Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

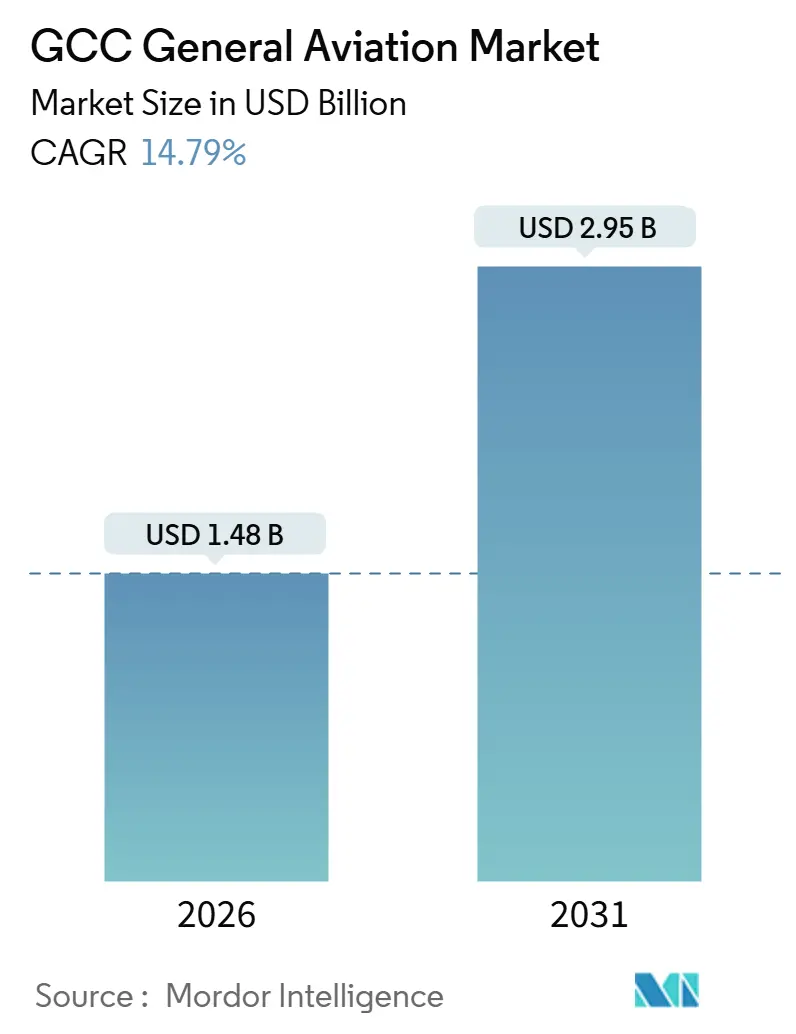

| Base Year Market Size (2025) | USD 1.27 Billion |

| Market Size (2026) | USD 1.48 Billion |

| Market Size (2031) | USD 2.95 Billion |

| Growth Rate (2026 - 2031) | 14.79% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC General Aviation Market Analysis by Mordor Intelligence

The GCC general aviation market is expected to grow from USD 1.24 billion in 2025 to USD 1.48 billion in 2026, and is forecast to reach USD 2.95 billion by 2031, at a 14.79% CAGR over 2026-2031. Infrastructure megaprojects such as Dubai’s Al Maktoum International expansion, coupled with sovereign wealth fund capital, have upgraded runways, aprons, and fixed base operator (FBO) facilities across the UAE, Saudi Arabia, Qatar, Oman, Kuwait, and Bahrain. Regulatory liberalization, including Saudi Arabia’s decision to allow foreign charter operators to operate domestic legs, erodes legacy barriers and fosters cross-border charter demand. The region’s ultra-high-net-worth individual (UNHWI) population continues to rise; the UAE registered a net inflow of 6,700 millionaires by the end of 2024, accelerating the uptake of large-cabin, ultra-long-range jets. Finally, early adoption of electric vertical take-off and landing (eVTOL) solutions, backed by multibillion-dollar purchase commitments, positions the GCC as a proving ground for advanced air mobility.

Key Report Takeaways

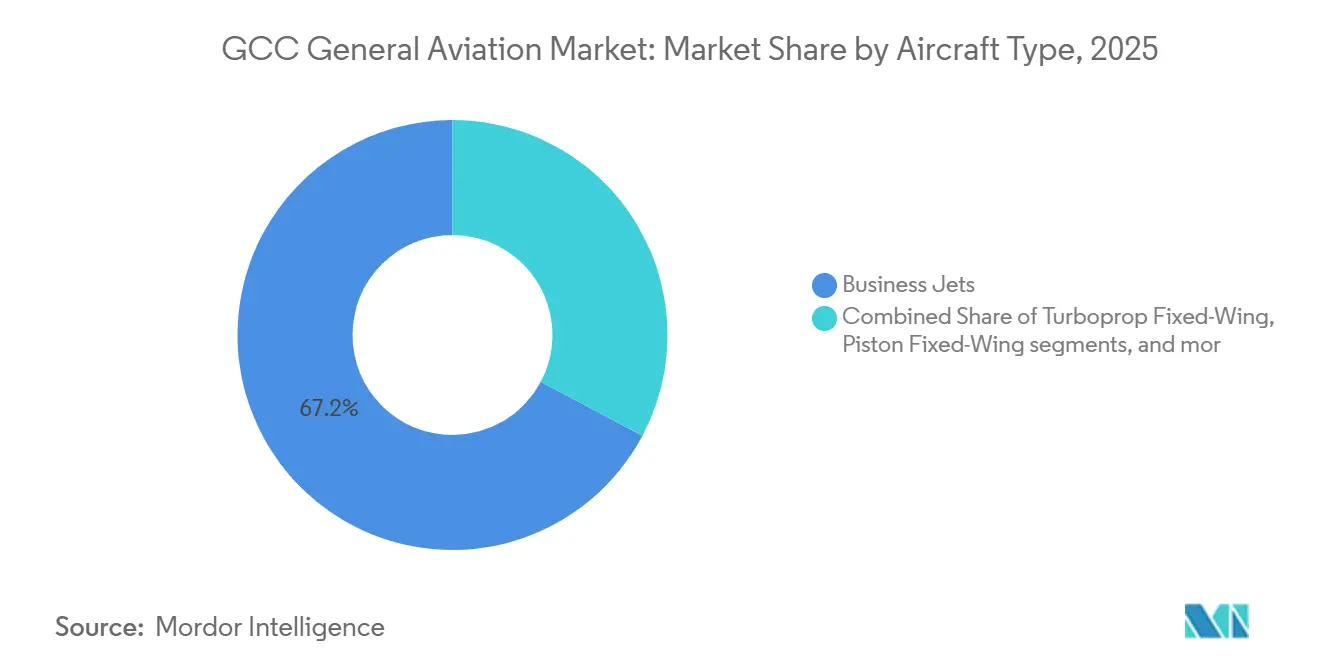

- By aircraft type, business jets led the GCC general aviation market, accounting for 67.24% of the market share in 2025. Meanwhile, eVTOL platforms are projected to expand at a 17.21% CAGR through 2031.

- By propulsion, conventional piston and turbine powerplants accounted for 87.65% of the GCC general aviation market size in 2025; all-electric systems are forecast to grow at 18.64% CAGR through 2031.

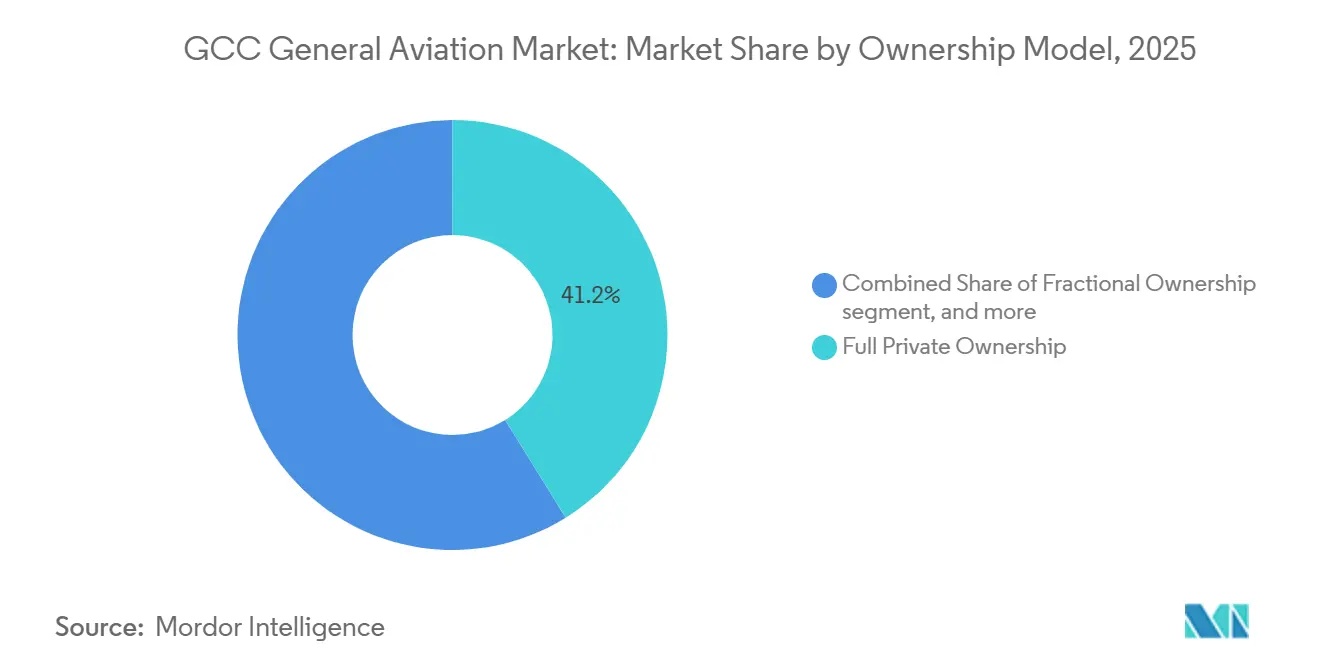

- By ownership model, full private ownership held a 41.16% share of the GCC general aviation market in 2025, while charter and air-taxi activity is forecast to grow at a 15.45% CAGR through 2031.

- By end-user, business and corporate transport accounted for 48.78% of the GCC general aviation market size in 2025; emergency medical services are projected to grow at a 15.82% CAGR through 2031.

- By geography, the UAE captured a 38.01% share of the GCC general aviation market in 2025, while Saudi Arabia is projected to post the fastest growth, with a 16.27% CAGR, between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

GCC General Aviation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-led airport and general aviation infrastructure expansion | +4.1% | Saudi Arabia, UAE, Oman | Long term (≥ 4 years) |

| Rising demand for large-cabin and ultra-long-range business jets | +3.2% | UAE, Saudi Arabia, Qatar | Medium term (2-4 years) |

| Dubai’s emergence as a regional general aviation hub | +2.8% | UAE, spillover to Qatar and Bahrain | Short term (≤ 2 years) |

| Expansion of dedicated general aviation airports and terminals | +2.3% | Saudi Arabia, UAE | Long term (≥ 4 years) |

| Liberalization of general aviation regulations and FBO licensing | +1.9% | Saudi Arabia, UAE, Kuwait | Medium term (2-4 years) |

| Emerging eVTOL and advanced air mobility development road maps | +1.6% | UAE, Saudi Arabia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Large-Cabin and Ultra-Long-Range Business Jets

Corporate buyers and UNHWIs prefer aircraft capable of flying nonstop from Dubai or Riyadh to London, New York, or Singapore. Qatar Executive already operates six Gulfstream G700s and plans to take four more by early 2026. Gulfstream lists more than 120 jets home-based in the Middle East, and 18- to 24-month lead times point to sustained backlog pressure.[1]Gulfstream Aerospace, “Middle East Market Presence and Delivery Timelines,” gulfstream.com RoyalJet ordered three Airbus ACJ320neos and holds six options, widening the premium narrowbody niche. Hub-and-spoke geography, long stage lengths, and VIP cabin expectations render super-mid-size aircraft less relevant, encouraging operators such as NasJet to double down on the G650/G700 family.

Government-Led Airport and General Aviation Infrastructure Expansion

Saudi Arabia aims to generate USD 2 billion in general aviation activity by 2030 and is budgeting six dedicated general aviation airports. Dubai’s Al Maktoum project triples FBO capacity and reserves segregated ramp space for business jets. Jetex opened its first FBO at Red Sea International in 2024, marking the beginning of a nationwide rollout of five new aviation gateways under Vision 2030.[2]Jetex, “Red Sea International Airport FBO Opening,” jetex.com Falcon Aviation Services has committed USD 100 million for a 13,705-square-meter MRO hangar at Al Maktoum. Oman’s civil aviation regulator has reduced the processing time for foreign aircraft permits from 14 days to 72 hours, diverting transient traffic away from Dubai and Doha.

Dubai’s Emergence as a Regional General Aviation Hub

Dubai South logged 17,891 movements in 2024, representing a 7% year-over-year increase, and aims to reach 18,000 by the end of 2026. ExecuJet opened a flagship FBO at the airport in December 2024 and secured European Aviation Safety Agency approval for Global 7500 maintenance in January 2025. DC Aviation Al-Futtaim expanded its managed and charter portfolio to nine aircraft and joined the Air Elite network in October 2025, gaining reciprocal handling at more than 240 locations. The Dubai Civil Aviation Authority typically issues general aviation permits within 48 hours, in contrast to the week-long approvals often required elsewhere. Jetex and Wright Electric are rolling out electric aircraft charging at over 30 FBOs, starting in Dubai, with the goal of targeting hybrid-electric business jet service by 2028.

Liberalization of General Aviation Regulations and FBO Licensing

Saudi Arabia opened its domestic sectors to foreign charter operators in May 2025; Vista Global immediately gained approval and now serves the Riyadh-Jeddah and Riyadh-Dammam routes. The UAE’s 2024 CAR-66 rollout recognizes European licenses, easing inflows of qualified engineers. Kuwait’s Directorate General of Civil Aviation trimmed FBO-license processing to 90 days and cut capital requirements by 40%, attracting three new applicants in early 2025. Bahrain’s tiered permit system, launched in 2024, lowered entry costs for operators with small fleets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of qualified pilots and maintenance personnel | -2.1% | GCC-wide, acute in Saudi Arabia and UAE | Short term (≤ 2 years) |

| Airspace congestion and slot constraints at major airports | -1.4% | UAE (Dubai, Abu Dhabi), Saudi Arabia (Riyadh), Qatar (Doha) | Short term (≤ 2 years) |

| High operating and ownership costs | -1.2% | GCC-wide | Medium term (2-4 years) |

| Supply chain delays affecting aircraft deliveries and spare parts | -0.9% | GCC-wide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Qualified Pilots and Maintenance Personnel

The Boeing Company projects that the Middle East will need 46,000 pilots and 62,000 technicians by 2043, yet regional flight academies graduate only about 750 professionals annually.[3]Boeing, “Pilot and Technician Forecast for Middle East 2024-2043,” boeing.com Emirates alone plans to hire 5,000 pilots over the next five years, prompting business-jet operators to offer high salaries. Horizon International Flight Academy produces 250 cadets annually, while the Saudi Aviation Club trains approximately 500 students, which falls short of the 1,200 pilots required each year. MRO shops face similar gaps; foreign engineers still wait up to 12 months for work visas despite CAR-66 reforms. Wet-leasing with crews from Europe and North America plugs short-term holes but raises hourly costs by 20%–30% for Gulf operators.

Airspace Congestion and Slot Constraints at Major Airports

Dubai International handled 92.30 million passengers in 2024, retaining top global status and leaving minimal peak-hour slots for general aviation. Dubai South picked up the overflow, registering a 15% flight-volume surge in H1-2025 versus H1-2024. Required Navigation Performance corridors added in 2024 boost capacity by 15%, yet 40% of turboprop and piston aircraft lack compliant avionics. Qatar’s Hamad International still enforces two-hour buffers on executive movements during major event rushes, forcing Qatar Executive to pre-position jets elsewhere. Saudi Arabia’s dedicated general aviation airport program will alleviate pressure, but the first three sites are not expected to open before 2028.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Aircraft Type: Business Jets Anchor Market, eVTOLs Set the Pace

The business jets segment accounted for 67.24% of the GCC general aviation market share in 2025, driven by nonstop demand for routes to London, New York, and Singapore. Qatar Executive's six-strong G700 fleet exemplifies the premium-cabin tilt, while RoyalJet's ACJ320neo order signals rising interest in narrowbody VIP aircraft. Turboprops serve Saudi Aramco's remote-field shuttles, and piston aircraft remain entrenched in flight schools, yet both niches account for less than 15% of flying hours.

The eVTOL segment is expected to grow at the highest CAGR of 17.21% through 2031, following Joby Aviation's delivery of its first unit in June 2025 and The Helicopter Company's preparation of a 2025 request for proposals covering up to 200 aircraft. Rotorcraft continue to underpin offshore energy, policing, and emergency medical services, with The Helicopter Company operating 58 helicopters as of 2025 and planning to have 30 dedicated EMS birds by the end of 2026.

By Propulsion Type: Conventional Dominance Faces Electric Disruption

Conventional piston/turbine engines accounted for 87.65% of the GCC general aviation market in 2025; however, all-electric systems are expected to expand at an 18.64% CAGR through 2031. Wright Electric and Jetex are installing 30 fast-charging stations to cover 540 km of hybrid-jet legs by 2028. Hydrogen-electric initiatives, such as JEKTA’s PHA-ZE 100 and Beyond Aero’s BYA-1, aim for 2030 entries, but fueling infrastructure remains nascent beyond the Dubai South pilots.[4]JEKTA, “PHA-ZE 100 Hydrogen-Electric Aircraft Development,” jekta.ch

Hybrid-electric turboprops, illustrated by Daher’s EcoPulse demonstrator, offer transitional efficiency while retaining conventional range, making them attractive for Saudi Arabia’s oil-field hops. Rolls-Royce Pearl 700 engines continue to dominate the longest-range missions, and turbine powerplants will likely preserve the bulk of premium-cabin segments through at least 2035.

By Ownership Model: Charter Growth Challenges Full Ownership

Full private ownership represented 41.16% of 2025 activity; however, charter and air-taxi operators are on track for a 15.45% CAGR, as Gulf corporations prefer asset-light access to lift. Vista Global secured USD 1.3 billion in April 2025 to scale, and its domestic charter permissions in Saudi Arabia expand the addressable pool by 47% of local departures.

Managed fleets also expand. For instance, DC Aviation Al-Futtaim added eight diverse jets between 2023 and 2025 and joined Air Elite to guarantee service at 240 airports. Government mission fleets, notably The Helicopter Company’s EMS and security assets, follow multi-year contracts that stabilize demand regardless of macro cycles.

By End-User Application: Corporate Transport Leads, Medical Services Accelerate

Business/corporate transport accounted for 48.78% of flying hours in 2025, as large Gulf conglomerates maintained robust travel budgets despite oil price fluctuations. Emergency medical services are expected to log a 15.82% CAGR through 2031. The Saudi Red Crescent deal includes 28 helicopters and up to six fixed-wing air ambulances over four years, reducing Riyadh-Tabuk transfer times to 90 minutes.

Private leisure flying still lags due to a limited number of general aviation airports and high operating costs, yet Oman’s 72-hour permit timeline now encourages more foreign-registered arrivals. Special-mission tasks, border patrol, law enforcement, and offshore surveillance remain niche but strategic, involving King Air 350s, Pilatus PC-12s, and Leonardo AW139 helicopters.

Geography Analysis

The UAE commanded 38.01% of the GCC general aviation market share in 2025, driven by increasing departures from Dubai and the expansion of Al Maktoum, which is expected to triple FBO throughput. ExecuJet’s luxury FBO and EASA Global 7500 approval, plus Falcon Aviation’s USD 100 million MRO build, deepen the services ecosystem. Abu Dhabi, meanwhile, is positioning itself as the GCC’s eVTOL test bed through its Archer Aviation partnership, with trial flights set for 2026. Wright Electric’s regional charging network initiative aligns with projections indicating that 35% of intra-GCC sectors fall within a 540-km electric-range envelope.

Saudi Arabia is projected to post a 16.27% CAGR, the fastest in the bloc, as Vision 2030 mandates six GA-only airports and eliminates domestic-charter protectionism. Jetex’s Red Sea FBO and Joby Aviation’s 200-aircraft framework deal exemplify the momentum of foreign investment. The Helicopter Company plans 30 EMS rotorcraft by 2026, while Mukamalah Aviation and Archer Aviation eye urban-air-mobility corridors linking Riyadh’s new downtown to King Khalid International.

Oman, Kuwait, and Bahrain together hold under a 20% market share but benefit from spillover traffic when Dubai or Doha face curfews or slot caps. Oman’s fast-track permits, Kuwait’s 90-day FBO licensing, and Bahrain’s light-permit tier have already lured a trio of start-ups focusing on piston and turboprop niches.

Competitive Landscape

The market remains moderately fragmented, with no operator exceeding a 20% share, yet consolidation is accelerating. Original-equipment manufacturers (OEMs) wield pricing power amid long backlogs; Gulfstream’s G700 and Bombardier’s Global 7500 waitlists stretch beyond 24 months, obliging operators to retain aging fleets and driving up MRO volumes.

DC Aviation Al-Futtaim broadened its fleet mix and joined the Air Elite network, ensuring brand-consistent ground handling across 240 airports and appealing to enterprise clients with multi-leg itineraries. The Helicopter Company’s framework agreements covering 250 Airbus and Leonardo S.p.A. helicopters, plus anticipated eVTOL orders, position it to dominate EMS and special-mission verticals as oil majors outsource flight operations.

Vista Global manages 270 owned aircraft and coordinates 2,100 alliance jets; its USD 1.3 billion financing, announced in April 2025, underwrites deeper Gulf penetration and domestic Saudi flying, a first for a foreign brand. ExecuJet’s January 2025 EASA nod for Global 7500 maintenance distinguishes its Dubai South complex in a region that craves heavy-jet MRO capacity. Smaller incumbents, such as NasJet, feel a margin squeeze after relinquishing Dassault operations and losing exclusivity on domestic Saudi routes. First movers in electric charging infrastructure, such as Jetex and Wright Electric, may secure an early share of the emerging hybrid-electric maintenance market.

GCC General Aviation Industry Leaders

Textron Inc.

Embraer S.A.

Gulfstream Aerospace Corporation (General Dynamics Corporation)

Leonardo S.p.A.

Dassault Aviation SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Intercontinental Aviation Enterprise FZ-LLC signed a Memorandum of Understanding (MoU) with Diamond Aircraft Industries GmbH to procure 10 Diamond training aircraft, aiming to enhance pilot training capacity and operational capabilities across the UAE, aligning with its global expansion objectives.

- January 2025: Qatar Executive, the private jet charter division of Qatar Airways Group, expanded its fleet with two additional Gulfstream G700 aircraft, increasing the total to six. Four more G700s are planned for delivery by 2025 and early 2026, further enhancing QE’s capacity to provide luxury aviation services.

GCC General Aviation Market Report Scope

General aviation covers all non-commercial civil aviation activities, excluding scheduled airline services and military operations. This sector spans private flying, business aviation, flight training, and air charter services. The aircraft ranged from small piston planes to advanced turboprops, rotorcraft, business jets, and advanced air mobility vehicles. General Aviation is pivotal in supporting sectors such as business, tourism, and medical services. It provides flexible, tailored aviation solutions while strictly adhering to safety regulations set by local and international authorities.

The GCC general aviation market is segmented by aircraft type, propulsion type, ownership model, end-user application, and geography. By aircraft type, the market is segmented into business jets, turboprop fixed-wing aircraft, piston fixed-wing aircraft, rotorcraft, and advanced air mobility eVTOLs. By propulsion type, the market is segmented into conventional piston/turbine, hybrid-electric, and all-electric. By ownership model, the market is segmented into full private ownership, fractional ownership, charter/air-taxi operators, training and academic institutions, and government and special-mission operators. By end-user application, the market is segmented into business/corporate transport, personal and leisure flying, special mission (ISR, surveillance, law enforcement), emergency medical/air ambulance, and pilot training. The report also covers the GCC general aviation market size and forecasts for six regional countries. For each segment, the market size is provided in terms of value (USD).

By Aircraft Type

| Business Jets | Large Jet |

| Mid-Size Jet | |

| Light/Very-Light Jet | |

| Turboprop Fixed-Wing Aircraft | |

| Piston Fixed-Wing Aircraft | |

| Rotorcraft | |

| Advanced Air Mobility eVTOLs |

By Propulsion Type

| Conventional Piston/Turbine |

| Hybrid-Electric |

| All-Electric |

By Ownership Model

| Full Private Ownership |

| Fractional Ownership |

| Charter/Air-Taxi Operators |

| Training and Academic Institutions |

| Government and Special Mission Operators |

By End-User Application

| Business/Corporate Transport |

| Personal and Leisure Flying |

| Special Mission (ISR, Surveillance, Law Enforcement) |

| Emergency Medical/Air-Ambulance |

| Pilot Training |

By Geography

| United Arab Emirates |

| Saudi Arabia |

| Qatar |

| Oman |

| Kuwait |

| Bahrain |

| By Aircraft Type | Business Jets | Large Jet |

| Mid-Size Jet | ||

| Light/Very-Light Jet | ||

| Turboprop Fixed-Wing Aircraft | ||

| Piston Fixed-Wing Aircraft | ||

| Rotorcraft | ||

| Advanced Air Mobility eVTOLs | ||

| By Propulsion Type | Conventional Piston/Turbine | |

| Hybrid-Electric | ||

| All-Electric | ||

| By Ownership Model | Full Private Ownership | |

| Fractional Ownership | ||

| Charter/Air-Taxi Operators | ||

| Training and Academic Institutions | ||

| Government and Special Mission Operators | ||

| By End-User Application | Business/Corporate Transport | |

| Personal and Leisure Flying | ||

| Special Mission (ISR, Surveillance, Law Enforcement) | ||

| Emergency Medical/Air-Ambulance | ||

| Pilot Training | ||

| By Geography | United Arab Emirates | |

| Saudi Arabia | ||

| Qatar | ||

| Oman | ||

| Kuwait | ||

| Bahrain |

Key Questions Answered in the Report

How fast is market demand expanding across the Gulf states?

The GCC general aviation market is growing at a 14.79% CAGR, doubling from USD 1.48 billion in 2026 to USD 2.95 billion by 2031.

Which country leads regional business-jet departures?

The UAE holds 38.01% market share and logged the highest share of business-jet take-offs in 2025, the highest in the bloc.

What is fueling the surge in large-cabin aircraft acquisitions?

Growing UNHWI populations, long intercontinental stage lengths, and FBO infrastructure upgrades favor Gulfstream G700, ACJ320neo, and similar jets.

How are Gulf regulators addressing pilot shortages?

Saudi Arabia and the UAE signed training-capacity pacts, adopted CAR-66 licensing convergence, and partnered with OEMs to scale academies, yet demand still outstrips supply by more than 20% annually.

Page last updated on: