Automotive Exhaust Emission Control Device Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 55.72 Billion |

| Market Size (2030) | USD 65.45 Billion |

| Growth Rate (2025 - 2030) | 3.27% CAGR |

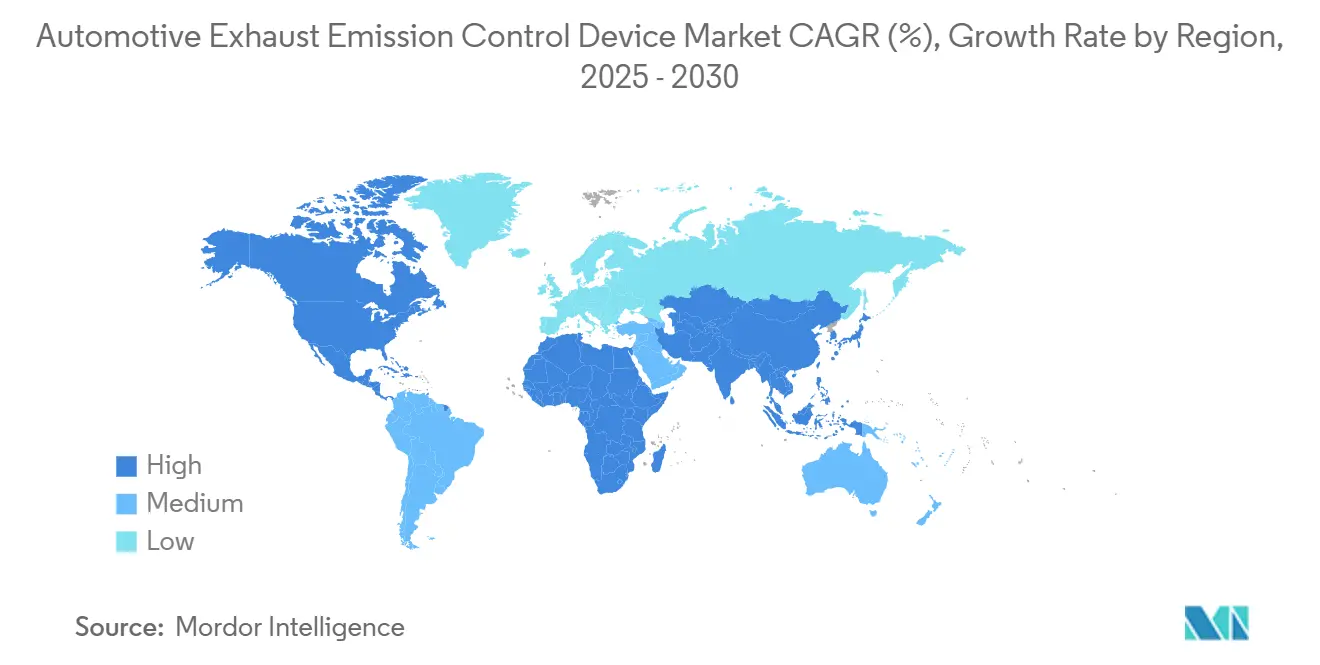

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

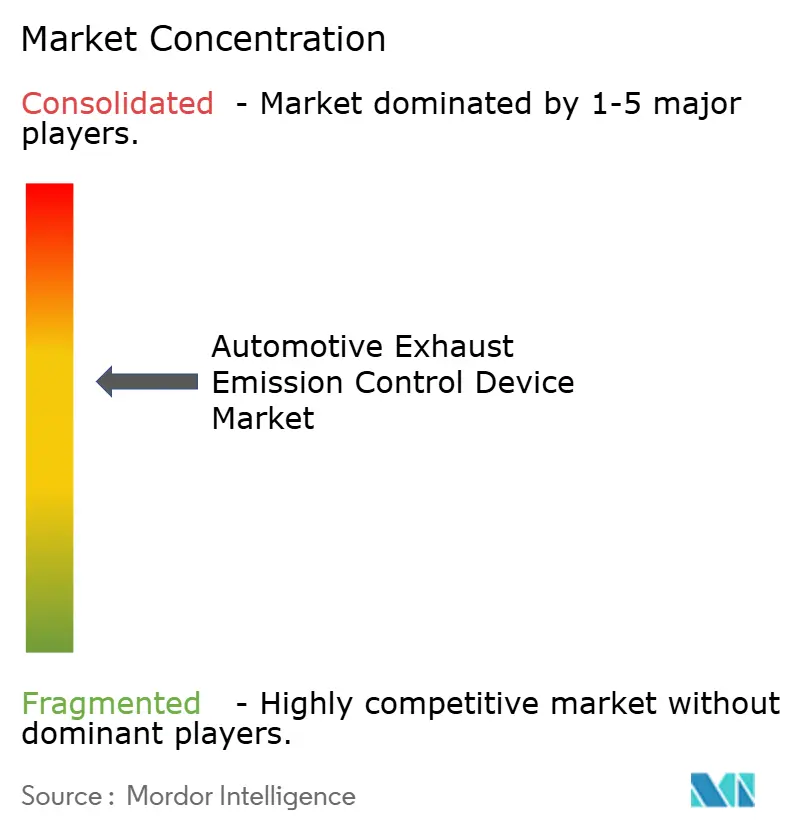

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Exhaust Emission Control Device Market Analysis by Mordor Intelligence

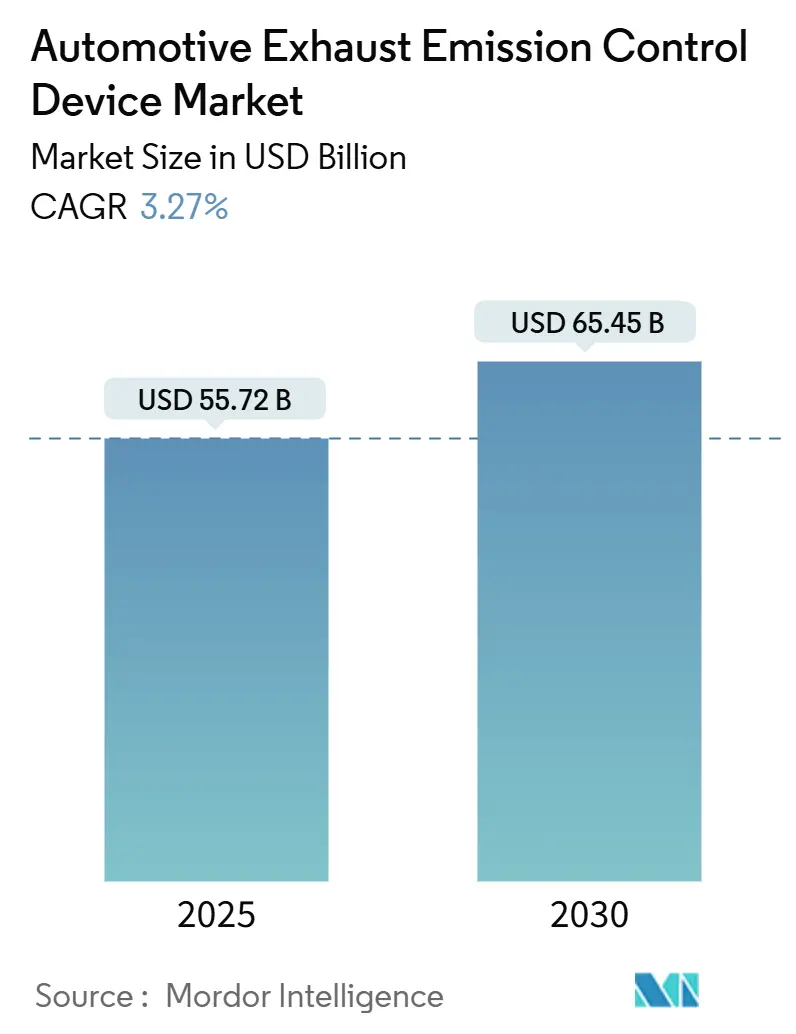

The automotive exhaust emission control device market size is valued at USD 55.72 billion in 2025 and is forecast to reach USD 65.45 billion by 2030, translating into a 3.27% CAGR during the forecast period. The measured trajectory reflects a transition phase in which tighter global emission rules sustain demand for advanced after-treatment hardware even as battery-electric vehicle (BEV) growth erodes volumes tied to internal combustion engines. Euro 7 Real Driving Emissions requirements, in force from 2025, oblige every vehicle category to meet stricter limits under real-world conditions, which pushes manufacturers toward higher-capacity three-way catalysts, gasoline particulate filters, and predictive sensor suites. In parallel, California’s Advanced Clean Cars II rules demand that 35% of a brand’s 2026 sales be zero-emission models, creating a split market where premium emission-control solutions thrive beside a fast-rising BEV base[1]“Advanced Clean Cars II factsheet,”, California Air Resources Board, arb.ca.gov. Asia-Pacific maintains clear leadership because India’s BS-VI leap and China’s National VI-B enforcement raise technology content per vehicle, while diesel’s energy advantage sustains heavy-duty demand. Precious-metal supply shocks influence catalyst design strategies and procurement costs, particularly palladium and rhodium.

Key Report Takeaways

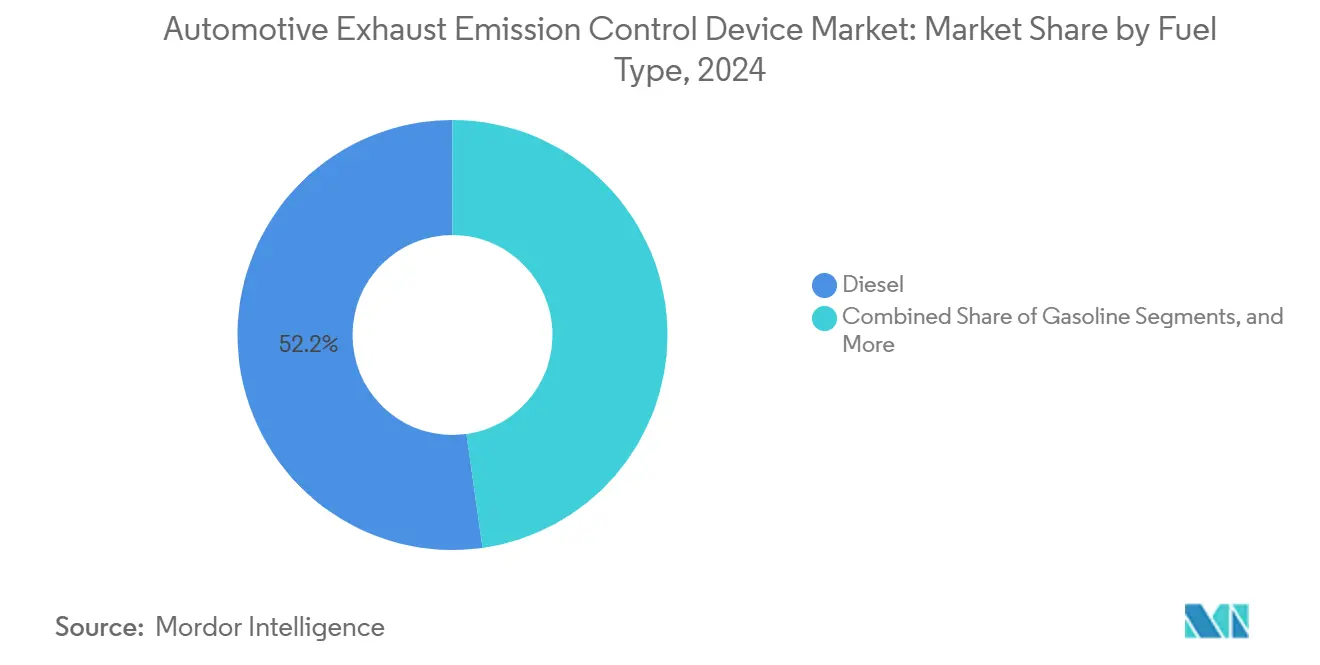

- By fuel type, diesel led with 52.22% of the automotive exhaust emission control device market share in 2024, while alternative fuels are projected to expand at a 5.32% CAGR through 2030.

- By vehicle type, passenger cars accounted for 58.81% of the automotive exhaust emission control device market share in 2024, whereas light commercial vehicles are forecast to post the fastest 4.37% CAGR to 2030.

- By material type, platinum commanded 43.87% of the automotive exhaust emission control device market share in 2024, and rhodium is expected to register the highest 4.83% CAGR over the forecast horizon.

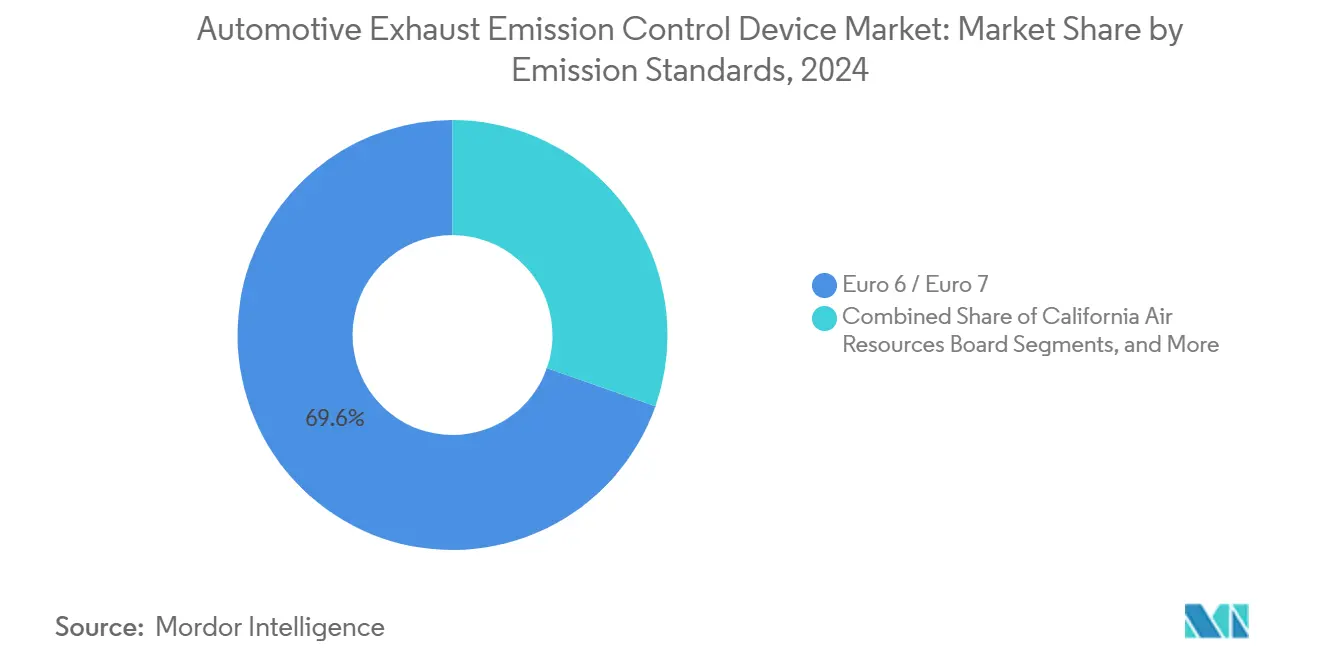

- By emission standard, Euro 6/Euro 7 platforms captured 69.63% share of the installed base of the automotive exhaust emission control device market in 2024, but BS-VI systems are set to grow the quickest at a 5.74% CAGR through 2030.

- By distribution channel, the OEM route held 72.77% of the automotive exhaust emission control device market share in 2024, whereas the aftermarket is anticipated to rise at a 3.84% CAGR to 2030.

- By geography, Asia-Pacific dominated with 38.31% of the automotive exhaust emission control device market share in 2024 and is also projected to achieve the fastest 4.34% CAGR through 2030.

Global Automotive Exhaust Emission Control Device Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening Euro 7 And U.S. Tier 3/LEV III Regulations | +0.8% | Europe, North America, spillover to Asia-Pacific | Medium term (2-4 years) |

| Hybrid-Vehicle Production Surge Sustaining ICE After-Treatment Demand | +0.7% | Japan, Europe, China | Long term (≥4 years) |

| Platinum For Palladium Substitution Moderating Cost Swings | +0.6% | Global manufacturing hubs | Short term (≤2 years) |

| Wider Adoption of Gasoline Particulate Filters in GDI Engines | +0.5% | Europe, North America, Asia-Pacific | Medium term (2-4 years) |

| Monetization of CO₂ Credits Via Lower-Emission Ices | +0.4% | Europe, California, other regions | Medium term (2-4 years) |

| Mandatory On-Board AI Exhaust Monitoring | +0.3% | Europe, North America, Asia-Pacific | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Euro 7 and U.S. Tier 3 Enforcement Widen Technology Needs

Euro 7 introduces Real Driving Emissions evaluation over broader temperature bands, forcing OEMs to adopt higher oxygen-storage catalysts, integrated particulate filtration, and fast-light-off substrates. The rule’s 10 mg/km particle-number ceiling pushes gasoline particulate filters into high-volume B-segment cars, while California Tier 3 brings SCR upgrades to light trucks. Together, these rules accelerate a global technology refresh that favors suppliers holding proven designs and flexible precious-metal recipes[2]“Euro 7 proposal details,”, European Commission, ec.europa.eu.

Hybrid Volumes Keep ICE Demand Resilient

Toyota alone delivered 3.6 million hybrids 2023 and required low-temperature light-off formulations to curb cycling emissions [3]“Global EV and hybrid outlook 2024,”, International Energy Agency, iea.org. Hybrid penetration cushions the automotive exhaust emission control device market against an immediate BEV displacement shock and extends the revenue stream for advanced after-treatment through at least 2030.

Platinum-heavy Recipes Temper Palladium Exposure

To cut costs, catalyst makers are turning away from palladium, opting for platinum-rich formulations that still meet emissions standards. Industry giants Johnson Matthey and BASF are spearheading this transition, innovating and strategically sourcing to lessen their dependence on palladium from Russia. These companies are developing advanced technologies and leveraging alternative supply chains to ensure a steady supply of raw materials. These industry shifts underscore a larger movement towards balancing cost, performance, and supply chain stability in emissions control technologies.

Particulate Filter Uptake Broadens to Mainstream Cars

Volkswagen shifted to standard GPF installation across all TSI engines, highlighting a cost-down trajectory that places filters even on 1.0 L city cars. Continental’s electrically heated GPF releases trapped soot during urban short trips, solving regeneration challenges and lifting fuel economy. Chinese brands are following suit ahead of National VII, meaning GPF demand will scale quickly outside premium tiers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating BEV Uptake in Urban Fleets | -0.9% | Global urban centers | Short term (≤2 years) |

| Precious-Metal Price Spikes and Supply Disruption | -0.7% | Global | Short term (≤2 years) |

| OEM Thrifting of PGM Loadings | -0.4% | Global volume brands | Medium term (2-4 years) |

| Low-Cost Chinese BEVs Cannibalizing Entry-Level Ices | -0.5% | Asia-Pacific, emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

BEV Share Rises Quickly in Delivery Fleets

Major logistics players are rapidly deploying electric vans in European urban delivery fleets. As these vehicles become more concentrated, they displace high-value diesel aftertreatment systems. This shift has a pronounced effect on parts revenue, overshadowing what fleet numbers might indicate. Meanwhile, BYD's assertive export strategy amplifies this transition, particularly in city-center applications facing tightening zero-emission mandates.

PGM Supply Disruptions Compound Cost Risk

Mining strikes and geopolitical sanctions have caused significant price fluctuations in precious metals. This volatility has pressured catalyst suppliers bound by fixed-price contracts with automakers. As a result, these suppliers are facing tighter profit margins and heightened demands for working capital. Moreover, with recycling addressing just a small portion of end-of-life catalysts, the industry is vulnerable to sudden supply disruptions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fuel Type: Diesel Retains Bulk Yet Alternatives Scale Fast

Diesel technologies accounted for 52.22% of the automotive exhaust emission control device market share in 2024. Complex SCR-with-DPF layouts remain mandatory for long-haul trucks and off-road equipment. However, the alternative-fuel slice is growing at 5.32% CAGR through 2030, with compressed natural gas buses and hydrogen fuel cell range extenders attracting public transport operators because NOx and particulate levels start lower. The automotive exhaust emission control device market size for alternative fuels will widen further as renewable biogas mandates under the EU Renewable Energy Directive II raise biogenic blend rates.

Emissions parity across fuel types under Euro 7 erases any historic diesel leniency, while the California Heavy-Duty Omnibus cuts diesel NOx 90% by 2027, pushing costs higher. Natural gas engines leverage simpler oxidation catalysts with lean-burn combustion to meet these limits. Hydrogen mobility is nascent but triggers demand for low-temperature ammonia slip catalysts and dedicated particulate traps when used in internal-combustion form. Suppliers with modular layouts adaptable across fuels hold a competitive edge.

By Vehicle Type: Commercial Demand Intensifies Technology Complexity

Passenger cars occupied 58.81% of the automotive exhaust emission control device market share in 2024, yet light commercial vehicles are set for the swiftest 4.37% CAGR through 2030, thanks to e-commerce logistics. Delivery vans often face stricter urban limits and therefore adopt combined SCR-on-filter systems. Daimler Truck’s latest SCR catalyst stores extra ammonia for heavy trucks and extends service intervals beyond 500,000 km, illustrating the imperative for durability.

For fleet operators, downtime is costly. Predictive diagnostics tied to AI modules alert users to catalyst deactivation, encouraging proactive replacement. Such connectivity adds revenue streams beyond the physical substrate, a trend poised to lift the automotive exhaust emission control device market even if raw unit counts fall.

By Material Type: Rhodium Scarcity Drives Design Innovation

Platinum captured the most significant slice at 43.87% of the automotive exhaust emission control device market share in 2024 because its supply base is broader and less geopolitically risky than palladium. Despite representing only single-digit loading grams, Rhodium is critical for gasoline NOx control and is expanding at a 4.83% CAGR through 2030. Prices touched USD 15,000 per ounce in 2024, prompting single-atom dispersion research that lowers rhodium grams per catalyst by up to 40% while holding conversion efficiency. BASF is piloting rhodium-free tri-metal configurations that could reset the material mix once scale-validated.

Rhodium’s scarcity forces suppliers to hedge inventories months ahead. At the same time, recycling plants such as Johnson Matthey’s sites aim to recover PGMs from scrapped catalysts, bolstering circular supply and supporting climate objectives.

By Emission Standard: Asian Rules Accelerate Growth

Euro 6/Euro 7 systems owned 69.63% of the automotive exhaust emission control device market share in 2024, yet India’s BS-VI upgrade is the fastest climber at 5.74% CAGR through 2030. The overnight switch from BS-IV to BS-VI required catalysts and electronic control upgrades for real-time diagnostics. China’s National VI-B brought similar changes in 2024, creating a large wave of fresh demand, and National VII drafts will add ammonia slip targets that require next-generation sensors.

United States rules follow a different cadence. Tier three focuses on reduced sulfur fuel and durability up to 150,000 miles, which stretches catalyst lifespan designs. Harmonization across states simplifies OEM supply chains but obliges catalysts to meet the strictest California bin.

By Distribution Channel: Aftermarket Gains as Vehicles Age

The OEM channel’s 72.77% of the automotive exhaust emission control device market share in 2024 results from mandatory fitment at production and warranty coverage. Nonetheless, the aftermarket advances at a 3.84% CAGR through 2030 thanks to prolonged vehicle life in emerging countries and European right-to-repair regulations. Independent workshops now access OEM-grade catalyst data, allowing them to install compliant replacements without voiding warranties. Predictive analytics embedded in telematics flags nearing failure, driving pre-emptive aftermarket sales, especially in light commercial fleets focused on uptime.

Geography Analysis

Asia-Pacific led with 38.31% of the automotive exhaust emission control device market share in 2024 and is forecast to grow at a 4.34% CAGR to 2030. India’s BS-VI step lifted average catalyst value per vehicle, while China’s National VI-B sweep now covers motorcycles and off-road categories, broadening the product pool. Japan has a significant share of world hybrid output, which fuels high demand for cold-start catalysts and gasoline particulate filters able to withstand frequent engine on–off events[4]“Hybrid production statistics 2024,”, Japan Automobile Manufacturers Association, jama.or.jp.

Europe remains technology-dense. Euro 7 legal text locks in particulate number limits, making gasoline filters standard. Despite long-term goals for zero-tailpipe emissions, Germany’s industry invests heavily in internal combustion engine (ICE) technologies. Recent efforts focus on refining catalyst washcoats and integrating sensors to improve emissions control. Retrofit demand in low-emission zones adds recurring revenue from older diesel vehicles, reinforcing the value of ICE innovation in the near term.

North America posts steady gains. California’s Clean Cars II stringency, plus the federal Tier 3 rollout, sustain the automotive exhaust emission control device market even as BEV titles rise. Class 8 trucks are now designed around the 2027 Heavy-Duty Omnibus package, requiring higher SCR volumes, close-coupled light-off catalysts, and ammonia slip monitors. Mexico’s growing assembly base produces cost-competitive catalysts for USMCA flows, while natural-gas truck fleets in Texas add distinct oxidation and methane-slip catalysts.

Competitive Landscape

The automotive exhaust emission control device market shows moderate concentration, led by suppliers such as Johnson Matthey, BASF, Umicore, Faurecia (FORVIA), Continental, and Tenneco. Competitive advantage hinges on precious metal sourcing, material science, and integrated electronics. FORVIA’s 2024 launch of its Clean Mobility division merges exhaust hardware with hydrogen systems, offering a hedge as ICE volumes taper.

Continental patented an AI-enabled exhaust gas recirculation valve that adjusts in real time to sensor data, prolonging catalyst life and reducing ammonia consumption. Tenneco and Cummins formed a heavy-duty SCR joint venture to couple engine calibration with optimized after-treatment packaging for North America fleets. Umicore secured platinum through a significant South African partnership to reduce exposure to palladium volatility. At the same time, BASF expanded its capabilities by acquiring Cataler and gaining expertise in gasoline particulate filters for Asian markets. These moves reflect broader efforts to stabilize supply chains and enhance regional specialization in emissions control technologies. Barriers for new entrants remain high due to capital intensity, regulatory certification costs, and the need for stable PGM supply channels.

Automotive Exhaust Emission Control Device Industry Leaders

FORVIA SE

Tenneco Inc.

Johnson Matthey Plc

Eberspächer Gruppe GmbH & Co. KG

BASF SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Cummins India Limited, a top player in power solutions technology, unveiled its Retrofit Aftertreatment System (RAS). This cutting-edge clean air solution enables customers to upgrade their existing CPCBII and CPCBI gensets, ensuring compliance with the latest emission regulations. Designed and developed locally, this advanced retrofit emission control device boasts an impressive efficiency, slashing emissions of Particulate Matter (PM), Carbon Monoxide (CO), and Hydrocarbons (HC) from genset exhaust by up to 90%.

- January 2024: In Pinghu, China, BASF Environmental Catalyst and Metal Solutions (ECMS) and Heraeus Precious Metals have launched their joint venture, BASF HERAEUS Metal Resource Co., Ltd (BHMR). This new facility specializes in extracting precious metals from used automotive catalysts, promoting a circular economy and bolstering China's sustainability and supply security objectives.

Global Automotive Exhaust Emission Control Device Market Report Scope

| Gasoline |

| Diesel |

| Natural Gas |

| Alternative Fuels |

| Passenger Car |

| Light Commercial Vehicles |

| Medium & Heavy Commercial Vehicles |

| Platinum |

| Palladium |

| Rhodium |

| Euro 6 / Euro 7 |

| California Air Resources Board (CARB) |

| Tier 2 Bin 5 / U.S. Tier 3 |

| BS-VI & Successor Norms |

| Original Equipment Manufacturer (OEM) |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle-East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Fuel Type | Gasoline | |

| Diesel | ||

| Natural Gas | ||

| Alternative Fuels | ||

| By Vehicle Type | Passenger Car | |

| Light Commercial Vehicles | ||

| Medium & Heavy Commercial Vehicles | ||

| By Material Type | Platinum | |

| Palladium | ||

| Rhodium | ||

| By Emission Standard | Euro 6 / Euro 7 | |

| California Air Resources Board (CARB) | ||

| Tier 2 Bin 5 / U.S. Tier 3 | ||

| BS-VI & Successor Norms | ||

| By Distribution Channel | Original Equipment Manufacturer (OEM) | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle-East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the automotive exhaust emission control device market in 2025?

The automotive exhaust emission control device market size is USD 55.72 billion in 2025.

What CAGR is expected for these exhaust systems through 2030?

The market is projected to grow at a 3.27% CAGR, reaching USD 65.45 billion by 2030.

Which region leads revenue generation?

Asia-Pacific holds 38.31% of 2024 global revenue and also records the fastest 4.34% CAGR to 2030.

How are platinum and palladium trends affecting costs?

Catalyst makers are substituting platinum for palladium to cut exposure to price spikes, reducing palladium use by up to 20% while maintaining performance.

What is driving aftermarket demand?

Longer vehicle lifetimes, roadside emission checks, and right-to-repair laws are fueling a 3.84% CAGR for aftermarket catalyst replacements.

Page last updated on: