Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

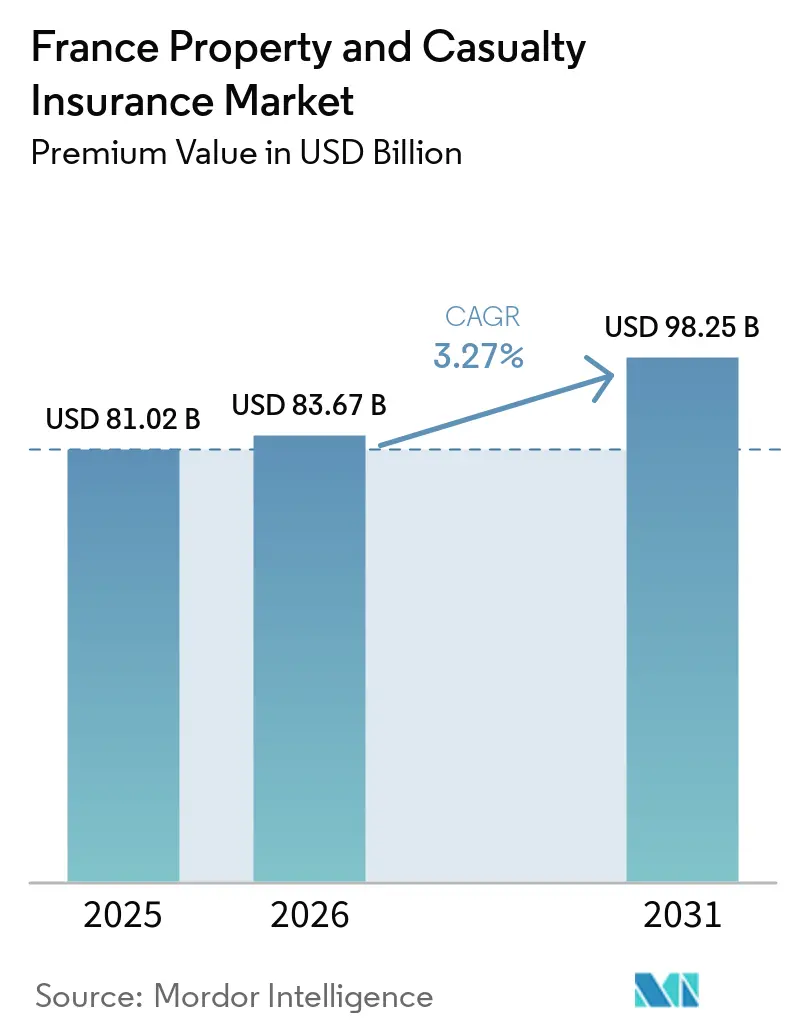

| Base Year Market Size (2025) | USD 81.02 Billion |

| Market Size (2026) | USD 83.67 Billion |

| Market Size (2031) | USD 98.25 Billion |

| Growth Rate (2026 - 2031) | 3.27% CAGR |

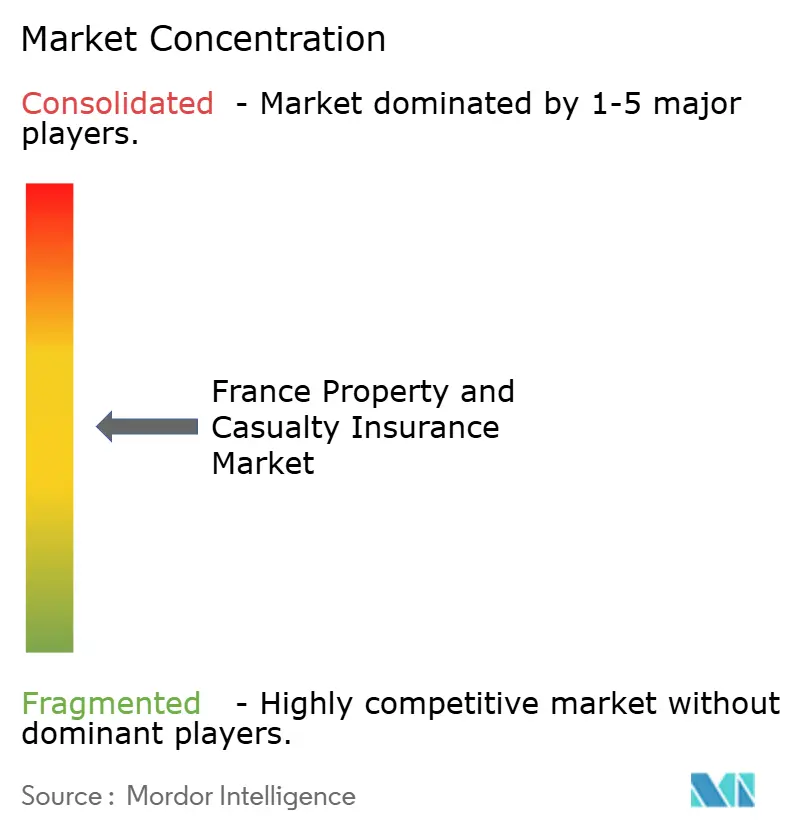

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Property and Casualty Insurance Market Analysis by Mordor Intelligence

The France Property And Casualty Insurance Market size in terms of premium value is projected to expand from USD 81.02 billion in 2025 and USD 83.67 billion in 2026 to USD 98.25 billion by 2031, registering a CAGR of 3.27% between 2026 to 2031.

This measured expansion reflects steady premium growth built on structural climate-risk pricing, mandatory coverage extensions, and rate hardening in commercial lines. Underwriting discipline in property segments offsets motor-insurance competition, while embedded distribution partnerships widen access to new premium pools. Regulatory initiatives, including the CatNat surcharge increase and DORA-driven resilience standards, provide supportive but costly guardrails. Sustained investment in digital claims automation and behavioral pricing allows incumbents to preserve margins even as insurtech challengers erode traditional agency advantages[1]Autorité de contrôle prudentiel et de résolution, “2024 Climate Stress-Test Results,” banque-france.fr.

Key Report Takeaways

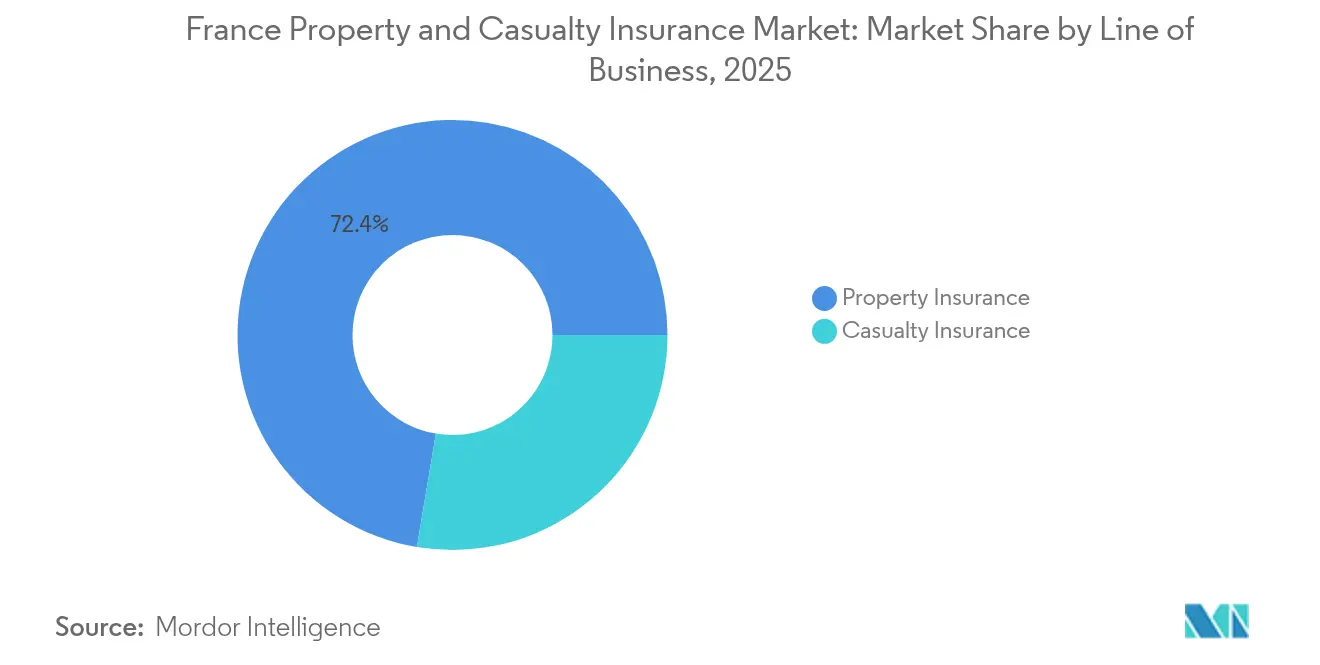

- By line of business, property insurance held 72.35% of the France Property and Casualty Insurance market share in 2025, while casualty insurance is projected to expand at a 3.95% CAGR to 2031.

- By distribution channel, the direct model accounted for 46.25% of the France Property and Casualty Insurance market size in 2025; affinity partnerships and embedded platforms represent the fastest trajectory with a 4.55% CAGR through 2031.

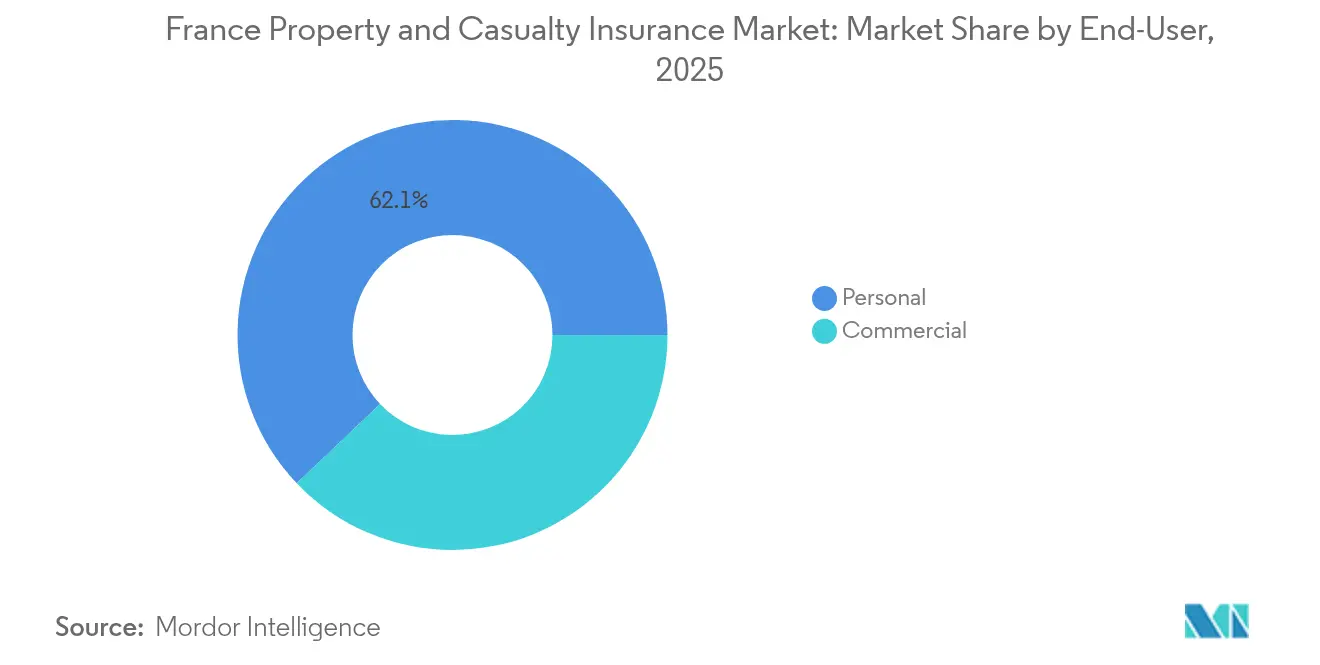

- By end-user, personal lines kept a 62.10% share of the France Property and Casualty Insurance market size in 2025, whereas commercial lines are tracking a 3.69% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

France Property and Casualty Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising frequency & severity of climate-related catastrophes | +1.2% | National, with concentrated exposure in flood-prone regions | Long term (≥ 4 years) |

| Persistent hard-market rate increases in commercial lines | +0.8% | National, with emphasis on urban commercial centers | Medium term (2-4 years) |

| Mandatory insurance expansion into new risk classes | +0.5% | National, driven by regulatory requirements | Medium term (2-4 years) |

| Digitalization & usage-based motor insurance adoption | +0.4% | National, with urban concentration | Short term (≤ 2 years) |

| Parametric micro-insurance growth for SMEs & agriculture | +0.3% | Rural and agricultural regions primarily | Long term (≥ 4 years) |

| Embedded insurance via e-commerce ecosystems | +0.3% | National, with e-commerce platform integration | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising frequency & severity of climate-related catastrophes

France experienced EUR 10.6 billion (USD 11 billion) in insured losses in 2022 and EUR 6.5 billion (USD 6.7 billion) in 2023, establishing a new baseline for annual exposure. Subsidence from drought-induced soil shrinkage alone is expected to trigger EUR 43 billion in claims during 2020-2050, shifting the loss pattern from episodic flooding to chronic structural damage. The 2025 CatNat surcharge hike from 12% to 20% embeds premium inflation that lifts the France Property and Casualty Insurance market, even as volumes stabilize. ACPR’s 2024 climate stress test demonstrates regulatory focus on capital adequacy under adverse weather scenarios. Insurers are therefore revising catastrophe models, increasing reinsurance cessions, and investing in satellite-based risk monitoring to refine underwriting granularity.

Persistent hard-market rate increases in commercial lines

Commercial segments have posted annual rate rises of 5-8% since 2023 as carriers recapture profitability after years of underpricing[2]AXA Group, “Full-Year 2024 Results,” axa.com. Capacity withdrawal by global reinsurers tightens supply, reinforcing discipline across fire, cyber, and professional indemnity covers. Combined ratios have improved, with Groupama reporting 96.8% in 2024 versus triple-digit levels two years earlier. Larger accounts face higher retentions, fueling demand for parametric top-up products that pay out on predefined triggers. While rising prices buoy the France Property and Casualty Insurance market, they also entice digital insurers that promise leaner cost structures and selective underwriting on standard risks.

Mandatory insurance expansion into new risk classes

Civil-Code reforms effective 2025 widen compulsory coverage to cyber and broaden professional liability, adding an estimated 6% to commercial premium volume according to government consultation papers. Cyberattacks hit 54% of French firms in 2021, yet cyber insurance comprised only 3% of premiums in 2024, leaving a sizable protection gap. Regulatory compulsion, therefore, creates captive demand, cushioning the France Property and Casualty Insurance market against economic slowdowns. However, compliance costs weigh heavily on SMEs, encouraging pooled purchasing and embedded micro-covers distributed via accounting platforms. Carriers that build modular policies and digital onboarding pathways secure early-mover advantages.

Digitalization & usage-based motor insurance adoption

Telematics programs such as YouDrive grew 27% year on year, delivering average annual savings of EUR 200 (USD 208.3) to participants. Real-time driving data fosters fairer pricing, reducing anti-selection and cutting claims frequency. Open-banking APIs now allow instant policy retrieval and pre-filled quotes, trimming acquisition costs across direct channels. Even so, privacy-conscious consumers remain wary of data sharing, limiting penetration to price-sensitive demographics. For insurers, usage data extends beyond rating to crash detection and automated FNOL, shrinking loss-adjustment expenses and accelerating settlement times.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying motor-insurance price competition | -0.6% | National, with urban market concentration | Short term (≤ 2 years) |

| Legacy low-interest-rate drag on investment returns | -0.4% | National, affecting all major insurers | Long term (≥ 4 years) |

| Rising consumer litigation & claims disputes | -0.3% | National, with judicial system constraints | Medium term (2-4 years) |

| Talent shortage in actuarial & cyber-risk underwriting | -0.2% | National, with skills concentration in major cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Intensifying motor-insurance price competition

Average motor premiums rose just 5% to EUR 545 (USD 567.6) in 2025, lagging claims inflation as digital comparison platforms push commoditization[3]LeLynx.fr, “Motor Premium Index 2025,” lelynx.fr. Entrants like Lovys promote policies from EUR 3.99 (USD 4.15) a month, leveraging cloud-native operations to cut distribution costs. Regulatory constraints on risk-based pricing inhibit granular differentiation, while repair-cost inflation squeezes underwriting margins. Carriers respond by cross-selling ancillary covers and loyalty perks, yet profitability remains fragile. Smaller mutuals with mono-line motor portfolios face the greatest strain, prompting mergers or niche refocusing.

Legacy low-interest-rate drag on investment returns

Although new-money yields improved in 2025, legacy portfolios still reflect a decade of near-zero rates, capping reinvestment income. Euro-fund inflows reached EUR 13.9 billion (USD 14.4 billion) in May 2025, but yields of 2.5-3.5% trail long-term targets[4]Groupe BPCE, “Monthly Savings and Insurance Dashboard May 2025,” groupebpce.com. Unrealized gains on real-estate holdings fell 20% from 2023 valuations, and rising solvency capital charges for equities constrain allocation flexibility. Larger groups offset pressure through infrastructure debt and private-credit mandates, while smaller players lack scale for diversified alternatives. Consequently, investment drag dilutes the France Property and Casualty Insurance market’s overall return on equity despite underwriting gains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Line of Business: Property Dominance Amid Casualty Acceleration

In 2025, property covers generated 72.35% of total premiums, underscoring their foundational role in the France Property and Casualty Insurance market. Rate hikes linked to the CatNat surcharge and higher construction-cost indices underpin revenue momentum, even as insured values plateau. Casualty lines, representing a smaller base, deliver the fastest growth at a 3.95% CAGR, propelled by cyber liability and widened professional indemnity mandates. Residential property remains buoyant due to compulsory mortgage insurance and subsidized catastrophe protection schemes. Commercial property adds breadth through supply-chain-triggered parametric clauses that pay within 72 hours of a qualifying event.

Cyber liability is the standout casualty sub-line, doubling premium volume between 2023 and 2025, yet still only 3% of commercial property and casualty totals, leaving significant headroom. Professional liability reforms in 2025 add immediate uplift, while workers’ compensation sees incremental growth tied to payroll expansion. Agricultural parametric covers, distributed via farm-equipment dealers, speed payouts for drought and frost, enhancing rural resilience. Together, these dynamics reinforce the France Property and Casualty Insurance market’s balanced growth profile and hedge cyclical exposure to single-line shocks.

By Distribution Channel: Direct Dominance Faces Embedded Disruption

Direct sales captured 46.25% of 2025 premium inflows, benefitting from strong brand recognition and sustained investment in omnichannel service. Online journeys now close 65% of new personal-lines sales for leading carriers, driving cost-to-acquire below EUR 50 per policy. Embedded and affinity channels, however, are scaling rapidly at a 4.55% CAGR, inserting protection into retail, fintech, and mobility ecosystems. Carrefour’s “Garantie Pouvoir d’Achat” offers voyage and household covers at checkout, increasing attachment rates and underscoring the power of context-rich distribution. Wakam’s Play&Plug reaches 32 countries with white-label APIs, confirming France’s position as a continental hub for insurance-as-a-service.

Broker networks defend relevance in complex commercial placements, especially where multi-year programs and captives interplay. Bancassurance retains clout; Groupe BPCE logged 10% non-life premium growth in Q1 2025, illustrating the cross-sell leverage of existing banking relationships. Overall, competitive tension across channels sharpens value propositions and accelerates digital investment, sustaining France Property and Casualty Insurance market expansion.

By End-User: Personal Lines Stability Versus Commercial Growth

Personal lines held 62.10% in 2025, anchored by mandatory motor and homeowners covers, and delivered predictable cash flows that underpin capital planning. Premium upticks hinge chiefly on CatNat pass-through and telematics adoption. Commercial lines, by contrast, expand at 3.69% CAGR to 2031 as French SMEs digitize operations and confront new cyber and supply-chain exposures. Parametric micro-covers priced below EUR 1,000 (USD 1,041.5) per annum resonate with small firms seeking liquidity over indemnity.

Large corporates drive bespoke multi-tower programs blending traditional indemnity layers with catastrophe bonds and specialty captives. The convergence of personal and commercial journeys surfaces in embedded propositions where gig-economy workers buy liability protection alongside payments apps. Such overlap supports portfolio diversification, enhances customer lifetime value, and fortifies the France Property and Casualty Insurance market against single-segment cyclical swings.

Geography Analysis

In Île-de-France and Auvergne-Rhône-Alpes, half of all written premiums are concentrated, reflecting the alignment with regional population density and economic activity. Urban centers play a pivotal role in driving demand for commercial specialties, which, in turn, leads to larger average policy sizes. Mediterranean départements face heightened risks of wildfires and droughts, necessitating higher deductibles and CatNat surcharges. Meanwhile, northern river basins remain vulnerable to flooding, prompting insurers to adopt adjustable deductibles and implement early-warning monitoring services. Although catastrophe-prone areas experience premium differentials of up to 40% compared to low-risk regions, regulatory frameworks ensure balanced pricing to maintain affordability and market stability.

Rural regions, despite significant asset exposure, continue to face under-insurance challenges. To address this gap, parametric agriculture programs, delivered through cooperatives and supported by public-private co-funding, are proving effective. These programs provide tailored solutions to mitigate risks in rural areas. Additionally, the 2025 rollout of DORA introduces uniform resilience standards, favoring insurers with centralized technology hubs over regionally dispersed mutuals. This regulatory shift is expected to enhance operational efficiency and resilience across the insurance landscape, particularly benefiting larger players with advanced technological infrastructure.

While EU passporting facilitates cross-border sales, domestic brands maintain a competitive edge due to their familiarity with local language, claims-handling processes, and established consumer trust. These factors create barriers for foreign entrants despite regulatory allowances. The proposed asset-management collaborations between BPCE and Generali highlight the importance of scale in navigating multi-jurisdictional compliance and optimizing capital allocation. Collectively, these geographic and regulatory nuances shape distribution strategies and product customization, driving the evolution of the French Property and Casualty Insurance market.

Competitive Landscape

Market leadership rests with AXA, Covéa, Groupama, Allianz France, and Crédit Mutuel Assurances, whose combined heft shapes pricing and innovation agendas. AXA recorded 7% P&C premium growth in 2024, divested non-core asset-management holdings for EUR 5.4 billion (USD 5.6 billion), and acquired a 51% stake in insurtech platform Prima in 2025 to reinforce digital distribution. Covéa invested in AI-powered claims automation that cut average handling time by 25%, while Groupama strengthened regional networks to safeguard agricultural shares. These incumbents’ vast customer bases and balanced product portfolios create efficient capital allocation and underwriting clout across the France Property and Casualty Insurance market.

Mid-tier mutuals, including MAIF and MACIF, pursue niche positioning and community loyalty to resist commoditization, emphasizing ESG-aligned products and member dividends. Insurtech challengers such as Wakam, Lovys, and Neat focus on usage-based, subscription, or embedded models, leveraging low-code platforms to launch propositions within weeks. Although their gross written premium remains under 3% of the France Property and Casualty Insurance market, rapid funding inflows and partnerships with e-commerce giants threaten entrenched distribution structures.

Technology capability is the critical battleground. Investment in predictive analytics, IoT-enabled loss prevention, and omnichannel self-service improves combined ratios and customer retention. ACPR’s DORA enforcement elevates cybersecurity and continuity spending, advantaging scale players that can amortize costs. Meanwhile, reinsurer capacity constraints and climate uncertainty steer carriers toward strategic alliances for retrocession and data-sharing, deepening ecosystem collaboration and sharpening competitive differentiation across the France Property and Casualty Insurance market.

France Property and Casualty Insurance Industry Leaders

AXA France

Covéa (MAAF, MMA, GMF)

Groupama

Macif

Allianz France

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: AXA acquired a 51% stake in Prima to accelerate technology-enabled customer acquisition and strengthen embedded-insurance partnerships.

- June 2025: AXA executed a EUR 724.6 million (USD 754.7 million) share repurchase to neutralize equity-based compensation dilution, signaling robust capital generation.

- January 2025: BPCE and Generali agreed to form a 50/50 asset-management joint venture overseeing EUR 1.9 trillion (USD 1.97 trillion), enhancing cross-sell collaborations for non-life affiliates.

- May 2024: ACPR unveiled the findings of its second climate stress test for the insurance sector, setting clear supervisory benchmarks for managing climate risks and ensuring capital adequacy in challenging scenarios.

France Property and Casualty Insurance Market Report Scope

The French property & casualty insurance market is one of the most widely demanded property & casualty insurance markets as people are keen to get secure and have a protective shield to fulfill their aims after a casualty or any property loss. A complete background analysis of the French property & casualty insurance market, which includes an assessment of the economy, market overview, market size estimation for key segments, emerging trends in the market, market dynamics, and key company profiles, is covered in the report.

The French property & casualty insurance market is segmented by policy type and distribution channel. By policy type, the market is sub-segmented into car insurance - personal and commercial, condo insurance, homeowner insurance, renters insurance, and others. By distribution channel, the market is sub-segmented into direct, banks, agents, brokers, and others. The report offers the market sizes and forecasts in value (USD) for all the above segments.

By Line of Business

| Property Insurance | Residential Property Insurance |

| Motor Insurance | |

| Commercial Property Insurance | |

| Agricultural Property Insurance | |

| Casualty Insurance | General Liability |

| Professional Liability | |

| Workers’ Compensation | |

| Cyber Liability |

By Distribution Channel

| Direct (Online & Agency) |

| Brokers |

| Bancassurance |

| Affinity Partnerships & Embedded Platforms |

By End-User

| Personal |

| Commercial |

| By Line of Business | Property Insurance | Residential Property Insurance |

| Motor Insurance | ||

| Commercial Property Insurance | ||

| Agricultural Property Insurance | ||

| Casualty Insurance | General Liability | |

| Professional Liability | ||

| Workers’ Compensation | ||

| Cyber Liability | ||

| By Distribution Channel | Direct (Online & Agency) | |

| Brokers | ||

| Bancassurance | ||

| Affinity Partnerships & Embedded Platforms | ||

| By End-User | Personal | |

| Commercial | ||

Key Questions Answered in the Report

What is the current value of the France Property and Casualty Insurance market?

The France Property and Casualty Insurance market size is USD 83.67 billion in 2026.

How fast is the France Property and Casualty Insurance market expected to grow?

It is projected to expand at a 3.27% CAGR, reaching USD 98.25 billion by 2031.

Which line of business is growing fastest within French P&C?

Casualty insurance, led by cyber liability and professional-indemnity reforms, is advancing at a 3.95% CAGR.

Which distribution channel is gaining the most momentum?

Affinity partnerships and embedded platforms are growing at a 4.55% CAGR, outpacing direct and broker channels.

How will climate change influence French P&C premiums?

Higher CatNat surcharges and rising catastrophe losses embed structural premium inflation that underpins long-term market growth.

What role do insurtech companies play in France?

Insurtechs such as Wakam and Lovys leverage embedded models and low-cost operations to capture niche segments and challenge incumbent distribution.

Page last updated on: