Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 20.40 Billion |

| Market Size (2031) | USD 27.15 Billion |

| Growth Rate (2026 - 2031) | 5.88% CAGR |

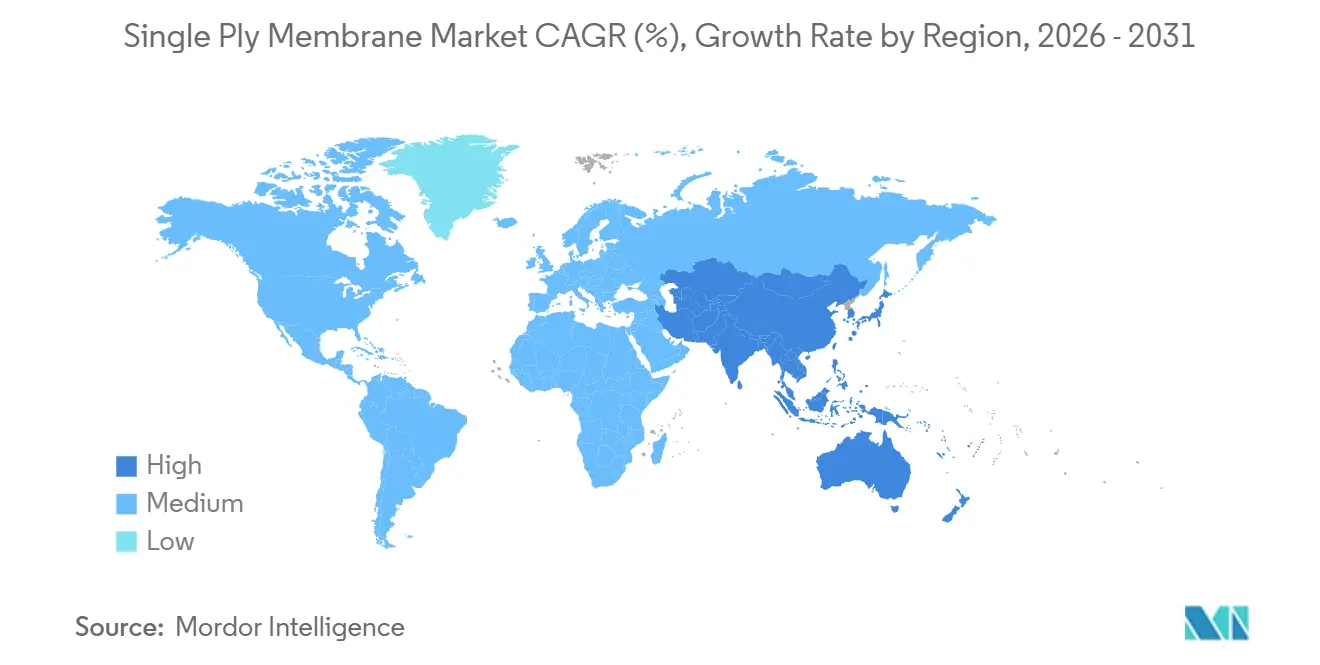

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

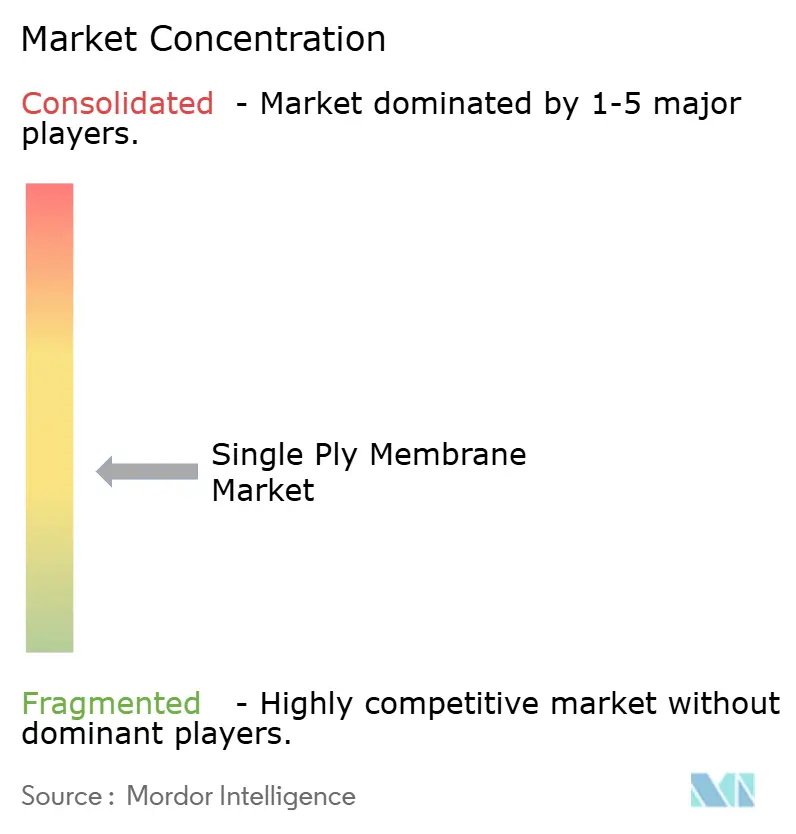

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Single Ply Membrane Market Analysis by Mordor Intelligence

The Single Ply Membrane Market size is estimated at USD 20.40 billion in 2026, and is expected to reach USD 27.15 billion by 2031, at a CAGR of 5.88% during the forecast period (2026-2031). Demand momentum stems from overlapping forces. Commercial reroofing cycles in the United States and Canada have entered peak replacement years, data-center construction is scaling across Asia-Pacific, and green-building mandates such as the European Union’s 2024/1275 directive are tightening performance thresholds for roofing assemblies. Thermoplastic and elastomeric sheets are displacing built-up roofs because they install faster, offer higher solar reflectance, and deliver superior life-cycle economics. Labor-saving 16-foot-wide TPO rolls, cool-roof utility rebates, and growing solar-ready specifications are further widening the cost–benefit gap in favor of single-ply membranes. Competitive intensity remains moderate, yet regional specialists are carving out share in installer-constrained markets and in niches such as green-roof systems and photovoltaic-integrated assemblies.

Key Report Takeaways

- By product type, Poly Vinyl Chloride held 36.39% of the single ply membrane market share in 2025, while Thermoplastic Polyolefin is projected to record the fastest 7.01% CAGR to 2031.

- By application, infrastructure topped revenue with 44.17% share in 2025; residential retrofits are expected to advance at a 5.95% CAGR through 2031.

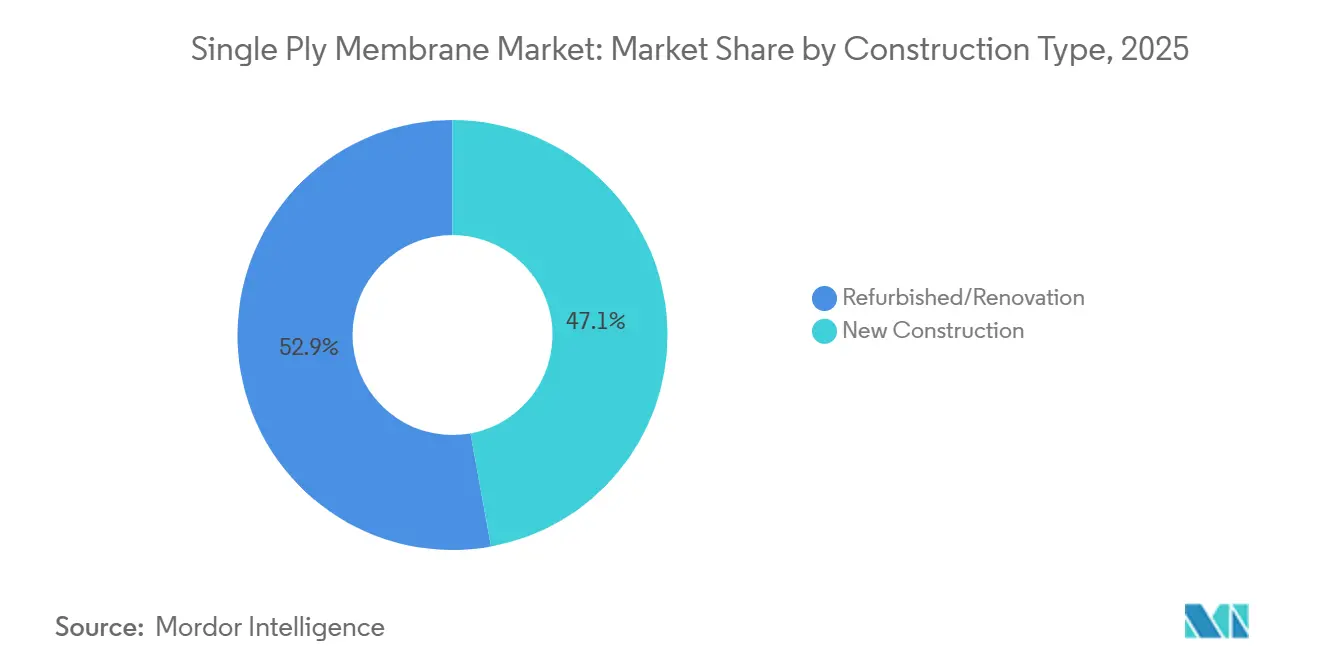

- By construction type, renovation captured 52.87% of the single ply membrane market size in 2025, whereas new-build demand is forecast to scale at a 6.23% CAGR over 2026-2031.

- By region, Asia-Pacific led with a 33.97% share in 2025 and is set to accelerate at a 6.55% CAGR, outpacing all other geographies.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Single Ply Membrane Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for energy-efficient and cool-roof systems | +1.2% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Commercial reroofing boom in North America | +1.5% | North America, particularly United States and Canada | Short term (≤ 2 years) |

| Urbanization-led construction up-cycle in Asia-Pacific | +1.3% | Asia-Pacific core, spill-over to Middle-East and Africa | Long term (≥ 4 years) |

| Government incentives and stricter green-building codes | +0.9% | North America, Europe, select Asia-Pacific markets | Medium term (2-4 years) |

| Adoption of 16-ft wide TPO rolls cuts labour 15-20% | +0.6% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Energy-Efficient and Cool-Roof Systems

Cool-roof membranes enable ENERGY STAR certification and LEED v4 points, all while meeting the Cool Roof Rating Council’s stringent aged-reflectance standards[1]Cool Roof Rating Council, “CRRC‐1 Program Manual,” coolroofs.org. California’s Title 24 code now mandates cool roofs on every low-slope commercial building, pushing contractor lead times for white TPO and PVC beyond eight weeks in late 2024[2]California Energy Commission, “2024 Title 24 Building Standards,” energy.ca.gov. The U.S. EPA is expanding its Heat-Island Reduction Program to 15 new metro areas in 2026, triggering municipal subsidies for reflective retrofits on government facilities. Large-scale solar developers favor bright membranes that limit thermal stress on photovoltaic modules, a requirement addressed by Carlisle’s SeamShield coating that pairs high albedo with induction-welded seams.

Commercial Reroofing Boom in North America

In 2024, the U.S. nonresidential roofing sector experienced significant growth, supported by aging low-slope stock. Contractors predominantly favor single-ply membranes, which constitute the majority of their project mix. Within this category, TPO holds the largest share, followed by PVC and EPDM. Carlisle's construction-materials revenue was bolstered by a strong EBITDA margin, thanks to normalized distributor inventories and robust contractor backlogs. GAF's upcoming shingle plant in Newton, Kansas, announced in March 2024 and set to break ground in June 2025, underscores the company's faith in sustained reroofing demand. However, with automation in play, the workforce expansion is limited to a modest number of roles.

Urbanization-Led Construction Up-Cycle in Asia-Pacific

In 2024, ASEAN drew in significant foreign direct investment, with a notable surge in construction inflows. The region's data-center capacity has now expanded across numerous facilities, all of which are in need of high-performance low-slope roofing systems. In its 2024-25 budget, India set aside substantial funds for capital projects, with a significant portion directed towards logistics corridors, often opting for cost-efficient TPO or EPDM assemblies. While China's real-estate investment saw a year-over-year decline in early 2024, the renovation of existing industrial assets has somewhat mitigated this downturn. Research from OECD on climate risks is prompting coastal governments to mandate membranes that adhere to strict wind-uplift ratings, with a clear preference for mechanically fastened TPO and PVC in areas vulnerable to typhoons.

Government Incentives and Stricter Green-Building Codes

In 2024, the EU Building Energy Performance Directive 2024/1275 mandated a 2030 zero-emission target for all new structures, emphasizing the importance of solar-readiness and life-cycle carbon disclosure. LEED v5 beta has tightened its standards, raising embodied-carbon thresholds and offering bonus points for membranes containing recycled content. Notably, Carlisle achieved this benchmark in 2024 by reclaiming post-consumer scrap. Meanwhile, the U.S. Department of Energy rolled out its 2024 Cool-Surfaces Deployment Plan, providing grants for municipal retrofits. In parallel, India's Bureau of Energy Efficiency is formulating cool-roof mandates for its major metropolitan areas.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Polymer and additive price volatility | -0.8% | Global, with acute impact in Europe and Asia-Pacific | Short term (≤ 2 years) |

| Shortage of certified single-ply installers | -0.5% | North America and Europe | Medium term (2-4 years) |

| Municipal PVC bans in parts of EU | -0.3% | Europe, concentrated in Germany, France, and Nordic countries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Polymer and Additive Price Volatility

In June 2025, PVC resin prices in the U.S. declined year over year. Meanwhile, European prices increased, tightening the margins for global producers. Propylene, the feedstock for TPO, experienced fluctuations throughout 2024, influenced by turnarounds at Gulf Coast refineries. Ethylene prices for EPDM also varied, primarily due to outages at crackers. After peaking in 2023, titanium-dioxide costs stabilized in 2025. However, with supply concentrated among just three global vendors, an oligopoly pricing power remains intact. In a strategic move, major membrane producers are securing multi-year resin contracts. These contracts, featuring floor-and-ceiling clauses, shield a significant portion of their feedstock exposure but cap potential gains when spot prices dip.

Shortage of Certified Single-Ply Installers

NRCA ProCertification costs discourage entry-level roofers and stifle workforce growth, especially in rural regions. The Technical Roofing Academy's certification capacity falls short of North America's projected demand. In Q2 2024, Carlisle noted that many of its contractor partners grappled with labor shortages, pushing project starts back significantly. GAF's training initiative for 2025 targets the certification of more installers by 2027, but its stipulation for brand exclusivity risks fragmenting the industry. Handwerkskammer in Germany highlights a decline in roofing apprenticeships since 2020, pointing to analogous challenges across Europe.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: TPO Gains as PVC Navigates Regulatory Headwinds

Thermoplastic Polyolefin is projected to post a 7.01% CAGR from 2026-2031, the fastest rate among material classes, buoyed by labor-saving 16-foot rolls and stricter cool-roof codes. Poly Vinyl Chloride retained a 36.39% single ply membrane market share in 2025, protected by strong chemical resistance and fire-safety credentials, yet municipal bans in Germany, France, and Nordic countries are eroding its European footprint. Ethylene Propylene Diene Monomer remains popular for warehouse roofs where capital cost eclipses reflectivity, although EPDM’s darker color disqualifies it from many utility rebates. Modified bitumen continues to lose relevance as contractors migrate toward hot-air-welded TPO solutions that cut installation schedules.

Innovation is witnessing a resurgence. Sika’s felt-back self-adhered PVC is designed for sub-40 °F applications, where traditional solvent-based adhesives falter. Meanwhile, Carlisle’s Sure-Weld TPO boasts tensile strengths exceeding ASTM standards. While specialty blends like KEE and composite sheets command a modest share, they're increasingly chosen for green roofs and photovoltaic-integrated setups due to their puncture resistance and electrical insulation properties. With FM Global Class 90 ratings becoming essential for facilities in hurricane-prone areas, there's a noticeable uptick in investments towards seam-welding and uplift-test capabilities.

By Application: Infrastructure Dominates, Residential Accelerates

Infrastructure accounted for 44.17% of 2025 demand, spanning logistics hubs, transit terminals, and solar farms that prioritize durability and low maintenance. The residential segment, though smaller, is projected to lead growth at a 5.95% CAGR as homeowners chase utility rebates and FORTIFIED insurance discounts by retrofitting shingle roofs with cool TPO and PVC assemblies. While North America and ASEAN data-center hubs continue to see robust commercial demand, China's market is cooling as new real-estate projects decline. To earn LEED v5 points, institutional projects like schools and hospitals are increasingly opting for membranes containing recycled content.

GAF's partnership with the Insurance Institute for Business and Home Safety streamlines the FORTIFIED certification process, leading to a reduction in insurance premiums for homeowners in the Gulf Coast. Prefabricated membrane panels, which combine insulation and cover boards at the factory, are becoming popular in occupied buildings, especially where obtaining on-site hot-work permits proves challenging. In densely populated European cities, green-roof assemblies are opting for root-resistant PVC or KEE sheets, trading stormwater credits against a premium. Additionally, PV-ready roofs are now requiring membranes thicker than 72 mils to endure mounting-rail loads and thermal cycling.

By Construction Type: Renovation Leads, New Construction Gains Momentum

Renovation captured 52.87% of global revenue in 2025, underscoring the prevalence of aging low-slope roofs. By using mechanically fastened TPO overlays, contractors can often skip the tear-off process, leading to cost savings and shorter project timelines. New construction is forecast to rise at a 6.23% CAGR, fueled by greenfield projects set to launch across ASEAN in 2024 and bolstered by India's ambitious capex plan for logistics corridors. In new builds, fully adhered or self-adhered membranes are preferred for their ability to achieve higher wind ratings and seamlessly integrate with below-grade waterproofing. Meanwhile, in China, developers are shifting their focus to renovating existing industrial properties, maintaining demand levels even as interest in residential towers wanes.

Geography Analysis

Asia-Pacific controlled 33.97% of global revenue in 2025 and is expected to outpace every other region with a 6.55% CAGR to 2031. Cross-border investments in electronics, electric vehicles (EVs), and pharmaceuticals are driving the construction of factories that increasingly favor clean-roof PVC systems. Concurrently, data centers have boosted their capacity significantly, each requiring sturdy low-slope roofs to support heavy HVAC equipment. India's unprecedented infrastructure allocations, coupled with mandatory cool-roof initiatives in hotter regions, are further propelling regional adoption. Despite a pullback in China's real estate sector, the ongoing renovation of its vast existing stock continues to bolster demand, particularly for cost-effective EPDM overlays.

North America stands as the second-largest market for single-ply membranes. The U.S. nonresidential roofing sector is experiencing growth, with single-ply assemblies taking center stage in project portfolios. The push from Title 24 cool-roof mandates, alongside FORTIFIED hurricane standards, is accelerating the adoption of TPO and PVC. While Canada reaps the benefits of federal infrastructure investments, Mexico's automotive and electronics near-shoring boom is driving the construction of logistics parks in states like Nuevo León and Guanajuato. However, labor shortages are extending lead times and inflating labor costs, particularly in Alberta, British Columbia, and the U.S. Sunbelt.

Europe is navigating a landscape of contradictions. The tightening of lead limits in PVC by Commission Regulation 2023/923, along with bans on PVC roofs for public buildings in several municipalities, is pushing the market towards TPO and EPDM alternatives. On the other hand, the EU's zero-emission-building mandate is spurring a surge in retrofit activities, especially in Germany, France, and the U.K. Here, property owners are overlaying existing roofs with reflective TPO to align with carbon reduction targets. However, declining apprenticeship rates in Germany and labor shortages post-Brexit in the U.K. are extending project timelines. In Russia, due to market constraints from sanctions, there's a preference for locally produced EPDM and bitumen. Meanwhile, countries like Brazil, Saudi Arabia, and South Africa are witnessing selective growth, driven by projects in airports, stadiums, and utilities.

Competitive Landscape

The global single-ply membranes market is moderately fragmented. Carlisle’s USD 2.025 billion divestiture of its interconnect unit and USD 410 million acquisition of MTL Holdings in 2024 sharpened its focus on building products. Sika is executing a diversification play, purchasing Cromar in the U.K., Elmich in Singapore, and Gulf Seal in Saudi Arabia to cross-sell waterproofing and green-roof solutions. Distributor consolidation is another flashpoint. QXO’s USD 11 billion hostile bid for Beacon Roofing Supply in January 2025 signals tightening channel leverage that could compress supplier margins for firms lacking direct-to-contractor programs. Technology is a differentiator: leaders invest in prefabricated membrane panels that cut field labor 20%, self-adhered sheets that eliminate VOCs, and recycled-content formulations that satisfy LEED v5 credits.

Single Ply Membrane Industry Leaders

Carlisle SynTec Systems

GAF

Holcim Elevate (Firestone)

Sika AG

Johns Manville

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Seaman Corporation’s FiberTite single-ply membranes received a 40-year reference service life under a cradle-to-grave environmental product declaration, reinforcing performance credentials for institutional owners.

- September 2024: Kingspan acquired IB Roof Systems, marking its first entry into the United States single-ply segment and complementing organic TPO and polyiso insulation investments in Oklahoma and Maryland.

Global Single Ply Membrane Market Report Scope

Single-ply membranes are synthetic sheets made of rubber and other materials that can be ballasted or chemically bonded to insulation to create a layer of security for a building.

The single-ply membranes market is segmented into type, application, construction type, and geography. By type, the market is segmented into ethylene propylene diene monomer (EPDM), thermoplastic polyolefin (TPO), polyvinyl chloride (PVC), modified bitumen, and other types. By application, the market is segmented into residential, commercial, institutional, and infrastructure. By construction type, the market is segmented into new construction and refurbished/renovation. The report also covers the market size and forecasts for the single-ply membranes market in 18 countries across major regions. The market sizing and forecasts for each segment have been done based on revenue (USD).

By Type

| Ethylene Propylene Diene Monomer (EPDM) |

| Thermoplastic Polyolefin (TPO) |

| Poly Vinyl Chloride (PVC) |

| Modified Bitumen |

| Other Types |

By Application

| Residential |

| Commercial |

| Institutional |

| Infrastructure |

By Construction Type

| New Construction |

| Refurbished/Renovation |

By Geography

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Ethylene Propylene Diene Monomer (EPDM) | |

| Thermoplastic Polyolefin (TPO) | ||

| Poly Vinyl Chloride (PVC) | ||

| Modified Bitumen | ||

| Other Types | ||

| By Application | Residential | |

| Commercial | ||

| Institutional | ||

| Infrastructure | ||

| By Construction Type | New Construction | |

| Refurbished/Renovation | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the single-ply membrane market in 2026?

The single-ply membrane market size is valued at USD 20.40 billion in 2026.

What is the projected CAGR for single-ply membranes to 2031?

The market is forecast to grow at a 5.88% CAGR between 2026 and 2031, reaching USD 27.15 billion.

Which material type is expected to grow fastest through 2031?

Thermoplastic Polyolefin is poised for the quickest expansion at a 7.01% CAGR.

Why is Asia-Pacific the leading growth region?

Robust data-center builds, rising infrastructure budgets, and cool-roof mandates drive Asia-Pacific’s 6.55% CAGR outlook.

What factors limit faster market expansion?

Price volatility in polymer feedstocks, a shortage of certified installers, and localized PVC bans in Europe restrain growth.

Page last updated on: