Forensic Accounting Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

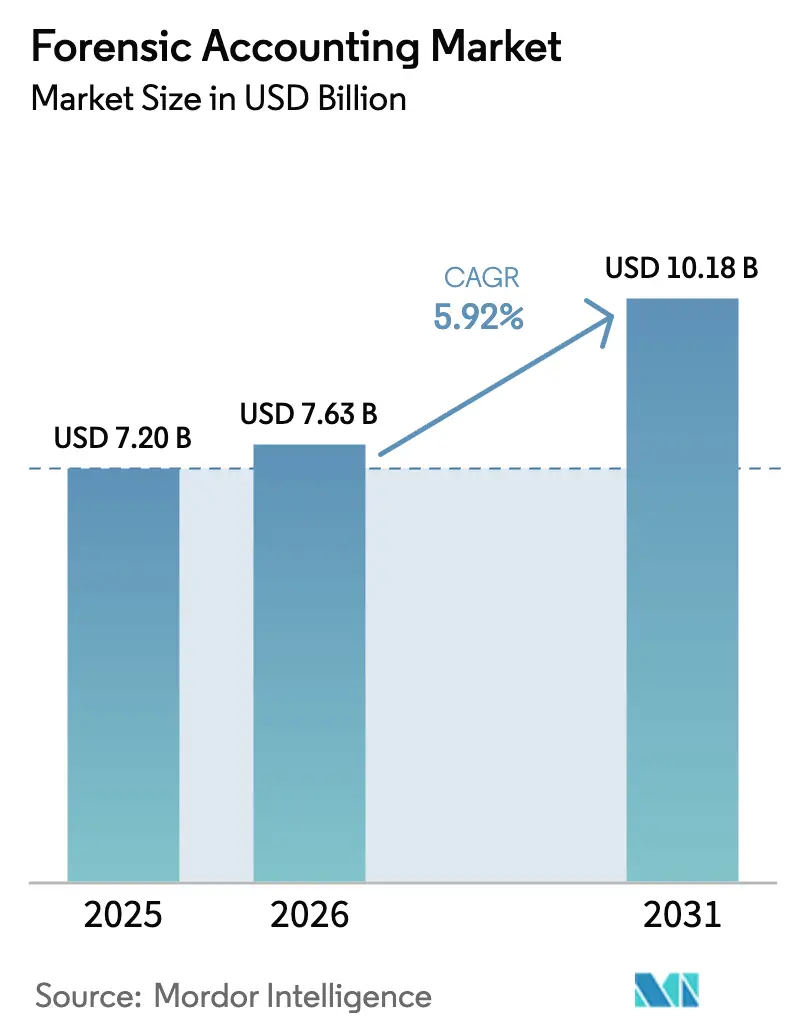

| Market Size (2026) | USD 7.63 Billion |

| Market Size (2031) | USD 10.18 Billion |

| Growth Rate (2026 - 2031) | 5.92% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

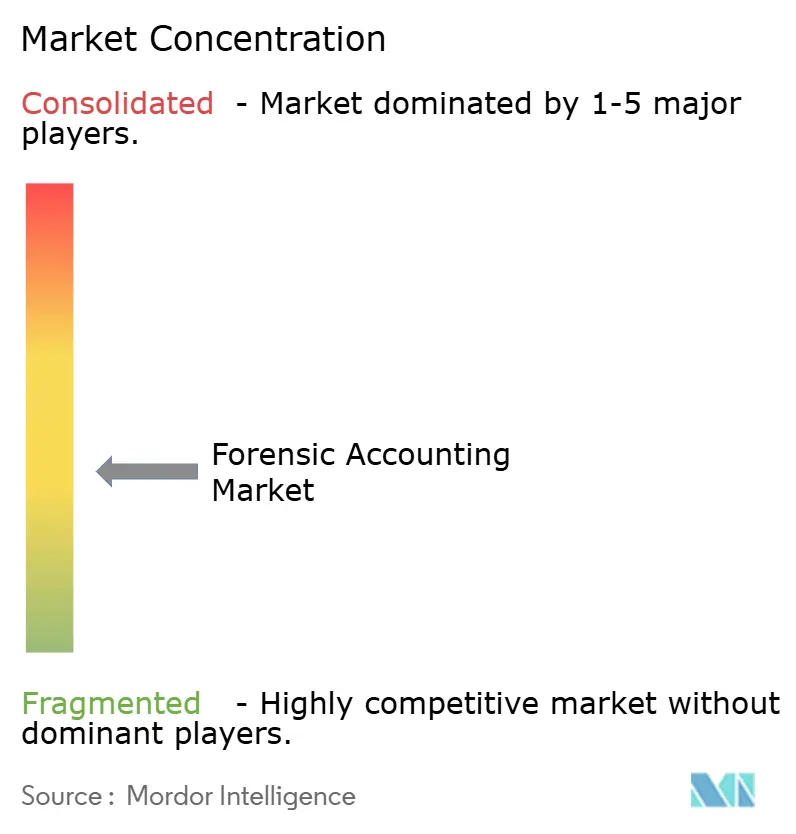

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Forensic Accounting Market Analysis by Mordor Intelligence

The forensic accounting market size is expected to grow from USD 7.20 billion in 2025 to USD 7.63 billion in 2026 and is forecast to reach USD 10.18 billion by 2031 at 5.92% CAGR over 2026-2031. Strong growth reflects the convergence of escalating cyber-enabled fraud, intensifying anti-money-laundering mandates, and rapid adoption of advanced analytics across investigations. Financial institutions remain the largest single demand centre, yet public agencies, healthcare payers, and energy companies are enlarging the client base as transparency laws tighten, and ESG-linked litigation accelerates. Technology has become the decisive competitive lever: firms embedding AI-driven anomaly detection, blockchain forensics, and multilingual e-discovery solutions are widening their addressable revenue pools. At the same time, shortages of qualified specialists, rising software licensing costs, and privacy-driven data-access constraints temper expansion prospects in the short run.

Key Report Takeaways

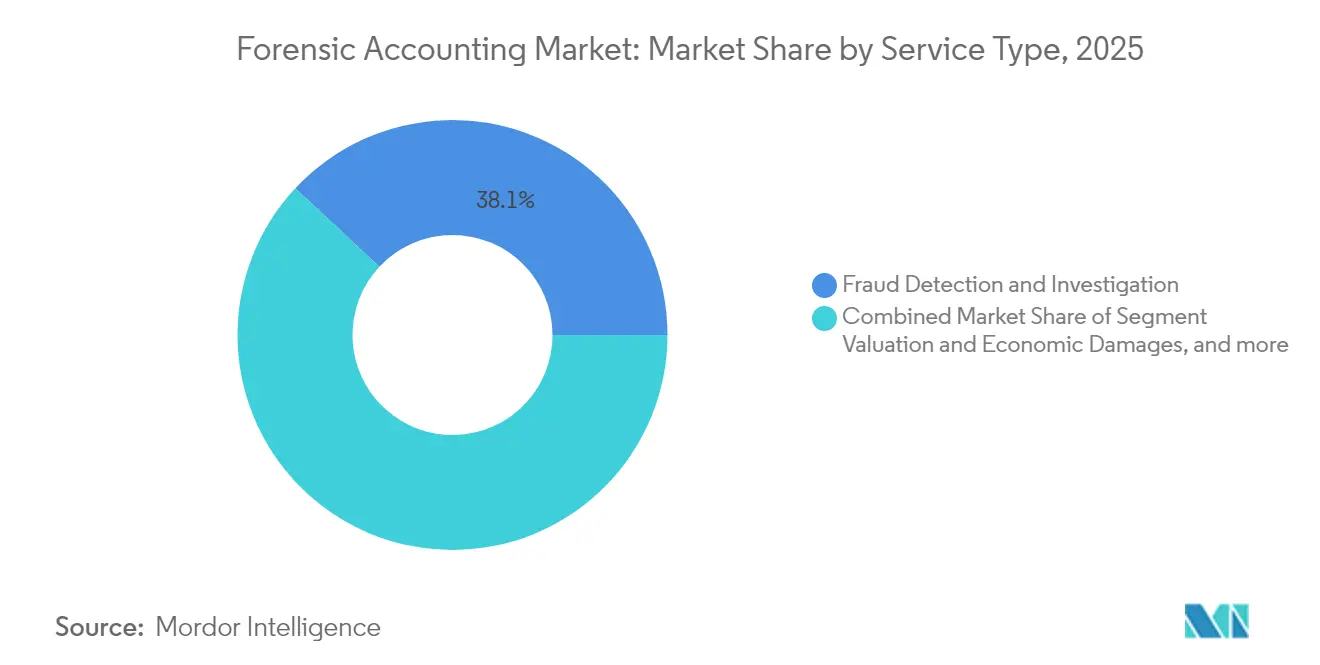

- By service type, Fraud Detection & Investigation held 38.05% of the forensic accounting market share in 2025, while Risk Management & Compliance is projected to register the fastest 8.92% CAGR through 2031.

- By end-user industry, Banking, Financial Services & Insurance commanded 41.12% revenue in 2025; Government & Public Sector is set to grow at an 8.44% CAGR to 2031.

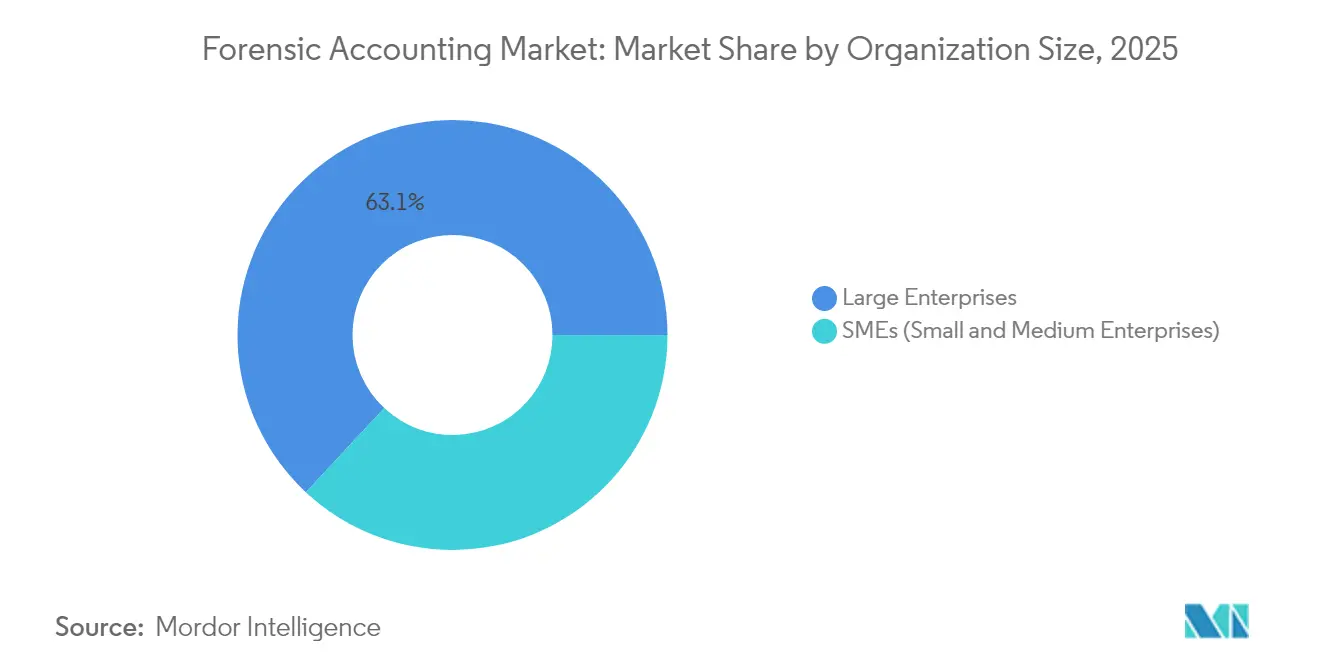

- By organisation size, large enterprises accounted for 63.05% share of the forensic accounting market size in 2025, whereas the SME segment is on track for a 9.28% CAGR through 2031.

- By geography, North America commanded 40.25% revenue in 2025; Asia-Pacific is set to grow at a 10.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Forensic Accounting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating corporate fraud incidence & financial crimes | +1.8% | Global, with a concentration in North America & Europe | Medium term (2-4 years) |

| Stricter regulatory compliance & AML requirements | +1.5% | Global, led by EU AML/CFT regime and US PCAOB standards | Long term (≥ 4 years) |

| Integration of data analytics & AI in forensic audits | +1.2% | North America & Europe early adoption, APAC following | Short term (≤ 2 years) |

| Digitalization-driven cyber fraud in BFSI | +0.9% | Global, with the highest impact in digitally advanced markets | Medium term (2-4 years) |

| ESG-linked litigation boosting demand | +0.7% | North America & Europe primarily | Medium term (2-4 years) |

| PE-backed law firms driving dispute valuations | +0.4% | North America & Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Corporate Fraud Incidence & Financial Crimes

Corporate fraud volumes continue to rise as perpetrators weaponise generative AI, cryptocurrencies and synthetic identities to evade conventional controls. Regulators have responded with larger whistle-blower awards and novel transparency statutes, fuelling demand for deep-dive forensic reviews across payroll, vendor and royalty streams. Notable cases, such as a USD 10 million music-streaming scam built entirely on AI-generated content, demonstrate how digital channels multiply opportunities for deception. The UK’s 2024 Economic Crime Act now obliges corporates to deter fraud proactively, pushing boards to commission preventive forensic mandates. As enforcement widens beyond financial statements into cyber and operational areas, the forensic accounting market benefits from a broader, multi-disciplinary scope of work.

Stricter Regulatory Compliance & AML Requirements

The EU Anti-Money-Laundering Regulation (EU 2024/1624) establishes AMLA and broadens “obliged entities” to include accounting and crypto-asset service providers, expanding compliance workloads from 2028[1]European Parliament, “Regulation (EU) 2024/1624 on the Prevention of Money Laundering,” europarl.europa.eu. In the US, the PCAOB’s proposed NOCLAR standard demands auditors actively search for non-compliance, effectively injecting forensic techniques into routine audits. Hong Kong banks, under heightened HKMA scrutiny, now earmark larger budgets for analytics-led investigations, while the UAE’s SCA circular requires COSO-aligned internal-control audits from 2025. These overlapping statutes increase complexity, prompting corporates to outsource specialised reviews to providers with cross-jurisdictional expertise. Consequently, proactive risk-management engagements are eclipsing ad-hoc fraud probes in revenue importance.

Integration of Data Analytics & AI in Forensic Audits

Machine-learning models such as EY Helix GL Anomaly Detector triple anomalous-entry hit rates compared with rules-based tests, compressing review timetables for multi-billion-row ledgers. Grant Thornton reports that natural-language processing cut document vetting from months to days, reducing billable hours on routine tasks but freeing consultants for higher-value analysis. March 2025 saw FTI Consulting release IQ.AI for Review, an AI reviewer that flags privilege, foreign-language risk, and sentiment in real time, extending applicability to complex cross-border litigations[2]FTI Consulting, “FTI Technology Unveils IQ.AI for Review,” fticonsulting.com . Such tools allow mid-tier firms to challenge incumbents on speed and pricing, intensifying competition inside the forensic accounting market. Simultaneously, regulators insist auditors understand algorithmic biases, raising the technical bar for practitioner accreditation.

Digitalization-Driven Cyber Fraud in BFSI

Banks undergoing digital overhaul report a parallel upswing in account takeover, authorised push payment, and synthetic identity attacks, with traditional rules engines capturing some of the events. AI-powered surveillance platforms now monitor data flows in real time, generating granular forensic trails that feed both compliance and dispute-resolution workflows. However, implementing these systems requires substantial capital and specialist skill sets, making outsourcing the default option for Tier 2 and cooperative lenders. Cryptocurrency rails add further investigative complexity by blending pseudonymous wallets with fiat flows, compelling institutions to seek blockchain forensic expertise. As monetary authorities demand demonstrable controls, forensic engagements tied to cyber fraud have shifted from episodic to programmatic, materially enlarging the forensic accounting market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of qualified forensic accountants | -1.4% | Global, particularly acute in emerging markets | Long term (≥ 4 years) |

| High cost of software & investigations | -0.8% | SME segment globally, emerging markets | Medium term (2-4 years) |

| Client data-privacy reluctance | -0.6% | Europe (GDPR), Asia-Pacific privacy regulations | Short term (≤ 2 years) |

| Automation is shrinking routine billable hours | -0.5% | Developed markets with high automation adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shortage of Qualified Forensic Accountants

Universities remain slow to embed multi-disciplinary fraud analytics into core curricula, leaving graduates under-prepared for fast-evolving practice requirements. Big Four firms in India alone forecast 80,000 new roles, yet talent pipelines lag, especially for cyber forensics and e-discovery specialists. Professional organizations emphasize a comprehensive array of investigative methodologies, reflecting a significant learning curve that may hinder the entry of new participants. Scarcity inflates wage costs and stretches project timelines, notably in emerging markets where on-shore expertise is thin. Unless distance-learning and apprenticeship models scale rapidly, capacity constraints could cap the forensic accounting market’s attainable growth ceiling.

High Cost of Software & Investigations

High costs of enterprise licenses for graph analytics, blockchain tracing, and AI-enabled review suites often restrict access for smaller audit firms and corporate users, as these expenses frequently exceed annual budgets. SMEs struggle to justify full-scope forensic engagements when potential recoveries are modest, creating pockets of latent but untapped demand. New SEC rules obliging third-party valuations in adviser-led secondary transactions impose additional compliance spend on mid-market private-equity funds. As cost-benefit equations narrow, buyers opt for lite-version diagnostics, limiting fee pools despite underlying risk. Cloud-based subscription tools are gradually easing barriers, yet price remains a meaningful restraint in the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Fraud Detection Leads Despite Compliance Surge

Fraud Detection & Investigation produced the largest revenue contribution, holding 38.05% of the forensic accounting market share in 2025. Surging AI-driven payment frauds, false-invoice rings and cryptocurrency theft keep demand elevated, anchoring the service line’s dominance. Risk Management & Compliance, although smaller, is expanding at a 8.92% CAGR as boards prioritise preventative frameworks over post-event inquiries. This pivot aligns with regulators mandating continual controls testing, prompting enterprises to bundle compliance consulting with assurance mandates. Litigation Support & Dispute Resolution gains traction too, fuelled by cross-border M&A, ESG-related class actions and private-equity secondary deals that require valuation testimony.

The forensic accounting market size for cyber forensics, sitting within the “Others” category, is forecast to multiply as ransomware and crypto investigations converge. Blockchain analytics firms increasingly partner with traditional practices to follow illicit token flows, embedding real-time dashboards that courts now accept as evidentiary artefacts. Insurance-claim probes are likewise rising, as digitised policy administration exposes fresh fraud vectors during claim filing and adjustment cycles. Ethical use of AI remains a live debate, with practitioners balancing investigatory breadth against privacy obligations under GDPR and CCPA. Providers able to integrate low-code analytics, multilingual review bots and qualified testimony stand to capture disproportionate wallet share as the forensic accounting market evolves.

By End-User Industry: BFSI Dominance Challenged by Government Growth

Banking, Financial Services & Insurance preserved its 41.12% share of 2025 revenue, sustained by perennial AML, sanctions and cyber-fraud pressures. Yet Government & Public Sector is accelerating at an 8.44% CAGR to 2031, buoyed by transparency statutes and federal recovery audits recouping pandemic funds. Healthcare organisations are another emergent buyer group, reacting to False Claims Act enforcement on Medicare Advantage coding practices. Manufacturing and energy companies commission ESG-linked investigations into supply-chain and carbon-credit assurance, widening sectoral spread. Retail and e-commerce players, grappling with synthetic identities and loyalty points theft, increasingly seek digital fraud expertise unavailable in-house.

Demand heterogeneity forces providers to craft industry-specific playbooks covering differing regulatory lexicons, data architectures, and risk taxonomies. Within finance, stablecoin-related compliance reviews now complement legacy AML engagements, whereas public agencies favour enterprise-risk management roadmaps anchored in COSO. Life-science firms focus on speaker-bureau and market-access controls amid heightened DOJ scrutiny, while utilities demand carbon-offset verification amid investor activism. This multifaceted landscape reinforces the forensic accounting market’s need for deep vertical knowledge alongside cross-disciplinary investigative technique. Firms that combine sector fluency with scalable analytics are outpacing peers in both win-rates and price-realisation.

By Organization Size: SME Segment Drives Future Growth

Large enterprises generated 63.05% of the forensic accounting market size in 2025 due to complex, multi-jurisdictional engagements that favour global networks. However, SMEs represent the fastest-growing cohort at 9.28% CAGR as cloud platforms and subscription analytics lower entry barriers. Regulatory authorities no longer exempt smaller entities from AML and data-protection rules, compelling them to seek external guidance. Outsourced forensic hotlines, remote log-capture tools and modular e-discovery bundles now allow mid-market firms to buy only what they need, reducing cost friction. Private-equity sponsorship of mid-cap roll-ups further lifts demand for pre-deal forensic due diligence and post-merger integration audits.

The forensic accounting market share captured by tech-enabled boutiques serving SMEs is expanding as they leverage virtual teams and workflow automation to undercut incumbents on price without eroding margins. FinTech and RegTech collaborations also speed onboarding and continuous transaction monitoring, giving SMEs near-enterprise-grade defences. Cross-border e-commerce exposes smaller merchants to international VAT fraud risks, creating incremental sales opportunities for advisors versed in multi-jurisdictional rules. Skills shortages remain acute at the SME level, reinforcing the preference for managed-service outsourcing over in-house build. Over time, scaled delivery hubs in lower-cost geographies are expected to equalise access, supporting inclusive growth across the forensic accounting market.

Geography Analysis

North America remains the largest regional contributor with a CAGR of 40.25%, sustained by vigorous SEC and DOJ enforcement programmes that amplify whistle-blower payouts and expand investigative scopes. Cross-border trade via USMCA elevates compliance complexity for Canadian and Mexican corporates, funnelling more disputes into US courts where discovery standards are stringent. Market maturity has spurred a pivot towards technology-driven productivity, with AI-assisted reviews routinely embedded in engagements. Nonetheless, regulatory discussion around AI governance introduces uncertainty, prompting providers to maintain human-in-the-loop safeguards. Mid-tier firms are edging into cyber and ESG niches that the Big Four have historically underserved, gradually diversifying the competitive roster across the forensic accounting market.

Europe offers the highest long-run upside, energised by the EU’s AMLA rollout and expanding ESG-disclosure mandates. The UK’s post-Brexit environment layers additional domestic compliance, including the 2024 Economic Crime Act that criminalises failure to prevent fraud, catalysing forensic demand. GDPR remains both a constraint and an opportunity: strict data-transfer rules complicate cross-border probes yet fuel advisory work on privacy-compliant methodologies. Mid-sized providers with multilingual capacity find Europe fertile ground for share gains as global networks prioritise higher-margin US mandates.

Asia-Pacific is projected to clock the fastest CAGR of 10.05% to 2031, backed by India’s Big Four revenue targets exceeding INR 450 billion (USD 5.4 billion) in FY25 amid robust consulting and tech spend economictimes.com. Rising digital-payment penetration in Southeast Asia escalates cyber-fraud exposure, compelling banks to add AI-enhanced monitoring and forensic-readiness tooling. China’s focus on capital-markets integrity and Hong Kong’s strengthened AML code elevate demand for onshore specialists conversant with bilingual evidentiary standards. Meanwhile, PwC’s withdrawal from nine Sub-Saharan African countries has redirected some international work to Asian delivery centres, accelerating skill-cluster formation. Together, these factors push the forensic accounting market toward a more balanced global revenue profile by decade-end.

Competitive Landscape

Competitive intensity is shaped by moderate concentration: the top five players account for almost half of global revenue, yet the Big Four alone control majority of high-value mandates in markets like India. Regulatory inquiries into audit concentration and potential conflicts of interest are encouraging corporates to test alternative providers, particularly for cyber forensics and ESG investigations. Chambers Rankings now list Alvarez & Marsal, Forensic Risk Alliance and FTI Consulting alongside the traditional leaders, signalling a more plural competitive field chambers.com. Technology investment remains the primary differentiator; KPMG’s 2025 launch of KPMG Law US illustrates a strategy of embedding end-to-end legal-forensic solutions that could redraw market boundaries.

Private-equity fuelled consolidation is also reshaping mid-market dynamics, exemplified by the USD 7 billion Baker Tilly–Moss Adams merger that created the US’s sixth-largest CPA network[3]The Finance Story, “Inside the Baker Tilly–Moss Adams USD 7 Billion Tie-up,” thefinancestory.com . Such deals generate integration risk that, in turn, creates fresh forensic workstreams around data-migration validation and cultural-fit assessments. Pricing pressure has intensified in India and select ASEAN markets as local consultancies undercut global rates, prompting the Big Four to emphasise value-added analytics. Simultaneously, point-solution disruptors offering AI-as-a-service for anomaly detection compete for slices of scope that once sat exclusively within audit engagements. The forensic accounting market’s technology arms race is therefore likely to continue, rewarding firms able to standardise digital workflows while retaining courtroom-defensible rigour.

Forensic Accounting Industry Leaders

PwC

Deloitte

KPMG

Ernst & Young (EY)

FTI Consulting

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: PwC disclosed 1,500 global layoffs, signalling margin compression that may spur further market consolidation.

- April 2025: Baker Tilly and Moss Adams completed their USD 7 billion merger, creating a USD 6 billion revenue firm projected for 2030.

- April 2025: PwC exited nine Sub-Saharan African markets, opening competitive gaps for regional midsized firms.

- February 2025: KPMG LLP launched KPMG Law US, the first Big Four-owned law firm in the US, leveraging AI platforms for managed legal and forensic services.

Global Forensic Accounting Market Report Scope

Forensic accounting, also known as forensic audit, is the practice of examining financial data for signs of criminal activity. The forensic accounting market is segmented by enterprise size (large enterprises and small and medium enterprises), by industry vertical into automotive, and by BFSI. Healthcare, travel and hospitality, media and entertainment, government and public sector), by application (business fraud, tax fraud, securities fraud, asset misappropriation or hidden assets, partnership and shareholding dispute, insurance claims, economic losses and bankruptcy, money laundering, marital and family disputes by region, the market is segmented into North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa. The report offers market size and forecasts for the forensic accounting market in value (USD) for all the above segments.

| Fraud Detection & Investigation |

| Litigation Support & Dispute Resolution |

| Valuation & Economic Damages |

| Risk Management & Compliance |

| Others (Cyber Forensics, Insurance Claims, etc.) |

| Banking, Financial Services & Insurance (BFSI) |

| Government & Public Sector |

| Healthcare |

| IT & Telecom |

| Manufacturing |

| Energy & Utilities |

| Retail & E-commerce |

| Others |

| Large Enterprises |

| Small & Medium Enterprises (SMEs) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX | |

| NORDICS | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| South-East Asia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East & Africa |

| By Service Type | Fraud Detection & Investigation | |

| Litigation Support & Dispute Resolution | ||

| Valuation & Economic Damages | ||

| Risk Management & Compliance | ||

| Others (Cyber Forensics, Insurance Claims, etc.) | ||

| By End-user Industry | Banking, Financial Services & Insurance (BFSI) | |

| Government & Public Sector | ||

| Healthcare | ||

| IT & Telecom | ||

| Manufacturing | ||

| Energy & Utilities | ||

| Retail & E-commerce | ||

| Others | ||

| By Organization Size | Large Enterprises | |

| Small & Medium Enterprises (SMEs) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX | ||

| NORDICS | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

What is the current size of the forensic accounting market?

The forensic accounting market is valued at USD 7.63 billion in 2026 and is projected to reach USD 10.18 billion by 2031.

Which service line is growing the fastest?

Risk Management & Compliance services are expanding at the highest 8.92% CAGR as companies shift from reactive investigations to preventive controls.

Why is the Government & Public Sector segment important?

Public agencies are adopting AI-enabled fraud-prevention tools, giving the segment an 8.44% CAGR—faster than any other industry group through 2031.

What role does AI play in modern forensic accounting?

Machine-learning tools now flag anomalies, classify privilege, and trace blockchain transactions, trimming review timelines from months to days and lowering total investigation costs.

How concentrated is the competitive landscape?

The top five firms generate nearly half of global revenue, indicating a moderately concentrated market structure and presenting growth opportunities for mid-tier specialized players.

What is the biggest challenge facing market growth?

A shortage of qualified forensic accountants—particularly those with cyber forensics skills—continues to raise wage costs and extend project timelines worldwide

Page last updated on: