Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 33.29 Billion |

| Market Size (2026) | USD 37.25 Billion |

| Market Size (2031) | USD 62.78 Billion |

| Growth Rate (2026 - 2031) | 11.00% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Biofuel Market Analysis by Mordor Intelligence

The Europe Biofuel Market size is expected to grow from USD 33.29 billion in 2025 to USD 37.25 billion in 2026 and is forecast to reach USD 62.78 billion by 2031 at 11% CAGR over 2026-2031.

Stronger renewable-energy quotas, widening carbon-pricing spreads, and rapid aviation uptake are encouraging refiners to divert capital from fossil fuels toward scalable hydrotreatment, gasification, and alcohol-to-jet pathways. EU Allowance prices above EUR 80 per tonne are giving waste-oil renewable diesel price parity with conventional diesel, while the ReFuelEU Aviation regulation is turning sustainable aviation fuel into a strategic offtake market for both oil majors and specialist producers. Advanced-generation routes are moving from pilot to demonstration scale as RED III sustainability caps squeeze first-generation crop capacity and reward waste and residue supply chains. Competitive intensity remains moderate because proprietary catalysts, enzyme platforms, and long-tenor supply contracts create defensible margins even as feedstock prices fluctuate.

Key Report Takeaways

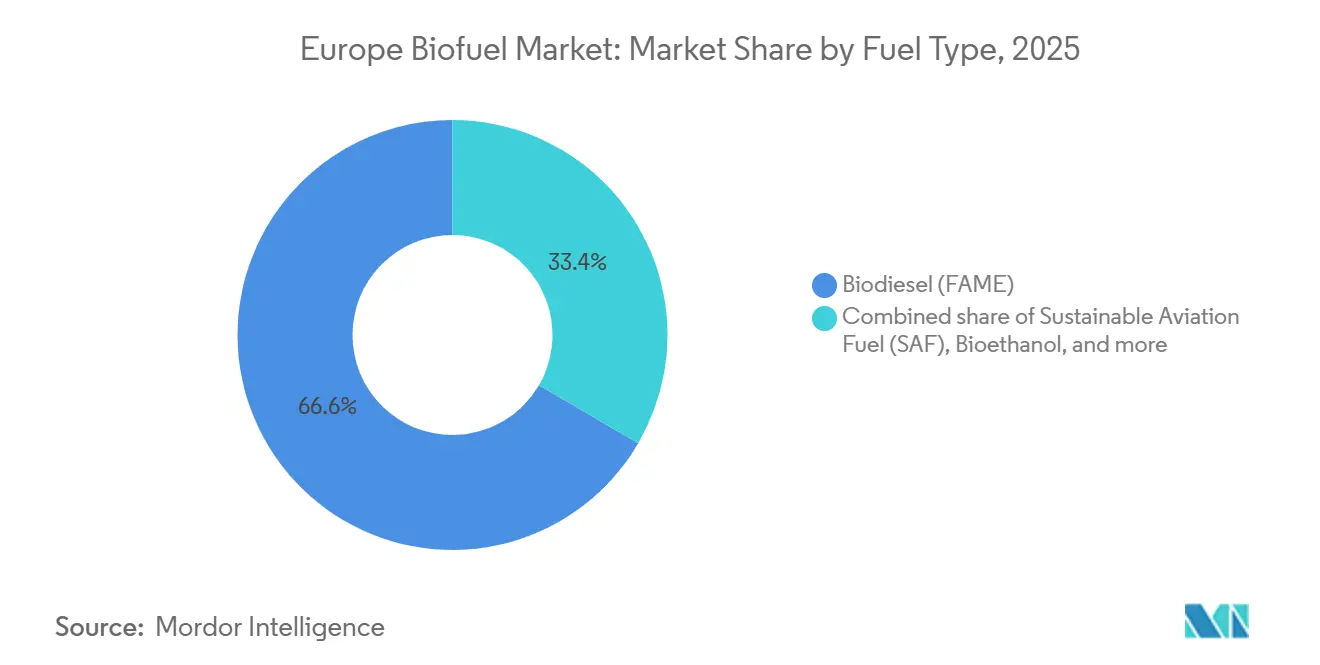

- By fuel type, biodiesel captured 66.6% of Europe's biofuel market share in 2025, whereas sustainable aviation fuel is forecast to expand at a 25.2% CAGR through 2031.

- By generation, first-generation platforms from sugar and starch crops accounted for 65.2% of the European biofuel market size in 2025, while fourth-generation synthetic-biology routes are projected to grow 19.5% annually to 2031.

- By feedstock, oilseeds supplied 45.9% of volume in 2025, yet algae-derived inputs are poised to increase 18.1% each year over the outlook period.

- By technology, trans-esterification represented 55.1% of installed capacity in 2025, but hydrotreatment units are scaling at 17.6% per year on the back of aviation offtake agreements.

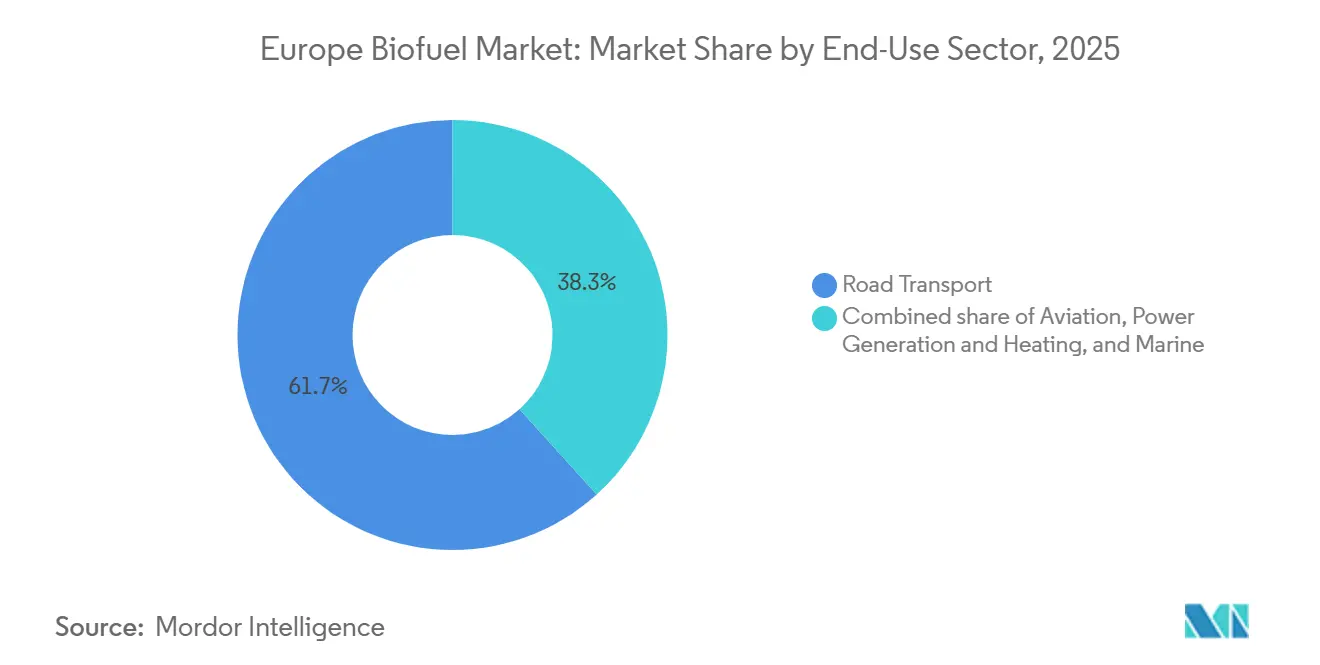

- By end-use sector, road transport absorbed 61.7% of demand in 2025, whereas aviation volumes are rising 25.2% per year as airlines secure long-term SAF contracts.

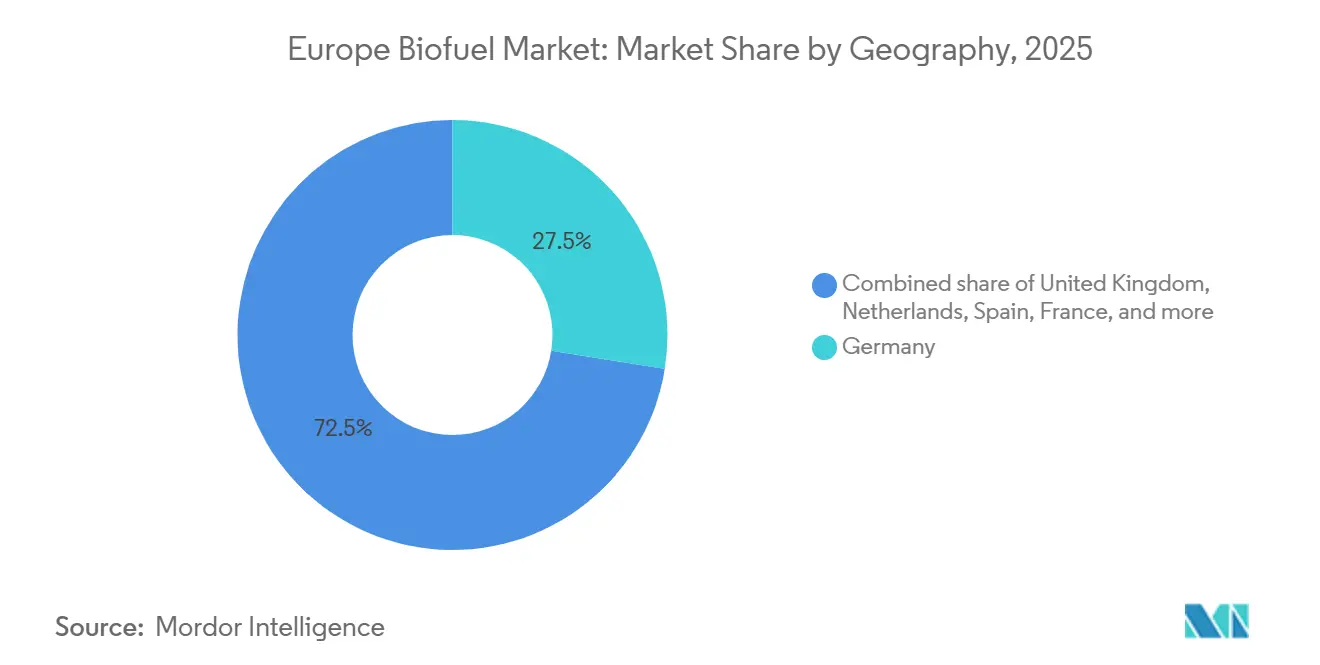

- By geography, Germany led with 27.5% revenue share in 2025, while the United Kingdom is advancing at a 17.2% CAGR thanks to strengthened Renewable Transport Fuel Obligation targets.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Biofuel Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU Renewable Energy Directive III escalating mandates | +2.8% | EU-wide, strongest in Germany, France, Netherlands | Medium term (2-4 years) |

| Fit-for-55 GHG-reduction targets | +2.3% | EU-wide, accelerated adoption in Nordic countries | Medium term (2-4 years) |

| Rising EU ETS carbon prices | +1.9% | EU-wide, particularly Germany, Netherlands, Belgium | Short term (≤ 2 years) |

| Sustainable-aviation-fuel (ReFuelEU) mandates | +2.5% | EU-wide, concentrated in France, Netherlands, UK aviation hubs | Long term (≥ 4 years) |

| BECCS credit upside for integrated plants | +0.9% | Sweden, Netherlands, Finland | Long term (≥ 4 years) |

| Waste-to-biofuel projects driven by landfill bans | +1.4% | Germany, France, Italy, Spain | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EU Renewable Energy Directive III Escalating Mandates

RED III, effective 2024, requires renewable energy to cover 29% of transport consumption by 2030 and sets a 5.5-percentage-point sub-target for advanced biofuels.[1]European Commission, “Fit-for-55 Package Details,” ec.europa.eu Member states must transpose the law by May 2025, creating a synchronized compliance wave that has already accelerated investment decisions across Germany, France, and the Netherlands. High-ILUC-risk feedstocks such as palm oil and soy face a gradual phase-out, redirecting capital toward waste oils, agricultural residues, and algae. Germany issued draft rules in 2025 that penalize first-generation volumes from 2028 onward, spurring developers to retool distilleries for lignocellulosic ethanol. France lifted its advanced-biofuel multiplier to 1.5 in 2024, prompting TotalEnergies to retrofit hydrotreatment lines for used-cooking-oil and tallow feedstocks. The tightened sustainability screen is squeezing conventional biodiesel margins but opening room for integrated biorefineries that can fractionate biomass into multiple products.

Fit-for-55 Greenhouse-Gas-Reduction Targets

The Fit-for-55 package obliges a 55% net GHG cut by 2030 versus 1990, with new emission ceilings of 37.5% for cars and 31% for vans in 2030. Renewable diesel and bioethanol remain the only drop-in options for heavy-duty fleets lacking viable electrification routes. Finland’s St1 Nordic started a 400,000-tonne waste-ethanol plant in Gothenburg in 2024 to capture this diesel-substitution opportunity. Maritime and aviation are now inside the EU ETS, boosting demand for bio-marine fuels and SAF. Italy’s Venice biorefinery began producing bio-marine gasoil in 2024 to serve vessels preparing for FuelEU Maritime emission caps.

Rising EU ETS Carbon Prices

EU Allowances rallied to EUR 90 per tonne in early 2024 before stabilizing near EUR 80 in 2025. At these prices, renewable diesel from waste oils, with lifecycle emissions below 50 g CO₂e/MJ, achieves cost parity with conventional diesel even without subsidies. Shell’s Rotterdam complex began co-processing 10% UCO in its hydrocracker in 2024 to monetize both the carbon-cost avoidance and Dutch HBE certificate premiums. Higher carbon prices are also shrinking the cost gap for gasification-to-liquid pathways; Velocys closed GBP 150 million in project finance for a waste-to-jet plant in Immingham in 2025, structured around a Brent-plus-carbon premium offtake.

Sustainable-Aviation-Fuel (ReFuelEU) Mandates

ReFuelEU Aviation obliges 2% SAF blending from 2025, climbing to 6% by 2030 and 70% by 2050, with penalties of EUR 5 per kilogram for non-compliance. Neste has earmarked 30% of its Rotterdam and Singapore renewable-products slate for SAF by 2027 under long-term contracts with Lufthansa, Air France-KLM, and British Airways. SkyNRG locked a 10-year deal with Amsterdam Schiphol in 2025 to supply 200,000 tonnes of SAF, aggregating volumes from UPM and Preem. Rising mandates are also catalyzing alcohol-to-jet and power-to-liquid projects; LanzaJet’s Freedom Pines plant exported ethanol-derived jet fuel to European carriers in late 2024, showcasing ASTM D7566 approval for non-HEFA routes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Feedstock price volatility & supply tightness | -1.6% | EU-wide, acute in Germany, Netherlands, Belgium | Short term (≤ 2 years) |

| Land-use & ILUC sustainability caps | -1.2% | EU-wide, particularly affecting palm-oil and soy imports | Medium term (2-4 years) |

| High CAPEX for advanced biofuel plants | -0.9% | EU-wide, concentrated in Nordic countries, Germany, Netherlands | Long term (≥ 4 years) |

| Competition from e-fuels & green hydrogen | -0.7% | Germany, Netherlands, Spain | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Feedstock Price Volatility & Supply Tightness

UCO spot prices in Rotterdam surged from EUR 800 per tonne in January 2024 to EUR 1,350 by December 2025 as renewable-diesel refiners outbid chemical and animal-feed buyers. Rapeseed oil hovered near EUR 1,100 per tonne in mid-2025 after drought slashed French and German harvests. Feedstock now represents three-quarters of renewable-product cash costs for Neste, heightening margin sensitivity. Imports of palm-oil methyl ester have waned under RED III’s high-ILUC cap, meaning any weather-induced supply disruption in Indonesia causes immediate European price spikes. Producers are therefore hedging by signing multi-year offtake deals and investing in alternative feedstocks such as straw and lignin.

High CAPEX for Advanced Biofuel Plants

Cellulosic-ethanol projects can cost EUR 300-500 million for 100,000-tonne annual output, nearly triple a conventional corn-ethanol plant, because of complex pretreatment and enzymatic hydrolysis.[2]International Energy Agency, “Advanced Biofuels Cost Benchmarks,” iea.org Hydrotreatment units require EUR 200-400 million for 200,000-tonne capacity plus additional hydrogen and feedstock logistics. Debt for advanced projects commands a 200–300 basis-point premium over refinery loans, reflecting technology risk. Germany’s KfW attempted to bridge the gap with EUR 100 million in concessional finance to Verbio in 2024, but the pipeline of bankable projects remains thin.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fuel Type: SAF Surge Reshapes Refinery Economics

The Europe Biodiesel Market accounted for 66.6% of the European biofuel market share in 2025, supported by established blending mandates and widespread use in the transportation sector. However, sustainable aviation fuel (SAF) expanded at an annual rate of 25.2% and is forecast to maintain similar growth through 2031. Renewable diesel, chemically identical to fossil diesel, is winning fleet contracts across Scandinavia and Germany because it meets more stringent greenhouse-gas-reduction quotas. The European biofuel market size for SAF reached USD 2.4 billion in 2025 and is projected to surpass USD 10 billion by 2031, underscoring aviation's compliance pull. Airlines are locking 10- to 15-year supply agreements. Air France-KLM is committed to 800,000 tonnes through 2035, providing predictable revenue streams that de-risk hydrotreatment and alcohol-to-jet investments. Biodiesel demand is plateauing as legacy engines max out at B7 blending levels and ILUC caps constrain virgin-oil feedstock. Renewable diesel's drop-in characteristics, coupled with HBE certificate premiums, are cannibalizing biodiesel volumes in the Netherlands and Germany. Niche molecules such as bio-naphtha remain below 3% of volumes but are gaining strategic relevance as petrochemical feedstocks for renewable plastics.

Bioethanol consumption depends on flex-fuel adoption; Sweden's E85 sales increased 12% in 2024 under tax incentives, while Italy and Spain saw declines amid gasoline demand shrinkage. SAF growth is driving product-slate re-optimization at refineries: TotalEnergies shifted 40% of La Mède output to jet fuel in 2024, and Neste plans a similar pivot in Rotterdam by 2027. The hydrotreatment route's ability to swing cut yields between diesel and jet provides margin insurance against demand fluctuations. As ReFuelEU blending rates escalate, SAF production is expected to account for nearly one-quarter of hydrotreating capacity additions between 2026 and 2031, permanently altering European refinery economics.

By Generation: Fourth-Generation Platforms Transition from Lab to Pilot

First-generation pathways from sugar and starch crops controlled 65.2% of the European biofuel market in 2025, but policy ceilings and feedstock costs cap further growth. Second-generation, residue-based plants are moving into commercial viability, helped by double-counting credits; Clariant’s Sunliquid facility in Romania delivered ethanol at EUR 0.90 per liter in 2024, closing to within 10% of first-generation economics. Third-generation algae remains at demonstration scale; Dutch startup Photanol attracted EUR 30 million in 2025 to pilot a 10,000-tonne cyanobacteria plant that converts CO₂ and sunlight directly into ethanol. Fourth-generation synthetic-biology platforms, such as LanzaTech’s gas-fermentation, are forecast to lift their share of the European biofuel market size by growing 19.5% annually. That trajectory reflects corporate-venture funding and falling genome-editing costs, which shorten lab-to-pilot cycles and improve strain productivity.

As RED III tightens ILUC caps, first-generation facilities in France and Germany are exploring waste-oil retrofits or capacity closures. Tereos will idle two distilleries by 2026, removing 400,000 tonnes of crop-based ethanol supply. Investors are favoring platforms with land-neutral feedstocks; British Airways placed GBP 10 million into a LanzaTech project in Port Talbot to secure early access to gas-fermentation SAF. Fourth-generation projects must still prove scalability and cost competitiveness, but the technological learning curve and BECCS credit potential make them a material share gainer beyond 2030.

By Feedstock: Algae and Residues Challenge Oilseed Dominance

Oilseeds supplied 45.9% of 2025 volumes, yet the European biofuel market size linked to algae-sourced inputs is projected to post an 18.1% CAGR, eating into the vegetable-oil share. Used cooking oil collection hit 3.5 million tonnes in 2024 as municipal landfill bans expanded, and animal-fat renderers in Denmark shipped 200,000 tonnes of tallow to renewable-diesel producers. Rapid growth in waste-oil demand is now creating logistical bottlenecks; Spain and Italy import Asian UCO at premiums of EUR 100-150 per tonne over domestic supply. Lignocellulosic residues are scaling as straw-aggregation networks mature; Verbio’s Zörbig plant processes 240,000 tonnes of straw each year and delivers ethanol with an 85% lower carbon footprint than corn ethanol.

Algae cultivation finally moved beyond lab scale; Photanol’s pilot in Rotterdam targets photosynthetic efficiencies near 15%, doubling conventional algae benchmarks and avoiding freshwater stress by using brackish water. Oilseed dependence remains an economic hedge because existing crushers and trans-esterification units are designed for rapeseed and soy. However, tightening ILUC rules and price spikes underscore the strategic value of diversified, land-neutral feedstocks. Investors anticipate residues and algae will exceed one-third of the total feedstock supply by 2031, advancing Europe’s compliance with RED III sustainability criteria.

By Technology: Hydrotreatment Gains on Trans-Esterification

Trans-esterification still provided 55.1% of production capacity in 2025, but hydrotreatment is expanding 17.6% annually because it produces multiple drop-in fuels (renewable diesel, SAF, bio-naphtha, and bioLPG) from diverse feedstock slates.

Pyrolysis-oil upgrading, piloted by Fortum and BTG, offers a modular route to liquid fuels but still yields 20-30% less finished product per tonne of biomass than hydrotreatment. Green-field hydrotreatment capital costs align with trans-esterification, but higher netbacks and aviation offtake agreements shorten payback periods. Co-processing strategies at refineries like Shell Pernis avoid green-field spend altogether, underscoring hydrotreatment’s flexibility. As a result, the European biofuel market size added via hydrotreatment is expected to outpace all other technology pathways through 2031.

By End-Use Sector: Aviation Overtakes Road in Growth Momentum

Road transport absorbed 61.7% of volume in 2025, but electric-vehicle adoption is flattening diesel and gasoline demand. Tightened German greenhouse-gas quotas increased renewable diesel uptake, yet the ceiling at B7 biodiesel blends limits further growth. Aviation is rising 25.2% each year, mirroring SAF supply. Lufthansa pledged to achieve 10% SAF use across its network by 2030, guaranteeing offtake that underwrites new hydrotreatment units. The European biofuel market size attributed to aviation stood at USD 2.4 billion in 2025 and will likely exceed USD 10 billion by 2031.

Marine demand is emergent under IMO net-zero targets; Eni’s Venice plant began producing 750,000 tonnes of bio-marine gasoil in 2024, although bunkering infrastructure remains limited outside Rotterdam and Antwerp. Power generation and heating markets are marginal but lucrative under carbon-removal economics; Stockholm Exergi will monetize 800,000 tonnes of CO₂ removals annually from 2026. Road-sector biofuel growth will plateau near 2028, whereas aviation and, to a lesser extent, marine will capture incremental demand. End-use segmentation, therefore, shifts from road-centric to aviation-centric over the forecast horizon.

Geography Analysis

Germany held 27.5% of revenue in 2025, reflecting 2.5 million tonnes of biodiesel and renewable-diesel capacity under a 25% greenhouse-gas-reduction quota. Verbio’s Schwedt complex processed 450,000 tonnes of UCO and straw in 2024, supplying domestic fleets and exports to Poland. Carbon prices above EUR 80 per tonne make Germany an attractive market for waste oil and residue-based fuels, narrowing the cost gap with fossil diesel. The country’s Biofuels Quota Act revision in 2025 penalizes first-generation biofuels after 2028, compelling producers to accelerate cellulosic and hydrotreatment conversions.

The United Kingdom posted the fastest growth, rising 17.2% annually toward 2031 as the Renewable Transport Fuel Obligation raised the development-fuel multiplier and overall quota to 12.4% by 2032.[3]UK Department for Transport, “Renewable Transport Fuel Obligation 2024 Revision,” gov.uk Velocys and LanzaJet projects, backed by British Airways and Virgin Atlantic, are transforming the UK into a SAF hub. France controlled 18% market share in 2025 thanks to TotalEnergies’ La Mède and Grandpuits plants, which process 1 million tonnes of waste oils yearly. The French energy law of 2024 lifted the advanced-biofuel multiplier to 1.5, driving cellulosic and hydrotreatment investments.

Nordic countries collectively held 16% of the European biofuel market. Neste’s Porvoo refinery delivered 1.5 million tonnes of renewable diesel in 2024, exporting 60% to California and the Netherlands. Preem’s Swedish refineries produced 1 million tonnes of renewable diesel and plan a 500,000-tonne expansion by 2027. UPM’s tall-oil biorefinery in Lappeenranta produced 150,000 tonnes in 2024, leveraging forestry residue integration. Italy and Spain each accounted for around 9% in 2025; Eni’s converted Gela and Venice sites process 1.5 million tonnes of waste oils, while Cepsa is building a 500,000-tonne SAF plant in Huelva by 2028. The Netherlands, with 7% share, operates as a biofuel trading hub through Rotterdam’s deepwater port, where Shell and Neste co-process bio-feedstocks.

The rest of Europe, Belgium, Austria, Poland, and smaller markets, combined for 12% in 2025. Belgium’s biodiesel sector, anchored by Cargill and Bunge, meets domestic blending mandates and exports a surplus to France. Russia remains marginal at under 2% given limited domestic mandates and export infrastructure. Geographic leadership, therefore, tracks policy stringency, feedstock availability, and refinery flexibility, cementing Germany, France, and the Nordics as regional anchors while the UK emerges as the pace-setter for SAF commercialization.

Competitive Landscape

The top five producers, Neste, TotalEnergies, Shell, Eni, and Preem, collectively control about 40% of European capacity, placing the European biofuel market in moderate-concentration territory. Neste leverages proprietary NEXBTL hydrotreatment to process a wide feedstock slate and captured 30% of renewable-diesel volumes in 2025. TotalEnergies repurposed La Mède and Grandpuits from fossil refining to biofuel production, illustrating the capital efficiency of brownfield conversions.[4]TotalEnergies, “Grandpuits Biorefinery Conversion,” totalenergies.com Shell’s Pernis refinery co-processes 10% bio-feedstock in a hydrocracker, exploiting existing hydrogen and distillation assets to lower capital outlay.

Specialist firms such as Verbio, UPM, and Clariant differentiate through technology niches, straw-to-ethanol, tall-oil-to-diesel, and cellulosic enzymes, respectively. SkyNRG has pioneered the SAF aggregator model, signing decade-long supply deals with airports and airlines without owning refining hardware. Stockholm Exergi is demonstrating the BECCS-plus-biofuel dual-revenue model, capturing removals for sale under Article 6 while selling heat and power locally. Technology moats matter: proprietary catalysts, enzyme cocktails, and certified traceability systems allow players to defend margins even as feedstock prices spike.

Regulatory compliance creates barriers to entry; detailed sustainability audits under RED III favor incumbents with established chains of custody. Capital discipline is visible: Shell directs 40% of low-carbon spend toward hydrogen and e-fuels, hedging against long-term biofuel margin erosion. Overall, strategic moves center on feedstock security, refinery flexibility, and lifecycle-emissions credentials, reinforcing the mid-pack concentration while leaving room for technology disruptors.

Europe Biofuel Industry Leaders

Neste Oyj

TotalEnergies SE

Preem AB

UPM-Kymmene Oyj

Verbio Vereinigte BioEnergie AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Etlas, a new joint venture between Corteva Inc. and energy giant BP, is set to extract oil from crops such as canola, mustard, and sunflower. This oil will be utilized in producing biofuels, including sustainable aviation fuel (SAF) and renewable diesel (RD).

- December 2025: Germany's cabinet has approved a law to adopt the EU's Renewable Energy Directive (RED III). The legislation simplifies renewable energy project approvals, removes red tape, and sets clear guidelines for expanding wind, solar, and other clean energy technologies.

- September 2025: Velocys-owned Altalto (Immingham) Limited has secured funding from the UK Department for Transport's Advanced Fuels Fund. This grant is aimed at finalizing the Basic Engineering Design for Altalto's flagship waste-to-SAF facility.

- December 2024: BP has rolled out BP Bioenergy HVO in Spain, targeting the heavy-duty road transport sector. This renewable diesel will be offered at select service stations in Madrid, Valencia, and Navarre. Spain's pilot project comes on the heels of bp bioenergy HVO's debut at filling stations across several European nations, such as the UK, Austria, Germany, and the Netherlands.

Europe Biofuel Market Report Scope

Biofuel is a type of fuel that is made in a short amount of time from biomass instead of through the very slow natural processes that make fossil fuels like oil. Biofuel can be produced from plants or from agricultural, domestic, or industrial biowaste.

The European biofuel market is segmented by fuel type, generation, feedstock, technology, end-use, and geography. By fuel type, the market is segmented into bioethanol, biodiesel, renewable diesel/HVO, SAF, and bio-naphtha. By generation, the market is segmented into first, second, third, and fourth. By feedstock, the market is segmented into sugar, starch, oilseeds, UCO, lignocellulosic, and algae. By technology, the market is segmented into fermentation, trans-esterification, hydrotreatment, gasification, and pyrolysis. By end-use, the market is segmented into road transport, aviation, marine, and power generation and heating. The report also covers the market size and forecasts for the European biofuel market across the major countries in the region. For each segment, the market sizing and forecasts have been done based on revenue (USD).

By Fuel Type

| Bioethanol |

| Biodiesel (FAME) |

| Renewable Diesel/HVO |

| Sustainable Aviation Fuel (SAF) |

| Bio-naphtha and Other Drop-in Biofuels |

By Generation

| First-Generation (Sugar and Starch) |

| Second-Generation (Cellulosic) |

| Third-Generation (Algae-based) |

| Fourth-Generation (Synthetic Biology/Photobiological) |

By Feedstock

| Sugar Crops (Sugarcane, Sugar Beet) |

| Starch Crops (Corn, Wheat, Cassava) |

| Oilseeds (Soy, Rapeseed, Palm) |

| Used Cooking Oil and Animal Fat |

| Lignocellulosic Agri-Residues |

| Algae |

By Technology

| Fermentation |

| Trans-esterification |

| Hydrotreatment (HVO / SAF) |

| Gasification and FT-Synthesis |

| Pyrolysis and Upgrading |

By End-use Sector

| Road Transport |

| Aviation |

| Marine |

| Power Generation and Heating |

By Geography

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Netherlands |

| NORDIC Countries |

| Russia |

| Rest of Europe |

| By Fuel Type | Bioethanol |

| Biodiesel (FAME) | |

| Renewable Diesel/HVO | |

| Sustainable Aviation Fuel (SAF) | |

| Bio-naphtha and Other Drop-in Biofuels | |

| By Generation | First-Generation (Sugar and Starch) |

| Second-Generation (Cellulosic) | |

| Third-Generation (Algae-based) | |

| Fourth-Generation (Synthetic Biology/Photobiological) | |

| By Feedstock | Sugar Crops (Sugarcane, Sugar Beet) |

| Starch Crops (Corn, Wheat, Cassava) | |

| Oilseeds (Soy, Rapeseed, Palm) | |

| Used Cooking Oil and Animal Fat | |

| Lignocellulosic Agri-Residues | |

| Algae | |

| By Technology | Fermentation |

| Trans-esterification | |

| Hydrotreatment (HVO / SAF) | |

| Gasification and FT-Synthesis | |

| Pyrolysis and Upgrading | |

| By End-use Sector | Road Transport |

| Aviation | |

| Marine | |

| Power Generation and Heating | |

| By Geography | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe |

Key Questions Answered in the Report

What is the value of the Europe biofuel market in 2026?

The Europe biofuel market size stood at USD 37.25 billion in 2026 and is projected to increase to USD 62.78 billion by 2031, growing at a CAGR of 11% through 2031.

Which technology pathway is scaling quickest across European biorefineries?

Hydrotreatment units are adding capacity at 17.6% per year because they yield renewable diesel, SAF, and coproducts in a single train.

What share of European biofuel capacity do the top five producers control today?

Neste, TotalEnergies, Shell, Eni, and Preem together account for about 40% of installed capacity, indicating moderate concentration.

Why are oilseeds losing feedstock share despite high historical use?

Tight ILUC caps, land-use concerns, and price spikes are redirecting investment toward waste oils, residues, and algae that avoid food-versus-fuel conflicts.

How do EU carbon-pricing trends influence biofuel competitiveness?

EU Allowance prices above EUR 80 make low-carbon biofuels cost-competitive with fossil diesel even without blending subsidies, accelerating refiners' shift to renewable feedstocks.

How fast will aviation demand for sustainable fuel grow in Europe by 2031?

Aviation volumes for sustainable aviation fuel are expanding at a 25.2% CAGR, lifting the segment above USD 10 billion by 2031.

Page last updated on: