Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

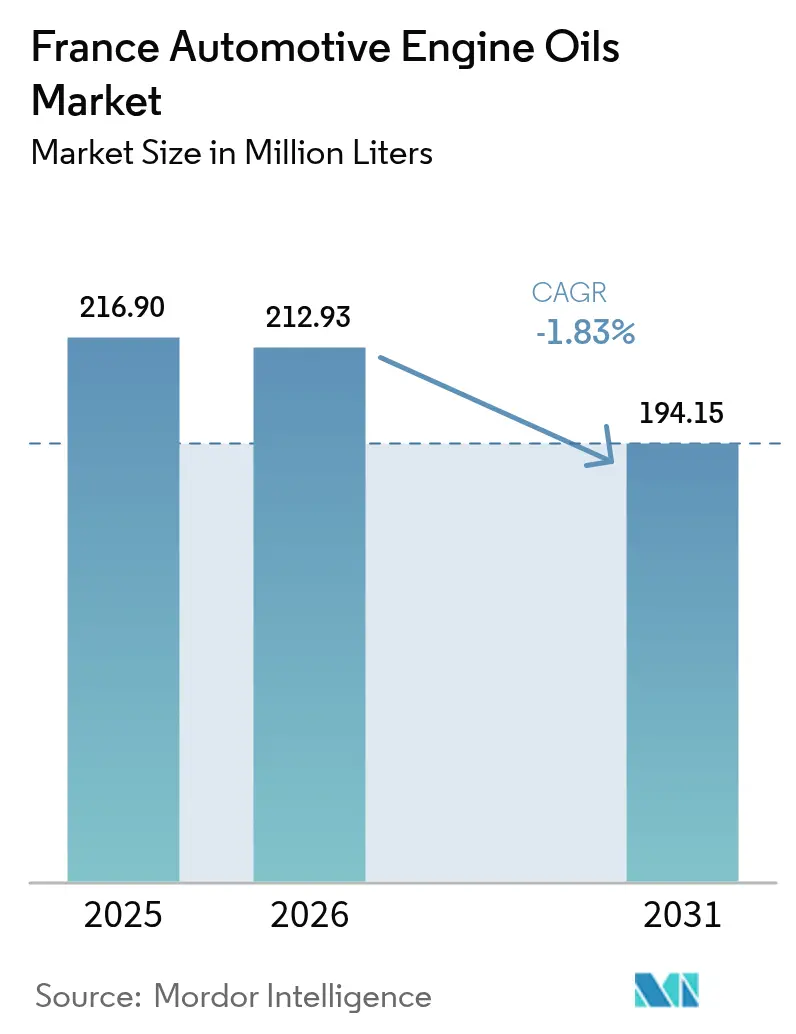

| Base Year Market Size (2025) | 216.90 Million liters |

| Market Volume (2026) | 212.93 Million liters |

| Market Volume (2031) | 194.15 Million liters |

| Growth Rate (2026 - 2031) | -1.83% CAGR |

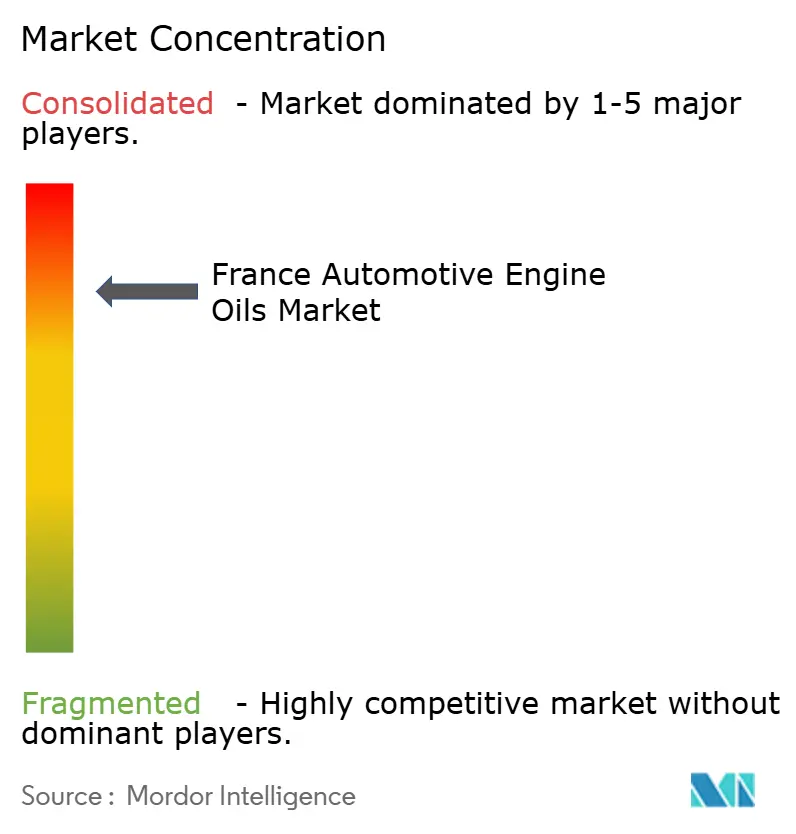

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Automotive Engine Oils Market Analysis by Mordor Intelligence

The France Automotive Engine Oils Market size is expected to grow from 216.90 million liters in 2025 to 212.93 million liters in 2026 and is forecast to reach 194.15 million liters by 2031 at -1.83% CAGR over 2026-2031. Passenger car motor oil (PCMO) continues to drive demand, yet shifting powertrain preferences, stricter Euro 7 emission limits, and longer-drain synthetic formulations progressively erode annual requirements. At the same time, a notably old national vehicle fleet, averaging 11.5 years in service, prolongs maintenance cycles and mitigates volume loss, particularly in rural and suburban areas with slower EV adoption. Synthetic and semi-synthetic blends gain ground as OEMs transition to 0W-20 and 0W-30 grades to meet real-driving-emission targets, thereby raising per-liter value even as total liters shrink. Operators also face higher Extended Producer Responsibility (EPR) fees and recovery mandates under France’s Anti-Waste Circular Economy Law, which is accelerating investment in regenerated-oil capacity and prompting suppliers to realign their business models toward a circular economy. Competitive intensity remains high as global majors defend their share through OEM tie-ups, omni-channel distribution, and data-driven maintenance services aimed at protecting margins within a contracting opportunity set.

Key Report Takeaways

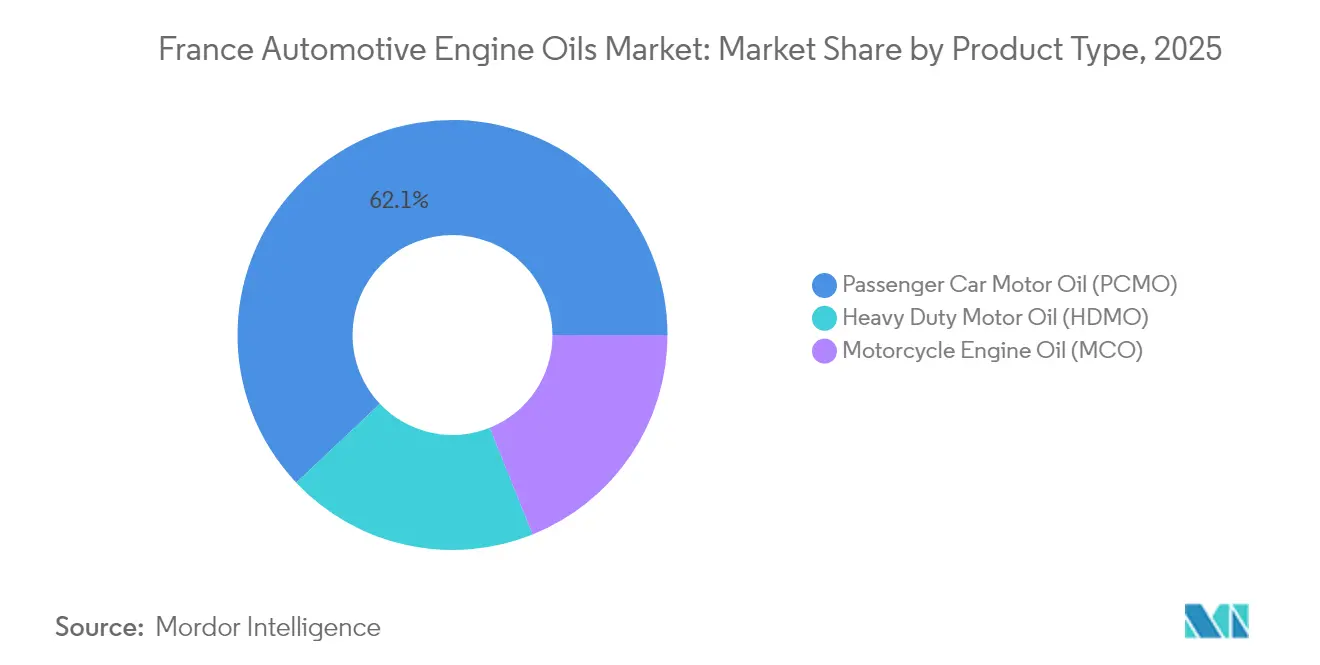

- By product type, passenger car motor oil held 62.05% of the France automotive engine oils market share in 2025, while motorcycle engine oil is forecast to contract at the slowest pace of −1.64% CAGR through 2031.

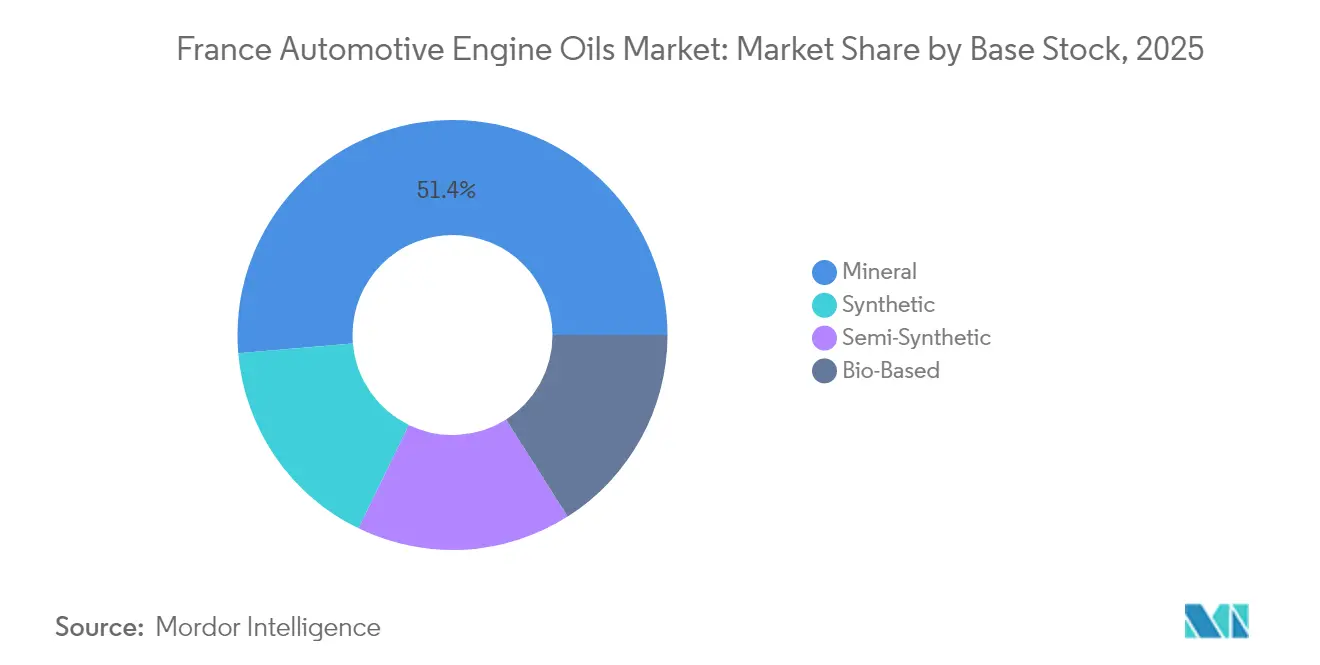

- By base stock, mineral formulations accounted for 51.35% of the France automotive engine oils market size in 2025, whereas synthetic grades are projected to shrink at a comparatively milder −1.55% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

France Automotive Engine Oils Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging vehicle parc prolongs maintenance demand | +0.8% | National, strongest in rural and suburban departments | Long term (≥ 4 years) |

| OEM-driven shift to low-viscosity synthetics | +0.4% | National, most visible in premium urban‐market segments | Medium term (2-4 years) |

| E-commerce and organized after-sales channels | +0.3% | National, accelerated in metropolitan areas | Short term (≤ 2 years) |

| Passenger-car oil resilience versus other lubes | +0.2% | National, especially in high-density ownership districts | Medium term (2-4 years) |

| Connected oil‐analysis and smart-tank services | +0.1% | National, early adoption by commercial fleets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ageing Vehicle Parc Prolongs Maintenance Demand

France's passenger cars have an average service life of 11.5 years, keeping a large share of petrol and diesel engines on the road well past the typical OEM warranty window. Nearly half the fleet falls within the 8-15-year band, a mileage bracket that typically requires at least one oil change per year. Rural and peri-urban drivers tend to retain ICE vehicles longer due to limited public charging infrastructure and lower disposable income, thereby sustaining base-load demand for mineral and semi-synthetic PCMO. Extended vehicle ownership also fuels demand for viscosity grades engineered for older engines, with the ACEA 2024 sequences introducing higher oxidative stability thresholds that favor premium synthetics[1]ACEA, “ACEA Oil Sequences 2024,” acea.auto. Consequently, while overall liters ebb, the market still records predictable maintenance cycles that partially buffer rapid EV substitution.

OEM-Driven Low-Viscosity Synthetic Shift (Euro 6/7)

Euro 7 brings real-driving-emission compliance from 2025 for new vehicle types, pushing factory-fill standards toward 0W-20 and, in diesel passenger applications, 5W-30 ACEA C5 or C6 categories[2]European Commission, “Euro 7 Emissions Standards,” ec.europa.eu. French OEMs under the Stellantis umbrella have already transitioned many of their new gasoline models to low-viscosity fill, a trend mirrored in the aftermarket through dealer and quick-service channels. Synthetic oils meeting these newer sequences deliver extended intervals of 20,000-30,000 km, enabling oil marketers to offset lower units with premium positioning. ATIEL’s Code of Practice ties product approvals to rigorous quality audits, fostering a high barrier to entry that favors established blenders. Over the medium term, low-viscosity uptake is forecast to increase the synthetic share of the French automotive engine oils market.

E-Commerce and Organized After-Sales Channels

Digital migration is reshaping the go-to-market model. Pure-play platforms and omni-channel chains such as Norauto and Feu Vert capitalize on transparent pricing and same-day click-and-collect services, diverting volume from legacy wholesalers. Carter-Cash’s bundled oil-change offer, rolled out nationwide, illustrates how low-cost, quick service can scale when paired with regenerated mineral grades that meet the requirements of older fleets. For suppliers, the rise of organized retail drives consolidated procurement, increased inventory transparency, and data feedback loops that encourage demand forecasting smoothing and targeted promotions.

Passenger-Car Oil Resilience Versus Other Lubes

French lubricant statistics for PCMO outperform the broader lubricants basket. Mandatory technical inspections (Contrôle Technique) are conducted every two years, compelling owners to address engine maintenance, while warranty stipulations tie vehicle resale value to documented service. Consumer surveys by automotive clubs indicate most drivers prioritize OEM-approved oils, even outside the dealership network, to preserve engine reliability. As a result, PCMO maintains higher brand loyalty and pricing power than industrial, marine, or process lubricants, helping suppliers defend their margins amid contracting volumes.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV parc expansion cutting ICE-oil volumes | −2.1% | National, fastest in Paris, Lyon, Lille metropolitan areas | Medium term (2-4 years) |

| Long-drain synthetics lower liter turnover | −0.8% | National, premium and commercial-fleet channels | Long term (≥ 4 years) |

| Counterfeit/private-label dilution in retail | −0.4% | National, pronounced in price-sensitive rural markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

EV Parc Expansion Cutting ICE-Oil Volumes

New registrations of battery-electric vehicles are increasing, and government policy aims for 66% market penetration by 2030. Urban low-emission zones (ZFE) covering Paris, Lyon, and Marseille already impose access restrictions on older diesel models, accelerating ICE scrappage. The volume erosion is particularly acute in ride-sharing and last-mile delivery segments, which collectively log high mileage but adopt EVs the fastest to capture total-cost-of-ownership gains. As charging infrastructure expands along national highways, the adoption of medium-duty commercial vehicles accelerates, creating a second-order drag on heavy-duty engine oils.

Long-Drain Synthetic Oils Lower Liter Turnover

OEM service programs for Euro 6d and Euro 7 compliant powertrains now prescribe oil-change intervals of 20,000-30,000 km, effectively trimming annual oil consumption by up to 40% for typical commuter mileage. Fleet operators utilize oil-life monitoring to synchronize maintenance with vehicle downtime, reducing unscheduled stops and labor costs. Premium-vehicle penetration of synthetics already exceeds 70% in Paris and Mediterranean coastal cities; as synthetic prices remain resilient, suppliers face a mix shift that raises revenue per liter but magnifies unit contraction. The aggregate drag is forecast at −0.8 percentage points to the France automotive engine oils market CAGR through 2030.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: PCMO Anchors Volume, Yet Faces EV Disruption

Passenger car motor oil accounted for 62.05% of the France automotive engine oils market share in 2025. The segment nevertheless registers the steepest absolute volume decline as EV uptake accelerates in urban zip codes. Heavy-duty motor oil exhibits a more moderate contraction, despite rising hybrid and light-commercial vehicle adoption. Long-haul trucking retains diesel propulsion pending the development of infrastructure for hydrogen or high-capacity charging. Motorcycle engine oil exhibits the most resilient trajectory, shrinking at only a −1.64% CAGR, cushioned by the recreational riding culture and lower regulatory urgency to electrify two-wheelers. Within PCMO, 0W-30 and 5W-30 synthetics are gaining market share as the Euro 7 implementation nears, squeezing legacy 10W-40 mineral volumes. Connected-vehicle data platforms increasingly tailor oil-change alerts, nudging consumer behavior toward “service when needed,” rather than calendar-based routines, thereby reshaping short-chain retail traffic patterns.

Continued PCMO dominance also derives from policy delays on used-car electrification. Second-hand ICE imports from Southern European neighbors supply rural dealerships, extending the lifecycle of older engines that still rely on mid-SAP blends. However, once true pricing parity arrives for BEVs in the late 2020s, analysts expect a sharper PCMO downshift, compelling suppliers to diversify into transmission fluids, EV coolants, and ancillary driveline lubricants to stabilize their revenue. Synthetic PCMO premiumization mitigates the blow, lifting revenue per unit despite contracting volumes, an adaptation visible in TotalEnergies’ Rubia and Quartz EV3R ranges, which incorporate regenerated base oil to meet sustainability metrics.

By Base Stock: Mineral Leads, Synthetic Climbs on Regulatory Tailwinds

Mineral oils retained 51.35% of the French automotive engine oils market size in 2025, driven by an aging vehicle pool and price-sensitive driver segments. Still, their dominance is in gradual retreat as synthetic and semi-synthetic blends capture incremental share, buoyed by Euro 7 demands and OEM warranty stipulations. Synthetic‐grade volume declines at a softer −1.55% CAGR through 2031, underscoring its relative defensiveness amid structural contraction. Semi-synthetics serve as a cost-performance bridge, posting mid-single-digit volume declines yet improving mix quality.

Bio-based and regenerated base stocks, although still niche, benefit directly from the Anti-Waste Circular Economy Law, which assigns specific recovery quotas to lubricant producers. ExxonMobil’s project to integrate a rerefining line at its Gravenchon refinery by H2 2025, providing the company with vertical control while reducing lifecycle CO₂ emissions.

Geography Analysis

Highly urbanized regions drive the narrative of premiumization. Île-de-France, with a large car park, already shows a large synthetic penetration for new service fills. The French automotive engine oil market size for Île-de-France is expected to experience a steeper deceleration as EV registrations grow. Rhône-Alpes and Provence-Alpes-Côte d’Azur follow similar curves, buoyed by affluent demographics and accelerated ZFE enforcement that phase out pre-Euro 5 diesels. Conversely, Grand Est and Bourgogne-Franche-Comté, anchored by agrarian economies, sustain higher mineral-oil uptake, extending PCMO lifecycles.

Regional disparities manifest in channel structure. Northern ports favor importers and global brands, while southern departments rely on national oil company distribution hubs. Paris and Lyon have emerged as testbeds for smart-tank oil delivery, where connected bulk dispensers alert suppliers when fleets near service thresholds, thereby smoothing last-mile logistics. In contrast, Brittany and Normandy workshops cling to 200-liter drums and cash-on-delivery terms, thereby delaying the adoption of digital orders. Government subsidies under ADEME support refining facilities in Seine-Maritime and Bouches-du-Rhône, anchoring regenerated base-oil supply chains near consumption centers.

Rural departments, while contracting more gradually, will face pressure from channel consolidation as independent distributors lose scale. Suppliers that synchronize their product portfolios with local fleet dynamics—synthetic in cities, value-grade minerals in the countryside—stand the best chance of preserving their share.

Competitive Landscape

Global majors command a major share of national liters, but private-label and counterfeit intrusion compresses gross margin. Competitive vectors now include data services. Motul partners with telematics players to bundle oil health analytics into subscription plans, a move that yields recurring revenue and embeds the brand in fleet decision-making cycles. Private-label share expansion, however, forces majors to justify price premiums via OEM endorsements, enhanced warranty coverage, and regenerative credentials. To deter counterfeit risk, TotalEnergies embeds NFC tags in quart bottles, enabling instant authenticity verification via a mobile app. These digital safeguards aim to preserve brand trust and protect revenue streams against gray imports that could otherwise skew market economics.

France Automotive Engine Oils Industry Leaders

TotalEnergies

Shell plc

Exxon Mobil Corporation

BP p.l.c.

Motul

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: BP p.l.c. initiated the sale process for its Castrol lubricants arm, valued near USD 10 billion, to rebalance its upstream portfolio. The outcome could reorganize distribution alliances in the France automotive engine oils market as potential acquirers weigh European footprints.

- May 2025: ExxonMobil France Holding entered into exclusive negotiations to divest an 82.89% stake in Esso S.A.F. to North Atlantic France SAS, a deal that retains the Esso retail fuel banner but allows ExxonMobil to concentrate on specialty lubricants marketing within the country.

France Automotive Engine Oils Market Report Scope

By Product Type

| Passenger Car Motor Oil (PCMO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Heavy Duty Motor Oil (HDMO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Motorcycle Engine Oil (MCO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades |

By Base Stock

| Mineral |

| Synthetic |

| Semi-Synthetic |

| Bio-Based |

| By Product Type | Passenger Car Motor Oil (PCMO) | 0W-XX |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Heavy Duty Motor Oil (HDMO) | 0W-XX | |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Motorcycle Engine Oil (MCO) | 0W-XX | |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| By Base Stock | Mineral | |

| Synthetic | ||

| Semi-Synthetic | ||

| Bio-Based | ||

Key Questions Answered in the Report

How will Euro 7 standards affect lubricant formulations in France?

Euro 7 pushes factory fills toward ultra-low-viscosity 0W-20 and 0W-30 synthetics, accelerating synthetic penetration and extending drain intervals, thereby reshaping demand patterns after 2025.

Which base stock category is losing share fastest?

Mineral oils still lead but contract quickest as OEM approvals and circular-economy mandates steer workshops toward premium synthetics and rerefined blends.

Why is motorcycle engine oil more resilient than PCMO?

Recreational riding demand and lagging two-wheeler electrification keep motorcycle engine oil volumes declining at a milder −1.64% CAGR versus sharper drops in passenger-car oils.

What impact will EV adoption have on heavy-duty engine oils?

Heavy-duty oils face a slower decline because long-haul trucking remains diesel-centric, though urban delivery electrification will gradually trim HDMO liters through the decade.

How are suppliers countering counterfeit lubricant risks?

Majors deploy NFC tags, blockchain batch tracking, and QR-code verification to help workshops and drivers authenticate products instantly, preserving brand value and safety.

What is the current market size of France automotive engine oils market?

The France Automotive Engine Oils Market size is estimated at 212.93 million liters in 2026 and is expected to decline to 194.15 million liters by 2031, at a CAGR of -1.83% during the forecast period (2026-2031).

Page last updated on: