Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

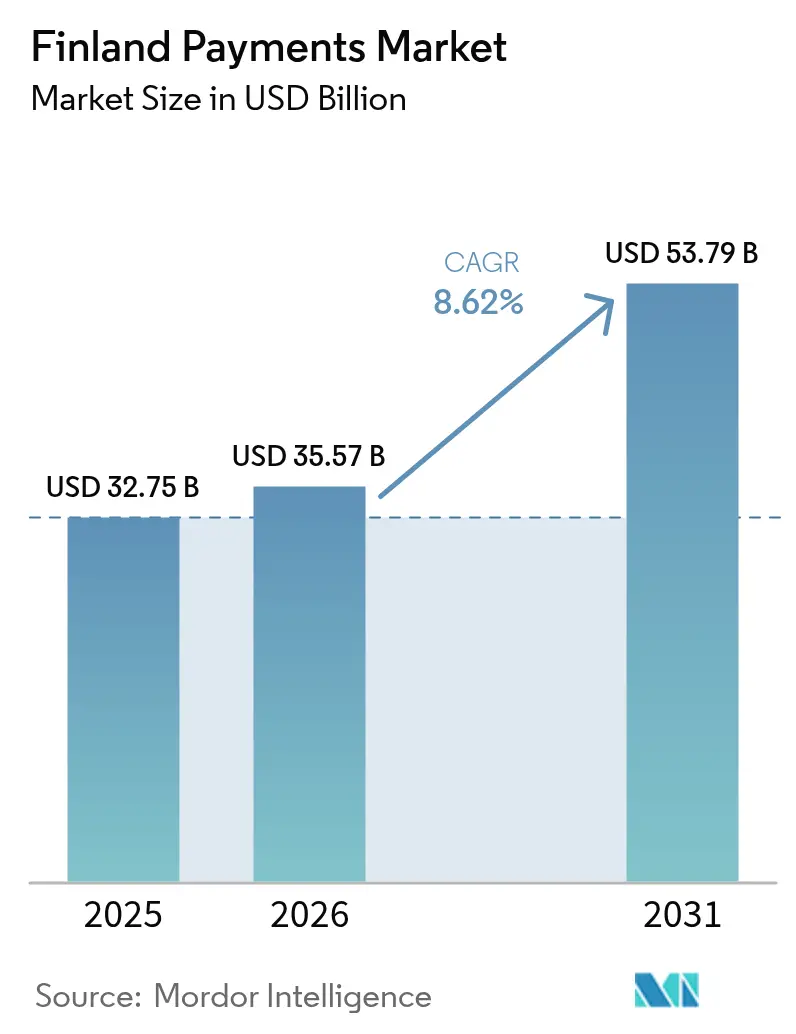

| Base Year Market Size (2025) | USD 32.75 Billion |

| Market Size (2026) | USD 35.57 Billion |

| Market Size (2031) | USD 53.79 Billion |

| Growth Rate (2026 - 2031) | 8.62% CAGR |

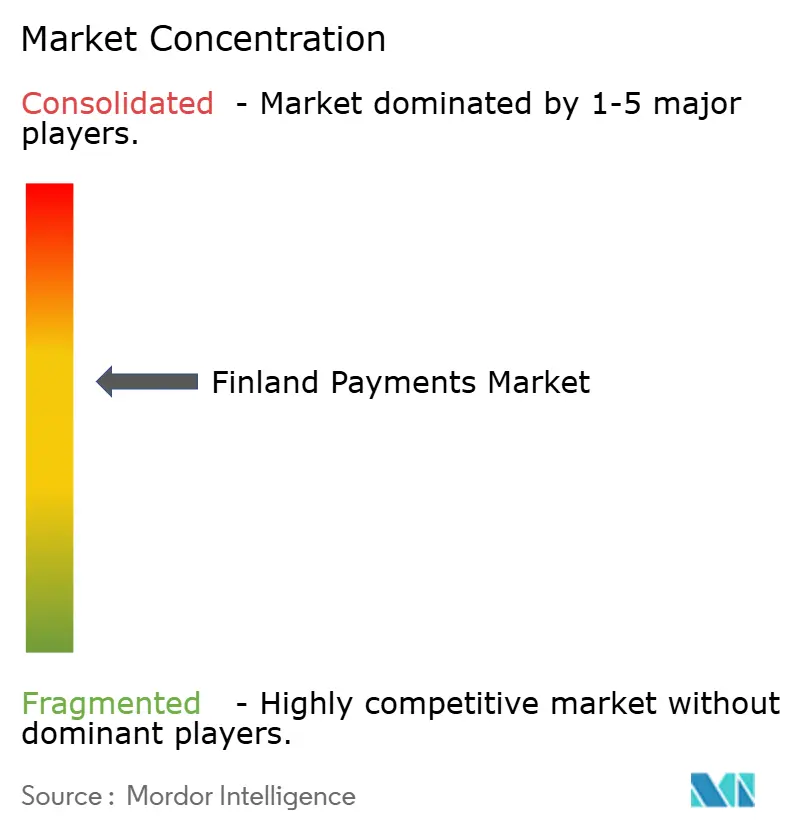

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Finland Payments Market Analysis by Mordor Intelligence

The Finland payments market size was valued at USD 32.75 billion in 2025 and estimated to grow from USD 35.57 billion in 2026 to reach USD 53.79 billion by 2031, at a CAGR of 8.62% during the forecast period (2026-2031). Sustained digital adoption, Nordic wallet interoperability, and the government’s ISO 20022-based real-time rails keep momentum high. Digital payments already cover 75% of retail transactions, well ahead of the European average.[1]U.S. Department of Commerce, “Finland – Digital Economy Guide,” trade.gov Card usage at point-of-sale (POS) remains widespread, yet mobile and account-to-account (A2A) options gain share as millennials and Gen Z prioritise low-cost, mobile-first methods. The MobilePay–Vipps merger now gives merchants one interface to 27 million Nordic consumers, reducing cross-border processing costs by up to 20%. Government policy is equally catalytic: instant payments exceeded 60.65 million transactions in 2024 and are a test bed for the European Central Bank’s (ECB) digital-euro pilots. Fraud trends nevertheless pressure margins: authorised push-payment scams rose 156% year-over-year, compelling banks to accelerate AI-based authentication investments.

Key Report Takeaways

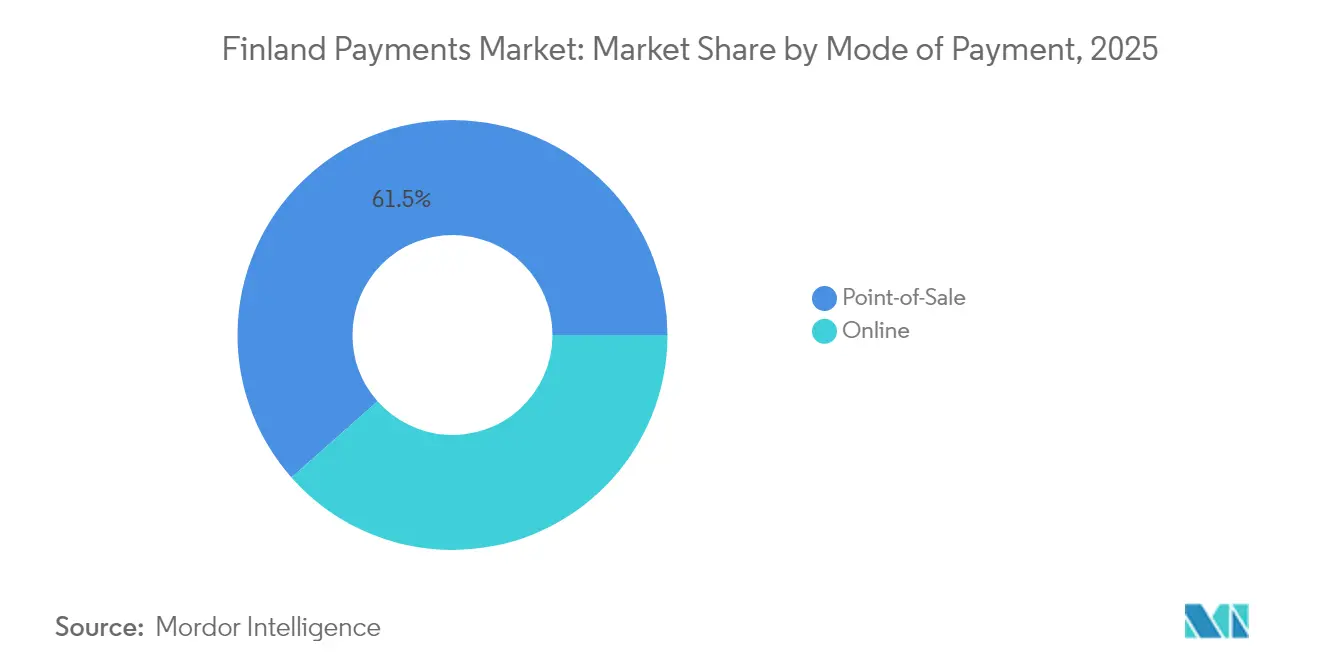

- By mode of payment, Card payments at POS held 12.48% of Finland payments market share in 2025; ;Point-Of-Sale Payment held at around 61.52% share; Digital Wallet & A2A in online channels are projected to grow at a 13.02% CAGR to 2031.

- By interaction channel, POS captured 20.78% of Finland payments market size in 2025, while E-commerce/M-commerce will expand at an 10.86% CAGR through 2031.

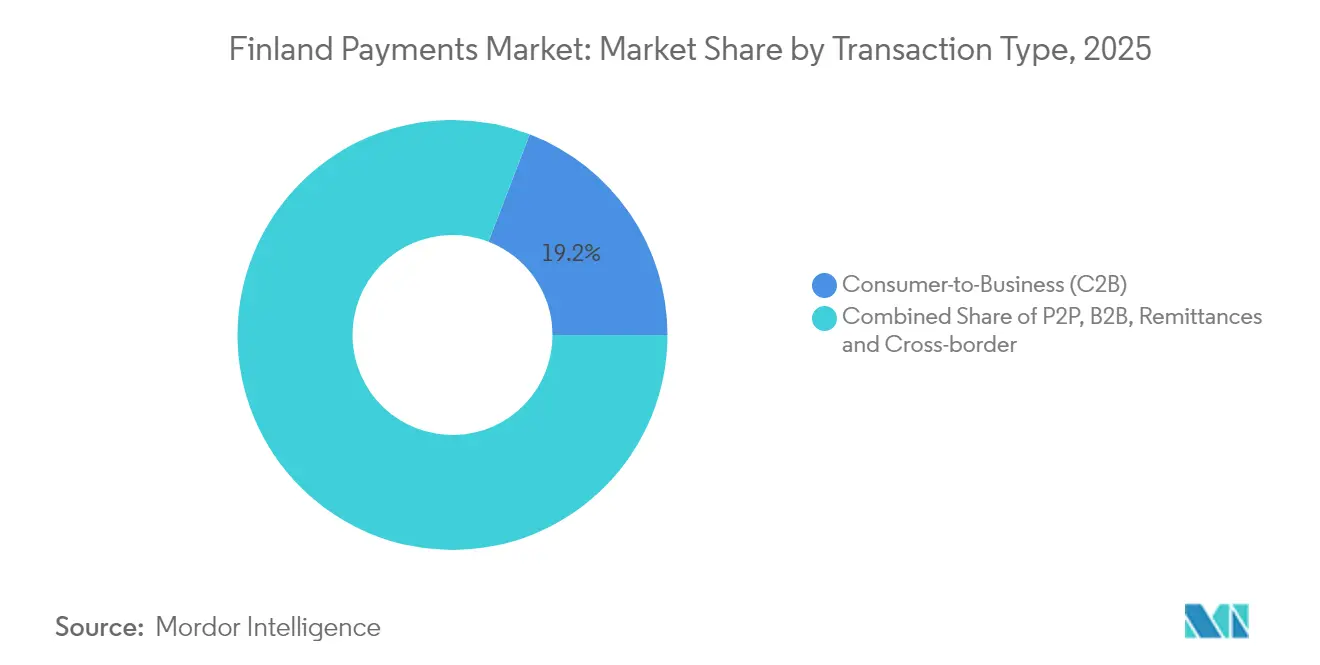

- By transaction type, Consumer-to-Business led with 19.15% Finland payments market share in 2025; Person-to-Person will advance at a 12.01% CAGR during 2026-2031.

- \By end-user industry, Retail commanded 11.32% share of Finland payments market size in 2025, whereas Entertainment & Digital Content is forecast to rise at a 12.74% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Finland Payments Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce & m-commerce Surge Driven by Cross-Border Retail Spend Growth | +1.8% | Finland with Nordic spillover effects | Medium term (2-4 years) |

| Government-Led Digital ID & Real-Time Payment Infrastructure Expansion | +2.1% | National, concentrated in Helsinki metropolitan area | Long term (≥ 4 years) |

| Rapid Adoption of A2A & BNPL Instruments among Gen Z and Millennials | +1.5% | National with urban concentration | Short term (≤ 2 years) |

| Merger of MobilePay-Vipps Accelerating Nordic Wallet Interoperability | +1.2% | Nordic region with Finland as key beneficiary | Medium term (2-4 years) |

| Retailers' Omnichannel Push for Cost-Efficient Cashless Acceptance | +1.0% | National with retail sector focus | Short term (≤ 2 years) |

| ISO 20022 Migration Boosting Data-Rich Corporate Payments Automation | +0.7% | National with B2B sector concentration | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-commerce & m-commerce surge driven by cross-border retail spend growth in Finland

E-commerce turnover hit USD 15.8 billion in 2024, with 62% of shoppers preferring domestic online stores that now integrate global rails for stock access. Mobile-payment penetration jumped from 18% in 2021 to an estimated 58% in 2025, underscoring Finland payments market momentum. Finnish merchants leverage A2A rails to cut card fees, and such transfers already power 28.1% of online payments.[2]The Paypers, “Nordic e-commerce Insights,” thepaypers.com Cross-border enablement widens addressable demand, helping smaller retailers defend share against global platforms. Nordic wallet interoperability after the MobilePay-Vipps deal further enhances checkout speed and lowers cost for shoppers abroad.

Government-led digital ID & real-time payment infrastructure expansion drives the market

The 2030 National Digital Roadmap aligns with the EU Digital Decade by positioning instant payments as economic infrastructure. Transaction volumes on real-time rails rose to 60.65 million in 2024. Seamless linkage between digital identity and payments cuts authentication friction in high-value transfers. Cash circulation fell from EUR 13.2 billion (USD 15.4) in 2019 to EUR 8.1 billion (USD 8.9 billion) in 2024, providing runway for the ECB’s digital-euro pilots.

Rapid adoption of A2A & BNPL instruments among Gen Z and Millennials

Bank transfers are now the preferred online bill-pay method for 64% of Finns, well above card preference at 40%. Younger cohorts value fee transparency and mobile flow, steering demand to A2A and instalment products. BNPL’s rise faces regulatory scrutiny after Klarna investigations, but also invites banks to launch compliant instalment lines with predictable credit checks. Competitive pressure accelerates innovation in responsible lending models inside Finland payments market.

Merger of MobilePay-Vipps accelerating Nordic wallet interoperability

With P27’s collapse, the MobilePay-Vipps merger became the Nordic fix for cross-border retail payments. The combined wallet reaches 27 million users and brings scale against card schemes. Finnish merchants can now accept a single QR or tokenised credential for consumers from Norway, Denmark, and Sweden. Early data suggest processing cost reductions of 15-20% and 10-point faster checkout conversion among Nordic travellers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating APP & Real-Time Fraud Pressure Despite PSD2 SCA | -1.4% | National with urban concentration | Short term (≤ 2 years) |

| High Interchange & Scheme Fees vs. Low-Margin Nordic Merchants | -1.1% | Nordic region with Finland impact | Medium term (2-4 years) |

| Aging Rural Demographics Retaining Cash Preference | -0.8% | Rural Finland regions | Long term (≥ 4 years) |

| Fragmented Legacy POS Estates Slowing Contactless Hardware Roll-outs | -0.6% | National with SME sector focus | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating APP & real-time fraud pressure despite PSD2 SCA

Banks blocked EUR 44 million (USD 48.4 million) of fraudulent transfers in 2024, but total losses still reached EUR 80 million (USD 88 million).[3]Finanssiala, “Fraud Statistics 2024,” finanssiala.fi Sophisticated social-engineering scams leverage voice cloning and AI to circumvent Strong Customer Authentication. Nordic banks invest in machine-learning engines capable of contextual risk scoring, yet smaller PSPs struggle with the cost of advanced models. Incoming Payment Services Regulation raises liability on providers, compelling industry-wide fraud-share agreements that may slow onboarding times.

High interchange & scheme fees vs. low-margin Nordic merchants

Interchange caps of 0.2% (debit) and 0.3% (credit) still feel high in sub-2% margin retail categories. Merchants therefore push A2A, QR payments, and future digital-euro options that promise near-zero merchant service fees. Card volumes remain sizable but growth plateaus as merchants steer consumers to cheaper rails through loyalty programmes and checkout incentives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Payment: Digital transformation accelerates beyond cards

Card payments at POS remained the largest slice with 12.48% of Finland payments market share in 2025, reflecting decades-long card penetration and near-universal contactless issuance. Overall, Point-of-Sale Payment is largest share with 61.52%. Yet Digital Wallet & A2A options in online channels will climb at 13.02% CAGR, underscoring consumer appetite for app-based checkouts and merchant need to bypass card fees. The segment’s Finland payments market size is projected to add over USD 4.6 billion in absolute value by 2031. Apple Pay, Google Pay, and regionally Siirto already ride tokenised rails for secure credential storage, but local wallets now extend into QR and biometric wearables. The regulatory path under PSD3 mandating broader central-bank-system access for non-banks further catalyses A2A.

Wearables and QR-code POS payments show early promise in transport and events, but the category remains below 3% of transaction count. Cash still covers some low-value rural purchases, yet the declining circulation trend signals limited upside. Corporate treasury and bill-pay ecosystems increasingly route invoices through direct bank transfers, capitalising on the ISO 20022 data layer. Overall, the payment-mode transition narrative is one of gradual card share erosion and rapid A2A ascent, powered by fintech-bank collaboration inside Finland payments market.

By Interaction Channel: E-commerce momentum challenges POS dominance

POS retains 20.78% Finland payments market size in 2025 because physical retail traffic recovered post-pandemic and contactless checkout is friction-free. Nonetheless, E-commerce/M-commerce channels are forecast to expand at an 10.86% CAGR through 2031, closing the gap as remote shopping habits persist. Same-day delivery expectations and integrated payment-in-app flows lift basket conversion for online merchants. Instant-payment APIs embedded in checkout pages settle funds in seconds, improving working capital and lowering chargeback risk.

The 5G rollout gives mobile-commerce an extra push with latency-free experiences; merchants embed augmented-reality try-outs tied to one-click payments. Finnish consumers lean on national online-bank credentials for 60% of digital purchases, followed by cards at 48% and invoicing at 24%. These mixed behaviours push PSPs to maintain multiple rails inside unified back-office platforms. The Finland payments market hence sees channel strategy shift toward “channel-agnostic” orchestration, where merchants can toggle rails dynamically based on cost, risk, and consumer preference.

By Transaction Type: P2P growth reflects social payment trends

Consumer-to-Business flows continue as the anchor, standing at 19.15% market share in 2025, thanks to retail, leisure, and urban services. Yet Person-to-Person volumes register a 12.01% CAGR outlook, driven by mobile apps that let users send money via phone numbers in under a minute. University campuses and shared-economy services intensify P2P frequency, while low-fee instant transfers make small-value payments economical. The MobilePay–Vipps integration now allows cross-border P2P among Finns working in neighbouring countries, adding another impetus.

Business-to-Business payments sit at a digital tipping point: ISO 20022 enables straight-through processing, detailed remittance, and AI-based cash-flow forecasting. Early adopters reduce reconciliation time by 70%, freeing treasury staff for analytics tasks. Remittances benefit from SEPA’s near-real-time transfers, but the ECB’s Project Icebreaker emphasises even faster cross-currency CBDC corridors, which could further transform cross-border salary and supplier disbursements. Altogether, diversification of transaction types creates a richer revenue mix for PSPs in Finland payments market.

By End-user Industry: Entertainment digitisation drives growth

Retail holds 11.32% Finland payments market share in 2025 because omnipresent card terminals and loyalty apps make cashless the norm in grocery, apparel, and fuel. However, Entertainment & Digital Content is the clear outperformer, predicted to grow 12.74% CAGR to 2031. Streaming subscriptions, in-game purchases, and e-sports ticketing favour recurring, low-friction payments that suit wallets and direct-debit mandates. Tokenised credentials and parental controls make these rails attractive for younger demographics.

Healthcare and public-sector payments slowly digitalise as e-prescription platforms and municipal e-services integrate mobile ID and instant-payment buttons. Hospitality & Travel, still recovering traffic, introduces contactless guest journeys from check-in to minibar. Manufacturing and logistics embrace corporate A2A to shorten supply-chain settlement cycles. Sector-specific developments signal that Finland payments market continues to expand on top of core retail volumes by embedding payments deeper into digital customer journeys.

Geography Analysis

Finland payments market is anchored in the Helsinki metropolitan area, where fintech start-ups co-locate with major banks and where 5G coverage approaches 100%. The city’s talent pool and sandbox initiatives such as the Bank of Finland Innovation Hub accelerate prototype testing. Rural districts lag digital payment penetration; cash utilisation remains over 25% in certain eastern municipalities, prompting policy attention to broadband access and financial inclusion.

Nordic regional factors drive cross-border volumes. Finns vacationing in Sweden expect the same mobile wallet to pay for public transport, which the MobilePay-Vipps merger now supports. Although the pan-Nordic P27 project was shelved, the bilateral approach shows success, and regional regulators observe the model for wider EU replication. Finnish merchants selling to neighbours enjoy lower acquiring costs and simplified refunds thanks to shared token vaults across the three participating countries.

At European scale, PSD3 and the Instant Payments Regulation oblige all euro-area banks to deliver 10-second transfers at the same price as standard SEPA credit transfers. Finnish institutions are comparatively advanced, yet compliance costs still rise as open-data obligations extend. The ECB’s digital-euro preparation places Finland in the early pilot wave, giving local PSPs a first-mover knowledge edge for future pan-European wallet builds. Cumulatively, geography acts less as a barrier and more as a competitive differentiator based on infrastructure readiness.

Competitive Landscape

Market concentration is moderate. OP Financial Group, Nordea, and Danske Bank processed roughly 60% of payments in 2024, underpinned by entrenched retail customer bases and multiyear merchant-acquiring contracts. Each bank invests heavily in API marketplaces: Nordea’s portal logs over 50 million API calls monthly, enabling third parties to overlay services while keeping accounts “sticky”.

Fintechs leverage open-banking mandates to cherry-pick profitable niches. Trustly, Enfuce, and Paytrail white-label A2A checkout, lowering costs for SMEs. Tietoevry Banking captured micro-merchant flows with Tap-on-Phone, bypassing hardware vendors. Larger incumbents respond through alliances: Nordea and OP formed a joint venture for phone-number-based payments and e-invoice automation, gaining regulatory approval in February 2025.

Artificial-intelligence investments separate leaders from laggards. EY survey data show 40% of Nordic banks deploy machine learning for fraud and customer-insight use cases. Smaller PSPs face capability gaps, often partnering with cloud-native regtech firms for compliance modules. Overall, competitive dynamics shift away from pure scale and toward data-driven risk management and embedded-payments capabilities within Finland payments market.

Finland Payments Industry Leaders

2Checkout (Verifone)

OP Financial Group

S-Pankki Oyj

Nordea Bank Abp

Danske Bank A/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: ECB Decision (EU) 2025/222 entered into force, opening Eurosystem payment systems to non-bank PSPs and narrowing the competitive gap between fintechs and incumbent banks.

- April 2025: Nordea Bank posted 7% growth in private deposits, underpinned by its acquisition of Danske Bank’s Norwegian lending arm, reinforcing capital strength for future payment-technology deployment.

- December 2024: ECB issued its second digital-euro progress report, detailing rulebook revisions and short-listed component vendors, which offers Finnish PSPs insight into near-term CBDC integration steps.

- June 2024: Finnish Competition and Consumer Authority opened a probe into Klarna over billing complaints, illustrating tightening regional oversight on BNPL providers.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Finland payments market as every domestic or cross-border consumer or commercial transaction that clears electronically through card networks, Siirto instant rails, digital wallets, or bank-linked online checkouts, whether the purchase starts at a point-of-sale terminal, inside an app, or on a web page. According to Mordor Intelligence, cash is counted only when it finances cash-on-delivery orders or ATM withdrawals already captured by banks.

Scope Exclusion: pure crypto transfers, inter-bank treasury flows, and securities settlement sit outside scope.

Segmentation Overview

- By Mode of Payment

- Point-of-Sale

- Card (Debit, Credit, Pre-paid)

- Digital Wallets (Apple Pay, Google Pay, Interac Flash)

- Cash

- Other POS (Gift-cards, QR, Wearables)

- Online

- Card (Card-Not-Present)

- Digital Wallet and Account-to-Account (Interac e-Transfer, PayPal)

- Other Online (COD, BNPL, Bank Transfer)

- Point-of-Sale

- By Interaction Channel

- Point-of-Sale

- E-commerce/M-commerce

- By Transaction Type

- Person-to-Person (P2P)

- Consumer-to-Business (C2B)

- Business-to-Business (B2B)

- Remittances and Cross-border

- By End-user Industry

- Retail

- Entertainment and Digital Content

- Healthcare

- Hospitality and Travel

- Government and Utilities

- Other End-user Industries

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed card-scheme officers, acquiring banks, wallet founders, and central-bank supervisors in Helsinki, Tampere, and Oulu. The conversations clarified hidden fees, rural wallet usage, and ISO 20022 timelines, letting us fine-tune assumptions that raw statistics could not address.

Desk Research

Our team gathered public data from the Bank of Finland, Finance Finland, Eurostat, the European Central Bank warehouse, and parliamentary notes on the EU Instant Payments Regulation, which anchored transaction values and interchange caps. Company filings, merchant disclosures, and news archived in Dow Jones Factiva aligned average ticket sizes, while D&B Hoovers supplied issuer revenue snapshots. Questel patent abstracts signaled upcoming authentication tools, and trade papers from Ecommerce Europe traced wallet uptake. The sources listed illustrate breadth; many additional outlets were reviewed for cross-checks.

The second sweep linked smartphone adoption, contactless limits, tourism receipts, and card density, giving us timely indicators that desk datasets often overlook, yet buyers demand. These linkages provided the scaffolding for later model refinements.

Market-Sizing & Forecasting

We start with a top-down build that layers Bank of Finland transaction series on population and GDP outlooks, then nets outward spend leakage. Select bottom-up checks, sampled acquirer volumes, verified wallet user counts, and observed average selling prices test the totals before reconciliation. Smartphone penetration, e-commerce sales, contactless share, real-time payment adoption, interchange ceilings, and inbound tourist growth feed a multivariate regression, while scenario analysis cushions policy or macro shocks. Gaps are bridged with regional ratios vetted during expert calls.

Data Validation & Update Cycle

Outputs pass variance checks against macro indicators, followed by a two-step peer review. Our team refreshes the model annually and issues interim updates when fee caps, wallet mergers, or economic swings occur, so clients always receive the latest view.

Why Mordor's Finland Payments Baseline Earns Confidence

Published estimates often differ because firms choose contrasting scopes, currency treatments, and refresh cadences. Some include cash in circulation or outbound remittances, others ignore account-to-account volumes, and a few freeze 2023 exchange rates. We revisit each factor every year and roll forward daily averages, giving buyers a stable yet current baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 32.75 B (2025) | Mordor Intelligence | - |

| USD 76 B (2024) | Regional Consultancy A | Counts POS plus remittances twice, omits online B2B flows |

| USD 30.12 B (2024) | Global Consultancy B | Consumer-only scope, static FX, excludes instant rails |

Together, the disciplined scope, timely data cadence, and dual-layer validation used by Mordor analysts give decision-makers a transparent figure they can trust.

Key Questions Answered in the Report

What is the projected growth rate for Finland payments market between 2026 and 2031?

The market is expected to rise at an 8.62% CAGR, increasing from USD 35.57 billion in 2026 to USD 53.79 billion by 2031.

Which payment mode is growing fastest in Finland?

Digital Wallet and A2A payments in online channels are on track for a 13.02% CAGR through 2031, outpacing card expansion.

How significant is Nordic wallet interoperability for Finnish merchants?

The MobilePay–Vipps merger grants access to 27 million regional users and can cut cross-border processing costs by up to 20%.

What share of transactions still use cash in Finland?

Cash usage has declined sharply but remains higher in rural areas, averaging 25–30% of payments in some regions.

Why is ISO 20022 important for Finnish businesses?

The new message standard embeds rich remittance data enabling automated reconciliation and faster cash-flow forecasting for corporate payers.

Which industry vertical is projected to grow fastest in payment volume?

Entertainment & Digital Content is forecast to advance at a 12.74% CAGR as subscription and in-game payments spread.

Page last updated on: