Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

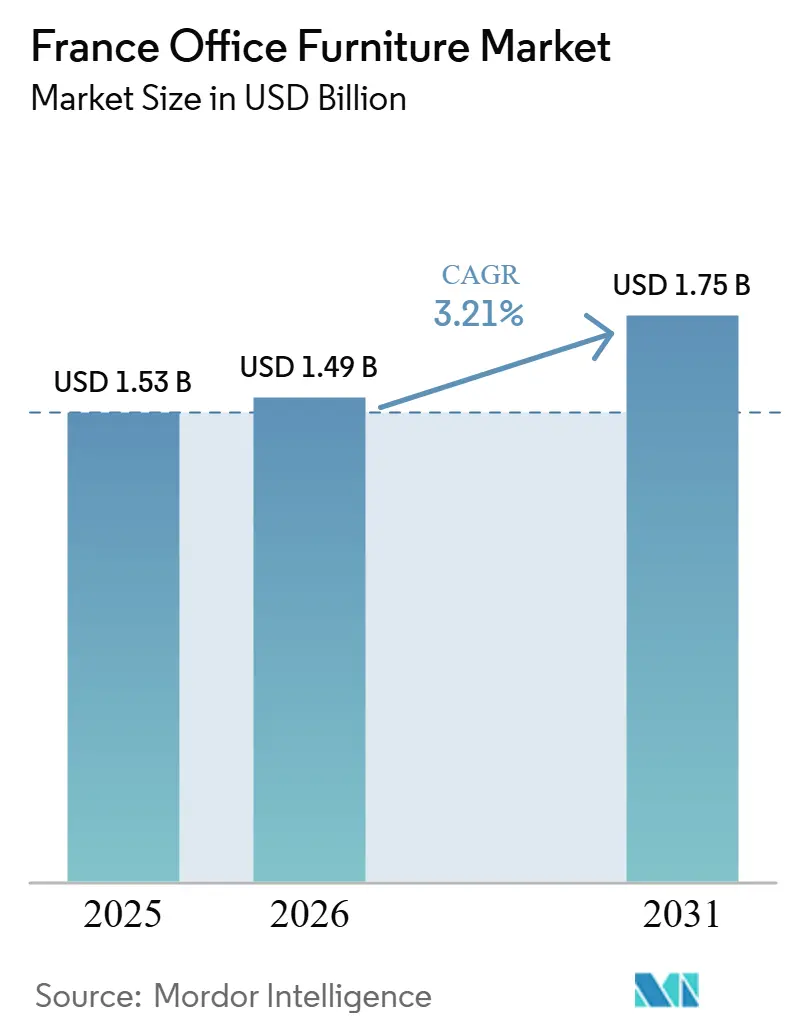

| Base Year Market Size (2025) | USD 1.53 Billion |

| Market Size (2026) | USD 1.49 Billion |

| Market Size (2031) | USD 1.75 Billion |

| Growth Rate (2026 - 2031) | 3.21% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Office Furniture Market Analysis by Mordor Intelligence

The France office furniture market size is expected to grow from USD 1.74 billion in 2025 to USD 1.87 billion in 2026 and is forecast to reach USD 2.31 billion by 2031 at 4.32% CAGR over 2026-2031. This outlook reflects how sustainability rules and post-pandemic workspace redesign continue to shape buying decisions in 2026. Circular-economy mandates to steer public procurement toward second-hand and recycled-content items are changing the way manufacturers design, certify, and price their lines. Product mix is shifting as hybrid work stabilizes demand for booths, acoustic solutions, and modular dividers that support privacy and fast reconfiguration. Premium specifications are gaining traction in consolidated headquarters projects, while take-back and remanufacturing programs reduce lifecycle costs and help buyers comply with reporting obligations. The result is a France office furniture market that rewards traceability, environmental documentation, and flexible service models over one-time capital purchases.

Key Report Takeaways

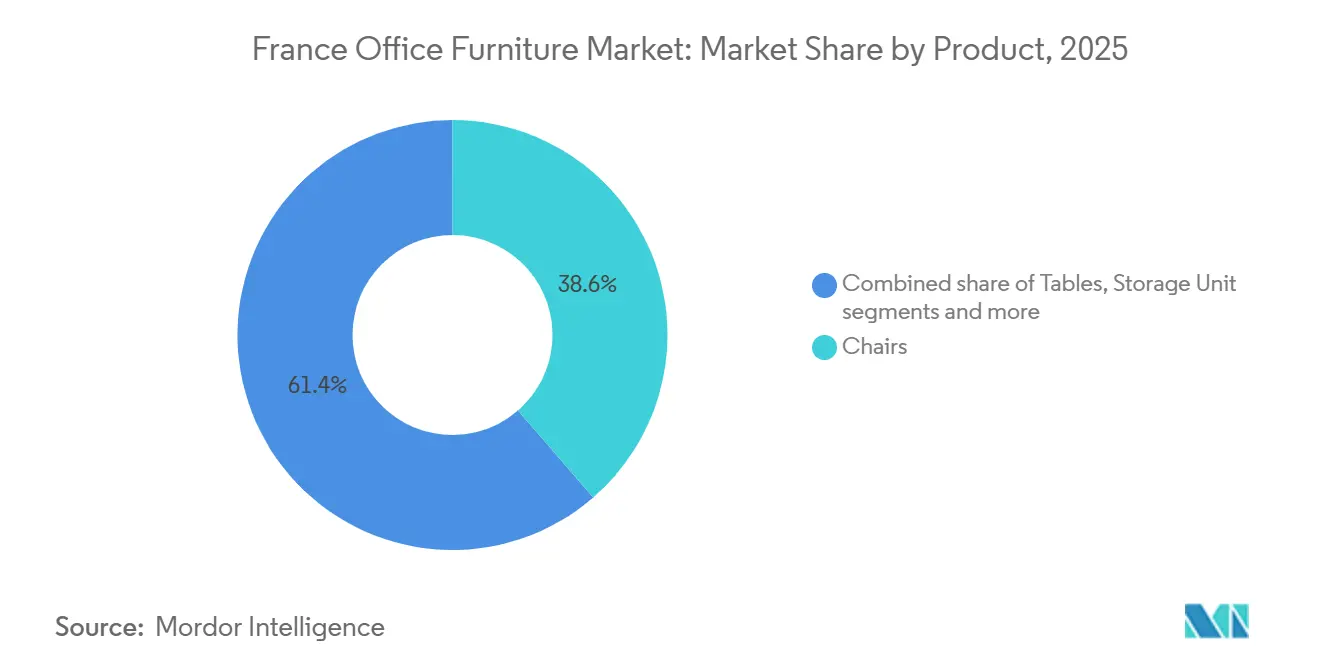

- By product category, chairs led with a 38.64% of the France office furniture market share in 2025. Booths and office dividers are the fastest-growing product category, with a 6.74% CAGR through 2031.

- By material, wood accounted for 44.82% of the France office furniture market size in 2025. Plastics and polymers are the fastest-growing materials, with a 6.12% CAGR through 2031.

- By price range, mid-range products held 49.37% of the France office furniture market share in 2025. The premium products price tier is the fastest growing, with a 6.89% CAGR through 2031.

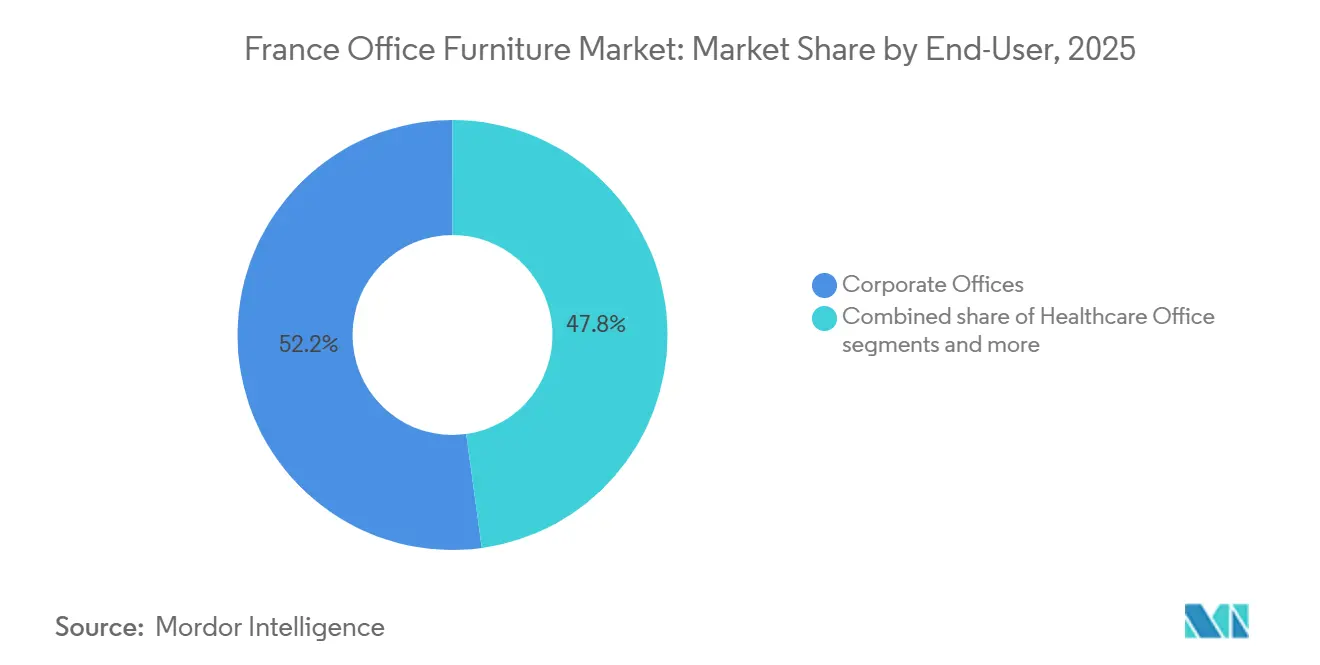

- By end-user, corporate offices accounted for 52.18% of the France office furniture market share in 2025. Healthcare offices are the fastest-growing end-user, with a 6.43% CAGR through 2031.

- By distribution channel, B2B direct sales commanded a 57.26% of the France office furniture market share in 2025. Online B2C is the fastest-growing distribution route, with a 7.14% CAGR through 2031.

- By geography, Île-de-France captured 34.71% of the France office furniture market share in 2025. Auvergne-Rhône-Alpes is the fastest-growing region, with a 5.94% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

France Office Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tertiary Decree-driven office refurbishments and space reconfiguration | +0.9% | Île-de-France core, spillover to Auvergne-Rhône-Alpes | Medium term (2-4 years) |

| EPR and AGEC procurement quotas accelerate reuse, take-back, and remanufactured buying | +1.2% | National, with early gains in Paris, Lyon, Marseille | Short term (≤ 2 years) |

| Flight-to-quality and prime fit-outs sustain ergonomic and collaborative investments | +0.8% | Paris CBD, secondary Paris business districts | Long term (≥ 4 years) |

| CSRD-driven material transparency and low-VOC/recycled specifications | +0.7% | National, compliance-driven in corporate offices | Medium term (2-4 years) |

| Circular services (remanufacture, buy-back) reduce TCO and unlock budgets | +0.6% | National, accelerated adoption in the public sector | Medium term (2-4 years) |

| Hybrid work boosts demand for booths, acoustic solutions, and flexible zoning | +1.0% | Île-de-France core, spillover to major cities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Tertiary Decree-driven Office Refurbishments and Space Reconfiguration

The Tertiary Decree sets staged energy-reduction goals for large tertiary buildings, which brings new specifications into interior refresh projects. Landlords and tenants update lighting, partitions, and integrated sensor hardware as part of modernization programs, and these changes often trigger the replacement of legacy desks and storage systems. These projects favor modular systems with traceable materials and recognized certifications, which streamline approvals for corporate and public tenders. A 2025 case from Kinnarps in Aix-en-Provence illustrates the scale of integrated acoustic and biophilic furniture supplied for a regional headquarters program, highlighting how fit-out updates align with energy and airflow considerations in the built environment[1]KINNARPS.COM https://www.kinnarps.com/client-cases/groupama-mediterranee/.. This regulatory context benefits suppliers that can document environmental performance and adjust layouts in phases without disrupting building operations.

EPR and AGEC Procurement Quotas Accelerate Reuse, Take-Back, and Remanufactured Buying

France’s Extended Producer Responsibility (EPR) and the French AGEC (Anti-Waste for a Circular Economy) framework require public buyers to source a minimum portion of office furniture from second-hand and recycled-content channels, thereby redirecting a significant volume into certified reuse streams. Ecomaison has committed multi-year funding to expand reuse and refurbish capacity and reports a high overall recovery rate across furniture flows that supply recycled wood and materials back to manufacturers. This program is supported by a nationwide network of social-economy partners that collect, triage, and route returns to refurbishers with auditable records. Manufacturers align with this policy by publishing Environmental Product Declarations, expanding recycled content in flagship products, and qualifying for eco-modulation bonuses that reward local, post-consumer sourcing of plastics and foam within defined distances from production sites. Product-level disclosures such as NSF-certified EPDs for chairs made in France are now routine in public tenders and help streamline compliance checks.

Flight-to-Quality and Prime Fit-Outs Sustain Ergonomic and Collaborative Investments

As tenants consolidate into higher-quality buildings, project briefs emphasize ergonomic chairs, height-adjustable desks with integrated cable management, and collaborative seating clusters that support hybrid meeting patterns. These specifications require recognized quality and environmental marks, and suppliers with the right labels are at an advantage in both public and private competitions. Nowy Styl holds multiple French NF Office Excellence and NF Environnement certifications across product lines, which positions the company well for projects where documentation is a gating factor. BURONOMIC extended its warranty coverage from five to ten years and expanded its showroom presence to support decisions that weigh lifecycle assurance alongside fit-out aesthetics[2]Buronomic, “Company Overview and 2026 Catalog,” Buronomic, buronomic.fr. This emphasis on certified ergonomics and durable construction supports a premiumization trend that lifts the France office furniture market in Paris CBD and core business districts.

CSRD-driven Material Transparency and Low-VOC/Recycled Specifications

Large European firms are preparing to report scope-3 emissions, and procurement teams now request Environmental Product Declarations (EPD), recyclability data, and low-VOC documentation at the line-item level. Manufacturers have responded with product passports and EPDs that detail recycled content and emissions profiles, easing the path through ESG questionnaires in RFPs. Steelcase publishes EPDs for its France-made chairs and aligns those disclosures with recognized third-party certifications that verify recycled content and air-quality performance. Sedus maintains EcoVadis and SA8000 certifications, reducing friction in compliance reviews and social responsibility checks. These documentation practices create a structural moat for incumbents that have invested in testing and certification capacity, supporting the steady expansion of the France office furniture market in corporate accounts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Weak office leasing and take-up delays with new fit-outs | -0.9% | Île-de-France, Hauts-de-France | Short term (≤ 2 years) |

| Input cost volatility (wood, metal, upholstery) pressures pricing and margins | -0.7% | National | Medium term (2-4 years) |

| EPR and AGEC labeling compliance burden slows non-compliant procurement | -0.4% | National, with stricter enforcement in the public sector | Short term (≤ 2 years) |

| Limited local recycling capacity for mixed plastics and upholstery constrains circularity | -0.3% | National, concentrated in Nouvelle-Aquitaine, Hauts-de-France | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Weak Office Leasing and Take-Up Delays New Fit-Outs

Weak leasing activity extends the timeline for tenant improvements, slowing large-scale furniture orders tied to move-ins and new layouts. Occupiers also hedge commitments with shorter-term leases and flex memberships, reducing the share of projects that require full-floor fit-outs. As a result, volume can shift from traditional desking toward modular, rental-ready solutions that accommodate variable occupancy. Suppliers with furniture-as-a-service and phased-delivery options are better positioned in this environment because they fit tighter budgets and timeline uncertainty. These dynamics weigh on the France office furniture market in the near term but favor providers with flexible programs and certified circular channels that can redeploy assets efficiently.

Input Cost Volatility (Wood, Metal, Upholstery) Pressures Pricing and Margins

Raw material costs remain a pressure point, especially when weather events and supply constraints affect wood feedstock and when energy pricing affects metal frames and hardware. EU sustainability policies and deforestation rules increase the need for verifiable sourcing and chain-of-custody tracking, thereby raising compliance costs for manufacturers and their suppliers. These requirements lead some buyers to prioritize certified timber and higher recycled content in metals and plastics to meet reporting thresholds. Rising input variability also strengthens the case for circular inputs sourced through national recovery programs that shorten logistics and reduce exposure to virgin-material markets. Together, these factors encourage a gradual shift in specifications while manufacturers work to maintain pricing discipline and on-time delivery in the France office furniture market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Chairs Lead Share While Acoustic Solutions Capture Hybrid-Work Growth

Chairs accounted for 38.64% of the French office furniture market in 2025, reflecting the foundational role of ergonomic seating in workstation standards. Booths and office dividers are projected to grow at a 6.74% CAGR through 2031, the fastest among product categories, as hybrid work cements demand for focus zones and reconfigurable collaboration spaces. This mix supports a steady refresh cycle where high-use seating anchors budgets and acoustic solutions absorb incremental spending to improve mid-week productivity. New product families emphasize safety and ergonomics, including height-adjustable desks with anti-collision and memory settings that align with common workstation guidelines. Premium amenity areas in major business districts continue to support soft seating, lounge tables, and movable partitions that refresh the look and function of shared spaces.

Active supplier roadmaps back the category leader in fast growth. Buronomic expanded its range in 2025 with an acoustic booth line to meet spontaneous meeting and private call needs in open-plan offices. Sedus introduced collaborative and acoustic systems that reduce ambient noise and simplify space reconfiguration across zones. Nowy Styl’s Orgatec lineup added electric desks and recyclable aluminum chair frames, reflecting the shift toward safe, certifiable mechanisms and circular-ready materials. Bene complemented the trend with modular sofas and recycled-polypropylene chairs that align with AGEC procurement briefs focused on material recovery and verifiable recycled inputs. These developments reinforce a product mix that supports the France office furniture market as offices balance collaboration and quiet work in the same footprint.

By Material: Wood Dominates Despite Disruptions, Plastic and Polymer Gains Accelerate

Wood retained a 44.82% share in the France office furniture market in 2025, underpinned by design preferences and strong brand positioning. Plastics and polymers are the fastest-growing materials, expanding at a 6.12% CAGR through 2031 as buyers combine circular-economy goals with durability and ease of maintenance. EU sustainability policies and due diligence rules increase costs for non-certified timber and raise demand for accurate origin documentation, favoring FSC and PEFC pathways in new bids. Metal remains stable as aluminum frames and steel structures benefit from mature recycling channels and consistent quality in modular systems. In this context, plastic and polymer blends with higher recycled content help buyers satisfy environmental criteria without sacrificing performance or cost control[3]European Environment Agency, “Waste Prevention Index,” European Environment Agency, eea.europa.eu.

Circular economic incentives nudge material choices. Ecomaison’s eco-modulation framework rewards manufacturers that use post-consumer PP, HDPE, ABS, and PU foam sourced within set distances, thereby strengthening local loops and reducing supply-chain transport emissions. Bene’s 100% recycled polypropylene chair and Flokk’s high-recycled-content seating demonstrate how product lines can pivot to documented circular inputs while preserving ergonomics and durability. Manufacturers also adjust lamination, finishing, and textile selection to streamline recycling at the end of life, often by reducing mixed-material assemblies and using standard fasteners or modular panels. These shifts align with public tenders that value transparent material data and reward products with proven recyclability and low VOC credentials. Together, they reinforce material innovations that lift the France office furniture market over the forecast horizon.

By Price Range: Mid-Range Leads, Premium Captures Flight-to-Quality Spend

Mid-range products accounted for 49.37% of sales in 2025, reflecting consistent demand from organizations balancing functionality, warranty coverage, and per-station budgets. Premium lines are the fastest-growing tier, with a 6.89% CAGR through 2031, as consolidated headquarters and serviced-office suites specify higher-grade ergonomics, modular collaboration zones, and longer warranties to achieve predictable lifecycle costs. Buyers compare total ownership across five to ten years and increasingly integrate trade-in credits or remanufactured components to manage spending. Premium kits emphasize advanced ergonomic features, consistent surface durability, and test acoustics in shared spaces. This tilt toward premium projects supports broader growth in the France office furniture market, particularly where fit-out packages underpin tenant experience and retention in core districts.

Suppliers are differentiating on services and documentation as much as on design. Buronomic’s longer warranty is one example of lifecycle assurance that appeals to project planning, staged refreshes, and sustained use. Haworth’s second-life credits ease upgrade paths, build customer loyalty, and reduce waste, thereby lowering effective ownership costs over a multi-year horizon. EOL’s reuse program complements this approach with take-back, refurbishment, and credit allocation for new ergonomic purchases. These strategies, combined with rising documentation standards, keep premium-focused vendors well placed as the France office furniture industry expands its service layer and account retention models.

By End-User: Corporate Offices Dominate, Healthcare Accelerates with Modernization Mandates

Corporate offices accounted for 52.18% of the market in 2025, making them the largest end-user segment in the France office furniture market. Healthcare offices are the fastest-growing sector, with a 6.43% CAGR through 2031, supported by clinic expansions, telemedicine rooms, and stricter indoor air-quality standards for administrative areas. Corporate projects now emphasize collaboration assets, adaptable meeting spaces, and ergonomic seating as hybrid work stabilizes. Education maintains a steady demand for durable, repairable products and is shifting toward refurbished options in budget-constrained institutions. Government and public sector buyers reinforce demand for certified reuse and recycled-content furniture under national EPR obligations, which routes volume through established collection and refurbishment networks.

Healthcare programs often require low-VOC surfaces, easily cleanable upholstery, and modular components that simplify maintenance and reconfiguration. Corporate buyers use showrooms and pilots to validate acoustic performance and durability before scaling a standard across floors or buildings. Manufacturers respond with clearer product data sheets, more extensive EPD coverage, and transparent warranty terms to lower perceived risk in high-utilization settings. As a result, the specification and approval process favors vendors with recognized certifications and complete documentation sets. These patterns support steady demand across enterprise, public, and healthcare accounts in the France office furniture market through 2031.

By Distribution Channel: B2B Direct Dominates, Online B2C Captures SME Growth

B2B direct sales from manufacturers accounted for 57.26% in 2025, reflecting the complexity of projects that require specification support, phased delivery, and on-site installation. Online B2C is the fastest-growing channel, with a 7.14% CAGR through 2031, as small firms and startups buy modular, quick-ship items to individualize shared spaces and manage shorter commitments. Specialty retailers and design galleries continue to play a role in curation and consultation, especially for projects that seek multi-brand vignettes. B2B advantages include logistics reach, service-level agreements, and warranty administration that are difficult for purely retail channels to replicate at scale. These strengths support the continued dominance of B2B channels while e-commerce expands access and transparency in the France office furniture market.

Network coverage and delivery speed are decisive factors in large orders. EOL Group operates a central warehouse and multiple regional platforms in France, providing short lead times for standard orders and predictable installation windows for multi-site rollouts. Buronomic’s digital catalogs support remote specification and reduce the need for repeated in-person visits, lowering acquisition costs and compressing decision timelines. Manufacturers also invest in showrooms that allow project teams to test ergonomics, acoustics, and finishes before making volume commitments. These enhancements smooth the buyer journey and reinforce the channel mix that underpins the France office furniture market into the next cycle.

Geography Analysis

Île-de-France accounted for 34.71% of revenue in 2025, reflecting the concentration of corporate headquarters, premium buildings, and large occupier projects in and around Paris. The region’s fit-out programs prioritize certified ergonomics, acoustic privacy, and modular collaboration zones that support variable attendance across the week. As tenants focus on quality, budgets for well-documented furniture lines and extended warranties remain resilient in core districts. This focus on amenity and lifecycle value reinforces demand for suppliers with comprehensive certifications and service options. The region’s scale and specification intensity keep it central to the France office furniture market, even as other regions add share over time.

Auvergne-Rhône-Alpes is the fastest-growing region, with a projected 5.94% CAGR through 2031, supported by a strong corporate presence in Lyon and a diverse base of tech and research hubs across the region. Regional headquarters and multi-site expansions support investments in ergonomic seating, focus pods, and collaborative furnishings for mixed-use floors. Suppliers cite growing interest in modular systems that can be moved between sites and floors without extensive building work, reducing downtime. Southern regions, including Provence-Alpes-Côte d’Azur, also see steady investment in furniture tied to regional headquarters and services clusters, where climate and lifestyle factors align with employee expectations. These regional dynamics broaden the demand base and reduce reliance on single-market cycles in the France office furniture market.

Manufacturing hubs and national logistics coverage provide additional support for regions outside the Paris area. Domestic brands leverage French production and established distribution platforms to shorten lead times for regional projects and to support post-sale service. Reusing channels maintained by eco-organizations helps public buyers across regions meet EPR quotas by documenting take-back and refurbishment, generating a predictable flow in secondary cities and towns. Showrooms and digital tools let buyers preview materials, seating ergonomics, and acoustic performance, both remotely and in person, helping close projects without long travel. These elements sustain geographic diversification for the France office furniture market as it grows into 2031[4] ECOMAISON.COM https://www.ecomaison.com/en/prevention-reuse/..

Competitive Landscape

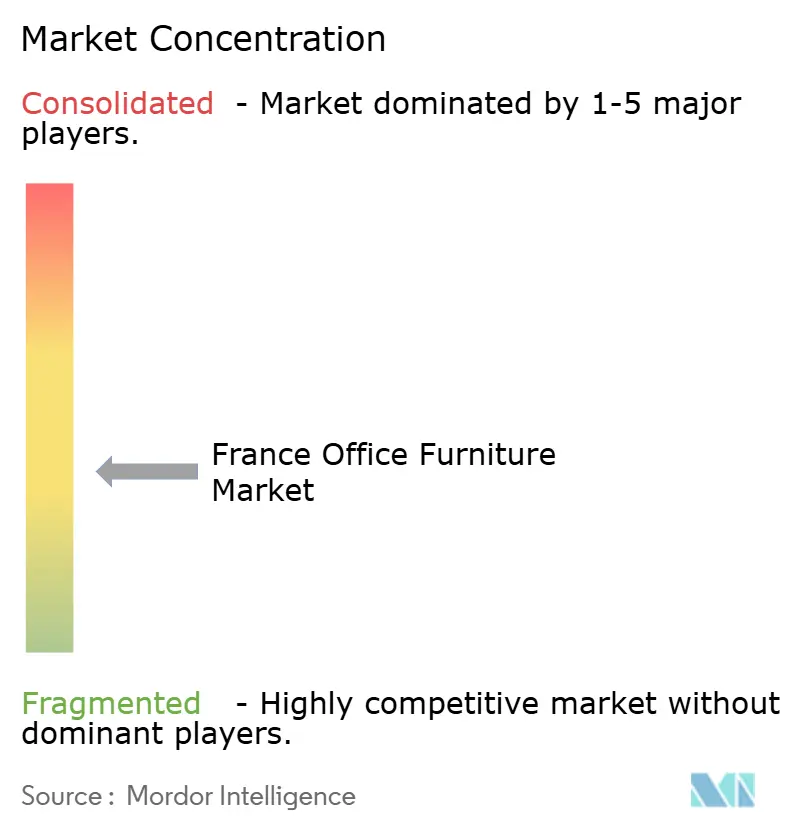

The France office furniture market exhibits moderate concentration, with the top five players controlling half of the revenue. Global giants like Steelcase, MillerKnoll, and IKEA benefit from scale, global sourcing, and R&D strength, allowing them to compete effectively in enterprise RFPs. However, their size can be a disadvantage when catering to French clients seeking bespoke, design-centric solutions. Steelcase’s “Hybrid Spaces” portfolio integrates sensors and Teams-certified devices, appealing to data-driven facility managers but demanding ERP integration that smaller companies may find challenging. In contrast, IKEA’s USD 1.3 billion investment targets SMEs, offering sustainable flat-pack lounge sets made from recycled plastics that comply with EU ecolabel standards.

Local manufacturers such as Majencia, Buronomic, and Gautier leverage their “Made-in-France” credentials, enabling shorter lead times and customization flexibility prized by architects. Majencia enhances its value proposition with AiM software, which uses parametric design and cost-based prompts to streamline the creation of custom reception areas. Gautier is boosting automation with cobot-powered sanding lines to deliver consistent low-VOC finishes while increasing throughput. These domestic players respond to market demand for quick-turn, tailored office setups with sustainable finishes. Their agility and proximity offer a strong counterpoint to larger, global competitors.

Emerging disruptors in the French market include SCOP-structured ateliers promoting circular economy models such as furniture leasing, refurbishing, and blockchain-based emissions tracking. These suppliers are increasingly partnering with co-working operators to align with strong sustainability narratives. Meanwhile, innovation is blurring industry lines as builders integrate prefabricated fixed-furniture units into CLT (cross-laminated timber) office structures. This bundling of walls and furniture into turnkey packages redefines traditional trade roles. As such, the market sees a dynamic interplay between scale, sustainability, and design customization.

France Office Furniture Industry Leaders

Steelcase Inc.

Kinnarps AB

Nowy Styl (incl. Majencia)

Vitra

EOL Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: SOKOA joined the French Living in Motion pavilion at INDEX Saudi Arabia 2025 to showcase French-manufactured furniture in export markets. SOKOA added seven collections to the pCon platform to support remote specification and visualization by architects and project managers

- June 2025: Steelcase published an NSF-certified Environmental Product Declaration for the Karman chair produced in Sarrebourg, detailing recycled content, recyclability, and low-emission credentials.

- April 2025: Buronomic unveiled its latest offerings- a Coworking Table and a Library system at the Workplace Event 2025.

France Office Furniture Market Report Scope

A complete background analysis of the France Office Furniture Market, which includes an assessment of the National accounts, economy, and the emerging market trends by segments, significant changes in the market dynamics, and the market overview is covered in the report.

By Product

| Chairs | Employee Chairs |

| Meeting Chairs | |

| Guest Chairs | |

| Tables | Conference Tables |

| Desks | |

| Other Tables | |

| Storage Units | Filing Cabinets |

| Bookcases & Shelving | |

| Sofas/Soft Seating | |

| Booths and Office Dividers | |

| Other Office Furniture (Stools, Reception Area Furniture, Accessories, Others) |

By Material

| Wood |

| Metal |

| Plastic & Polymer |

| Other Materials |

By Price Range

| Economy |

| Mid-range |

| Premium |

By End-user

| Corporate Offices |

| Healthcare Offices |

| Educational Institutions |

| Government & Public Offices |

| Hospitality & Retail Back-office |

| Others |

By Distribution Channel

| B2C / Retail | Home Centers |

| Specialty Furniture Stores | |

| Online | |

| Other Distribution Channels | |

| B2B / Directly from Manufacturers |

By Geography

| Île-de-France |

| Auvergne-Rhône-Alpes |

| Provence-Alpes-Côte d’Azur |

| Hauts-de-France |

| Rest of France |

| By Product | Chairs | Employee Chairs |

| Meeting Chairs | ||

| Guest Chairs | ||

| Tables | Conference Tables | |

| Desks | ||

| Other Tables | ||

| Storage Units | Filing Cabinets | |

| Bookcases & Shelving | ||

| Sofas/Soft Seating | ||

| Booths and Office Dividers | ||

| Other Office Furniture (Stools, Reception Area Furniture, Accessories, Others) | ||

| By Material | Wood | |

| Metal | ||

| Plastic & Polymer | ||

| Other Materials | ||

| By Price Range | Economy | |

| Mid-range | ||

| Premium | ||

| By End-user | Corporate Offices | |

| Healthcare Offices | ||

| Educational Institutions | ||

| Government & Public Offices | ||

| Hospitality & Retail Back-office | ||

| Others | ||

| By Distribution Channel | B2C / Retail | Home Centers |

| Specialty Furniture Stores | ||

| Online | ||

| Other Distribution Channels | ||

| B2B / Directly from Manufacturers | ||

| By Geography | Île-de-France | |

| Auvergne-Rhône-Alpes | ||

| Provence-Alpes-Côte d’Azur | ||

| Hauts-de-France | ||

| Rest of France | ||

Key Questions Answered in the Report

What is the France office furniture market size and growth outlook through 2031?

The France office furniture market size reached USD 1.74 billion in 2025 and is projected to reach USD 2.31 billion by 2031 at a 4.32% CAGR through 2031.

Which product categories are growing the fastest in France?

Booths and office dividers are projected to grow the fastest through 2031, driven by hybrid work needs for privacy and reconfiguration.

How are French EPR and AGEC rules changing furniture procurement?

Public buyers must meet second-hand and recycled-content targets, which support reuse, take-back, and remanufactured buying through Ecomaison’s partner network.

Which region contributes the most to France’s office furniture demand?

Île-de-France holds the largest share due to the concentration of headquarters and high-spec fit-outs in and around Paris.

What documentation do corporate tenders in France expect from furniture suppliers?

Buyers often require Environmental Product Declarations, low-VOC certifications, recognized NF labels, and data on recyclability and material disclosure.

Which distribution channels are most important in France’s office furniture space?

B2B direct sales lead due to project complexity and service requirements, while online B2C grows fastest with modular, quick-ship orders from smaller firms.

Page last updated on: