Europe Tissue And Hygiene Paper Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

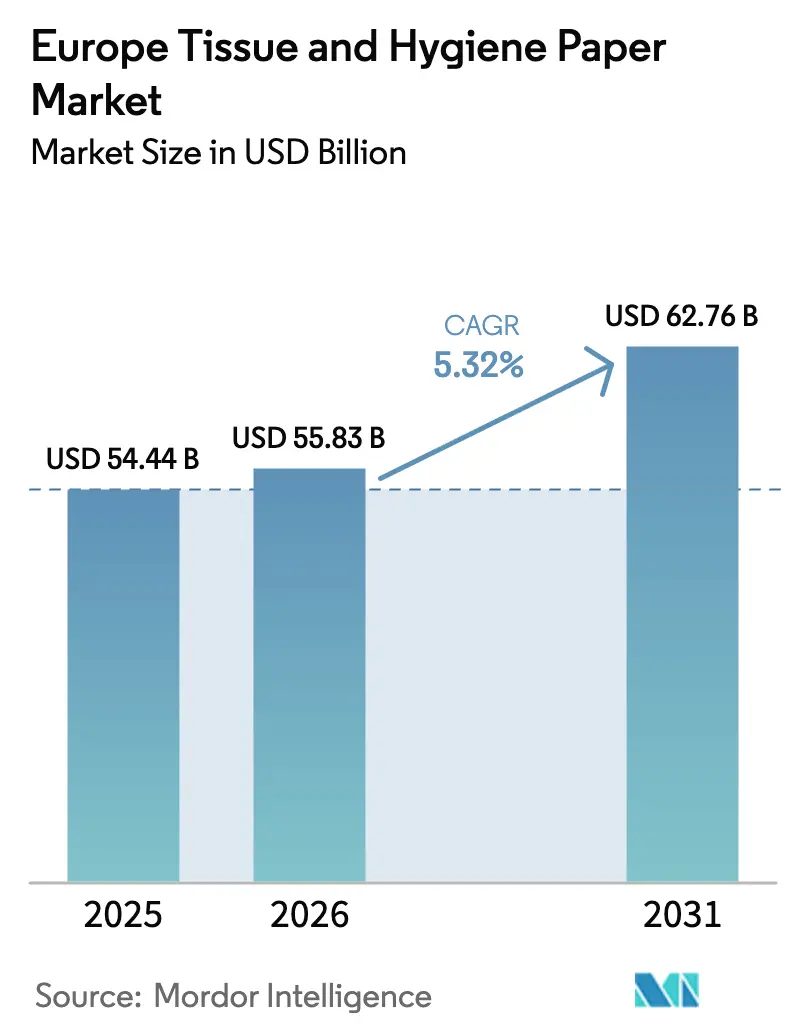

| Base Year Market Size (2025) | USD 54.44 Billion |

| Market Size (2026) | USD 55.83 Billion |

| Market Size (2031) | USD 62.76 Billion |

| Growth Rate (2026 - 2031) | 5.32% CAGR |

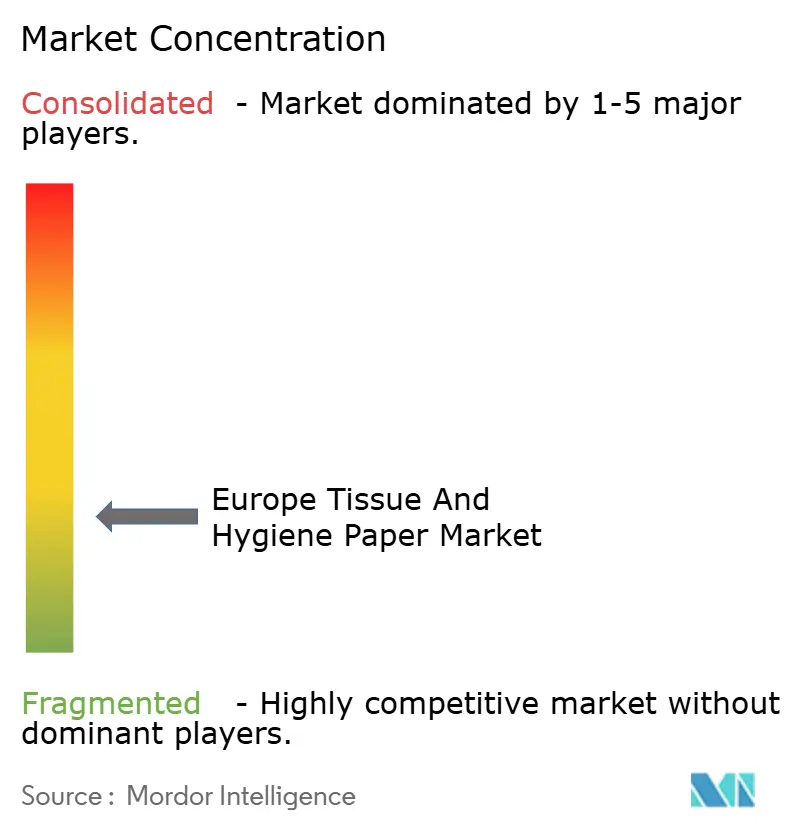

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Tissue And Hygiene Paper Market Analysis by Mordor Intelligence

The Europe Tissue And Hygiene Paper Market size is expected to grow from USD 54.44 billion in 2025 to USD 55.83 billion in 2026 and is forecast to reach USD 62.76 billion by 2031 at 5.32% CAGR over 2026-2031. Robust elderly-care spending, the structural switch to recycled fiber under European Union sustainability mandates, and the gradual rebound of hospitality demand form the core expansion pillars. Producers are accelerating vertical integration into waste-paper collection to lock in fiber security, while premium incontinence formats are widening unit margins despite raw-material volatility. At the same time, pulp and electricity price swings, private-label shelf gains, and looming Phase IV carbon-price escalations are squeezing operating spreads and forcing aggressive cost-to-serve optimization. The interplay of these drivers and restraints defines a competitive field where scale, sustainability readiness, and channel agility increasingly determine winners.

Key Report Takeaways

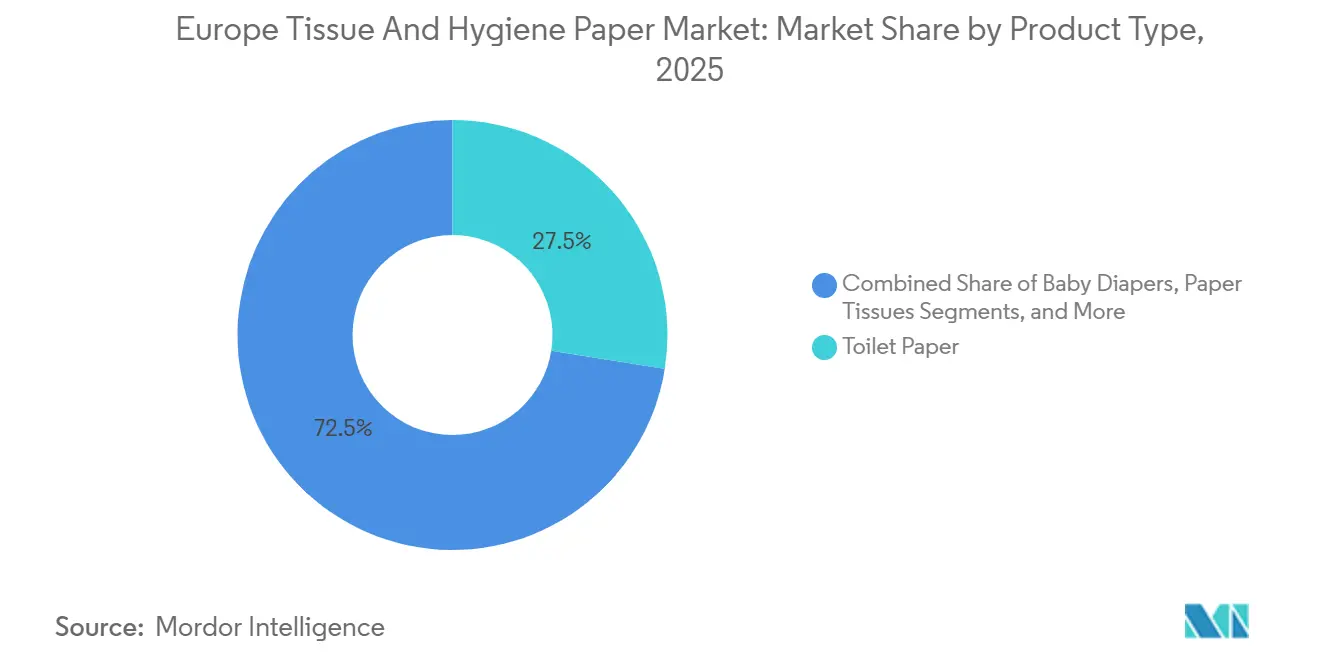

- By product type, toilet paper held 27.50% of Europe tissue and hygiene paper market share in 2025, while incontinence products are projected to grow at 7.80% CAGR through 2031.

- By raw material, recycled fiber commanded 46.80% share of Europe tissue and hygiene paper market size in 2025 and is expected to expand at 5.40% CAGR to 2031.

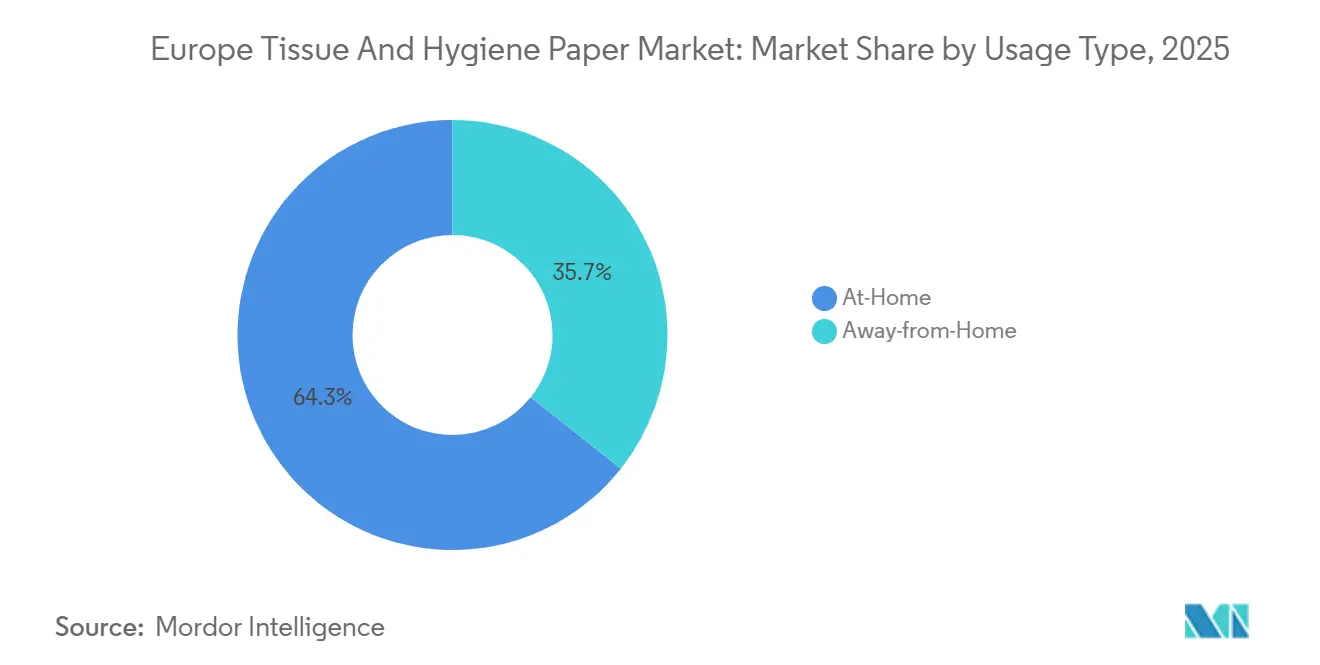

- By usage type, at-home consumption accounted for 64.32% of Europe tissue and hygiene paper market size in 2025, whereas away-from-home demand is rising at 5.90% CAGR to 2031.

- By end-use industry, residential households commanded 58.20% share of Europe tissue and hygiene paper market size in 2025, whereas Healthcare and Aged-Care Facilities demand is rising at 6.5% CAGR to 2031.

- By Country, Germany led with 24.78% revenue share in 2025, and Poland is forecast to record the fastest 6.90% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Tissue And Hygiene Paper Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging Population Boosting Adult-Incontinence Demand | +1.2% | Germany, Italy, Spain, France, Nordic countries | Long term (≥ 4 years) |

| Heightened Hygiene Awareness | +0.8% | Western Europe urban centers | Medium term (2-4 years) |

| EU Deforestation Rules Accelerating Recycled Tissue Uptake | +0.7% | European Union-wide | Long term (≥ 4 years) |

| Surge in E-Commerce and D2C Retail Channels | +0.6% | United Kingdom, Germany, France, Netherlands, Poland, Spain | Medium term (2-4 years) |

| Tourism Rebound Elevating AFH Tissue Demand | +0.5% | Spain, Italy, France, Greece, Portugal, Croatia | Short term (≤ 2 years) |

| Rapid Adoption of Digital Watermarks to Improve Paper Recycling | +0.4% | Germany, Netherlands, France, Belgium, United Kingdom | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aging Population Boosting Adult-Incontinence Demand

Europe’s demographic shift is translating directly into higher consumption of absorbent hygiene products for adults. The European Association of Urology estimated that 55–60 million residents lived with incontinence in 2023, costing EUR 69.1 billion (USD 77.9 billion) with a forecast jump to EUR 87 billion (USD 98.1 billion) by 2030.[1]European Association of Urology, “Economic Burden of Urinary Incontinence in Europe,” uroweb.org German and Italian long-term-care facilities are upgrading to premium briefs that promise longer wear intervals, a change that cuts nursing labor and lifts average selling prices. Multinationals have responded by dedicating new converting lines to high-absorbency SKUs and bundling product-plus-service contracts with healthcare procurement agencies. The resulting 7.80% CAGR for incontinence products materially outpaces the broader Europe tissue and hygiene paper market.

Heightened Hygiene Awareness

Post-pandemic behaviors have locked in structurally higher tissue usage per capita. European consumption stabilized at 14.3 kilograms in 2024, helped by sustained preference for single-use towels in foodservice and clinical environments. Compliance with ISO 22000 and ISO 13485 has moved from voluntary to baseline procurement criteria, especially in hospitals that replaced cotton cloths with disposable alternatives. Urban households continue to stockpile facial tissues and paper towels as remote-work norms persist. Collectively, these factors lift unit demand in both retail and professional hygiene segments, supporting a +0.8% contribution to forecast CAGR.

EU Deforestation Rules Accelerating Recycled Tissue Uptake

The European Union Deforestation Regulation, effective December 2024, obliges operators to submit granular due-diligence statements for wood-based inputs, steering mills toward recovered fiber to cut compliance friction.[2]European Commission, “EU Deforestation Regulation Implementation Timeline,” environment.ec.europa.eu Large producers that locked in recycled feedstock ahead of the December 2025 deadline have carved short-term cost advantages, while small and medium plants face a June 2026 cutoff. Recycled fiber already holds 46.80% share and is advancing at 5.40% CAGR, aided by investments in de-inking and quality-control technology. The rule also spurs mill ownership stakes in waste-paper collection to guarantee chain-of-custody integrity.

Surge in E-Commerce and D2C Retail Channels

Digital retail penetration for fast-moving consumer goods crossed double-digit thresholds in the United Kingdom, Germany, and the Netherlands by 2025. Brands now push subscription packs of toilet paper and diapers that trim fulfillment costs and enhance consumer loyalty, a model that lifted Procter and Gamble’s Baby, Feminine and Family Care organic sales by 3% in fiscal Q1 2025. Smaller challengers exploit social-commerce algorithms and recyclable shipping formats to sidestep shelf-space battles, supporting a +0.6% CAGR tailwind for the Europe tissue and hygiene paper market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Pulp and Energy Prices Squeezing Margins | -1.0% | European Union-wide, high exposure in Germany, Poland, Italy | Short term (≤ 2 years) |

| Decarbonization CAPEX Pressure under EU-ETS Phase IV | -0.8% | Finland, Sweden, Germany, France | Long term (≥ 4 years) |

| Environmental and PFAS Concerns over Disposables | -0.6% | Nordic countries, Germany, Netherlands, Belgium, France | Medium term (2-4 years) |

| Private-Label Price Wars in Mature Retail | -0.5% | United Kingdom, Germany, France, Spain | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Pulp and Energy Prices Squeezing Margins

Wholesale electricity in Europe peaked near EUR 400 per MWh in August 2022 before easing to 70–120 EUR per MWh in early 2023, while northern bleached softwood kraft pulp mirrored that turbulence. AFRY Consulting calculated that tissue production costs jumped 43% for virgin grades during 2020-2021. Although hedging contracts and cogeneration projects soften shocks, the lag in retail price passthrough compresses EBITDA and deters discretionary capital spend, subtracting a full percentage-point from forecast CAGR.

Decarbonization CAPEX Pressure under EU-ETS Phase IV

Carbon allowances averaged EUR 63.85 per tonne in December 2023 and could touch EUR 90-100 per tonne by 2030. Tissue mills, which rely on steam drying and large thermal loads, must invest in biomass boilers, heat-recovery systems, and renewable electricity procurement.[3]CEPI, “Pulp and Paper Industry Resilience in 2023,” cepi.org Essity’s SEK 3.3 billion (USD 316 million) program illustrates the magnitude of mandatory spend. Although these projects cut long-run emissions charges, their near-term cash drain curtails growth and trims CAGR by 0.8% over the outlook horizon.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Incontinence Products Accelerate Amid Aging Demographics

In 2025, toilet paper generated the highest revenue, yet incontinence products exhibit the steepest trajectory at 7.80% CAGR through 2031. Europe tissue and hygiene paper market size for incontinence products is projected to rise sharply as care homes adopt premium, high-absorbency designs. The demographic shift places sustained pressure on supply chains for superabsorbent polymers and breathable films.

Manufacturers now bundle sensor-enabled briefs and digital ordering portals to deepen procurement contracts with healthcare institutions. Conversely, baby diapers weaken due to falling fertility in Western Europe, prompting SKU premiumization to protect value. Tissue converters on the continent thus manage a two-speed portfolio, defending commoditized toilet paper volumes while chasing margin in adult-care lines.

By Raw Material: Recycled Fiber Gains Ground on Regulatory Tailwinds

Recycled fiber accounted for 46.80% of Europe tissue and hygiene paper market share in 2025, and its share is widening on the back of EU forest-risk commodity rules. Europe tissue and hygiene paper market size linked to recycled fiber is set for 5.40% CAGR, overshadowing kraft and sulfite pulp grades.

Quality improvements emerge from better sorting: the HolyGrail 2.0 digital watermark pilots in Germany and the Netherlands demonstrated near-infrared detection accuracy above 95%. Nordic mills still deploy virgin fiber for strength-critical formats, yet even these producers integrate de-inked pulp into mid-tier SKUs to lower carbon intensity and reduce ETS liabilities.

By Usage Type: Away-From-Home Segment Outperforms

At-home channels captured 64.32% of Europe tissue and hygiene paper market size in 2025 thanks to pandemic-era stocking, but away-from-home demand recovers at 5.90% CAGR as tourism and office occupancy rebound. Hotels in Spain and Italy shifted from linen to disposable napkins to accelerate table turns, expanding jumbo-roll sales to distributors.

Hospitals tightened infection-control norms, prompting a switch to single-use towels under ISO 13485 frameworks. Producers respond with high-capacity dispensers and dispenser-as-a-service models that cut refilling labor, thereby boosting stickiness with facility managers.

By End-Use Industry: Healthcare and Aged-Care Facilities Lead Value Growth

Residential households still represent 58.20% of Europe tissue and hygiene paper market size in 2025, but their growth plateaus as penetration saturates in Western Europe. Healthcare and aged-care sites climb at 6.50% CAGR through 2031, absorbing premium wipes and underpads aligned with reimbursement schemes.

Hospital procurement increasingly specifies traceable, PFAS-free substrates to future-proof against regulatory action, creating product differentiation levers for compliant suppliers. Hospitality and foodservice follow closely, underpinned by international tourist arrivals surpassing 200 million in 2024, which translated into higher napkin and towel turnover in hotels and quick-service restaurants.

Geography Analysis

Germany remains the anchor of the Europe tissue and hygiene paper market, contributing 24.78% of revenue in 2025 and benefiting from 1.5 million tonnes of annual tissue capacity. Its mature retail mix balances branded loyalty and aggressive private-label pricing, while its recovered-paper infrastructure underpins recycled-fiber growth.

Poland is the fastest-expanding geography at 6.90% CAGR, driven by rising disposable incomes, retail modern-trade penetration, and fresh capacity investments such as Sofidel’s recent 60,000-tonne mill extension. The country’s central location within the customs union enables efficient distribution to both Western and Eastern customers.

Southern Europe gains momentum from tourism. Spain, Italy, and France together absorb significant away-from-home volumes as hotels update hygiene protocols. Nordic nations post the highest per-capita usage thanks to cultural cleanliness norms and premium positioning of eco-certified products. Eastern European markets beyond Poland, including the Czech Republic and Romania, represent medium-term upside once logistics and waste-paper collection networks mature.

Competitive Landscape

The field shows moderate concentration as global majors such as Essity, Kimberly-Clark, and Procter and Gamble compete with regional specialists such as Sofidel and WEPA. Essity delivered SEK 38.5 billion (USD 3.7 billion) in Q3 2024 sales, assisted by 5.8% organic growth in Professional Hygiene. Private-label penetration remains an existential challenge in mature markets like the United Kingdom, where branded toilet-tissue volume fell by 9.4 million packs in 2024.

Sustainability investments differentiate front-runners: Essity and Metsä Group have announced fossil-free roadmaps, while producers join HolyGrail 2.0 to standardize digital watermarks. Technology adoption extends to mill automation and predictive maintenance, enabling tighter fiber-blend control. Niche disruptors leverage direct-to-consumer models for organic baby diapers and biodegradable feminine products, bypassing retailer margin demands.

Collaborative projects emerge as strategic hedges. Producers co-finance shared recovered-paper depots and renewable-energy clusters near mills to pool risk. Compliance with ISO 22000 and ISO 13485 increasingly appears in tenders, pushing mills to certify quality systems as a competitive prerequisite.

Europe Tissue And Hygiene Paper Industry Leaders

Sofidel Group

Kimberly Clark Corporation

Metsa Group

Industrie Cartarie Tronchetti SpA

Lucart SpA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Essity announced a SEK 3.3 billion (USD 316 million) cost-savings and fossil-free production program targeting a 35% emission cut by 2030.

- December 2024: European Union Deforestation Regulation entered into force, initiating staggered compliance deadlines for pulp and paper operators.

- November 2024: Sofidel completed a EUR 50 million (USD 53.5 million) line addition in Poland, boosting annual output by 60,000 tonnes.

- October 2024: Kimberly-Clark launched premium adult incontinence products in Germany and France featuring wetness indicators.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study regards the European tissue & hygiene paper market as the yearly value generated by toilet paper, household towels, paper tissues, baby diapers, feminine hygiene, and adult-incontinence products that are sold in retail or institutional channels within 32 European nations, from the Nordics to the Balkans, and manufactured from virgin kraft or sulfite pulp as well as recycled fiber.

Scope exclusion: industrial sack, specialty filter, and printing grades remain outside this definition.

Segmentation Overview

- By Product Type

- Baby Diapers

- Feminine Hygiene

- Household Paper

- Incontinence Products

- Paper Tissues

- Paper Napkins

- Paper Towels

- Facial Tissues

- Specialty and Wrapping Tissues

- Toilet Paper

- By Raw Material

- Kraft Pulp

- Sulfite Pulp

- Recycled Fiber

- Other Raw Materials

- By Usage Type

- At-Home

- Away-from-Home

- By End-Use Industry

- Residential Households

- Hospitality and Foodservice

- Healthcare and Aged-Care Facilities

- Other End-Use Industry

- By Country

- United Kingdom

- Germany

- France

- Italy

- Spain

- Netherlands

- Denmark

- Sweden

- Russia

- Poland

- Rest of Europe

Detailed Research Methodology and Data Validation

Primary Research

Multiple guided discussions with European tissue mills, AFH distributors, private-label buyers, pharmacy chains, and aged-care facility procurement leads helped us verify price corridors, recycled-fiber adoption, and demand seasonality. They sharpened our understanding of country-level regulatory impacts on SKU mix.

Desk Research

We compiled macro and trade indicators from open-access authorities such as Eurostat for household spend, the European Tissue Symposium for per-capita consumption, CEPI customs flows for pulp and parent-roll trade, and tourism-night data from Eurostat to size the away-from-home pool. Company 10-Ks, investor decks, and reputable press briefings supplemented channel shifts, while paid platforms, D&B Hoovers for converter revenues and Dow Jones Factiva for deal tracking, filled ownership and pricing gaps. This list is illustrative, not exhaustive, and many additional sources informed our desk work.

Market-Sizing & Forecasting

A top-down reconstruction begins with Eurostat production plus net trade to derive available supply, which is then split by application using ETS consumption ratios. Selective bottom-up checks, sampled mill output, converter capacity, and average selling price (ASP) audits align totals. Key variables include 65+ population growth, hotel-bed-night recovery, private-label share, pulp price index, recycled-fiber penetration, and hygiene-spend elasticity. We project each driver with ARIMA methods, validate coefficient direction through expert interviews, and run scenario analysis before locking the base case. Short bottom-up gaps are bridged by interpolating ASP from audited retail scanner averages.

Data Validation & Update Cycle

Mordor analysts cross-check modeled outputs against independent signals, ETS tonnage, listed-player sales, and airline arrivals. Variances above predefined bands trigger rework and senior review. Reports refresh annually, and any material event, mill closure, regulatory step-up, or >10% pulp-price swing prompts an interim update before client delivery.

Why Mordor's Europe Tissue and Hygiene Paper Baseline Earns Decision-Maker Confidence

Published estimates often diverge because firms pick different product baskets, raw-material assumptions, and refresh cadences.

Key gap drivers include: some publishers exclude away-from-home towels, others fold baby diapers into broader disposable-hygiene studies, many apply static ASPs, and several keep 2023 as the base year, whereas Mordor rolls 2025 data and updates currency conversions quarterly.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 54.36 B (2025) | Mordor Intelligence | - |

| USD 51.49 B (2024) | Global Consultancy A | Older base year, limited raw-material split, single-source ASP |

| USD 55.50 B (2024) | Industry Research B | Includes disposable baby-care only in selected nations, no AFH coverage |

| USD 22.40 B (2023) | Regional Consultancy C | Excludes diapers & incontinence, relies on shipment values, conservative scope |

Side-by-side, clients see that Mordor's figures stem from clearly declared scope, fresher inputs, and dual-path validation, giving planners a balanced, reproducible baseline for capex or channel strategy discussions.

Key Questions Answered in the Report

What is the forecast growth rate for the Europe tissue and hygiene paper market through 2031?

The market is expected to record a 5.32% CAGR, rising from USD 55.83 billion in 2026 to USD 62.76 billion in 2031.

Which product category is growing fastest in Europe’s tissue sector?

Incontinence products lead with a projected 7.80% CAGR, driven by an aging population and healthcare procurement upgrades.

How large is recycled fiber’s role in European tissue production?

Recycled fiber already accounts for 46.80% of output value and is set to expand at 5.40% CAGR under EU deforestation rules.

Which country is the quickest-growing market for tissue in Europe?

Poland is forecast to expand at 6.90% CAGR thanks to retail modernization, rising incomes, and new mill investments.

Page last updated on: