Flexible Hybrid Electronics (FHE) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

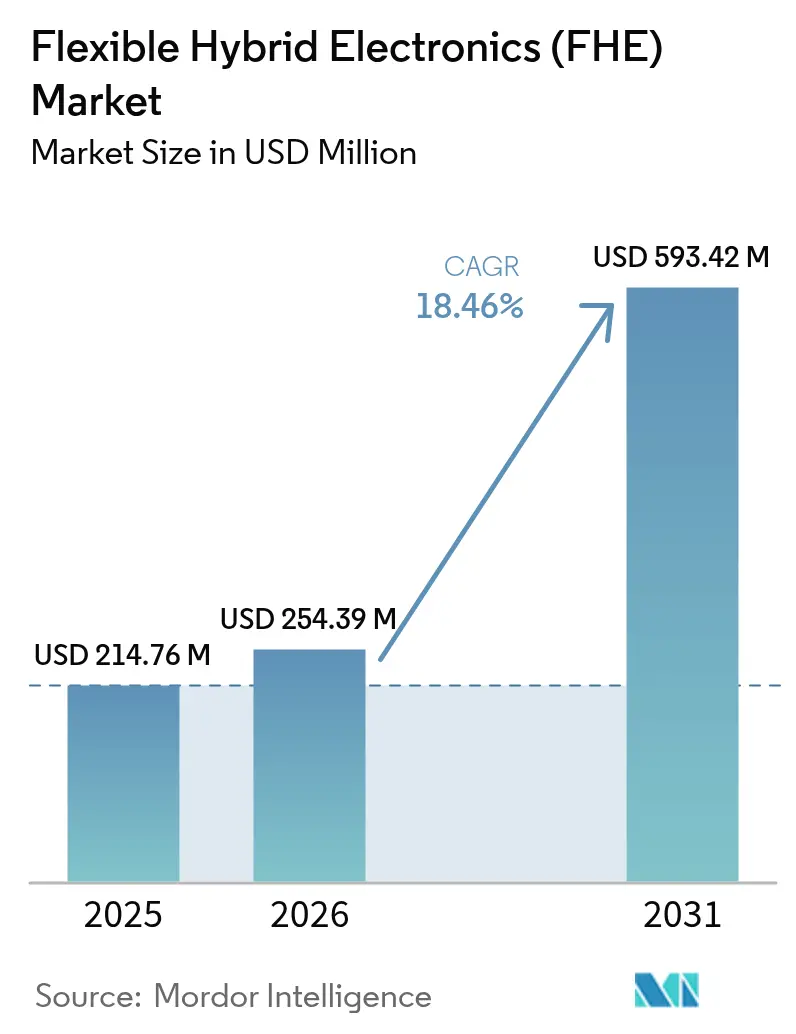

| Market Size (2026) | USD 254.39 Million |

| Market Size (2031) | USD 593.42 Million |

| Growth Rate (2026 - 2031) | 18.46% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Flexible Hybrid Electronics (FHE) Market Analysis by Mordor Intelligence

Flexible hybrid electronics market size in 2026 is estimated at USD 254.39 million, growing from 2025 value of USD 214.76 million with 2031 projections showing USD 593.42 million, growing at 18.46% CAGR over 2026-2031. Technology convergence between silicon devices and printed flexible components is opening high-value use cases in wearables, automotive interiors, and smart packaging. Robust government funding, expanding roll-to-roll (R2R) capacity, and reliability gains in flexible sensors continue to reinforce demand. Companies are prioritizing lightweight architectures that bend, fold, and stretch without compromising electrical performance, while substrate innovation is reducing materials cost and enabling sustainable designs. Competitive intensity remains moderate, yet the entrance of foundry-style service models promises to broaden supplier diversity in the flexible hybrid electronics market.

Key Report Takeaways

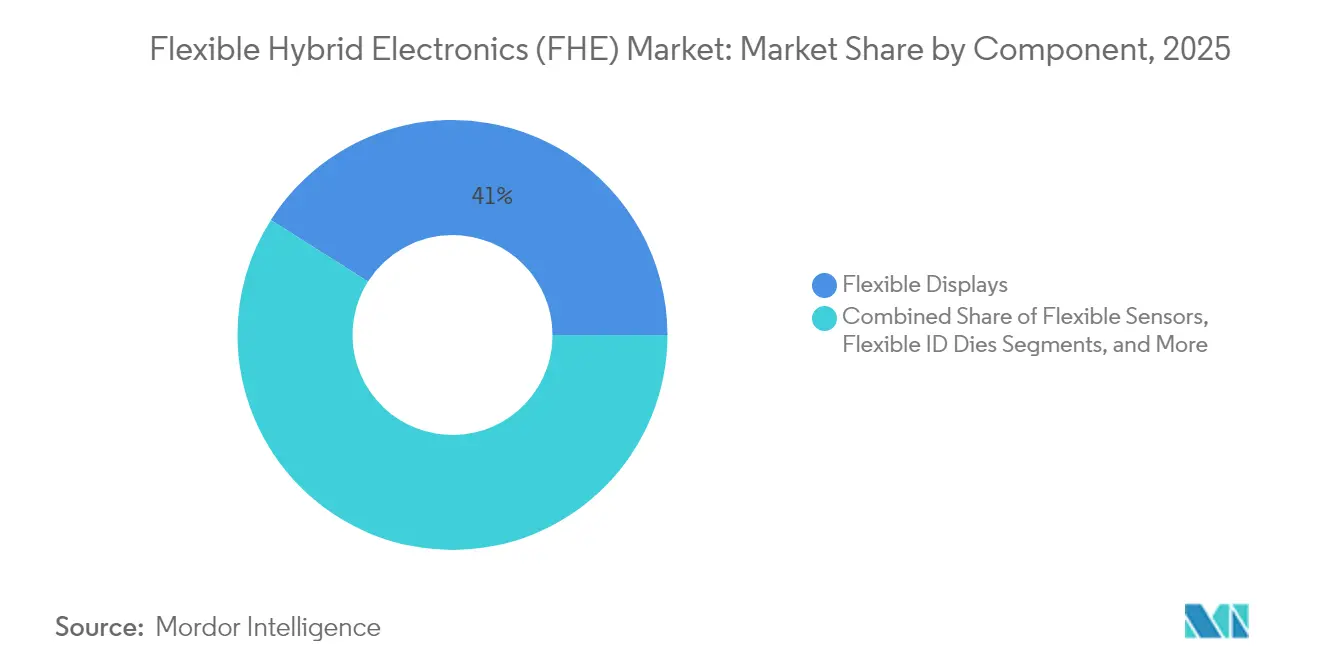

- By component, flexible displays led with 41.02% of the flexible hybrid electronics market share in 2025.

- By substrate, polyimide commanded 45.78% share of the flexible hybrid electronics market size in 2025, while paper and cellulose substrates are advancing at a 19.02% CAGR through 2031.

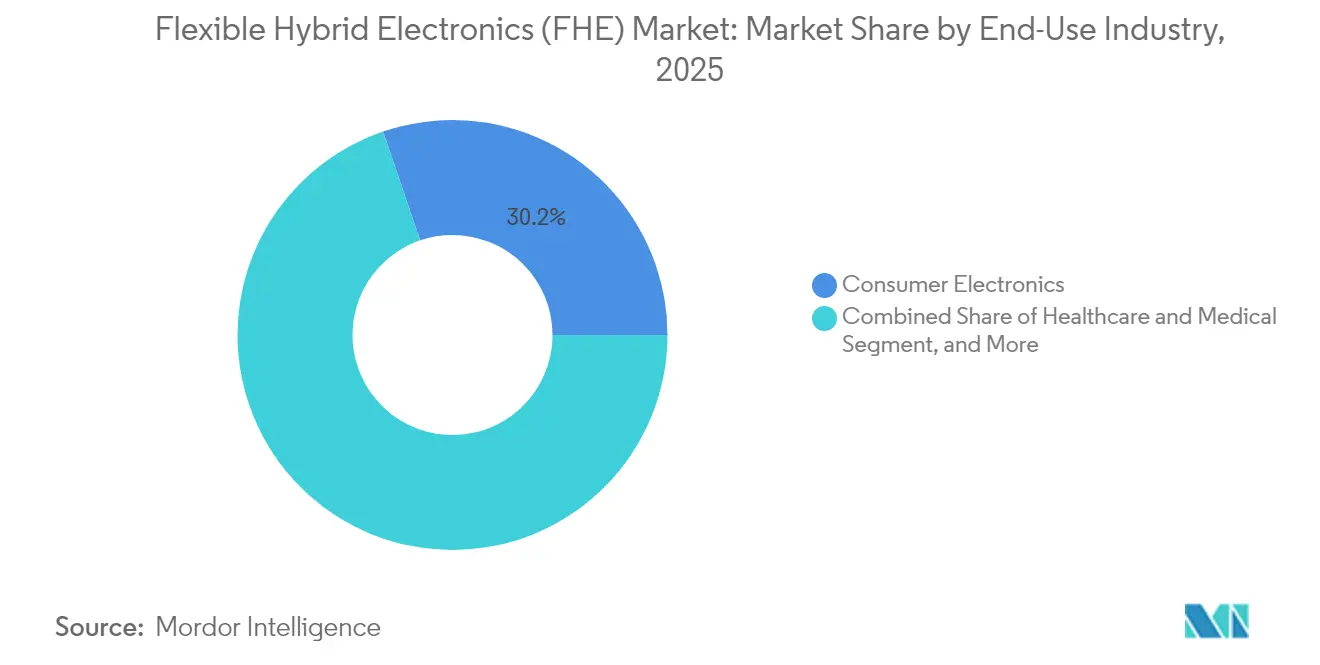

- By end-use, consumer electronics held 30.24% revenue share in 2025 in the flexible hybrid electronics market and healthcare applications are projected to expand at a 18.88% CAGR to 2031.

- By manufacturing process, sheet-to-sheet (S2S) held 34.47% revenue share in 2025 in the flexible hybrid electronics market, and roll-to-roll (R2R) is projected to expand at a 18.95% CAGR to 2031.

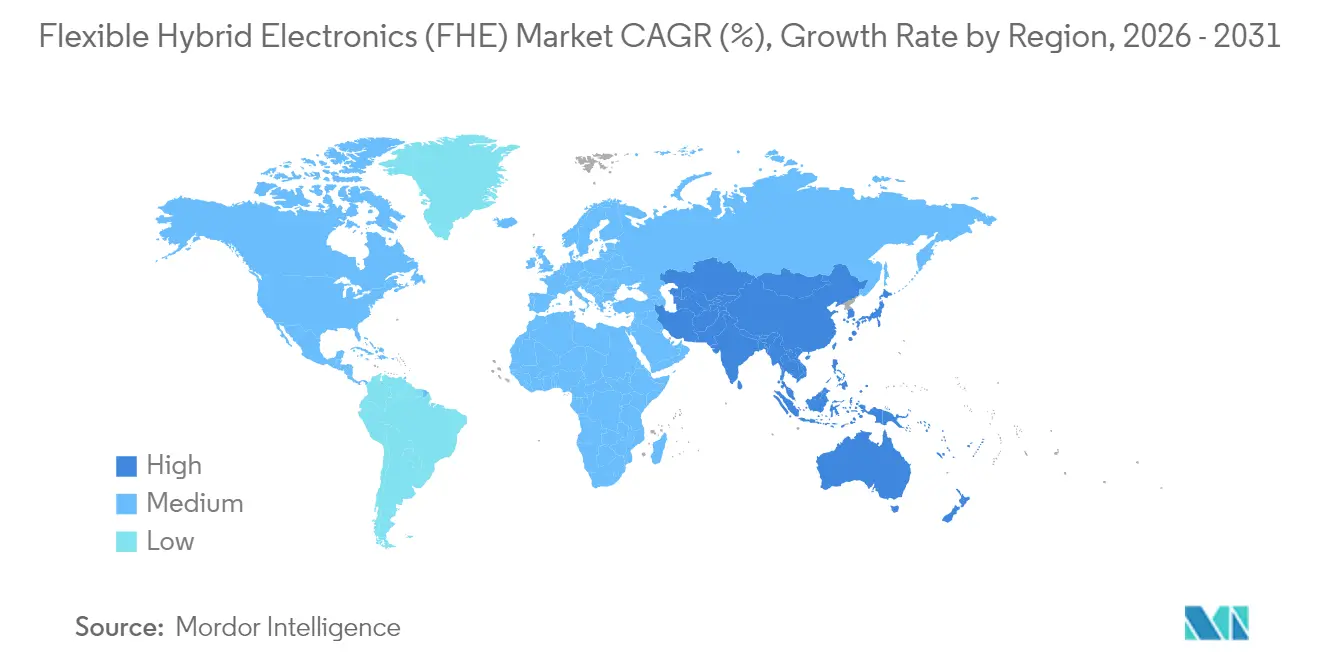

- By geography, North America accounted for a 38.10% share in 2025 in the flexible hybrid electronics market, whereas Asia-Pacific is progressing at a 18.97% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Flexible Hybrid Electronics (FHE) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lightweight, mechanically-flexible and cost-effective product demand | +3.2% | Global with early gains in North America and APAC | Medium term (2-4 years) |

| Government-funded commercialization programs | +2.8% | North America and EU with spill-over to APAC | Long term (≥ 4 years) |

| Wearable health monitoring proliferation | +2.5% | Global, concentrated in developed markets | Short term (≤ 2 years) |

| Shift to low-cost PET/paper substrates for high-volume packaging | +2.1% | APAC core, expanding globally | Medium term (2-4 years) |

| Photonic sintering and low-temperature solders enabling PET adoption | +1.9% | Global manufacturing hubs | Medium term (2-4 years) |

| In-mold structural electronics in vehicle interiors | +1.7% | North America, EU, expanding to APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lightweight, mechanically-flexible and cost-effective product demand

Consumer-facing brands now compete on form-factor freedom rather than incremental performance gains. Samsung Display’s 18.1-inch foldable OLED panel with more than 500,000 fold cycles demonstrated that reliability thresholds for premium devices are achievable.[1]Samsung Display, “CES 2025 OLED Innovations,” samsungdisplay.com Simultaneously, cost-sensitive markets are embracing paper and cellulose substrates that support disposable electronics for logistics, smart labels, and one-time medical tests. VARTA AG’s multilayer printed battery based on recycled inputs shows how sustainable design goals can coexist with the need for flexible power sources. Collectively, these advances widen the accessible customer base for the flexible hybrid electronics market and stimulate fresh design activity across multiple tiers of the value chain.

Government-funded commercialization programs

NextFlex has deployed USD 165 million since 2015 to move pilot concepts toward volume production, allocating USD 5.3 million in 2024 and USD 5.0 million in 2025 to R2R scale-up and in-mold electronics. Grant recipients coordinate through technical working groups that standardize materials sets, metrology, and workforce training, shortening learning curves for smaller firms. In Europe, IMEC’s EUR 14 million PI-SCALE line delivered a foundry model that produced flexible thin-film microprocessors across several independent fabs.[2]DuPont, “Pyralux Flexible Laminates,” dupont.com Such initiatives address costly equipment barriers and accelerate time-to-market, adding 2.8 percentage points to forecast CAGR for the flexible hybrid electronics market.

Wearable health monitoring proliferation

Healthcare providers value continuous data streams generated by multimodal patches that conform to skin. A 2025 Nature Communications study introduced a vialess heterogeneous patch that unites ECG capture, photoplethysmography, and transdermal drug delivery in one flexible stack. Self-healing graphene electrodes maintain signal fidelity after damage, extending device lifespan under normal daily movement. Energy harvesting layers storing 5.82 mWh/cm² eliminate bulk batteries, unlocking multi-day operation. These capabilities support clinical moves toward preventive and personalized medicine, making healthcare the fastest-growing end-use in the flexible hybrid electronics market.

Shift to low-cost PET/paper substrates for high-volume packaging

High-volume consumer goods and logistics labels rarely require the 200 °C tolerance of polyimide. Paper and cellulose substrates now rival synthetic polymers in flexibility and basic conductivity, yet bring end-of-life recyclability. Conductive inks print directly onto uncoated paper, cutting process steps, and material cost. This pathway registers a 19.54% CAGR and places APAC converters at the center of capacity expansion owing to strong regional demand for smart packaging. Remaining technical limitations include moisture uptake and restricted operating temperature windows, which confine cellulose substrates to ambient environments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High R&D and capex requirements | -2.3% | Global with heavier impact on SMEs | Long term (≥ 4 years) |

| Fragmented standards and supply-chain complexity | -1.8% | Global with differing regional frameworks | Medium term (2-4 years) |

| Reliability of thinned dies under cyclic bending | -1.5% | Global manufacturing and application sites | Medium term (2-4 years) |

| Absence of fast, low-cost inline test/inspection | -1.2% | APAC and North America fabs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High R&D and capex requirements

Tooling for R2R photonic sintering, ultra-thin die handling, and precision printing incurs multimillion-dollar outlays that smaller enterprises struggle to finance. Although public grants offset some cost, multiple process steps still require bespoke fixtures. Venture financing for capital-heavy hardware remains limited compared with software, curbing entry of new players into the flexible hybrid electronics market and prolonging payback periods for existing investors.

Fragmented standards and supply-chain complexity

Materials stacks, inspection criteria, and data exchange formats differ by region and by application. A polyimide-based aerospace circuit cannot share qualification reports with a cellulose smart label, creating paperwork duplication. Industry associations have initiated common file formats, yet adoption is uneven, particularly among Tier-2 converters in emerging economies. This fragmentation slows cross-border sourcing and raises compliance costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Displays Lead While Sensors Accelerate

Flexible displays contributed 41.02% of the flexible hybrid electronics market share in 2025, validating early investments in foldable and rollable form factors. The segment benefits from established mass-production fabs and premium consumer willingness to pay for novel user experiences. Sensors are advancing at a 18.96% CAGR as healthcare, industrial IoT, and smart packaging adopt thin, conformal sensing layers. Energy storage elements such as stretchable lithium-ion batteries are witnessing double-digit growth, ensuring autonomous operation for mobile or disposable devices. Flexible IC dies remain technically challenging yet strategically critical for on-board processing, while flexible antennas close the performance loop by enabling robust wireless links.

Product diversification has intensified competition yet accelerated ecosystem maturation. Display vendors extend existing OLED platforms toward transparent and multi-fold designs, creating technology spill-overs that sensor and battery suppliers exploit for their own roll-to-roll upgrades. Breakthroughs in thin-film transistor stability are narrowing performance gaps with rigid driver ICs, improving overall system reliability in the flexible hybrid electronics market.

By Substrate Material: Polyimide Dominance Challenged by Sustainable Alternatives

Polyimide held 45.78% share of the flexible hybrid electronics market size in 2025 due to its high-temperature resilience during solder reflow and chemical robustness in aerospace settings. Yet cellulose substrates are rising quickly (19.02% CAGR) on the back of eco-design regulations and brand sustainability pledges. PET films have reclaimed attention as photonic sintering unlocked low-temperature metallization, positioning PET as a cost-efficient alternative for large-area circuits.

Material choice now hinges on an application’s thermal, mechanical, and environmental profile. High-reliability markets such as defense continue to favor polyimide, whereas packaging lines in APAC gravitate toward paper webs that match existing printing infrastructure. Elastomeric substrates enable stretchable wearables, though washing durability poses engineering hurdles. Each substrate advances process innovation, expanding the addressable customer base for the flexible hybrid electronics market.

By End-Use Industry: Healthcare Acceleration Challenges Consumer Electronics Leadership

Consumer electronics remained the top revenue contributor at 30.24% in 2025 as foldable phones and rollable TVs achieved mainstream adoption. However, healthcare represents the fastest trajectory at 18.88% CAGR, fueled by multimodal monitoring patches that serve chronic disease management and post-surgical recovery. Industrial automation is embedding strain and vibration sensors into equipment for predictive maintenance, while packaging firms deploy disposable RFID and environmental sensors on logistics cartons.

Automotive interiors are embracing in-mold electronics to consolidate touch controls and lighting, aligning with cabin digitization trends. Aerospace and defense applications prioritize ruggedized circuits capable of operating across extreme temperature and vibration profiles. Emerging agriculture use cases, though nascent, underscore the breadth of opportunity extending beyond headline sectors, reinforcing long-term demand for the flexible hybrid electronics market.

By Manufacturing Process: Roll-to-Roll Gains Momentum

Sheet-to-sheet lines retained 34.47% market share in 2025 through compatibility with legacy semiconductor tooling. Yet roll-to-roll throughput advantages are driving a 18.95% CAGR, especially for packaging labels and large-area lighting. R2R photonic sintering removes lengthy oven stages, cutting cycle time and energy use. In-mold electronics is growing more than 15% annually, leveraging plastics molding equipment already prevalent in automotive supply chains.

Transfer printing offers heterogeneous integration by relocating ultrathin dies onto flexible webs without exceeding thermal budgets. Additive manufacturing supports rapid prototyping, but scalability remains limited. Process choice thus reflects a balance between unit volume, performance profile, and capital availability, with the flexible hybrid electronics market steadily gravitating toward continuous-flow platforms for cost-sensitive applications.

Geography Analysis

North America commanded 38.10% of total revenue in 2025, supported by NextFlex’s funding pipeline and strong defense, aerospace, and medical device ecosystems. Federal grants de-risk R&D, while a network of contract manufacturers accelerates pilot-to-production transitions. Canada contributes niche strengths in advanced materials and space-qualified circuitry, complementing the region’s broader competitive edge.

Asia-Pacific records the highest regional CAGR at 18.97% through 2031, reflecting China’s dominance in display and smartphone manufacturing coupled with Japan’s materials expertise and South Korea’s leadership in OLED technology. Local governments offer subsidies for high-volume R2R lines, and electric vehicle adoption stimulates demand for in-mold electronics dashboards. The flexible hybrid electronics market size in Asia-Pacific is therefore poised for rapid scaling, with multinational suppliers forming joint ventures to tap regional growth.

Europe maintains momentum through automotive and industrial opportunities. IMEC’s PI-SCALE pilot line validates a foundry model that reduces entry barriers for startups, while regulatory emphasis on sustainability encourages cellulose substrate adoption, particularly in Germany and France. The Middle East and Africa explore flexible photovoltaics for off-grid power in remote areas, whereas South America, led by Brazil, integrates flexible circuits into consumer appliances and packaging. Overall, geography dictates adoption speed but global collaboration continues to spread best practices across borders.

Regulatory Landscape

Flexible hybrid electronics (FHE) adoption is increasingly shaped by standards and qualification frameworks rather than product-specific regulation, with reliability and test methods serving as key compliance anchors for OEM sourcing. In April 2026, SEMI released the FH5 Guide for Reliability of Flexible Hybrid Electronics, offering a consensus-driven approach to reliability assurance for heterogeneous systems built on flexible substrates, which reduces ambiguity in customer qualification across consumer, industrial, and defense-led programs.

Regional standardization is also tightening manufacturing specifications. In May 2026, China implemented GB/T 18334-2025 for flexible multilayer printed circuit boards (superseding the 2001 version), reflecting a push to modernize national requirements for flexible circuitry used in hybrid assemblies. Alongside these formal standards, NextFlex and SEMI FlexTech continue to coordinate standards, test, and reliability work through technical working groups and global committees, aiming to reduce fragmented references to existing IPC and SEMI benchmarks and improve cross-supplier comparability for FHE stacks.

Value Chain Analysis

The FHE value chain runs from specialty materials (substrates such as polyimide, PET, and paper and cellulose; conductive inks; encapsulants and adhesives) to equipment (screen/inkjet and roll-to-roll printers, photonic sintering, lamination, inspection, and metrology). It then extends to device and module manufacturing, including flexible displays, sensors, batteries, antennas, and flexible IC dies, before system integration by OEMs across consumer electronics, healthcare wearables, automotive interiors (in-mold electronics), industrial IoT, and aerospace and defense. Government-backed commercialization infrastructure acts as a connective layer, with NextFlex organizing technical working groups that align materials sets, process windows, metrology, and workforce practices to move concepts from pilot builds to repeatable production.

Bottlenecks cluster around heterogeneous integration, especially mechanical and thermal mismatch where rigid silicon interfaces with compliant substrates, along with the need for scalable, high-accuracy placement and bonding over large areas. This shifts emphasis toward packaging and interconnect know-how (ultra-thin die handling, alignment-tolerant bonding, and low-temperature attachment) and creates demand for specialized foundry and equipment partners, such as InnovaFlex (semiconductor foundry capabilities on glass and flexible substrates) and TracXon (modular R2R printing equipment). As qualification requirements tighten, inline inspection and common design and reliability guides become key value-chain enablers and influence supplier selection as much as material cost.

Competitive Landscape

Competition is moderate as high capex and multidisciplinary expertise deter rapid new entry. DuPont, Samsung, LG Display, and other incumbents leverage established supply chains and R&D budgets to push material and device frontiers. DuPont’s Pyralux laminates earned Samsung’s 2024 best partner award, underscoring the strategic value of substrate innovation.

Strategic partnerships dominate. Continental teams with Aurora and Google Cloud to merge software, cloud analytics, and in-mold hardware for smart cockpits. SmartKem secured USD 8.7 million to commercialize rollable microLED backplanes, while Flex Ltd. committed USD 400 million to a Dallas expansion aimed at AI server boards and flexible power distribution layers. Such alliances blend process know-how, upstream materials science, and end-market access, strengthening the flexible hybrid electronics industry’s ecosystem.

Emerging foundry-style service models pioneered by IMEC may intensify rivalry by lowering fabrication hurdles for design-centric firms. Nonetheless, ruggedized sectors like aerospace, with stringent qualification cycles, favor established vendors, sustaining current market structure. Intellectual-property portfolios around photonic sintering recipes, self-healing conductors, and ultra-thin die handling remain key differentiation levers.

Flexible Hybrid Electronics (FHE) Industry Leaders

Domicro BV

General Electric Company

Lockheed Martin Corporation

American Semiconductor Inc

DuPont Teijin Films U.S. Limited Partnership

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

High-throughput manufacturing scale-up is a near-term whitespace for volume deployment, particularly for packaging and large-area sensor circuits that benefit from continuous processing. In May 2026, DP Patterning opened a production facility in Norrkoping, Sweden, citing capacity up to 10 million square meters for flexible electronics, which points to more industrial-grade printed electronics output feeding hybrid assemblies. For OEMs and integrators, this supports efforts to qualify printed conductors and sensor layers for higher-volume programs, while also expanding supplier options beyond captive pilot lines.

Standardized reliability and substrate mapping work is another practical enabler for cross-industry adoption, since it reduces qualification friction between suppliers and end users. SEMI FH5 (April 2026) provides a more consistent reference point for reliability assurance in FHE systems, complementing consortium roadmaps and technical working groups under NextFlex and SEMI FlexTech that target heterogeneous integration challenges such as chiplet attachment, alignment-free bonding, and process automation for roll-to-roll flows. With industrial capacity expanding and reliability practices becoming more codified, room opens for foundry-style service models and contract manufacturing for design-centric firms that lack capex for full process stacks, including use cases in healthcare patches, smart packaging, and automotive in-mold electronics where thin, conformal form factors differentiate the end product.

Recent Industry Developments

- May 2026: SEMI released the FH5 Guide for Reliability of Flexible Hybrid Electronics, providing a consensus-driven framework for qualifying FHE systems. The guide helps buyers and suppliers align on reliability assurance and test approaches across heterogeneous stacks, lowering friction in sourcing and speeding transitions from pilot builds to production programs.

- February 2026: DoMicro partnered with ChemCubed to advance flexible hybrid electronics deployments, focusing on the distribution of ElectroJet conductive inks and related equipment solutions. The move strengthens access to printable conductor materials and application support for FHE prototyping and scale-up workflows in key end markets.

- February 2025: Flex Ltd. opened a 400,000 sq ft facility in Dallas to support demand for advanced electronics and power-related builds. The added footprint expands North American manufacturing capacity relevant to hybrid electronics integration and reinforces supply availability for OEM programs that require local production and fast-turn engineering.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as the value of flexible hybrid electronics solutions where flexible substrates and printed circuitry are combined with mounted semiconductor components to deliver functional sensing, display, connectivity, or control in a flexible form factor.

Scope exclusions: It excludes conventional rigid electronics, standard flexible printed circuit boards sold as interconnects only, and raw materials that are not part of an FHE assembly.

Segmentation Overview

- By Component

- Flexible Sensors

- Flexible Displays

- Flexible Batteries and Energy Storage

- Flexible IC Dies

- Flexible Antennas and RF Components

- Flexible Memory

- Flexible Photovoltaics

- By Substrate Material

- Polyimide (PI)

- PET

- PEN

- TPU/Elastomeric

- Paper and Cellulose

- Fabric/Textile

- By End-use Industry

- Healthcare and Medical

- Consumer Electronics

- Industrial Manufacturing

- Packaging and Logistics

- Automotive

- Aerospace and Defense

- Energy and Utilities

- Agriculture

- By Manufacturing Process

- Sheet-to-Sheet (S2S)

- Roll-to-Roll (R2R)

- Transfer Printing

- In-Mold Electronics (IME)

- Pick-and-Place Hybrid Assembly

- 3D / Additive Printing

- By Geography

- North America

- United States

- Canada

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia and New Zealand

- Rest of Asia Pacific

- Middle East

- GCC

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the technical boundary and build the starting data series that can be checked year over year. We typically referred to public sources such as the US Patent and Trademark Office and WIPO patent databases, IEEE and other peer reviewed journals, USITC trade statistics, and government standards or program pages that track printed electronics and flexible device development.

To translate technology signals into a usable market model, we also reviewed company filings and annual reports, investor presentations, conference proceedings, and press releases that disclose capacity expansions, pilot line output, or commercialization timelines. In a few places, paid subscriptions for company financials and patent intelligence were used to speed up cross checks on revenue splits and keyword based innovation activity. These sources are illustrative and not exhaustive, and other public references were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on interviews and surveys with material suppliers, manufacturing process specialists, device integrators, and end use teams that specify FHE in wearables, industrial monitoring, automotive interiors, and medical tools. We covered demand and supply views across APAC, EMEA, and the Americas so adoption timing, pricing, and manufacturability assumptions could be stress tested in more than one region.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 17% | APAC: 42% |

| Mid tier: 53% | Functional/Unit leaders: 37% | EMEA: 36% |

| Smaller Players: 17% | Managers: 46% | Americas: 22% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where production activity and adoption indicators are translated into an addressable demand pool for FHE assemblies, and then converted into value using price and mix assumptions. To keep the totals realistic, results are corroborated using selective bottom-up approximations, such as sampled average selling price by application multiplied by unit volumes, plus supplier and channel checks to adjust any overstatements.

Inputs that matter in this market include the mix shift across flexible sensors versus displays, substrate choices like polyimide and PET that influence BOM cost, the share of roll-to-roll versus sheet-to-sheet processing that affects throughput, typical yield and rework rates on hybrid mounting, and end-use adoption timing in healthcare wearables and industrial monitoring. When a data gap exists for smaller or early stage deployments, we used proxy indicators from patents, pilot line announcements, and expert ranges, which were then narrowed through follow up calls.

Forecasts were built using scenario analysis around commercialization speed and cost-down curves, and it was paired with a light multivariate regression check using variables like wearable shipments, industrial sensor adoption, and electronics manufacturing output trends. Assumptions were locked only after they were consistent with interview feedback and did not break the historical trend line.

Data Validation & Update Cycle

Validation is done by comparing model outputs against independent signals, including technology adoption milestones, manufacturing capacity movement, and end-market shipment trends, and then checking whether implied pricing sits within realistic ranges. Outliers are reviewed in a second pass so sudden jumps are explained by a real event, such as a new production line, a regulatory push in medical devices, or a major design win.

Before sign-off, estimates go through multi-step analyst reviews where key drivers and calculations are rechecked, and respondents are re-contacted when a critical assumption shows high variance. The report is refreshed annually, and interim updates are made when material events change demand or supply. Right before delivery, we do a fresh review so clients receive the most current view available.

Mordor Intelligence's Flexible Hybrid Electronics Market Estimate Compared With Other Published Estimates

Published market values for flexible hybrid electronics often vary because each study draws the market boundary differently and does not always treat pricing, early pilot volumes, and geography in the same way. Even when the technology sounds identical, the year chosen as the base and the way forecasts are extended can shift the final value.

The benchmark table shows a wide spread, and in Mordor Intelligence's model the count is limited to flexible hybrid electronics assemblies that combine flexible substrates and printed elements with mounted semiconductor components, instead of adding adjacent flexible electronics or interconnect-only products. Some external estimates also stretch the scope by using optimistic adoption curves for wearables and automotive, or by applying broader average selling prices without separating pilot versus scaled production, which can inflate the near-term market.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 254.39 M (2026) | |

| Global Research Publisher A | USD 1800.00 M (2025) | Uses a broader definition that appears to bundle multiple flexible electronics and printed electronics revenue pools into FHE, and it also sets a higher starting year value that is not clearly tied to scaled production volumes. |

| Industry Research Publisher B | USD 214.00 M (2024) | Anchors the base year earlier and applies a slower growth path that likely assumes more gradual qualification cycles in medical and industrial uses, which can undercount faster ramps once manufacturing yields stabilize. |

Taken together, the differences mainly come from what is counted as FHE, how early stage revenues are treated, and the year and growth path used to project forward. By keeping the scope tied to identifiable FHE assemblies and by cross-checking assumptions with practical production and adoption signals, the final number stays traceable and repeatable for planning.

Key Questions Answered in the Report

What is the current value of the flexible hybrid electronics market?

It stands at USD 254.39 million in 2026 and is projected to reach USD 593.42 million by 2031.

Which component dominates sales today?

Flexible displays contribute 41.02% of total 2025 revenue.

Which region is expanding fastest?

Asia-Pacific is advancing at a 18.97% CAGR through 2031 amid expanded electronics manufacturing capacity.

Why are healthcare applications growing so rapidly?

Multimodal monitoring patches and self-healing sensors meet clinical demand for continuous, comfortable health tracking, driving a 18.88% CAGR.

What key manufacturing shift is underway?

Roll-to-roll processing is rising at a 18.95% CAGR, outpacing legacy sheet-to-sheet lines on throughput and cost.

Page last updated on: