Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

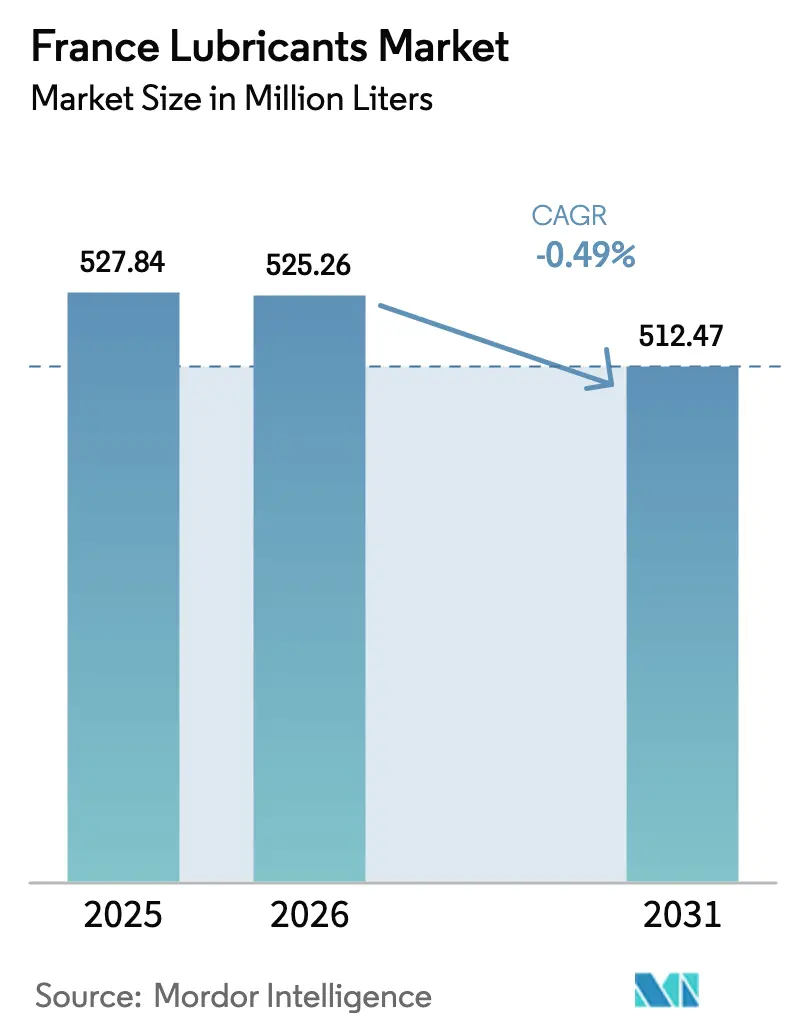

| Base Year Market Size (2025) | 527.84 Million liters |

| Market Volume (2026) | 525.26 Million liters |

| Market Volume (2031) | 512.47 Million liters |

| Growth Rate (2026 - 2031) | -0.49% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Lubricants Market Analysis by Mordor Intelligence

The France Lubricants Market size was valued at 527.84 million liters in 2025 and estimated to grow from 525.26 million liters in 2026 to reach 512.47 million liters by 2031, at a CAGR of -0.49% during the forecast period (2026-2031). This trajectory confirms that the France lubricants market is shifting from volume expansion to value optimization as premium synthetics, EV-ready fluids, and specialized industrial blends command higher margins despite lower absolute demand. Performance-oriented regulations, the electrification of vehicle and vessel fleets, and heightened sustainability mandates are reshaping product portfolios. On the supply side, the shutdown of Group-I base-oil capacity at Gravenchon has tightened feedstock availability, prompting blenders to shift toward re-refined and imported Group-II/III stocks. Competition intensifies around technical differentiation and OEM approvals, with integrated majors defending cost positions while niche players capture margins in aerospace, marine, and biodegradable formulations.

Key Report Takeaways

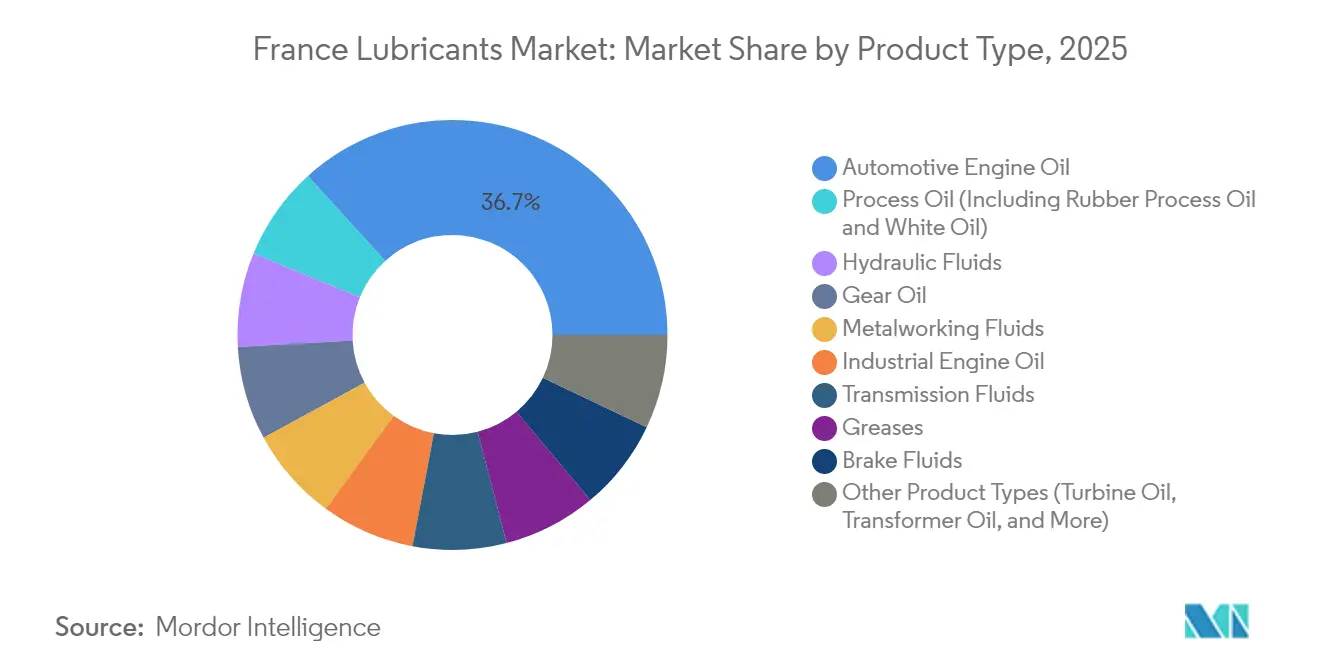

- By product type, automotive engine oil led with 36.74% Egypt lubricants market share in 2025, and turbine oil is forecast to expand at a 2.05% CAGR through 2031.

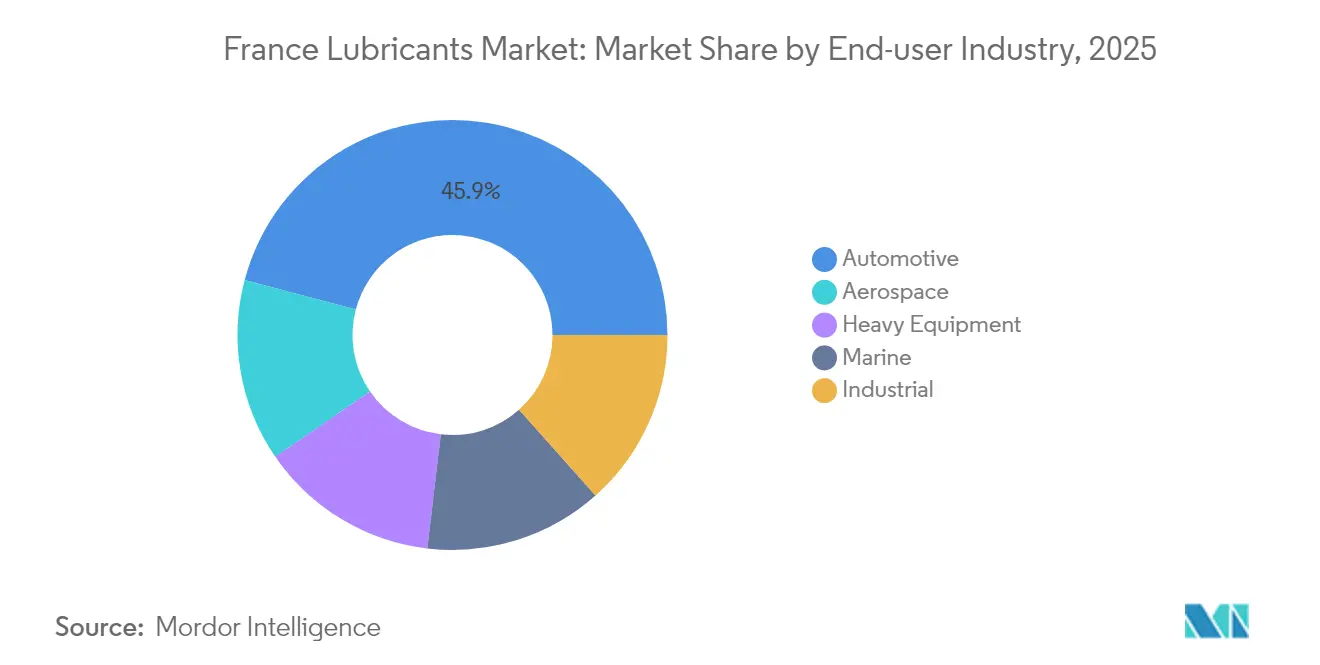

- By end-user industry, automotive accounted for 45.88% of the Egypt lubricants market size in 2025, while aerospace is advancing at a 1.77% CAGR between 2026-2031.

- By base stock type, mineral oil-based lubricants accounted for 60.45% of the market share, and during the forecast period (2026-2031), the share of bio-based lubricants is expected to rise with a CAGR of 1.92%.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

France Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter Euro-7 emission limits accelerating adoption of high-performance synthetics | +0.3% | France, EU spill-over | Medium term (2-4 years) |

| Rising French vehicle-parc and vehicle-kilometers post-COVID | +0.2% | National, urban centers | Short term (≤ 2 years) |

| OEM-mandated extended drain intervals | +0.15% | National aftermarket | Medium term (2-4 years) |

| Electrification of inland-waterway fleet spurring demand for biodegradable hydraulic oils | +0.12% | Seine & Rhône corridors | Long term (≥ 4 years) |

| Maintenance cycle for France’s nuclear-submarine fleet boosting specialty gear and turbine oils | +0.08% | Defense-specific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stricter Euro-7 Emission Limits Accelerating Adoption of High-Performance Synthetics

Euro-7 rules in force from 2025 impose sulfated-ash, phosphorus, and sulfur thresholds that conventional mineral oils cannot meet, locking in demand for synthetic or semi-synthetic low-SAPS blends[1]European Commission, “Proposal for Euro-7 Emission Standards,” europa.eu. TotalEnergies introduced its Quartz EV3R range in 2024, reducing carbon footprints by 35% while meeting OEM drain interval targets of 30,000 km. French assemblers have already shifted factory-fill specifications to Euro-7-compliant grades, cementing a permanent advantage for synthetics. Distributors that fail to list approved products risk being excluded from warranty-related benefits within dealership networks. The France lubricants market, therefore, sees synthetics gaining structural share as reverting to mineral alternatives would breach compliance.

Rising French Vehicle-Parc and Vehicle-Kilometers Post-COVID

More than 2 million rechargeable vehicles were on French roads by 2024, up 40% from 2022; yet the legacy ICE parc continued to grow as owners delayed replacements amid supply shortages. INSEE traffic indicators show that total vehicle-kilometers are back at pre-pandemic highs, and commercial traffic is up 8% compared to 2019, fueling the consumption of high-viscosity engine oils for urban delivery fleets. The national average vehicle age reached 10.2 years in 2024, resulting in increased maintenance-related lubricant throughput. Heavy-duty fleets stationed around Paris and Lyon operate extended idle-stop cycles, which accelerate oil oxidation, thereby reinforcing demand for premium synthetics with robust additive retention. Altogether, operating-hour intensity rather than fleet size is sustaining lubricant volumes in the France lubricants market.

OEM-Mandated Extended Drain Intervals

OEMs now specify up to 30,000-km or 24-month oil-change cycles to lower the total cost of ownership and reduce waste, thereby reducing annual oil volumes while increasing the per-liter value. Ford’s 2024 pact with TotalEnergies set 25,000-km service intervals for its French commercial line-up. Such intervals can only be achieved with full-synthetic base stocks featuring high oxidation stability. Independent workshops must stock these approved fluids to preserve factory warranties, curbing price competition and supporting aftermarket margins. For the France lubricants market, fewer drain events may trim bulk volumes yet strengthen demand for premium formulations that meet OEM approval lists.

Electrification of Inland-Waterway Fleet Spurring Demand for Biodegradable Hydraulic Oils

Paris has earmarked EUR 150 million through 2027 to electrify barges and service vessels on the Seine and Rhône, mandating the use of ISO 15380-compliant biodegradable hydraulic fluids. The SYNERGETICS consortium demonstrated an 85% lower ecological impact for these fluids compared to their mineral equivalents. TotalEnergies’ Biohydran SE series already covers 4,500 French commercial craft, anchoring early mover advantage[2]TotalEnergies, “Quartz EV3R Launch,” totalenergies.com. Operators in ecologically sensitive zones face fines for spills of non-compliant fluids, effectively creating a captive market for these substances. As electrification scales, the France lubricants market gains a new, value-rich niche centered on biodegradable hydraulics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Prolonged slowdown in domestic auto production from 2024 | –0.25% | Manufacturing regions | Short term (≤ 2 years) |

| Crude-price volatility inflating base-oil costs | –0.18% | Global input, local pass-through | Short term (≤ 2 years) |

| Closure of French steam-cracker and Group-I lines tightening feedstock supply | –0.12% | Domestic blenders | Medium term (2-4 years) |

| EU-taxonomy sustainability rules raising compliance costs for SME blenders | –0.08% | EU-wide, SME impact | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Prolonged Slowdown in Domestic Auto Production from 2024

French passenger-car output declined 18% in 2024 as manufacturers retooled for battery models, reducing factory-fill demand for break-in oils. Stellantis shifted selected assembly lines abroad, reducing local industrial lubricant use for machining and component washing. Because pure EVs need about 70% less lubricant than ICE vehicles, unit losses are amplified in volume terms. Job cuts in Sochaux and Mulhouse cascaded down the supply chain, resulting in reduced short-run orders for specialty process oils. The France lubricants market, therefore, faces near-term headwinds until EV volumes plateau and specialized EV fluids scale up.

Crude-Price Volatility Inflating Base-Oil Costs

Brent swung between USD 70-95/bbl during 2024, boosting base-oil quotes and squeezing blender margins. The Gravenchon shutdown removed France’s lone Group-I source, forcing small blenders to rely on spot imports, along with freight premiums. Integrated majors hedge exposures via long-term supply contracts, but independent SMEs struggle to pass through surcharges in commoditized segments as feedstock inflation collides with price-sensitive customers, consolidation risk mounts across the France lubricants market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Engine Oils Retain Scale while Turbine Oils Outpace

The France lubricants market share for automotive engine oils reached 36.74% of total demand in 2025. Turbine oils, however, are projected to post the fastest 2.05% CAGR as France extends the lifetimes of its nuclear reactors and accelerates the roll-out of offshore wind. In commercial practice, synthetics dominate new-generation turbine units that operate at higher temperatures and tighter clearances. Brake-fluid volumes contract as regenerative systems reduce hydraulic-brake duty cycles, whereas biodegradable hydraulic oils increase in use with the growing electric construction equipment sector. Gear oils serving wind-turbine gearboxes and heavy-duty trucks maintain a stable demand, supported by the growth of renewables and logistics. White and process oils serve the rubber, plastics, and personal-care industries, delivering flat though profitable niches. Metal-working fluids gain incremental volumes at Airbus’ Toulouse hub, where increased A320 machining requires high-lubricity, low-foaming coolants. Overall, the product mix tilts toward high-performance, low-volume specialties, underlining how the France lubricants market optimizes value per liter.

The adoption of Euro-7-ready engine oils is accelerating, with at least 30% of factory-fill demand expected to shift to low-SAPS synthetics by 2025. Transmission-fluid demand benefits from extended-drain mandates, an area where OEM approvals dictate supplier access. Meanwhile, demand for transformer oils aligns with grid-reinforcement projects that integrate onshore renewables. Altogether, turbine-oil momentum and specialty niches partially offset structural headwinds in mainstream engine oils, keeping the France lubricants market diversified across applications.

By End-User Industry: Automotive Dominance Meets Aerospace Upswing

Passenger, commercial, and two-wheeler fleets accounted for nearly half the market in 2025, resulting in the automotive channel's 45.88% share of the France lubricants market size. Aerospace, the fastest riser at 1.77% CAGR, captures lubricant value through high-spec turbine and hydraulic fluids used in Airbus A320neo and A350 production runs. Electric-vehicle penetration reduces passenger-car engine oil volumes, but commercial-vehicle lubricants remain resilient as long-haul electrification lags and diesel trucks continue to drive higher mileage. Inland-waterway electrification encourages the adoption of biodegradable hydraulic oil among marine operators. Heavy equipment across construction and agriculture maintains steady consumption of high-viscosity engine and gear oils.

In the two-wheeler market, electrification remains nascent, so conventional motorcycle oils continue to persist. Power-generation applications expand in step with nuclear life-extension works, lifting demand for turbine and transformer oils. Industrial sectors such as metallurgy, textiles, and food processing require niche process oils with food-grade or high-temperature ratings, which carry attractive margins. Consequently, while automotive volumes taper, specialized industrial and aerospace segments prop up value, keeping the France lubricants market balanced across end users.

By Base Stock Type: Mineral Oils Erode as Synthetics and Bio-Based Blends Gain

Mineral formulations still control 60.45% of demand but will continue ceding ground to synthetics as Euro-7 and OEM drain-interval mandates tighten. Bio-based blends, supported by EU taxonomy incentives, are projected to post a leading 1.92% CAGR through 2031, carving out a share in marine, hydraulics, and industrial segments that value biodegradability. Semi-synthetics remain popular in mainstream automotive service outlets, offering cost relief versus full synthetics. Following the closure of the Gravenchon Group-I, local blenders rely on imports or re-refined alternatives. TotalEnergies’ re-refined base-oil unit in Gonfreville produces Group-II-equivalent stocks, reducing carbon intensity by 35% compared with virgin mineral streams.

OEM specifications for Euro-7 have largely shifted to Group-III-heavy blends, accelerating synthetic substitution. Bio-lubricants featuring rapeseed or ester bases help operators comply with ISO 14001 procurement policies. The France lubricants market thus illustrates a two-pronged shift: from mineral to synthetic for performance and from fossil to bio-based for sustainability.

Geography Analysis

The Île-de-France region anchors lubricant demand through its dense automotive, aerospace, and logistics footprint around Paris-Charles de Gaulle and Le Havre. Normandy, despite losing the Gravenchon refinery, still pulls significant turbine-oil demand for its nuclear reactors and petrochemical complexes. Auvergne-Rhône-Alpes benefits from both Airbus structures in Toulouse and vehicle assembly near Lyon, supporting premium synthetic materials in the aerospace and automotive channels. Mediterranean ports—from Marseille to Fos-sur-Mer—generate a marine lubricant pull, amplified by the IMO 2020 sulfur limits that favor low-ash blends.

Northern industrial belts exhibit higher automotive and lubricant intensity, while southern corridors post faster gains in aerospace and shipping. Inland waterways along the Seine, Rhône, and Rhine underpin biodegradable hydraulic-fluid demand as electrification programs advance. Cross-border trade with Germany and Belgium influences pricing parity because integrated supply chains can arbitrage EU-wide specifications. Nuclear-heavy regions extend turbine-oil lifecycles as EDF pursues reactor life extensions to 60 years, underpinning specialized demand. Meanwhile, burgeoning offshore-wind clusters off the Atlantic coast need gear oils with high scuffing resistance for turbines exposed to salt spray. Balanced across these zones, the France lubricants market remains national in scope yet locally nuanced in product mix.

Competitive Landscape

The France Lubricants Market is moderately concentrated. Integrated majors—TotalEnergies, Shell, and BP/Castrol—hold entrenched channel reach and feedstock leverage, yet specialized brands such as Motul, FUCHS, and LIQUI MOLY outperform in high-margin niches. For instance, TotalEnergies capitalizes on its domestic refining-to-retail chain to manage mineral-oil cost inflation. SME blenders face higher compliance costs under EU taxonomy rules, prompting consolidation or niche specialization. In short, performance validation and sustainability positioning, rather than bulk volume, now dictate competitive edge within the France lubricants market.

France Lubricants Industry Leaders

BP p.l.c.

Exxon Mobil Corporation

Shell plc

Motul

TotalEnergies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: LM France SAS, the French arm of Ulm-based lubricant expert LIQUI MOLY, acquired the former importer, LIQUI MOLY France SAS. This acquisition positions LIQUI MOLY, renowned for its engine oils, additives, and car care products, for a brighter and more prosperous future in the French market.

- November 2024: Lubricant powerhouses PETRONAS Lubricants International (PLI) and KENNOL Performance Oil announced their partnership for the French market, which will see the brands team up in a co-branded offering for the automotive sector.

France Lubricants Market Report Scope

Lubricant products are made from a combination of base oils and additives. The composition of base oil in the formulation of lubricants is primarily between 75-90%. Base oils possess lubricating properties and makeup up to 90% of the final lubricant product.

The France lubricants market is segmented based on the product type and end-user industry. By product type, the market is segmented into engine oils, transmission and gear oils, hydraulic fluids, metal working fluids, greases, and other product types (dry film lubricants). The market is segmented by end-user industries: power generation, automotive, heavy equipment, metallurgy and metal working, and other end-user industries (food processing, marine, etc.). For each segment, the market sizing and forecasts have been done based on volume (liters).

By Product Type

| Automotive Engine Oil |

| Industrial Engine Oil |

| Transmission Fluids |

| Gear Oil |

| Brake Fluids |

| Hydraulic Fluids |

| Greases |

| Process Oil (Including Rubber Process Oil and White Oil) |

| Metalworking Fluids |

| Turbine Oil |

| Transformer Oil |

| Other Product Types |

By End-user Industry

| Automotive | Passenger Vehicles |

| Commercial Vehicles | |

| Two-Wheelers | |

| Marine | |

| Aerospace | |

| Heavy Equipment | Construction |

| Mining | |

| Agriculture | |

| Industrial | Power Generation |

| Metallurgy and Metalworking | |

| Textiles | |

| Oil and Gas | |

| Other End-Use Industries |

By Base Stock Type

| Mineral Oil-Based Lubricants |

| Synthetic Lubricants |

| Semi-Synthetic Lubricants |

| Bio-Based Lubricants |

| By Product Type | Automotive Engine Oil | |

| Industrial Engine Oil | ||

| Transmission Fluids | ||

| Gear Oil | ||

| Brake Fluids | ||

| Hydraulic Fluids | ||

| Greases | ||

| Process Oil (Including Rubber Process Oil and White Oil) | ||

| Metalworking Fluids | ||

| Turbine Oil | ||

| Transformer Oil | ||

| Other Product Types | ||

| By End-user Industry | Automotive | Passenger Vehicles |

| Commercial Vehicles | ||

| Two-Wheelers | ||

| Marine | ||

| Aerospace | ||

| Heavy Equipment | Construction | |

| Mining | ||

| Agriculture | ||

| Industrial | Power Generation | |

| Metallurgy and Metalworking | ||

| Textiles | ||

| Oil and Gas | ||

| Other End-Use Industries | ||

| By Base Stock Type | Mineral Oil-Based Lubricants | |

| Synthetic Lubricants | ||

| Semi-Synthetic Lubricants | ||

| Bio-Based Lubricants | ||

Key Questions Answered in the Report

How large is the France lubricants market in 2026?

It measures 525.26 million liters, reflecting the latest France lubricants market size figure.

What is the expected growth trend through 2031?

The market is forecast to contract at a –0.49% CAGR, ending at 512.47 million liters.

Which product category is expanding the fastest?

Turbine oils lead with a 2.05% CAGR driven by nuclear maintenance and wind-power growth.

Which end-use sector will grow quickest?

Aerospace shows the highest 1.77% CAGR as Airbus ramps up aircraft output.

How will Euro-7 affect lubricant formulations?

The new standard mandates low-SAPS blends, pushing blenders toward synthetic or semi-synthetic base stocks only.

Page last updated on: