Germany Electric Commercial Vehicle Battery Pack Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

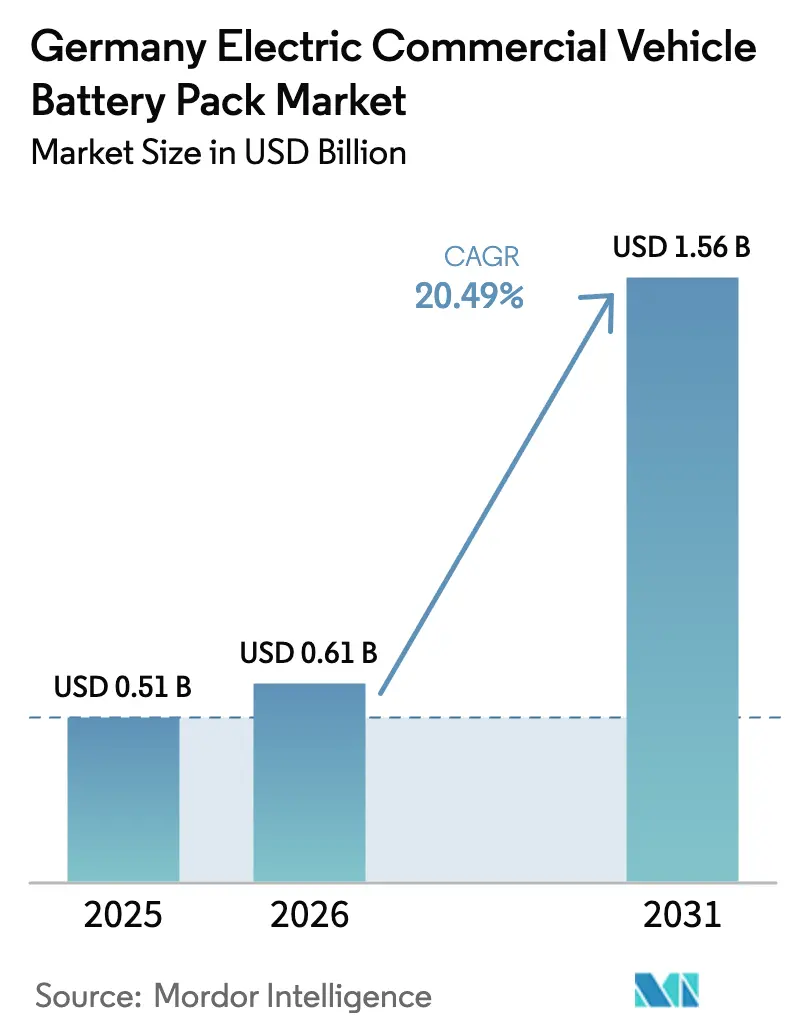

| Base Year Market Size (2025) | USD 0.51 Billion |

| Market Size (2026) | USD 0.61 Billion |

| Market Size (2031) | USD 1.56 Billion |

| Growth Rate (2026 - 2031) | 20.49% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Electric Commercial Vehicle Battery Pack Market Analysis by Mordor Intelligence

The German electric commercial vehicle battery pack market size is expected to increase from USD 0.51 billion in 2025 to USD 0.61 billion in 2026 and reach USD 1.56 billion by 2031, growing at a CAGR of 20.49% over 2026-2031. The acceleration stems from Germany’s pivot away from passenger-EV dominance toward fleet electrification as diesel’s total cost of ownership (TCO) advantage collapses. Operators are increasingly turning to battery-electric trucks and buses, driven by a recalibration of federal subsidies, stringent CO₂ mandates from the EU for heavy-duty vehicles, and a swift drop in costs for lithium-iron-phosphate (LFP) packs. While light commercial vehicles continue to lead in adoption rates, articulated buses and heavy trucks are poised to spearhead the next wave of growth, especially as advanced systems enable rapid charging. Innovations like cell-to-pack architectures and the establishment of localized anode supply chains are driving down pack prices. However, the limited truck-charging corridors are the primary operational hurdle for Germany's electric commercial vehicle battery pack market.

Key Report Takeaways

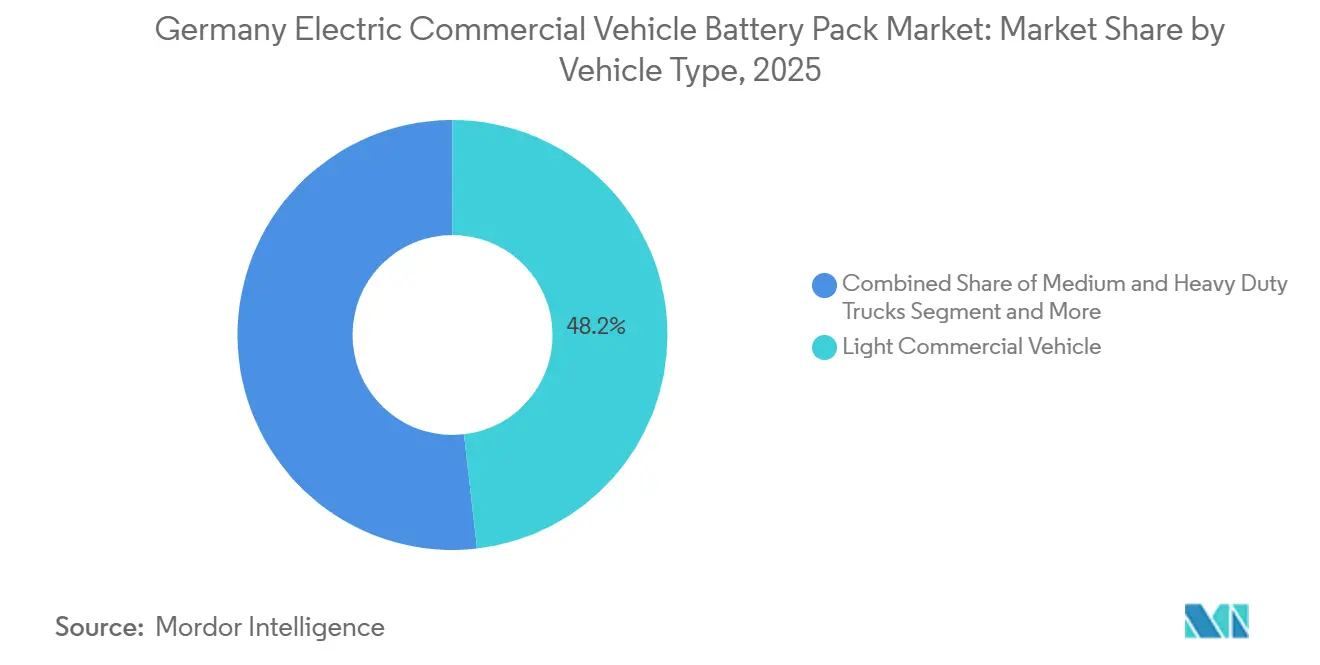

- By vehicle type, light commercial vehicles led with 48.18% of Germany's electric commercial vehicle battery pack market share in 2025; medium and heavy-duty trucks are expected to advance at a 22.38% CAGR through 2031.

- By propulsion, battery-electric platforms captured an 81.62% share of the German electric commercial vehicle battery pack market in 2025, while plug-in hybrids lagged as battery electric vehicle systems grew at a 21.21% CAGR.

- By chemistry, Lithium Iron Phosphate (LFP) held 45.09% of Germany's electric commercial vehicle battery pack market share in 2025. Lithium Manganese Iron Phosphate (LMFP) is projected to expand at a 22.52% CAGR to 2031.

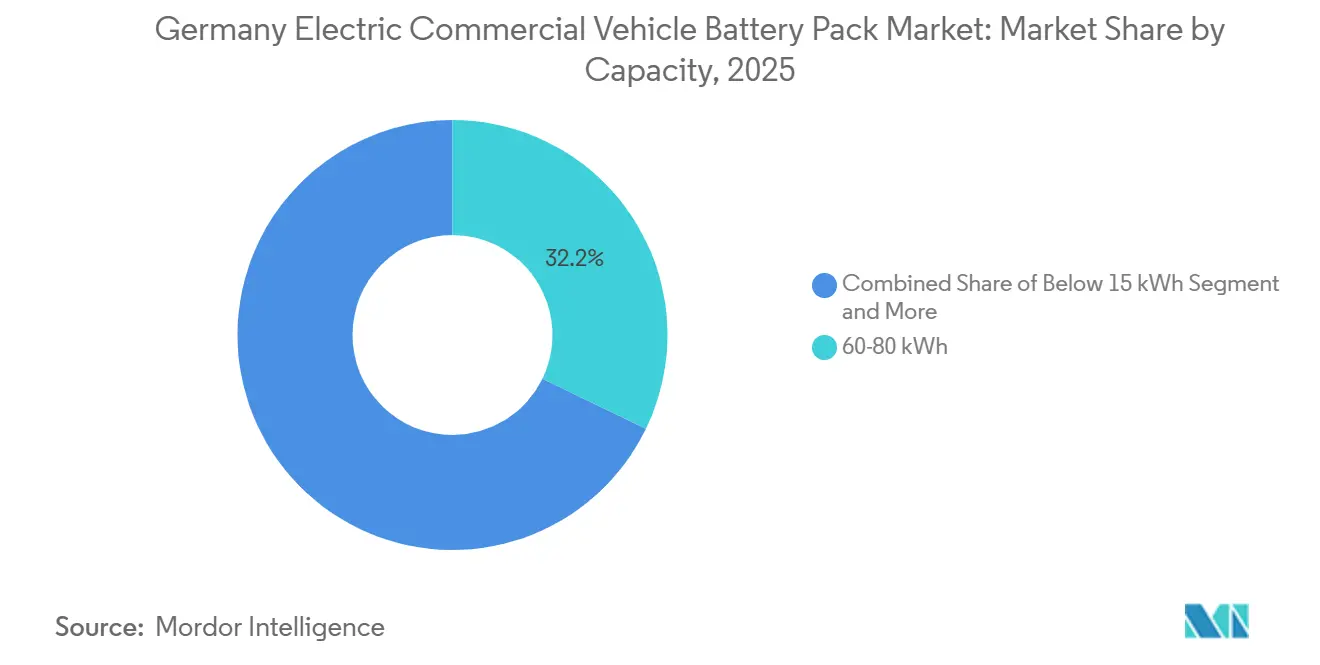

- By capacity, 60-80 kWh packs accounted for a 32.19% share of the German electric commercial vehicle battery pack market in 2025, whereas packs above 150 kWh are expected to grow at a 20.71% CAGR.

- By battery form, prismatic cells led the German electric commercial vehicle battery pack market, accounting for 42.16% of the market in 2025; cylindrical formats posted the fastest growth at a 20.98% CAGR.

- By voltage class, 400-600 V systems accounted for 36.28% of the German electric commercial vehicle battery pack market size in 2025, and solutions above 800 V are on track for a 21.16% CAGR.

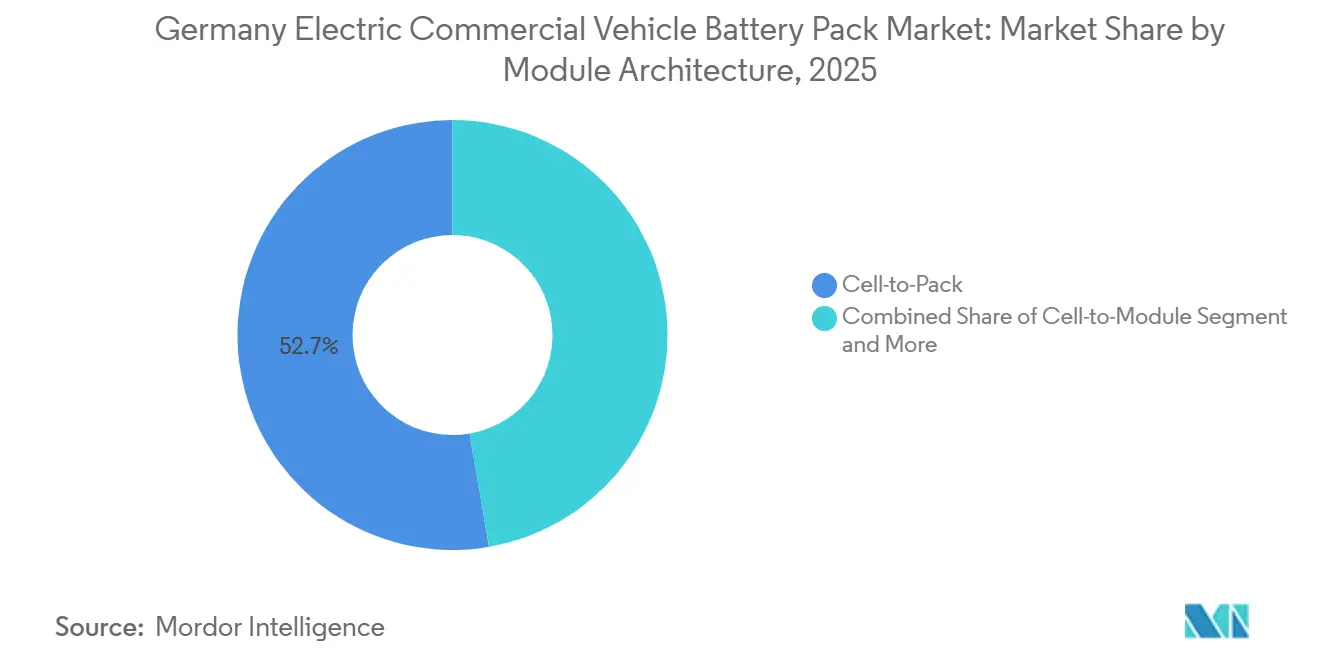

- By module architecture, cell-to-pack designs dominated the German electric commercial vehicle battery pack market, accounting for 52.72% of the market in 2025 and expected to post the fastest 21.41% CAGR through 2031.

- By component, cathodes accounted for 43.12% of the German electric commercial vehicle battery pack market in 2025; anodes recorded the highest 20.82% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Electric Commercial Vehicle Battery Pack Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Federal E-CV Subsidies | +3.2% | Germany, spillover to Austria and Netherlands | Short term (≤ 2 years) |

| Europe HDV CO₂ Targets | +2.8% | Germany with Europe alignment | Long term (≥ 4 years) |

| Lithium Iron Phosphate Cost Decline | +2.1% | Germany and wider Europe base | Medium term (2-4 years) |

| City Logistics Noise Caps | +1.9% | German cities, expanding Europe-wide | Medium term (2-4 years) |

| 800V Coach Platforms | +1.6% | Germany, tech export potential | Medium term (2-4 years) |

| Battery-as-a-Service Contracts | +1.4% | German transit authorities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Federal E-CV Subsidy Program Driving the Market Growth

Germany’s national incentive program is significantly improving the economics of battery-electric trucks. By reducing ownership costs and accelerating procurement timelines, the scheme enables faster fleet transitions and makes electric commercial vehicles more attractive to operators [1]“Commercial Vehicle Subsidy Guidelines 2024-27,”, Federal Ministry for Digital and Transport, bmvi.de. Local-content clauses shield domestic suppliers and partially neutralize Chinese cost advantages. The program focuses on packs above 40 kWh, catalyzing demand in medium and heavy-duty classes facing infrastructure gaps. Stakeholders voice concern that the 2027 sunset could create a volume cliff, yet near-term pull-forward orders lend momentum to the German electric commercial vehicle battery pack market. OEMs are now front-loading production schedules to maximize grant capture and lock in cell allocations.

EU HDV CO₂ Targets

Brussels’ requirement for a 90% cut in heavy-duty vehicle emissions by 2040 converts battery demand from optional to obligatory[2]“Regulation (EU) 2024/2823 on Heavy-Duty Vehicle CO₂ Standards,”, European Commission, europa.eu. Non-compliant trucks will attract penalties per gram of excess CO₂, forcing German OEMs to cease new internal-combustion programs. Interim 2030 targets accelerate platform redesign, pushing the German electric commercial vehicle battery pack market toward higher-capacity packs over hybrid stopgaps. Procurement teams now secure four-year supply contracts to de-risk compliance. The regulation stabilizes long-run demand but intensifies short-term sourcing pressure.

LFP Pack Cost Drops Below USD 100/kWh

In 2025, urban delivery fleets will be operating electric vehicles at costs on par with diesel counterparts, due to declining battery pack prices and without the need for government subsidies[3]“Battery Price Survey 2025,”, BloombergNEF, bloomberg.com. This transformation is primarily driven by advancements in battery chemistry, notably a diminished dependence on volatile commodities like cobalt and nickel, leading to more stable operating costs. Major logistics players, including Deutsche Post and DB Schenker, have ramped up orders for electric vans, signaling robust, escalating demand in the German market. This heightened adoption is bolstering the foundational demand for electric commercial vehicles.

Manufacturers channel investments into European-based cell assembly to navigate geopolitical risks and bolster supply chain resilience. Looking to the future, industry experts predict continued declines in battery costs, potentially paving the way for the electrification of larger regional trucks to become both feasible and profitable by decade's end.

Battery-as-a-Service Bus Contracts

German transit agencies are leasing batteries for e-buses through service-fee plans, slashing upfront vehicle costs significantly. Providers take on the risks of degradation and recycling, transitioning batteries into second-life storage post fleet usage. This model not only liberates municipal budgets but is also making inroads into freight, broadening its market appeal. Financial institutions are drawn to Battery-as-a-Service (BaaS) for its cash flow profiles, which mirror those of infrastructure assets. Such a framework not only diversifies revenue streams in Germany's electric commercial vehicle battery pack market but also smooths the path for smaller operators to adopt these innovations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sparse Truck-Charging Corridors | -2.3% | German highways, cross-border routes | Medium term (2-4 years) |

| Up-Front Cost Premium vs Diesel | -1.8% | Germany, fleet budgets | Short term (≤ 2 years) |

| Graphite-Plant Permitting Delays | -1.2% | German industrial regions | Long term (≥ 4 years) |

| Lithium Manganese Iron Phosphate License-Fee Volatility | -0.9% | German cell makers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Sparse Truck-Charging Corridors

Major logistics firms are increasingly turning to electric urban delivery fleets due to a significant drop in battery pack prices, making them competitive with diesel. Yet, the infrastructure hasn't kept pace, particularly for heavy-duty vehicles. The number of fast-charging points falls short of targets, curtailing long-haul efficiency and potentially leading to future bottlenecks if the rollout doesn't speed up. As a stopgap, OEMs are deploying mobile charging trailers, and in a strategic move to mitigate geopolitical risks, supply chains are pivoting towards European cell assembly.

Graphite-Plant Permitting Delays

Despite efforts to bolster domestic production, a significant share of processed graphite in Germany remains reliant on imports. New plants in the EU face a lengthy hurdle: securing environmental permits can take considerable time. German cell manufacturers, prioritizing safety, maintain higher stock levels, which, in turn, tie up their working capital. This cautious approach underscores the market's fragility: any disruption in trade could significantly impact the production of battery packs, especially for light commercial vehicles, which represent the largest volume segment of the market. While policymakers are actively drafting more streamlined regulations, the timelines for implementation remain unclear. Such uncertainties, especially around raw-material bottlenecks, cast a shadow on the outlook for Germany's electric commercial vehicle battery-pack market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Regulatory Mandates Lift Heavy-Duty Adoption

Light commercial vehicles (LCVs) held 48.18% of Germany's electric commercial vehicle battery pack market share in 2025, underpinned by courier and postal fleets operating 100-200 km daily routes. Shipment surges in e-commerce sustain baseline pack demand in the 60-80 kWh bracket. In contrast, medium and heavy trucks show the swiftest 22.38% CAGR as policy subsidies override lingering cost and payload concerns. Federal grants for heavy trucks have expedited orders and hastened platform launches. Urban noise regulations and low-emission zones are bolstering the electrification of light commercial vehicles (LCVs), while EU CO₂ penalties are steering original equipment manufacturers (OEMs) towards battery-electric drivetrains for long hauls.

Fleet operators are consolidating orders to gain priority production slots and negotiate better pricing on bulk cells. The focus of innovation is on modular pack designs that enable fleets to interchange cartridges for optimized range. While overnight depot charging is standard for LCVs, public high-power stations are essential for trucks on long routes. As a result, the German market for electric commercial vehicle battery packs is charting a dual-speed path: LCV volumes are driving early revenues, while truck platforms are poised to achieve scale in the future.

By Propulsion Type: Battery-Electric Dominance Becomes Structural

Battery-electric vehicles captured 81.62% of 2025 deliveries and will log a 21.21% CAGR as OEMs phase out plug-in hybrids. Zero-tailpipe-emission rules and simpler driveline maintenance tilt fleets toward BEVs despite higher initial prices. PHEVs are only found in regional bus operators that lack depot power upgrades. Regulatory credit systems also incentivize pure BEVs, deepening their advantage in the German electric commercial vehicle battery pack market for propulsion solutions.

Charging ecosystems are adapting: depot smart-charging software staggers load to avoid peak tariffs, while megawatt chargers are piloting along the Rhine-Main corridor. Component suppliers now tune thermal systems to enable quicker DC fast-charge cycles to meet tight delivery windows. With residual values stabilizing, leasing companies are increasingly open to underwriting BEV fleets, thereby broadening access for SMEs. Stakeholders anticipate that PHEV market share will decline, further solidifying the momentum behind battery-electric platforms.

By Battery Chemistry: LFP Leads While LMFP Gains Traction

LFP packs commanded a 45.09% share in 2025 due to their lower costs, safety, and stable supply chains. The absence of nickel and cobalt shields prices from metal volatility, giving LFP a strategic edge in the German electric commercial vehicle battery pack market. LMFP, however, posts a brisk 22.52% CAGR, promising an energy density 10-15% higher without compromising thermal stability. OEMs earmark LMFP for premium regional trucks, where pack-weight savings enable extra payload.

NMC chemistries remain essential for long-range buses that require compact footprints, yet high-nickel blends are subject to price swings. Suppliers are increasingly co-locating LFP and LMFP lines to hedge against demand shifts. Solid-state prototypes are entering validation but will not influence volume before 2029. Chemistries are evolving from cost-driven dominance toward performance-tiered portfolios that let fleets match pack characteristics to duty cycles.

By Capacity: Mid-Range Sweet Spot, High-End Surge

The 60-80 kWh bracket delivered 32.19% of 2025 revenue, bolstered by last-mile vans and municipal service vehicles. Above-150 kWh units are growing at a 20.71% CAGR as highway e-trucks and intercity coaches seek 500-km autonomy. Depot charge patterns favor smaller battery packs for mid-distance distribution. However, next-gen systems are leaning towards larger packs to harness the potential of ultra-fast chargers. Once the Deutschlandnetz infrastructure hits its milestones, Germany's electric commercial vehicle battery pack market, particularly in high-capacity segments, stands poised to grow significantly.

Designers are now embedding structural packs into chassis beams, achieving weight reduction and maximizing cargo space. With modular capacity scaling, fleet operators can optimally size batteries for varying duty cycles. To promote heavier loads in long-haul trucks, policymakers are mulling over road-toll rebates linked to vehicle capacity. This capacity mix strikes a balance between cost-effectiveness and energy demand, especially as technological advancements increase energy density and reduce charging downtime.

By Battery Form: Prismatic Efficiency vs Cylindrical Scalability

Prismatic cells led with a 42.16% share in 2025, prized for packaging efficiency and straightforward thermal paths. Large flat cells simplify bus-bar layouts and suit cell-to-pack formats pivotal to the German electric commercial vehicle battery pack market. Cylindrical 4680-type cells, however, record a 20.98% CAGR, riding economies of scale from passenger-car lines. Pouch formats cater to custom retrofits where flexible stacking matters more than volumetric density.

Manufacturers optimize cooling plates for prismatic blocks, trimming assembly time. Cylindrical packs gain ground in cost-sensitive LCVs where slightly lower volumetric density is an acceptable trade-off. As cylinder energy density approaches prismatic levels, mixed-form strategies may emerge. For now, form-factor choices reflect supply contracts and platform heritage rather than clear technical superiority.

By Voltage Class: Legacy 400-600 V Systems Give Way to >800 V

Systems operating at 400-600 V represented 36.28% of 2025 shipments, mirroring legacy passenger-car architectures. The push to slash charging times is driving above-800-V solutions at a 21.16% CAGR, particularly for heavy trucks. Mid-tier 600-800 V packages bridge existing depot hardware and megawatt future standards. Component suppliers expand insulation ratings and develop high-voltage contactors to support the transition in the German electric commercial vehicle battery pack market.

Inverters and onboard chargers evolve in lockstep, raising upfront costs but lowering lifetime operating expenses through efficiency gains. Fleets with tight route schedules factor in downtime savings to justify the premium. Industry consensus expects above 800 V to dominate new long-haul platforms after 2028, although dual-voltage strategies may persist during infrastructure build-out.

By Module Architecture: Cell-to-Pack Redefines Integration

Cell-to-pack architecture captured a 52.72% share and sits atop the growth chart with a 21.41% CAGR. Eliminating intermediate modules slashes parts count and lifts volumetric energy density by roughly 15%. German producers retrofit thermal buffers between cell rows to meet stringent UNECE fire-safety rules. Cell-to-module formats still appeal to operators who value easy field service. Module-to-pack stays relevant for bespoke chassis conversions in specialist fleets.

As pack designs converge on structural concepts, OEMs reclaim under-floor space for payload. CTP also dovetails with prismatic-cell dominance, reinforcing mutual uptake. The architecture shift anchors cost declines, making subsidy-free price parity plausible in light-duty segments by 2028.

By Component: Cathode Dominance, Anode Momentum

Cathodes accounted for 43.12% of the 2025 bill-of-materials value, making them the primary leverage point for cost and performance. High-manganese LFP and LMFP mixes cut costs yet preserve stability. Anodes grow at 20.82% CAGR as silicon-enhanced graphite lifts energy density by up to 20%. Incremental improvements in electrolytes and separators are paving the way for crucial breakthroughs in solid-state technology advancements anticipated later in the decade.

To mitigate raw material volatility, German manufacturers are adopting closed-loop cathode recycling, achieving high recovery rates for lithium and manganese. This vertical integration not only safeguards profit margins but also ensures regulatory traceability compliance. Consequently, the evolution of these components aligns with the overarching trend in Germany's electric commercial vehicle battery pack market, which is characterized by a push for efficiency-driven innovations and a focus on capturing localized value.

Geography Analysis

Germany anchors European supply chains with multiple gigafactories coming online and the continent’s most comprehensive incentive regime. Domestic OEMs have locked in long-term cell contracts that guarantee volume for the German electric commercial vehicle battery pack market and meet local-content thresholds. Federal infrastructure plans also align depot charging grants with freight corridors, smoothing deployment.

Neighboring France and the Netherlands adopt similar CO₂ targets and offer tax breaks for zero-emission trucks, creating export avenues for German pack assemblers. Cross-border logistics fleets increasingly standardize on German-spec 400-600 V systems to streamline maintenance. Eastern Europe lags due to economic constraints and sparse charging, but remains a strategic growth frontier once EU cohesion funds address infrastructure gaps.

Northern Europe’s early uptake provides a proving ground for >800 V platforms, giving German suppliers field data for second-generation designs. Germany’s central location shortens lead times to Scandinavian ports and Iberian distribution centers, reinforcing its hub status. Regulatory synchronization and logistical adjacency collectively sustain a regional multiplier effect that bolsters the German electric commercial vehicle battery pack market beyond domestic borders.

Competitive Landscape

Market concentration remains moderate as global heavyweights and European newcomers vie for OEM contracts. CATL’s EUR 7.3 billion (USD 8.54 billion) expansion in Erfurt lifts capacity to 100 GWh by 2026, narrowing cost gaps with Asian imports. BYD’s localized assembly enables fleet operators to access integrated chassis-plus-battery offerings. Home-grown contenders Northvolt and PowerCo prioritize strategic tie-ups with Daimler, MAN, and Volkswagen, emphasizing supply-chain sovereignty.

Samsung SDI’s decade-long deal to supply Daimler consolidates high-energy nickel-rich packs for premium trucks. Smaller German integrators compete on niche applications such as refrigerated vans and refuse trucks where customization trumps scale. Battery-as-a-Service entrants like Leclanché carve out service revenues, diversifying the value pools of the German electric commercial vehicle battery pack industry.

Regulatory tilt toward European content could tip volume in favor of Northvolt and ACC once ramp-ups stabilize. Yet Chinese players still hold a technological lead in LMFP and CTP implementations, compelling local firms to accelerate R&D alliances. Competitive dynamics thus hinge on a blend of capacity, chemistry, leadership, and policy navigation.

Germany Electric Commercial Vehicle Battery Pack Industry Leaders

Contemporary Amperex Technology Co. Ltd. (CATL)

NorthVolt AB

Samsung SDI Co. Ltd.

LG Energy Solution Ltd.

BYD Company Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Mercedes-Benz Trucks unveiled the eActros 400, a fresh battery-electric truck variant, drawing from the technology of the eActros 600. The eActros 400 features two 207 kWh LFP battery packs, totaling 414 kWh, showcasing advancements in the battery pack market with its high energy density and efficiency, which contribute to the growing adoption of electric vehicles.

- May 2025: Daimler Buses is set to unveil its latest innovations at the UITP Summit 2025 in Hamburg, emphasizing sustainability, cost-efficiency, and the digital evolution of electric city buses. Making its public debut at the summit, the Mercedes-Benz eCitaro will feature a new, more powerful fourth-generation NMC battery (NMC4), highlighting advancements in the battery pack market.

Germany Electric Commercial Vehicle Battery Pack Market Report Scope

The Germany commercial vehicle EV battery pack market report is segmented by vehicle type (light commercial vehicle, medium and heavy duty truck, and bus), propulsion type (battery electric vehicle, and plug-in hybrid electric vehicle), battery chemistry (lithium iron phosphate, LMP (lithium manganese iron phosphate), NMC (nickel manganese cobalt oxide), NCA (nickel cobalt aluminum oxide), LTO (lithium titanium oxide), and others (LCO, LMO, NMX, emerging battery technologies, etc.)), capacity (below 15 kwh, 15 kWh - 40 kWh, 40 kWh - 60 kWh, 60 kWh - 80 kWh, 80 kWh - 100 kWh, 100 kWh - 150 kWh, and above 150 kWh), battery form (cylindrical, pouch, and prismatic), voltage class (below 400 v, 400-600 V, 600-800 V, and above 800 V), module architecture ( CTM, CTO, and MTP), and component (anode, cathode, electrolyte, and separator). The market forecasts are provided in terms of value (USD) and volume (units).

| Light Commercial Vehicle |

| Medium and Heavy Duty Truck |

| Bus |

| Baterry Electric Vehicle |

| Plug-in Hybrid Electric Vehicle |

| LFP (Lithium Iron Phosphate) |

| LMFP (Lithium Manganese Iron Phosphate) |

| NMC (Nickel Manganese Cobalt Oxide) |

| NCA (Nickel Cobalt Aluminum Oxide) |

| LTO (Lithium Titanium Oxide) |

| Others (LCO, LMO, NMX, Emerging Battery Technologies, etc.) |

| Below 15 kWh |

| 15-40 kWh |

| 40-60 kWh |

| 60-80 kWh |

| 80-100 kWh |

| 100-150 kWh |

| Above 150 kWh |

| Cylindrical |

| Pouch |

| Prismatic |

| Below 400 V (48-350 V) |

| 400-600 V |

| 600-800 V |

| Above 800 V |

| Cell-to-Module (CTM) |

| Cell-to-Pack (CTP) |

| Module-to-Pack (MTP) |

| Anode |

| Cathode |

| Electrolyte |

| Separator |

| By Vehicle Type | Light Commercial Vehicle |

| Medium and Heavy Duty Truck | |

| Bus | |

| By Propulsion Type | Baterry Electric Vehicle |

| Plug-in Hybrid Electric Vehicle | |

| By Battery Chemistry | LFP (Lithium Iron Phosphate) |

| LMFP (Lithium Manganese Iron Phosphate) | |

| NMC (Nickel Manganese Cobalt Oxide) | |

| NCA (Nickel Cobalt Aluminum Oxide) | |

| LTO (Lithium Titanium Oxide) | |

| Others (LCO, LMO, NMX, Emerging Battery Technologies, etc.) | |

| By Capacity | Below 15 kWh |

| 15-40 kWh | |

| 40-60 kWh | |

| 60-80 kWh | |

| 80-100 kWh | |

| 100-150 kWh | |

| Above 150 kWh | |

| By Battery Form | Cylindrical |

| Pouch | |

| Prismatic | |

| By Voltage Class | Below 400 V (48-350 V) |

| 400-600 V | |

| 600-800 V | |

| Above 800 V | |

| By Module Architecture | Cell-to-Module (CTM) |

| Cell-to-Pack (CTP) | |

| Module-to-Pack (MTP) | |

| By Component | Anode |

| Cathode | |

| Electrolyte | |

| Separator |

Market Definition

- Battery Chemistry - Various types of battery chemistry considred under this segment include LFP, NCA, NCM, NMC, Others.

- Battery Form - The types of battery forms offered under this segment include Cylindrical, Pouch and Prismatic.

- Body Type - Body types considered under this segment include, LCV (light commercial vehicle), M&HDT (medium & heavy duty trucks)and buses.

- Capacity - Various types of battery capacities inldude under theis segment are 15 kWH to 40 kWH, 40 kWh to 80 kWh, Above 80 kWh and Less than 15 kWh.

- Component - Various components covered under this segment include anode, cathode, electrolyte, separator.

- Material Type - Various material covered under this segment include cobalt, lithium, manganese, natural graphite, nickel, other material.

- Method - The types of method covered under this segment include laser and wire.

- Propulsion Type - Propulsion types considered under this segment include BEV (Battery electric vehicles), PHEV (plug-in hybrid electric vehicle).

- ToC Type - ToC 2

- Vehicle Type - Vehicle type considered under this segment include commercial vehicles with various EV powertrains.

| Keyword | Definition |

|---|---|

| Electric vehicle (EV) | A vehicle which uses one or more electric motors for propulsion. Includes cars, buses, and trucks. This term includes all-electric vehicles or battery electric vehicles and plug-in hybrid electric vehicles. |

| PEV | A plug-in electric vehicle is an electric vehicle that can be externally charged and generally includes all electric vehicles as well as plug-electric vehicles as well as plug-in hybrids. |

| Battery-as-a-Service | A business model in which the battery of an EV can be rented from a service provider or swapped with another battery when it runs out of charge |

| Battery Cell | The basic unit of an electric vehicle's battery pack, typically a lithium-ion cell, that stores electrical energy. |

| Module | A subsection of an EV battery pack, consisting of several cells grouped together, often used to facilitate manufacturing and maintenance. |

| Battery Management System (BMS) | An electronic system that manages a rechargeable battery by protecting the battery from operating outside its safe operating area, monitoring its state, calculating secondary data, reporting data, controlling its environment, and balancing it. |

| Energy Density | A measure of how much energy a battery cell can store in a given volume, usually expressed in watt-hours per liter (Wh/L). |

| Power Density | The rate at which energy can be delivered by the battery, often measured in watts per kilogram (W/kg). |

| Cycle Life | The number of complete charge-discharge cycles a battery can perform before its capacity falls under a specified percentage of its original capacity. |

| State of Charge (SOC) | A measurement, expressed as a percentage, that represents the current level of charge in a battery compared to its capacity. |

| State of Health (SOH) | An indicator of the overall condition of a battery, reflecting its current performance compared to when it was new. |

| Thermal Management System | A system designed to maintain optimal operating temperatures for an EV's battery pack, often using cooling or heating methods. |

| Fast Charging | A method of charging an EV battery at a much faster rate than standard charging, typically requiring specialized charging equipment. |

| Regenerative Braking | A system in electric and hybrid vehicles that recovers energy normally lost during braking and stores it in the battery. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all its reports.

- Step-1: Identify Key Variables: To build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built based on these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. Market revenue is calculated by multiplying the volume demand with volume-weighted average battery pack price (per kWh). Battery pack price estimation and forecast takes into account various factors affecting ASP, such as inflation rates, market demand shifts, production costs, technological developments, and consumer preferences, providing estimations for both historical data and future trends.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms