GCC Algae Biofuel Prospects Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

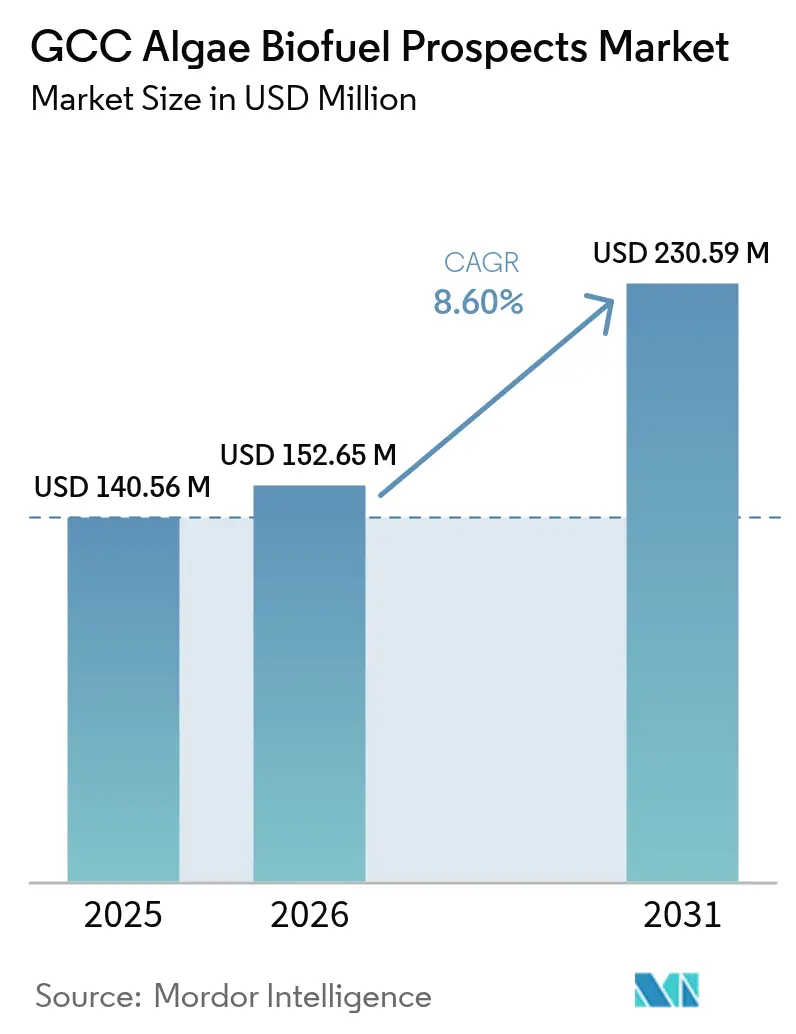

| Base Year Market Size (2025) | USD 140.56 Million |

| Market Size (2026) | USD 152.65 Million |

| Market Size (2031) | USD 230.59 Million |

| Growth Rate (2026 - 2031) | 8.60% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC Algae Biofuel Prospects Market Analysis by Mordor Intelligence

GCC Algae Biofuel Prospects Market size in 2026 is estimated at USD 152.65 million, growing from 2025 value of USD 140.56 million with 2031 projections showing USD 230.59 million, growing at 8.6% CAGR over 2026-2031.

Expansion is driven by intensified carbon-pricing schemes, mandated sustainable aviation fuel (SAF) blending rules, and the availability of abundant seawater and industrial CO₂ streams, which reduce feedstock costs. International oil majors now leverage existing petrochemical logistics to reduce capital needs, while seawater-based cultivation lowers operating expenses by 40–60% compared to freshwater systems. Vertical integration is accelerating as producers link upstream algae cultivation with downstream refining to secure higher margins. Competitive tension also reflects the rapid rise of ultra-low-cost green hydrogen, which pressures algae fuel economics but simultaneously pushes airlines and militaries to lock in drop-in solutions that meet decarbonization deadlines.

Key Report Takeaways

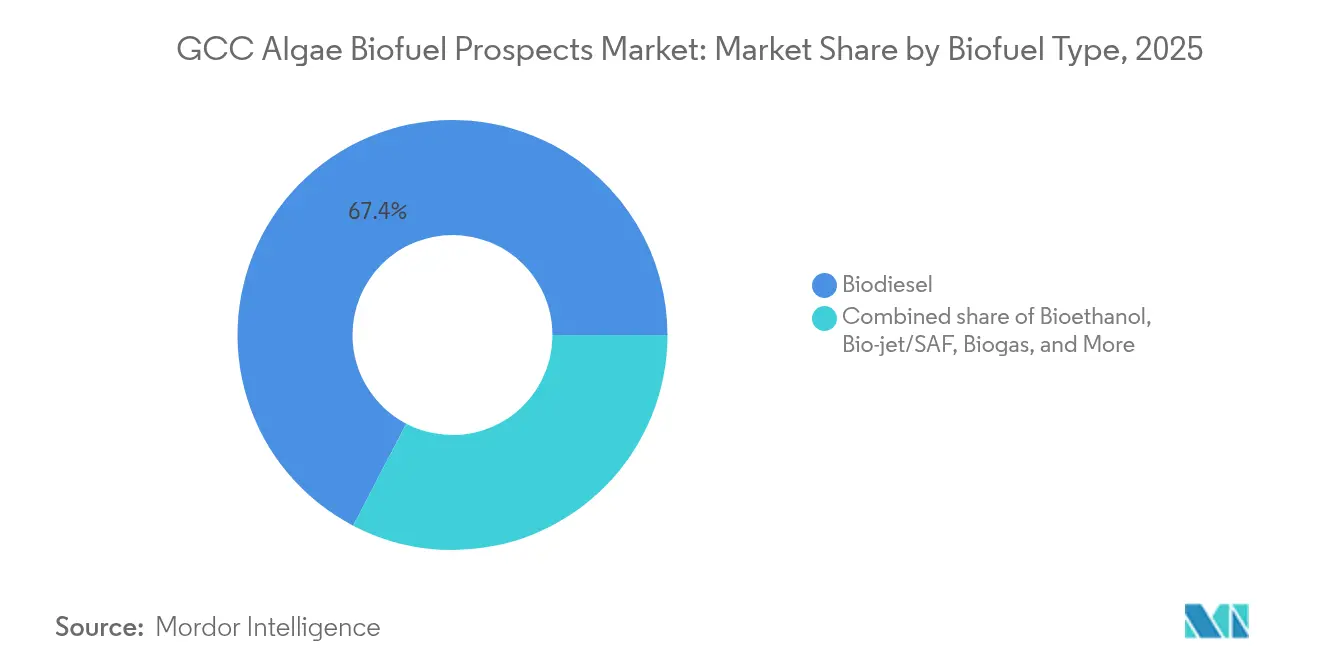

- By biofuel type, biodiesel led with 67.35% revenue share in 2025; bio-jet fuel is projected to grow at a 16.5% CAGR to 2031.

- By feedstock species, microalgae captured a 88.60% share in 2025 and are advancing at a 9.96% CAGR through 2031.

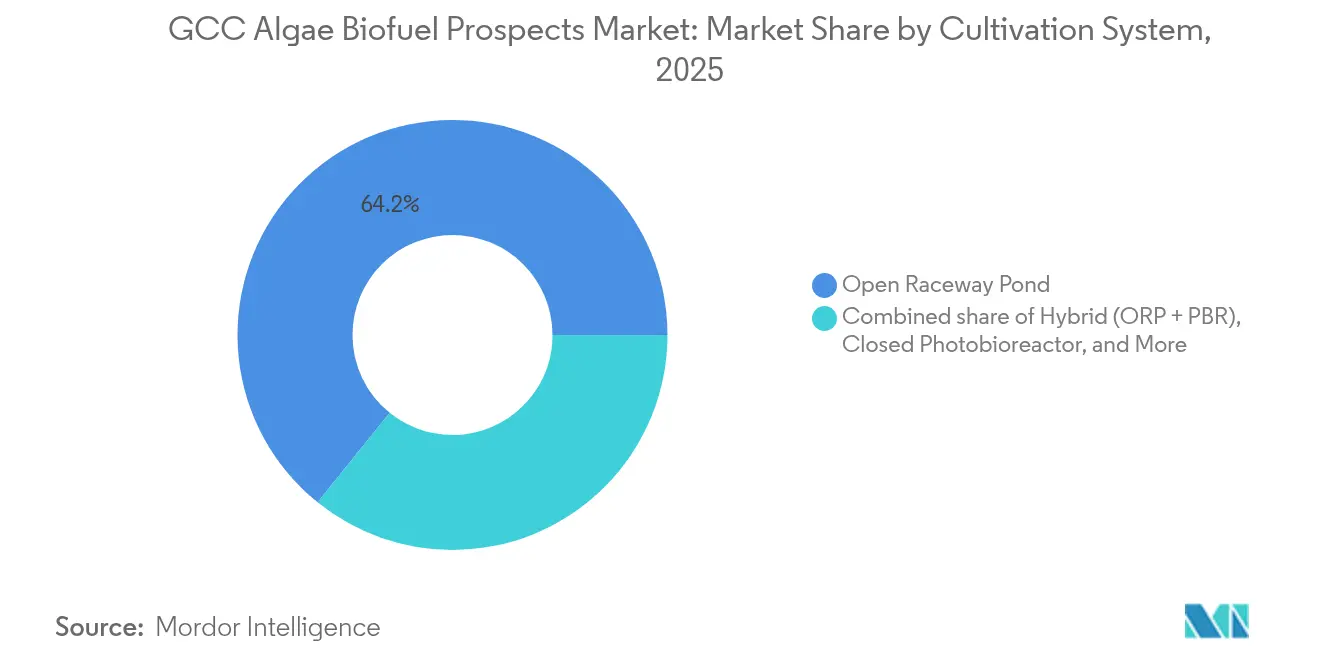

- By cultivation system, open raceway ponds accounted for 64.20% of the GCC algae biofuel market share in 2025, while hybrid systems are projected to expand at an 17.8% CAGR through 2031.

- By end-use application, transportation accounted for a 60.30% share of the GCC algae biofuel market size in 2025; aviation is projected to surge at a 20.4% CAGR through 2031.

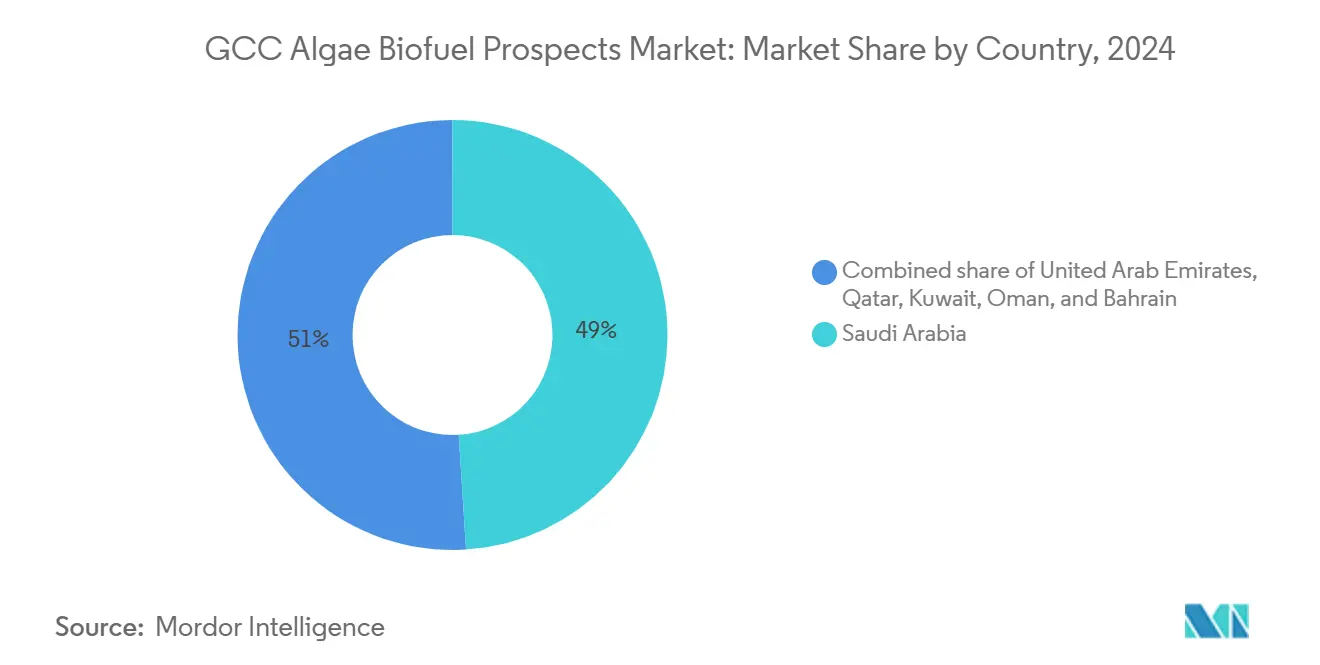

- By country, Saudi Arabia commanded a 48.60% share in 2025, and the UAE records the fastest CAGR at 15.3% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

GCC Algae Biofuel Prospects Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Carbon-pricing pressure on oil-exporting GCC economies | 2.10% | Saudi Arabia, UAE, Qatar core markets | Medium term (2-4 years) |

| Mandated SAF blending targets for national airlines | 1.80% | UAE, Qatar, Saudi Arabia aviation hubs | Short term (≤ 2 years) |

| Seawater-based cultivation cost savings versus freshwater systems | 1.50% | Coastal GCC regions, UAE desalination zones | Long term (≥ 4 years) |

| CO₂-utilisation partnerships with steel & desalination plants | 1.20% | Saudi Arabia industrial corridors, UAE processing zones | Medium term (2-4 years) |

| Military demand for logistics-friendly drop-in fuels | 0.90% | Saudi Arabia, UAE defense sectors | Long term (≥ 4 years) |

| Waste-heat integration from gas-fired power plants | 0.60% | Qatar, Kuwait power generation regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Carbon-pricing pressure on oil-exporting GCC economies

Tightening carbon-pricing frameworks across the Gulf accelerates government diversification into algae-based biofuels, which safeguard export revenues in line with Vision 2030 objectives.[1]Vision 2030, “Vision 2030 Kingdom of Saudi Arabia,” vision2030.gov.sa Saudi Arabia’s Public Investment Fund allocated USD 20 billion to renewable energy in 2024, with a focus on algae platforms that retrofit existing petrochemical sites.[2]Arab News Staff, “PIF Allocates $20bn to Renewable Energy,” Arab News, arabnews.com Using refinery CO₂ as feedstock converts compliance costs into biomass value, granting algae producers long-term offtake contracts from emitting industries. The policy mix, therefore, anchors predictable demand, mitigates stranded asset risk, and reinforces the GCC algae biofuel market as a hedge against shrinking fossil fuel margins.

Mandated SAF blending targets for national airlines

Emirates, Qatar Airways, and Saudia must meet 5-10% SAF mandates by 2030, guaranteeing a captive aviation customer base. Emirates already holds a decade-long SAF supply agreement that earmarks 30% local algae content by 2028. Blending rules stabilise revenue for algae refiners, unlock project finance, and encourage rapid scale-up near hub airports. Because the GCC controls critical aviation transit corridors, regional producers can supply foreign carriers that refuel en route, widening the GCC algae biofuel market beyond domestic consumption.

Seawater-based cultivation cost savings versus freshwater systems

Demonstration plants in Abu Dhabi and Fujairah confirm that halophilic microalgae achieve comparable lipid yields to freshwater strains, with 40–60% lower operating costs when using unprocessed seawater. Co-location with desalination plants further drops costs by sharing pumping stations and leveraging brine effluent that matches optimal salinity ranges. The result is a structural feedstock advantage that offsets the energy-intensive harvesting, thereby anchoring the long-term competitiveness of the GCC algae biofuel industry in arid climates.

CO₂-utilisation partnerships with steel & desalination plants

SABIC’s steel operations emit more than 50 million tons of CO₂ annually, and pilot link-ups utilise 10–15% of this stream for algae growth, shrinking capture costs and boosting biomass productivity. ADNOC tests similar integration with desalination units to pair concentrated CO₂, waste heat, and seawater, reinforcing circular-economy credentials. Such symbiosis raises project IRRs and places vertically integrated complexes at the centre of the GCC algae biofuel market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High salinity-tolerant strain IP owned by foreign firms | -1.40% | Regional, technology transfer constraints | Long term (≥ 4 years) |

| Limited local downstream transesterification capacity | -0.80% | Saudi Arabia, UAE processing gaps | Medium term (2-4 years) |

| Scarce venture funding for pre-revenue bio-refineries | -0.60% | GCC startup ecosystem limitations | Short term (≤ 2 years) |

| Competition from ultra-low-cost solar-H2 in GCC | -0.50% | Saudi Arabia, UAE renewable energy zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High salinity-tolerant strain IP owned by foreign firms

Key patents covering halophilic microalgae are controlled by US and European biotech companies such as Algenol Biotech, resulting in expensive licence fees and limited technology transfer.[3]Algenol Biotech, “Salinity-Tolerant Algae Patents,” algenol.comUAE pilot plants have already faced commissioning delays while negotiating access rights, exposing the market to supply-chain risks and slowing indigenous R&D. Local universities are ramping up gene-editing programs, yet commercial strains may take 5–10 years to reach scale, restraining the growth of the GCC algae biofuel market.

Limited local downstream transesterification capacity

Existing GCC biodiesel units are optimised for palm-oil feedstocks, not algae lipids, covering less than 30% of the anticipated 2030 output.[4]ENOC Group, “Biodiesel Operations Overview,” enoc.com Consequently, producers must ship crude algae oil to Asia or Europe, forfeiting value and facing freight exposure. Green-field refineries are planned, but reliance on imported equipment heightens capital expenditure (capex) and scheduling risk.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Biofuel Type: Aviation Fuels Drive Premium Growth

The segment commanded a GCC algae biofuel market size of USD 94.67 million in 2025, with biodiesel holding a 67.35% share thanks to established fleets in road transport. Bio-jet fuel, however, is projected to record a 16.5% CAGR through 2031, spurred by mandatory 5-10% SAF mandates at Gulf hubs. Airlines accept 2-3 times the price of kerosene to meet compliance timelines, shielding producers from commodity price fluctuations and thereby elevating their margins.

Growing SAF demand widens feedstock procurement opportunities while encouraging investments in certification. Bioethanol retains a 15.20% share chiefly through ground-transport blending, and biogas stands at 8.10% because plentiful pipeline gas crowds out methane-rich digestate. Algae-derived hydrogen captures only 4.05% share but attracts R&D dollars as national energy agendas eye export-ready green molecules, indicating an emerging, though longer-dated, diversification path for the GCC algae biofuel market.

By Feedstock Species: Microalgae Dominance Accelerates

Microalgae generated 88.60% of 2025 volume and expanded at a 9.96% CAGR, cementing leadership through superior lipid yields and year-round output. Strains such as Nannochloropsis and Chlorella reach lipid concentrations of 20-30% when cultivated in high-salinity ponds along the Arabian Gulf. The GCC algae biofuel market size for microalgae is forecast to maintain its expansion on the back of ongoing genetic optimisation initiatives.

Macroalgae hold an 11.40% share due to episodic harvest windows and lower oil content; however, brown seaweed trials show promise for integrated biorefinery chemicals. Spirulina farms straddle nutrition markets, offering cross-subsidies that improve early-stage cash flow. Indigenous strain programs aim to cut royalty costs, underpinning long-term autonomy for the GCC algae biofuel industry.

By Cultivation System: Hybrid Systems Capture Efficiency Gains

Open raceway ponds represented 64.20% of the installed capacity in 2025, leveraging their low capital intensity. However, hybrid systems that pair ponds with photobioreactors are growing at an 17.8% CAGR, delivering 40-50% productivity gains in Qatar trials. Closed photobioreactors hold a 20.10% share for pharmaceutical-grade outputs, whereas heterotrophic fermentation lags at 8.05% due to costly sugar substrates.

Hybrid design mitigates contamination risk during early growth phases and then shifts biomass to open ponds for economical scale-up. Waste-heat recovery from nearby power plants stabilises culture temperatures and reduces energy costs, a decisive advantage in the high ambient heat that shapes the GCC algae biofuel market.

By End-Use Application: Aviation Sector Transforms Demand

Transportation commanded a 60.30% share in 2025, driven by diesel blending mandates; however, aviation is the breakout sector with a 20.4% CAGR, as carriers pre-purchase SAF to secure compliance. The GCC algae biofuel market share for aviation is expected to expand rapidly, as Emirates, Qatar Airways, and Saudia collectively consume over 400 million liters of jet fuel annually.

Marine fuels capture a 12.10% share, aided by voluntary emissions cuts among container lines using Gulf ports, while power generation accounts for 8.05% due to the abundance of natural gas. Industrial feedstock accounts for the remaining 7.10%, focusing on surfactants and specialty solvents that fetch premium pricing, thus diversifying revenue streams and cushioning price risk in the GCC algae biofuel market.

Geography Analysis

Saudi Arabia anchors the GCC algae biofuel market with a 48.60% share, owing to its retrofitted refinery assets, vast industrial CO₂ streams, and USD 20 billion in renewable allocations under Vision 2030. Aramco tests indigenous strains at King Abdullah University of Science and Technology, seeking IP sovereignty while utilizing refinery flue gas to reduce feedstock costs. The country’s inland desert tracts also offer inexpensive land leases, facilitating large pond footprints without competing agricultural demand.

The UAE is the fastest-growing geography, expanding at a 15.3% CAGR, underpinned by Masdar’s cross-sector renewable energy ecosystem and Emirates’ long-term SAF contracts. ADNOC pilots desalination-linked cultivation where brine effluent, waste heat, and concentrated CO₂ converge, reinforcing resource circularity. Regulatory fast-track visas and free-zone incentives accelerate foreign biotech participation, positioning Abu Dhabi as a hub for scaling up the GCC algae biofuel market.

Qatar, Kuwait, Oman, and Bahrain collectively hold a 33.40% share. Qatar benefits from LNG-linked carbon capture integration, Kuwait repurposes refinery waste heat for military diesel substitutes, Oman leverages university clusters to incubate hybrid technologies, and Bahrain uses its financial sector to channel Sharia-compliant funding into pilot assets. Together, they provide testing grounds for niche approaches that may later migrate to larger Gulf economies, spreading technical knowledge across the broader GCC algae biofuel market.

Competitive Landscape

The GCC algae biofuel market features moderate fragmentation. Oil majors, such as Saudi Aramco and QatarEnergy, exploit refining synergies to realize economies of scale, whereas biotech specialists, like Seambiotic, concentrate on high-yield strain development. International energy firms TotalEnergies and Shell contribute proprietary cultivation designs and global SAF distribution networks, creating collaborative yet competitive consortia.

Vertical integration is intensifying. Aramco’s USD 500 million R&D fund supports in-house strain libraries and captive refining, while Masdar structures joint ventures that span culture, processing, and offtake, capturing premium margins and insulating against supply disruption. Patent filings for salinity-tolerant genetics surged 40% in 2024, highlighting the strategic value of IP in lowering license fees and raising barriers to entry.

Smaller firms face funding gaps and thus pursue niche strategies—nutraceutical Spirulina co-products or military contracts—that provide early revenue. Some partner with state-owned utilities offering CO₂ streams and waste heat. Consolidation is expected as standalone cultivators seek to scale or exit to vertically integrated players, thereby tightening the market while also accelerating the diffusion of technology across the GCC algae biofuel industry.

GCC Algae Biofuel Prospects Industry Leaders

Saudi Aramco

Masdar (incl. Algae Fuels JV)

TotalEnergies

Shell plc

QatarEnergy

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Saudi Aramco committed USD 500 million for indigenous strain research with King Abdullah University of Science and Technology.

- December 2024: Emirates has signed a 10-year SAF deal with Neste, worth USD 2 billion, stipulating a 30% algae-derived content by 2028.

- November 2024: QatarEnergy and TotalEnergies formed a joint venture in Ras Laffan targeting a 50,000-ton-per-year capacity.

- October 2024: Masdar launched USD 300 million in R&D centres with three global biotech firms in Abu Dhabi.

GCC Algae Biofuel Prospects Market Report Scope

The GCC algae biofuel prospects market report include:

| Biodiesel |

| Bioethanol |

| Bio-jet / SAF |

| Biogas |

| Bio-hydrogen & Others |

| Microalgae (Nannochloropsis, Chlorella, Spirulina, Dunaliella, Others) |

| Macroalgae (Red, Brown, Green) |

| Open Raceway Pond |

| Closed Photobioreactor |

| Hybrid (ORP + PBR) |

| Heterotrophic Fermentation |

| Road Transportation |

| Aviation (SAF) |

| Marine |

| Power Generation and CHP |

| Industrial and Others |

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Kuwait |

| Oman |

| Bahrain |

| By Biofuel Type | Biodiesel |

| Bioethanol | |

| Bio-jet / SAF | |

| Biogas | |

| Bio-hydrogen & Others | |

| By Feedstock Species | Microalgae (Nannochloropsis, Chlorella, Spirulina, Dunaliella, Others) |

| Macroalgae (Red, Brown, Green) | |

| By Cultivation System | Open Raceway Pond |

| Closed Photobioreactor | |

| Hybrid (ORP + PBR) | |

| Heterotrophic Fermentation | |

| By End-Use Application | Road Transportation |

| Aviation (SAF) | |

| Marine | |

| Power Generation and CHP | |

| Industrial and Others | |

| By Country | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Oman | |

| Bahrain |

Key Questions Answered in the Report

What is the current value of the GCC algae biofuel market?

The GCC algae biofuel market size is valued at USD 152.65 million in 2026 and is projected to reach USD 230.59 million by 2031.

Which biofuel type is growing the fastest?

Bio-jet fuel is expanding at a 16.5% CAGR to 2031, driven by mandatory sustainable aviation fuel blending across Gulf airlines.

Why do Gulf producers prefer seawater-based cultivation?

Using raw seawater cuts operating costs 40-60% and aligns with regional water-scarcity constraints, giving Gulf projects a cost advantage over freshwater systems.

Which country leads algae biofuel deployment in the GCC?

Saudi Arabia holds 48.60% market share owing to its integrated refinery infrastructure and Vision 2030 funding priorities.

How are intellectual property restrictions affecting growth?

Foreign ownership of key halophilic strains raises licensing costs and slows local innovation, reducing the regional CAGR by an estimated 1.4 percentage points.

What are the main restraints on immediate scale-up?

Limited downstream refining capacity and competition from low-cost solar hydrogen restrict rapid expansion, though new integrated projects aim to close these gaps.

Page last updated on: