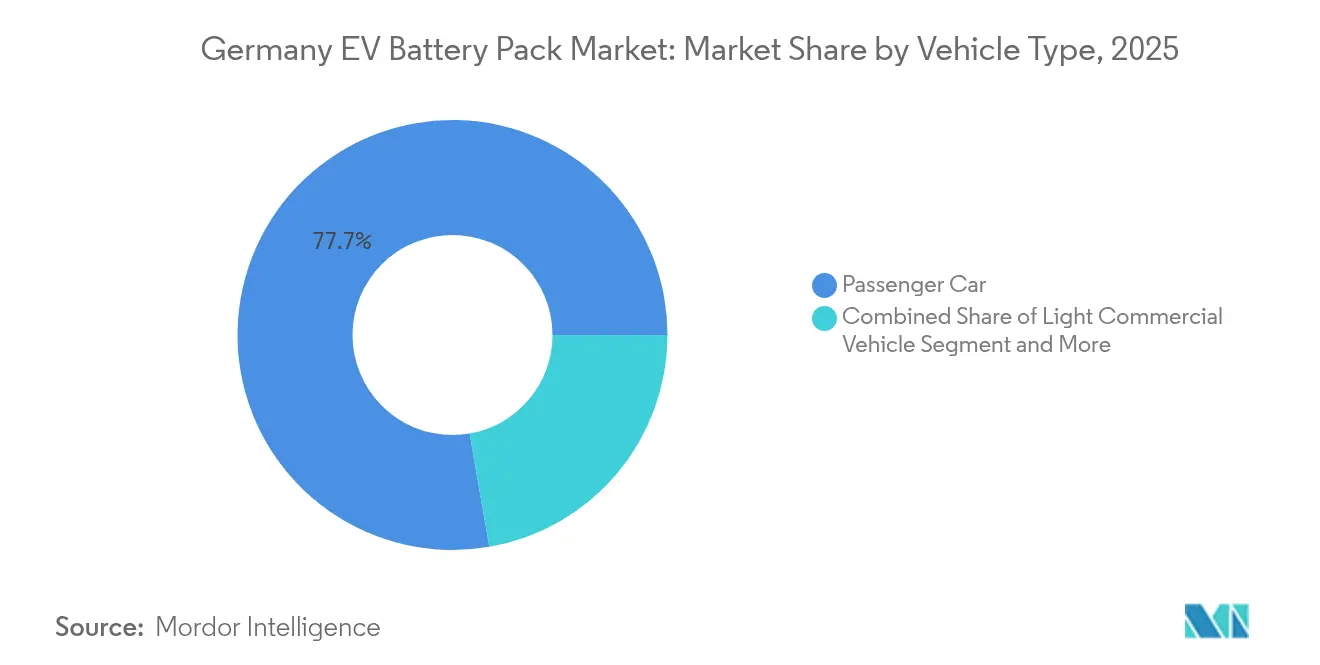

- By vehicle type, passenger cars led with 77.74% of Germany's EV battery pack market share in 2025, while buses are projected to advance at a 15.88% CAGR through 2031.

- By propulsion, battery electric vehicles accounted for 66.41% of the German EV battery pack market size in 2025 and are set to expand at a 15.82% CAGR to 2031.

- By battery chemistry, nickel-manganese-cobalt (NMC) held a 51.62% share of the German EV battery pack market size in 2025; lithium iron phosphate is forecast to record a 16.74% CAGR to 2031.

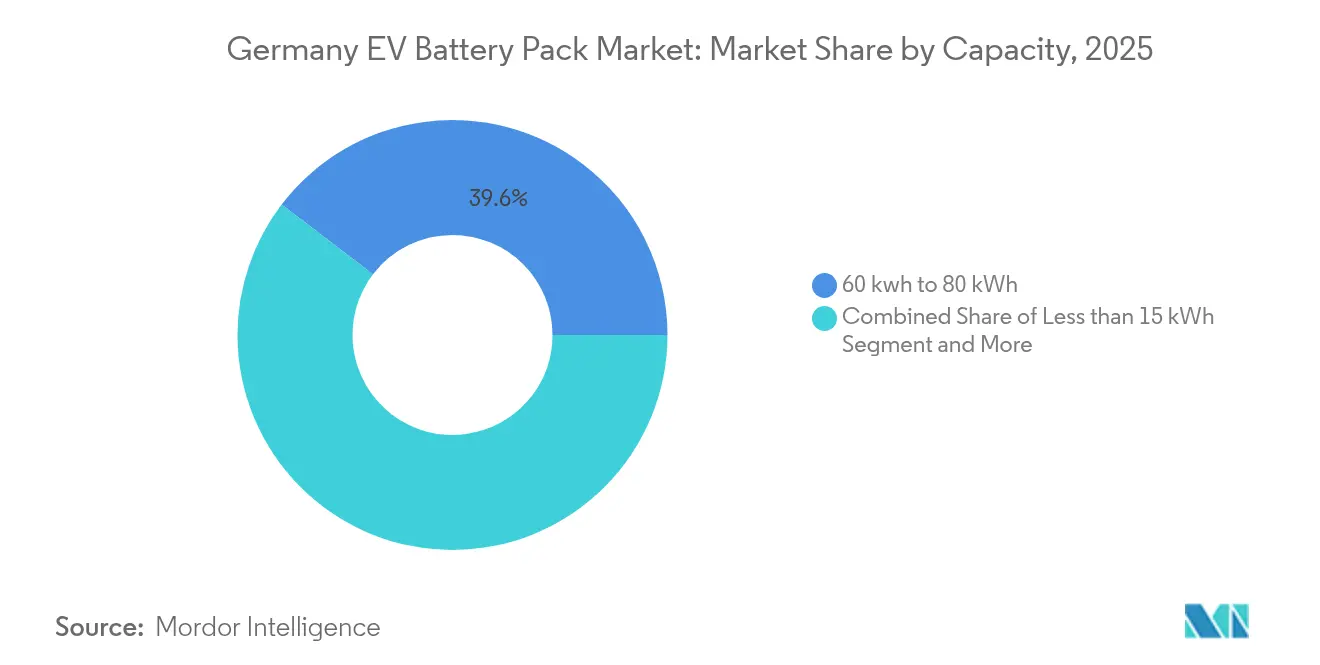

- By capacity, the 60-80 kWh segment commanded 39.62% of the German EV battery pack market size in 2025, whereas packs above 150 kWh are expected to grow at 16.55% CAGR through 2031.

- By battery form, prismatic cells captured 45.71% of the German EV battery pack market size in 2025 and are projected to rise at a 16.98% CAGR by 2031.

- By voltage class, systems below 400 V controlled 62.35% of the German EV battery pack market size in 2025; 600-800 V platforms are slated for a 16.03% CAGR to 2031.

- By module architecture, module-to-pack designs represented 56.98% of the German EV battery pack market size in 2025, whereas cell-to-pack solutions are advancing at a 15.22% CAGR.

- By component, cathode materials contributed 34.11% of the German EV battery pack market size in 2025, while separators are poised for a 15.41% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany EV Battery Pack Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU Fit-For-55 CO₂ Fleet Limits (2025 Step) | +2.5% | Germany and broader EU automotive manufacturing regions | Short term (≤ 2 years) |

| EU Battery Regulation Boosting Local Sourcing | +2.1% | EU-wide with concentrated impact in Germany | Medium term (2-4 years) |

| Domestic Gigafactory Build-Out (East Germany) | +1.8% | Primarily East Germany with spillover to Central Europe | Medium term (2-4 years) |

| High-power Charging Corridor Coverage Above AFIR Targets | +1.4% | Germany with cross-border connectivity to neighboring EU states | Short term (≤ 2 years) |

| Lithium Manganese Iron Phosphate Breakthroughs (Above 230 Wh Kg⁻¹ At Lithium Iron Phosphate Cost) | +1.2% | Global technology impact with German manufacturing advantage | Long term (≥ 4 years) |

| 75% 1st-Year Depreciation for Commercial BEVs | +0.9% | Germany national policy with potential EU adoption | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

EU Fit-for-55 CO₂ Fleet Limits Drive Immediate Compliance Demand

The EU mandates a 15% cut in average fleet CO₂ by 2025, exposing German automakers to EUR 95 penalties per excess gram[1]“Fit for 55: delivering on the European Green Deal,”, European Commission, europa.eu. OEMs respond by securing multi-year battery agreements such as Volkswagen’s 240 GWh annual requirement pledge. Compliance urgency shifts procurement from price competition to guaranteed capacity. Battery suppliers able to demonstrate reliable volume and local content gain preferred-vendor status. Plant scheduling now aligns with regulatory milestones rather than consumer demand cycles, compressing development timelines yet cementing long-term volume visibility for pack integrators.

EU Battery Regulation Creates Structural Sourcing Advantages

In the near future, the European Union will mandate that batteries sold within its borders contain minimum levels of recycled materials, including cobalt, lead, lithium, and nickel. Furthermore, manufacturers will be obligated to reveal the complete carbon footprint of their products, tracing it from raw material extraction to production. These regulations aim to bolster sustainability and transparency throughout the battery supply chain. Some German recyclers, as early adopters, have set up advanced recovery facilities that align with these new standards, granting them a competitive edge. Moreover, in regions with a high share of renewable energy, the environmental profile of locally produced batteries stands out, especially when juxtaposed with counterparts from fossil fuel-reliant areas.

The rollout of mandatory digital battery passports complicates compliance, benefiting producers already embedded in the EU’s stringent quality management frameworks. Collectively, these initiatives serve as non-tariff barriers, safeguarding domestic manufacturing and spurring investments throughout the battery lifecycle—from processing raw materials to recovering them at the end of their life.

Domestic Gigafactory Expansion Reduces Import Dependency

Northvolt’s EUR 5 billion Heide complex and CATL’s Thuringia site exceed 100 GWh annual capacity, tilting the German EV battery pack market toward self-sufficiency[2]“Northvolt to build Europe’s largest battery factory in Heide,”, Northvolt, northvolt.com. Eastern locations offer lower labor costs and ample industrial land while remaining within trucking range of Bavarian and Lower Saxon vehicle plants. Cell, module, and pack line co-location lowers logistics expense and improves quality control. Tesla’s Berlin facility illustrates how integrated sites streamline just-in-time final assembly. Scale economies from domestic plants reduce delivered cost variance versus Asian imports, strengthening Germany’s negotiating position in Europe-wide supply contracts.

High-Power Charging (HPC) Infrastructure Exceeds AFIR Targets Enabling Larger Battery Adoption

Germany hosts public chargers rated at 150 kW or higher, surpassing 2025 AFIR thresholds[3]“Charging infrastructure statistics,”, Bundesnetzagentur, bundesnetzagentur.de. Ionity plans 7,000 ultra-fast points by 2030, each designed for 800 V systems. With the expansion of charging infrastructure, range anxiety is becoming a thing of the past. This shift enables automakers to adopt larger battery packs as the norm across their electric vehicle lineup. These enhanced battery packs boost vehicle performance and elevate the average selling price, driving revenue growth in pivotal markets such as Germany.

Utilities' increasing dedication to procuring electricity from renewable sources amplifies the allure of electric vehicles for eco-conscious consumers. Many are ready to invest more for greener charging alternatives, underscoring the market's pivot towards sustainable transportation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Electricity Prices Post-Subsidy | +1.6% | Germany with broader European energy market exposure | Medium term (2-4 years) |

| Import Dependency (Graphite Export Controls) | +1.3% | Germany and EU with global supply chain implications | Long term (≥ 4 years) |

| Domestic Energy and Labor Cost Premium | +0.8% | Germany relative to Eastern European and Asian competitors | Long term (≥ 4 years) |

| Used-BEV Resale-Value Gap | +0.7% | Germany with spillover to European secondary markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Electricity Price Volatility Creates Manufacturing Cost Uncertainty

In certain regions, high electricity costs erode the competitiveness of energy-intensive battery production. Rising future energy prices, driven by the phase-out of nuclear energy and diminished support for renewables, are casting financial uncertainty over new manufacturing facilities. While some producers are countering this risk by investing in on-site renewable generation, they still grapple with higher energy costs than those of their international counterparts. Such price volatility complicates production planning, compelling companies to stockpile materials during cheaper periods, thereby inflating working capital needs.

While additional investments in energy storage and long-term renewable power contracts aid in stabilizing operations, they also escalate the overall cost of battery packs. These heightened costs, in turn, impact vehicle pricing, influencing the economics of electric mobility in the region.

Domestic Energy and Labor Cost Premium Weighs on Margins

The average German manufacturing wage exceeds Eastern European levels by 40%, while industrial power costs outpace the EU average by 30%. Although automation narrows labor differentials, final assembly and quality control remain people-intensive. Combined with high environmental-compliance expenses, these factors compress gross margins compared with sites in Poland or Hungary. Scale helps, yet small and mid-size suppliers risk being priced out unless they specialize in high-value chemistries or engineering services.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Passenger Cars Anchor Volume, Buses Propel Growth

Passenger cars accounted for 77.74% of Germany's EV battery pack market size in 2025, reflecting scaled platforms and extensive consumer incentives. City buses, however, are forecast to post a 15.88% CAGR through 2031 as local authorities comply with the EU Clean Vehicles Directive. Passenger car volume supports continuous cell production, stabilizing utilization at new gigafactories. Municipal bus tenders generate large single-order volumes that favor suppliers capable of delivering 250-300 kWh packs with liquid cooling and high cycle life.

Rising bus demand encourages specialized module designs with reinforced enclosures and redundant safety electronics suitable for depot fast-charging. Passenger-car systems concentrate on cost-optimized prismatic cell clusters, whereas bus packs integrate telematics for fleet-wide predictive maintenance. These divergent technical needs allow manufacturers to diversify offerings without overhauling core production lines, strengthening competitive resilience within the German EV battery pack market.

By Propulsion Type: BEV Command Sets Pace for Complete Electrification

Battery electric vehicles held a 66.41% share in 2025 and will expand at a 15.82% CAGR to 2031, eclipsing plug-in hybrids as battery prices fall. CO₂ fleet limits discourage PHEV reliance due to weighted emission calculations; OEMs channel R&D budgets into BEV-first architectures. BEV platforms simplify chassis integration by eliminating exhaust routing and fuel-tank packaging, freeing space for larger flat-pack batteries.

PHEVs retain relevance for rural drivers lacking home charging, yet declining subsidy support and rising battery capacities diminish their total-cost-of-ownership advantage. German policy makers signal further incentive cuts for hybrids by 2027, accelerating BEV share gains. Suppliers focus engineering resources on 400 V and 800 V BEV packs, while maintaining modular tooling to convert select lines to hybrid modules when demand warrants.

By Battery Chemistry: Lithium Manganese Iron Phosphate (LMFP) Surge Erodes Nickel Manganese Cobalt (NMC) Leadership

NMC commanded 51.62% of Germany's EV battery pack market share in 2025, but LFP and LMFP chemistries will outpace nickel systems through 2031 thanks to cost and safety benefits. LMFP’s 230 Wh kg⁻¹ rating allows mainstream sedans to hit 400 km range targets without cobalt or high-purity nickel. German automakers position LMFP in entry-and mid-segment models, reserving NMC for flagship SUVs requiring maximum range.

Lower-temperature runaway risk in LFP/LMFP permits thinner separators and more compact modules, cutting pack-level cost. Recycling processes for iron-based cathodes also require less energy, aligning with EU carbon-footprint declarations. Suppliers maintain chemistry-agnostic electrode lines to hedge against raw-material volatility, enhancing long-term commercial flexibility across the German EV battery pack industry.

By Capacity: High-Energy Systems Drive Premium Revenue

The 60-80 kWh band held 39.62% share in 2025, the sweet spot for midsize cars, balancing motorway range and price. Above-150 kWh packs are poised to grow at 16.55% CAGR through 2031 as premium brands and heavy-duty fleets need extended range between charging stops. Improvements in high-rate charging and thermal spreading enable 150 kWh packs to add only 25% more weight versus 2023 models while delivering 40% more energy.

Fleet operators deploying electric box trucks favor 120-180 kWh packs sized for one-shift duty cycles. Luxury vehicle buyers equate larger packs with status and convenience, sustaining robust demand despite higher list prices. This stratification boosts average selling price and margin contribution, supporting reinvestment in next-generation cell formats across the German EV battery pack market.

By Battery Form: Prismatic Packaging Maximizes Volume Utilization

Prismatic cells secured a 45.71% share in 2025 and are set for a 16.98% CAGR to 2031 as platform engineers prioritize under-floor space efficiency. The rectangular shape aligns seamlessly inside the skateboard chassis, reducing voids and enabling cell-to-pack transitions that skip module casings. Cylindrical formats persist in high-power sports cars due to superior thermal dissipation, while pouch cells serve niche designs requiring curvature.

Advances in laser-welded tabless prismatic designs elevate cycle life, narrowing historic durability gaps with cylindrical variants. Simplified pack assembly trims labor minutes per vehicle, partially offsetting Germany’s wage premium. Therefore, Prismatic dominance reflects engineering optimization and cost-down imperatives within the German engineering optimization and cost-down imperatives within the Germany EV battery pack market.

By Voltage Class: 800 V Systems Unlock Rapid Recharging

Sub-400 V architectures formed 62.35% of installations in 2025, yet 600-800 V designs will post the fastest 16.03% CAGR through 2031. Porsche and Audi demonstrate 5-minute 0-80% top-ups at 800 V, resetting consumer expectations for long-distance trips. Higher voltage cuts current, reducing copper mass and heat losses, particularly beneficial in 100 kWh-plus packs.

Charging-infrastructure providers align investment roadmaps with 800 V compatibility, while backward-compatible converters protect legacy fleets. Suppliers adapt BMS algorithms to manage greater insulation and isolation requirements. Cost deltas narrow as 800 V power electronics scale, accelerating adoption in upper-mid and premium segments of the Germany EV battery pack market.

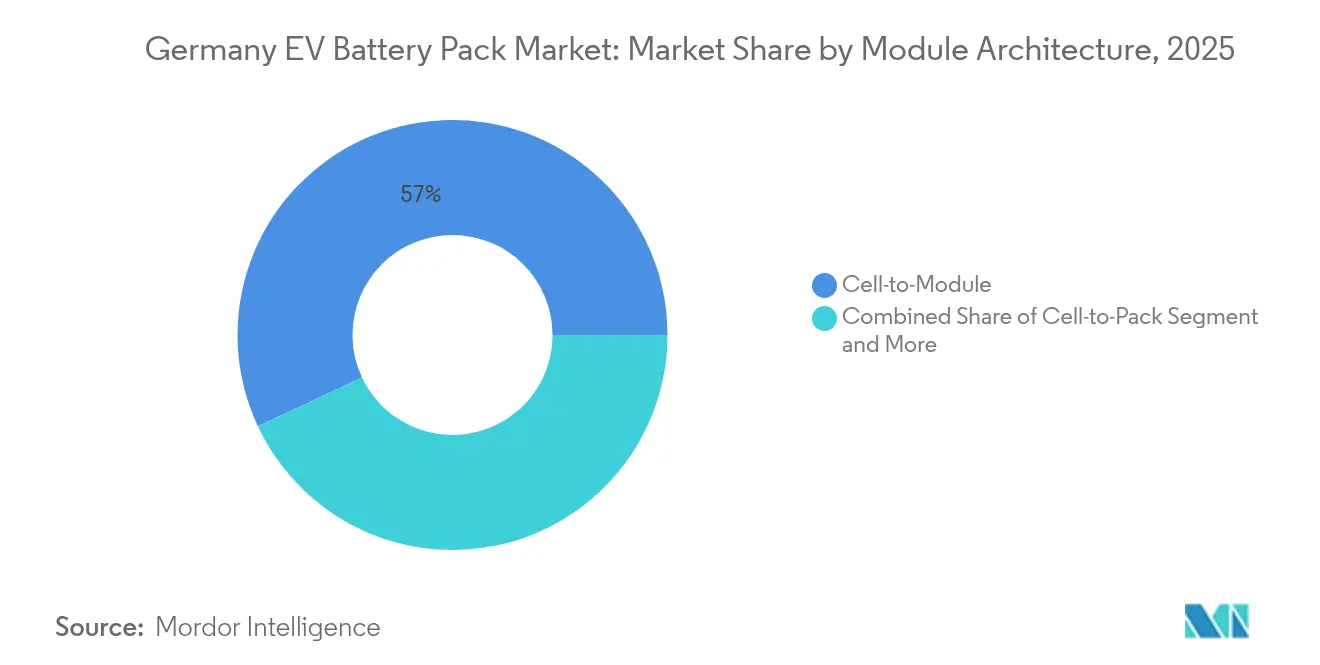

By Module Architecture: Cell-to-Pack (CTP) Gains Production Traction

Module-to-pack represented 56.98% share in 2025, yet CTP will capture incremental growth with a 15.22% CAGR through 2031. Eliminating module casings raises usable volume by 10-15%, translating to range gains without enlarging the chassis footprint. CATL’s third-generation CTP leads commercial implementation, and German lines are retooling to accommodate large top-loading prismatic cells.

CTP reduces parts count and assembly steps, offsetting initial capex through labor savings and scrap reduction. Integrated liquid-cooling plates maintain uniform cell temperatures, enhancing cycle life. Adoption proceeds fastest on new dedicated BEV platforms, while legacy lines retain module structures to preserve backward compatibility.

By Component: Separator Innovation Outpaces Cathode Dominance

Cathodes remained the most significant value contributor at 34.11% in 2025, given raw-material intensity. Even so, separators will grow at 15.41% CAGR through 2031 as thinner, ceramic-coated films enable higher energy density and safety margins. Leading polymer suppliers introduce 5 µm multilayer membranes with shutdown characteristics activating at 135 °C, essential for large prismatic stacks.

Anode suppliers scramble to diversify graphite beyond Chinese sources, trialing Swedish natural flakes and U.S. synthetic grades. Electrolyte blenders adopt high-voltage additives compatible with 800 V packs, expanding addressable formulation demand. Vertical integration into separator films offers German chemical firms new revenue streams while securing domestic supply for future capacity expansions.

Geography Analysis

Germany remains the epicenter of European battery activity, claiming more new cell-production announcements between 2024 and 2025. The German EV battery pack market benefits from clustering effects surrounding Heide, Thuringia, and Berlin, where combined annual output will top 100 GWh by 2027. Co-located cell and vehicle plants shorten logistics paths to Bavarian and Lower Saxon assembly hubs, cutting transit time to under six hours and reducing inventory buffers. Renewable electricity share above 50% lowers cradle-to-gate carbon footprints, assisting compliance with EU Battery Regulation disclosures.

Exports to France, Italy, and Spain grow as automakers source packs from German facilities to meet local-content rules and minimize shipping risk. Italian commercial-vehicle makers value German engineering support for high-duty cycles, while French OEMs leverage cross-Rhineland rail corridors for just-in-sequence deliveries. The Netherlands and Belgium function as distribution gateways, reinforcing Germany’s central logistical role. Nordic countries sustain the highest regional EV penetration but rely on German pack imports for high-volume segments below luxury price points. Eastern Europe represents an emerging consumer market and low-cost component supplier base. German tier-one suppliers establish satellite module plants in Poland and Czechia to balance wage structures while retaining high-value cell manufacturing domestically. Overall, geographic diversification serves to secure supply continuity yet maintains Germany as the strategic command center of the continental battery ecosystem.

Competitive Landscape

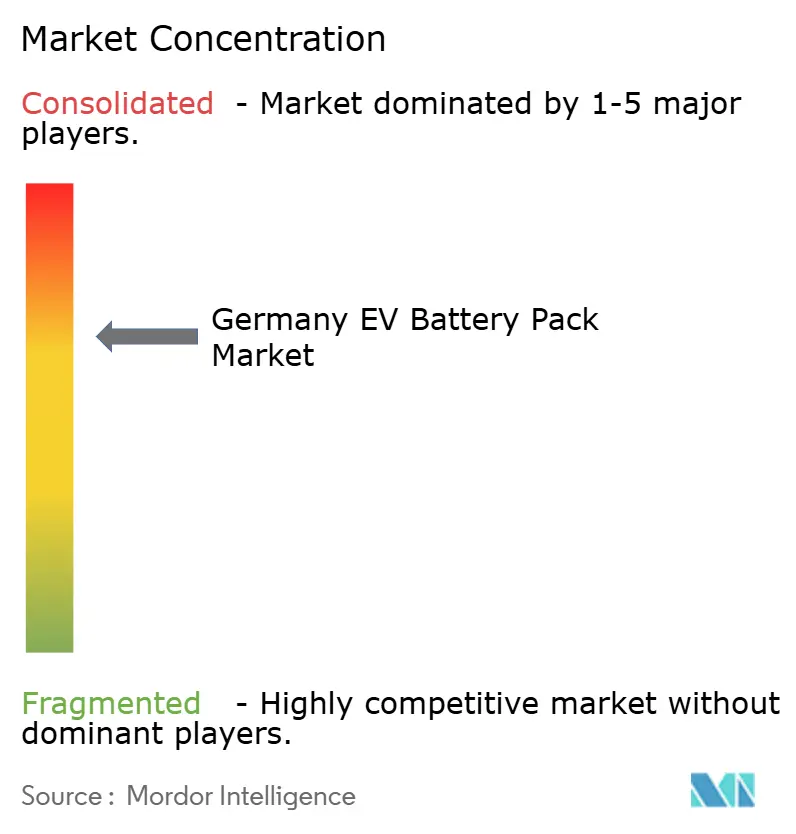

The German EV battery pack market features moderate concentration with CATL, LG Energy Solution, and Samsung SDI sharing space with Northvolt, ACC, and in-house automaker ventures. Asian incumbents bring unrivaled scale, but EU regulations tilt procurement toward local sites achieving recycled-content thresholds. CATL leverages its Thuringia plant to anchor German OEM contracts, while Northvolt positions Heide as Europe’s premium nickel-free supply hub.

Technology differentiation centers on LMFP rollout, 800 V architectures, and cell-to-pack manufacturing. LG Energy Solution partners with Porsche on silicon-rich anodes for ultra-fast charging, whereas Samsung SDI secures BMW’s cylindrical-cell program valued at EUR 2.8 billion. Automakers hedge reliance by launching joint ventures: Volkswagen pairs with QuantumScape for solid-state pilots, and Mercedes-Benz allies with Umicore on closed-loop recycling.

Cost structures remain sensitive to electricity and labor premiums, encouraging automation investments and renewable PPAs. Firms with vertically integrated cathode and recycling capacity hedge raw-material exposure and strengthen ESG credentials, which are increasingly vital in OEM supplier scoring matrices. Thus, competitive dynamics pivot more on compliance readiness and technological agility than purely on price.

Germany EV Battery Pack Industry Leaders

Contemporary Amperex Technology Co. Ltd. (CATL)

LG Energy Solution Ltd.

Samsung SDI Co. Ltd.

Automotive Cells Company (ACC)

BMZ Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: IBU-tec advanced materials AG ("IBU-tec") inked a deal with PowerCo SE to produce LFP battery materials. As per the agreement, starting in 2026, IBU-tec will manufacture LFP cathode material for automotive uses at its Weimar site, exclusively for PowerCo. By 2028, IBU-tec targets to fully utilize its production capacity, aiming for over 3,000 tons annually of LFP battery materials.

- January 2024: In line with the Green Deal Industrial Plan, the European Commission has greenlit a EUR 902 million initiative in Germany, backing Northvolt's new electric vehicle battery plant. This measure aims to accelerate the transition to a net-zero economy by supporting the production of sustainable batteries, which are critical for the growing electric vehicle market.

- November 2024: PowerCo, Volkswagen Group's battery division, has teamed up with QuantumScape in a landmark deal aimed at bringing QuantumScape's advanced solid-state lithium-metal battery technology to the industrial forefront. This collaboration seeks to accelerate the commercialization of next-generation battery solutions, which promise to enhance energy density, charging speed, and overall performance, thereby addressing critical challenges in the electric vehicle market.

Germany EV Battery Pack Market Report Scope

The Germany EV Battery Pack Market Report is Segmented by Vehicle Type (Passenger Car, and More), Propulsion Type (BEV, and More), Battery Chemistry (LFP, and More), Capacity (Less than 15 kWh, and More), Battery Form (Cylindrical, and More), Voltage Class (Below 400V, and More), Module Architecture (Cell-to-Module, and More), Component (Anode, and More). The Market Forecasts are Provided in Terms of Value (USD).

| Passenger Car |

| Light Commercial Vehicles |

| Medium and Heavy Duty Trucks |

| Bus |

| Baterry Electric Vehicle |

| Plug-in Hybrid Electric Vehicle |

| Lithium Iron Phosphate (LFP) |

| Lithium Manganese Iron Phosphate (LMFP) |

| Nickel Manganese Cobalt (NMC) (111 / 523 / 622 / 712 / 811) |

| Nickel Cobalt Aluminum (NCA) |

| lithium-titanium-oxide (LTO) |

| Others |

| Less than 15 kWh |

| 15 kWh to 40 kWh |

| 40 kWh to 60 kWh |

| 60 kWh to 80 kWh |

| 80 kWh to 100 kWh |

| 100 kWh to 150 kWh |

| Above 150 kWh |

| Cylindrical |

| Pouch |

| Prismatic |

| Below 400 V (48- 350 V) |

| 400 - 600 V |

| 600 - 800 V |

| Above 800 V |

| Cell-to-Module (CTM) |

| Cell-to-Pack (CTP) |

| Module-to-Pack (MTP) |

| Anode |

| Cathode |

| Electrolyte |

| Separator |

| By Vehicle Type | Passenger Car |

| Light Commercial Vehicles | |

| Medium and Heavy Duty Trucks | |

| Bus | |

| By Propulsion Type | Baterry Electric Vehicle |

| Plug-in Hybrid Electric Vehicle | |

| By Battery Chemistry | Lithium Iron Phosphate (LFP) |

| Lithium Manganese Iron Phosphate (LMFP) | |

| Nickel Manganese Cobalt (NMC) (111 / 523 / 622 / 712 / 811) | |

| Nickel Cobalt Aluminum (NCA) | |

| lithium-titanium-oxide (LTO) | |

| Others | |

| By Capacity | Less than 15 kWh |

| 15 kWh to 40 kWh | |

| 40 kWh to 60 kWh | |

| 60 kWh to 80 kWh | |

| 80 kWh to 100 kWh | |

| 100 kWh to 150 kWh | |

| Above 150 kWh | |

| By Battery Form | Cylindrical |

| Pouch | |

| Prismatic | |

| By Voltage Class | Below 400 V (48- 350 V) |

| 400 - 600 V | |

| 600 - 800 V | |

| Above 800 V | |

| By Module Architecture | Cell-to-Module (CTM) |

| Cell-to-Pack (CTP) | |

| Module-to-Pack (MTP) | |

| By Component | Anode |

| Cathode | |

| Electrolyte | |

| Separator |

Market Definition

- Battery Chemistry - Various types of battery chemistry considred under this segment include LFP, NCA, NCM, NMC, Others.

- Battery Form - The types of battery forms offered under this segment include Cylindrical, Pouch and Prismatic.

- Body Type - Body types considered under this segment include, passenger cars, LCV (light commercial vehicle), M&HDT (medium & heavy duty trucks)and buses.

- Capacity - Various types of battery capacities inldude under theis segment are 15 kWH to 40 kWH, 40 kWh to 80 kWh, Above 80 kWh and Less than 15 kWh.

- Component - Various components covered under this segment include anode, cathode, electrolyte, separator.

- Material Type - Various material covered under this segment include cobalt, lithium, manganese, natural graphite, nickel, other material.

- Method - The types of method covered under this segment include laser and wire.

- Propulsion Type - Propulsion types considered under this segment include BEV (Battery electric vehicles), PHEV (plug-in hybrid electric vehicle).

- ToC Type - ToC 1

- Vehicle Type - Vehicle type considered under this segment include passenger vehicles, and commercial vehicles with various EV powertrains.

| Keyword | Definition |

|---|---|

| Electric vehicle (EV) | A vehicle which uses one or more electric motors for propulsion. Includes cars, buses, and trucks. This term includes all-electric vehicles or battery electric vehicles and plug-in hybrid electric vehicles. |

| PEV | A plug-in electric vehicle is an electric vehicle that can be externally charged and generally includes all electric vehicles as well as plug-electric vehicles as well as plug-in hybrids. |

| Battery-as-a-Service | A business model in which the battery of an EV can be rented from a service provider or swapped with another battery when it runs out of charge |

| Battery Cell | The basic unit of an electric vehicle's battery pack, typically a lithium-ion cell, that stores electrical energy. |

| Module | A subsection of an EV battery pack, consisting of several cells grouped together, often used to facilitate manufacturing and maintenance. |

| Battery Management System (BMS) | An electronic system that manages a rechargeable battery by protecting the battery from operating outside its safe operating area, monitoring its state, calculating secondary data, reporting data, controlling its environment, and balancing it. |

| Energy Density | A measure of how much energy a battery cell can store in a given volume, usually expressed in watt-hours per liter (Wh/L). |

| Power Density | The rate at which energy can be delivered by the battery, often measured in watts per kilogram (W/kg). |

| Cycle Life | The number of complete charge-discharge cycles a battery can perform before its capacity falls under a specified percentage of its original capacity. |

| State of Charge (SOC) | A measurement, expressed as a percentage, that represents the current level of charge in a battery compared to its capacity. |

| State of Health (SOH) | An indicator of the overall condition of a battery, reflecting its current performance compared to when it was new. |

| Thermal Management System | A system designed to maintain optimal operating temperatures for an EV's battery pack, often using cooling or heating methods. |

| Fast Charging | A method of charging an EV battery at a much faster rate than standard charging, typically requiring specialized charging equipment. |

| Regenerative Braking | A system in electric and hybrid vehicles that recovers energy normally lost during braking and stores it in the battery. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all its reports.

- Step-1: Identify Key Variables: To build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built based on these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. Market revenue is calculated by multiplying the volume demand with volume-weighted average battery pack price (per kWh). Battery pack price estimation and forecast takes into account various factors affecting ASP, such as inflation rates, market demand shifts, production costs, technological developments, and consumer preferences, providing estimations for both historical data and future trends.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms