Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

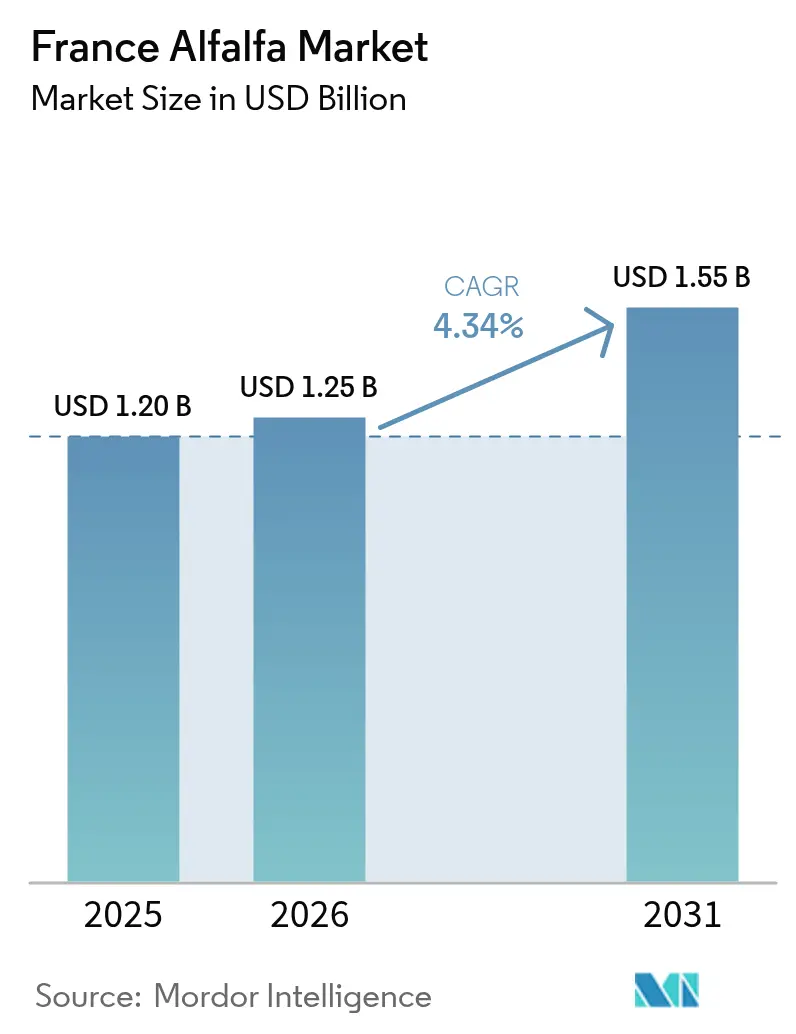

| Base Year Market Size (2025) | USD 1.20 Billion |

| Market Size (2026) | USD 1.25 Billion |

| Market Size (2031) | USD 1.55 Billion |

| Growth Rate (2026 - 2031) | 4.34% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

France Alfalfa Market Analysis by Mordor Intelligence

The France alfalfa market size is projected to expand from USD 1.20 billion in 2025 and USD 1.25 billion in 2026 to USD 1.55 billion by 2031, registering a CAGR of 4.34% between 2026 to 2031. The France alfalfa market is supported by a cooperative drying facility that runs on forest wood chips, and that shift has cut greenhouse gas (GHG) emissions, strengthening the product’s position in low-emission livestock supply chains. The France alfalfa market also benefits from policy support linked to protein autonomy, stronger certification demand, and widening interest from equine, porcine, and human nutrition channels described in the source. Competitive conditions are being reshaped by plant consolidation, export redirection toward European Union buyers, and expanding quality requirements from downstream feed users, while pressure from herd contraction, labor shortages, and freight volatility still limits upside. The France alfalfa market is therefore moving forward on a broader demand base, but future gains still depend on keeping domestic value addition ahead of volume pressure in traditional ruminant channels.

Key Report Takeaways

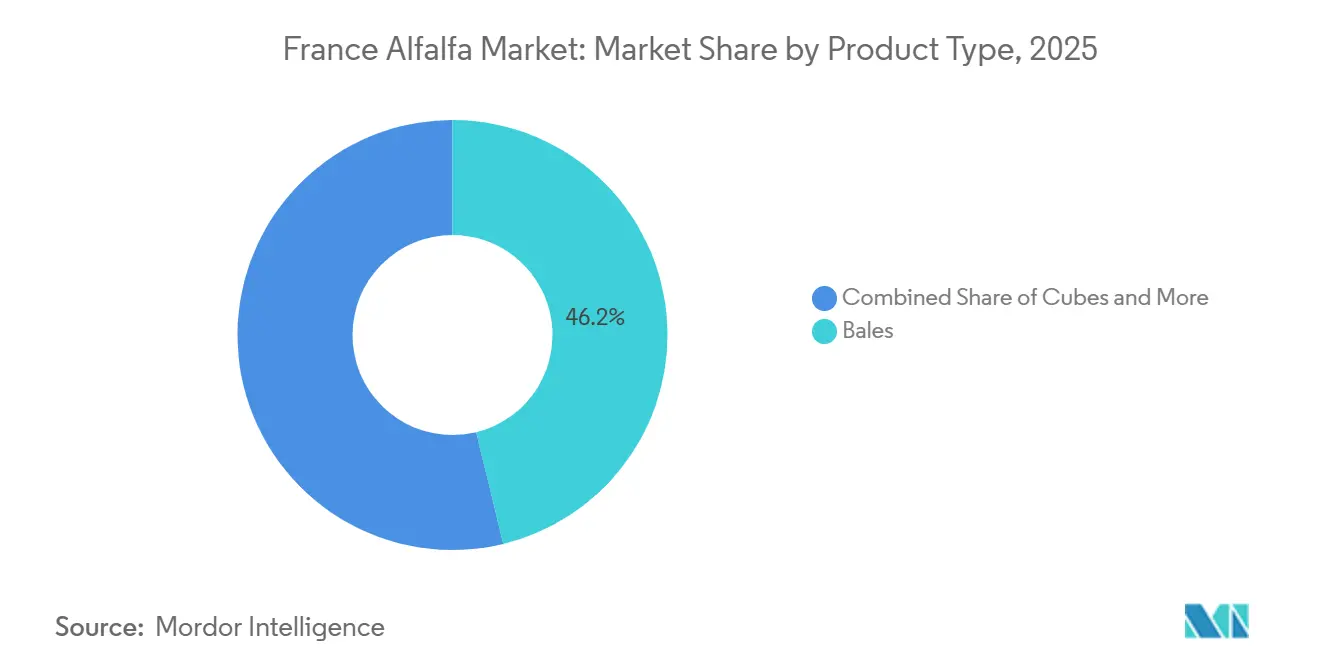

- By product type, bales were the largest segment, accounting for 46.2% of the France alfalfa market share in 2025, while pellets are the fastest-growing segment, with a 5.9% CAGR from 2026 to 2031.

- By application, dairy cattle feed was the largest segment, accounting for 53.7% of the France alfalfa market size in 2025, while equine feed is the fastest-growing segment with a 5.6% CAGR from 2026 to 2031.

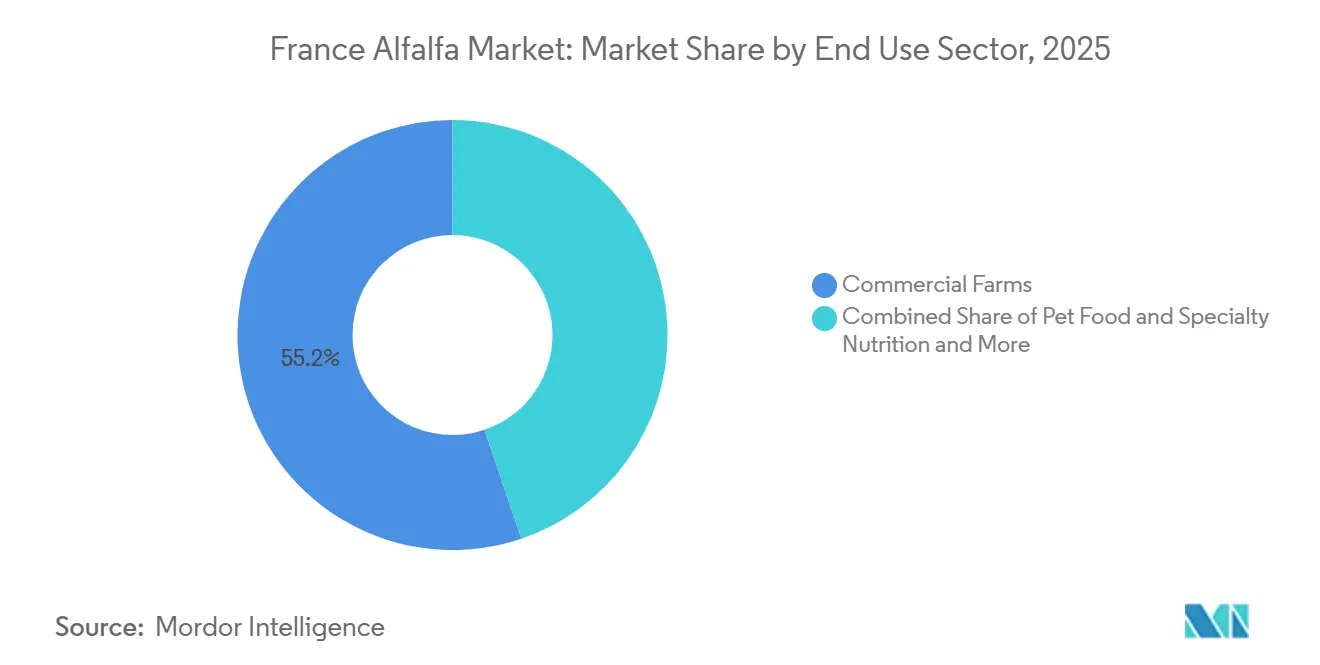

- By end-use sector, commercial farms were the largest segment with a 55.2% share in 2025, while pet food and specialty nutrition is the fastest segment with a 6.0% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

France Alfalfa Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising dairy and beef herd demand in France | +1.2% | National, with early gains in Grand-Est and Centre-Val de Loire | Medium term (2-4 years) |

| Protein sovereignty push for domestic feed inputs | +0.9% | National, with premium pull from Normandy dairy zones and export buyers | Medium term (2-4 years) |

| Expansion of low-carbon and organic livestock specifications | +0.7% | Grand-Est, Hauts-de-France, and western processing links | Medium term (2-4 years) |

| Expansion of dehydration capacity and plant consolidation | +0.6% | Grand-Est, Normandy, Brittany, and Pays de la Loire | Short term (≤ 2 years) |

| Carbon-monetized legume rotations and low-emission pellets | +0.5% | National, with commercial development in France and wider Europe | Long term (≥ 4 years) |

| Climate-resilient forage planning in arable-livestock interfaces | +0.4% | Grand-Est, Burgundy, and Poitou-Charentes | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Dairy And Beef Herd Demand In France

France’s bovine herd kept shrinking in 2025, but feed demand per animal remained firm because productivity expectations continued to rise. According to the French Ministry of Agriculture and Food Sovereignty (Agreste), the dairy cow population fell to 3.22 million head in 2025, yet milk collection still rose to 24.2 million metric tons as milk yield per cow increased 5.2%[1]Source: French Livestock Institute (IDELE), "Annual Beef Cattle Report 2025: 2026 Outlook," idele.fr.. That pattern matters for the France alfalfa market because higher-output herds need more stable fiber and protein inputs across the year, especially in tightly managed feeding systems. This shift to robotized feeding and more precise ration design supports the continued use of dehydrated alfalfa even when total herd numbers decline. The France alfalfa market also draws support from horses, which already represented dehydrated alfalfa consumption in France and gives the sector a buffer outside cattle feed demand.

Protein Sovereignty Push For Domestic Feed Inputs

Market is closely tied to the country’s effort to reduce dependence on imported soybean meal and strengthen domestic protein supply. Analysis cited in the shows that dehydrated alfalfa in a 3-year rotation can reduce synthetic nitrogen use by 53 kilograms per hectare each year and can generate 284,000 metric tons of digestible intestinal protein annually in France[2]Source: Innovations Agronomiques, “The Dehydrated Alfalfa Sector in France: History of Its Cooperative Structure, Challenges, and Development Prospects,” doi.org. That evidence gives the France alfalfa market a measurable role in domestic feed substitution rather than only an agronomic role in crop rotation. Certification also supports this position because non-GMO and Feed Chain Alliance standards make French alfalfa more usable for compound feed manufacturers facing traceability and emissions reporting requirements in Europe.

Expansion Of Low-Carbon And Organic Livestock Specifications

The France alfalfa market is benefiting from tighter sourcing standards in dairy and meat supply chains, especially where buyers want feed ingredients with clear carbon and origin credentials. The French dehydration base reduced greenhouse gas emissions after shifting dryers away from fossil fuels and toward biomass wood chips. That improvement makes French dehydrated alfalfa easier to place in low-emission livestock programs than less traceable imported alternatives. It also notes that protected cheese chains in Normandy rely on non-genetically modified feed rules, which helps keep certified French alfalfa relevant in premium dairy systems. This trend supports the France alfalfa market because it protects pricing in quality-led channels and strengthens long-term contracting for cooperatives that can document production and processing standards.

Expansion Of Dehydration Capacity And Plant Consolidation

It is also being shaped by consolidation at the processing stage, where scale matters for cost control and quality consistency. The June 2025 merger announcement between Tereos SCA and Capdéa SAS, followed by the June 2026 formalization of Tereos CapDéshy, created a larger cooperative structure with 210,000 metric tons of alfalfa capacity, 100,000 metric tons of beet pulp, and 20,000 metric tons of other forage products[3]Source: The French Sugar Beet Grower, "Tereos and Capdéa Merge Their Beet Pulp and Alfalfa Businesses," lebetteravier.fr.. This kind of plant grouping lowers fixed cost per unit and gives cooperatives more room to invest in energy optimization, quality analytics, and wider customer service. It also helps the France alfalfa market because alfalfa, beet pulp, and other dehydrated feed products can move through a shared operating base instead of separate infrastructure. It presents this consolidation pattern as a template that smaller operators may need to follow as labor and cost pressures continue.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from maize silage and alternative forages | -0.8% | National, with strongest pull in dairy basins such as Normandy and Brittany | Short term (≤ 2 years) |

| Farm labor scarcity during harvest and transport windows | -0.6% | National, with broad impact on traditional ruminant demand | Medium term (2-4 years) |

| Export freight and energy cost volatility | -0.5% | Grand-Est, Hauts-de-France, and Centre-Val de Loire | Short term (≤ 2 years) |

| Nitrate-zone compliance and administrative burden | -0.4% | Export-oriented eastern cooperatives and Grand-Est-centered output base | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Competition From Maize Silage And Alternative Forages

The market still competes against maize silage, which remains the main incumbent feed option in many ruminant systems. ARVALIS reported national maize forage yield at 11.8 metric tons of dry matter per hectare in 2025, and the crop’s energy quality improved from earlier years, which made it a stronger substitute in dairy rations. When maize silage is both cheaper and nutritionally stronger, feed formulators can shift away from dehydrated alfalfa and reduce demand at cooperative plants. La Coopération Agricole – Luzerne de France openly recognized this substitution risk at the November 2025 World Alfalfa Congress, which is why the sector is pushing harder into equine and porcine channels. This remains a real brake on the France alfalfa market because commodity forage competition affects volumes more quickly than newer specialty uses can replace them.

Farm Labor Scarcity During Harvest And Transport Windows

The France alfalfa market depends on a production model that requires 3 to 4 timed cuts each growing season, and each cut has to move quickly through harvest, transport, and plant intake. It says these peaks overlap with cereal and sugar beet fieldwork in Grand-Est and Hauts-de-France, tightening labor availability when timing matters most. According to a research study titled "Dehydrated Alfalfa Sector in France: History of Its Cooperative Structure, Challenges, and Development Prospects," harvest costs and the need for specialized conservation and dehydration logistics remain key constraints on acreage expansion, particularly in regions without established forage-processing infrastructure. Cooperatives are trying to improve scheduling and route efficiency with digital tools, but access to that investment is not even across the network. For the France alfalfa market, this creates a cost gap between larger consolidated groups and smaller operators that have less room to absorb operational delays.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Pellets Lead as Cubes Drive Premium Channel Growth

Bales were the largest segment, accounting for 46.2% of the France alfalfa market share in 2025. It remained important for direct farm use where handling simplicity mattered more than precision feeding, while compressed bales added value in export channels by improving freight efficiency. Equine buyers are driving that growth because cube formats support portion control, palatability, and digestive management more effectively than standard hay products. France Luzerne, Désialis, and Lab To Field launched the In-PULSA research program in December 2024 to study dehydrated alfalfa and its impact on equine gastric health, which supports stronger premium positioning for DÉSIALIS cube products. The same logic is opening new room in the pigs, poultry, and specialty retail channels, helping the France alfalfa industry reduce its dependence on bulk commodity formats.

Pellet are the fastest segment, and the France alfalfa market size for cubes is projected to expand at a 5.9% CAGR from 2026 to 2031. Pellets were the largest segment and held 46.2% of France alfalfa market share in 2025. Their position reflects strong fit with automated total mixed ration (TMR) systems and the needs of compound feed manufacturers that want dense, consistent, and easy-to-dose material. Pellet processing also improves moisture control and reduces dust, which supports transport, storage, and formulation quality in the France alfalfa market.

By Application: Dairy Cattle Feed Remains Largest as Equine Feed Expands Fastest

Dairy cattle feed was the largest application and accounted for 53.7% share of the France alfalfa market size in 2025. That leadership rested on the scale of the national dairy base and on higher feed intensity per animal, even as herd numbers moved lower in 2025. Dehydrated alfalfa fits those systems because it delivers protein and fiber in a predictable manner across automated, performance-focused feeding programs. The France alfalfa market therefore remains anchored in dairy, even while the sector is working to diversify away from a single livestock base.

Equine feed is the fastest application, and the France alfalfa market size for this segment is set to rise at a 5.6% CAGR from 2026 to 2031. The equine feed drives strong demand for French dehydrated alfalfa and offers a higher value per metric ton, as buyers prioritize digestive health, ration stability, and format quality. Small ruminant feed remained a specialized outlet in protected cheese systems that require traceable, non-GMO inputs, while poultry feed is gaining ground through enrichment-led uses rather than solely on bulk nutrition. Beef cattle feed remained under pressure from herd decline, and camelid and other livestock feed remained small, but both still offered selective outlets where French suppliers could sell certified or differentiated French Livestock Institute (IDELE) material.

By End Use Sector: Commercial Farms Anchor Volume as Pet Food and Specialty Nutrition Advances

Commercial farms were the largest end use sector with a 55.2% share in 2025. That result came from the cooperative model, where member growers supply raw material and also buy processed alfalfa back into feeding programs under established operating relationships. This structure gives the France alfalfa market a stable baseline because usage is tied to on-farm routines and not only to short-term spot pricing. Compound feed manufacturers remained the next major demand layer because they absorb pellet volumes for broader ration products sold across neighboring European markets.

Pet food and specialty nutrition are the fastest end use sector, and the France alfalfa market size for this segment is forecast to grow at a 6.0% CAGR from 2026 to 2031. Demand here is linked to traceable plant protein, certified sourcing, and premium positioning in rabbits and small mammal diets rather than to bulk feed tonnage. The segment also benefits from defined retail formats, which offer better pricing than commodity pellet contracts and open the door for branded products. In this part of the France alfalfa industry, household and hobby animal owners remain fragmented buyers, but they support high-margin demand that complements the volume base provided by commercial farms and feed manufacturers.

Geography Analysis

Grand-Est was the largest region of French dehydrated alfalfa output in 2025, which made it the clearest expression of France alfalfa market share by geography. The region’s role rests on established cooperative infrastructure, suitable soils, and operating routines built around repeated cuts and fast plant intake. 24 dehydration plants operate under 10 cooperative entities, and much of that industrial base is concentrated in this eastern belt. The Tereos CapDéshy combination further reinforced that weight by grouping Marne and Aube dehydration activities into a single larger unit. For the France alfalfa market, this concentration improves throughput and cost control, but it also means the national supply base is less geographically balanced than demand.

Outside Grand-Est, Poitou-Charentes and Normandy serve different roles in the France alfalfa market. Poitou-Charentes appears as a testing ground for modular and hybrid drying ideas, suggesting a route to more distributed processing. Normandy is more important as a demand center because its protected cheese systems require traceable feed inputs and support sustained purchasing of non-genetically modified alfalfa pellets and cubes. The links to dairy corridors serving Camembert, Livarot, and Pont-l'Évêque, where feed compliance has direct commercial value. Pays de la Loire and Brittany also depend on eastern supply because their local alfalfa area remains smaller than feed demand. This creates room for cooperatives with strong internal logistics to capture margins between producing and consuming zones.

France’s wider European position continues to shape the France alfalfa market at home. France produced dehydrated alfalfa 725,000 metric tons in 2025 and remained Europe’s second-largest producer behind Spain and ahead of Italy. It states that Spain’s export exposure to Gulf routes created an opening for France to re-enter more European demand pockets, while 95% of French exports were already directed to European Union buyers. China accreditation obtained in late 2025 gives the sector a longer-term external option, but the same makes clear that commercial scale in that market will take time to build.

Competitive Landscape

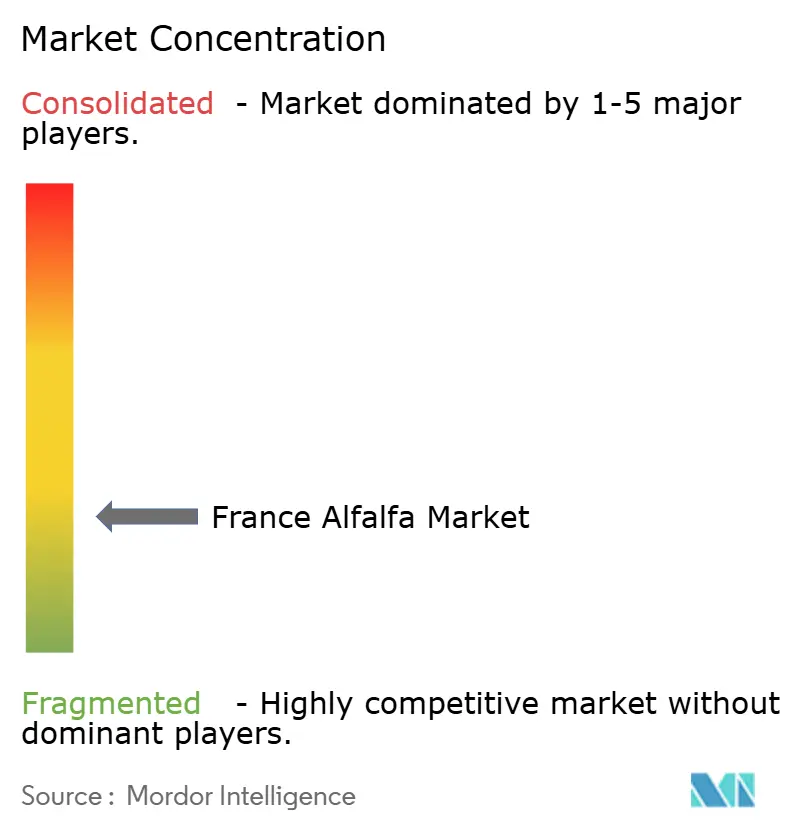

The France alfalfa market remains fragmented, with the top Groupe Florimond Desprez SAS, Tereos SCA, Groupe Luzéal, Cérience SAS (Terrena Group), and Eureden Group, holding significant market shares in 2025. The France alfalfa market is organized around a cooperative processing core, and that gives the sector a different competitive profile than many private branded feed categories. Désialis acts as the commercial arm for export development and product certification, helping connect cooperative supply with buyers that need documented non-genetically modified products and feed-chain standards. This structure gives the France alfalfa market a concentrated processing base without removing competition in seed inputs, product development, and customer access. It also means that scale at plant level matters more than brand visibility alone in explaining market position.

One of the clearest competitive moves in the France alfalfa market was the formation of Tereos CapDéshy in April 2024, which brought together major dehydration cooperatives to consolidate processing capacity and strengthen export positioning. In-PULSA research program, which aimed to build evidence-based value in equine nutrition rather than rely solely on volume growth. By investing in nutritional research, these players sought to differentiate their products in premium segments and reduce dependence on commodity-driven demand. Together, these actions indicate that the France alfalfa market is simultaneously defending margins through scale, specialty demand, and export diversification.

Competition is still active upstream and across adjacent feed systems. The Groupe Limagrain, DLF Seeds A/S, Cérience SAS, and Jouffray-Drillaud SAS as relevant names in forage seed development for French conditions, where persistence, winter hardiness, and leaf-to-stem ratio affect grower economics. Integrated agricultural groups such as Agrial Cooperative Group and Vivescia Cooperative Group also matter because their feed and crop positions can strengthen direct procurement links with dehydration units. Valorex SAS represents another route into higher-value feed concepts where formulation matters more than bulk tonnage. The France alfalfa market therefore remains concentrated in processing, but not closed to competitive pressure from seed providers, livestock cooperatives, and downstream nutrition specialists.

France Alfalfa Industry Leaders

-

Groupe Florimond Desprez SAS

-

Tereos SCA

-

Groupe Luzéal

-

Eureden Group

-

Cérience SAS (Terrena Group)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: France hosted the World Alfalfa Congress 2025 in Reims, marking the first time the event has been held in Europe. The event spotlighted French alfalfa production and sustainability initiatives, raising national attention to alfalfa's role in low-carbon farming.

- May 2024: Cérience SAS showcased new alfalfa mixtures (Alfamax, Linsey) and forage solutions at Salon de l'Herbe et des Fourrages (Grass and Forage Fair) 2024. The company positioned these seed innovations to support agroecological transitions and improved on-farm forage systems.

- January 2024: Cérience SAS has acquired Dutch seed company Vandinter Semo, expanding its forage and alfalfa seed portfolio and deepening its European production footprint. The combined genetic resources and capabilities position Cérience to strengthen its leadership in the French and broader European seed markets.

France Alfalfa Market Report Scope

Alfalfa is a nutrient-rich perennial flowering plant in the pea family, widely cultivated as livestock fodder. The France Alfalfa Market Report is Segmented by Product Type (Bales, Pellets, Cubes, and Compressed Bales), by Application (Dairy Cattle Feed, Beef Cattle Feed, Poultry Feed, Equine Feed, Small Ruminant Feed, Camelids and Other Livestock Feed), by End Use Sector (Commercial Farms, Compound Feed Manufacturers, Household and Hobby Animal Owners, and Pet Food and Specialty Nutrition). Market Forecasts are Provided in Value (USD) and Volume (Metric Tons).

By Product Type

| Bales |

| Pellets |

| Cubes |

| Compressed Bales |

By Application

| Dairy Cattle Feed |

| Beef Cattle Feed |

| Poultry Feed |

| Equine Feed |

| Small Ruminant Feed |

| Camelids and Other Livestock Feed |

By End Use Sector

| Commercial Farms |

| Compound Feed Manufacturers |

| Household and Hobby Animal Owners |

| Pet Food and Specialty Nutrition |

| By Product Type | Bales |

| Pellets | |

| Cubes | |

| Compressed Bales | |

| By Application | Dairy Cattle Feed |

| Beef Cattle Feed | |

| Poultry Feed | |

| Equine Feed | |

| Small Ruminant Feed | |

| Camelids and Other Livestock Feed | |

| By End Use Sector | Commercial Farms |

| Compound Feed Manufacturers | |

| Household and Hobby Animal Owners | |

| Pet Food and Specialty Nutrition |

Key Questions Answered in the Report

What is the 2026 value of the France alfalfa market?

The France alfalfa market stands at USD 1.25 billion in 2026 and is projected to reach USD 1.55 billion by 2031 at a 4.34% CAGR.

Which product type leads demand in France?

Bales are the largest product type with a 46.2% share in 2025 because they fit automated feeding systems and compound feed production.

Which application is growing the fastest?

Equine feed is the fastest application with a 5.6% CAGR from 2026 to 2031, supported by demand for digestive health and premium feeding formats.

Why does Grand-Est matter so much for alfalfa production?

Grand-Est accounted for 80% of output in 2025 because it has the strongest cooperative infrastructure, suitable soils, and dense dehydration capacity.

What is the main competitive threat to alfalfa in livestock feed?

Maize silage is the main competing forage because strong 2025 yield and energy values made it harder for alfalfa to defend standard ration space.

What is driving premium opportunities in this space?

Premium growth is coming from certified low-emission supply, pet food and specialty nutrition, and application-led formats such as cubes for equine health.

Page last updated on: