Geomembranes Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

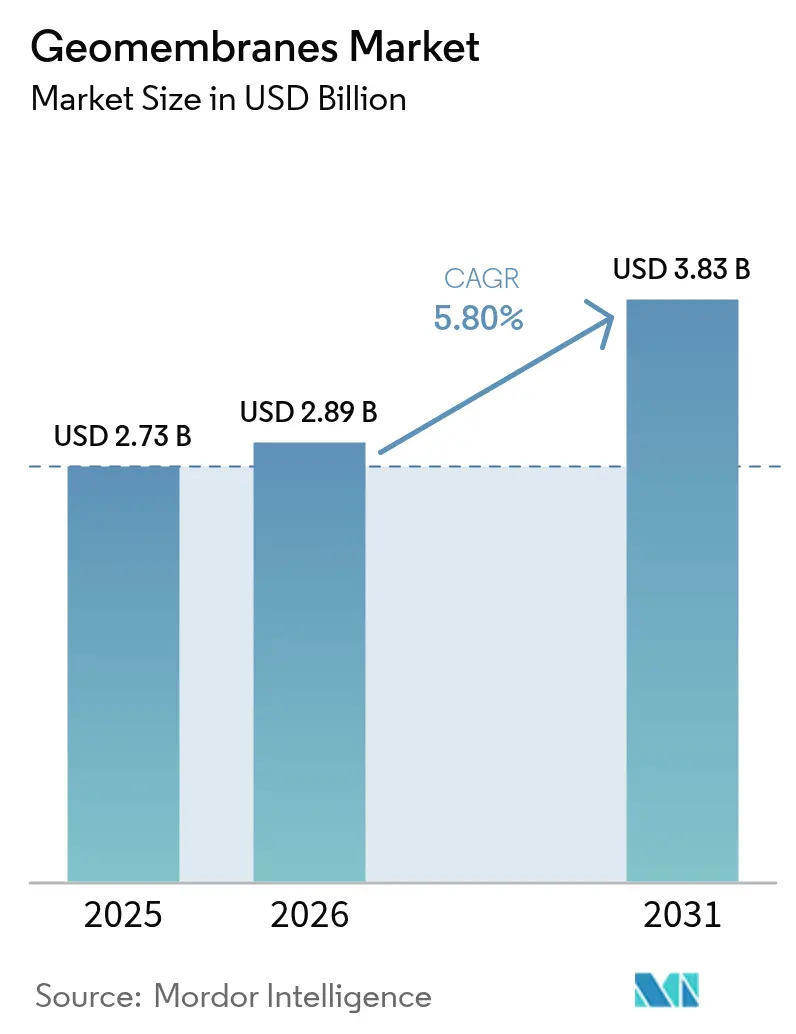

| Market Size (2026) | USD 2.89 Billion |

| Market Size (2031) | USD 3.83 Billion |

| Growth Rate (2026 - 2031) | 5.80% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Geomembranes Market Analysis by Mordor Intelligence

Geomembranes Market size in 2026 is estimated at USD 2.89 billion, growing from 2025 value of USD 2.73 billion with 2031 projections showing USD 3.83 billion, growing at 5.8% CAGR over 2026-2031. Sustained demand arises from strict environmental containment mandates in waste management and mining, coupled with large-scale water infrastructure programs that prioritize seepage control. Intensifying tailings-dam safety reforms after the Brumadinho and Chambishi failures have accelerated specification upgrades, while resin price volatility keeps margins fluid for producers that rely heavily on HDPE and PVC inputs. Extrusion remains the dominant manufacturing route; however, multilayer co-extrusion is gaining interest as operators seek membranes with higher chemical resistance and embedded sensor functionality. Heightened competitive intensity is evident in strategic takeovers, production footprint realignments, and continuous R&D efforts aimed at developing differentiated surface textures or reflective layers that unlock new solar and ag-tech end uses.

Key Report Takeaways

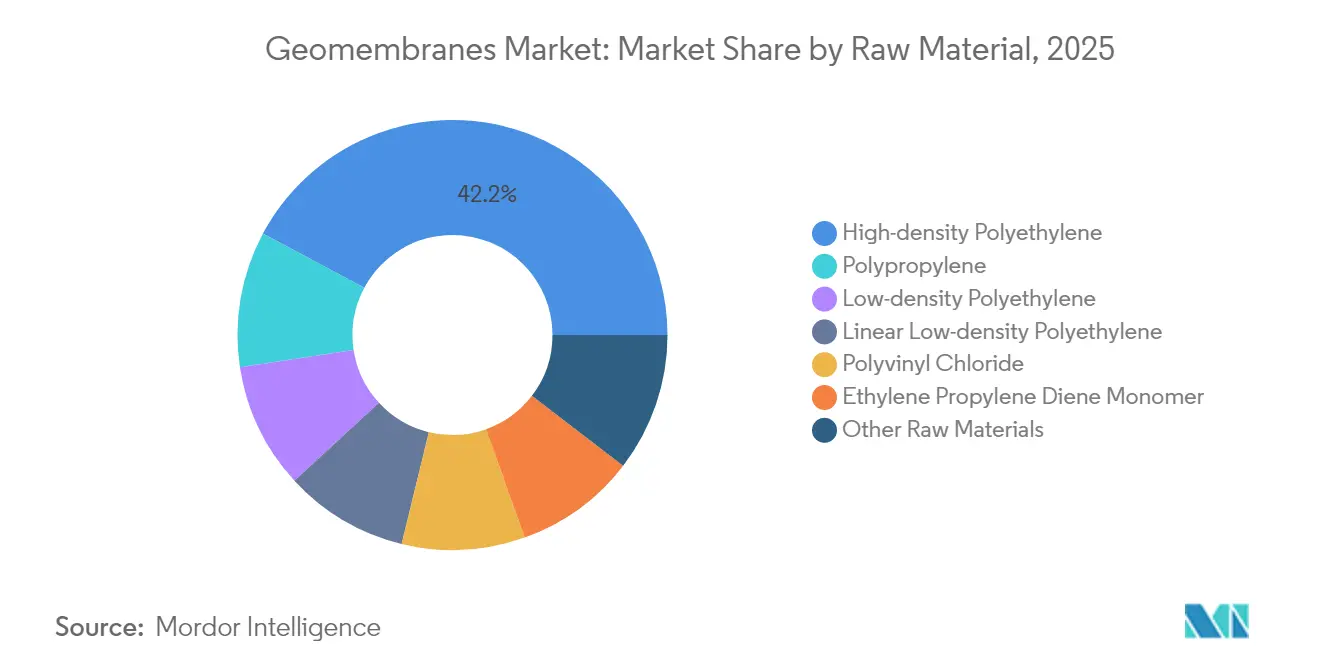

- By raw material, HDPE led with 42.18% of the geomembranes market share in 2025, whereas PP is forecast to post the fastest 5.95% CAGR to 2031.

- By application, waste management held 36.35% of the geomembranes market size in 2025; mining applications are advancing at a 6.15% CAGR through 2031.

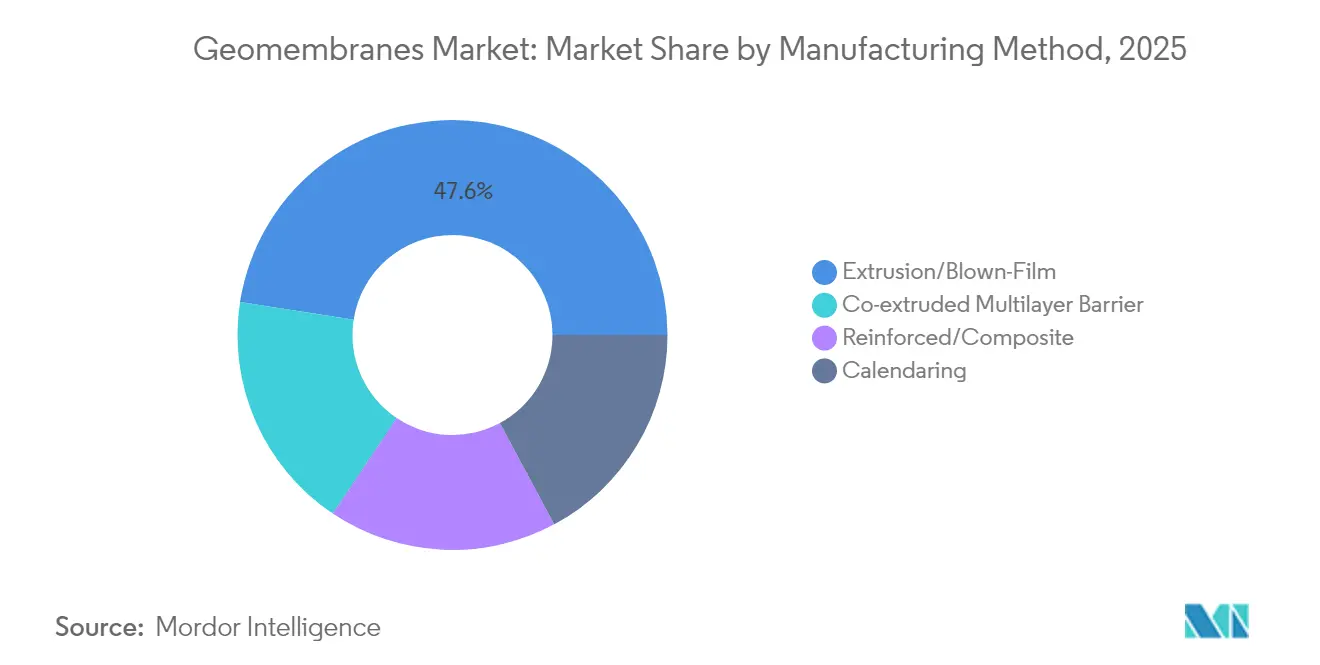

- By manufacturing method, extrusion/blown-film commanded 47.55% share of the geomembranes market size in 2025, while co-extruded multilayer barriers will expand at a 5.92% CAGR to 2031.

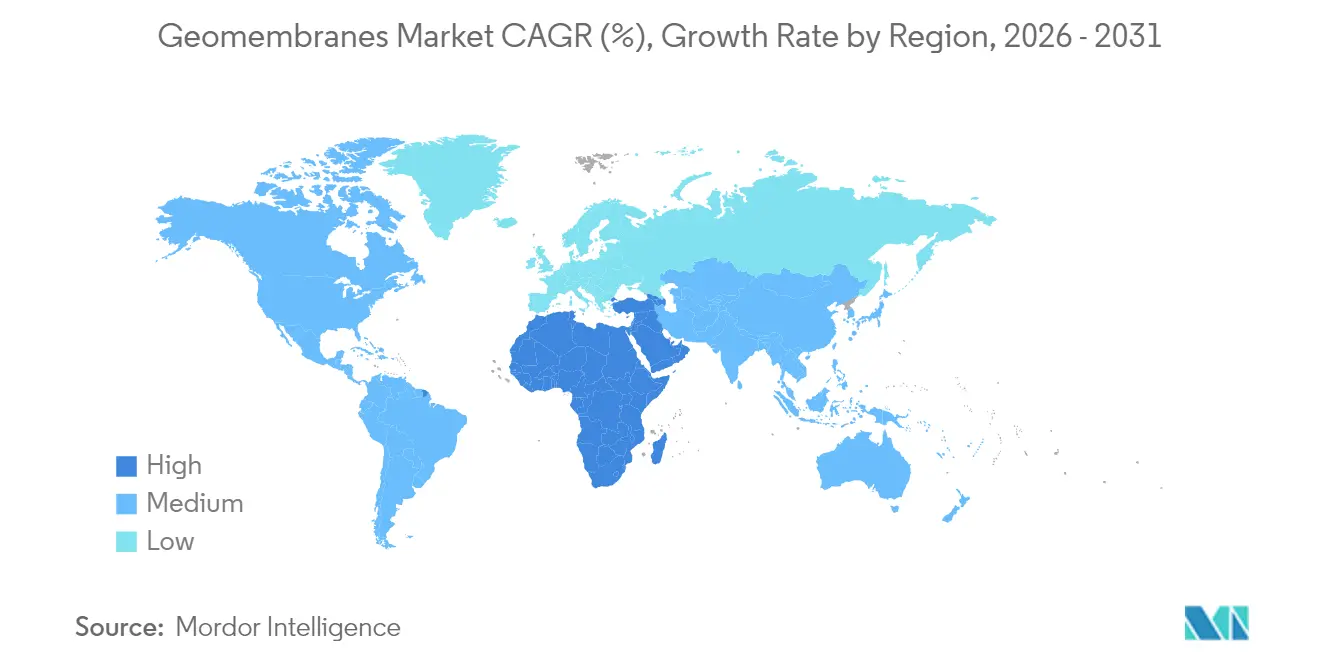

- By geography, Asia-Pacific captured 45.05% revenue in 2025, whereas the Middle East and Africa is set to grow the fastest at 5.78% CAGR up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Geomembranes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter landfill-seepage regulations | +1.20% | North America, EU, global rollout | Medium term (2-4 years) |

| Heap-leach copper expansion in Andes | +0.80% | South America core, global spill-over | Long term (≥ 4 years) |

| Reservoir lining mandates in water-scarce MEA | +1.00% | Middle East & North Africa | Medium term (2-4 years) |

| Rapid tailings-dam safety reforms | +1.40% | Global mining hubs, priority in South America | Short term (≤ 2 years) |

| Ag-tech driven lined irrigation ponds | +0.60% | Asia-Pacific, especially China, India, Southeast Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stricter Global Landfill-Seepage Regulations

Worldwide landfill directives now compel composite liner systems, pushing operators to adopt thicker, chemically robust geomembranes that guarantee near-zero permeability over long service lives. The U.S. EPA’s 40 CFR Part 258 updates, as well as similar EU rules, have set higher leakage detection standards that roll downstream into emerging economies[1]U.S. Environmental Protection Agency, “Hazardous Waste Regulations,” epa.gov . U.S. state amendments, such as Kentucky’s heightened liner provisions, illustrate how local jurisdictions can exceed federal baselines to mitigate liability exposure. This regulatory cascade drives continuous product upgrades, prompting suppliers to market multilayer HDPE films fortified with UV stabilizers and conductive layers for integrity surveys. Market participants able to demonstrate full compliance through third-party certifications gain pricing power and preferred-bid status in municipal bids. Capital budgets for new landfill cells increasingly earmark 10-15% of project value for liner packages, embedding steady demand into the geomembranes market.

Surging Heap-Leach Copper Projects in Andean Region

Copper miners in Chile and Peru are scaling heap-leach operations to process lower-grade ores cost-effectively, each pad demanding millions of square meters of high-acid-resistant liners. CODELCO’s alignment of all tailings facilities to GISTM exemplifies elevated containment spend that ripples through contractor and resin supply chains. HDPE and PP grades modified with antioxidants and higher molecular weight are becoming standard to endure high sulfuric acid concentrations and elevated temperatures. Regional installers are building niche expertise in cold-weld fusion and integrity testing, creating a competitive moat against generalist civil contractors. Suppliers that offer localized stock points and bilingual technical support secure repeat orders as maintenance campaigns run concurrently with expansion phases. By 2030, the Andean corridor is expected to remain the largest single regional pocket of geomembranes market demand outside Asia-Pacific.

Water-Scarcity-Led Reservoir Lining Mandates (Middle East)

Governments across Morocco, Algeria, and the Gulf Cooperation Council have mandated impervious reservoir linings to curtail evaporation and seepage as part of national water security strategies. Morocco’s USD 40 billion program alone will retrofit aging impoundments and build new lined reservoirs that rely on conductive HDPE or flexible PP membranes to facilitate leak-location surveys. Desalination brine ponds and treated effluent lagoons likewise require superior chemical compatibility to handle high salinity. Regional climate extremes reinforce demand for UV-stabilized, high-temperature-tolerant geomembranes. Modular factory-fabricated panels are favored to overcome labor shortages, enabling rapid field deployment ahead of summer peak demand. Collectively, these mandates are projected to lift Middle East & Africa volume demand faster than any other region over the forecast horizon.

Ag-Tech Boom Driving Lined Irrigation Ponds (APAC)

Governments in China and India subsidize precision farming tools that depend on reliable, loss-free water storage, leading to widespread deployment of lined ponds that mitigate seepage and algae growth. IoT-enabled irrigation platforms integrate leak sensors embedded in conductive PP geomembranes, enabling real-time water balance monitoring. Shrimp and finfish farmers in coastal Andhra Pradesh have adopted white-on-black HDPE liners that modulate pond temperature and facilitate pathogen control, raising yield while lowering antibiotic use. Sector tailwinds include tightening groundwater extraction limits that incentivize water recapture systems, all of which employ geomembranes. Suppliers offering small-roll, easy-to-handle membrane formats penetrate fragmented farm holdings, broadening the consumption base of the geomembranes market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Petro-resin price volatility | -0.90% | Global, acute in price-sensitive emerging economies | Short term (≤ 2 years) |

| Adoption of geosynthetic-clay liners | -0.50% | North America & EU, spreading to mature Asia markets | Medium term (2-4 years) |

| Limited certified installers in frontiers | -0.30% | Africa, Latin America, Southeast Asia mining frontiers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price Volatility of Petro-Based Resins

HDPE and PVC resin prices have experienced 15-20% quarter-to-quarter swings since 2024, driven by refinery outages and logistics disruptions. Membrane producers operate under fixed-award contracts that compress margins when resin costs spike. Some projects now include resin cost escalation clauses, but municipal tenders often resist variable pricing structures, forcing suppliers to hedge through forward contracts. Material substitution with PP or specialty blends partially offsets volatility but introduces supply complexities. The issue is more pronounced in emerging markets where cost sensitivity can delay liner upgrades, moderating short-term geomembranes market growth.

Limited Certified Installers in Frontier Mining Regions

Africa’s burgeoning copper and gold sectors face shortages of crews certified under the IAGI’s AIC program, extending project timelines and increasing the risk of poor seam quality[2]International Association of Geosynthetic Installers, “Approved Installation Contractor Program,” iagi.org . Mining majors import specialists at a premium cost, inflating total installed liner budgets. Training initiatives lag behind regional growth, constraining expansion until local capabilities improve. Manufacturers that offer onsite supervision and training packages differentiate themselves, but cannot scale enough to close the gap rapidly.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Raw Material: HDPE Retains Lead While PP Accelerates

HDPE anchored 42.18% of the geomembranes market share in 2025 thanks to its proven chemical resistance, UV stability, and stress-crack endurance in exposed containment systems. The material remains the first choice for landfill caps, mining ponds, and canal linings where design lives exceed 50 years. HDPE’s property profile and global resin supply chains allow consistent quality, yet its price fluctuation risk nudges some buyers toward PP. PP’s 5.95% CAGR through 2031 positions it as the fastest-growing raw material, underpinned by advances in biaxially oriented and multilayer blends that deliver high flexibility and low thermal expansion. These traits suit floating covers and solar-pond hybrids where membrane dimensional stability is critical.

Polyvinyl chloride continues to serve chemical storage and tunnel waterproofing where ease of factory pre-fabrication and weldability are paramount, though environmental concerns cap its growth. LDPE and LLDPE occupy specialist niches requiring conformability over irregular subgrades or temporary linings that demand rapid field seaming. EPDM addresses roofing and potable-water reservoirs because of its elastomeric behavior at extreme temperatures. Hybrid formulations incorporating recycled polymers and nanofillers are emerging, offering improved puncture resistance and scratch toughness. Adoption remains limited but showcases the innovation bandwidth that characterizes the geomembranes market.

By Application: Mining Uptick Challenges Waste Management Dominance

Waste management controlled 36.35% of the geomembranes market size in 2025, benefiting from mature regulatory frameworks that mandate composite liners and secondary containment. Municipal operators budget periodic cell expansions, providing a predictable revenue stream for membrane suppliers. Nonetheless, tighter landfill permitting processes in Europe and parts of North America moderate future volume growth. Mining applications are projected to grow at a 6.15% CAGR, reflecting the post-Brumadinho surge in global tailings-dam upgrades and the relentless copper heap-leach build-out in South America. Tailings facilities increasingly specify double HDPE liners with leak detection layers, boosting square-meter demand per facility.

Water management applications tap rising investments in desalination brine ponds, irrigation reservoirs, and flood-control basins, particularly in water-scarce MEA regions. Construction and tunnel lining employ flexible PVC or composite membranes for underground stations and deep excavations, though they represent a smaller share of the geomembranes market. Agriculture and aquaculture usage grows rapidly in Asia-Pacific, where lined ponds improve water efficiency and biosecurity. Soil management and erosion control rely on geomembranes as hydraulic barriers beneath reinforced earth structures, helping stabilize slopes and protect roadbeds amid more intense rainfall events attributed to climate variability.

By Manufacturing Method: Co-Extrusion Gains on Extrusion Dominance

Extrusion/blown-film processes supplied 47.55% of global volume in 2025 owing to their cost-effective, wide-width, and uniform-thickness output that aligns with large project needs. Investments in auto-gauge control and die-gap optimization have trimmed scrap rates, enhancing producer margins. Co-extruded multilayer barriers will register a 5.92% CAGR through 2031, propelled by demand for membranes that combine conductive layers for spark testing, white reflective surfaces for solar ponds, or odor-control films for waste treatment plants. These complex structures extend service life and broaden functional integration, reducing overall project cost despite higher per-square-meter pricing.

Calendaring remains essential for PVC membranes where precise thickness and surface smoothness are required, such as subway tunnel waterproofing. Reinforced/composite methods, embedding scrims or geotextiles between polymer layers, target applications subject to puncture hazards and high tensile loads, including oil-and-gas secondary containment. Emerging inline quality inspection systems with infrared thermography and machine-learning-driven defect recognition reduce post-production testing effort, reinforcing adoption of advanced manufacturing routes. As customers increasingly request documented roll-by-roll properties, digital traceability becomes a differentiator within the geomembranes market.

Geography Analysis

Asia-Pacific captured 45.05% of global revenue in 2025, reflecting a scale of public infrastructure investment unmatched elsewhere. China’s approval of the USD 137 billion Motuo Hydropower Project and India’s USD 13.2 billion Siang Upper Multipurpose Project illustrate mega-developments that embed long-term liner demand. Robust agricultural modernization programs across China and Southeast Asia deploy lined ponds for aquaculture and irrigation, while Indonesia and the Philippines expand municipal solid-waste landfills under new environmental rules. Regional resin production capacity offers cost advantages, enabling local manufacturers to serve projects with shorter lead times. Export-oriented producers in China and South Korea ship factory-fabricated panels to the Americas and Africa, leveraging currency competitiveness to win international bids within the geomembranes market.

Middle East and Africa is on track to post a 5.78% CAGR to 2031, propelled by national water strategies that prescribe lined reservoirs, evaporation ponds, and tailings dams. Morocco’s USD 40 billion water plan and Algeria’s multi-phase desalination roll-outs typify government-backed megaprojects that embed geomembrane line items into every tender. Mining investment from southern Africa’s copperbelt to Ghana’s gold fields heightens demand for chemical-resistant HDPE liners compliant with global standards. Regional supply chains still lean heavily on imports of premium membranes, encouraging global suppliers to establish distribution hubs in Dubai and Casablanca for faster delivery.

North America and Europe maintain steady replacement-cycle demand as older landfill cells and wastewater lagoons reach end-of-life. Tightened EPA rules and EU circular-economy directives elevate specification thickness and require double-liner systems in new cells, sustaining volume despite flat landfill openings. South America remains a bright spot because of Andean mining expansion and strict tailings legislation in Chile and Peru. Local liners compete on cost, but major projects rely on globally branded membranes to secure financier confidence, nurturing a healthy mix of regional and international suppliers within the geomembranes market.

Regulatory Landscape

Regulation for geomembranes is anchored in environmental containment and quality assurance requirements that translate into mandated liner performance, testing, and installation controls. In the United States, U.S. EPA landfill rules (40 CFR Part 258) and related guidance on geomembrane seam inspection practices reinforce documentation, seam testing, and leak detection expectations for composite liner systems. Standard-setting bodies also shape procurement: in June 2025, the Geosynthetic Institute (GSI) released Revision 7 of GRI-GM25 for geomembrane seam laboratory testing, tightening conformance requirements frequently referenced by owners, designers, and QA/QC teams.

Regulatory and trade measures increasingly affect material selection and delivered costs. China issued GB/T 17643-2025 for polyethylene geomembrane in April 2025 (implemented from November 2025), supporting more uniform product qualification for domestic infrastructure and export supply chains. On the import side, the Philippines Bureau of Customs implemented the third-year safeguard duty on HDPE imports in May 2025 under DAO 22-13, which increases landed-cost sensitivity for HDPE-heavy specifications. In May 2026, the U.S. Court of International Trade ruled that the February 2026 Section 122 global tariffs were invalid, underscoring how trade-policy shifts can quickly alter sourcing strategies for resin and finished rolls.

Value Chain Analysis

The geomembranes value chain starts upstream with crude oil and natural gas feedstocks converted into polymer resins (HDPE, LLDPE, PP, PVC), where resin producers and compounders influence cost and availability. Membrane manufacturers convert resins into sheets via extrusion/blown film, calendering (notably for PVC), or co-extruded multilayer structures, then add value through texturing, conductive layers, prefabrication, and roll-by-roll QA documentation. Distribution typically runs through direct-to-project supply for large tenders, regional distributors and stock points for smaller orders, and fabrication shops that deliver factory-welded panels to reduce field seaming.

Key bottlenecks include resin price volatility and project execution, particularly transport constraints for bulky rolls and the availability of certified installation crews for welding and integrity testing. To manage these constraints, producers and converters increase inventory buffers (commonly multi-week resin coverage) and use longer-term resin supply arrangements with major suppliers such as Dow and LyondellBasell. They also offer installation support and QA/QC services to de-risk performance. Downstream, owners and EPCs increasingly specify system-level deliverables, including geomembrane plus protection layers, seam test plans, and leak detection, which increases the service component of the chain and favors suppliers with fabrication capacity and installer networks.

Competitive Landscape

The geomembranes market displays moderate fragmentation with a gradual tilt toward consolidation as large players leverage M&A to secure technology and geographic reach. Solmax, with revenue estimated at USD 428.7 million, anchors the supplier base and operates in 58 countries, giving it scale to negotiate resin contracts and fund R&D on specialty products like GEOLUX, which boosts bifacial solar efficiency by raising ground albedo. Officine Maccaferri’s 2025 acquisition of Synteen Technical Fabrics adds technical scrim capabilities that bolster reinforced membrane portfolios.

Technology differentiation is an essential competitive lever. Producers invest in conductive-layer co-extrusion, antimicrobial formulations for aquaculture, and sensor-embedded films that enable real-time leak detection. Early-stage pilots combine printed circuitry with wireless transmitters to automate integrity monitoring over decades. Regional specialists in India and Turkey compete on price and project agility, targeting domestic irrigation and infrastructure segments where certification requirements are less stringent.

Service scope is evolving into a decisive factor. Leading suppliers offer design assistance, installation training, and lifecycle monitoring to mitigate the restraint of limited certified installers in frontier markets. Firms aligned with IAGI’s Approved Installation Contractor network gain a trust premium when bidding for mining or hazardous waste projects. Resin suppliers collaborate upstream with membrane producers to create tailored grades that offset price volatility and meet ESG criteria, reinforcing strategic partnerships throughout the geomembranes market value chain.

Geomembranes Industry Leaders

AGRU America, Inc.

ATARFIL, S.L.

NAUE GmbH & Co KG

Officine Maccaferri S.p.A

SOLMAX

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Water infrastructure rehabilitation and reservoir relining remain a concrete demand pool where geomembranes compete as a quicker containment solution versus full structural replacement. In the United States, U.S. EPA announced USD 3.6 billion for water infrastructure upgrades in October 2024, and federal water infrastructure funding for fiscal year 2025 reached a USD 6.2 billion annual total under the Infrastructure Investment and Jobs Act. This supports municipal programs that often include lining of lagoons, ponds, and reservoirs. Project activity also shows owners selecting higher-performing reinforced systems for critical assets, as seen in June 2026 when Layfield Geosynthetics was awarded a contract by the Metropolitan Water District of Southern California to reline the Garvey Reservoir using a double-lined reinforced HypaFlex CSPE geomembrane system.

On the supply side, capacity and productivity upgrades create whitespace in large-footprint containment projects (mining, waste, and water) by improving output economics and reducing seaming labor. In June 2026, Haoyang Environmental launched a 14-meter ultra-wide geomembrane production line that doubled capacity to a reported daily output of 50 tons, reflecting industry emphasis on wider widths, integrated texturing, and fewer field seams for mega-sites. Another opportunity area is the shift toward performance-based specifications and verified QA, where compliance to widely adopted standards (ASTM and GRI test methods and seam testing regimes such as GRI-GM25) supports premium positioning for multilayer, conductive, or reinforced products in projects with elevated containment liability.

Recent Industry Developments

- June 2026: Layfield Geosynthetics was awarded a contract by the Metropolitan Water District of Southern California to reline the Garvey Reservoir using a double-lined reinforced HypaFlex CSPE geomembrane system. The award highlights rising adoption of reinforced membranes and multi-layer containment designs in critical water infrastructure assets. It also reinforces the value of turnkey fabrication and installation capabilities as owners prioritize schedule certainty and verified field quality.

- April 2025: RENOLIT announced plans to expand in India with a new plant in Pune to manufacture geomembranes for civil engineering projects, with production planned to begin in April 2026 and an annual capacity of 6,000 tons. The investment adds regional manufacturing depth for Asia-Pacific infrastructure supply, shortening lead times versus imported rolls. Local output also supports participation in tenders that emphasize traceability and compliance documentation.

- May 2024: Solmax introduced a new geomembrane manufacturing line at its Houston, Texas facility to produce HDPE and LLDPE geomembrane liners for the GSE product line. The line expansion increases North American supply availability for landfill, mining, and water containment projects. Additional domestic capacity also helps suppliers manage logistics risk for bulky shipments and improves responsiveness to project-driven delivery windows.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the geomembranes market is defined as the revenue generated from manufactured polymeric sheets used as low-permeability liners and barriers for containment, separation, and waterproofing needs across industrial and civil applications, counted at the point of sale of the geomembrane product.

Scope exclusions: This sizing excludes installation and welding services, geotextiles and geogrids sold as standalone products, and full lining system packages unless the geomembrane value is separately priced.

Segmentation Overview

- By Raw Material

- High-density Polyethylene (HDPE)

- Low-density Polyethylene (LDPE)

- Linear Low-density Polyethylene (LLDPE)

- Polyvinyl Chloride (PVC)

- Ethylene Propylene Diene Monomer (EPDM)

- Polypropylene (PP)

- Other Raw Materials

- By Application

- Water Management

- Waste Management

- Mining

- Construction and Tunnel Lining

- Agriculture and Aquaculture

- Soil Management and Erosion Control

- By Manufacturing Method

- Extrusion/Blown-Film

- Calendaring

- Co-extruded Multilayer Barrier

- Reinforced/Composite

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Nigeria

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building a fact base on where geomembranes are consumed and what drives ordering patterns. We reviewed public infrastructure and construction pipelines, mining and waste-management activity, and water projects, using sources such as the US EPA, the US Geological Survey, the World Bank, and UN Comtrade, to ground demand direction and trade flows.

From there, pricing and supply context are added using public resin and polymer indicators, customs and tariff notes, patents, and safety or performance standards that affect material choice (for example, ASTM references available through public summaries). We also used company annual reports, investor presentations, and reputable industry press to cross-check capacity additions, utilization commentary, and regional mix. In a few places, paid subscriptions for company financials and an import-export shipment-level database were used to confirm shipment patterns and revenue ranges. These desk sources are illustrative only, and many other public references were also used to collect, validate, and clarify data points.

Primary Interviews and Surveys

Primary work focused on checking how demand is split across major use cases like landfills, mining containment, and water-related lining, and how buyers weigh thickness, resin choice, and certifications. We spoke with a mix of manufacturers, converters, distributors, engineering contractors, and large end users across major consuming regions, so assumptions from desk research could be adjusted where needed.

Pricing behavior was validated carefully because it can move with resin inputs and project timing. The discussion also helped set realistic adoption rates when alternative lining approaches can substitute in specific jobs.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 17% | APAC: 43% |

| Mid tier: 52% | Functional/Unit leaders: 36% | EMEA: 37% |

| Smaller Players: 19% | Managers: 47% | Americas: 20% |

Market-Sizing & Forecasting

The core sizing uses a top-down model where infrastructure and industrial activity are translated into a demand pool for lined area and containment needs. That demand pool is then converted into geomembrane volume using typical thickness and material selection, followed by revenue using region-specific average selling prices. To keep totals realistic, we corroborated results with selective bottom-up checks, including sampled supplier revenue ranges, channel mix checks, and a volume times price sanity test for a few high-usage applications.

Key inputs used in the model include landfill and waste containment additions, mining project activity and tailings storage needs, water reservoir and canal lining programs, regulatory enforcement intensity for environmental containment, resin price movement that affects pricing and substitution, and average thickness mix by application. Where bottom-up signals were incomplete, gaps were handled by applying conservative coverage ratios, then rechecking the implied per-project consumption against interview feedback.

For forecasting, scenario analysis was used around construction and mining cycles. Year-by-year growth was shaped with exponential smoothing on the underlying activity indicators. Assumptions on price progression were kept explicit, using a mix of resin-linked movement and contract lag behavior discussed by market participants, so the forecast does not overreact to short-term price spikes.

Data Validation & Update Cycle

Outputs are validated in practical steps to ensure the final numbers match real-world signals. We compare regional totals against independent indicators like project starts, trade flows, and known capacity expansions, and then investigate any sharp jumps that do not align with these signals.

Before sign-off, the model is reviewed by another analyst who checks variable logic, unit conversions, and whether price and volume movement are consistent with the market narrative. Reports are refreshed annually, and interim updates are triggered when material events occur, such as large resin price resets, major plant additions, or policy changes affecting containment requirements. Right before delivery, a final review pass is done so clients receive the most current view available.

Mordor Intelligence's Geomembranes Market Size Compared Against Other Published Estimates

Published market sizes for geomembranes can differ even when they appear to cover the same product, because timing, pricing logic, and the included boundary around adjacent lining materials are not always handled the same way. Gaps are also created when one estimate is anchored on a single base year and another uses newer price and project signals.

In practice, the largest gaps usually come from how average selling prices are carried forward during resin swings, how currency conversion is timed for regional revenues, and whether installation-heavy packages are partially counted as product revenue. A refresh-led approach that rechecks prices and volumes together reduces drift, and the model also stays cleaner when only the geomembrane product value is counted, rather than broader geosynthetic system spending.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.89 B (2026) | |

| Global Consultancy A | USD 2.07 B (2024) | Uses an earlier base year and may not fully roll forward regional ASP changes tied to resin movements, which can understate revenue in periods of price recovery and mix shifts. |

| Industry Publisher B | USD 2.48 B (2024) | Longer forecast framing with estimated years can rely on smoother price curves and different currency timing, which affects near-term totals when exchange rates and contract repricing are volatile. |

The table shows that the spread is largely a function of update timing and price handling, not just growth expectations. By revalidating ASP progression and currency timing close to publication, then stress-testing those results with channel checks, Mordor Intelligence keeps the 2026 value tied to current demand signals rather than older price anchors.

Key Questions Answered in the Report

How large is the geomembranes market in 2026 and how fast is it growing?

The geomembranes market size is USD 2.89 billion in 2026 and is projected to grow at a 5.80% CAGR to reach USD 3.83 billion by 2031.

Which raw material currently leads global demand?

HDPE holds the lead with 42.18% share in 2025 due to its chemical resistance and long service life.

Which application segment is expanding the fastest through 2031?

Mining applications are advancing at a 6.15% CAGR as operators invest in upgraded tailings and heap-leach containment.

What region offers the highest growth outlook?

Middle East and Africa is forecast to register the fastest 5.78% CAGR, underpinned by large water-security infrastructure programs.

How are manufacturers differentiating their products?

Suppliers are embracing co-extruded multilayer barriers, conductive surfaces for leak detection, and reflective films for solar applications.

What key risk could temper near-term demand?

Volatile resin prices can compress producer margins and delay projects in cost-sensitive markets.

Page last updated on: