Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

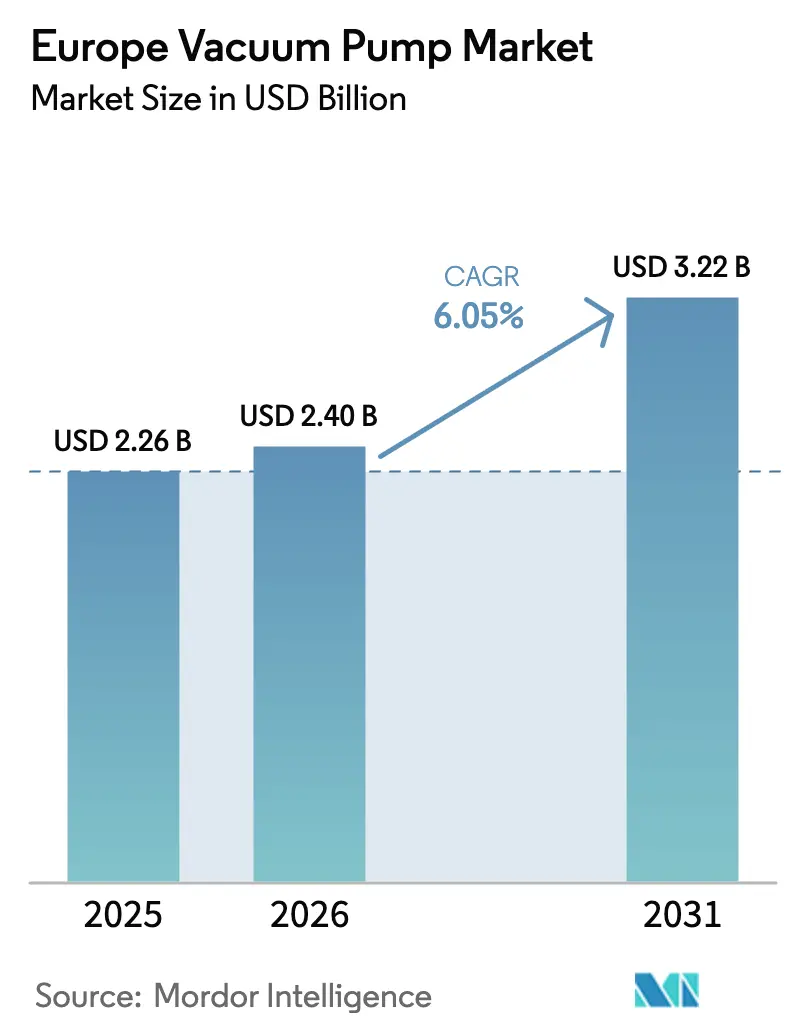

| Base Year Market Size (2025) | USD 2.26 Billion |

| Market Size (2026) | USD 2.4 Billion |

| Market Size (2031) | USD 3.22 Billion |

| Growth Rate (2026 - 2031) | 6.05% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Vacuum Pump Market Analysis by Mordor Intelligence

The Europe vacuum pump market size was valued at USD 2.26 billion in 2025 and estimated to grow from USD 2.4 billion in 2026 to reach USD 3.22 billion by 2031, at a CAGR of 6.05% during the forecast period (2026-2031). Persistent fab expansions, battery‐cell gigafactories, and hydrogen-electrolyser roll-outs keep demand resilient despite margin pressure from Asian imports. Semiconductor manufacturers specify ever-lower base pressures, which accelerates turbomolecular pump adoption, while EU PFAS rules are steering users toward dry, oil-free designs. Germany’s industrial ecosystem anchors current volume, but pan-EU decarbonisation programs, quantum-computing research, and pharmaceutical freeze-drying capacity upgrades diversify the addressable base. As a result, the Europe vacuum pump market continues to pivot from commodity equipment to high-performance, service-centric offerings that raise switching costs and embed suppliers deeper into customer workflows.

Key Report Takeaways

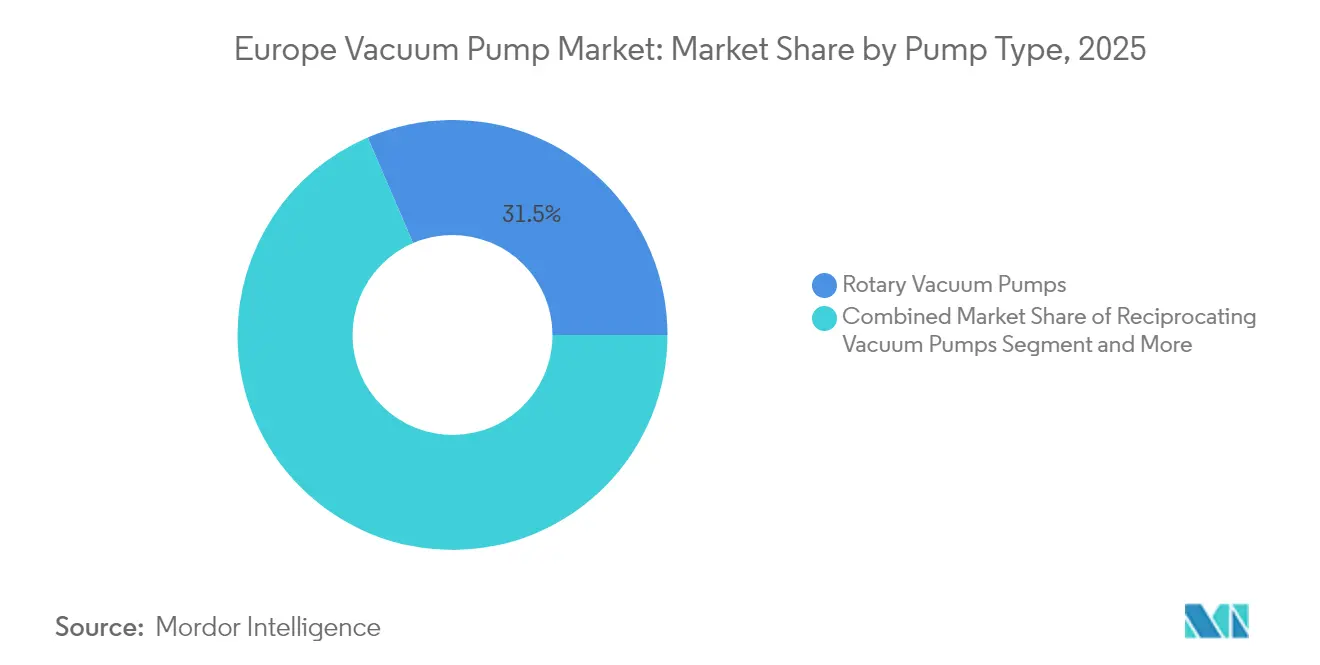

- By pump type, rotary vane units led with 31.45% revenue share in 2025, while turbomolecular pumps are projected to expand at a 7.42% CAGR through 2031.

- By vacuum level, rough-vacuum applications captured 45.30% of the Europe vacuum pump market share in 2025, but high and ultra-high vacuum segments are advancing at an 8.35% CAGR to 2031.

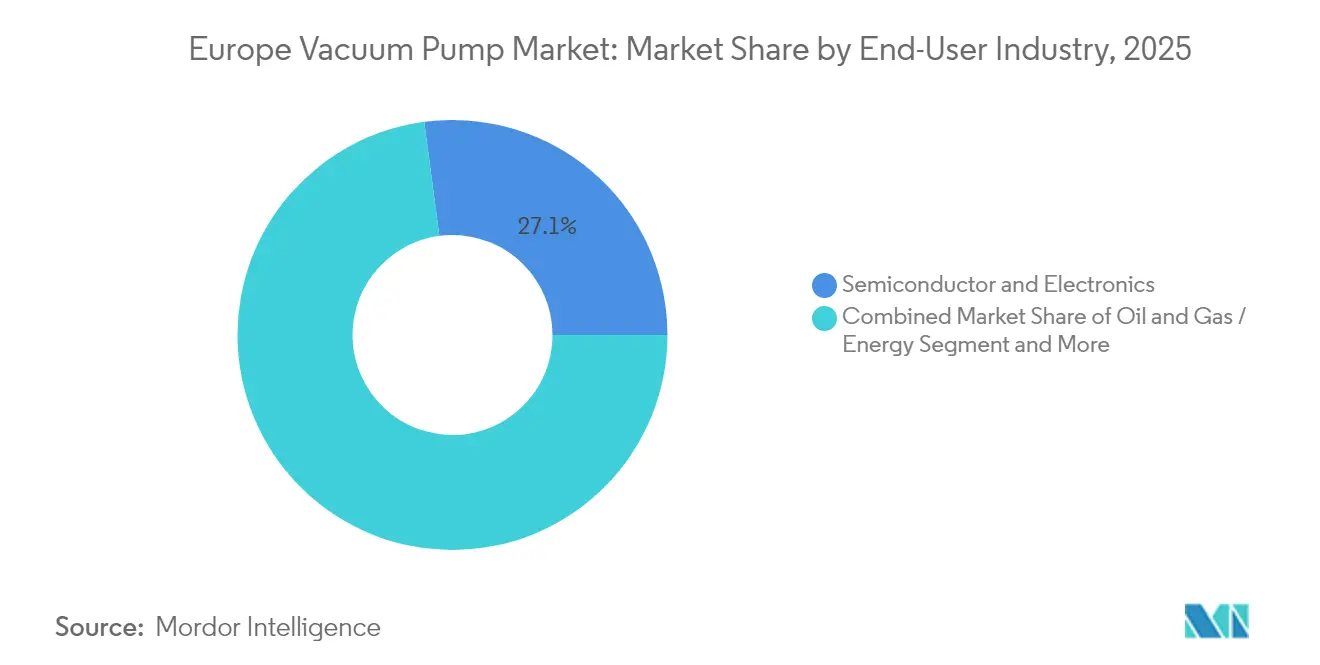

- By end-user industry, semiconductor and electronics accounted for 27.10% of the Europe vacuum pump market size in 2025; battery cell manufacturing is the fastest-growing application at a 7.05% CAGR.

- By drive and lubrication, oil-sealed pumps still held 54.20% share of the Europe vacuum pump market size in 2025, yet dry pumps are expanding at an 8.02% CAGR.

- By geography, Germany contributed 23.70% of the Europe vacuum pump market in 2025, while the Netherlands is forecast to record the highest 7.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Vacuum Pump Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in semiconductor & MEMS fab expansions | 1.80% | Germany, Netherlands, France | Medium term (2-4 years) |

| Shift toward dry, oil-free pumps in clean processes | 1.20% | EU-wide, strongest in Germany, Netherlands | Long term (≥ 4 years) |

| Pharma & biotech freeze-drying capacity build-out | 0.90% | Germany, Switzerland, France, UK | Medium term (2-4 years) |

| Hydrogen-electrolyser gigafactories need high vacuum | 0.70% | Netherlands, Denmark, Germany | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Semiconductor and MEMS Fab Expansions

Europe’s push to secure 20% of global chip output drives unprecedented vacuum demand. GlobalFoundries is investing EUR 1.1 billion (USD 1.2 billion) to raise Dresden capacity to 1.5 million wafers annually, while Infineon’s EUR 5 billion (USD 5.4 billion) Smart Power Fab comes online in 2026, each specifying 10⁻⁷ mbar base pressures for advanced nodes. [1]Infineon Technologies AG, “Infineon receives building permit for final construction phase of Smart Power Fab in Dresden”, Infineon, infineon.com New wide-band-gap lines such as Nexperia’s SiC/GaN facility tighten particulate-control tolerances, lifting turbomolecular pump penetration. The Europe vacuum pump market therefore realigns around high-flow, contamination-free systems that bundle pumps with abatement and condition-monitoring modules.

Shift Toward Dry, Oil-Free Pumps in Clean Processes

EU Regulation 2024/573 phases out long-chain PFAS lubricants and imposes recovery mandates, accelerating the migration from oil-sealed to dry pumps. Dry screw, claw, and scroll technologies mitigate vapor contamination and lower disposal costs, a key selling point for pharmaceutical and food processors facing stricter hazard-analysis audits. OEMs such as Pfeiffer Vacuum respond with DuoVane oil-free rotary designs that retain familiar maintenance intervals while eliminating PFAS exposure risks. As compliance windows close, Europe vacuum pump market participants monetize retrofit services and predictive-maintenance subscriptions.

Pharma and Biotech Freeze-Drying Capacity Build-Out

EMA quality directives push drug makers to add redundancy and contamination control to freeze-dryers, where chamber pressures fluctuate between 10⁻¹ and 10⁻³ mbar. OEMs like Leybold promote dry-running pumps that prevent hydrocarbons from entering sterile zones and endure thermal shocks from –50 °C to +60 °C cycles. Pump makers capture value through validation support, GMP documentation, and rapid-response field service. The Europe vacuum pump industry leverages these high-margin aftermarket streams to offset price competition in standard rotary segments.

Hydrogen-Electrolyser Gigafactories Need High Vacuum

EU-funded SOEC projects demand 10⁻⁶ mbar environments during cell sintering and sealing, linking vacuum performance directly to electrolyser efficiency. The TopSOEC program’s EUR 94 million (USD 102 million) grant exemplifies the shift toward mass-manufactured green hydrogen systems, while EBARA’s 16 billion yen (USD 105 million) liquid-hydrogen test center underlines the equipment roadmap. Suppliers able to engineer corrosion-resistant, helium-tight pumps earn first-mover advantages as national hydrogen strategies scale to 10 million tonnes output by 2030.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX of advanced dry/turbo pumps | –0.8% | EU-wide, particularly Germany, France | Short term (≤ 2 years) |

| Asian import price pressure squeezing margins | –0.6% | EU-wide, strongest in price-sensitive segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High CAPEX of Advanced Dry/Turbo Pumps

Turbomolecular pumps cost 3-5 times more than oil-sealed rotary units, reflecting magnetic-bearing and position-control complexity. PFAS-free seals add 15-25% to bill-of-materials, slowing adoption in SMEs with stretched payback horizons. Although semiconductors absorb these premiums, cost-sensitive packaging, plastics, and woodworking lines defer upgrades, limiting near-term penetration for high-end models in the Europe vacuum pump market.

Asian Import Price Pressure Squeezing Margins

VDMA data show 2024 vacuum revenues slipping despite stable pump output as low-cost Asian brands undercut European list prices by up to 30% in rotary vane and liquid-ring categories. Local champions defend share through acquisitions—Atlas Copco closed 33 deals in 2024 alone—and by bundling equipment with 24/7 service contracts. Nonetheless, commoditized segments face persistent gross-margin compression that narrows R&D budgets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Pump Type: Rotary Dominance Faces Kinetic Challenge

Rotary vane designs held 31.45% revenue in 2025, underpinning the largest slice of the Europe vacuum pump market. The familiar architecture serves packaging, material handling, and general industrial tasks where 10⁻¹ to 10⁻³ mbar suffices. Yet turbomolecular units post a 7.42% CAGR through 2031 as fabs, quantum-computing labs, and surface-science tools impose ultra-high vacuum thresholds. Hybrid rotary-screw designs such as Pfeiffer’s DuoVane promise oil-free operation while preserving port-to-port interchangeability, easing migration costs.

Within kinetic pumping, turbo, diffusion, and ejector technologies fill the <10⁻⁷ mbar niche, justifying premium price-points. Entrapment pumps—getter and cryo—extend the spectrum to 10⁻¹⁰ mbar for gravitational-wave observatories and cold-atom systems. As specialist requirements proliferate, the Europe vacuum pump market size for kinetic and entrapment categories is projected to outgrow rotary sales by value after 2030, even though volumetric shipments remain lower.

By Vacuum Level: High-Vacuum Applications Accelerate

Rough-vacuum duties represented 45.30% revenue in 2025, anchored by food packaging and thermoforming lines. Medium vacuum applications—coatings, analytical instruments, legacy semiconductor steps—span 10⁻³ to 10⁻⁷ mbar and integrate roots-blowers or multistage dry screws as backing pumps. High and ultra-high segments, however, are growing at an 8.35% CAGR as advanced logic nodes, EUV lithography, and MBE systems scale.

Quantum-computing prototypes now specify continuous 10⁻¹⁰ mbar environments, necessitating bakeable chambers and low-outgassing pump materials. The Europe vacuum pump market size for ultra-high vacuum services thus expands alongside European Research Council programs, while high-vacuum growth parallels AI chip volumes at 12 nm and below. Process toolmakers respond by offering modular pump racks that cascade from fore-vacuum to turbo stages, compressing footprint and simplifying service.

By End-User Industry: Semiconductor Leadership, Battery Growth

Semiconductors captured 27.10% value in 2025, reaffirming their role as the strategic anchor tenant of the Europe vacuum pump market. Each 30,000 m² fab module requires hundreds of pumps across etch, deposition, and implant stations; tool density escalates further at advanced nodes. Battery cell manufacturing, aided by EUR 450 million (USD 488 million) EIB funding for the Douai plant, records a 7.05% CAGR as electrolyte drying and pouch sealing add vacuum stages.

Chemical and petrochemical operators modernize distillation and solvent-recovery loops, demanding corrosion-resistant screws and liquid-ring systems. Pharma multiplies freeze-drying skids for biologics, while food packaging maintains a steady pull for rotary vane workhorses. This end-market diversity shields suppliers from single-sector cyclicality and sustains a balanced revenue pyramid across the Europe vacuum pump industry.

By Drive/Lubrication: Dry Transition Accelerates

Oil-sealed machines still represent 54.20% 2025 revenue, favored for simplicity and lower first cost. Yet dry screws, claws, and scrolls log an 8.02% CAGR under PFAS scrutiny. Semiconductor fabs already mandate dry pumps to avert backstreaming, and pharmaceutical users follow to meet GMP hazard-analysis thresholds. Based on announced retrofit programs, the Europe vacuum pump market share for dry configurations may surpass 50% of new installations by 2028, although the installed base evolves more slowly due to long service lives.

Service models also diverge: oil-sealed units need frequent oil changes, whereas dry pumps require periodic seal kit and bearing cartridge swaps. OEMs exploit this by bundling long-term service agreements that lock in revenue and ensure genuine-part usage, offsetting shorter mechanical overhaul cycles.

Geography Analysis

Germany generated 23.70% of the Europe vacuum pump market in 2025 thanks to dense automotive, semiconductor, and chemical clusters. GlobalFoundries and Infineon expansions intensify local turbomolecular demand, while battery-pack automation in Saxony adds rough-vacuum volume. German OEMs leverage DAkkS-certified calibration services to uphold precision requirements, turning service responsiveness into a differentiator. A skilled-labor deficit, however, caps ramp-up speed and reinforces vendor lock-in.

The Netherlands leads growth with a 7.12% CAGR through 2031. Hydrogen-hub projects around Rotterdam and ternary-cathode battery lines along the North Sea Canal necessitate corrosion-resistant, oil-free pumps at scale. EU-sponsored SOEC programs embed Dutch-Danish supply chains that favor European pump suppliers, buffering them against low-cost imports. Local integrator Induvac extends aftermarket reach through 24-hour on-call service, illustrating how niche providers thrive alongside global brands.

France, Italy, Spain, and the UK form a mature consumption block where pharmaceuticals, aerospace, and renewable-energy OEMs ensure steady orders. The French Douai gigafactory alone requires upward of 600 pumps across electrode production and electrolyte filling. Italy’s precision machining sector specifies oil-free screws for vacuum heat treatment, while Spain’s wind-blade factories use roots blowers for composite infusion. The UK pharmaceutical cluster maintains high-vacuum demand for analytical QC despite Brexit-related logistics friction. Eastern Europe, including Poland and Romania, posts above-average expansion as supply chains migrate eastward; Busch Group’s Romanian service hub pre-positions capacity for this shift.

Competitive Landscape

The Europe vacuum pump market is moderately concentrated around Atlas Copco, Pfeiffer Vacuum+Fab Solutions, Busch Group, Leybold, and Edwards. Collectively these five suppliers exceed 60% revenue, but no single firm dominates all technology classes. Atlas Copco’s 2024–2025 acquisition spree, including Oerlikon’s vacuum segment, widens its portfolio and complements compressor lines to deliver “plant-air-to-process-vacuum” packages. Busch’s tri-brand architecture unifies rough, claw, and turbo offerings, improving cross-selling while preserving niche brand equity.

Technology differentiation centers on magnetic bearing turbopumps, chemical-resistant coatings, and embedded analytics. Patent filings for active-magnetic suspension reduce vibration and extend service intervals, enabling higher throughput in EUV lithography. Digital twins hosted on OEM cloud platforms provide runtime diagnostics and energy-efficiency benchmarking, allowing vendors to sell outcome-based contracts rather than spare parts alone.

Asian entrants leverage cost leadership in commoditized segments, prompting European incumbents to focus on advisory services, application engineering, and regulatory compliance support. Partnerships with toolmakers and line integrators lock pumps into proprietary recipes, raising switching barriers. White-space opportunities emerge in quantum-computing dilution refrigerators and liquid-hydrogen logistic chains, both demanding ultra-high vacuum and cryogenic capability that few low-cost providers can match.

Europe Vacuum Pump Industry Leaders

-

Atlas Copco AB

-

Pfeiffer Vacuum GmbH

-

Flowserve Corporation

-

Busch Group

-

Edwards Vacuum

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: GlobalFoundries announced plans for EUR 1.1 billion investment to expand its Dresden chip fabrication facility, nearly doubling production capacity from 800 000–850 000 wafers to 1.5 million annually, with German federal government support expected.

- March 2025: Atlas Copco acquired Kyungwon Machinery Industry Co., Ltd. for approximately 60 BKRW (USD 465 million), expanding oil-free compressor offerings for semiconductor and food clients.

- February 2025: Flowserve Corporation reported record Q4 2024 results, with Pumps Division bookings of USD 3.3 billion, a 13% increase year over year.

- January 2025: Busch Group expanded its presence in Romania through strategic market-development initiatives, enhancing service coverage in Eastern Europe.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the European vacuum pump market as all new, factory-built equipment that evacuates sealed chambers by mechanically or kinetically removing gas molecules. Coverage spans rotary, reciprocating, kinetic, dynamic, and entrapment pumps sold across EU-27, the United Kingdom, EFTA, and Turkey.

Scope Exclusion: We exclude aftermarket spares, rental fleets, stand-alone compressors, and maintenance services.

Segmentation Overview

-

By Pump Type

-

Rotary Vacuum Pumps

- Rotary Vane Pumps

- Screw and Claw Pumps

- Roots Pumps

-

Reciprocating Vacuum Pumps

- Diaphragm Pumps

- Piston Pumps

-

Kinetic Vacuum Pumps

- Ejector Pumps

- Turbomolecular Pumps

- Diffusion Pumps

-

Dynamic Pumps

- Liquid Ring Pumps

- Side Channel Pumps

-

Specialised / Entrapment Pumps

- Getter Pumps

- Cryogenic Pumps

-

Rotary Vacuum Pumps

-

By Vacuum Level

- Rough Vacuum (≥10⁻³ mbar)

- Medium Vacuum (10⁻³ – 10⁻⁷ mbar)

- High and Ultra-High Vacuum (<10⁻⁷ mbar)

-

By End-user Industry

- Semiconductor and Electronics

- Oil and Gas / Energy

- Chemical and Petrochemical

- Pharmaceutical and Biotechnology

- Food and Beverage Packaging

- Power Generation

- Wood, Paper and Pulp

- Other Manufacturing (Automotive, Aerospace, etc.)

-

By Drive / Lubrication

- Oil-Sealed Pumps

-

Dry (Oil-free) Pumps

- Dry Scroll Pumps

- Dry Screw Pumps

- Dry Claw Pumps

-

By Country

- Germany

- United Kingdom

- France

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

Detailed Research Methodology and Data Validation

Primary Research

Interviews with pump OEM executives, wafer-fab process engineers, biopharma utility heads, and regional distributors across Central, Northern, and Southern Europe let us validate price moves, duty cycles, and emerging clean-vacuum preferences.

Desk Research

Mordor analysts begin with desk research. We mine Eurostat PRODCOM shipment values, German VDMA pump indices, and HMRC trade codes to benchmark unit flows and prices. Additional insight comes from European Semiconductor Industry Association capacity lists, ECHA PFAS dossiers, and articles in the Journal of Vacuum Science and Technology.

We also review company 10-Ks, investment releases, and customs databases such as Volza for country splits, while D&B Hoovers and Dow Jones Factiva verify vendor scale. These sources are illustrative; many other public and paid references support data collection, validation, and clarification.

Market-Sizing & Forecasting

Our top-down model reconstructs demand from production and trade data, then cross-checks totals with bottom-up supplier roll-ups. Key drivers include semiconductor capacity additions, EU chemical output, pharma fill-finish line installations, battery gigafactory projects, and average pump replacement age. Multivariate regression anchored to industrial production and capex series projects volumes, while exponential smoothing captures short-run swings. Gaps in country data are bridged with three-year moving averages that are confirmed during primary calls.

Data Validation & Update Cycle

Mordor's senior analysts run variance checks, resolve anomalies, and release figures only after peer review. We refresh the database annually and issue interim revisions when material events occur, so clients receive the most current view.

Why Mordor's Europe Vacuum Pump Baseline Merits Reliance

Published European vacuum pump values often differ, and we recognize these contrasts.

Differences arise from whether dry microelectronics pumps are bundled with cryogenic units, the inclusion of aftermarket revenues, inflation treatment, and refresh cadence. Mordor reports equipment-only values, fixes currency to average 2024 EUR-USD, and updates each year, which explains the spread you see below.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.26 B (2025) | Mordor Intelligence | - |

| USD 2.36 B (2025) | Regional Consultancy A | Includes limited aftermarket kits and mid-year currency conversion |

| USD 1.60 B (2024) | Global Consultancy B | Omits high and ultra-high vacuum segments and forecasts from 2024 base |

| USD 1.19 B (2022) | Industry Data Provider C | Covers wet pumps only and relies on older trade data with no recent primary checks |

The comparison shows that scope choice and refresh cadence drive most variance. Mordor's disciplined definitions, blended modeling, and annual verification create a balanced, transparent baseline decision makers can trust.

Key Questions Answered in the Report

What is the current value of the Europe vacuum pump market?

The market is valued at USD 2.4 billion in 2026 and is projected to reach USD 3.22 billion by 2031, registering a 6.05% CAGR.

Which pump type leads the Europe vacuum pump market?

Rotary vane pumps retain leadership with 31.45% 2025 revenue, although turbomolecular designs are the fastest-growing at a 7.42% CAGR.

How big is the semiconductor end-user segment?

Semiconductors represented 27.10% of the Europe vacuum pump market size in 2025, driven by ongoing fab expansions and advanced node investments.

Why are dry vacuum pumps gaining traction?

EU PFAS regulations and contamination-control requirements push users toward oil-free pumps that eliminate fluorinated lubricants and lower total compliance costs.

Which country offers the strongest growth outlook?

The Netherlands shows the highest 7.12% CAGR through 2031, supported by hydrogen-hub projects and new battery manufacturing capacity.

Page last updated on: