External Fixators Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

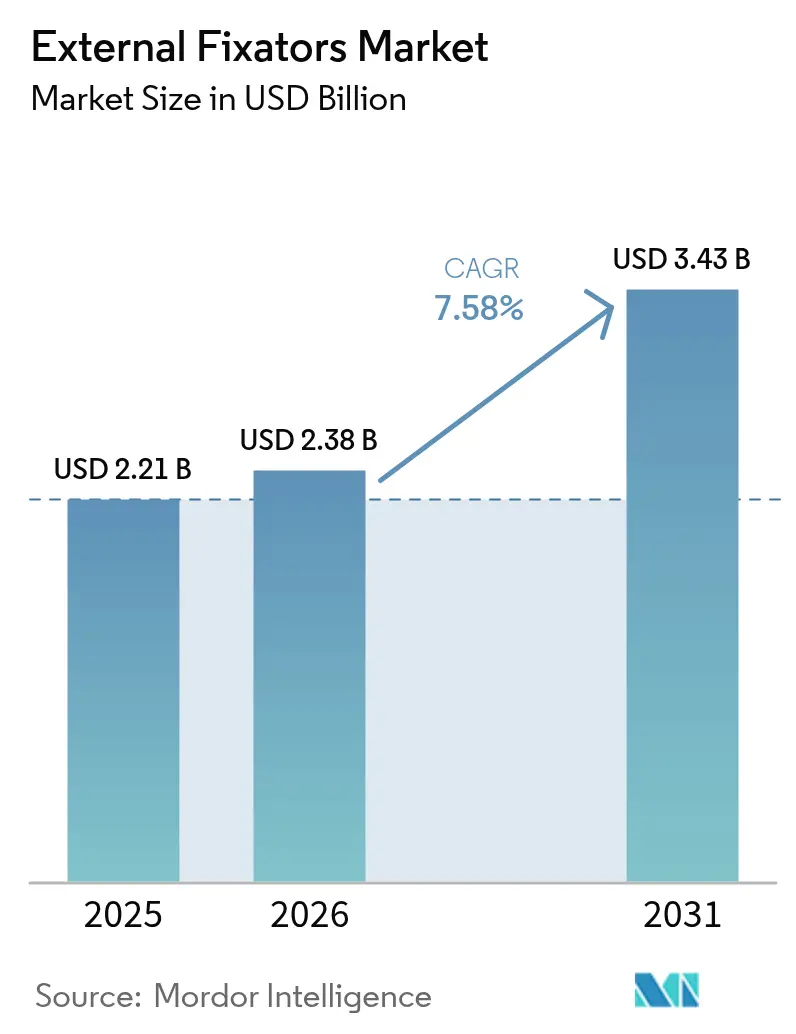

| Market Size (2026) | USD 2.38 Billion |

| Market Size (2031) | USD 3.43 Billion |

| Growth Rate (2026 - 2031) | 7.58% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

External Fixators Market Analysis by Mordor Intelligence

External fixators market size in 2026 is estimated at USD 2.38 billion, growing from 2025 value of USD 2.21 billion with 2031 projections showing USD 3.43 billion, growing at 7.58% CAGR over 2026-2031. This sizeable expansion reflects the sector’s shift from purely mechanical frames to computer-aided, sensor-enabled platforms that promise tighter alignment control, faster rehabilitation, and lighter patient load. Demand is being fuelled by the twin macro forces of a rapidly ageing population—particularly prone to osteoporotic fractures—and an unrelenting rise in road-traffic and sports injuries that require immediate stabilization. Smart systems designed around automated strut adjustment and cloud-based monitoring are also winning surgeon support because they reduce calculation errors and cut adjustment time in busy trauma theatres. Together, these forces anchor a clear growth runway for the external fixators market even as reimbursement hurdles and infection concerns linger in several regions.

Key Report Takeaways

- By product type, manual devices led with 43.72% revenue share in 2025, whereas computer-aided systems are on track for the fastest 9.48% CAGR through 2031.

- By fixation configuration, unilateral and bilateral frames accounted for 48.10% of the external fixators market share in 2025, while circular constructs are expected to advance at an 10.74% CAGR.

- By application, fracture fixation contributed 56.05% of the external fixators market size in 2025; limb-lengthening procedures are projected to rise at 11.56% CAGR.

- By anatomical site, lower-extremity trauma commanded 52.64% share, yet pelvic and hip usage is growing at a 10.01% CAGR to 2031.

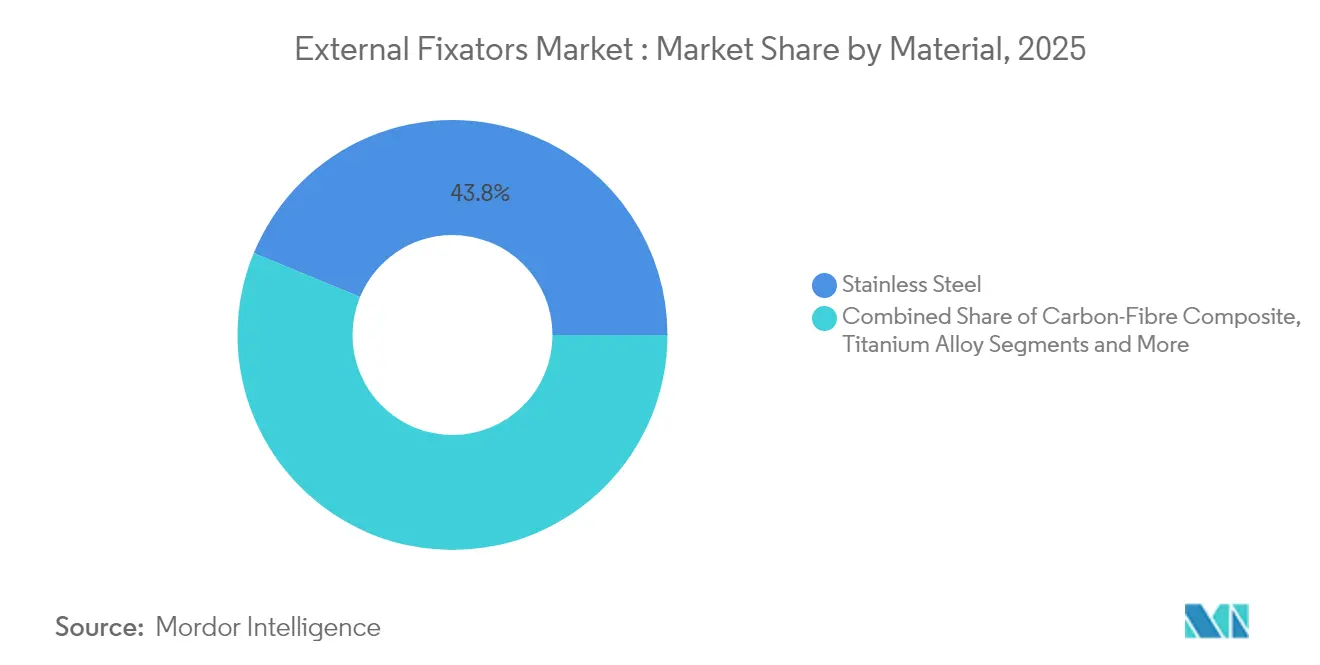

- By material, stainless steel remained dominant at 43.78%, whereas carbon-fiber composites are forecast to expand at 11.02% CAGR.

- By end user, hospitals captured 63.72% share in 2025, while ambulatory surgical centers (ASCs) show the quickest 8.62% CAGR.

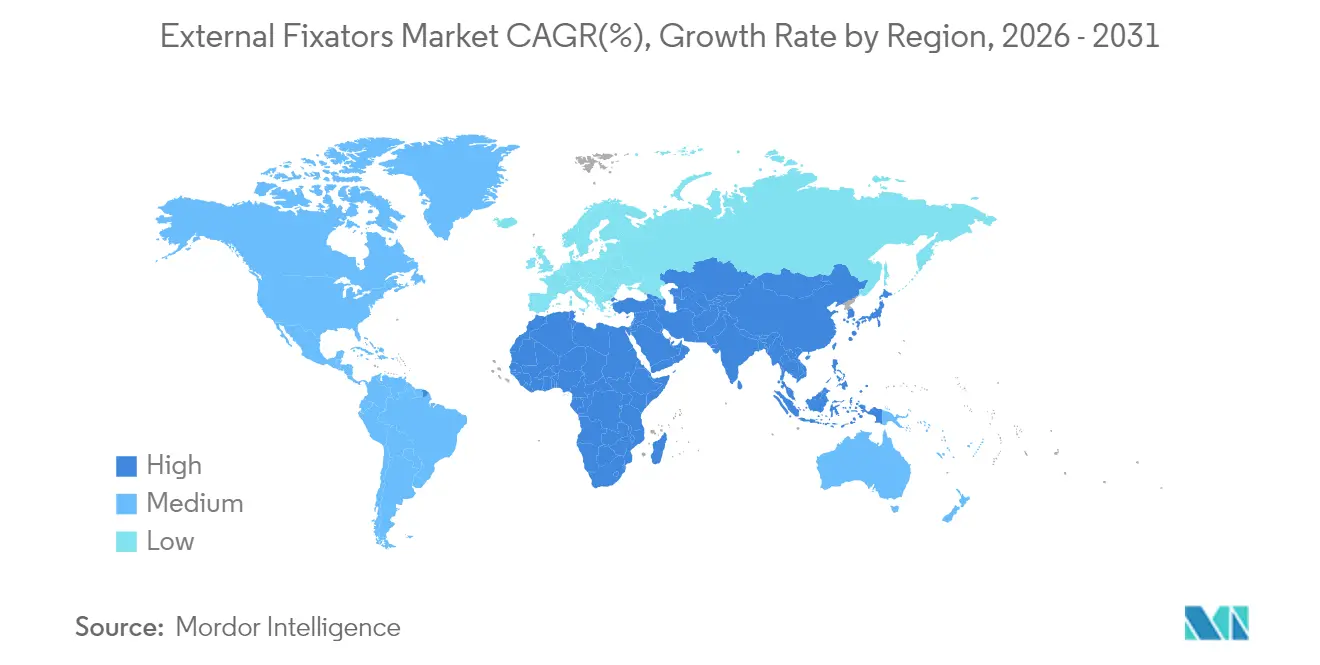

- By geography, North America held 36.10% share, but the Asia-Pacific external fixators market is accelerating at 9.08% CAGR on the back of infrastructure upgrades and rising trauma volumes.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of External Fixators Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging road accidents & sports injuries | +1.8% | Global, most acute in APAC and Latin America | Medium term (2-4 years) |

| Rising preference for minimally invasive care | +1.5% | North America & Europe, expanding into APAC | Short term (≤ 2 years) |

| Rapidly ageing osteoporotic population | +2.1% | Global, concentrated in developed regions | Long term (≥ 4 years) |

| Breakthrough 3-D printed patient-specific units | +1.2% | North America & Europe, early-adopter phase | Medium term (2-4 years) |

| Wider military and disaster-zone deployment | +0.7% | Conflict areas worldwide | Long term (≥ 4 years) |

| Diabetic-foot infection reconstructions | +0.9% | Diabetes-endemic emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Road Accidents & Sports Injuries

Accelerating urban traffic density and higher amateur sports participation keep trauma volumes high, pushing hospitals to favor rapid, damage-control techniques. External frames allow swift stabilization when full internal fixation resources are unavailable, which is common in middle-income nations where injury rates are spiking.[1]World Health Organization, “Improving Care of the Injured,” who.int Asia-Pacific’s urban corridors thus represent a major demand node. Adoption is also rising in North American emergency departments that seek to shorten time to initial stabilization in poly-trauma cases.

Rising Preference for Minimally Invasive Care

Payers and providers now emphasize protocols that shorten theatre time and enable same-day discharge. External frames satisfy that aim by avoiding extensive soft-tissue dissection, and recent data confirm that closing pin sites primarily can cut infection risk and improve cosmetic results.[2]James D. Brodell Jr., “Primary Closure of External Fixator Pin Sites Is Safe After Orthopaedic Trauma Surgery,” PubMed, pubmed.ncbi.nlm.nih.govSurgeons in outpatient centers see added benefit because frame assembly is simpler with today’s lighter carbon-fiber struts, fitting neatly with the ASC growth trend.

Rapidly Ageing Osteoporotic Population

Fragility fractures in people over 70 remain stubbornly high, and only 15.2% of patients receive post-fracture osteoporosis therapy. External frames give surgeons an option when bone quality is too poor for screw purchase. Firms are answering with pin coatings and load-sharing designs that cater specifically to porous bone, ensuring the external fixators market stays relevant for geriatric trauma services.

Breakthrough 3-D Printed Patient-Specific Fixators

Additive manufacturing now produces tailor-made rings for EUR 10-15 versus EUR 50-150 for conventional steel alternatives, slashing cost while improving fit. In high-income trauma units, patient-matched frames cut operative planning time, whereas in low-resource areas, local printing eliminates supply delays. The pairing of CT-based design software with hospital-based printers positions smart, bespoke frames as the next leap for the external fixators market.

Restraints Impact Analysis of External Fixators Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability of internal fixation alternatives | −1.4% | Global, especially in developed healthcare | Short term (≤ 2 years) |

| Shortage of skilled orthopaedic surgeons | −1.1% | Acute in rural and developing regions | Long term (≥ 4 years) |

| High pin-site infection scepticism | −0.8% | Varies by hospital infection-control quality | Medium term (2-4 years) |

| Patchy reimbursement for smart fixators | −0.9% | Complex payer systems in high-income regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Availability of Internal Fixation Alternatives

Modern plates and intramedullary nails have improved biomechanical profiles and avoid external hardware, tilting surgeon preference toward internal solutions when soft-tissue condition permits. Studies using the Femoral Neck System report high union and low complication rates, challenging frame use in subcapital fractures. Developed markets therefore present headwinds for the external fixators market as internal implants gain ground in elective suites.

Shortage of Skilled Orthopaedic Surgeons

Applying a multi-axial frame demands precise pin placement and post-operative modulation that junior staff often find daunting. Workforce shortfalls are most apparent in rural Asia and Africa, where trauma burdens are highest. Automated systems such as the MAXFRAME AUTOSTRUT reduce adjustment complexity, yet wide-scale skill transfer remains a long-term hurdle.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

External Fixators Market Segment Analysis

By Product Type:

Smart Systems Drive InnovationThe external fixators market size for manual frames stood at USD 0.97 billion in 2025, translating into 43.72% share and underscoring their dominant role in frontline trauma theatres. However, computer-aided platforms are expanding at a 9.48% CAGR, reflecting the urgent need for precision without manual calculations. Strut-driven hexapod frames, typified by Johnson & Johnson’s MAXFRAME AUTOSTRUT, automatically realign bones under software guidance, reducing clinic visits for frame tweaking.

Surgeons leaning toward data-driven correction appreciate how smart dashboards cut human error and bring reproducibility to complex deformity cases. Manual systems will remain prevalent in resource-constrained hospitals, but cloud-connected variants are poised to tilt market share toward the smart end of the spectrum across the forecast horizon. Continued R&D in sensor feedback and remote monitoring underscores why the external fixators market is migrating toward an integrated, digitally enabled product mix.

By Fixation Type:

Circular Systems Gain MomentumUnilateral and bilateral bars generated the largest external fixators market size contribution in 2025, covering 48.10% of revenue thanks to ease of application and lower cost. Their straightforward design makes them indispensable in emergency trauma where long-bone stabilization is urgent. By contrast, circular frames register the fastest 10.74% CAGR because they evenly distribute load and allow gradual deformity correction, qualities indispensable in limb reconstruction clinics.

Pelvic injury management via the subcutaneous INFIX method showcases the biomechanical edge of circular constructs, reporting 99.5% union with fewer nerve complications than traditional scaffolds. Growth also comes from hybrid assemblies combining monolateral bars with rings to address multi-plane fractures. Rising resident training in Ilizarov techniques should cement circular systems’ trajectory, shifting the external fixators market share equilibrium over time.

By Application:

Limb Lengthening Shows PromiseTrauma-driven fracture stabilization accounted for 56.05% of the external fixators market share in 2025, confirming its entrenched role in damage-control orthopaedics. Yet limb-lengthening and deformity correction procedures are forecast to record the segment’s 11.56% CAGR as patient expectations rise and surgical outcomes improve with programmable struts.

Advances in automated distraction engines simplify daily adjustments, encouraging elective uptake among both paediatric and adult stature-lengthening candidates. These innovations underpin the belief that limb-lengthening revenue will form a larger slice of the external fixators market size by 2031, diversifying revenues beyond acute trauma.

By Anatomical Site:

Pelvic Applications AccelerateLower-limb fractures, particularly tibial and femoral injuries, drove 52.64% of 2025 revenue because of high accident incidence and established fixation protocols. The pelvic and hip segment, however, is outpacing others with a 10.01% CAGR aided by minimally invasive INFIX approaches that hide hardware under soft tissue for better patient comfort.

Population ageing and lifestyle diseases such as osteoporosis reinforce hip-fracture prevalence, propelling demand for specialized pelvic frames capable of withstanding multi-directional forces. Given these dynamics, pelvic solutions will account for a rising portion of external fixators market growth, driving dedicated R&D into lighter anatomically contoured hardware.

By Material:

Carbon-Fiber Composite Leads InnovationStainless steel remained the workhorse material with 43.78% share in 2025 due to affordability and predictable strength. Nonetheless, carbon-fiber composite platforms are forecast to expand at 11.02% CAGR on the back of radiolucency—which eases intra-operative imaging—and lightness that improves patient mobility.

Hospitals use CT and X-ray frequently during follow-up; a frame that does not obscure the site therefore accelerates healing verification, a clear clinical benefit. Titanium retains niche value in infection-sensitive cases, while bio-resorbable polymers are emerging for paediatric use where secondary surgeries must be avoided. These shifts validate material innovation as a critical lever in redefining external fixators market dynamics.

By End-User:

ASCs Capture GrowthHospitals stayed dominant with 63.72% revenue in 2025 because complex trauma usually arrives via emergency departments. Yet ASCs are climbing at 8.62% CAGR as reimbursement models reward outpatient fracture care and minimally invasive platforms shorten stays. External frames that can be fitted quickly, allow immediate weight-bearing, and need limited follow-up suit the ASC model, helping the external fixators market penetrate this cost-sensitive setting.

Specialist trauma centers continue to house expertise for intricate frame corrections, but design simplification is lowering the learning curve, allowing ASCs to manage straightforward fractures safely. Product labeling that highlights “ASC-ready” features signals how manufacturers tailor packaging, instrument trays, and training to this expanding venue.

Geography Analysis

North America External Fixators Market

North America retained the biggest external fixators market slice at 36.10% in 2025 because of comprehensive trauma networks, solid reimbursement, and an ecosystem that rewards digital orthopaedic innovation. Regular 510(k) clearances for smart frames attest to a regulatory environment that encourages product renewal while safeguarding patient safety. Ongoing capital investment in level-I trauma centers sustains high procedural volume, giving suppliers predictable demand visibility.

APAC External Fixators Market

Asia-Pacific posted the quickest 9.08% CAGR thanks to surging road-traffic accidents, urban expansion, and nationwide insurance programmes that lift procedure affordability. China’s public–private hospital build-out widens access, while Japan faces an unprecedented geriatric fracture load owing to population ageing. Multinational device firms, including Smith+Nephew, are planting country-specific portfolios such as foot-and-ankle kits for Australia and New Zealand, proving the region’s pull for innovation.

Europe External Fixators Market

Europe remains a mature but technology-forward zone where carbon-fiber and automated frames resonate with outcome-driven procurement. Germany spearheads clinical evidence generation, the United Kingdom focuses on cost-effective outpatient care, and France invests in limb-reconstruction fellowships that deepen circular-frame expertise. CE-mark safety standards guide not only European purchases but also shape design requirements for exporters entering the global external fixators market.

Regulatory Landscape

External fixators are regulated as orthopedic external fixation devices in major markets, with the United States commonly treating these systems as Class II devices under 21 CFR 888.3030 and using the 510(k) pathway as a primary route to market. A notable 2026 compliance milestone is the FDA Quality Management System Regulation (QMSR) taking effect on February 2, 2026. It aligns US quality-system expectations more closely with ISO 13485:2016 and raises the bar on documentation, supplier controls, and post-market processes for manufacturers selling into North America.

Standards alignment is also tightening: the FDA has recognized ASTM F1541-24 for external skeletal fixation devices, with a transition window from the prior version (ASTM F1541-17) running through December 19, 2027. This requires OEMs to refresh test evidence packages over the study period. In Europe, the Medical Device Regulation (MDR) framework continues to shape conformity assessment and technical documentation expectations for external fixation platforms, influencing product design controls and clinical evidence strategies for global suppliers that target both CE marking and US clearance.

Value Chain Analysis

The external fixators value chain starts with specialized raw materials (surgical-grade stainless steel, titanium alloys, and carbon-fiber composites) and moves through precision manufacturing (CNC machining, Swiss-style turning, surface treatments and coatings), assembly and packaging, sterilization services, and distribution to hospitals, ambulatory surgical centers, and trauma centers. For digital and smart systems, the upstream layer expands to include software development, verification and validation, and secure data workflows, which increases the role of design controls and supplier qualification under quality systems.

Recent supply-side signals point to fragility in materials logistics and service capacity. In March 2026, Jayon Implants reported 14 to 15 tonnes of titanium raw material stranded in Germany amid shipping route disruptions linked to Middle East conflict, highlighting how titanium availability and transit can affect lead times for pins, rods, and structural components. Industry responses increasingly emphasize dual-sourcing critical inputs, longer-term blanket purchase orders, and inventory buffers, while sterilization capacity constraints in the United States and the geographic concentration for high-end carbon fiber continue to shape cost and fulfillment performance across global OEM networks.

Competitive Landscape

The external fixators market is moderately fragmented. Johnson & Johnson, Stryker, Smith+Nephew, Zimmer Biomet, and Globus Medical anchor global supply, yet none surpasses a dominantly high share, giving mid-tier innovators room to compete. Leaders differentiate via proprietary digital algorithms, automated strut kits, and lightweight composite architectures. Johnson & Johnson’s MAXFRAME AUTOSTRUT, for instance, automates correction schedules and transmits alignment data to surgeons’ tablets, reducing follow-up imaging frequency.

The merger trend continues: Enovis’s acquisition of LimaCorporate expands its reconstruction tool-box to include external-frame know-how, illustrating consolidation around smart implants. Simultaneously, nimble 3-D printing start-ups collaborate with university hospitals to prototype patient-specific frames at point-of-care, nibbling at traditional mass-manufacture volumes.

Suppliers chase white-space in emerging economies with cost-down stainless kits while upselling premium composites in OECD markets. Portfolio breadth, surgeon education, and field-service response times remain the core competitive levers, ensuring that digital augmentation alone does not guarantee victory in the external fixators market.

External Fixators Industry Leaders

Stryker

Zimmer Biomet

Smith & Nephew

Orthofix Holdings, Inc.

Johnson and Johnson

- *Disclaimer: Major Players sorted in no particular order

External Fixators Market Companies Covered in this Report

- Johnson & Johnson

- Stryker

- Smiths Group

- Zimmer Biomet

- Orthofix Holdings

- Medtronic

- Globus Medical

- Acumed

- B. Braun (Aesculap)

- GPC Medical

- Ortho-SUV

- Response Ortho

- Auxein Medical

- Double Medical

- Kanghui (MDT)

- Fixus (USA)

- Orthopaedic Implant Co.

- Tianjin Walkman Biomaterial

- DeRoyal Industries

Market Opportunities and Future Outlook

External fixators opportunities are expanding where they translate into workflow gains and tighter clinical precision, especially with computer-aided and hexapod platforms that reduce manual calculation steps in multi-planar deformity correction and support automated distraction protocols. Regulatory standardization also creates commercialization whitespace for companies that build test and documentation packages around recognized benchmarks, including ASTM F1541-24 (with the prior-version transition period running to December 19, 2027). Under the FDA QMSR, with ISO 13485:2016 aligned expectations effective February 2, 2026, these setups can support more efficient multi-region submissions and supplier qualification.

Platform breadth is another visible avenue, including circular systems that integrate bone reconstruction and soft-tissue management. BlueOcean Global, for example, received FDA 510(k) clearance in January 2026 for its Excelsior External Fixation System, illustrating ongoing entry by newer platforms within Class II external fixation. Materials-led differentiation remains active as well, with radiolucent carbon-fiber frames aligning to imaging-intensive follow-up pathways in trauma and limb reconstruction. At the same time, supply-chain constraints in titanium and sterilization services create room for manufacturers that secure inputs through nearshoring or simplify instrument and tray configurations to support faster hospital and ASC adoption.

Recent Industry Developments in External Fixators Market

- February 2026: Smith+Nephew signed an exclusive US distribution agreement with RMR Ortho to add the A’TOMIC Nitinol Fixation System to its trauma and extremities portfolio. The distribution arrangement expands access to patented nitinol-based fixation technology under a distribution-led route. This broadens portfolio depth without requiring a full platform redevelopment.

- January 2026: Zimmer Biomet announced the commercial launch of the Brachiator Mini-Rail External Fixation System for foot and ankle deformity correction and fracture stabilization, developed with Paragon 28. This expands Zimmer Biomet's presence in small-bone external fixation. It also supports procedure-specific solutions in extremities and trauma settings.

- May 2025: Fusion Orthopedics added Metalogix external fixation systems to its portfolio after completing operations and distribution transfer. The expanded distribution footprint improves availability for surgeons and facilities. It targets trauma and reconstruction workflows that rely on established external fixation systems.

External Fixators Market Report Scope and Research Methodology

Market Definition and Coverage

This market covers revenue generated from external fixation devices used to stabilize bones from outside the body, mainly in trauma and deformity correction, across hospitals and orthopedic care settings.

Scope exclusions: We exclude veterinary external fixation devices, internal fixation implants (plates, screws, nails), and single use casting or splinting supplies.

Segments Covered in This Report

- By Product Type

- Manual Fixators

- Computer-Aided / Smart Fixators

- Hexapod Fixators

- Rail & Ring Fixators

- By Fixation Type

- Unilateral & Bilateral

- Circular

- Hybrid

- Others

- By Application

- Fracture Fixation

- Orthopaedic Deformities

- Infected Fractures

- Limb Lengthening / Correction

- By Anatomical Site

- Upper Extremity

- Lower Extremity

- Pelvic & Hip

- By Material

- Carbon-Fibre Composite

- Stainless Steel

- Titanium Alloy

- Bio-resorbable Polymers

- By End-User

- Hospitals

- Ambulatory Surgical Centres

- Orthopaedic & Trauma Centres

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research helped us set the boundary of what should be counted and what should not, then build the first demand picture by geography. We referenced public sources such as the World Health Organization for injury burden context, the OECD for health system indicators, the US CDC for trauma and fracture-related surveillance signals, and peer-reviewed orthopedic journals for usage patterns and clinical practice trends.

We also checked regulatory and recall listings, procurement notices, and general medtech reporting, then used company filings and investor presentations to understand product mix and regional exposure. Where available, paid subscriptions for company financials, news and financials, and patent databases were used to speed up cross-checks on launches and portfolio changes. The desk sources listed here are illustrative and not exhaustive, and many other references were used for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work was used to test the early model against what is happening in clinics, and to correct assumptions that do not show up cleanly in public data. We spoke with a mix of device-side and care-side experts, including manufacturers, distributors, orthopedic surgeons, trauma center staff, and procurement teams. These interviews helped identify where procedure volumes translate into external fixation use across APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 19% | APAC: 47% |

| Mid tier: 50% | Functional/Unit leaders: 22% | EMEA: 34% |

| Smaller Players: 19% | Managers: 59% | Americas: 19% |

Market-Sizing & Forecasting

Sizing starts with a top-down build that reconstructs the demand pool from orthopedic trauma and limb reconstruction procedure activity, then translates expected external fixation usage into each country and care setting. To keep totals realistic, we corroborate the outputs with selective bottom-up approximations such as sampled average selling price times estimated unit volumes, channel checks by region, and supplier revenue sanity checks where disclosures allow it.

Key inputs used in the model include fracture incidence signals, trauma procedure volumes, the share of cases routed to external fixation (temporary and definitive), the mix between circular frames and unilateral frames, and average selling price ranges adjusted for tender versus private purchasing. Forecasts were developed using scenario analysis, where adoption shifts, pricing pressure, and procedure growth are flexed within ranges validated by primary inputs. When a bottom-up view is incomplete due to limited disclosure in smaller markets, gaps are handled through proxy markets with similar treatment pathways and then adjusted for healthcare access and pricing differences.

Data Validation & Update Cycle

Outputs are checked across multiple steps so that one single assumption does not drive the full number. We compare results against independent signals such as procedure indicators, import and export directionality where it is meaningful, and publicly visible pricing references, then look for sudden jumps that do not match known events.

Before sign-off, another analyst reviews the calculations, the scope boundary, and the reasonableness of the regional split, and sends questions back for re-check. Reports are refreshed annually, and interim updates are made when material events occur, including policy changes, product recalls, or pricing shifts. Right before delivery, a fresh pass is completed so clients receive the latest updated view.

Mordor Intelligence's External Fixators Market Estimate Compared With Other Published Estimates

Different published market values for external fixators can look far apart, even when the topic sounds identical at first glance. The gaps usually come from what is included in the device basket, which year is treated as the base, and how procedure usage and pricing are translated into revenue.

Procedure signals and treatment pathway checks from orthopedic experts were used to keep Mordor Intelligence's estimate tied to external fixation usage rather than a wider fixation systems bucket. In other places, differences often come from counting adjacent products, assuming faster price increases than tenders typically allow, or using an older exchange rate timing when converting regional revenues to USD.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.38 B (2026) | |

| Industry Portal A | USD 2.30 B (2024) | Uses an earlier base year and tends to report a broader external fixator definition without clearly separating temporary trauma use from longer-course reconstruction use, which can shift the implied ASP and volume mix. |

| Syndicated Publisher B | USD 2.28 B (2024) | Runs with a higher growth track through 2031 and appears to treat external fixation systems as a single pooled category, with limited visibility on currency timing and how regional tender discounts are applied. |

The table shows that the spread is mostly explained by base-year choice, scope tightness, and how pricing is handled across tender-heavy markets. By tying the model to procedure-linked demand indicators and then pressure-testing totals with practical pricing and mix checks, we can present a market number that is easier to trace and repeat.

Key Questions Answered in the Report

How large is the external fixators market in 2026?

The market is valued at USD 2.38 billion in 2026, with an 7.58% CAGR projected through 2031.

Which region is expanding fastest in the external fixators market?

Asia-Pacific is the fastest-growing region, expected to progress at a 9.08% CAGR because of rapid urbanization and greater trauma incidence.

What product segment is gaining the most momentum?

Computer-aided and smart external frames are climbing at a 9.48% CAGR thanks to automated strut adjustment and digital monitoring features.

Why are carbon-fiber composites important in external fixators?

Carbon-fiber composites are radiolucent and lightweight, improving imaging workflow and patient comfort, which is why they are growing at an 11.02% CAGR.

What is the main restraint holding back broader adoption?

Competition from advanced internal fixation plates and nails, which deliver strong biomechanical stability without external hardware, reduces uptake in elective cases.

Page last updated on: