Germany Dairy Alternatives Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

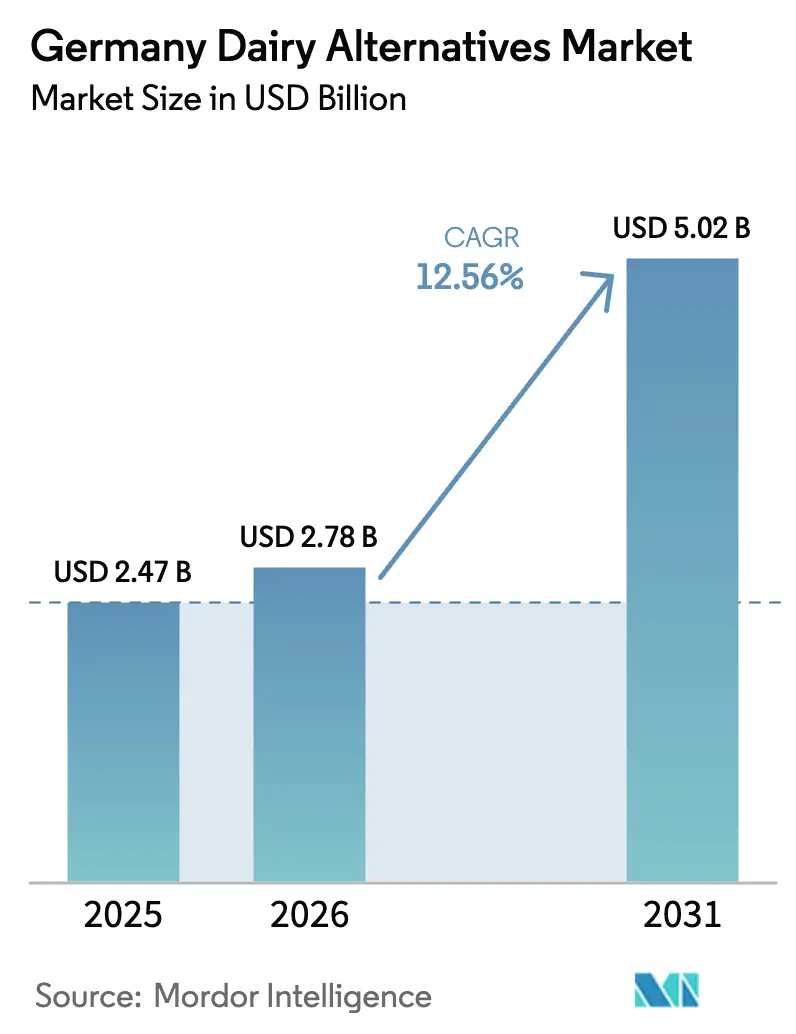

| Base Year Market Size (2025) | USD 2.47 Billion |

| Market Size (2026) | USD 2.78 Billion |

| Market Size (2031) | USD 5.02 Billion |

| Growth Rate (2026 - 2031) | 12.56% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Germany Dairy Alternatives Market Analysis by Mordor Intelligence

The Germany Dairy Alternatives Market size was valued at USD 2.47 billion in 2025 and estimated to grow from USD 2.78 billion in 2026 to reach USD 5.02 billion by 2031, at a CAGR of 12.56% during the forecast period (2026-2031). The expansion is fueled by rising lactose intolerance prevalence, rapid vegan and flexitarian adoption, and a growing preference for products with demonstrably lower carbon footprints. Cost-competitive oat cropping, precision-fermentation breakthroughs, and public-sector procurement targets for half-plant-based menus by 2030 further accelerate demand[1]Federal Ministry of Food and Agriculture. "Nutrition Report 2024." BMEL, 2024. https://www.bmel.de. Domestic brands use clean-label recipes and protein enrichment to resolve historic taste and nutrition gaps, while multinationals leverage wide distribution and marketing scale. Off-trade retail continues to dominate volumes, but on-trade foodservice has become the undisputed growth engine as cafés, restaurants, and institutional kitchens mainstream non-dairy options.

Key Report Takeaways

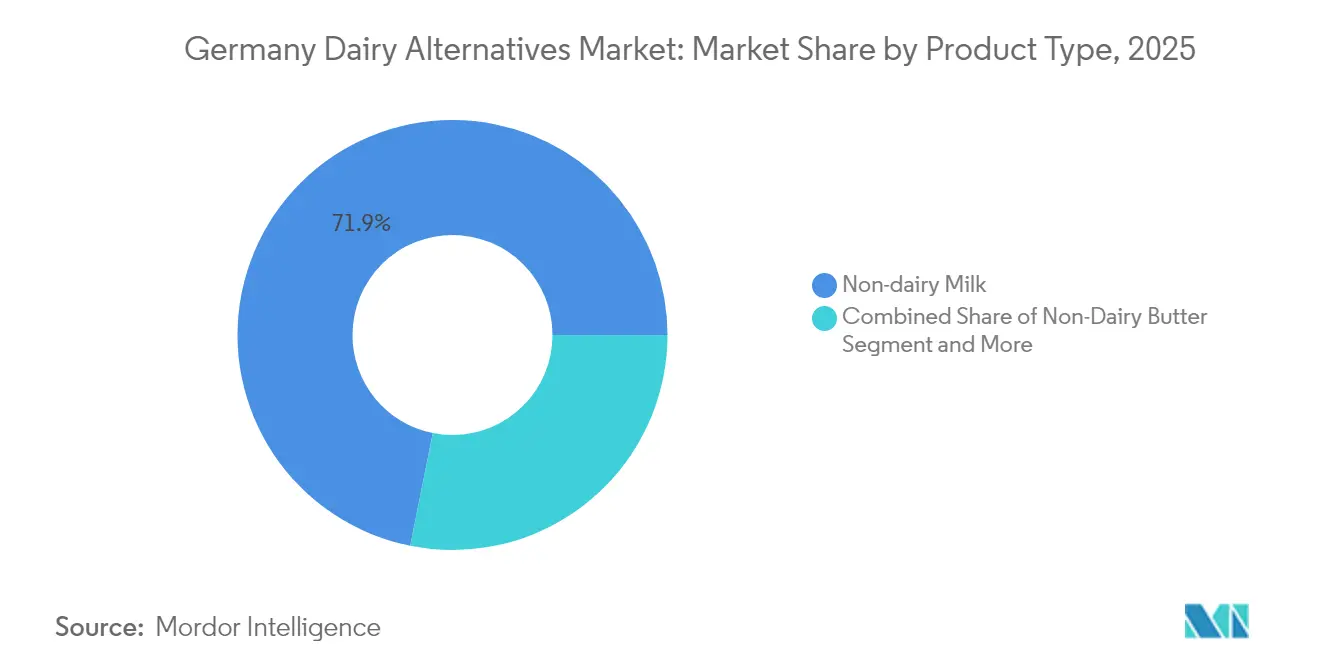

- By product type, non-dairy milk commanded 71.85% of Germany dairy alternatives market share in 2025; non-dairy butter is forecast to expand at a 10.62% CAGR to 2031.

- By source, oat captured 41.05% share of the Germany dairy alternatives market size in 2025, while almond leads growth at an 11.44% CAGR through 2031.

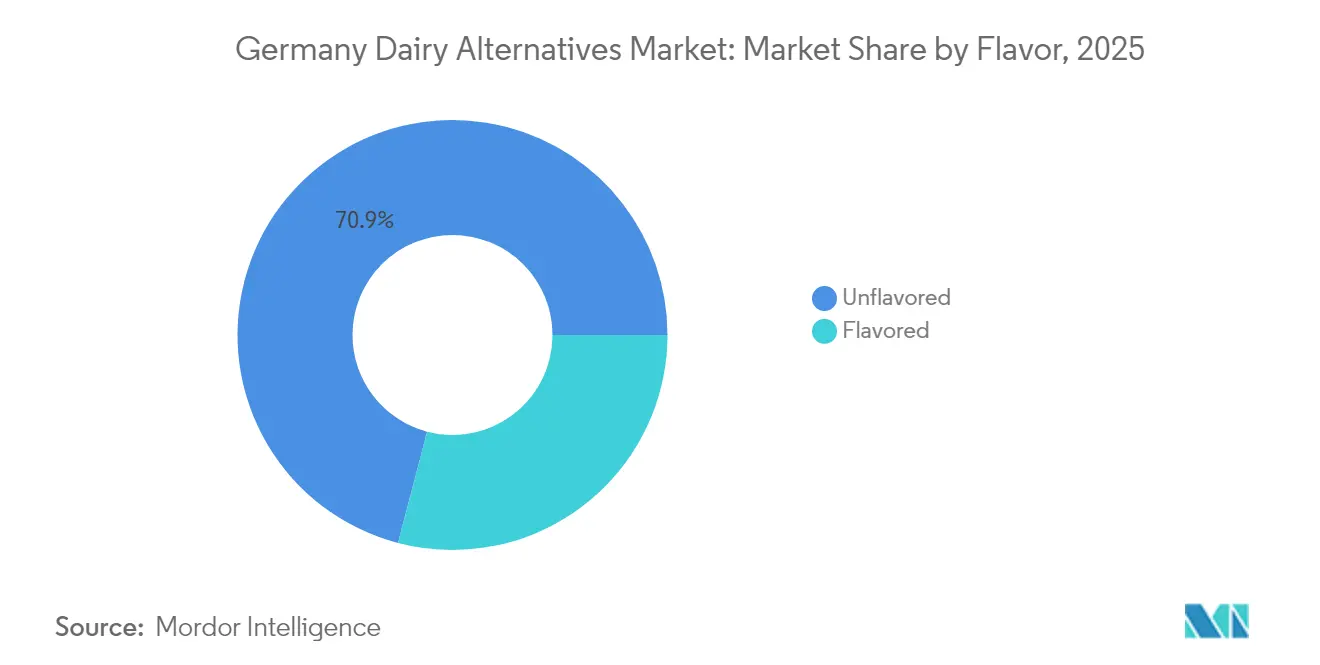

- By flavor, unflavored products represented 70.92% of the Germany dairy alternatives market size in 2025; flavored variants are advancing at a 9.38% CAGR over 2026-2031.

- By packaging, cartons accounted for 78.82% share of the Germany dairy alternatives market size in 2025, whereas innovative formats such as glass and pouch are set to grow at a 9.70% CAGR by 2031.

- By distribution channel, off-trade held 85.90% of Germany dairy alternatives market share in 2025; on-trade exhibits the fastest trajectory at a 10.04% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Dairy Alternatives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising lactose-intolerance & milk-protein allergy prevalence | +2.1% | Nationwide, urban focus | Medium term (2-4 years) |

| Rapid growth in vegan & flexitarian consumer base | +3.2% | Berlin, Hamburg, Munich | Short term (≤ 2 years) |

| Sustainability positioning & lower carbon footprint | +2.8% | Nationwide, EU alignment | Long term (≥ 4 years) |

| Accelerated product innovation | +1.9% | Bavaria, North Rhine-Westphalia R&D hubs | Medium term (2-4 years) |

| Public-sector catering commitment ≥ 50% plant-based menus | +1.4% | Federal & state facilities | Long term (≥ 4 years) |

| Domestic oat crop surplus enabling price competitiveness | +1.3% | Northern production belts | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Lactose-Intolerance & Milk-Protein Allergy Prevalence

Germany's expanding recognition of lactose intolerance as a widespread health condition is fundamentally reshaping dairy consumption patterns across demographic segments. The Federal Institute for Risk Assessment (BfR) reports that lactose malabsorption affects 15-20% of the German population, with higher prevalence rates observed in adults over 30 years of age[2]Federal Institute for Risk Assessment. "Plant-Based Food Alternatives Guidelines." BfR, 2024. https://www.bfr.bund.de. This physiological reality, combined with increased awareness of milk protein allergies affecting approximately 2-3% of children and 1% of adults, creates sustained demand for dairy alternatives that eliminate digestive discomfort. Healthcare professionals increasingly recommend plant-based alternatives as first-line interventions for lactose-sensitive patients, legitimizing consumption beyond lifestyle preferences. The trend extends beyond individual health concerns to encompass family purchasing decisions, where households adopt dairy alternatives to accommodate multiple dietary requirements simultaneously. Medical insurance coverage for specialized nutrition counseling has expanded access to professional guidance on dairy-free diets, institutionalizing the transition away from conventional dairy products.

Rapid Growth in Vegan & Flexitarian Consumer Base

The German consumer landscape has experienced unprecedented expansion in plant-based dietary adoption, driven by generational shifts and evolving food culture norms. The BMEL's 2024 nutrition survey reveals that 39% of German consumers purchase plant-based alternatives more frequently than in previous years, with 8% identifying as vegetarian and 2% as vegan, representing substantial growth from 2020 baseline measurements. Flexitarian consumers, who reduce but do not eliminate animal products, constitute the largest growth segment and drive volume increases across multiple product categories. Urban centers including Berlin, Hamburg, and Munich demonstrate accelerated adoption rates, with plant-based product availability in mainstream retail channels normalizing consumption patterns. Social media influence and celebrity endorsements have amplified awareness among younger demographics, while environmental documentaries and health-focused content create conversion moments for middle-aged consumers. The German Nutrition Society's updated dietary guidelines acknowledge plant-based diets as nutritionally adequate when properly planned, removing institutional barriers to adoption.

Sustainability Positioning & Lower Carbon Footprint of Plant-Based Dairy

Environmental consciousness has emerged as a primary purchase driver for German consumers evaluating dairy alternatives, supported by comprehensive life cycle assessments demonstrating significant ecological advantages. Independent studies conducted by German research institutions indicate that plant-based milk alternatives generate 50-80% lower greenhouse gas emissions compared to conventional dairy milk, with oat milk showing particularly favorable environmental profiles due to domestic production capabilities[3]German Environment Agency. "Life Cycle Assessment of Plant-Based Dairy Alternatives." Umweltbundesamt, 2024. https://www.umweltbundesamt.de. Water usage reductions of 60-90% for plant-based alternatives resonate with consumers increasingly concerned about resource scarcity and climate change impacts. The European Union's Farm to Fork Strategy and German Climate Action Plan 2050 create policy frameworks that favor lower-emission food products, influencing both consumer preferences and institutional purchasing decisions. Corporate sustainability reporting requirements compel foodservice operators and retailers to demonstrate environmental impact reductions, driving procurement shifts toward plant-based alternatives. German consumers demonstrate willingness to pay premium prices for products with verified sustainability credentials, creating competitive advantages for brands with transparent environmental reporting.

Accelerated Product Innovation (Fermentation, Protein Enrichment, Clean Labels)

Technological advancement in plant-based dairy production has reached inflection points that address historical barriers to mass market adoption, particularly in taste, texture, and nutritional adequacy. Precision fermentation technology enables German manufacturers to produce dairy-identical proteins without animal involvement, with companies like Formo raising EUR 50 million (USD 54 million) in 2024 to scale koji-based cheese production Formo. Protein enrichment strategies utilizing pea, hemp, and algae sources address nutritional concerns that previously limited consumer adoption, particularly among health-conscious demographics. Clean label formulations eliminating artificial additives, stabilizers, and preservatives respond to consumer preferences for minimal processing, with ingredient lists increasingly resembling whole food compositions. The Federal Institute for Risk Assessment (BfR) has established comprehensive guidelines for novel food ingredients in plant-based alternatives, providing regulatory clarity that accelerates innovation cycles. German food technology institutes collaborate with industry partners on sensory optimization projects that enhance palatability while maintaining nutritional integrity, creating products that satisfy both functional and hedonic consumption motivations.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price premium versus conventional dairy | -2.4% | Germany-wide, most pronounced in price-sensitive rural markets | Short term (≤ 2 years) |

| Nutritional adequacy concerns (protein, calcium, additives) | -1.8% | Germany-wide, strongest among healthcare professionals and elderly consumers | Medium term (2-4 years) |

| CAP subsidy tilt toward traditional dairy farmers | -1.1% | EU-wide policy impact, affecting German market competitiveness | Long term (≥ 4 years) |

| Supply-chain volatility for imported nuts | -0.9% | Germany-wide, concentrated in almond and cashew-based products | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price Premium Versus Conventional Dairy

The persistent price differential between plant-based alternatives and conventional dairy products represents the most significant barrier to mass market penetration across German consumer segments. Retail price analysis indicates that plant-based milk alternatives cost 2-3 times more than conventional dairy milk on a per-liter basis, with premium positioning limiting accessibility for price-sensitive households. The cost structure reflects higher raw material expenses, specialized processing equipment, and smaller production scales compared to established dairy infrastructure that benefits from decades of optimization and government subsidies. However, strategic pricing initiatives by major retailers demonstrate potential for cost reduction, with Lidl Germany's October 2023 decision to align vegan product prices with animal-based counterparts resulting in over 30% sales increases across plant-based categories. Consumer willingness to pay premium prices varies significantly by income level, education, and geographic location, with urban, higher-income demographics showing greater price tolerance. The European Central Bank's monetary policy and inflation trends directly impact discretionary spending on premium food products, creating cyclical demand fluctuations that affect market growth trajectories.

Nutritional Adequacy Concerns (Protein, Calcium, Additives)

Persistent consumer and healthcare professional concerns regarding nutritional completeness of plant-based dairy alternatives continue to limit adoption among health-conscious demographics and vulnerable populations. Protein quality assessments reveal that many plant-based alternatives provide incomplete amino acid profiles compared to dairy milk, requiring dietary diversification or fortification strategies to achieve nutritional equivalence. Calcium bioavailability from plant-based sources varies significantly by processing method and fortification approach, with some products demonstrating lower absorption rates than dairy calcium. The Federal Institute for Risk Assessment (BfR) has issued guidance on additive usage in plant-based alternatives, highlighting potential health implications of stabilizers, emulsifiers, and flavor enhancers commonly used to achieve dairy-like characteristics. Healthcare professionals express particular concern about plant-based alternative consumption among children, pregnant women, and elderly populations who have elevated nutritional requirements. Consumer education initiatives by manufacturers and health organizations aim to address knowledge gaps, but skepticism persists among traditional healthcare providers who recommend conventional dairy for optimal nutrition.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Non-Dairy Milk Dominance Amid Butter Innovation

Non-dairy milk maintains commanding market leadership with a 71.85% share in 2025, reflecting its role as the primary entry point for consumers transitioning from conventional dairy products. The segment's dominance stems from versatile applications across beverage consumption, cereal pairing, and cooking applications that mirror traditional milk usage patterns. German consumers demonstrate strong brand loyalty within the non-dairy milk category, with established products from Alpro, Oatly, and private-label offerings capturing significant market share through widespread retail distribution. The segment benefits from continuous product innovation in flavor profiles, nutritional fortification, and packaging formats that enhance convenience and shelf stability. Regulatory frameworks established by the Federal Institute for Risk Assessment (BfR) provide clear guidelines for nutritional claims and labeling requirements, enabling transparent consumer communication about protein content, vitamin fortification, and allergen information.

Non-dairy butter emerges as the fastest-growing product segment with a 10.62% CAGR through 2031, driven by culinary applications and baking functionality improvements that closely replicate conventional butter performance. The segment's acceleration reflects technological breakthroughs in fat composition and texture development that enable seamless substitution in traditional German baking recipes and cooking preparations. Companies like Upfield BV (Violife) and Simply V have invested heavily in R&D initiatives focused on melting characteristics, flavor release, and nutritional profiles that satisfy both functional and sensory requirements. The growth trajectory benefits from expanding foodservice adoption, where professional chefs increasingly incorporate plant-based butter alternatives in restaurant preparations and commercial baking operations. Consumer acceptance has improved significantly as product formulations eliminate the artificial taste profiles that historically limited adoption, with clean label ingredients and sustainable packaging further enhancing market appeal.

By Source: Oat Leadership Challenged by Almond Growth

Oat-based alternatives command the largest source segment share at 41.05% in 2025, benefiting from domestic agricultural production capabilities and favorable sustainability profiles that resonate with environmentally conscious German consumers. The segment's leadership position reflects Germany's robust oat cultivation infrastructure, which enables cost-competitive pricing and supply chain stability compared to imported raw materials. Oat milk's creamy texture and neutral flavor profile facilitate broad consumer acceptance across demographic segments, while beta-glucan content provides functional health benefits that differentiate the category from other plant-based options. Major retailers including REWE, Edeka, and Lidl have expanded private-label oat milk offerings, increasing accessibility and driving volume growth through competitive pricing strategies. The German Environment Agency's sustainability assessments consistently rank oat-based products favorably due to lower water usage, reduced transportation emissions, and compatibility with local agricultural systems.

Almond-based alternatives represent the fastest-growing source segment with an 11.44% CAGR through 2031, despite supply chain challenges associated with imported raw materials primarily sourced from California and Mediterranean regions. The segment's growth acceleration reflects consumer preferences for premium positioning, sophisticated flavor profiles, and perceived health benefits associated with almond nutrition. Product innovation in almond milk processing has addressed historical concerns about thin consistency and bland taste through enhanced formulations that incorporate natural thickeners and flavor enhancement techniques. However, supply chain volatility for imported almonds creates cost fluctuations that impact retail pricing and margin stability, with drought conditions in key growing regions contributing to raw material price increases. German consumers demonstrate willingness to pay premium prices for almond-based products that emphasize organic certification, fair trade sourcing, and artisanal production methods that differentiate from mass-market offerings.

By Flavor: Unflavored Preference Amid Flavored Innovation

Unflavored alternatives dominate the flavor segmentation with a 70.92% market share in 2025, reflecting German consumer preferences for versatile products that accommodate diverse culinary applications without imposing specific taste profiles. The segment's leadership position aligns with traditional German food culture that emphasizes natural flavors and minimal processing, where unflavored alternatives can seamlessly integrate into existing recipes and consumption patterns. Professional foodservice operators particularly favor unflavored options for their flexibility in menu development and compatibility with both sweet and savory preparations. The segment benefits from cost advantages associated with simplified production processes that eliminate flavoring ingredients and reduce manufacturing complexity. Regulatory compliance is streamlined for unflavored products, which face fewer labeling requirements and allergen considerations compared to flavored variants that may contain additional ingredients.

Flavored alternatives demonstrate accelerated growth with a 9.38% CAGR through 2031, driven by product innovation that targets specific consumer occasions and demographic preferences. Vanilla, chocolate, and strawberry flavors lead segment growth, appealing particularly to younger consumers and families with children who seek indulgent alternatives to conventional flavored milk products. The segment's expansion reflects successful marketing strategies that position flavored alternatives as premium lifestyle products rather than mere dairy substitutes. Companies invest significantly in natural flavoring technologies that avoid artificial additives while achieving authentic taste profiles that satisfy consumer expectations. Seasonal and limited-edition flavor launches create consumer excitement and drive trial behavior, with successful variants often transitioning to permanent product lines based on sales performance and consumer feedback.

By Packaging Type: Carton Dominance Amid Sustainable Innovation

Carton packaging maintains overwhelming market leadership with a 78.82% share in 2025, reflecting established consumer familiarity, retail compatibility, and functional advantages for liquid dairy alternatives. The segment's dominance stems from Tetra Pak and similar aseptic packaging technologies that enable extended shelf life without refrigeration, facilitating efficient distribution and reducing food waste throughout the supply chain. German retailers favor carton packaging for its space efficiency, stacking capabilities, and compatibility with existing dairy refrigeration systems that minimize operational disruption. Environmental considerations support carton preference, with recyclable paperboard construction and renewable material content aligning with German waste management systems and consumer sustainability expectations. The packaging format's association with conventional milk creates consumer comfort and reduces adoption barriers for households transitioning to plant-based alternatives.

Alternative packaging formats including pouches, glass bottles, and innovative containers represent the fastest-growing segment with a 9.70% CAGR through 2031, driven by sustainability initiatives and premium positioning strategies. The segment's growth reflects consumer demand for reduced plastic usage, enhanced recyclability, and differentiated brand presentation that commands premium pricing. Glass bottle packaging appeals to environmentally conscious consumers willing to pay higher prices for reusable containers and perceived quality advantages. The European Union's Packaging and Packaging Waste Regulation (PPWR) creates regulatory pressure for sustainable packaging innovation, driving investment in alternative materials and design optimization. Companies experiment with refillable systems, concentrated formats, and biodegradable materials that address environmental concerns while maintaining product integrity and consumer convenience.

By Distribution Channel: Off-Trade Dominance Amid On-Trade Acceleration

Off-trade distribution channels command dominant market share at 85.90% in 2025, reflecting the fundamental role of retail grocery channels in German food distribution and consumer purchasing behavior. Supermarkets and hypermarkets including REWE, Edeka, Kaufland, and Lidl drive segment leadership through extensive product assortments, competitive pricing, and strategic shelf placement that maximizes consumer exposure to plant-based alternatives. The segment benefits from private-label product development that offers cost-effective options while maintaining quality standards, with retailers leveraging their supply chain capabilities to optimize pricing and availability. Online retail within the off-trade segment demonstrates particular strength, with e-commerce platforms enabling subscription services, bulk purchasing, and specialized product discovery that traditional brick-and-mortar stores cannot match. German consumer shopping patterns favor weekly grocery shopping trips where dairy alternatives are purchased alongside conventional groceries, supporting off-trade channel dominance.

On-trade distribution channels exhibit the fastest growth trajectory with a 10.04% CAGR through 2031, driven by expanding foodservice adoption and institutional purchasing commitments that create substantial volume opportunities. The segment's acceleration reflects restaurant, café, and catering operations increasingly incorporating plant-based alternatives into menu offerings to accommodate dietary restrictions and sustainability preferences. Lidl Germany's commitment to achieving 20% plant-based protein content and 10% alternative dairy products by 2030 exemplifies institutional purchasing trends that drive on-trade growth. Professional barista training programs and equipment optimization enable coffee shops and cafés to achieve quality standards with plant-based milk alternatives that satisfy demanding consumer expectations. Public sector catering facilities including schools, hospitals, and government offices implement plant-based menu requirements that create sustained demand growth within the on-trade segment.

Geography Analysis

Germany represents the primary geographic focus for this market analysis, positioning as Europe's largest economy and most significant dairy-producing nation with 32.6 million tonnes of milk production in 2023, making it the largest producer within the European Union. The country's dairy alternatives market benefits from sophisticated consumer awareness, robust retail infrastructure, and progressive regulatory frameworks that facilitate product innovation and market access. Regional variations within Germany reflect demographic differences, with urban centers including Berlin, Hamburg, Munich, and Cologne demonstrating higher adoption rates and premium product acceptance compared to rural areas where traditional dairy consumption patterns persist. The northern German states of Lower Saxony and Schleswig-Holstein, which lead conventional dairy production, paradoxically show growing interest in plant-based alternatives as agricultural diversification strategies gain momentum among progressive farming operations.

The German market's growth trajectory aligns with broader European Union sustainability initiatives and climate action commitments that favor lower-emission food products. The European Green Deal and Farm to Fork Strategy create policy frameworks that indirectly support plant-based alternative adoption through carbon pricing mechanisms and environmental reporting requirements that highlight conventional dairy's ecological impact. Germany's position as the EU's economic powerhouse enables it to influence regional food policy and consumer trends, with German retail chains expanding plant-based offerings across their European operations based on domestic market success. The country's advanced food technology research infrastructure, concentrated in Bavaria and North Rhine-Westphalia, drives innovation that benefits the broader European plant-based dairy sector through technology transfer and collaborative research initiatives.

Cross-border trade dynamics within the European single market facilitate ingredient sourcing and finished product distribution that supports German market growth while creating competitive pressures from neighboring countries with different cost structures. The Netherlands and Denmark, with their advanced agricultural technology sectors, provide both competition and collaboration opportunities for German plant-based dairy companies seeking to optimize production efficiency and product quality. France's large agricultural sector and Italy's food processing expertise create regional supply chain opportunities that German companies leverage to access specialized ingredients and manufacturing capabilities not available domestically.

The on-trade segment represents a smaller but significant channel in the German dairy alternatives market, focusing on foodservice establishments, including restaurants, cafes, and other food service outlets. This segment has been experiencing notable transformation with the increasing number of vegan restaurants and the incorporation of plant-based options in traditional establishments. Major foodservice chains like Starbucks, Costa Coffee, and Dunkin' are actively expanding their plant-based menu options, particularly in beverages featuring vegan milk alternatives. The segment's evolution is particularly evident in major cities like Munich and Berlin, which host a significant number of vegan-friendly establishments. The channel's growth is supported by innovative product offerings, including specialized plant-based coffee drinks, desserts, and other culinary applications that showcase the versatility of dairy alternatives in foodservice settings.

Competitive Landscape

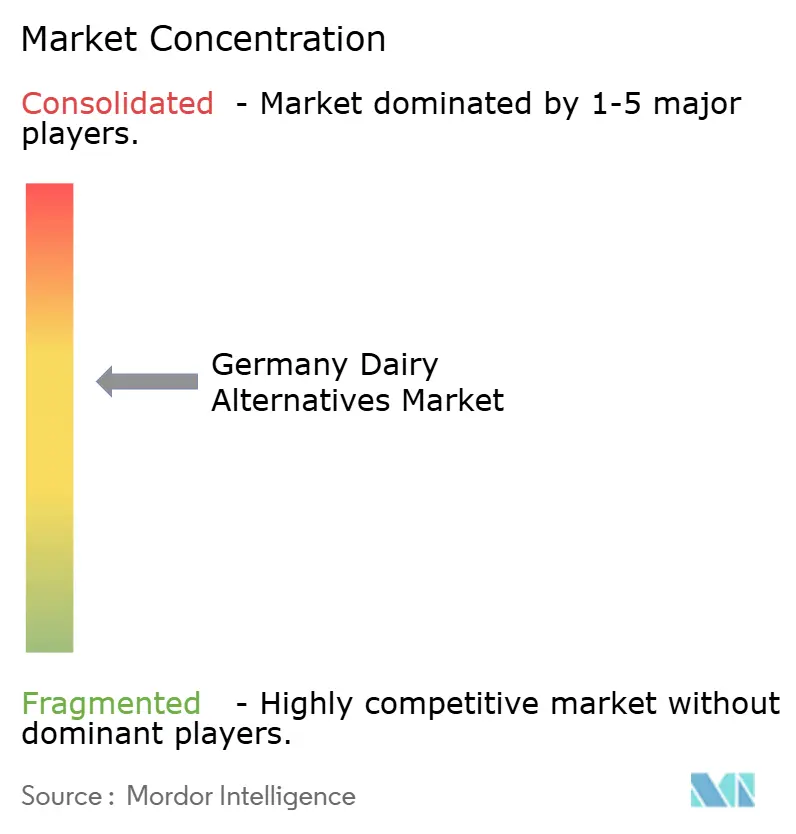

The Germany dairy alternatives market demonstrates a moderately concentrated competitive environment, with a market concentration score of 6 out of 10. This indicates a landscape where multinational corporations, specialized plant-based companies, and regional players actively compete. Danone SA (Alpro) leads the market with an 18.6% share, followed by Oatly Group AB at 14.2%. Their market leadership highlights the advantages of early entry, extensive distribution networks, and significant marketing investments, which contribute to strong consumer brand recognition and loyalty. Companies with diversified product portfolios across multiple plant-based categories benefit from cross-selling opportunities and economies of scale in production and distribution. Additionally, strategic partnerships between global food corporations and specialized plant-based innovators have resulted in hybrid competitive models that combine established market access with advanced product development capabilities.

Technology adoption has emerged as a critical competitive differentiator in the market. Companies are making substantial investments in precision fermentation, protein enhancement, and sensory optimization technologies to address historical barriers to mass-market adoption. The regulatory framework for novel foods established by the Federal Institute for Risk Assessment (BfR) creates opportunities for companies with advanced research and development capabilities to introduce innovative ingredients and processing methods that are difficult for competitors to replicate. Furthermore, white-space opportunities are evident in specialized segments such as sports nutrition, infant formula alternatives, and functional dairy products, which cater to specific consumer needs beyond basic milk substitution.

Emerging disruptors in the market are leveraging direct-to-consumer sales models, subscription services, and social media marketing to build strong brand communities. These approaches enable them to establish a competitive edge that traditional food companies often struggle to achieve through conventional retail channels. By focusing on consumer engagement and innovative distribution strategies, these disruptors are reshaping the competitive dynamics of the market. As a result, the Germany dairy alternatives market continues to evolve, driven by technological advancements, regulatory support, and the growing demand for specialized plant-based products.

Germany Dairy Alternatives Industry Leaders

-

AlnaturA Produktions- und Handels GmbH

-

Danone SA

-

Oatly Group AB

-

Upfield BV

-

Simply V

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2024: Germany’s Veganz Group has secured €10 million ($10.9 million) in equity financing to scale up production of its innovative 2D-printed oat milk product, Mililk, along with its plant-based meat analogue, Peas on Earth.

- February 2024: Oat drink manufacturer Oatly launched its new organic barista oat drink in Germany. According to Oatly, the Oatly Bio Barista is characterized by a special creaminess and is perfect for use in hot drinks, offering a professional quality froth for coffees and milk-style beverages.

Germany Dairy Alternatives Market Report Scope

Non-Dairy Butter, Non-Dairy Cheese, Non-Dairy Ice Cream, Non-Dairy Milk, Non-Dairy Yogurt are covered as segments by Category. Off-Trade, On-Trade are covered as segments by Distribution Channel.| Non-Dairy Butter | |

| Non-Dairy Milk | Almond Milk |

| Coconut Milk | |

| Oat Milk | |

| Soy Milk |

| Soy |

| Almond |

| Oat |

| Rice |

| Others |

| Flavored |

| Unflavored |

| Cartons |

| Plastic Bottle |

| Glass Bottle |

| Others (Tetrapacks, Pouches) |

| Off-Trade | Convenience Stores |

| Online Retail | |

| Specialist Retailers | |

| Supermarkets and Hypermarkets | |

| Others | |

| On-Trade |

| By Product Type | Non-Dairy Butter | |

| Non-Dairy Milk | Almond Milk | |

| Coconut Milk | ||

| Oat Milk | ||

| Soy Milk | ||

| By Source | Soy | |

| Almond | ||

| Oat | ||

| Rice | ||

| Others | ||

| Flavor | Flavored | |

| Unflavored | ||

| By Packaging Type | Cartons | |

| Plastic Bottle | ||

| Glass Bottle | ||

| Others (Tetrapacks, Pouches) | ||

| By Distribution Channel | Off-Trade | Convenience Stores |

| Online Retail | ||

| Specialist Retailers | ||

| Supermarkets and Hypermarkets | ||

| Others | ||

| On-Trade | ||

Market Definition

- Dairy Alternatives - Dairy alternatives are foods that are made from plant-based milk/oils instead of their usual animal products, such as cheese, butter, milk, ice cream, yogurt, etc. Plant-based or non-dairy milk alternative is the fast-growing segment in the newer food product development category of functional and specialty beverage across the globe.

- Non-Dairy Butter - Non dairy butter is a vegan butter alternative that is made from a mixture of plant oils. With an increase in alternative diets like vegetarianism, veganism, and gluten intolerance, plant butter is a healthy non-dairy substitute for normal butter.

- Non-Dairy Ice Cream - Plant based ice cream is a growing category. Non-dairy ice cream is a type of dessert made without any animal ingredients. This is typically considered a substitute for regular ice cream for those who cannot or do not eat animal or animal-derived products, including eggs, milk, cream, or honey.

- Plant-Based Milk - Plant based milks are milk substitutes that are made from nuts (e.g., hazelnuts, hemp seeds), seeds (e.g., sesame, walnuts, coconuts, cashews, almonds, rice, oats, etc.) or legumes (e.g., soy). Plant-based milk such as soy milk and almond milk have been popular in East Asia and the Middle East for centuries.

| Keyword | Definition |

|---|---|

| Cultured Butter | Cultured butter is prepared by having the raw butter go through chemical processing and has been added with certain emulsifiers and foreign ingredients. |

| Uncultured Butter | This type of butter is one which has not been processed in any way |

| Natural Cheese | The type of cheese in its most natural form. It is made from natural and simple products and ingredients, including fresh and natural salts, natural colors, enzymes, and high-quality milk. |

| Processed Cheese | Processed cheese undergoes the same processes as natural cheese; however, it requires more steps and many different forms of ingredients. Making processed cheese involves melting natural cheese, emulsifying it, and adding preservatives and other artificial ingredients or colorings. |

| Single Cream | Single cream contains around 18% fat. It’s a single layer of cream that appears over boiled milk. |

| Double Cream | Double cream contains 48% fat, more than double the amount of fat of single cream. It’s heavier and thicker than single cream |

| Whipping Cream | This has a much higher fat percentage than single cream (36%). Used to top cakes, pies, and puddings and as a thickener for sauces, soups, and fillings. |

| Frozen Desserts | Desserts that are meant to be eaten in frozen condition. E.g., sherbets, sorbets, frozen yogurts |

| UHT Milk (Ultra-high temperature milk) | Milk heated at a very high temperature. Ultra-high-temperature processing (UHT) of milk involves heating for 1–8 sec at 135–154°C. which kills the spore-forming pathogenic microorganism, resulting in a product with a shelf-life of several months. |

| Non-dairy butter/Plant-based butter | Butter made from plant-derived oil such as coconut, palm, etc. |

| Non-dairy Yogurt | Yogurt made from typically made from nuts, like almonds, cashews, coconuts, and even other foods like soybeans, plantains, oats, and peas |

| On-trade | It refers to restaurants, QSRs, and bars. |

| Off-trade | It refers to supermarkets, hypermarkets, on-line channels, etc. |

| Neufchatel cheese | One of the oldest kinds of cheese in France. It is a soft, slightly crumbly, mold-ripened, bloomy-rind cheese made in the Neufchâtel-en-Bray region of Normandy. |

| Flexitarian | It refers to a consumer preferring a semi-vegetarian diet, that is centered on plant foods with limited or occasional inclusion of meat. |

| Lactose Intolerance | Lactose intolerance is a reaction in digestive system to lactose, the sugar in milk. It causes uncomfortable symptoms in response to the consumption of dairy products. |

| Cream Cheese | Cream cheese is a soft and creamy fresh cheese with a tangy taste made from milk and cream. |

| Sorbets | Sorbet is a frozen dessert made using ice combined with fruit juice, fruit purée, or other ingredients, such as wine, liqueur, or honey. |

| Sherbet | Sherbet is a sweetened frozen dessert made with fruit and some sort of dairy product such as milk or cream. |

| Shelf stable | Foods that can be safely stored at room temperature, or "on the shelf," for at least one year and do not have to be cooked or refrigerated to eat safely. |

| DSD | Direct Store Delivery is the process in supply chain management wherein the product is delivered from manufacturing plant directly to the retailer. |

| OU Kosher | Orthodox Union Kosher is a kosher certification agency based in New York City. |

| Gelato | Gelato is a frozen creamy dessert made with milk, heavy cream and sugar. |

| Grass-fed Cows | Grass-fed cows are allowed to graze in pastures, where they eat a variety of grasses and clover. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms