File Integrity Monitoring Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

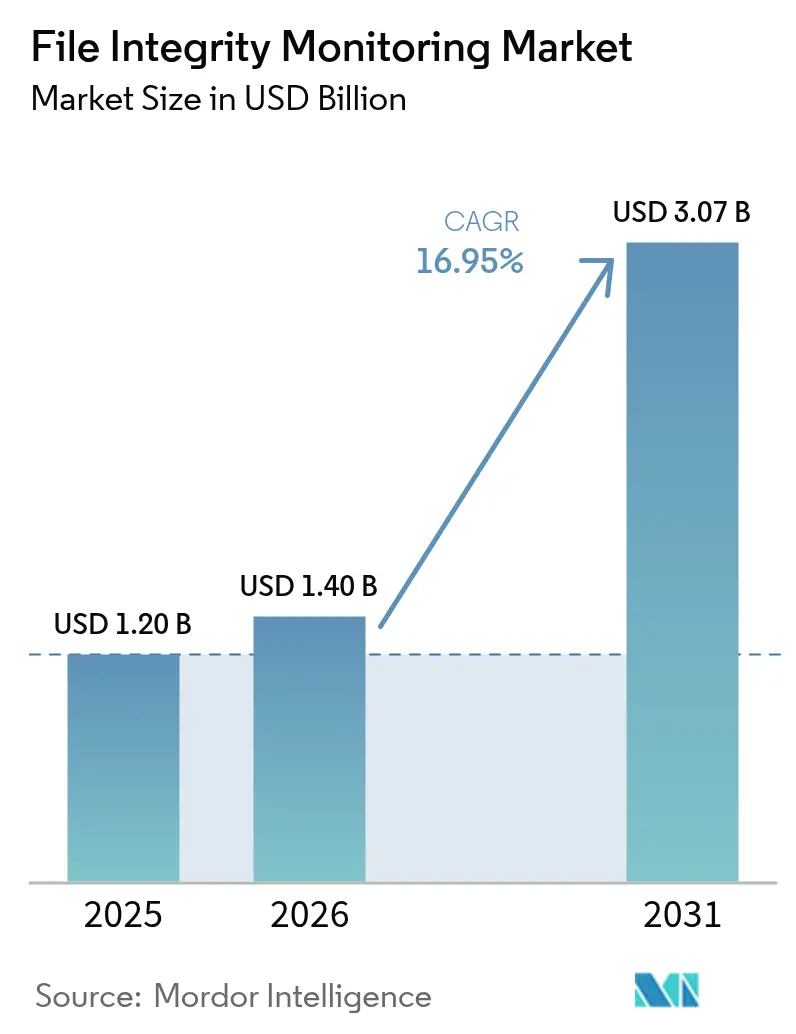

| Market Size (2026) | USD 1.4 Billion |

| Market Size (2031) | USD 3.07 Billion |

| Growth Rate (2026 - 2031) | 16.95% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

File Integrity Monitoring Market Analysis by Mordor Intelligence

The file integrity monitoring market size was valued at USD 1.20 billion in 2025 and estimated to grow from USD 1.40 billion in 2026 to reach USD 3.07 billion by 2031, at a CAGR of 16.95% during the forecast period (2026-2031). Momentum stems from tighter global cybersecurity regulations, rapid cloud workload expansion and the convergence of AI-driven security analytics that reduce alert fatigue. Enterprises are prioritizing real-time change detection because perimeter-centric controls no longer suffice against lateral attacks and ransomware. Demand also benefits from a global pivot toward zero-trust frameworks that regard file integrity monitoring as foundational for least-privilege enforcement. Across industries, rising cyber-insurance prerequisites and board-level scrutiny of operational resilience further propel the adoption of modern, cloud-native monitoring platforms.

Key Report Takeaways

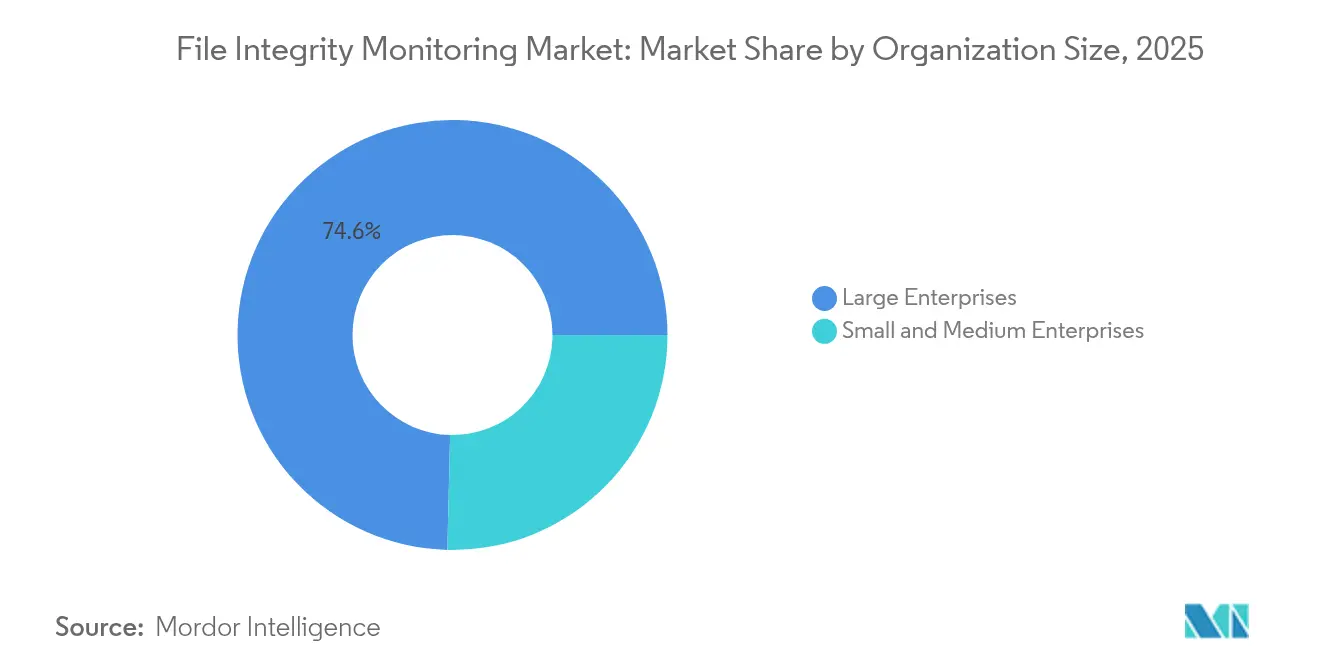

- By organization size, large enterprises held 74.62% of the file integrity monitoring market share in 2025, while small and medium enterprises posted the fastest 17.05% CAGR through 2031.

- By deployment type, cloud solutions captured 68.72% revenue in 2025 and are advancing at an 18.12% CAGR to 2031.

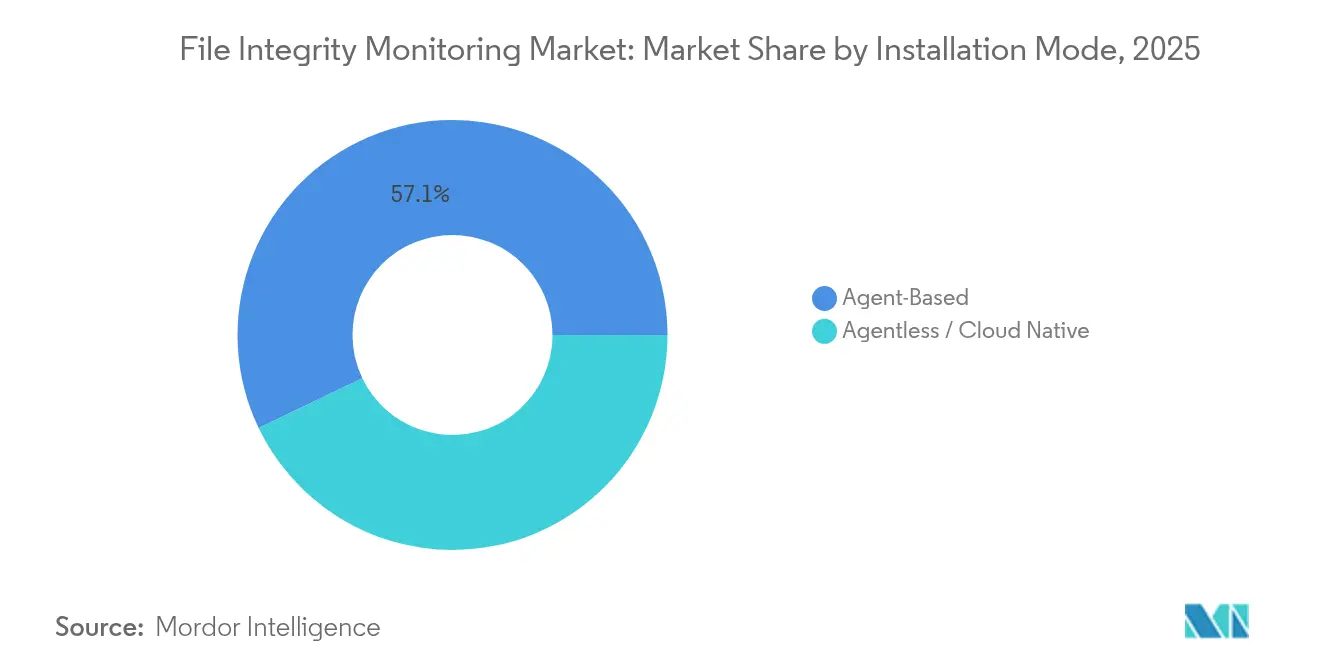

- By installation mode, agent-based tools led with a 57.12% share in 2025; agentless platforms recorded the highest 17.22% CAGR to 2031.

- By end-user industry, financial services commanded 26.35% revenue in 2025; hospitality is projected to grow at an 17.48% CAGR through 2031.

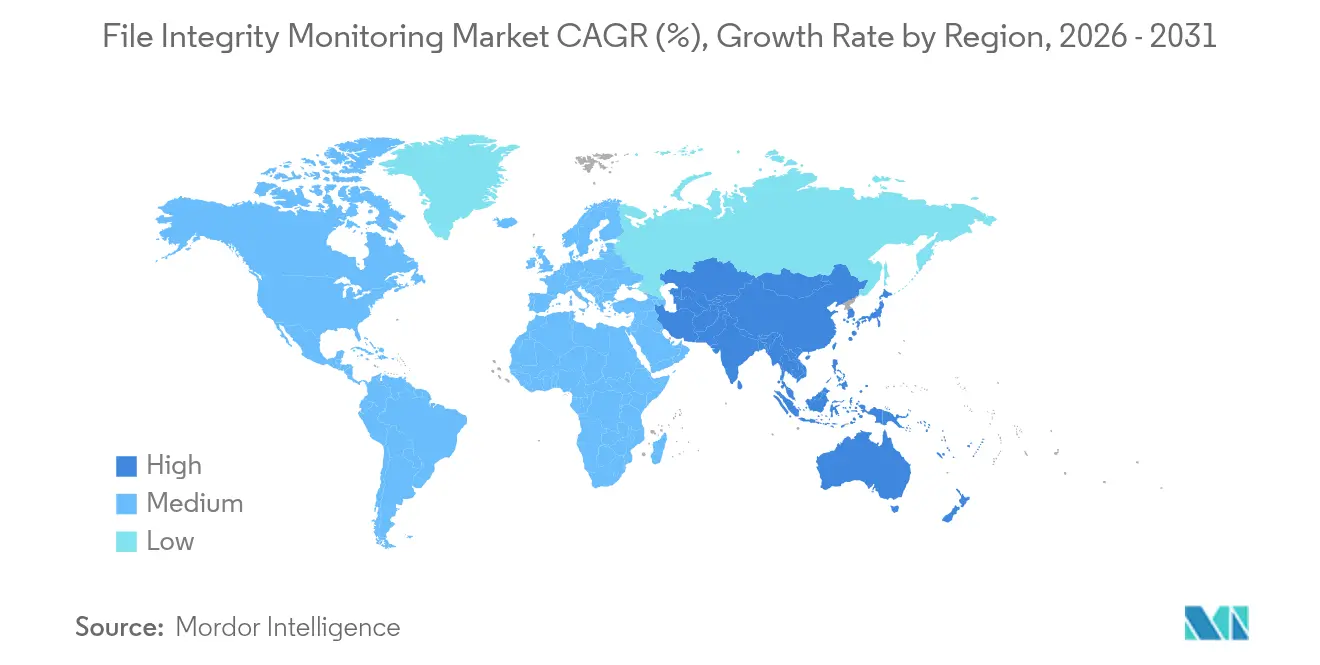

- By geography, North America accounted for 28.45% revenue in 2025, while Asia Pacific expanded at a 17.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global File Integrity Monitoring Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory compliance mandates | +3.2% | Global, with highest impact in North America and EU | Medium term (2-4 years) |

| Rising data-breach volume and sophistication | +2.8% | Global | Short term (≤ 2 years) |

| Cloud workload expansion needs cloud-native FIM | +2.1% | Global, led by North America and Asia-Pacific | Long term (≥ 4 years) |

| SME adoption of affordable SaaS FIM | +1.9% | Asia-Pacific core, spill-over to MEA | Medium term (2-4 years) |

| DevSecOps pipeline integration for code integrity | +1.5% | North America and EU, expanding to Asia-Pacific | Long term (≥ 4 years) |

| AI-driven noise-reduction boosting ROI | +1.3% | Global, early adoption in North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Compliance Mandates

Financial institutions face the May 2025 New York DFS Part 500 amendment that requires privileged-access oversight and multi-factor authentication, making file integrity systems critical for audit-trail evidence. The Federal Energy Regulatory Commission approved NERC CIP-015-1, extending internal monitoring to operational technology in bulk electric systems. Updated HIPAA rules add encryption and multi-factor authentication for electronic protected health information, strengthening demand for integrity monitoring in healthcare.[1]Cyera, “HIPAA 2025 Security Rule Updates,” cyera.ioSEC incident-disclosure rules compel listed companies to report material cyber events within four business days, driving real-time change detection requirements. Payment firms must also satisfy PCI DSS 4.0 logging and monitoring criteria by March 2025, positioning file integrity controls as core infrastructure.

Rising Data-Breach Volume and Sophistication

Average global breach costs climbed to USD 4.88 million in 2024 and are set to hit USD 5.00 million in 2025, with healthcare incidents peaking at USD 9.77 million. Credential abuse remains the dominant attack vector, often obscured in public disclosures, underscoring the value of granular file-level monitoring. Retail and hospitality operators report 39% of incidents emanating from third-party vendors, and 82% link to human error, raising urgency for supply-chain visibility.[2]Retail & Hospitality Information Sharing and Analysis Center, “2025 Retail and Hospitality Threat Landscape,” rhisac.org Enterprises implementing AI and automation within security operations saved USD 2.22 million per breach on average, validating investment in machine-learning-driven FIM that filters noise and accelerates response.

Cloud Workload Expansion Needs Cloud-Native FIM

Container adoption reached 80% among firms with more than 500 employees, yet only 66% have a formal security strategy, leaving a coverage gap that agentless FIM addresses. Wiz introduced a hybrid model that blends agentless discovery with runtime monitoring to protect ephemeral resources. Microsoft embedded file integrity capabilities inside Defender for Endpoint, allowing organizations to meet CIS, PCI and NIST controls without separate agents. In microservices architectures, insider risks escalate due to elevated DevOps privileges, prompting frameworks that extend beyond traditional file checks. Continuous, API-based asset discovery has become crucial for multicloud estates, eliminating performance drag while keeping coverage comprehensive.

AI-Driven Noise-Reduction Boosting ROI

AI lowered vulnerability alert volume by 98% and cut compute costs by 30% for healthcare users deploying Sysdig’s platform.[3]Sysdig, “2025 Cloud Security and AI Report,” sysdig.com Vendors such as CrowdStrike and Palo Alto Networks continuously refine machine-learning models that detect anomalous changes at the endpoint. IBM’s patent portfolio spans automated intrusion detection and predictive analytics, establishing barriers to entry while shaping competitive dynamics. Natural-language tools now accelerate incident triage by summarizing alerts for analysts, though most organizations still prefer human oversight for final remediation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High implementation and maintenance costs | -2.1% | Global, highest impact on SMEs in emerging markets | Short term (≤ 2 years) |

| Operational alert fatigue and skill shortage | -1.8% | Global, acute in Asia-Pacific and MEA | Medium term (2-4 years) |

| Container and micro-services blind-spots | -1.3% | North America and EU, expanding globally | Long term (≥ 4 years) |

| Shift to immutable infrastructure lowering need for file-level monitoring | -0.9% | Cloud-native organizations globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Implementation and Maintenance Costs

SMEs in emerging markets often allocate under USD 500,000 a year to security, making enterprise-grade FIM difficult to justify despite rising threats. Parallel operation of legacy and modern systems during migrations doubles expenses, while skill shortages hamper efficient deployment. European firms devote 9% of IT budgets to security, yet 89% say they need more staff to meet NIS 2 mandates, highlighting cost-driven adoption barriers.

Container and Micro-Services Blind-Spots

The ephemeral nature of containers renders baseline hashing obsolete; each build can introduce new dependencies or secrets, creating supply-chain risks. Ninety-seven percent of enterprises voice concern over Kubernetes security and 94% experienced incidents last year, magnifying demand for runtime integrity monitoring. Distributed microservices further expand attack surfaces, challenging organizations that lack specialized skills to monitor every component effectively.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Organization Size: Enterprise Dominance Drives Market Maturity

Large enterprises generated over three-quarters of 2025 revenue, underlining how regulatory scrutiny and complex hybrid environments drive sizeable deployments. These organizations run distributed data centers and multicloud estates that require continuous change detection across thousands of endpoints. Financial muscle also allows investment in AI-powered analytics that shrink false-positive rates and accelerate response. Meanwhile, SMEs post the fastest 17.05% CAGR, powered by subscription-based platforms that compress onboarding time and outsource upkeep. Government grants in Asia Pacific lower the initial outlay, while cyber-insurance carriers increasingly stipulate file integrity controls for policy issuance.

The SME opportunity is being unlocked by wizard-driven setup interfaces, managed services and usage-based pricing that sidestep heavy capital expense. Yet budget and talent gaps persist; many small firms still operate without dedicated security staff and therefore rely on provider expertise for tuning and incident handling. Vendors respond with curated rule sets, automated baselining and AI-guided investigation workflows that compress skill requirements while maintaining audit-ready evidence.

By Deployment Type: Cloud Solutions Accelerate Market Evolution

Cloud offerings held 68.72% revenue in 2025 and lead growth at an 18.12% CAGR, reflecting the broader enterprise refactoring toward SaaS and infrastructure-as-code. Modern platforms deliver elastic scale and API integration, letting security teams inherit native telemetry from hyperscale providers and layer integrity assessments without agent sprawl. Unified dashboards simplify compliance mapping across PCI, GDPR and HIPAA frameworks.

On-premises tools remain relevant for highly regulated institutions that must maintain data sovereignty or segmented networks. Hybrid deployments bridge those demands by feeding on-premises logs into cloud-hosted analytics engines. As an illustration, OkCupid’s migration to AWS leveraged Terraform to spin up a cloud-native FIM pipeline with minimal custom code and lower total cost than commercial alternatives. The convergence of cloud security posture management with file integrity functionality is blurring product boundaries and further accelerating migration to SaaS.

By Installation Mode: Agentless Architecture Gains Momentum

Agent-based utilities delivered 57.12% of 2025 revenue thanks to their granular host telemetry and real-time blocking capabilities required in regulated verticals. They excel in deep kernel monitoring and forensic detail. However, agentless and cloud-native models grow the fastest as organizations prioritize frictionless deployment across elastic resources. These tools harvest configuration metadata via APIs, sidestepping performance impact and maintenance cycles involved with agent upgrades. Fortinet added an agentless mode that leverages existing cloud audit logs to satisfy compliance without touching hosts.

A hybrid future is evident: enterprises increasingly mix deep agents for mission-critical servers with agentless discovery for transient workloads. Wiz’s policy engine unifies both modes, letting security teams manage baselines centrally while applying context-aware controls that match the dynamic nature of containers.

By End-User Industry: Financial Services Lead Adoption

Banks, insurers and capital-markets firms contributed 26.35% of 2025 revenue because data-rich environments and regulators push for airtight audit trails. New York DFS, the EU Digital Operational Resilience Act and international Basel III operational-risk updates all reference continuous monitoring, making file integrity controls indispensable. Fidelity Information Services employed NNT Change Tracker to secure network configurations and document change control for auditors. Hospitality is the fastest-advancing vertical through 2031 as hotels, restaurants and gaming operators digitize guest experiences and expose larger attack surfaces. Healthcare providers adopt file monitoring to prove HIPAA compliance and protect patient data, while government agencies activate integrity checks across critical infrastructure in line with NERC standards. Retailers focus on vendor-risk oversight after a surge in supply-chain-driven breaches, deploying FIM to verify code and asset changes across franchise networks.

Geography Analysis

North America generated 28.45% of 2025 revenue on the back of mature cyber regulations and heavy security spending by Fortune 1000 enterprises. The United States channels more than 40% of global cybersecurity budgets, and financial institutions carve out double-digit IT allocations for protection, ensuring continued leadership. Canada promotes harmonized breach-notification requirements, and Mexico’s fintech law raises baseline security obligations, reinforcing regional demand.

Asia Pacific is the fastest-growing territory at 17.05% CAGR as governments digitize services and invest in sovereign cloud. Japan’s first cybersecurity-focused investment fund and partnerships such as S&J with Cyleague HD expand managed detection capacity, highlighting a sophisticated buyer market. China’s data-localization norms spur domestic vendors to build compliance-ready FIM for critical industries. ASEAN’s finance hubs, led by Singapore, adopt advanced monitoring to support digital banking growth.

Regulatory Landscape

File integrity monitoring is grounded in security and audit frameworks that call for integrity verification and change-detection controls for systems and logs. NIST SP 800-53 Rev. 5 SI-7 requires automated integrity verification to detect unauthorized changes, while PCI DSS v4.0.1 mandates change-detection on critical files (Requirement 11.5.2) and on audit logs (Requirement 10.3.4), shaping how buyers map controls to evidence and SOC workflows across hybrid environments.

Competitive Landscape

The file integrity monitoring market is moderately fragmented. Enterprise stalwarts such as IBM, Splunk and Tripwire leverage long-standing compliance expertise and broad integration catalogs to preserve incumbent positions. Yet, cloud-native specialists grow faster by offering agentless discovery, consumption-based pricing and built-in DevOps pipelines. Google’s USD 23 billion purchase of Wiz in 2024 underscores hyperscalers’ appetite to embed integrity monitoring into platform services. Turn/River Capital’s USD 4.4 billion acquisition of SolarWinds realigns the latter toward hybrid observability while injecting capital for product modernization.

AI proficiency is now the principal differentiator. IBM defends early territory with patented predictive detection, while startups embed transformer models for contextual prioritization that cuts analyst workload. White-space opportunities include industry-specific compliance automation, microservices visibility and zero-trust orchestration. Vendors that unify agent-based and agentless telemetry in a single policy plane gain traction among enterprises aiming to normalize controls across legacy servers and cloud-native stacks.

File Integrity Monitoring Industry Leaders

McAfee

Cimcor

Qualys

AT&T

SolarWinds

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulatory timelines in Europe are tightening the window for audit-ready integrity controls and change-management integration. Germany's KRITIS-Dach-Gesetz enters into force on March 17, 2026, with a registration window through July 17, 2026, and Belgium's NIS2 conformity assessment deadline is April 18, 2026, creating procurement activity for FIM solutions. The EU Cyber Resilience Act also mandates incident and vulnerability reporting for digital element manufacturers starting September 11, 2026, while ENISA's Security by Design and Default Playbook (v0.4) released in March 2026 supports the same compliance shift.

In response, buyers are increasingly looking for platforms that combine change-detection, evidence mapping, and cloud plus on-premises coverage in a single workflow rather than assembling these capabilities across separate tools.

Recent Industry Developments

- June 2026: Netwrix expanded its distribution partnership with Halodata International to offer Netwrix Change Tracker across Southeast Asia. The partnership widens access to configuration drift controls and real-time file integrity monitoring through a regional channel, which can shorten deployment cycles in markets where in-house security staffing is constrained.

- June 2026: Netwrix updated its 1Secure SaaS platform with AI-driven governance capabilities that incorporate file integrity monitoring and anomaly detection for critical system files, including Windows Server environments. By placing FIM within a broader governance layer, the update shifts buyer evaluations toward consolidated platforms, particularly for hybrid Microsoft estates.

- April 2026: Atomicorp launched File Integrity Monitoring as a Service (FIM as a Service) for enterprise deployments and positioned it around PCI DSS 4.0 oriented compliance. Packaging FIM as a managed service targets large-scale organizations looking for easier deployment and tuning, increasing competitive pressure on traditional enterprise-first offerings.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers file integrity monitoring software and related subscriptions used to detect, log, and alert on unauthorized changes to critical files, including system binaries, application assets, and configuration files, across on-premises and cloud environments.

Scope exclusions: We exclude broader security tools that only perform adjacent functions such as SIEM log analytics or DLP, unless they have a dedicated file change monitoring and alerting function as part of the offering.

Segmentation Overview

- By Organization Size

- Small and Medium Enterprises

- Large Enterprises

- By Deployment Type

- On-Premise

- Cloud

- By Installation Mode

- Agent-Based

- Agentless / Cloud Native

- By End-user Industry

- Retail

- BFSI

- Hospitality

- Healthcare

- Government

- Entertainment and Media

- Other Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Netherlands

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market frame, build clean assumptions, and avoid double counting across overlapping security categories. We relied on public, non-paywalled sources such as NIST security guidance, CISA advisories, MITRE ATT&CK references, NVD vulnerability records, and SEC filings and annual reports from relevant vendors.

To size demand drivers, we also reviewed public cyber incident and complaint statistics from the FBI Internet Crime Complaint Center (IC3), broad security and network usage indicators published by the International Telecommunication Union (ITU), and macro and digital adoption indicators from the World Bank. Supporting checks were added from paid subscriptions for company financials and intelligence, news and financials, and patent databases to validate product positioning, release timing, and investment signals. The desk sources listed here are not exhaustive, and additional references were used to collect data, validate assumptions, and clarify open points.

Primary Interviews and Surveys

Primary work focused on buying and deployment reality for file integrity monitoring across regulated and high risk environments. We spoke with security and IT operations leaders, compliance owners, managed security teams, and channel partners across APAC, EMEA, and the Americas to confirm adoption patterns, pricing behavior, and what is counted as a true FIM deployment versus a bundled add-on.

These discussions helped close gaps left by public data, especially around cloud-native rollout patterns, replacement cycles, and how budgets are allocated between standalone FIM tools and broader security platforms.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 13% | APAC: 44% |

| Mid tier: 50% | Functional/Unit leaders: 33% | EMEA: 37% |

| Smaller Players: 14% | Managers: 54% | Americas: 19% |

Market-Sizing & Forecasting

Sizing started with a top-down build where overall cybersecurity and IT operations monitoring spend was reconstructed, then filtered using FIM-specific penetration and usage signals by region and industry. Inputs tracked included compliance intensity using PCI DSS, SOX, and HIPAA-aligned controls, ransomware incident pressure, the share of workloads moving to cloud and hybrid setups, typical endpoint and server footprints under monitoring, and average contract values by deployment type.

Those totals were then checked using selective bottom-up approximations, such as sampled vendor revenue exposure to FIM, channel feedback on deal sizes, and a volume-by-ASP check based on monitored asset counts and common pricing units. When a vendor bundled FIM within a wider suite, allocation factors were applied based on interview feedback and public product packaging, and unclear cases were kept conservative.

For forecasting, we used scenario analysis supported by simple trend fits on the key variables, and the scenarios were stress tested with expert views on regulation changes, cloud-native adoption pace, and pricing progression. Where data gaps existed by country or vertical, ratios from comparable markets were applied and then revalidated through regional interviews before finalizing the outlook.

Data Validation & Update Cycle

Outputs were validated through multiple checks so the final numbers do not depend on a single assumption. We compared modeled revenues with independent signals such as security spend direction, compliance audit activity, and cloud control adoption, and then investigated outliers when growth or pricing looked inconsistent with interview feedback.

A second analyst review was done to re-check calculations, currency conversions, and scope alignment, followed by re-contact triggers when a material mismatch was found in a key driver or when a major market event occurred. The report is refreshed annually, and interim updates are made when major regulation shifts, breach waves, or product packaging changes materially impact market totals. Before delivery, a final pass is completed so clients receive the most current view available.

Mordor Intelligence's File Integrity Monitoring Market Size Versus Other Published Estimates

Published market sizes for file integrity monitoring often do not match because different studies count different products, allocate services differently, and select different base years for the same demand narrative. Currency timing, cloud adoption assumptions, and whether suite bundles are treated as standalone FIM revenue also create visible gaps.

The main gap comes from how bundled security suites and adjacent controls are treated. Mordor Intelligence counts revenue only when the deployed capability is a dedicated file change monitoring and alerting function tied to monitored file assets, rather than counting broader logging or endpoint tools by default.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.20 B (2025) | |

| Global Research Publisher A | USD 1.04 B (2024) | Uses a different base year and may include a wider set of offerings under security monitoring bundles, which can pull in non-FIM revenue when pricing is packaged at the suite level. |

| Industry Research Publisher B | USD 1.31 B (2024) | Starts from a later base year and can apply higher average contract values without consistently separating stand-alone FIM from add-on modules inside broader platform contracts. |

Overall, the spread is mainly explained by year choice and how strictly FIM-only revenue is separated from broader security platform spend. By anchoring the model to monitored asset coverage, deployment mix, and packaging checks confirmed in interviews, the estimate stays traceable to inputs that can be reviewed and repeated over time.

Key Questions Answered in the Report

What is the current value of the file integrity monitoring market?

The file integrity monitoring market is valued at USD 1.40 billion in 2026.

How fast is the file integrity monitoring market expected to grow?

It is forecast to expand at a 16.95% CAGR, reaching USD 3.07 billion by 2031.

Which deployment model is growing the fastest?

Cloud-based solutions are advancing at an 18.12% CAGR as organizations modernize infrastructure.

What are the main restraints limiting adoption?

High implementation costs and a shortage of skilled analysts slow uptake, especially among SMEs.

Page last updated on: