Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

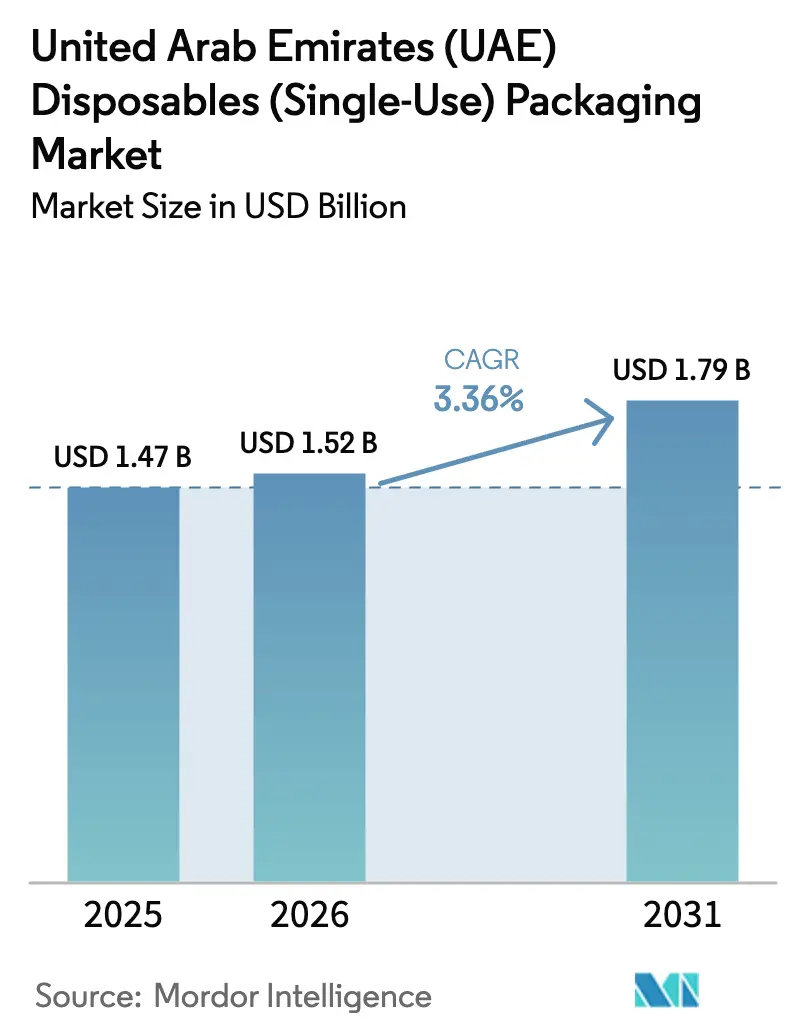

| Base Year Market Size (2025) | USD 1.47 Billion |

| Market Size (2026) | USD 1.52 Billion |

| Market Size (2031) | USD 1.79 Billion |

| Growth Rate (2026 - 2031) | 3.36% CAGR |

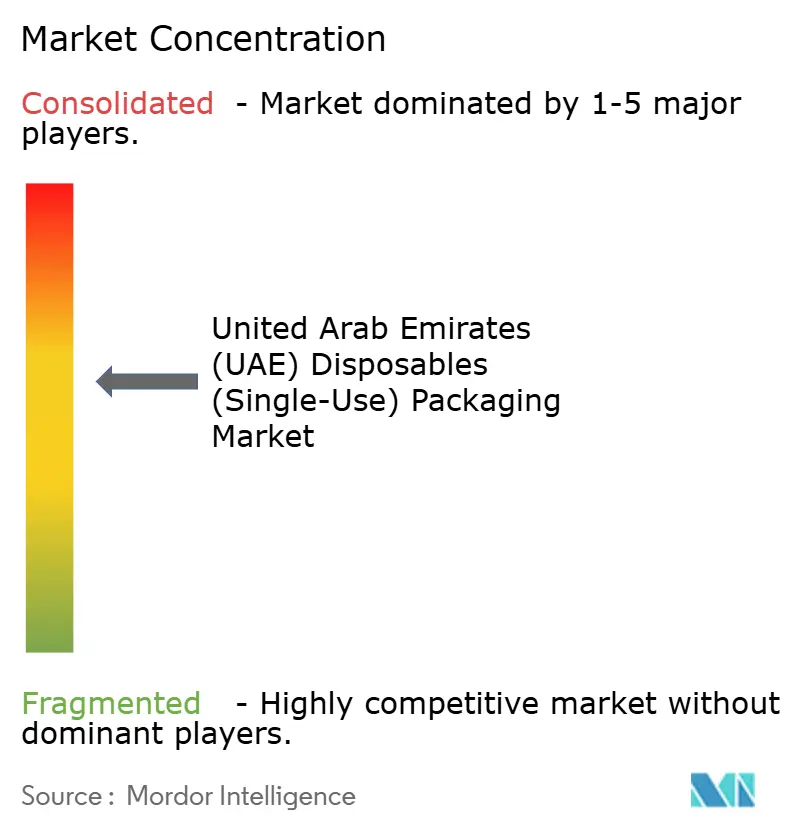

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Arab Emirates (UAE) Disposables (Single-Use) Packaging Market Analysis by Mordor Intelligence

The United Arab Emirates disposables packaging market size is expected to increase from USD 1.52 billion in 2026 to USD 1.79 billion by 2031, growing at a CAGR of 3.36% over 2026-2031. Demand is pivoting toward paperboard and bioplastic substrates as the January 2026 federal ban on selected single-use plastic products forces restaurants and coffee chains to eliminate polystyrene foam and conventional plastic cups. Quick-service operators have accelerated material-substitution projects, while local converters wrestle with resin price swings and new extended producer responsibility (EPR) compliance costs. Emirates Biotech’s November 2025 launch of locally produced PLA has shortened lead times to two weeks and reduced import freight premiums, giving domestic converters a cost-plus logistics advantage. At the same time, the tourism rebound, mega-event pipeline, and fast-growing online-food-delivery ecosystem continue to lift per-capita takeaway volumes, anchoring steady growth for the UAE disposables packaging market.

Key Report Takeaways

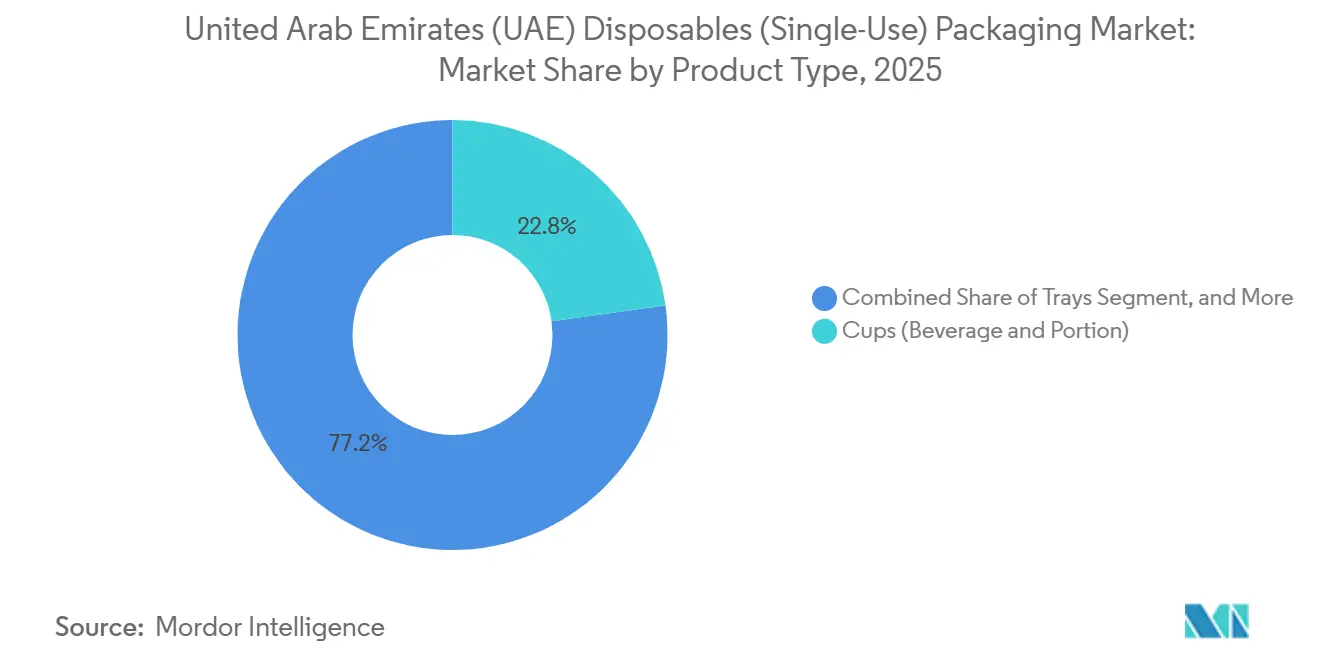

- By product type, cups held 22.80% of the United Arab Emirates (UAE) disposables (single-use) packaging market share in 2025, while bioplastic cups are projected to expand at a 5.17% CAGR through 2031.

- By end user, quick-service restaurants captured 29.63% of demand in 2025, whereas coffee and snack outlets are forecast to grow at 4.51% annually through 2031.

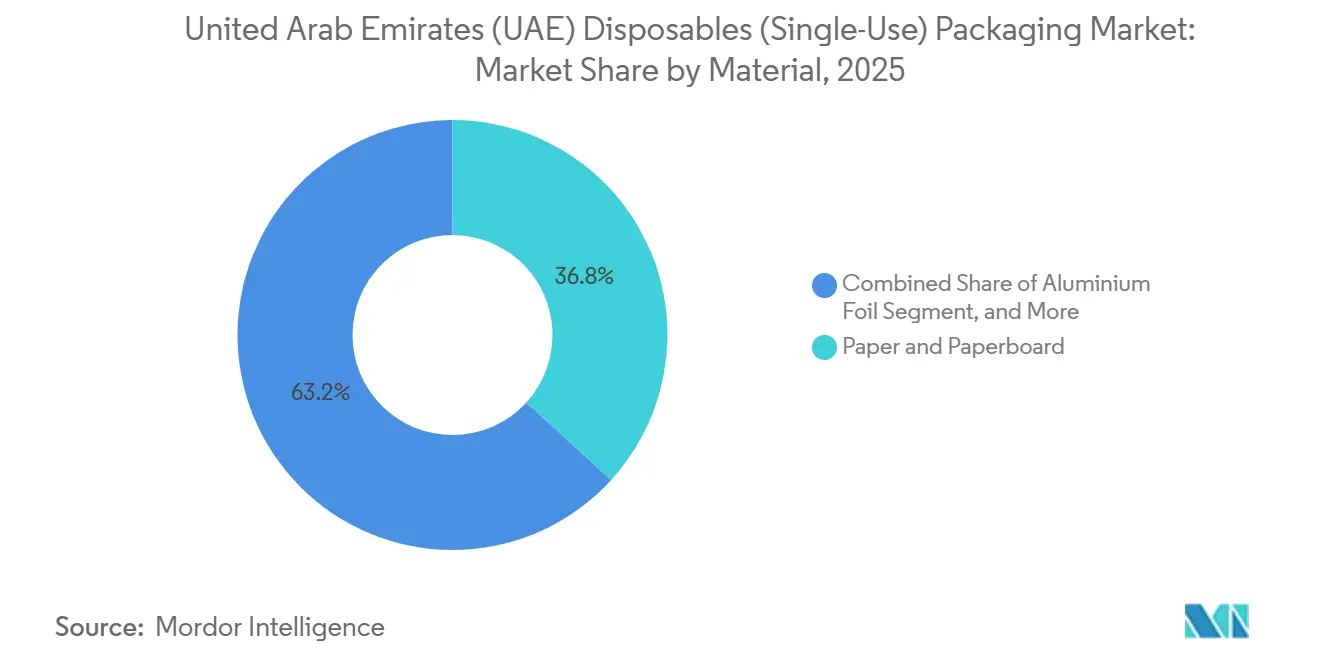

- By material, paper and paperboard accounted for 36.77% of the UAE disposables packaging market size in 2025, and bioplastics are set to grow at a 4.32% CAGR to 2031.

- By distribution channel direct, food-service distributors commanded 42.90% of channel volume of the United Arab Emirates (UAE) disposables (single-use) packaging market in 2025; e-commerce webstores are advancing at a 4.11% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Arab Emirates (UAE) Disposables (Single-Use) Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth Of Online Food-Delivery Platforms | +0.8% | Dubai, Abu Dhabi, Sharjah | Short Term (≤ 2 Years) |

| Expansion Of Quick-Service And Coffee Chains | +0.7% | Dubai, Abu Dhabi | Medium Term (2–4 Years) |

| Government Ban Timeline For Selected Single-Use Plastics | +0.6% | All Seven Emirates | Short Term (≤ 2 Years) |

| Tourism Rebound And Mega-Events Legacy | +0.5% | Dubai, Abu Dhabi | Medium Term (2–4 Years) |

| Commissioning Of World-Scale PLA Plant In UAE | +0.4% | Abu Dhabi, GCC | Long Term (≥ 4 Years) |

| Airline Caterers Closed-Loop Tray-To-Tray Recycling Programs | +0.2% | Dubai Aviation Hubs | Medium Term (2–4 Years) |

| Source: Mordor Intelligence | |||

Growth of Online Food-Delivery Platforms

Aggregator apps account for 75% of delivery orders in the UAE, and each transaction consumes three to five single-use items, creating packaging intensity that dine-in formats do not match. Younger consumers now place 4 to 6 delivery orders per month, double the 2020 level, locking restaurants into multi-year supply contracts for microwave-safe, leakproof formats. Cloud-kitchen clusters in Dubai and Sharjah amplify demand, while pilot reusable-container schemes remain below 2% penetration, keeping single-use formats dominant.

Expansion of Quick-Service and Coffee Chains

The quick-service segment was valued at USD 5.25 billion in 2024 and is growing at 19.2% a year as franchisees roll out new outlets. Every store typically consumes 200-300 kg of disposable cups, lids and takeaway boxes monthly. Coffee chains add incremental volume because a single drink requires multiple components, and the rise of iced beverages favors clear PLA or PET cups. Corporate sustainability mandates push premium brands to pay 15-25% more for certified-compostable SKUs, widening the price gap with value chains.[1]Emirates Group, “Sustainability Report 2025,” emirates.com

Government Ban Timeline for Selected Single-Use Plastics

The final phase of the federal ban took effect on 1 January 2026, prohibiting polystyrene foam containers, plastic beverage cups, cutlery, and straws. PLA and other certified bioplastics are exempt, channeling demand toward converters that can run bio-resins on existing lines. Abu Dhabi’s earlier plastic-bag ban proved that enforcement paired with retailer audits can shift demand within 18 months. The upcoming EPR regime will add 3-5% to landed costs, tightening margins for small converters.

Tourism Rebound and Mega-Events Legacy

Travel and tourism contributed AED 220 billion (USD 59.9 billion) to GDP in 2023 and visitor spending hit AED 175 billion (USD 47.7 billion). Airports handled more than 103 million passengers by September 2024, and large conferences can consume 500,000 disposable units in three days. Emirates Flight Catering, producing 225,000 meals daily, now recycles used plastic trays into pellets with 25% recycled content, trimming virgin-resin demand by 1,200 tonnes a year.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Raw-Material Price Volatility | -0.5% | Global Feedstock, UAE Converters | Short Term (≤ 2 Years) |

| Limited Industrial Composting And Recycling Infrastructure | -0.4% | UAE-Wide | Medium Term (2–4 Years) |

| Stringent EPR-Style Labeling And Compliance Costs For SMEs | -0.3% | All Emirates | Short Term (≤ 2 Years) |

| Rising Consumer Skepticism Of Oxo-Degradable Claims | -0.2% | UAE, Middle East | Medium Term (2–4 Years) |

| Source: Mordor Intelligence | |||

Escalating Raw-Material Price Volatility

Polyolefin prices track swings in crude oil and natural gas, while pulp for cup stock reached USD 1,400 per tonne in 2025. Small UAE converters lack scale to hedge feedstock exposure and often face 15-day payment terms to resin suppliers but grant 60-day terms to restaurant clients, stressing working capital. Freight risks persist because most PET, PS, and PLA still arrive from Asia or Europe until local PLA capacity starts up in 2028.[2]Borouge, “Borouge 4 Project Overview,” borouge.com

Limited Industrial Composting and Recycling Infrastructure

Most PLA, PHA, and bagasse packaging ends up in waste-to-energy plants because the UAE lacks high-temperature industrial composters. Tadweer’s 1.3 million-tonne material-recovery facility, due online in 2026, will prioritize PET, aluminum, and cardboard. Without credible end-of-life pathways, consumer surveys show 60-70% of residents doubt that “biodegradable” items actually break down locally, undermining willingness to pay price premiums.[3]Dubai Municipality, “Waste Management Initiatives,” dm.gov.ae

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Cups Anchor Demand While Bioplastic Variants Accelerate

Cups generated 22.80% of the revenue of the United Arab Emirates (UAE) disposables (single-use) packaging market in 2025, underpinned by the Emirates’ dense café network and the 70% of delivery orders that include beverages. Bioplastic cups are projected to expand at a 5.17% CAGR through 2031, fueled by the 2026 plastic-cup ban and the local availability of Embio PLA. Conventional plastic cups will retreat as chains lock in PLA-lined hot cups and clear PLA cold cups to de-risk compliance. Containers, trays, and clamshells together contribute roughly one-third of volume, aided by meal-kit operators that need microwave-safe formats. Wood stirrers and paper straws have replaced banned plastic variants, but user experience complaints are prompting some brands to delete stirrers entirely. A two-tier market is emerging: commodity napkins and generic containers face intense price competition, while certified-compostable or custom-printed SKUs command 20-30% margins, favoring agile domestic converters.

Value-focused operators in the Northern Emirates still opt for low-density polyethylene sandwich pouches and unlined kraft boxes, whereas premium brands in Dubai malls insist on PLA-coated board that withstands oily fillings. Lid and dome sales remain a profit pool because vented and tamper-evident designs are difficult to import in small lots. Going forward, local thermoformers plan to run multi-cavity tools capable of quick changeovers, enabling sub-24-hour delivery of small-batch clamshells that suit ghost-kitchen menu rotations. The UAE disposables packaging market thus rewards converters that balance cost, compliance and turnaround speed.

By End-User Application: Quick-Service Dominance, Coffee Outlets Outpace Growth

Quick-service restaurants controlled 29.63% of unit demand in 2025 because 90-95% of their transactions require disposables. Coffee and snack outlets are expected to grow 4.51% annually to 2031, propelled by 200-300 new specialty-coffee stores and higher iced-drink sales that need clear domed cups. Full-service restaurants use disposables mainly for delivery and takeaway and will expand more slowly. Retail channels such as supermarkets and petrol stations lean on hinged clamshells for salads and hot bars, producing stable mid-single-digit growth.

Institutional catering remains price-sensitive, awarding tenders to the lowest bidder each year, although federal contracts now stipulate minimum recycled-content requirements. Hospitality and events face strong seasonality, with November-March outdoor festivals triggering demand spikes that require 20-30% buffer stock. Ghost kitchens compound SKU complexity because each virtual brand expects distinctive graphics and shapes, pushing converters toward digital printing and smaller lot sizes. These patterns ensure the UAE disposables packaging market stays fragmented and innovation-driven.

By Material: Paper Leads, Bioplastics Gain Share

Paperboard held a commanding 36.77% share of the United Arab Emirates (UAE) disposables (single-use) packaging market in 2025, driven by printability and existing recycling streams in Dubai and Abu Dhabi. Bioplastics will expand at a 4.32% CAGR as the 160,000-tonne PLA plant comes online in 2028, shrinking today’s 4-6 week import lead times. Conventional plastics still account for roughly 28-30% of the UAE's disposable packaging market because clear cold-drink cups and microwaveable containers require properties that paper and early-generation biopolymers cannot match.

Aluminum foil trays are steady niche performers in airline catering thanks to heat retention and recyclability. Bagasse and molded-fiber tableware are growing at near 4% as restaurants chase visible sustainability cues, but moisture-resistance limitations confine them to dry foods unless coated with PLA. Material choices increasingly reflect end-of-life pathways: operators favor substrates that align with Dubai’s curbside recycling for paper and cans, while uncertainty around composting slows adoption of premium bioplastic formats despite regulatory exemptions.

By Distribution Channel: Direct Distributors Command Volume, E-Commerce Scales

Specialized food-service distributors moved 42.90% of tonnes in 2025, holding large inventories and offering next-day deliveries. Cash-and-carry warehouses in Deira and Al Quoz cater to independent eateries that need to inspect quality on site. E-commerce webstores are climbing at a 4.11% CAGR through 2031 as cloud-kitchen operators appreciate online catalogs that list certifications and accept small orders. Group purchasing organizations aggregate demand from franchise chains and institutional caterers, leveraging 10-15% cost savings and driving specification standardization.

Manufacturers are experimenting with direct online configurators that deliver custom-printed packs within 48 hours, bypassing wholesalers. Aggregator-owned micro-fulfilment centers already stock high-velocity SKUs such as cups and cutlery, signaling a future in which delivery platforms may disintermediate legacy distributors. The United Arab Emirates (UAE) disposables packaging market thus sees channel strategies converge around speed, transparency, and digital integration.

Geography Analysis

Dubai and Abu Dhabi together generate roughly 70-75% of the United Arab Emirates (UAE) Disposables (single-use) packaging consumption, reflecting dense restaurant footprints, high tourist volumes, and large expatriate populations inclined to order takeaway. Dubai processed 87 million passengers through its two airports in 2024, creating heavy demand for airline catering and food court services. Abu Dhabi adds institutional volumes from federal ministries, schools and hospitals and is investing in the nation’s first greenfield material-recovery facility, scheduled for 2026, which could shift material preferences toward readily recyclable substrates.

Sharjah, Ajman, and the Northern Emirates account for the remaining 20-25% but lean toward conventional paper and plastic owing to sharper price sensitivity. Enforcement capacity also diverges: Dubai executed the January 2026 plastic ban on schedule, while smaller emirates lag in audits, producing a two-speed compliance landscape. Nonetheless, the federation’s compact geography enables same-day deliveries between Dubai, Abu Dhabi, and Sharjah, letting converters serve all emirates from central warehouses and maintain lean stocks.

Tourism cycles accentuate regional patterns. Dubai’s event calendar peaks in the milder winter and again in midsummer for Gulf tourist inflows, each wave triggering disposable-packaging surges for outdoor festivals and mall food courts. Abu Dhabi’s Formula 1 and government conferences produce acute, date-specific spikes that distributors cover with 20-30% buffer stock. These dynamics require converters to combine flexible production with granular demand forecasting, keeping the UAE disposables packaging market responsive to geographic demand shifts.

Competitive Landscape

The United Arab Emirates (UAE) disposables packaging market remains fragmented: no player exceeds 8-10%, and the top five together hold under 35%. Hotpack Packaging, Al Bayader International, and Falcon Pack operate multi-line plants for cups, containers, and foil, while Huhtamaki Flexibles UAE and Detpak leverage global R and D to supply certified-compostable ranges. White-space opportunities cluster in PLA-lined cups, short-run custom clamshells, and closed-loop recycling programs.

Technology investments differentiate leaders. Al Bayader doubled its Jebel Ali capacity to 18,000 tonnes annually and rolled out Sukkar sugarcane packaging and Bio’d bio-based alternatives. Emirates Biotech’s Embio PLA supply narrows cost gaps with imports and supports converters’ compliance timelines. Borouge’s USD 6.2 billion Borouge 4 expansion will lift domestic polyethylene capacity to 6.4 million tonnes by late 2026, securing feedstock for microwave-safe containers but offering limited help for bioplastic demand.

Niche disruptors exploit e-commerce: Back To Nature Packaging claims to have displaced 10 million plastic units through online platforms, although third-party verification is pending. The pending EPR framework, expected in 2026, will impose collection and recycling fees that could add 3-5% to costs, accelerating consolidation as under-capitalized SMEs exit. In this context, converters that combine certified substrates, rapid custom printing and compliance support are best positioned to win share in the United Arab Emirates (UAE) disposables packaging market.

United Arab Emirates (UAE) Disposables (Single-Use) Packaging Industry Leaders

Al Bayader International LLC

Hotpack Packaging LLC

Falcon Pack Industries LLC

Detpak (Detmold Group) Pty Ltd

Gulf East Paper and Plastic Inds LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Emirates Flight Catering commissioned a 6-tonne-per-day biodigester at its Dubai facility, converting food waste into compost and biogas.

- November 2025: Emirates Biotech released Embio PLA, the first locally produced PLA resin, with two-week delivery windows.

- October 2025: Ground broke on Emirates Biotech’s 160,000-tonne-per-year PLA plant at KEZAD, slated for 2028 start-up.

- March 2025: Tetra Pak Arabia signed a three-year modernization pact with Al Rabie Saudi Arabia under the Next Generation Factory initiative.

United Arab Emirates (UAE) Disposables (Single-Use) Packaging Market Report Scope

The United Arab Emirates (UAE) Disposables (Single-Use) Packaging Market Report is Segmented by Product Type (Containers, Trays, Plates and Bowls, Boxes and Cartons, Cups, Lids and Domes, Clamshells, Bags and Wraps, Other Product Types), End-User Application (Quick-Service Restaurants, Full-Service Restaurants, Coffee and Snack Outlets, Retail Establishments, Institutional Catering, Hospitality and Events), Material (Paper and Paperboard, Plastics, Bioplastics, Aluminium Foil, Bagasse and Moulded-Fibre), and Distribution Channel (Direct Food-Service Distributors, Wholesale Cash-and-Carry, E-Commerce Packaging Webstores, Group Purchasing Organisations). The Market Forecasts are Provided in Terms of Value (USD).

By Product Type

| Containers |

| Trays |

| Plates and Bowls |

| Boxes and Cartons |

| Cups (Beverage and Portion) |

| Lids and Domes |

| Clamshells |

| Bags and Wraps |

| Other Product Types |

By End-User Application

| Quick-Service Restaurants |

| Full-Service Restaurants |

| Coffee and Snack Outlets |

| Retail Establishments |

| Institutional Catering |

| Hospitality and Events |

By Material

| Paper and Paperboard |

| Plastics (PP, PET, PS) |

| Bioplastics (PLA, PHA, PBAT Blends) |

| Aluminium Foil |

| Bagasse and Moulded-Fibre |

By Distribution Channel

| Direct Food-Service Distributors |

| Wholesale Cash-and-Carry |

| E-Commerce Packaging Webstores |

| Group Purchasing Organisations (GPOs) |

| By Product Type | Containers |

| Trays | |

| Plates and Bowls | |

| Boxes and Cartons | |

| Cups (Beverage and Portion) | |

| Lids and Domes | |

| Clamshells | |

| Bags and Wraps | |

| Other Product Types | |

| By End-User Application | Quick-Service Restaurants |

| Full-Service Restaurants | |

| Coffee and Snack Outlets | |

| Retail Establishments | |

| Institutional Catering | |

| Hospitality and Events | |

| By Material | Paper and Paperboard |

| Plastics (PP, PET, PS) | |

| Bioplastics (PLA, PHA, PBAT Blends) | |

| Aluminium Foil | |

| Bagasse and Moulded-Fibre | |

| By Distribution Channel | Direct Food-Service Distributors |

| Wholesale Cash-and-Carry | |

| E-Commerce Packaging Webstores | |

| Group Purchasing Organisations (GPOs) |

Key Questions Answered in the Report

What is the projected value of the United Arab Emirates (UAE) disposables packaging market in 2031?

The market is forecast to reach USD 1.79 billion by 2031.

How fast will the market grow between 2026 and 2031?

It is expected to post a 3.36% CAGR over the 2026-2031 period.

Which end-user segment is poised for the quickest growth?

Coffee and snack outlets are projected to expand at a 4.51% CAGR through 2031.

When will the first large-scale PLA resin plant start operating in the UAE?

Emirates Biotech’s 160,000-tonne PLA facility is scheduled to commence production in early 2028.

Which distribution channel currently dominates sales?

Direct food-service distributors account for 42.90% of volumes.

Page last updated on: