Germany Digital Transformation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

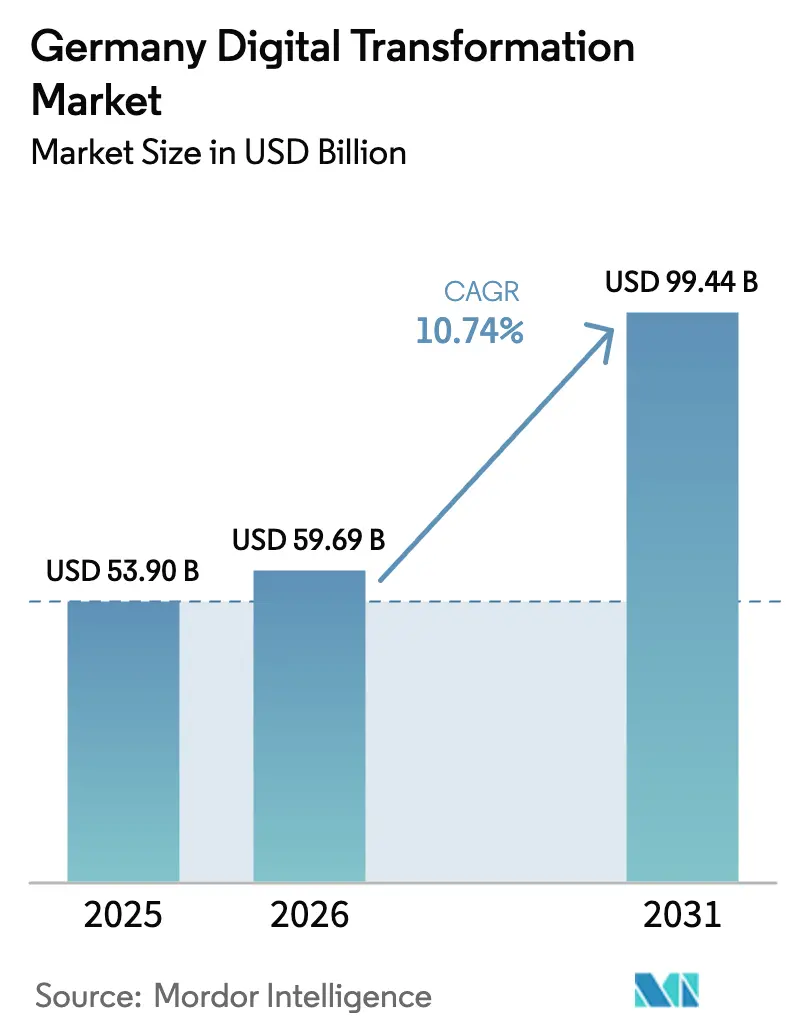

| Base Year Market Size (2025) | USD 53.90 Billion |

| Market Size (2026) | USD 59.69 Billion |

| Market Size (2031) | USD 99.44 Billion |

| Growth Rate (2026 - 2031) | 10.74% CAGR |

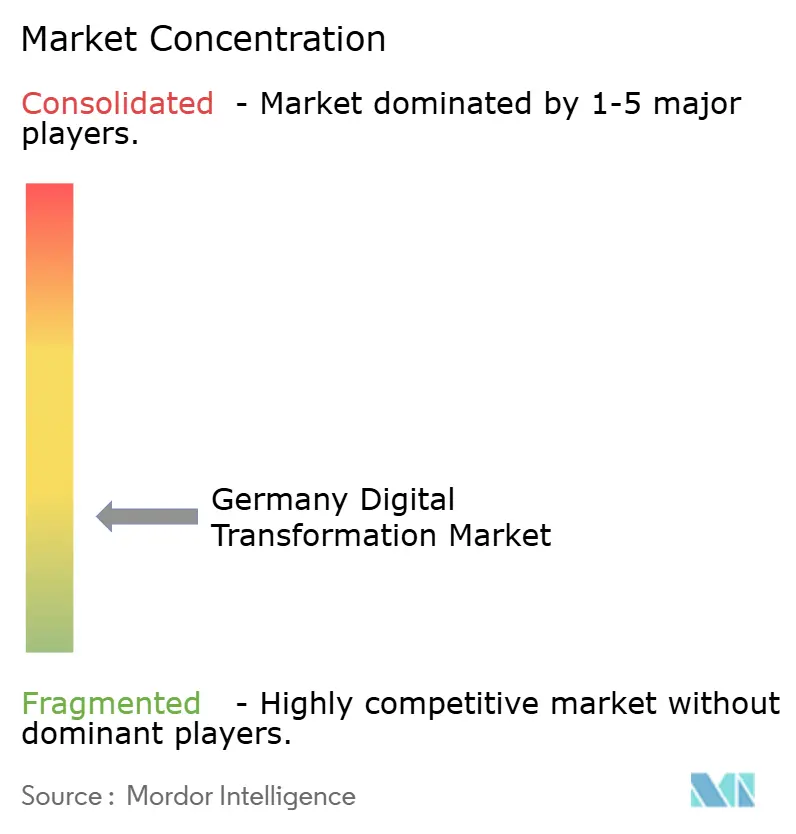

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Digital Transformation Market Analysis by Mordor Intelligence

Germany Digital Transformation Market size in 2026 is estimated at USD 59.69 billion, growing from 2025 value of USD 53.90 billion with 2031 projections showing USD 99.44 billion, growing at 10.74% CAGR over 2026-2031. This trajectory cements the country’s position as the largest digital transformation arena in Europe, supported by strong industrial roots, far-reaching Industry 4.0 programs, and federally funded initiatives such as Manufacturing-X.[1]Federal Ministry for Economic Affairs and Climate Action, “Manufacturing-X Funding Programme,” bmwk.de Strong sovereign-cloud investments, rising cybersecurity outlays, and nearly universal 5G cover create fertile conditions for scaling advanced analytics, industrial AI, and edge solutions. At the same time, the Germany digital transformation market faces energy-price volatility and persistent skills shortages that slow project timelines, yet these challenges rank below regulatory complexity in executive surveys. Companies respond by pairing hybrid-cloud architectures with local data-space projects, enabling compliance while securing data-driven productivity gains. These dynamics combine to push smart-factory rollouts deeper into automotive, machinery, and chemical plants, while driving healthcare, logistics, and public-sector agencies into double-digit adoption curves.

Key Report Takeaways

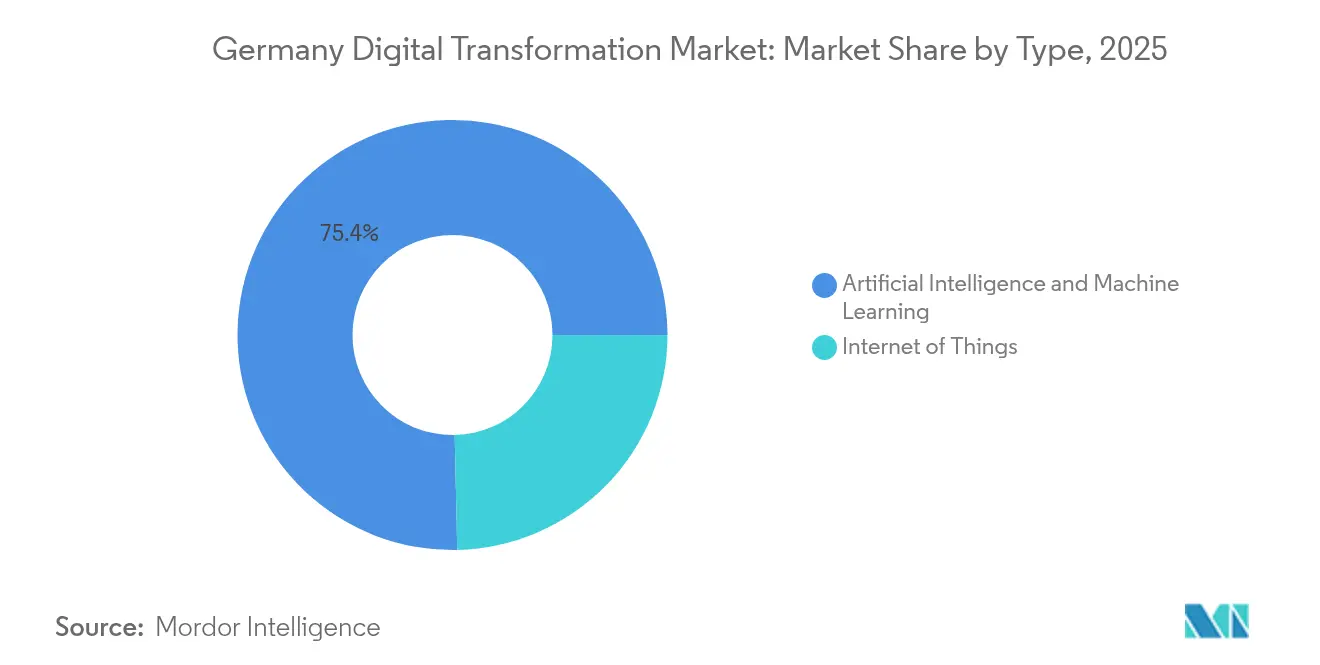

- By product type, IoT commanded 24.65% of Germany digital transformation market share in 2025, while AI and machine learning are projected to expand at an 17.68% CAGR through 2031.

- By deployment mode, cloud deployments held 66.40% of Germany digital transformation market share in 2025 and is advancing at an 18.25% CAGR through 2031.

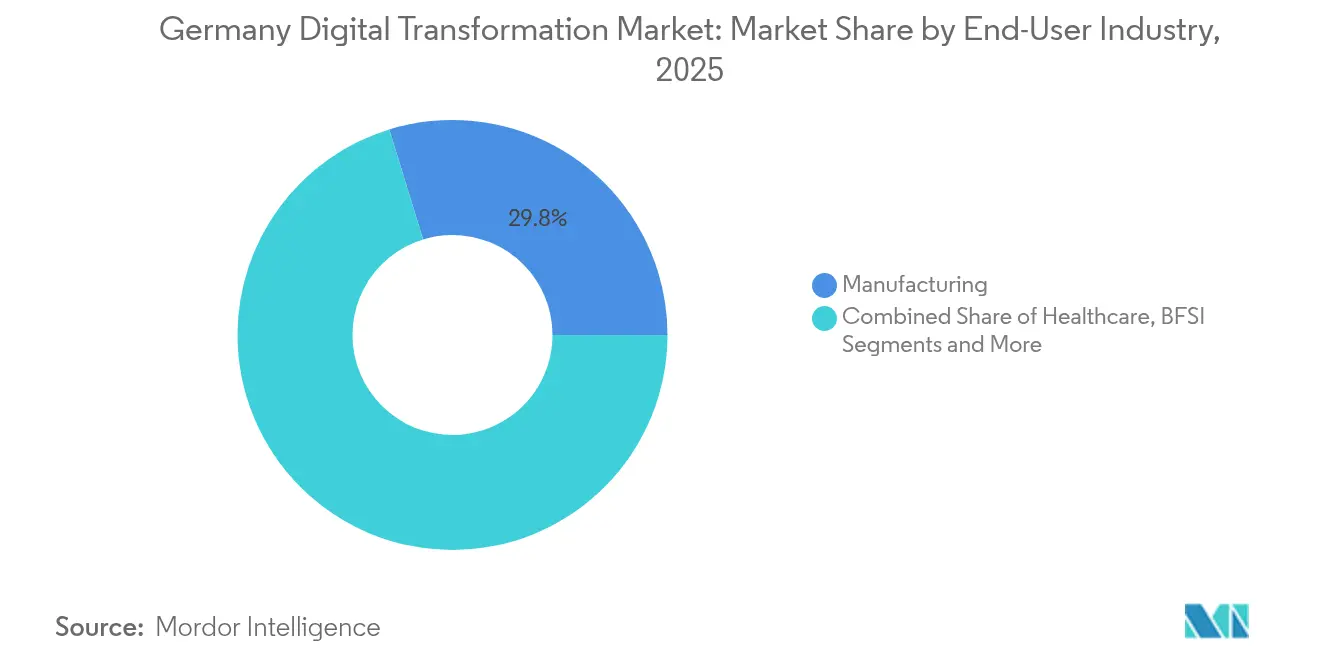

- By end-user industry, manufacturing accounted for 29.75% share of the Germany digital transformation market size in 2025, whereas healthcare is forecast to grow at a 13.74% CAGR to 2031.

- By enterprise size, large enterprises represented 46.20% of Germany digital transformation market size in 2025, while small and micro enterprises are expanding at a 15.74% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Companies active in Germany may frequently operate across several geographies, linking regional presence to global strategy. Mordor Intelligence captures the entire market landscape of the global digital transformation (dx) industry and how these positions are distributed.

Germany Digital Transformation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Start-up boom & VC inflows | +1.8% | Berlin, Munich, Hamburg | Medium term (2-4 years) |

| Explosive IoT device base | +2.1% | Nationwide; strongest in South and West manufacturing clusters | Short term (≤ 2 years) |

| Sovereign-cloud build-out by hyperscalers | +1.5% | Brandenburg, Frankfurt | Medium term (2-4 years) |

| Manufacturing-X industrial data-space rollout | +1.2% | Nationwide; most significant in core industrial regions | Long term (≥ 4 years) |

| Surge in cybersecurity budgets | +1.4% | Global | Short term (≤ 2 years) |

| 5G/Fibre densification enabling edge cases | +1.0% | Nationwide; rural areas prioritized | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Start-up Boom & VC Inflows

Germany’s venture capital ecosystem accelerated in 2025, with AI-focused funding rounds lifting investment totals and nurturing more than 500 young firms across mobility, industrial software, and robotics clusters in Berlin, Munich, and Stuttgart. Government co-investment programs such as KI-Innovationswettbewerb channel grants toward generative AI use cases in small and mid-sized enterprises, broadening the reach of cutting-edge technologies. As these firms commercialize digital twins, vision systems, and predictive-maintenance platforms, incumbent manufacturers face competitive pressure to modernize faster—further lifting demand across the Germany digital transformation market.

Explosive IoT Device Base

Forty-four percent of German manufacturers with more than 100 employees have already integrated industrial 3D printing, often as part of wider IoT ecosystems.[2]Germany Trade & Invest, “Digital Economy,” gtai.de Siemens’ Erlangen facility recorded a 69% productivity gain and 42% energy savings after pairing IoT sensors with AI-driven digital twins. The Factory-X project extends this model by creating sovereign data spaces for secure IoT data exchange in production networks. Together, these examples illustrate a compounding effect: each successful pilot proves the ROI of data-rich operations and pulls more enterprises into the Germany digital transformation market.

Sovereign-Cloud Build-Out by Hyperscalers

AWS, Microsoft, and Deutsche Telekom collectively earmarked EUR 18.6 billion for sovereign-cloud infrastructures that guarantee European data residency. AWS alone is investing EUR 7.8 billion in Brandenburg to operate an independent sovereign region staffed exclusively by EU personnel About Amazon.[3]About Amazon, “AWS Plans to Invest €7.8 Billion into the AWS European Sovereign Cloud,” aboutamazon.eu The GAIA-X framework further advances federated architectures, enhancing interoperability for regulated industries. These moves redefine competition away from scale toward compliance, lifting procurement in the Germany digital transformation market.

Manufacturing-X Industrial Data-Space Rollout

Manufacturing-X allocates EUR 150 million in federal support to harmonize machine data, product passports, and supply-chain transparency across automotive, machinery, and chemical verticals. Pilot projects such as Catena-X already connect 28 automotive champions on shared dataspace infrastructure, while Factory-X targets mechanical engineering SMEs. As these platforms mature, equipment-as-a-service, remote diagnostics, and cross-plant optimization become mainstream, expanding addressed revenue pools within the Germany digital transformation market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| GDPR-driven privacy compliance burden | -1.2% | EU markets, greatest friction for cross-border data movement | Long term (≥ 4 years) |

| Shortage of IT specialists | -1.8% | Nationwide, most acute in rural and eastern areas | Medium term (2-4 years) |

| Fragmented public-sector IT architectures | -0.8% | Varies by federal state, uneven modernisation across the country | Long term (≥ 4 years) |

| Energy-price swings delaying capital spend | -0.6% | Nationwide, hits energy-intensive industries hardest | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

GDPR-Driven Privacy Compliance Burden

The first year of new EU digital legislation generated EUR 53 billion in compliance costs, with GDPR representing the lion’s share and weighing heavily on SME budgets.[4]European Parliament, “The Impact of EU Legislation in the Area of Digital and Green Transition, Particularly on SMEs,” europarl.europa.eu Upcoming rules, including the AI Act and Cyber Resilience Act, add layers of uncertainty, prompting firms to delay or resize projects. Fintech platforms illustrate the issue: many outsource legal expertise rather than hire in-house counsel, adding expenses that compete with modernization budgets. While sovereign clouds lower cross-border risk, complex reporting remains a brake on overall spend in the Germany digital transformation market.

Shortage of IT Specialists

Eighty-nine percent of organizations anticipate hiring extra cybersecurity staff to comply with the NIS-2 Directive alone. The talent gap hits rural and eastern areas hardest, even as large infrastructure projects locate there to tap renewable energy. Programs like CloudCamp4SMEs and AWS-sponsored upskilling aim to close the divide, yet near-term supply remains tight. Extended hiring cycles and higher wage bills lengthen payback periods on major initiatives, tempering the otherwise strong growth curve of the Germany digital transformation market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: IoT Integration Consolidates Industrial Advantage

The IoT segment captured 24.65% of Germany digital transformation market share in 2025 by serving as the connective tissue for smart factories and connected supply chains. Robotics, sensor networks, and additive manufacturing converge inside digital twins, helping large OEMs lift throughput while trimming energy intensity. AI and machine learning technologies, projected to record an 17.68% CAGR, amplify these gains through predictive quality control and real-time optimization. Early adopters report double-digit efficiency improvements that validate new investment waves across discrete and process manufacturing.

Complementary solutions such as extended-reality training tools and blockchain-backed product passports widen addressable spend. Cybersecurity has become the fastest-moving niche after AI as companies spend EUR 11.2 billion to safeguard expanded attack surfaces. Cloud and edge installations under sovereign architectures give firms low-latency compute while satisfying regulatory demands. As industrial metaverse pilots proliferate, the Germany digital transformation market size for digital-twin software and enabling hardware is positioned for rapid scale-up through 2031.

By Deployment Mode: Cloud Gains on Sovereignty Mandates

Cloud retained a commanding 66.40% share of Germany digital transformation market size in 2025, powered by hyperscaler breadth and cost efficiency. Nevertheless, data-residency mandates are tilting procurement toward hybrid frameworks that blend local control with elastic capacity. The hybrid model is forecast to grow at 18.25% CAGR, reflecting adoption in finance and healthcare where sensitive workloads must remain in country.

Major retailers, insurers, and automotive suppliers deploy multi-cloud strategies to hedge vendor risk while optimizing latency and data protection. The Germany digital transformation market benefits as companies spend on orchestration platforms, zero-trust security, and workload-migration services. Private-cloud investments persist in defense, utilities, and critical infrastructure, but edge nodes located on factory floors or cell towers are now the fastest-growing segment under the broader hybrid umbrella.

By End-User Industry: Manufacturing Stays Dominant, Healthcare Surges

Manufacturing generated 29.75% of Germany digital transformation market size in 2025, underpinned by Industry 4.0, automotive electrification, and global supply-chain pressures. Flagship projects such as Catena-X demonstrate the traction of shared data spaces, while Siemens’ Erlangen facility shows that AI-enhanced production can deliver multi-year gains in energy and labor productivity. The oil, gas, and utilities segment is also accelerating digitization to meet sustainability targets.

Healthcare, forecast to expand at 13.74% CAGR, is propelled by e-prescription mandates, electronic patient records, and robust telemedicine adoption. Hospitals modernize imaging workflows through AI diagnostics, while insurers invest in preventative-care analytics. Logistics firms exploit 5G-enabled edge computing to automate terminal operations, and public agencies digitize permitting and school administration—each adding depth to the Germany digital transformation market.

By Enterprise Size: Large Firms Lead, SMEs Accelerate

Large enterprises contributed 46.20% of Germany digital transformation market share in 2025, leveraging global footprints to standardize platforms and negotiate favorable cloud contracts. Yet growth momentum shifts toward SMEs, which receive subsidized consulting and technology grants of up to EUR 50,000 under programs like Digital Jetzt. Small manufacturers increasingly adopt cloud-first ERP, IIoT starter kits, and SaaS cybersecurity, lowering barriers to advanced capabilities.

Medium-sized firms exploit go-digital vouchers for business-process redesign, while INQA-Coaching covers 80% of digital advisory costs to boost organizational change. As talent scarcity remains acute, managed-service providers step in to deliver turnkey solutions, ensuring SMEs maintain pace with larger competitors. This dynamic pushes more than one-third of incremental spending toward the SME cohort, expanding the base of the Germany digital transformation market beyond traditional heavyweights.

Geography Analysis

Regional investment patterns mirror Germany’s diversified economic map. The South, with Bavaria and Baden-Württemberg, held 34.05% of Germany digital transformation market share in 2025, buoyed by automotive OEMs, machinery clusters, and a rich start-up scene. Siemens is investing EUR 500 million to evolve Erlangen into a global R&D campus for industrial metaverse technologies.

The West ranks second on account of Frankfurt’s dense data-center ecosystem, supported by hyperscaler facilities and blockchain testbeds. North Rhine-Westphalia hosts the EUR 680 million Fraunhofer battery research factory, tying energy innovation to digital engineering. Meanwhile, the North leverages maritime logistics digitization through 5G port projects, advancing real-time container and vehicle handling efficiencies.

The East is the fastest-growing region at a 12.88% CAGR through 2031, fueled by renewable-energy capacity and marquee projects such as the AWS European Sovereign Cloud in Brandenburg. Lusatia’s EUR 40 billion clean-energy transition and Berlin’s additive-manufacturing clusters reinforce the region’s momentum. Coordinated funding such as the EUR 100 million EIB loan for school digitization reduces digital divides and positions the East as a sovereign-data hub. Central Germany benefits from logistics corridors and cost-competitive industrial land, helping balance growth across federal states as data-space projects bridge regional boundaries within the Germany digital transformation market.

The digital transformation (dx) market is assessed by Mordor Intelligence through a multi-layered geographic lens, covering other regions such as Europe, North America, and Africa, along with detailed country-level analysis for Netherlands, Poland, Canada, Nigeria, Qatar, and India.

Competitive Landscape

Competition is intensifying as industrial champions, cloud hyperscalers, and telecom operators converge on sovereign-technology propositions. Siemens applies domain expertise to AI-driven automation, while AWS and Microsoft localize operations to satisfy data-residency rules. Deutsche Telekom’s partnership with NVIDIA to deploy 10,000 GPUs inside an industrial AI cloud illustrates how telecom incumbents pivot toward high-performance computing services.

Edge-cloud rollouts by German Edge Cloud and regional data-center operators open room for specialized providers of orchestration, zero-trust security, and low-latency analytics. Sovereign workplace solutions from the Schwarz Group and Google demonstrate alliance-building that pairs global software with local hosting, enabling regulated sectors to adopt modern tools. Industrial players such as Bosch allocate multibillion-euro budgets to AI agent development, underscoring the strategic stakes.

Defense integrator Rheinmetall’s acquisition of blackned extends digital reach into secure battlefield networks and underscores a trend toward cross-sector digital convergence. Overall, the Germany digital transformation market favors players that blend vertical know-how with cloud-native architectures and compliance frameworks, creating moderate concentration but abundant niches for specialists.

Germany Digital Transformation Industry Leaders

Accenture PLC

Google LLC (Alphabet Inc.)

Siemens AG

IBM Corporation

Microsoft Corporation

SAP SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Deutsche Telekom and NVIDIA agreed to deploy an industrial AI cloud with 10,000 GPUs by 2026.

- June 2025: Bosch pledged EUR 2.5 billion toward AI agent technology over two years.

- May 2025: The federal government unveiled a EUR 500 billion, twelve-year infrastructure and climate package, allocating EUR 100 billion for digital administration.

- February 2025: Factory-X launched under Manufacturing-X with 50 partners to build secure data spaces for mechanical engineering.

Germany Digital Transformation Market Report Scope

Digital transformation is the process of incorporating digital technologies such as analytics, artificial intelligence, and machine learning, extended reality (XR), Iot, industrial robotics, blockchain, additive manufacturing/3D printing, cybersecurity, cloud and edge computing, and others (digital Twin, mobility, and connectivity) in various end-user industries across Germany.

Germany digital transformation market is segmented by type (analytics, artificial intelligence, and machine learning, extended reality (XR), IoT, industrial robotics, blockchain, additive manufacturing/3D printing, cybersecurity, cloud, and edge computing, and others [digital twin, mobility, and connectivity]), end-user industry (manufacturing, oil, gas, and utilities, retail & e-commerce, transportation, and logistics, healthcare, BSFI, telecom and IT, government and public sector and others). The market sizes and forecasts are provided in terms of value (USD) for the above segment

| Artificial Intelligence and Machine Learning |

| Extended Reality (VR/AR) |

| Internet of Things |

| Industrial Robotics |

| Blockchain |

| Additive Manufacturing/3D Printing |

| Cybersecurity |

| Cloud/Edge Computing |

| Digital Twin, Mobility and Connectivity |

| Cloud |

| On-premise |

| Manufacturing |

| Oil, Gas and Utilities |

| Retail and E-commerce |

| Transportation and Logistics |

| Healthcare |

| BFSI |

| Telecom and IT |

| Government and Public Sector |

| Education, Media and Others |

| Large Enterprises |

| Medium-sized Enterprises |

| Small and Micro Enterprises |

| By Type | Artificial Intelligence and Machine Learning |

| Extended Reality (VR/AR) | |

| Internet of Things | |

| Industrial Robotics | |

| Blockchain | |

| Additive Manufacturing/3D Printing | |

| Cybersecurity | |

| Cloud/Edge Computing | |

| Digital Twin, Mobility and Connectivity | |

| By Deployment Mode | Cloud |

| On-premise | |

| By End-User Industry | Manufacturing |

| Oil, Gas and Utilities | |

| Retail and E-commerce | |

| Transportation and Logistics | |

| Healthcare | |

| BFSI | |

| Telecom and IT | |

| Government and Public Sector | |

| Education, Media and Others | |

| By Enterprise Size | Large Enterprises |

| Medium-sized Enterprises | |

| Small and Micro Enterprises |

Key Questions Answered in the Report

What is the current value of the Germany digital transformation market?

The market stands at USD 59.69 billion in 2026 and is projected to reach USD 99.44 billion by 2031.

Which segment holds the largest Germany digital transformation market share?

IoT solutions lead with 24.65% share, driven by widespread industrial integration.

Which region is growing fastest inside Germany?

The East region is expanding at a 12.88% CAGR through 2031, supported by sovereign-cloud infrastructure and renewable energy assets.

Why is cloud gaining traction in Germany?

Hybrid deployments balance scalability with data-sovereignty mandates, pushing growth at an 18.25% CAGR.

How big is cybersecurity spending within the market?

German enterprises allocated EUR 11.2 billion to IT security in 2024, a 13.8% year-on-year increase that reinforces digital-transformation roadmaps.

What role do SMEs play in market growth?

SMEs are the fastest-growing customer group, advancing at a 15.74% CAGR thanks to grant programs that subsidize up to 80% of digital-consulting and technology costs.

Page last updated on: