Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

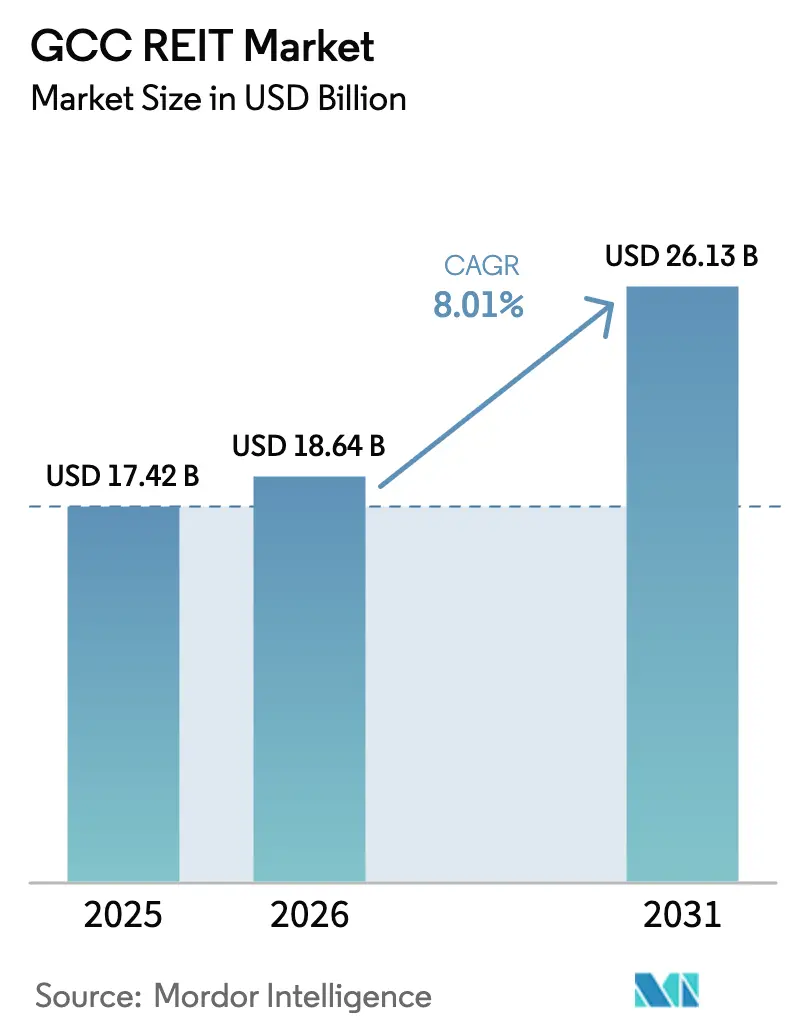

| Base Year Market Size (2025) | USD 17.42 Billion |

| Market Size (2026) | USD 18.64 Billion |

| Market Size (2031) | USD 26.13 Billion |

| Growth Rate (2026 - 2031) | 8.01% CAGR |

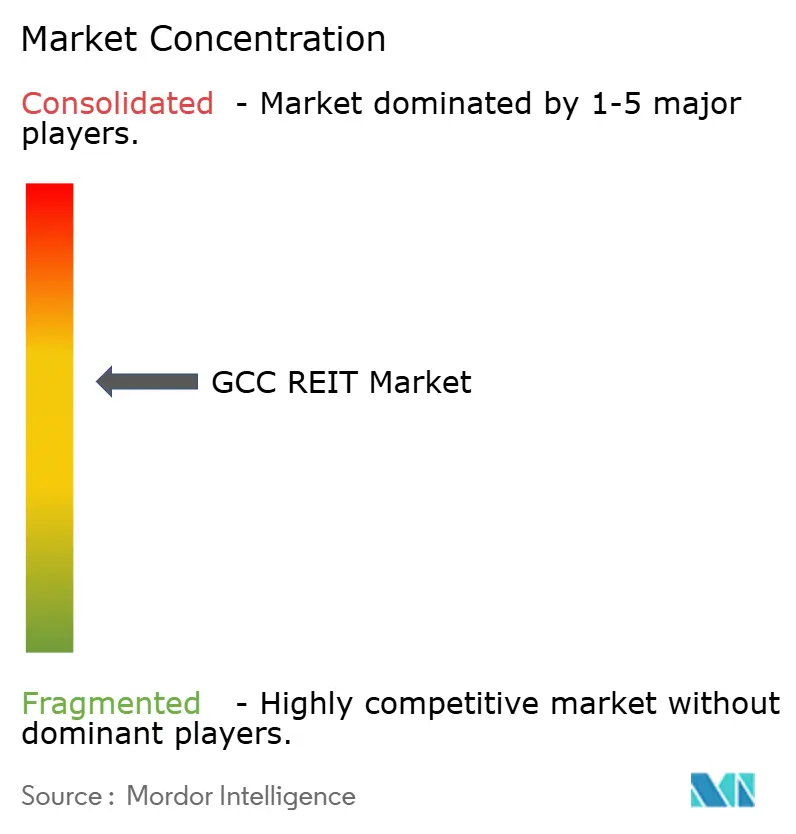

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC REIT Market Analysis by Mordor Intelligence

The GCC REIT Market size was valued at USD 17.42 billion in 2025 and is estimated to grow from USD 18.64 billion in 2026 to reach USD 26.13 billion by 2031, at a CAGR of 8.01% during the forecast period (2026-2031).

Robust sovereign appetite for domestic yield assets, progressive foreign-ownership reforms, and index inclusion on Tadawul and Dubai Financial Market are lifting the GCC REIT market toward deeper institutional participation. Mid-cycle policy traction, such as the 90% income-distribution mandate in Saudi Arabia and the UAE’s higher leverage ceiling, has converted latent real-estate value into liquid units. Foreign investors increasingly prefer listed trusts to direct property, where a 10% transaction fee now applies, redirecting capital into the GCC REIT market even as global rates rise[1]Capital Market Authority, “Real Estate Investment Funds Regulations,” CMA.ORG.SA. A maturing pipeline of giga-projects is supplying institutional-grade stock, while specialized data-center and logistics mandates are widening the sector mix across the GCC REIT market.

Key Report Takeaways

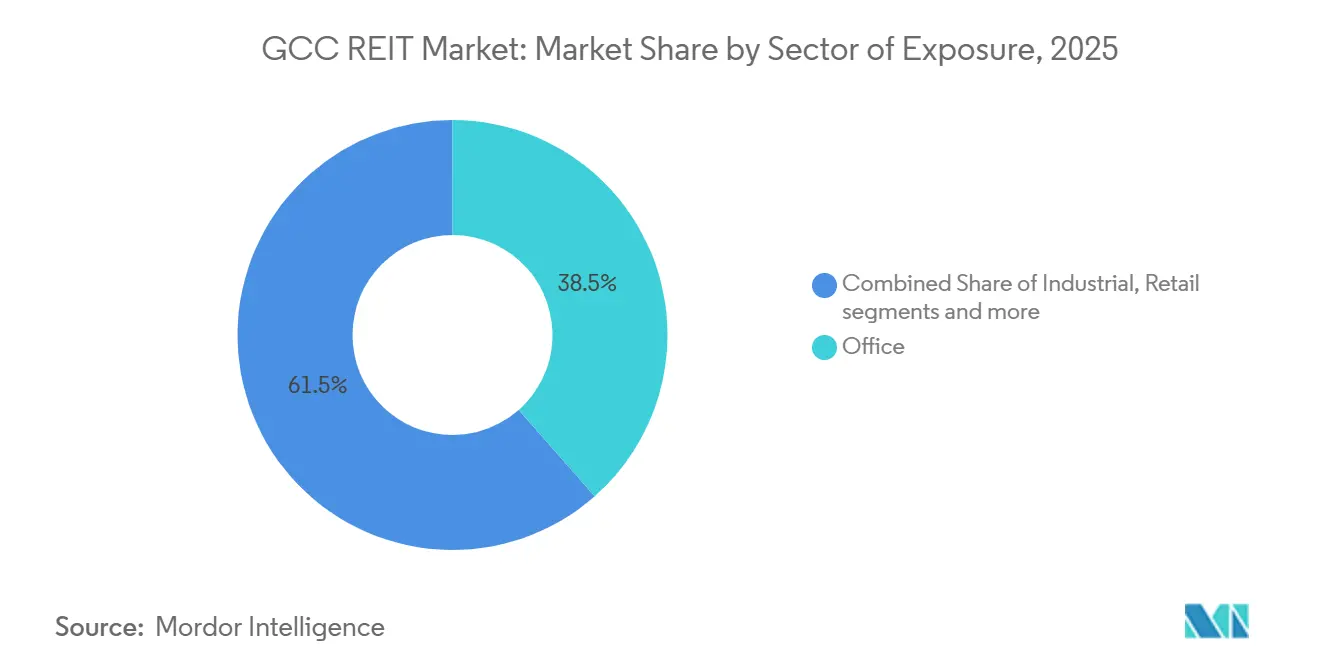

- By sector of exposure, office holdings led with 38.5% of GCC REIT market share in 2025; data-center assets are projected to expand at a 9.11% CAGR through 2031.

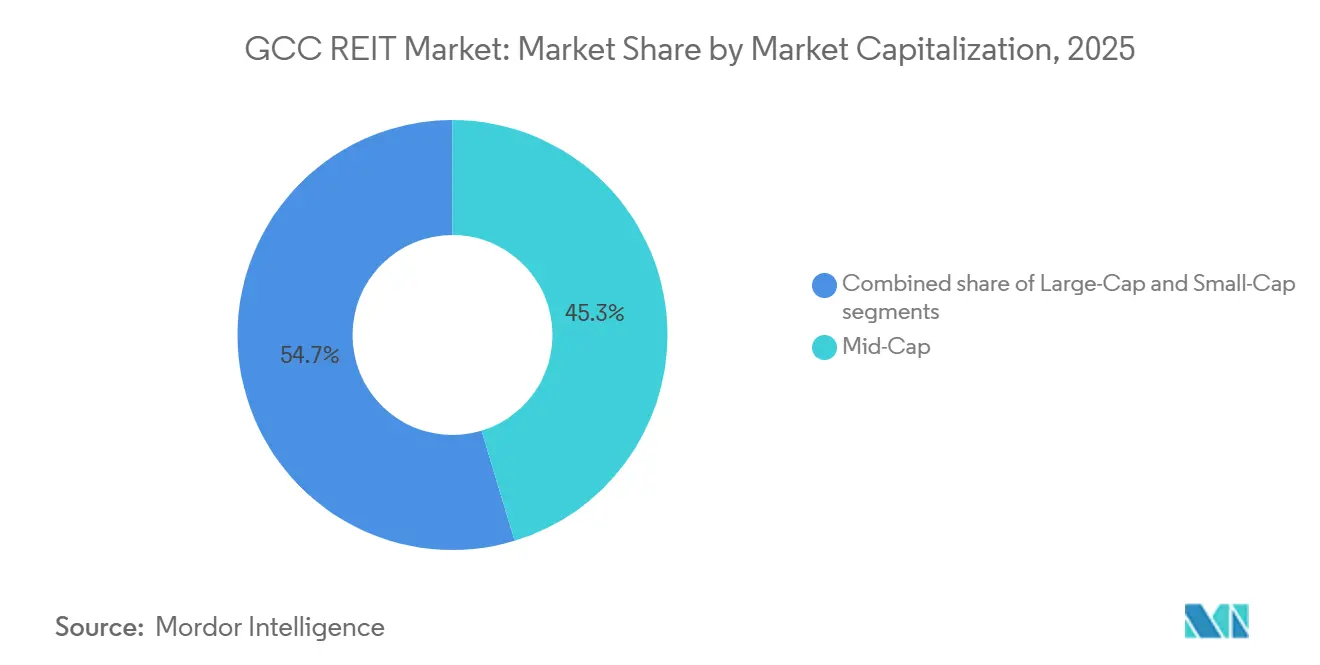

- By market capitalization, mid-cap vehicles accounted for 45.33% of the GCC REIT market size in 2025, while small-cap trusts are advancing at a 10.2% CAGR to 2031.

- By geography, Saudi Arabia captured 61.22% of the GCC REIT market share in 2025, while Oman is anticipated to register the fastest growth, expanding at a CAGR of 8.78% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

GCC REIT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising appetite of GCC sovereign wealth funds for domestic real-estate income streams | +1.8% | Saudi Arabia, UAE core; spillover to Qatar, Bahrain | Medium term (2–4 years) |

| Giga-project pipelines creating institutional-grade inventory | +1.6% | Saudi Arabia (NEOM), Qatar (Lusail), UAE | Long term (≥ 4 years) |

| Eased foreign-ownership limits in Saudi Arabia and UAE | +1.5% | Saudi Arabia, UAE | Short term (≤ 2 years) |

| Accelerated government privatization of public real-estate portfolios | +1.4% | Saudi Arabia, Kuwait, Oman | Long term (≥ 4 years) |

| Specialized digital-infrastructure & logistics assets fuelling new REIT structures | +1.3% | UAE, Saudi Arabia; early adoption in Qatar | Medium term (2–4 years) |

| Launch of REIT-focused indices on Tadawul and DFM driving passive inflows | +1.2% | Saudi Arabia, UAE | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Appetite of GCC Sovereign Wealth Funds for Domestic Real-Estate Income Streams

Major Gulf sovereign vehicles have pivoted from overseas trophy assets to domestic yield assets, anchoring several flagship trusts and improving market depth. The Public Investment Fund’s 2024 decision to seed a Saudi residential REIT and Abu Dhabi Investment Authority’s co-investment in regional logistics portfolios exemplify this repositioning[2]Knight Frank, “KSA Logistics Market Overview H1 2025,” KNIGHTFRANK.COM. Warehouse occupancy in Riyadh hit 98% in H1 2025, and rents climbed 16% year-on-year, prompting sovereign sponsors to crystallize gains through listed units. A compulsory 90% income distribution aligns these vehicles with pension and insurance liabilities, providing a predictable cash flow. Domestic redeployment also hedges against Western regulatory scrutiny of Gulf capital, reducing ex-territorial risk. Collectively, these factors reinforce sustained inflows into the GCC REIT market.

Eased Foreign-Ownership Limits in Saudi Arabia and UAE

Regulatory liberalization has carved out attractive channels for external investors. Saudi Arabia now levies a 10% transaction fee on foreigners buying property directly but exempts acquisitions via listed trusts, steering overseas capital into the GCC REIT market. Parallel reforms in Dubai permit leverage up to 50% of gross asset value, enhancing return potential without breaching prudential norms. These measures converge as global allocators seek yield alternatives to softened European offices, positioning Gulf trusts as a compelling blend of growth and dividend income. Early evidence shows passive fund-tracker money increasing allocation weightings after the rule change.

Launch of REIT-Focused Indices on Tadawul and DFM Driving Passive Inflows

The 2024 introduction of dedicated indices supplied the benchmark scaffolding needed by passive asset managers. Index inclusion triggers automatic buying from exchange-traded funds, creating a recurring bid beneath the GCC REIT market. Liquidity screens still exclude the smallest vehicles, but larger names meet minimum turnover, improving price discovery. Emirates REIT’s 81% occupancy and 49.4% loan-to-value ratio satisfied index committees, though funds-from-operations dropped 40% during Q1 2024 as higher rates bit[3]Emirates REIT, “Q1 2024 Financial Results,” EMIRATESREIT.COM. The Capital Market Authority’s 30% free-float rule, if strictly enforced, would expand the investable universe for future tracker products.

Accelerated Government Privatization of Public Real-Estate Portfolios

Monetizing state-owned real estate through REITs helps governments unlock capital for infrastructure without issuing debt. Saudi Arabia’s National Center for Privatization earmarked over 100 properties for conversion, ranging from ministry complexes to service buildings. Kuwait’s KFH Capital REIT demonstrated market receptivity by distributing monthly income on a 90% payout schedule. Qatar followed with a harmonized listing regime permitting borrowings up to 50% of gross asset value. These frameworks echo Singapore’s state-linked sponsor model, though Gulf issuers still face scrutiny over valuation transparency.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising benchmark rates widening valuation yield gaps | -1.1% | GCC-wide; pronounced in UAE, Saudi Arabia | Medium term (2–4 years) |

| Thin free-float and low daily liquidity of most GCC REITs | -0.9% | GCC-wide; acute in Kuwait, Bahrain, Oman | Short term (≤ 2 years) |

| High inter-emirate and cross-border transaction costs limiting diversification | -0.7% | GCC-wide | Long term (≥ 4 years) |

| NAV uncertainty from IFRS-16 lease-accounting adoption | -0.6% | Saudi Arabia, UAE, Qatar | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Thin Free-Float and Low Daily Liquidity of Most GCC REITs

Many vehicles still have founding stakes exceeding 60%, keeping daily turnover under USD 2 million and inflating bid-ask spreads. Illiquidity discourages large institutions that need exit pathways, forcing block trades off-exchange and dulling price signals. Kuwait’s retail-oriented fund trades sporadically despite a solid dividend track record, revealing the structural hurdle in smaller markets. Absence of mandatory market-making exacerbates the issue during stress events. Until older trusts widen public floats, passive inflows into the GCC REIT market will remain concentrated in a few names.

Rising Benchmark Rates Widening Valuation Yield Gaps

Regional policy rates shadow Unites States Federal Reserve hikes, raising the risk-free hurdle and compressing REIT premiums. Empirical research shows a 100 bp rate jump correlates with double-digit total-return erosion for Saudi trusts, well above equity betas. Emirates REIT recorded a 3.3% quarter-on-quarter rise in finance costs in Q1 2024, slicing distributable income by 40% even with 81% occupancy. Limited swap markets and Sharia constraints curb hedging capacity, leaving earnings more sensitive to monetary tightening.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sector of Exposure: Data Centres Outpace Legacy Office Holdings

Office assets captured 38.5% of GCC REIT market share in 2025, reflecting legacy holdings in Dubai’s Business Bay and Riyadh’s King Abdullah Financial District. Yet data-center portfolios are forecast to register a 9.11% CAGR through 2031, the quickest pace in the GCC REIT market. Knight Frank logged 98% warehouse occupancy in Riyadh alongside 16% rent growth during H1 2025, igniting sponsor interest in logistics conversions. Super-regional malls remain 95% let but are remixing tenants toward entertainment, driving 12-15% annual rent hikes in prime Dubai locations. Residential trusts are embryonic; Dubai’s USD 5.89 billion vehicle launched in 2025 signals a pivot to multifamily securitization. Healthcare and student-housing assets represent untapped lanes as privatization gathers pace.

The GCC REIT market size for office holdings delivered a stable yield in 2025, but yield compression is likely as refinancing costs climb. Conversely, the GCC REIT market size tied to data-center facilities enjoys structured escalators aligned with power-cost pass-throughs, buffering margins. Diversified funds use hospitality and retail to cushion swings, yet specialty vehicles often trade at premium valuations due to scarcity. Investor surveys confirm growing preference for single-theme strategies that can articulate clear operational KPIs such as megawatt utilization or cold-storage throughput.

By Market Capitalization: Small-Cap Vehicles Capture Niche Mandates

Mid-cap trusts controlled 45.33% of the GCC REIT market capitalization in 2025. Still, small-cap vehicles are slated to grow 10.2% annually as they carve space in digital-infrastructure and healthcare corridors. GFH Manrre REIT’s 112,000-square-foot chemical warehouse purchase typifies the targeted approach that draws premium rents and reduces rollover risk. Large-caps, often seeded by sovereigns, access cheaper debt but may under-yield because of perceived safety.

For small-cap sponsors, Parallel-Market listings permit higher leverage, sometimes 100% loan-to-value, allowing amplified equity returns, though at the expense of tighter governance. The GCC REIT market size tilted to mid-caps provides an equilibrium of liquidity and specialization. Retail investors favor mid-caps for monthly income streams, as shown by the KD 23.6 million raise of Kuwait’s fund. Meanwhile, large-caps wrestle with redemption spikes during rate shocks, evidenced when Emirates REIT’s funding costs rising sharply in early 2024. Cross-listing discussions are underway to broaden the investor pool, but currency and regulatory arbitrage remain challenges.

Geography Analysis

Saudi Arabia generated 61.22% of the GCC REIT market value in 2025, fortified by a 90% distribution and 50% leverage cap that cultivates sustainable payouts. The 2026 non-Saudi ownership law imposes a 10% fee on direct property but spares listed units, channeling cross-border money into Tadawul-listed trusts and lifting turnover. Riyadh logistics assets remain undersupplied, keeping occupancy near 98% while rents climb at mid-teens clips.

The United Arab Emirates hosts the most liquid secondary market. Dubai’s USD 5.89 billion residential REIT debut in 2025 set a record for single-vehicle size, reflecting confidence in multifamily cash flow. Grade-A office occupancy reached 95% with rents averaging USD 52 per square foot, up 22% year-on-year. Abu Dhabi’s KEZAD logistics hub funnels stabilized inventory into pipeline assets, diversifying tenant exposure.

Qatar streamlined its listing protocol in 2025, enabling 50% borrowing and requiring 80% income distribution. Pension funds value these safeguards, though the market remains smaller in absolute terms. Kuwait, Bahrain, and Oman each maintain distinct rulebooks; Oman’s projected 8.78% CAGR through 2031 stems from fee waivers tied to its Capital Markets Incentives Program. Limited secondary liquidity and fragmented costs, however, impede cross-listing strategies, keeping many trusts domestically concentrated.

Competitive Landscape

The field shows moderate concentration: the top five funds manage about half of the assets, creating a mid-tier where niche mandates flourish. Sovereign-backed managers leverage lower borrowing costs and faster regulatory clearances, while independent sponsors compete on specialized asset themes and agile deal sourcing. Diversified players use blended portfolios to steady distributions; sector-specific rivals chase higher yield by focusing on data centers, logistics, or soon-to-emerge healthcare facilities.

Technology use differentiates top performers. Leading managers deploy Internet-of-Things sensors for predictive maintenance, slashing operating costs and boosting ESG scores, which in turn feed into favorable index ratings. Smaller trusts often rely on manual processes, raising cap-ex exposure and reducing transparency. Compliance requirements, annual independent valuations, and quarterly financials raise overhead but elevate governance standards across the GCC REIT market.

Strategic activity intensified in 2025-2026: GFH Manrre REIT expanded its logistics footprint through niche acquisitions, while Emirates REIT refinanced short-term debt into longer tenors to cushion interest-rate risk. Funds linked to sovereigns explored cross-border acquisitions within the GCC REIT market, seeking portfolio diversification without straying beyond currency pegs. Early-stage blockchain tokenization pilots in Dubai hint at fractional ownership models, though custodial and settlement frameworks are still nascent under the Virtual Assets Regulatory Authority.

GCC REIT Industry Leaders

Jadwa REIT Saudi Fund

Emirates REIT (CEIC)

ENBD REIT

Musharaka REIT

Sedco Capital REIT

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: GFH Manrre REIT bought a temperature-controlled chemical warehouse in JAFZA, accelerating its niche logistics strategy.

- January 2026: Saudi Arabia enforced the non-Saudi ownership law, imposing a 10% fee on direct foreign property deals but exempting listed REITs, effectively diverting offshore capital into the GCC REIT market.

- May 2025: Wasl Asset Management Group announced the IPO of Dubai Residential REIT, a USD 5.89 billion vehicle that introduced large-scale multifamily exposure to the GCC REIT market.

- May 2025: Saudi Arabia’s Capital Market Authority issued enhanced REIT regulations mandating 90% income distribution, capping leverage at 50%, and imposing quarterly reporting.

GCC REIT Market Report Scope

By Sector of Exposure

| Retail |

| Industrial & Logistics |

| Office |

| Residential |

| Diversified |

| Data Centres |

| Healthcare |

| Other Sectors |

By Market Capitalisation

| Large-Cap |

| Mid-Cap |

| Small-Cap |

By Geography

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Kuwait |

| Bahrain |

| Oman |

| By Sector of Exposure | Retail |

| Industrial & Logistics | |

| Office | |

| Residential | |

| Diversified | |

| Data Centres | |

| Healthcare | |

| Other Sectors | |

| By Market Capitalisation | Large-Cap |

| Mid-Cap | |

| Small-Cap | |

| By Geography | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Bahrain | |

| Oman |

Key Questions Answered in the Report

How large is the GCC REIT market today and where is it headed?

The GCC REIT market size stands at USD 18.64 billion in 2026 and is forecast to reach USD 26.13 billion by 2031 at an 8.01% CAGR.

Which property sector is growing the fastest within GCC REIT portfolios?

Data-center assets are the fastest-growing segment, projected to expand at a 9.11% CAGR through 2031 as hyperscaler demand rises.

What recent policy change most affects foreign investors?

Saudi Arabia’s 2026 rule levies a 10% fee on direct property purchases by foreigners but exempts listed REITs, channeling offshore capital into exchange-traded trusts.

Why are sovereign wealth funds increasing stakes in local REITs?

Gulf sovereigns are reallocating capital toward domestic income streams to support diversification agendas and generate predictable distributions aligned with pension liabilities.

How does rising interest cost impact GCC REIT performance?

Higher benchmark rates widen valuation yield gaps and elevate finance charges, which can compress funds-from-operations unless debt is hedged or repriced at longer tenors.

Page last updated on: