Europe Tissue And Hygiene Paper Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

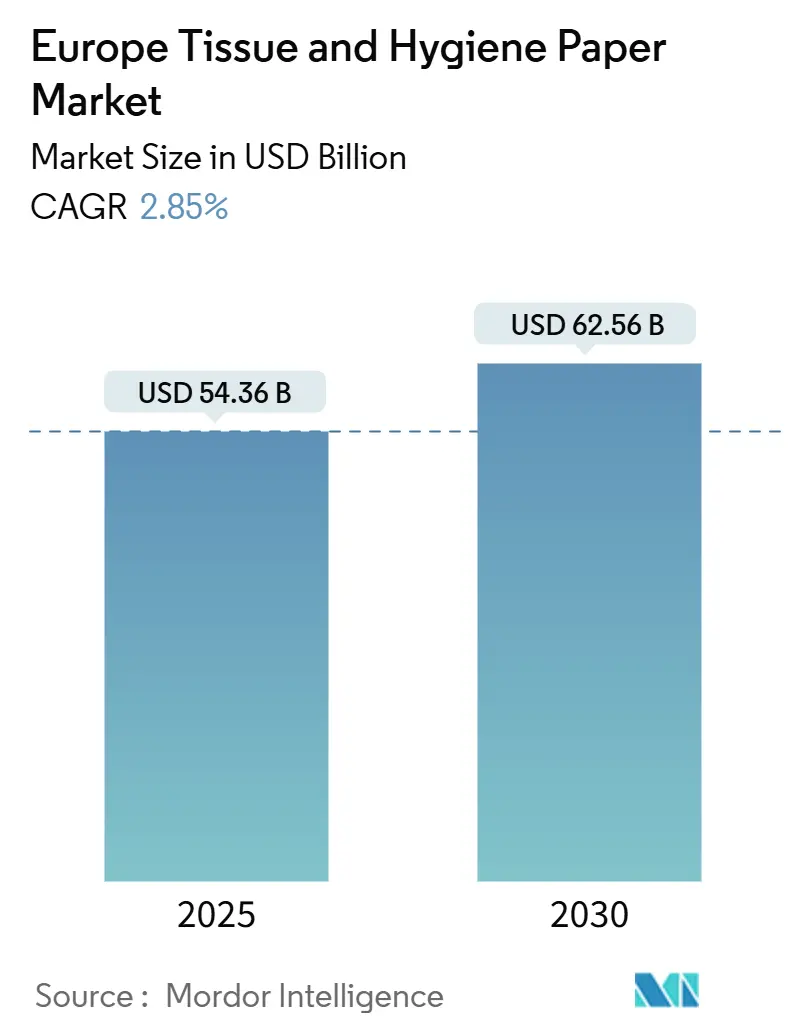

| Market Size (2025) | USD 54.36 Billion |

| Market Size (2030) | USD 62.56 Billion |

| Growth Rate (2025 - 2030) | 2.85% CAGR |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Tissue And Hygiene Paper Market Analysis by Mordor Intelligence

The Europe tissue and hygiene paper market Size stood at USD 54.36 billion in 2025 and is forecast to reach USD 62.56 billion by 2030, advancing at a 2.85% CAGR. This progression underscores a mature yet steadily expanding landscape where demographic ageing, post-pandemic hygiene priorities and sustainability regulations redefine category dynamics. Adult-incontinence demand rises in tandem with the 21.6% share of citizens aged 65 plus, while heightened hygiene awareness fuels premium tissue uptake in both retail and away-from-home (AFH) channels. Regulatory levers such as the EU Deforestation Regulation spur a 5.45% CAGR shift toward recycled fibre, and e-commerce proliferation strengthens direct-to-consumer (D2C) subscription models that lock in recurring volumes. Competitive intensity grows as private labels command 39% of grocery sales, prompting branded leaders to differentiate through smart manufacturing and eco-innovation.

Key Report Takeaways

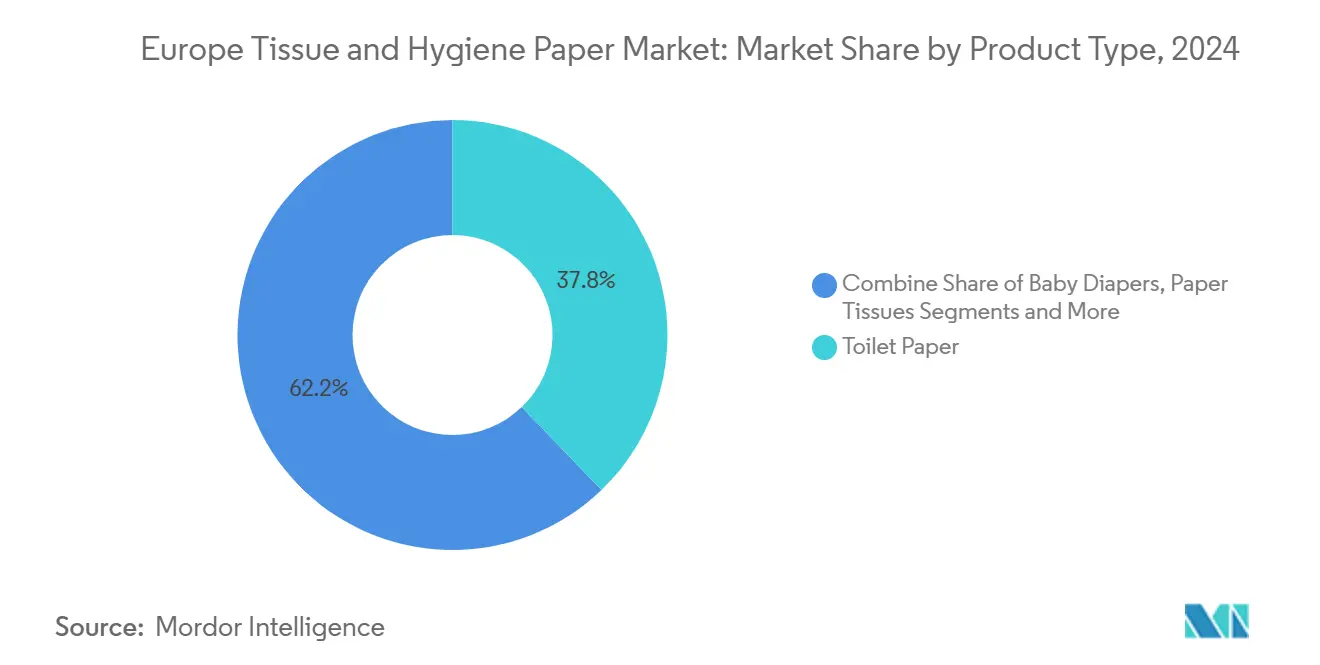

- By product type, toilet paper led with 37.81% revenue share in 2024, whereas paper tissues are set to climb at a 4.01% CAGR through 2030.

- By raw material, kraft pulp retained a 47.34% share of the Europe tissue and hygiene paper market size in 2024, while recycled fibre adoption is expanding at a 5.45% CAGR.

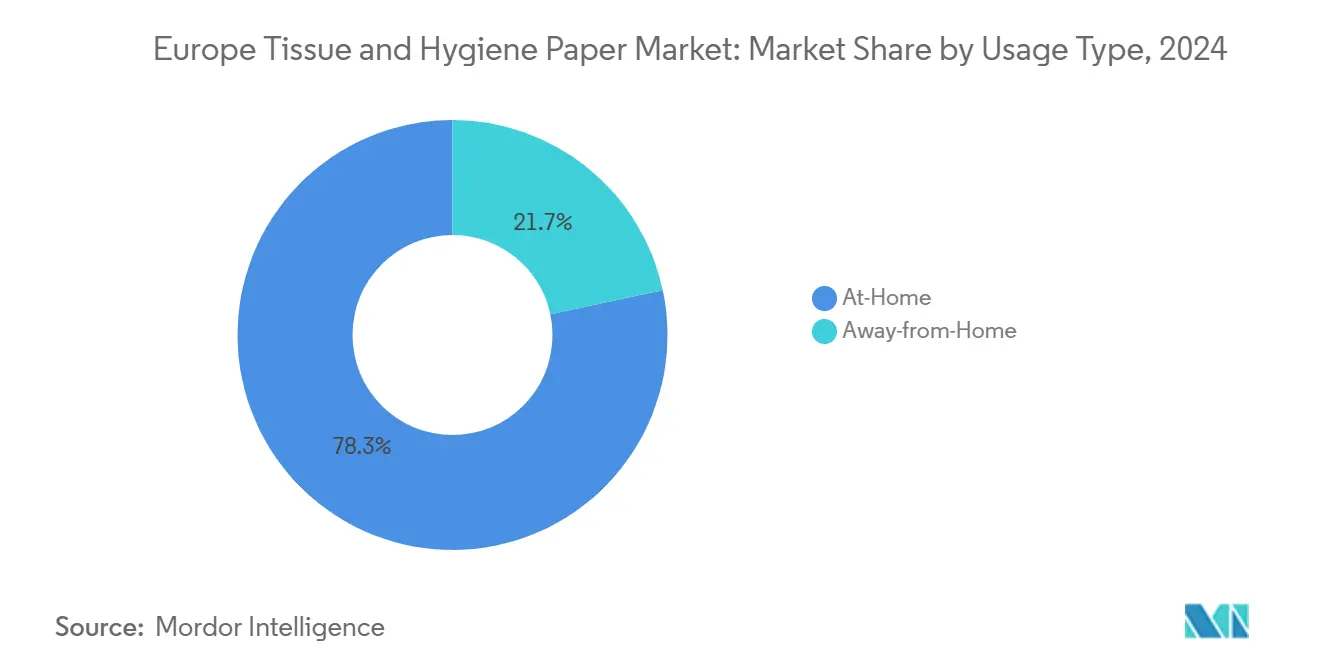

- By usage type, at-home consumption accounted for 78.33% of the Europe tissue and hygiene paper market share in 2024; AFH demand is projected to rise at a 3.38% CAGR to 2030.

- By end-use industry, healthcare and aged-care facilities are advancing at a 4.87% CAGR, outpacing the dominant residential segment’s stable base.

- By country, Germany held 18.21% of the Europe tissue and hygiene paper market share in 2024, while Sweden is projected to grow the fastest at a 5.11% CAGR through 2030.

Europe Tissue And Hygiene Paper Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging population boosting adult-incontinence demand | +0.8% | Western Europe core, spreading eastward | Long term (≥ 4 years) |

| Heightened hygiene awareness post-pandemic | +0.6% | Continent-wide | Medium term (2-4 years) |

| Surge in e-commerce and D2C retail channels | +0.4% | North & West Europe, expanding eastward | Medium term (2-4 years) |

| EU deforestation rules accelerating recycled tissue uptake | +0.5% | EU-wide, strongest in Germany, France, Nordics | Long term (≥ 4 years) |

| Tourism rebound elevating AFH tissue demand | +0.3% | Mediterranean countries, major cities | Short term (≤ 2 years) |

| Automation in tissue-converting plants enabling near-shoring | +0.2% | Germany, Italy, Sweden hubs | Medium term (2-4 years) |

Source: Mordor Intelligence

Aging population boosting adult-incontinence demand

Europe’s share of citizens aged 80 plus rose from 3.8% in 2004 to 6.1% in 2024, and Germany alone will need 2.15 million nurses by 2049, up from 1.62 million in 2019. [1]Eurostat, “Demography of Europe – 2025 Edition,” ec.europa.eu Healthcare and aged-care facilities therefore underpin a 4.87% CAGR for incontinence products, while new German procurement contracts for absorbent bed protection went live in June 2025. PAUL HARTMANN AG echoed the trend with 1.6% revenue growth in incontinence management during 2024. The old-age dependency ratio of 33.9% sustains purchasing power for premium, discreet, and eco-friendly formats, repositioning incontinence from clinical supply to mainstream wellness item.

Heightened hygiene awareness post-pandemic

Consumer risk perception permanently tilted toward health protection, lifting paper tissue volumes at a 4.01% CAGR even as toilet paper remains category anchor. IoT-enabled dispensers and UV-C cleaning robots in hospitals and airports push institutional buyers to stricter hygiene benchmarks, encouraging premium, skin-safe fibres. Lenzing responded by broadening LENZING Lyocell Dry biodegradable portfolio in November 2024, aligning with the EU Single-Use Plastics Directive. AFH volumes grow 3.38% as tourism nights climbed to 2.92 billion in 2023, 1.6% above 2019 levels.

Surge in e-commerce and D2C retail channels

Private-label sales touched EUR 354.5 billion (USD 409.04 billion) in 2024, equal to 39% of grocery turnover, demonstrating how digital platforms enhance price transparency and subscription convenience.[2]PLMA International, “European Private Label Sales Rose to 355 Billion €,” plmainternational.com Sofidel’s U.S. expansions exemplify suppliers pivoting to omnichannel fulfilment models that complement brick-and-mortar distribution. Consumers appreciate discreet online fulfilment for adult-care products, shrinking category stigma and supporting cross-sell opportunities.

EU deforestation rules accelerating recycled tissue uptake

The EU Deforestation Regulation, pushed to 30 December 2025, obliges full geo-traceability for wood-based imports and threatens 4% of global turnover fines for non-compliance. Fibre substitution thus advances recycled content at 5.45% CAGR despite kraft pulp’s 47.34% stronghold. Blockchain pilots and PEFC’s due-diligence portal mitigate compliance risk. Innovation such as Soft N Dry’s tree-free ecoLiite Core™ diaper illustrates early-mover benefit in circular sourcing.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile pulp and energy prices squeezing margins | -0.7% | Germany, Sweden, Finland mills | Short term (≤ 2 years) |

| Environmental and PFAS concerns over disposables | -0.4% | EU-wide, strictest in Nordics | Medium term (2-4 years) |

| Private-label price wars in mature retail | -0.5% | Western Europe | Medium term (2-4 years) |

| Decarbonization capex under EU-ETS Phase IV | -0.3% | Energy-intensive sites | Long term (≥ 4 years) |

Source: Mordor Intelligence

Volatile pulp and energy prices squeezing margins

Hardwood pulp now accounts for 70% of global supply as softwood costs rise, widening substitution yet complicating quality management. Though energy prices eased, EU-ETS carbon certificates multiplied tenfold, eroding industrial margins European Central Bank. CEPI noted industry resilience but flagged thin spreads, especially for independent converters.[3]CEPI, “Pulp and Paper Industry Resilience in 2023,” cepi.org

Environmental and PFAS concerns over disposables

The upcoming Packaging and Packaging Waste Regulation caps PFAS at 25 ppb single/250 ppb total from August 2026, driving reformulation costs. Italy’s July 2023 waste-reuse decree and recycling targets intensify compliance obligations. Brands investing in compostable fibres win early credibility among eco-sensitive Nordic consumers.

Segment Analysis

By Product Type: Toilet Paper Dominance Faces Tissue Innovation

Paper tissues are growing at a 4.01% CAGR, eroding toilet paper’s 37.81% grip as consumers prioritise portability, softness and perceived germ defence. Premium facial boxes and on-the-go pocket packs carry higher margin per tonne, cushioning the segment against pulp inflation. Baby diapers maintain stable volumes; Soft N Dry’s tree-free advancement shows how sustainability and performance coexist. Feminine hygiene enjoys tailwinds from online education and destigmatisation, while AFH towel demand tracks tourism recovery. Household roll segments endure price combat as retailers leverage their 39% private-label share to attract value shoppers. Specialty gifting tissues exploit seasonal peaks to lift category average selling price. Innovation centred on embossing patterns and lotion-infused plies supports brand differentiation against commoditisation pressure.

The Europe tissue and hygiene paper market size for paper tissues is set to widen its contribution by 2030, with soft-pack formats gaining traction in premium grocery chains. Toilet paper, while mature, still anchors household staples and benefits from loyalty programmes in e-commerce subscriptions. The Europe tissue and hygiene paper industry channels research into ultra-lightweight yet strong sheets that reduce fibre use without sacrificing handfeel. Segment leaders therefore balance cost savings and user experience to maintain competitiveness.

Note: Segment shares of all individual segments available upon report purchase

By Raw Material: Recycled Fibre Acceleration Challenges Kraft Pulp Leadership

Kraft pulp retained 47.34% share in 2024, reflecting its tensile strength and brightness attributes vital for high-speed converting lines. Yet recycled fibre volumes will swell at 5.45% CAGR as retailers demand certified low-carbon packaging. Blockchain-enabled traceability satisfies the EU Deforestation Regulation’s stringent origin proof. Hardwood pulp, now 70% of global usage, delivers softness prized in facial tissues, whereas sulfite grades serve niche premium formats. ANDRITZ air-laid technology underpins material versatility, processing blends of recycled and alternative fibres with minimal energy draw.

As recycled input rises, manufacturers recalibrate Yankee-dryer parameters to sustain sheet quality, illustrating the operational complexities of circular sourcing. The Europe tissue and hygiene paper market size tied to recycled fibre segments is projected to expand steadily alongside municipal collection upgrades. Brands publicise eco-certifications on-pack to justify premium shelf pricing, while cooperative pulp-supply agreements mitigate feedstock volatility. The Europe tissue and hygiene paper market thereby moves toward a dual-fibre system where virgin and secondary pulps coexist according to application needs.

By Usage Type: At-Home Stability Contrasts Away-From-Home Recovery

At-Home consumption still absorbed 78.33% of volumes in 2024 as hybrid work kept household demand elevated. Subscription e-commerce models lock in repeat toilet-paper deliveries and incentivise upselling of facial tissues and kitchen towels. Conversely, AFH demand is reviving at a 3.38% CAGR on the back of vibrant hotel and foodservice sectors. IoT sensor deployment optimises dispenser refill cycles, enhancing facility cleanliness perception and boosting per-capita usage.

The Europe tissue and hygiene paper market size attached to AFH channels will therefore outpace the at-home base in relative terms yet remain smaller in absolute tonnes. The segment’s margin profile is attractive thanks to customised emboss logos and touch-free dispenser rentals. The Europe tissue and hygiene paper market share of leading AFH converters could climb as hospitality groups consolidate procurement across regions.

By End-Use Industry: Healthcare Expansion Outpaces Residential Stability

Residential buyers, holding 74.47% share, display price sensitivity that favours private labels. However, Healthcare and aged-care facilities are advancing at a 4.87% CAGR, translating demographic pressure into steady contract volumes. Italy’s EUR 1.18 billion allocation for medical equipment underscores public-sector spending on infection-control consumables. German nursing home expansion similarly widens bulk tissue tender scopes.

The European tissue and hygiene paper market size tied to healthcare accounts is set for sustained gain as insurers recognise the cost avoidance of superior hygiene regimes. Hospitality and office segments also pivot to premium, dermatologically tested paper to reassure guests and employees. The Europe tissue and hygiene paper industry, therefore, invests in ISO-class cleanroom capacity to serve sensitive medical-grade SKUs.

Geography Analysis

Germany’s 18.21% share underscores its status as regional anchor for both retail and away-from-home (AFH) channels. High household penetration, robust e-commerce subscription programmes and hospital procurement frameworks sustain volume, while early compliance with EU carbon and deforestation rules positions German mills as credible export suppliers. France and the United Kingdom continue to advance premiumisation strategies; both markets benefit from private-label innovation that commands shelf space worth EUR 354.5 billion across Europe in 2024.

Sweden’s 5.11% CAGR leads regional growth thanks to large-scale capacity expansions and strong eco-labelling culture. The Netherlands serves as corporate headquarters hub, evidenced by the Suzano–Kimberly-Clark USD 3.4 billion joint venture that leverages Dutch logistics to reach more than 70 countries. Spain capitalises on tourism rebound, supported by Essity’s EUR 24 million Puigpelat upgrade that strengthens AFH supply.

Italy’s healthcare spending, including EUR 1.18 billion for medical equipment, expands demand for medical-grade tissue. Poland and other Central-Eastern economies exhibit rising per-capita consumption as living standards converge with Western norms, though infrastructure and compliance investments remain prerequisites. Mediterranean tourism—totaling 2.92 billion accommodation nights in 2023—boosts AFH consumption across coastal nations, while Nordic innovation and Eastern European volume potential together shape a geographically diverse opportunity landscape for the Europe tissue and hygiene paper market.

Competitive Landscape

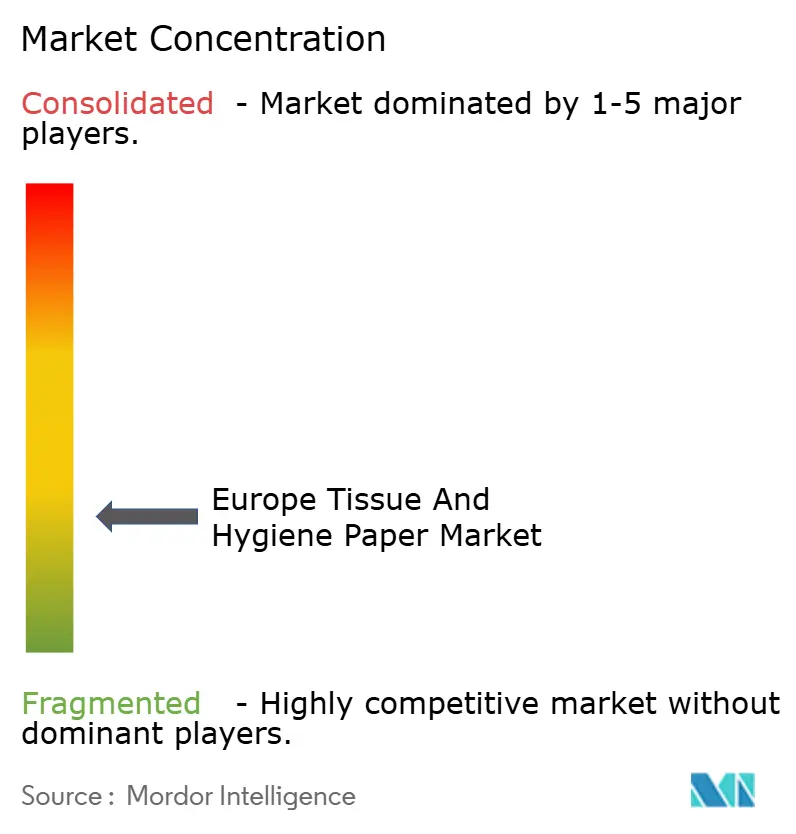

The Europe tissue and hygiene paper market is fragmented: multinationals such as Essity, Kimberly-Clark and Procter & Gamble coexist with regional leaders Sofidel, Lucart and WEPA. Private-label share at 39% exerts price pressure, compelling branded players to innovate around texture, packaging and verified sustainability. The Suzano–Kimberly-Clark USD 3.4 billion joint venture pools 22 mills across 14 countries, seeking scale synergies in procurement and R&D.

Automation and digital twins are strategic pivots; Valmet’s FactoryPal acquisition enhances predictive maintenance, trimming unplanned downtime. First Quality’s plan for two new TAD lines in Ohio highlights North-Atlantic capacity balancing aimed at ultra-premium towelling. Sustainability remains competitive differentiator: Lenzing’s biodegradable fibres and Soft N Dry’s tree-free core resonate with eco-conscious consumers and institutional buyers.

Region-specific specialists capture niches—e.g., healthcare-centric HARTMANN grew incontinence sales 1.6% in 202. Consolidation is likely to persist as players seek fibre-supply security and compliance capital amid tightening EU decarbonisation mandates. Digital D2C insurgents leverage personalised marketing to erode orthodox shelf dominance, yet scale incumbents retain brand equities and R&D heft to defend share.

Europe Tissue And Hygiene Paper Industry Leaders

-

Sofidel Group

-

Kimberly Clark Corporation

-

Metsa Group

-

Industrie Cartarie Tronchetti SpA

-

Lucart SpA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Suzano and Kimberly-Clark unveiled a USD 3.4 billion tissue joint venture headquartered in the Netherlands.

- April 2025: Sofidel agreed to acquire key assets of Royal Paper in the United States pending court approval.

- February 2025: First Quality Tissue detailed plans for two new TAD machines in Defiance, Ohio.

- January 2025: ANDRITZ completed the kraft-paper conversion at HEINZEL GROUP’s Steyrermühl mill in Austria.

Europe Tissue And Hygiene Paper Market Report Scope

The European tissue and hygiene paper market includes various tissue and hygiene paper products designed for end consumers. Tissue paper uses hardwood and softwood trees, water, and synthetic compounds. The method for producing tissue paper includes pulping and retting, adding color or components to strengthen or soften and improve the water-holding limit, and finally, squeezing the item to form into the necessary shape. The study on the European tissue and hygiene paper market tracks demands in terms of revenue. The study factors in the prevalent base scenarios, key themes, and end-user-related demand cycles. Toilet paper and bathroom tissues are used interchangeably, serving the same function.

The European tissue and hygiene paper market is segmented by product (baby diapers, feminine hygiene, household paper, incontinence, paper tissues [paper napkins, paper towels, face tissue, and specialty and wrapping tissue], and toilet paper), raw materials (kraft, sulfite, recycled, and other raw materials), type (at home and away from home), and country (United Kingdom, Germany, France, Italy, Spain, Netherlands, Denmark, Finland, Norway, Sweden, Ireland, Switzerland, Russia, Poland, and the Rest of Europe). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Product Type | Baby Diapers | ||

| Feminine Hygiene | |||

| Household Paper | |||

| Incontinence Products | |||

| Paper Tissues | Paper Napkins | ||

| Paper Towels | |||

| Facial Tissues | |||

| Specialty and Wrapping Tissues | |||

| Toilet Paper | |||

| By Raw Material | Kraft Pulp | ||

| Sulfite Pulp | |||

| Recycled Fiber | |||

| Other Raw Materials | |||

| By Usage Type | At-Home | ||

| Away-from-Home | |||

| By End-Use Industry | Residential Households | ||

| Hospitality and Foodservice | |||

| Healthcare and Aged-Care Facilities | |||

| Other End-use Industry | |||

| By Country | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Netherlands | |||

| Denmark | |||

| Sweden | |||

| Russia | |||

| Poland | |||

| Rest of Europe | |||

| Baby Diapers | |

| Feminine Hygiene | |

| Household Paper | |

| Incontinence Products | |

| Paper Tissues | Paper Napkins |

| Paper Towels | |

| Facial Tissues | |

| Specialty and Wrapping Tissues | |

| Toilet Paper |

| Kraft Pulp |

| Sulfite Pulp |

| Recycled Fiber |

| Other Raw Materials |

| At-Home |

| Away-from-Home |

| Residential Households |

| Hospitality and Foodservice |

| Healthcare and Aged-Care Facilities |

| Other End-use Industry |

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Netherlands |

| Denmark |

| Sweden |

| Russia |

| Poland |

| Rest of Europe |

Key Questions Answered in the Report

What is the current size of the Europe tissue and hygiene paper market?

It was valued at USD 54.36 billion in 2025 and is forecast to reach USD 62.56 billion by 2030 at a 2.85% CAGR.

Which product category is expanding fastest?

Paper tissues are growing at a 4.01% CAGR, outpacing toilet paper despite its larger base.

How will EU deforestation rules affect fibre sourcing?

The regulation mandates full traceability by late-2025, accelerating recycled-fibre uptake at a 5.45% CAGR and prompting investment in compliant supply chains.

Why are adult-incontinence products gaining momentum?

Europe’s ageing population drives a 4.87% CAGR in healthcare and aged-care facility demand, supported by rising nursing staff and procurement contracts.

How significant are private labels in this market?

Private-label tissue and hygiene products held 39% of European grocery sales in 2024, worth EUR 354.5 billion, intensifying price competition.

Which country is projected to grow the quickest?

Sweden leads with a 5.11% CAGR through 2030 owing to advanced automation and sustainability-focused capacity expansion.

Page last updated on: June 24, 2025