Market Overview

| Study Period | 2021 - 2031 |

|---|---|

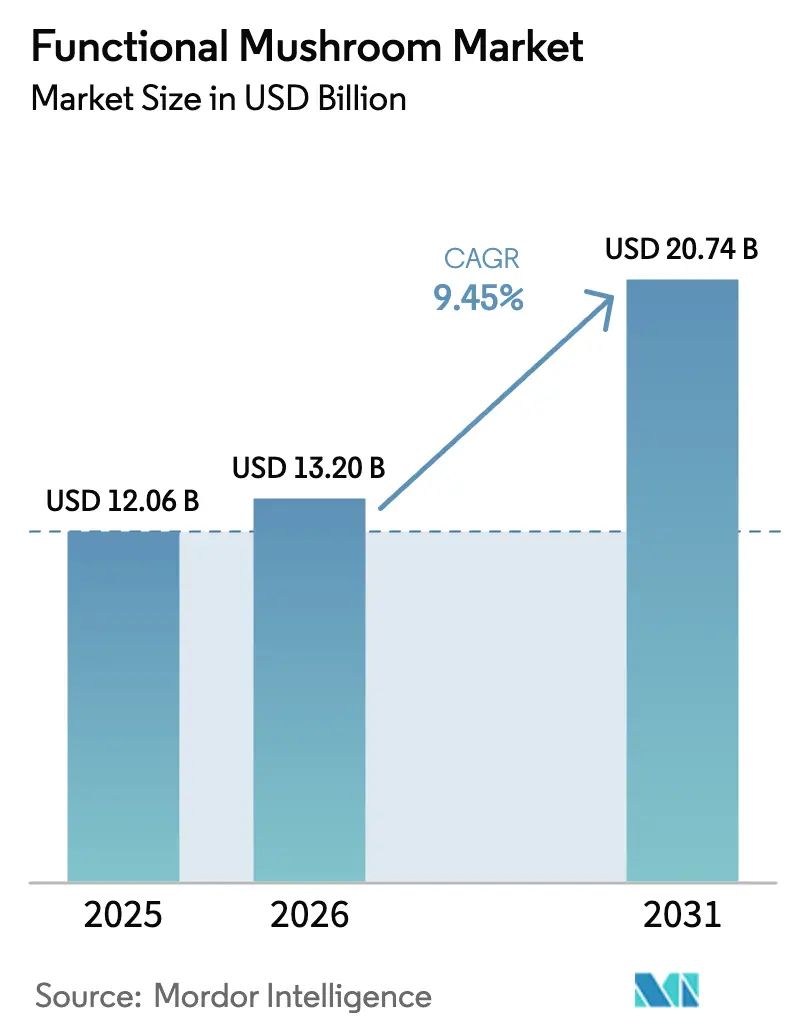

| Market Size (2026) | USD 13.20 Billion |

| Market Size (2031) | USD 20.74 Billion |

| Growth Rate (2026 - 2031) | 9.45% CAGR |

| Fastest Growing Market | Europe |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Functional Mushroom Market Analysis by Mordor Intelligence

The functional mushroom market size was valued at USD 12.06 billion in 2025 and estimated to grow from USD 13.20 billion in 2026 to reach USD 20.74 billion by 2031, at a CAGR of 9.45% during the forecast period (2026-2031). This growth trajectory reflects the convergence of consumer wellness priorities with scientific validation of bioactive compounds, particularly as regulatory frameworks evolve to accommodate novel food applications. This trajectory reflects a structural shift in consumer wellness priorities, where immune resilience, cognitive performance, and plant-based nutrition converge to redefine supplement and functional food categories. Moreover, the European Food Safety Authority's updated novel food guidance, effective February 2025, provides clearer pathways for mushroom-based ingredients. Technology upgrades, notably supercritical CO₂ extraction and precision fermentation, are improving yield, purity, and sustainability. Additionally, vertical integration in Asia-Pacific and stricter European quality standards reshape competitive dynamics in the functional mushroom market.

Key Report Takeaways

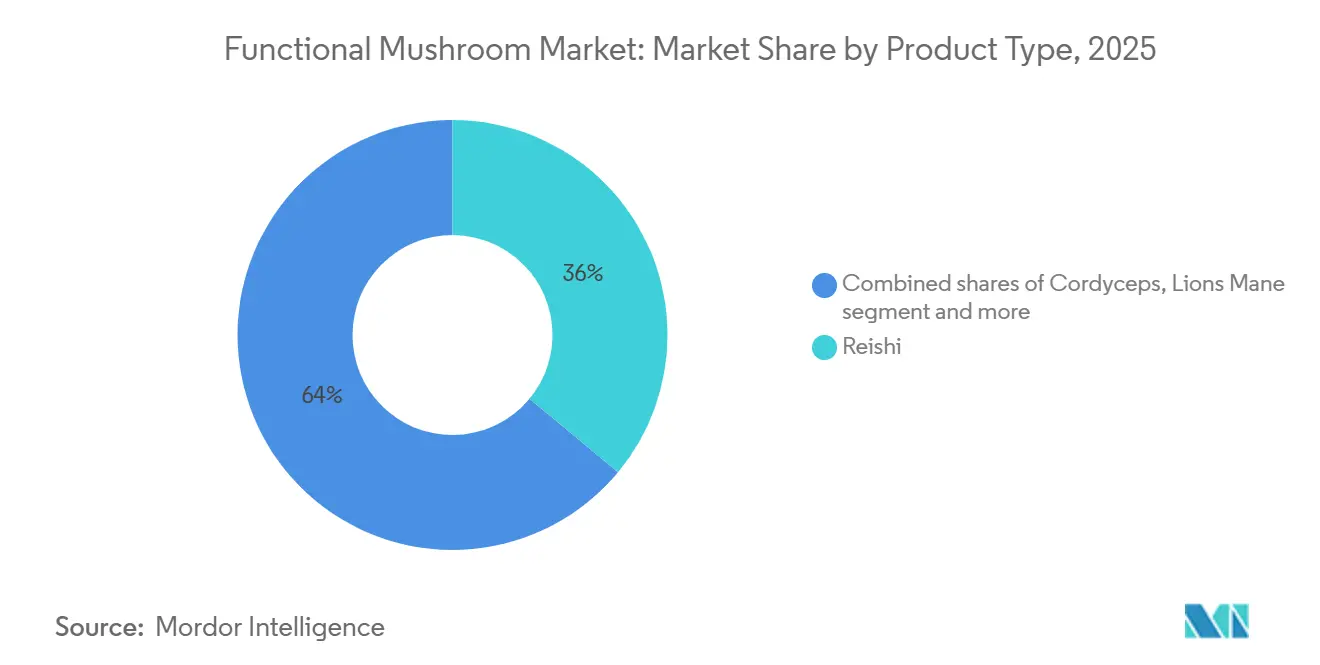

- By product type, reishi commanded 36.02% of functional mushroom market share in 2025; Cordyceps is forecast to post the fastest 9.87% CAGR through 2031.

- By nature, conventional variants held 57.11% of the functional mushroom market size in 2025, while organic products are set to rise at an 11.76% CAGR through 2031.

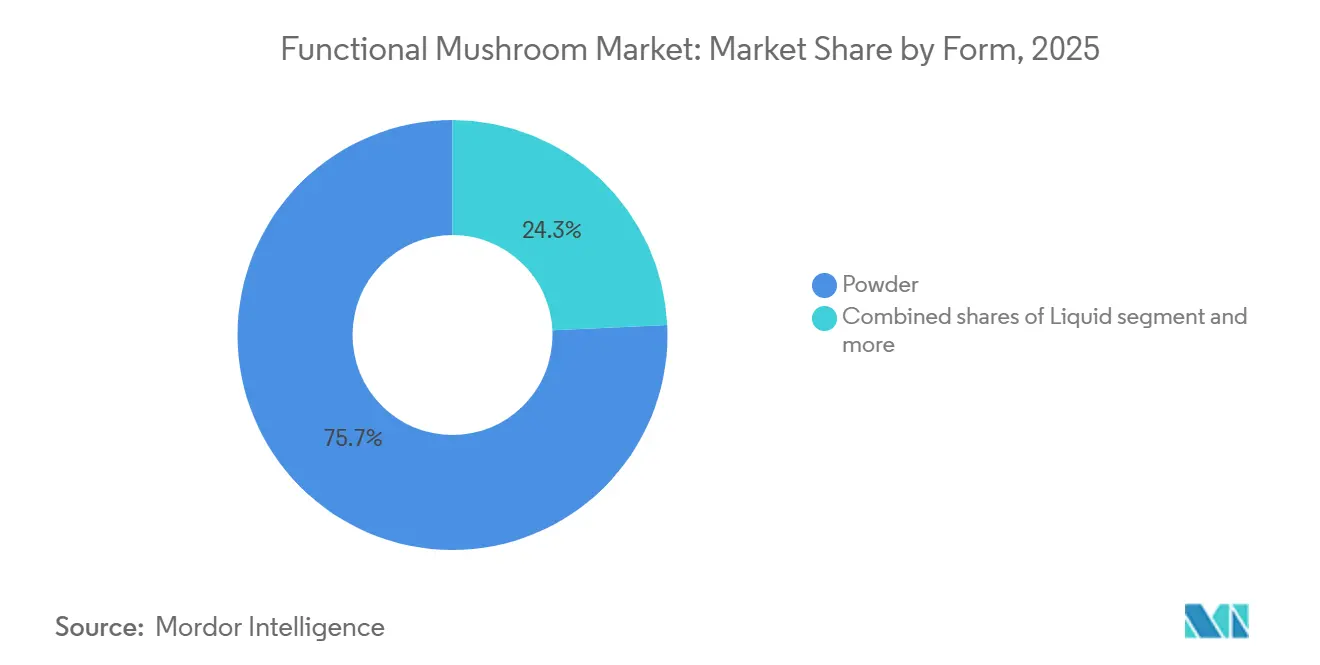

- By form, powder formats captured 75.74% of revenue in 2025 and liquid extracts are growing at a 10.62% CAGR through 2031.

- By application, dietary supplements controlled 38.55% of spending in 2025 and personal care is advancing at a 10.42% CAGR to 2031.

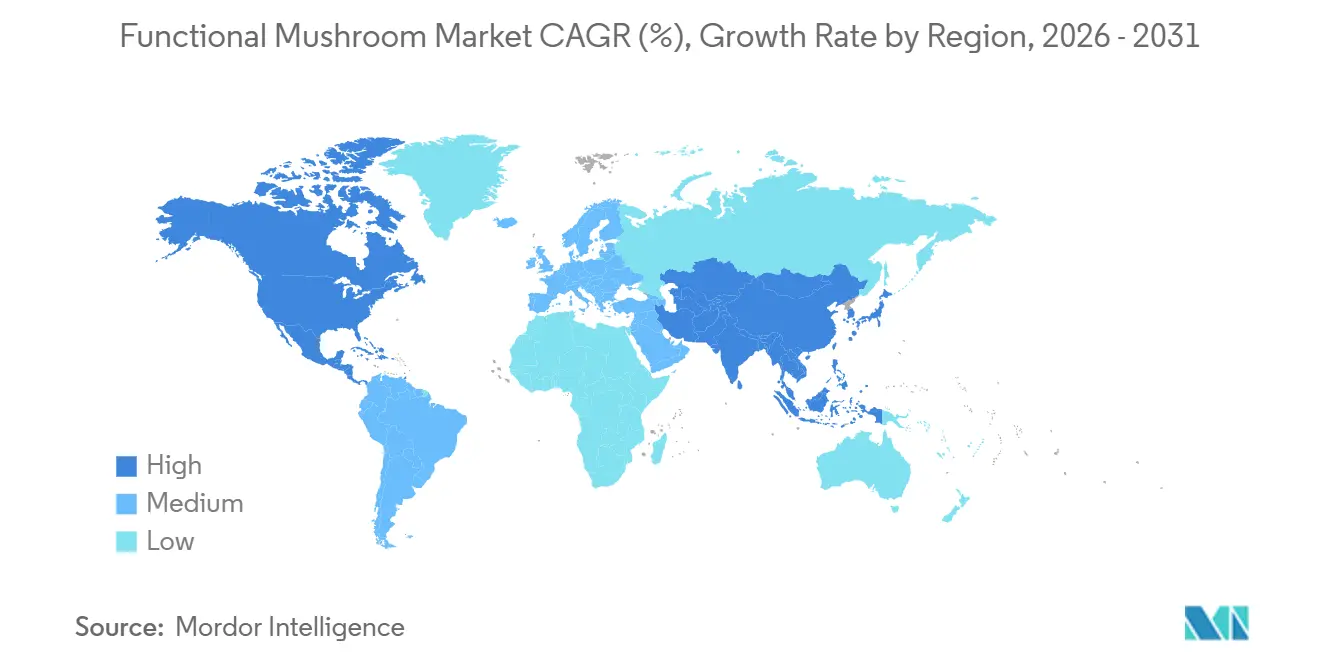

- Asia-Pacific accounted for 33.66% of sales in 2025, whereas Europe is projected to grow quickest at an 11.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Functional Mushroom Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Immune-boosting mushroom supplements | +2.1% | Global; strongest in North America and Europe | Medium term (2-4 years) |

| Mushrooms in plant-based diets | +1.8% | North America and Europe core, expanding to Asia-Pacific urban centers | Long term (≥4 years) |

| Mushroom-based skincare products | +1.4% | Europe and North America, early adoption in Asia-Pacific | Medium term (2-4 years) |

| Cognitive-enhancing mushroom supplements | +1.9% | Global with premium markets leading | Short term (≤2 years) |

| Mushrooms in sports performance nutrition | +1.2% | North America and Europe, spreading to Australia | Medium term (2-4 years) |

| Convenient mushroom-infused beverages | +1.6% | Global, driven by beverage innovation hubs | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Demand for immune-boosting mushroom supplements

Post-pandemic consumer behavior has entrenched immune support as a non-negotiable wellness pillar, and beta-glucan-rich mushrooms are displacing synthetic immunomodulators in both preventive and adjuvant protocols. A 2024 randomized controlled trial published in the International Journal of Medicinal Mushrooms demonstrated that Reishi polysaccharide supplementation increased natural killer cell activity by 34% over 8 weeks in healthy adults, a finding that has accelerated clinical adoption in integrative oncology settings, according to PubMed. Regulatory clarity is also improving, with the European Food Safety Authority issuing guidance in 2025 on acceptable beta-glucan content claims for mushroom extracts, reducing compliance uncertainty for brands targeting EU markets.

Adoption of Mushrooms in Plant-Based Diets

Mushrooms are emerging as a protein and umami source in plant-based formulations, addressing texture and flavor gaps that have limited consumer acceptance of legume-centric alternatives. Shiitake and Lion's Mane contain 20-25% protein by dry weight and deliver glutamate compounds that replicate the savory depth of animal products, making them attractive to food technologists reformulating meat analogs and dairy-free cheeses. Beyond protein, mushrooms offer prebiotic fibers and B vitamins that address nutritional deficiencies in vegan diets, a selling point that resonates with flexitarian consumers seeking nutrient density over ideological purity. The trend is most advanced in North America and Europe, where plant-based food sales grew in 2025 according to the Good Food Institute, with mushroom-based products capturing a disproportionate share of that growth.

Growth of Mushroom-Based Skincare Products

Plant-based food sales with mushroom-based alternatives are capturing disproportionate growth as texture and umami characteristics address key consumer acceptance barriers. Mycoprotein innovation accelerates beyond traditional meat substitutes, with companies developing dairy alternatives and hybrid formulations that combine plant and fungal ingredients for enhanced nutritional profiles. Sustainability credentials strengthen mushrooms' positioning, as cultivation requires significantly less water and land compared to animal protein production, aligning with environmental consciousness trends. However, cost competitiveness remains challenging, with mushroom proteins currently commanding premium pricing versus conventional alternatives. The integration of agricultural waste substrates presents pathways for cost reduction while enhancing circular economy credentials.

Demand for Cognitive-Enhancing Mushroom Supplements

Lion's Mane and Cordyceps are transitioning from niche nootropics to mainstream cognitive support ingredients, driven by clinical evidence of neuroplasticity enhancement and mental fatigue reduction. A 2024 systematic review in Nutrients analyzed 12 randomized controlled trials and concluded that Lion's Mane supplementation at 1-3 grams daily improved cognitive function scores by an average of 15% in adults aged 50-80, with benefits attributed to hericenones and erinacines that stimulate nerve growth factor synthesis, according to PubMed. Cordyceps militaris has shown promise in reducing perceived exertion during cognitive tasks, with a 2025 study in the Journal of Functional Foods reporting a 22% improvement in working memory accuracy among participants supplementing with 1.5 grams daily for 4 weeks, according to PubMed. These findings are resonating with aging populations in Japan and North America, where cognitive decline prevention is a top health priority, as well as with younger professionals seeking non-stimulant focus aids.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw material supply volatility | -1.8% | Global; acute where wild harvesting dominates | Short term (≤2 years) |

| Higher production costs | -1.2% | Global; heightened in price-sensitive economies | Medium term (2-4 years) |

| Storage and shelf-life limitations | -0.9% | Global; amplified in humid climates | Medium term (2-4 years) |

| Competition from alternative products | -1.1% | North America and Europe where synthetics are prevalent | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Growing competition from alternative products

The availability of synthetic ergothioneine and laboratory-produced beta-glucans creates cost-effective alternatives for functional mushroom products. These synthetic options appeal to price-sensitive consumers in developed markets, reducing the premium pricing potential of natural mushroom ingredients. The synthetic compounds often match the molecular structure of natural mushroom compounds at a fraction of the cost, making them attractive to manufacturers looking to optimize production costs. In response, mushroom product manufacturers emphasize the benefits of whole-mushroom compounds and their natural cultivation processes, supported by comprehensive traceability systems. Additionally, companies highlight their sustainable farming practices, organic certifications, and rigorous quality control measures to justify premium pricing and maintain market share against synthetic competition.

Higher production costs compared to conventional supplements

Specialized extraction processes like supercritical CO2 and enzyme-assisted ultrasound extraction command premium costs while delivering superior bioactive compound yields, creating cost-quality trade-offs that challenge mass market penetration. The transition from wild harvesting to controlled cultivation requires substantial infrastructure investment, with companies like Applied Food Sciences and KÄÄPÄ Biotech building state-of-the-art facilities to ensure consistent quality and supply. Quality control requirements under 21 CFR 111 for dietary supplements add compliance costs that disproportionately affect smaller producers and may drive market consolidation. In contrast, premium positioning in functional foods and nutraceuticals enables higher margins that can offset these costs for companies with strong brand differentiation and clinical validation[1]U.S. Food and Drug Administration, “GRAS Notice Inventory,” fda.gov.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Reishi Leadership Faces Cordyceps Challenge

Reishi held 36.02% market share in 2025, reflecting its established position in traditional Chinese medicine and decades of clinical research validating its immunomodulatory and hepatoprotective effects. However, Cordyceps is expanding at 9.87% CAGR through 2031, outpacing Reishi's growth as sports nutrition and energy supplement applications broaden its consumer base beyond wellness purists. Cordyceps militaris, cultivated on grain substrates, offers higher cordycepin content than wild-harvested Cordyceps sinensis, making it a cost-effective and sustainable alternative that appeals to environmentally conscious brands. Lion's Mane is carving out a niche in cognitive health, with sales concentrated among aging populations and students seeking non-stimulant focus aids, while Turkey Tail's PSK compound is gaining traction in integrative oncology protocols as an adjuvant to chemotherapy.

Shiitake and Chaga occupy smaller but stable shares, with Shiitake leveraging its culinary familiarity to enter functional food applications and Chaga benefiting from antioxidant positioning in premium supplement lines. The "Other Product Types" category includes emerging species like Maitake and Tremella, which are finding applications in immune support and skincare, respectively. Product innovation is accelerating, with brands launching multi-mushroom blends that combine Reishi, Lion's Mane, and Cordyceps to deliver synergistic benefits, a strategy that complicates single-species market share tracking but signals maturation of the category. Regulatory frameworks are also evolving, with the U.S. Pharmacopeia publishing monographs for Reishi and Lion's Mane in 2025 that establish quality standards for identity, purity, and potency, reducing adulteration risk and building consumer confidence.

By Nature: Organic Certification Drives Premium Positioning

Conventional products commanded a 57.11% share in 2025, benefiting from lower price points and established distribution in mass-market retail channels. Yet organic variants are accelerating at 11.76% CAGR through 2031, driven by European and North American consumers willing to pay 30-50% premiums for USDA (United States Department of Agriculture) Organic, EU Organic, or JAS-certified extracts that guarantee pesticide-free cultivation and non-GMO substrates. A 2024 survey by the Organic Trade Association found that 62% of U.S. mushroom supplement buyers prioritize organic certification over brand loyalty, a shift that is forcing conventional suppliers to either invest in organic conversion or accept margin compression, according to the PubMed. Organic certification also unlocks access to premium distribution channels, including natural food stores and direct-to-consumer e-commerce platforms that cater to health-conscious demographics.

The organic segment faces supply constraints, as transitioning cultivation facilities to organic standards requires 3-year waiting periods and ongoing compliance audits that smaller producers struggle to afford. China's organic certification infrastructure is improving, with the China Organic Food Certification Center accrediting over 200 mushroom farms in 2024-2025, but traceability concerns persist among Western buyers who prefer domestic or Japanese organic sources. Conventional products will retain the majority share in price-sensitive markets and food service applications where organic premiums are harder to justify, but the trajectory clearly favors organic as consumer education around pesticide residues and synthetic fertilizers intensifies. Compliance frameworks such as ISO 17065 for organic certification bodies are enhancing credibility and reducing the risk of fraudulent labeling, a development that benefits legitimate organic suppliers.

By Form: Liquid Extracts Challenge Powder Dominance

Powder formats maintain a 75.74% share of the functional mushroom market due to their extended shelf life and flexible dosing capabilities. The extraction process using supercritical CO₂ produces stable oil-soluble components for emulsified beverages, though it requires substantial capital investment. While cold-chain requirements limit distribution in developing markets, powder formats remain viable in ambient conditions. The industry faces challenges in masking flavors for high-dose liquid products, leading to increased research in microencapsulated bitter blockers. Market success increasingly depends on companies' ability to deliver both palatable and stable functional mushroom products.

The liquid concentrate segment is expected to grow at a CAGR of 10.62% through 2031, driven by increasing demand for ready-to-drink coffees, teas, and shots in cafes and convenience stores. The market also includes fermented sparkling tonics that improve nutrient absorption, while gummies and capsules serve specific consumer needs for precise dosing and convenience. Liquid concentrates outperform other forms in delivering bioactive compounds from functional mushrooms, such as beta-glucans, polysaccharides, triterpenoids, and antioxidants. Being in a liquid state, they enable swift absorption either sublingually or via the gastrointestinal tract, sidestepping the digestive breakdown that powders necessitate.

By Application: Personal Care Emerges as Growth Frontier

Dietary supplements represented 38.55% of applications in 2025, anchored by immune support, cognitive health, and energy formulations that leverage mushrooms' adaptogenic properties. This segment benefits from established consumer awareness and distribution through health food stores, pharmacies, and e-commerce platforms. However, personal care is expanding at 10.42% CAGR through 2031, as cosmetic chemists incorporate mushroom-derived beta-glucan, kojic acid, and polysaccharides into anti-aging, hydrating, and skin-brightening products that compete with synthetic actives. The clean beauty movement is accelerating this shift, with consumers seeking plant-based alternatives to retinoids, hydroquinone, and parabens that carry perceived safety risks.

Food and beverage applications are growing steadily, driven by mushroom-infused coffee, tea, and functional drinks that democratize access beyond the supplement aisle, while pharmaceutical applications remain niche but high-value, focused on PSK and PSP extracts used in adjuvant cancer therapy and immunomodulation protocols. "Other Applications" include animal nutrition and agricultural biostimulants, where mushroom mycelium is being tested as a probiotic feed additive and soil health enhancer. The application landscape is fragmenting as brands experiment with cross-category positioning, such as dietary supplements marketed for skin health or beverages formulated with pharmaceutical-grade extracts. Regulatory pathways differ significantly by application, with dietary supplements subject to the FDA's DSHEA framework, cosmetics regulated under the Federal Food, Drug, and Cosmetic Act, and pharmaceutical applications requiring IND filings and clinical trial data, creating compliance complexity for vertically integrated players.

Geography Analysis

Asia-Pacific dominates with 33.66% market share in 2025, leveraging traditional medicine heritage and established cultivation infrastructure that provides cost advantages and quality consistency across major mushroom species. China's Ministry of Science and Technology launched 7 synthetic biology projects focused on mushroom cultivation and alternative protein production in 2024, signaling state-level commitment to innovation and market leadership according to Frontiers in Microbiology[2]Frontiers in Microbiology, "Synthetic biology enables mushrooms to meet emerging sustainable challenges", frontiersin.org.

Europe emerges as the fastest-growing region with 11.02% CAGR through 2031, driven by regulatory harmonization through EFSA's updated novel food guidance and rising consumer health consciousness that prioritizes natural ingredients over synthetic alternatives. The region's stringent quality standards create barriers for lower-quality imports while favoring local producers and established international suppliers with robust compliance capabilities. The European Food Safety Authority's approval of vitamin D2 mushroom powder as a novel food in 2024 establishes precedents for broader mushroom ingredient acceptance according to the European Food Safety Authority[3]European Food Safety Authority, "Safety of vitamin D2 mushroom powder", efsa.europa.eu.

North America maintains strong market positioning through innovation leadership and premium consumer segments, as younger demographics drive adoption across supplements and functional foods. South America and Middle East and Africa represent emerging opportunities with growing health consciousness and expanding distribution infrastructure, though regulatory frameworks remain less developed compared to established markets.

Competitive Landscape

The functional mushroom market remains fragmented. The major players include Nammex, M2 Ingredients, CNC Exotic Mushrooms, Layn Natural Ingredients and Hirano Mushroom LLC. A 2024 facility upgrade by Applied Food Sciences and KÄÄPÄ Biotech signals a race to elevate functional mushroom supply reliability through climate-controlled cultivation and automated harvesting.

Technology adoption emerges as a primary differentiator, with companies investing in supercritical CO2 extraction, synthetic biology platforms, and controlled environment agriculture to enhance bioavailability and production reliability. The industry's vertical integration trend accelerates as companies seek control over quality and supply chain reliability, with partnerships like Applied Food Sciences and KÄÄPÄ Biotech's cultivation facility expansion exemplifying strategic responses to supply volatility.

Emerging disruptors leverage synthetic biology and precision fermentation to produce mushroom compounds without traditional cultivation constraints, potentially disrupting established supply chains while addressing sustainability and consistency challenges. However, consumer acceptance of synthetic alternatives remains uncertain, creating strategic risks for companies abandoning natural positioning in favor of technological efficiency.

Functional Mushroom Industry Leaders

-

Nammex

-

CNC Exotic Mushrooms

-

Hirano Mushroom LLC

-

M2 Ingredients

-

Layn Natural Ingredients

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: KÄÄPÄ Biotech, a Finnish developer specializing in functional mushroom nutraceuticals, secured a EUR 900,000 investment from global fund manager PeakBridge. The funds will bolster KÄÄPÄ's efforts to expand its business, particularly in cultivation and regional research and development.

- March 2025: Fungi specialist M2 Ingredients has launched Myco-Suspend, a groundbreaking beverage solution. This innovation allows whole mushroom powders to stay suspended in drinks for longer durations. The introduction of Myco-Suspend comes as a direct answer to the surging demand in the booming functional mushrooms market. The solution guarantees the prolonged efficacy of full-spectrum whole mushroom powders, whether in hot or cold ready-to-mix beverages.

- February 2024: To cater to the rising demand for its premium organic functional mushroom products, M2 Ingredients, a top provider in the industry, has opened a state-of-the-art facility spanning 155,000 square feet. Equipped with advanced technology, this new facility boosts M2 Ingredients' capacity, enabling the company to promise the industry's shortest lead times for all ten of its premium mushroom species, such as Reishi, Lion's Mane, Cordyceps, and Turkey Tail.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study sizes the functional mushroom market as the worldwide value of finished ingredients and consumer-ready goods made from non-psychoactive species such as Reishi, Cordyceps, Lion's Mane, Shiitake, Chaga, and Turkey Tail, whose bioactive compounds are taken for immune, cognitive, metabolic, or cosmetic benefits. Tracked formats include powders, liquid extracts, capsules, food or beverage infusions, personal-care items, and pharmaceutical-grade products sold through retail or B2B channels.

Scope Exclusions: Cultivation inputs, fresh culinary mushrooms with no stated health claim, and all psilocybin varieties remain outside our coverage.

Segmentation Overview

-

Product Type

- Reishi

- Cordyceps

- Lions Mane

- Turkey Tail

- Shiitake

- Chaga

- Other Product Types

-

Nature

- Conventional

- Organic

-

Form

- Powder

- Liquid

- Others

-

Application

- Dietary Supplements

- Food and Beverage

- Personal Care

- Pharmaceutical

- Other Applications

-

Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts talk with cultivators, contract extractors, formulators, and distributors across Asia-Pacific, Europe, and North America, then survey naturopathic practitioners and functional-beverage start-ups. These dialogues verify raw-material availability, typical selling prices, and nascent use cases that desk work alone cannot surface.

Desk Research

We begin with UN FAO output data, customs portals that detail HS-code trade in mushroom extracts, and food-safety registers listing novel ingredient approvals. Price and usage trends are drawn from bodies such as the American Herbal Products Association and the European Food Supplements Federation, while peer-reviewed journals quantify beta-glucan yields by strain. Company filings, investor decks, and trusted media enrich context, and paid files from D&B Hoovers plus Dow Jones Factiva add revenue and deal signals. The sources named illustrate the breadth; many additional references guide each datapoint.

Market-Sizing & Forecasting

A top-down reconstruction starts with recorded production and trade. These volumes are adjusted for extraction yields and average selling prices to build our 2025 base. Selective bottom-up supplier roll-ups and channel checks benchmark the totals. Multivariate regression anchored on cultivated output, extract-conversion ratios, supplement penetration, dosage-form pricing, regulatory approvals, and e-commerce share projects value through 2030, while scenario analysis tests sensitivity to price shocks and rule changes.

Data Validation & Update Cycle

We run variance checks, compare outputs with shipment volumes and retail-audit pulses, then escalate anomalies for senior review. Reports refresh each year, and analysts add interim tweaks after material events.

Why Mordor's Functional Mushroom Baseline Commands Confidence

Published estimates often differ because firms choose wider product baskets, optimistic price curves, or longer refresh cadences.

We update inputs every twelve months, ground yields in laboratory data, and keep culinary-only sales out of scope, which tightens our number.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 12.09 B (2025) | Mordor Intelligence | - |

| USD 33.72 B (2025) | Global Consultancy A | Includes gourmet culinary sales and counts multiple dosage forms without yield adjustments |

| USD 34.75 B (2024) | Industry Journal B | Projects forward from 2023 with uniform prices and no fresh primary checks |

The comparison shows totals swell when broader scopes or static pricing are used. Our disciplined, transparently sourced approach offers decision-makers a balanced baseline tied to measurable variables and a rigorously maintained review cycle.

Key Questions Answered in the Report

How large is the functional mushroom market today?

The functional mushroom market size reached USD 13.20 billion in 2026 and is projected to hit USD 20.74 billion by 2031.

Which region leads the functional mushroom market?

Asia-Pacific leads with 33.66% revenue share, helped by mature cultivation networks and strong traditional-medicine usage.

Which mushroom species is growing fastest?

Cordyceps is forecast to expand at a 9.87% CAGR through 2031 due to robust demand in sports nutrition and endurance products.

Why are organic functional mushroom products gaining traction?

Consumers in Europe and North America accept 30-50% price premiums for certified pesticide-free extracts, pushing organic variants to an 11.76% CAGR.

Page last updated on: