Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

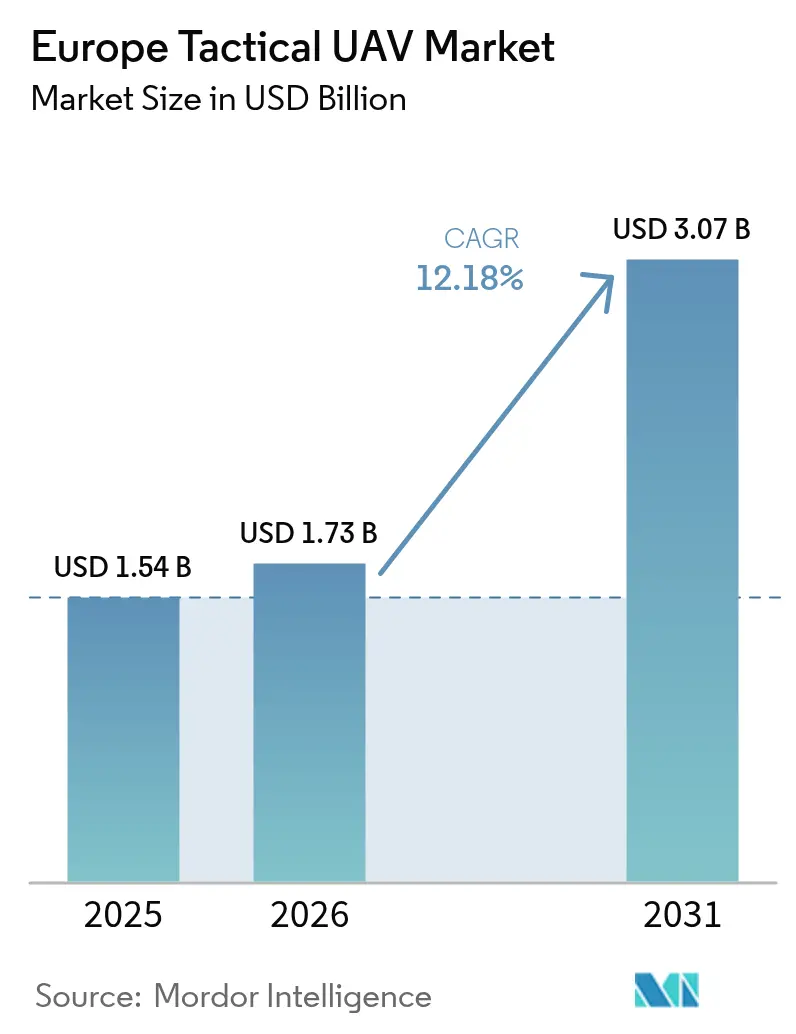

| Base Year Market Size (2025) | USD 1.54 Billion |

| Market Size (2026) | USD 1.73 Billion |

| Market Size (2031) | USD 3.07 Billion |

| Growth Rate (2026 - 2031) | 12.18% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Tactical UAV Market Analysis by Mordor Intelligence

The Europe tactical UAV market size is expected to grow from USD 1.54 billion in 2025 to USD 1.73 billion in 2026 and is forecast to reach USD 3.07 billion by 2031 at 12.18% CAGR over 2026-2031. Rapid spending increases on unmanned intelligence, surveillance, and reconnaissance assets by prominent NATO members, joint Eurodrone and PESCO investments, and momentum behind AI-enabled swarm experimentation together anchor growth. The Russia-Ukraine war revealed urgent gaps in small-drone resilience, prompting emergency re-equipping programs and multiyear procurement pipelines that stabilize demand. Parallel civil-security use cases, from wildfire mapping to border policing, are broadening the customer base. At the same time, unified U-space rules lower operational barriers for cross-border beyond-visual-line-of-sight flights. Competition features legacy aerospace primes defending entrenched positions as nimble specialists introduce lighter, hybrid-propulsion airframes and advanced autonomy stacks.

Key Report Takeaways

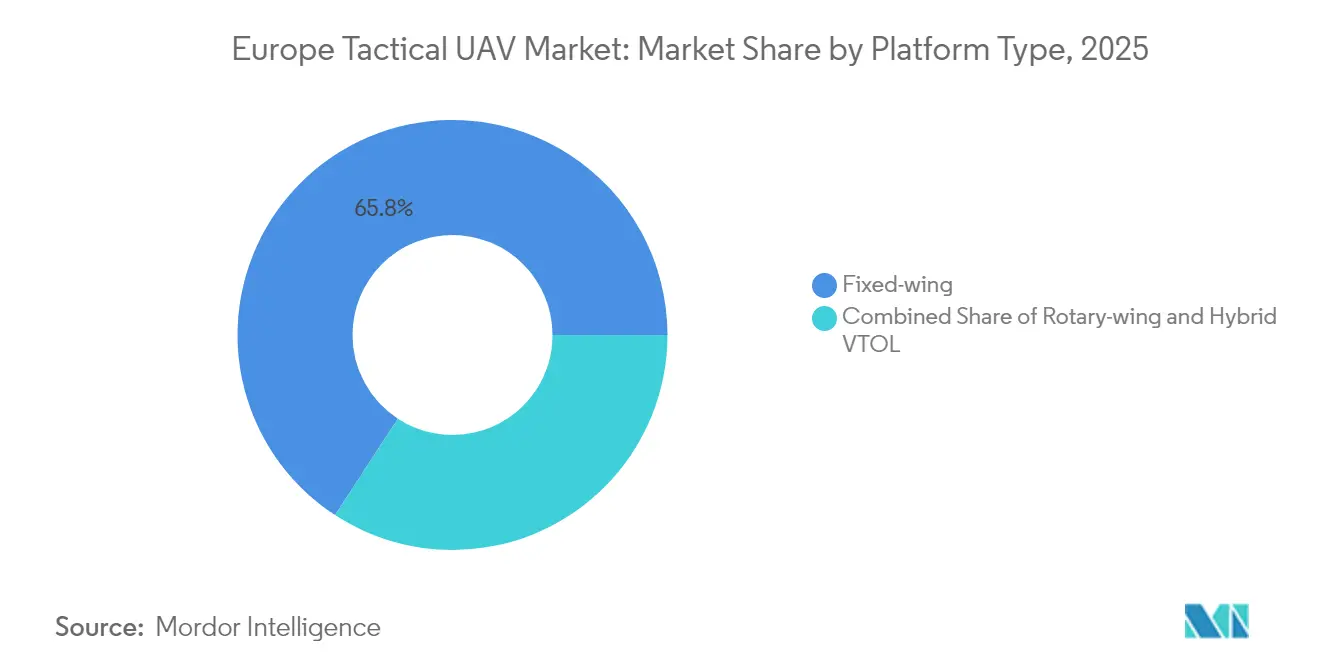

- By platform type, fixed-wing systems held 65.80% of Europe's tactical UAV market share in 2025; hybrid VTOL platforms are poised to expand at a 15.88% CAGR through 2031.

- By weight class, 20-150 kg light tactical units commanded 45.90% revenue in 2025, whereas sub-5 kg micro/nano craft are on track for an 18.12% CAGR to 2031.

- By range, 50-200 km medium-range models captured 54.10% share in 2025, while >200 km extended-range variants should climb at a 15.44% CAGR on the back of U-space harmonization.

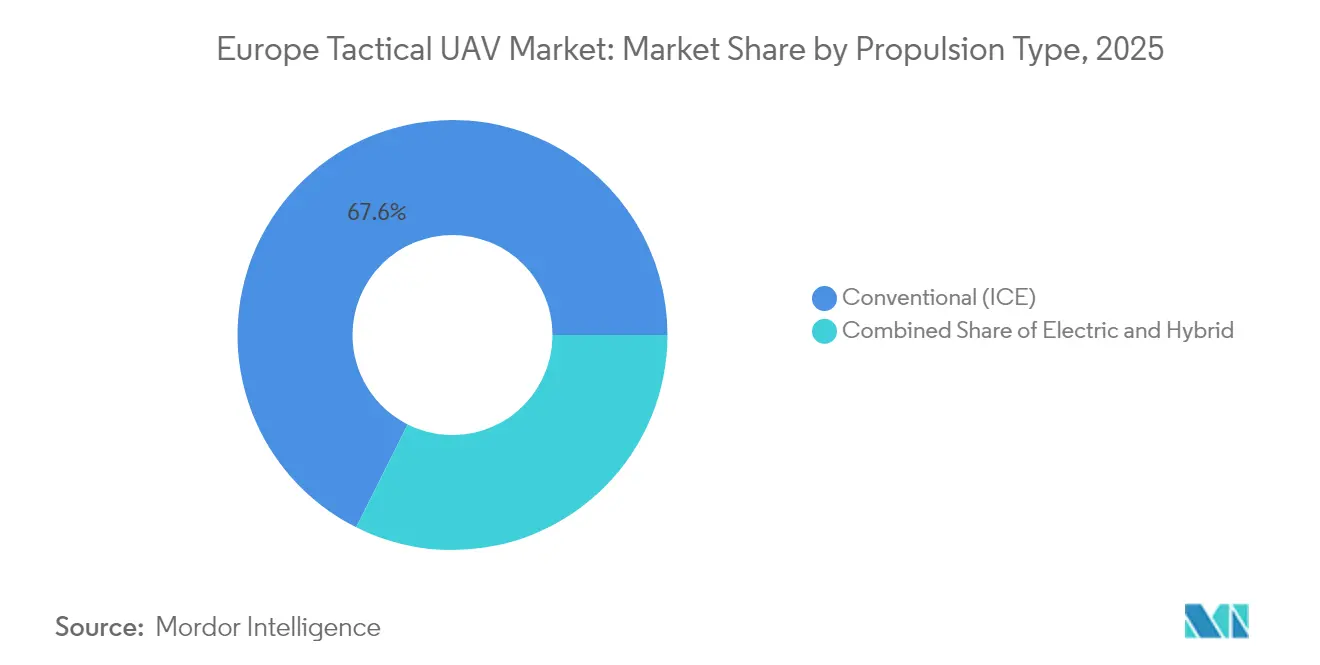

- By propulsion, conventional internal-combustion designs accounted for 67.60% of 2025 revenue; hybrid powertrains are expected to accelerate at a 17.63% CAGR, thanks to lower acoustic signatures and stricter emissions rules.

- By application, defense retained a 69.75% revenue lead in 2025, yet disaster-response deployments are charting an 18.01% CAGR as civil-protection agencies integrate drones into incident command workflows.

- By country, the United Kingdom led with 22.05% 2025 share, whereas Spain is forecast to log a 14.15% CAGR to 2031 under its indigenous-capability drive.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Tactical UAV Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising ISR-centric outlays | +2.8% | UK, France, Germany | Medium term (2-4 years) |

| Ukraine-driven urgency | +3.2% | Eastern and Western Europe | Short term (≤2 years) |

| Eurodrone and PESCO localization | +1.9% | Germany, France, Italy, Spain | Long term (≥4 years) |

| Cross-border U-space rules | +1.4% | EU-wide | Medium term (2-4 years) |

| NATO swarm experimentation | +1.1% | Alliance members | Long term (≥4 years) |

| Loitering-munition integration | +2.1% | Eastern frontline states | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Rising Defense-Budget Allocations Drive ISR-Centric Procurement

Defense ministries boosted 2024 tactical-drone budgets at the fastest clip in two decades, led by Germany’s 8.2% hike to EUR 52.1 billion (USD 55.7 billion) and France’s 7.4% lift to EUR 47.2 billion (USD 50.5 billion).[1]German Federal Ministry of Defence, “Defence Budget 2024,” BMVG.DE The UK locked in GBP 3.8 billion (USD 4.7 billion) for unmanned platforms through 2034, a 45% jump on the previous plan.[2]UK Ministry of Defence, “Defence Equipment Plan 2024-2034,” GOV.UK Poland doubled its tactical-drone line to USD 890 million, underscoring frontline urgency. Funding streams are increasingly referencing multi-domain operations that integrate real-time data from air, land, and cyber assets. This budget momentum secures multi-year order visibility for the European tactical UAV market.

Urgent Tactical-Drone Demand Sparked by Ukraine Conflict

Combat footage from Ukraine showcased the versatility of small drones for reconnaissance, artillery cueing, and precision strikes, prompting NATO states to re-baseline their requirements.[3]NATO Allied Command Transformation, “Ukraine Lessons Learned for Tactical UAV Operations,” ACT.NATO.INT Germany rushed a EUR 340 million (USD 364 million) buy of 1,200 systems, while France fast-tracked 800 units to close battlefield gaps. Planners now specify GPS-denied navigation, hardening against electronic warfare, and autonomous swarm maneuvers. These criteria reshape supplier road maps and lift the European tactical UAV market trajectory.

EU-Funded Eurodrone and PESCO Projects Accelerate Local Supply Chains

The EUR 7.1 billion (USD 7.6 billion) Eurodrone program achieved its first flight-ready airframe in 2024, marking a significant milestone for Europe’s largest collaborative UAV project. Parallel PESCO allocations of EUR 2.3 billion (USD 2.5 billion), spread across 14 states, underwrite component localization and interoperability testing.[4]European Defence Agency, “PESCO European UAV Programme Funding Allocation,” EDA.EUROPA.EU Italy’s Leonardo opened twin production lines, creating 1,400 jobs and securing EUR 890 million (USD 952 million) in support grants. These efforts curb reliance on non-European suppliers and channel fresh demand into domestic factories, deepening the European tactical UAV market base.

Cross-Border U-Space Regulations Enable BVLOS Operations

In January 2024, the EASA’s U-space framework came into effect, standardizing deconfliction, e-identification, and air traffic integration for drones operating beyond visual line of sight. The Netherlands established multinational corridors with Germany and Belgium, enabling real-time autonomous flights during joint exercises. France and Spain implemented similar corridors over the Pyrenees. These harmonized regulations remove legacy airspace barriers and create new revenue opportunities for extended-range solutions in the European tactical UAV market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented industrial base | -1.8% | EU-wide | Medium term (2-4 years) |

| Restrictive export licences | -2.1% | Intra-Europe trade | Long term (≥4 years) |

| EW/Cyber vulnerability | -1.4% | Eastern frontline | Short term (≤2 years) |

| Lethal-autonomy public scrutiny | -0.9% | Germany, Netherlands | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Fragmented Industrial Base Hampers Joint Procurement Efficiency

Twenty-seven national defense bureaucracies still run more than 30 separate tactical-drone tenders, diluting economies of scale and prolonging unit fielding by an average of 18 months. Germany's preference for local primes clashes with France's 'buy European' clauses, forcing duplicate R&D lines. Without deeper integration, the European tactical UAV market faces a cost drag and interoperability friction that favors non-European imports.

Export-Licence Regimes Constrain Cross-Border Sales Growth

Germany's dual-use controls caused a 14-month delay in shipments to Poland and the Czech Republic in 2024, significantly impacting supply chain timelines. France introduced individual component licenses, which increased delivery costs by up to 20%, adding financial strain to manufacturers and suppliers. Post-Brexit regulations in the UK imposed additional paperwork requirements for EU vendors, further complicating cross-border transactions. These challenges have disrupted the order flow within the European tactical UAV market, creating operational inefficiencies and posing significant hurdles for smaller innovators who lack the resources or dedicated compliance teams to navigate these regulatory complexities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform Type: Fixed-Wing Staying Dominant as VTOL Gains Ground

Fixed-wing aircraft generated 65.80% of Europe tactical UAV market revenue in 2025, buoyed by 18-hour endurance, 75 kg payload capacity, and lower lifecycle cost compared with rotary peers. The Europe tactical UAV market size for fixed-wing will still expand, albeit at single-digit CAGR as most Tier-1 forces already operate mature fleets. Hybrid VTOL models, however, are logging the segment’s headline 15.88% CAGR because commanders increasingly demand runway-independent launch paired with 300 km range capability. Programs in Germany, Sweden, and the UK validate the concept, pushing vendors to refine tilt-wing and vectored-thrust designs.

Continuous miniaturization of electric motors and lightweight composite wings is shrinking logistics footprints, letting brigades air-lift pre-assembled VTOL drones directly to forward bases. Software-defined flight controllers further blur lines between platform categories, enabling quick re-role from ISR to electronic-attack or loitering-munition carriage. Collectively these traits will let VTOL contenders erode fixed-wing share slowly but steadily through 2031 as training curricula pivot to vertical launch-and-recover proficiency.

By Weight Class: Light Tactical Leads, Micro/Nano Skyrocket

The 20-150 kg light segment accounted for 45.90% of Europe tactical UAV market size in 2025, sitting at the operational sweet spot between squad portability and sensor heft. Customers value its ability to haul multi-spectral gimbals, synthetic-aperture radar, or SIGINT pods without complex ground infrastructure. The micro/nano tier, though only 7.12% of revenue today, is outpacing all others at 18.12% CAGR as chipsets, micro-gimbals, and secure mesh radios shrink below 1 kg thresholds.

Urban counter-terror units favor palm-launched craft that stream 4K video through walls over 3 km, while artillery battalions adopt expendable micro-drones to verify strike results. To defend share, light-segment suppliers are adding modular plug-and-play bays so that a single airframe can toggle between ISR, electronic-warfare, or precision-strike payloads within minutes. Overall, technology spillovers ensure both tiers remain essential within the Europe tactical UAV market.

By Range Category: Medium-Range Still Core, Extended-Range Accelerates

Platforms able to cover 50-200 km delivered 54.10% of Europe tactical UAV market revenue in 2025 thanks to seamless fit with European border widths and maritime EEZ patrols. New U-space corridors are nevertheless propelling >200 km airframes toward a 15.44% CAGR, especially for Mediterranean migration monitoring, North Sea energy-site security, and Arctic domain awareness missions. Operators require datalink latency under 250 ms and 256-bit encrypted satcom fallback to achieve persistent coverage.

As doctrine shifts toward longer-reach standoff ISR, suppliers integrate high-bandwidth Ka-band terminals and wing-mounted fuel bladders that stretch endurance past 24 hours. Conversely, <50 km short-range drones retain tactical relevance for battalion-level maneuver and first-responder use, insulated from longer-range competition by distinct payload, cost, and training profiles.

By Propulsion Type: Combustion Engines Lead While Hybrid Power Scales

Conventional two-stroke and rotary engines powered 67.60% of the 2025 Europe tactical UAV market, favored for instant refuel turnaround and high power-to-weight on multi-sensor missions. Yet hybrid electric-thermal architectures are gaining 17.63% CAGR, balancing silent ingress and reduced infrared signature with cruise endurance. Germany’s procurement of hybrid reconnaissance units underscores the shift.

Manufacturers embed swappable battery trays and range-extender gensets, enabling commanders to toggle between zero-emission loiter and long-haul ferry legs without depot conversion. Carbon-emissions ceilings on EU defense estates add policy tailwinds, and falling battery prices make hybrid total-cost-of-ownership compelling for civil-security buyers.

By Application: Defense Dominates as Civil Protection Ramps Up

Military customers delivered 69.75% of 2025 revenue, anchoring the Europe tactical UAV market share through brigade-level modernization budgets and multi-year frameworks. However, wildfire surveillance, search-and-rescue, and flood mapping are propelling the disaster-response slice at 18.01% CAGR. Italy’s Civil Protection Department cut incident response times by 35% after fielding 340 drones last summer.

Law enforcement procurement lines are likewise pivoting toward persistent border and maritime situational awareness, often co-financed under EU internal-security funds. Such dual-use diversification stabilizes overall demand and buffers suppliers against cyclical defense budget swings.

Geography Analysis

Western Europe captured the lion’s share of 2025 revenue as the United Kingdom, France, and Germany combined for more than half of the Europe tactical UAV market size. London’s GBP 3.8 billion (USD 4.7 billion) unmanned-systems roadmap guarantees a steady domestic backlog, while Paris and Berlin run concurrent national and Eurodrone programs that blend sovereign and collaborative fleets. Deep industrial capacity, long-standing export channels, and active NATO deployments reinforce regional dominance.

Southern Europe is the fastest-growing bloc; Spain’s 14.15% CAGR trajectory is driven by Seville- and Madrid-based final-assembly lines that absorb Eurodrone work shares and indigenous development. Italy leverages Mediterranean border-security imperatives to spur Leonardo deliveries across defense and coast-guard accounts, while Greece and Portugal tap EU cohesion funds for ISR coastal coverage.

Northern and Eastern Europe together shape the market’s strategic urgency. Finland, Sweden, and Norway prioritize Arctic-weatherized drones to surveil expanded NATO frontiers. Poland’s USD 890 million budget and the Baltic trio’s pooled tenders channel orders to rugged, EW-resilient models. EU Eastern-Partnership financing also seeds capability growth in Ukraine, Moldova, and Georgia, creating future export footholds for EU manufacturers once reconstruction accelerates

Competitive Landscape

European Tactical UAV Market Vendor Market Share Analysis

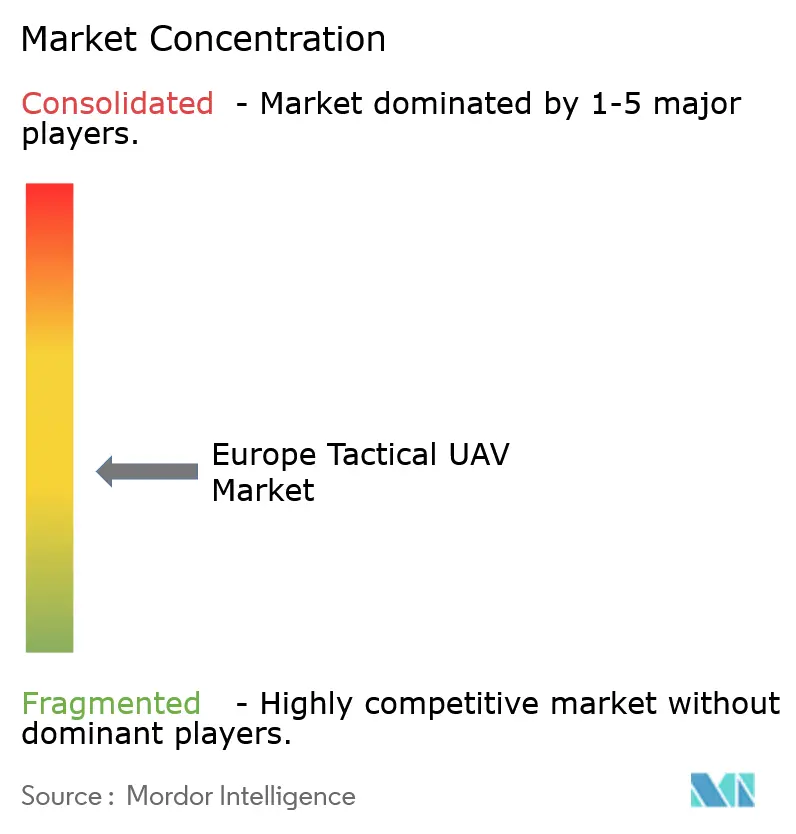

The European tactical UAV market is currently moderately concentrated, with the top five suppliers accounting for the majority of 2024 revenue, while emerging specialists rapidly nibble at niche segments. Airbus Defence and Space, Leonardo, Thales, BAE Systems, and Saab maintain their lead through multi-decade defense relationships, certified quality systems, and extensive service networks. Airbus won a record EUR 890 million (USD 952.3 million) , 240-unit German order in January 2025, underscoring its scale advantage.

Disruptors such as Quantum-Systems, Helsing, and Israel-origin firms with European plants focus on hybrid VTOL designs, mesh-networked swarms, and AI-powered edge analytics. Quantum-Systems’ EUR 67 million (USD 71.1 million) funding round bankrolls new German and French lines to meet swelling demand for its Vector VTOL. Strategic alliances multiply: Thales and Helsing formed a JV to integrate real-time autonomy modules, while Leonardo acquired UK lightweight-drone maker Tekever to capture home-market orders.

Sustained differentiation will hinge on electronic-warfare robustness, propulsion versatility, and secure cloud-native mission-planning suites. Vendors that deliver open-architecture APIs and NATO-accredited cyber hardening stand to grow share as doctrine increasingly mandates multi-domain, multi-vendor plug-and-play interoperability.

Europe Tactical UAV Industry Leaders

-

Leonardo S.p.A.

-

Airbus SE

-

BAYKAR MAKİNA SANAYİ VE TİCARET A.Ş.

-

Elbit Systems Ltd.

-

Thales Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Germany is set to award contracts valued at up to EUR 900 million (USD 950 million) for kamikaze drones to two defense start-ups and an established contractor, despite one company's systems experiencing significant failures during recent military trials.

- October 2025: Germany intends to invest EUR 10 billion (USD 10.8 billion) over the coming years to substantially expand its military drone fleet.

- October 2025: The United Kingdom will retain its Watchkeeper WK450 drones in service until at least March 2027, extending their operational timeline by two years beyond the original plan. This decision aligns with the Ministry of Defence's (MoD) ongoing efforts to procure a new tactical unmanned aerial system under the Corvus program.

- March 2025: The Ministry of Defence (MoD) released an Invitation to Tender (ITT) to procure approximately ten batches of Tactical Multirotor ISR Unmanned Aerial Systems (UAS).

Europe Tactical UAV Market Report Scope

Tactical UAVs are mainly used for Intelligence gathering, surveillance, and reconnaissance. However, their mission set can include applications like target acquisition and designation, strike, chemical-bio detection, mine countermeasures, air missile defense, electronic warfare, and information warfare.

The European tactical UAV market is segmented based on application and geography. By application, the market is segmented into military, law enforcement, and other applications. Other applications include disaster management operations such as search and rescue (SAR) operations and firefighting. The report also offers the market size and forecasts for five countries across the region. For each segment, the market sizing and forecasts have been done based on value (USD) and volume (ton).

By Platform Type

| Fixed-wing |

| Rotary-wing |

| Hybrid VTOL |

By Weight Class

| Micro/Nano (Less than 5 kg) |

| Mini (5 to 20 kg) |

| Light Tactical (20 to 150 kg) |

| Medium Tactical (150 to 600 kg) |

| Heavy Tactical (Greater than 600 kg) |

By Range Category

| Short-Range (Less than 50 km) |

| Medium-Range (50 to 200 km) |

| Extended-Range (Greater than 200 km) |

By Propulsion Type

| Electric |

| Hybrid |

| Conventional (ICE) |

By Application

| Military |

| Law Enforcement |

| Disaster and Emergency Response |

| Environmental Monitoring |

| Other Applications |

By Country

| United Kingdom |

| France |

| Germany |

| Italy |

| Spain |

| Russia |

| Rest of Europe |

| By Platform Type | Fixed-wing |

| Rotary-wing | |

| Hybrid VTOL | |

| By Weight Class | Micro/Nano (Less than 5 kg) |

| Mini (5 to 20 kg) | |

| Light Tactical (20 to 150 kg) | |

| Medium Tactical (150 to 600 kg) | |

| Heavy Tactical (Greater than 600 kg) | |

| By Range Category | Short-Range (Less than 50 km) |

| Medium-Range (50 to 200 km) | |

| Extended-Range (Greater than 200 km) | |

| By Propulsion Type | Electric |

| Hybrid | |

| Conventional (ICE) | |

| By Application | Military |

| Law Enforcement | |

| Disaster and Emergency Response | |

| Environmental Monitoring | |

| Other Applications | |

| By Country | United Kingdom |

| France | |

| Germany | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe |

Key Questions Answered in the Report

How big will the Europe tactical UAV market be by 2031?

It is forecast to reach USD 3.07 billion, rising at a 12.18% CAGR over 2026-2031.

Which platform type leads current demand?

Fixed-wing drones command 65.80% 2025 revenue thanks to long endurance and high payload ceilings.

Which segment is growing the fastest?

Hybrid VTOL aircraft show the quickest growth, advancing at a 15.88% CAGR through 2031.

Why is Spain viewed as a high-growth hotspot?

Strategic government funding and local production partnerships give Spain a 14.15% CAGR outlook.

What technology trend shapes new procurements?

AI-enabled swarm autonomy is becoming a procurement priority after NATO experimentation success.

What limits cross-border drone sales inside the EU?

Divergent export-licensing regimes add 6-14 months to delivery cycles and raise costs by up to 20%.

Page last updated on: