Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.93 Billion |

| Market Size (2026) | USD 2.04 Billion |

| Market Size (2031) | USD 2.69 Billion |

| Growth Rate (2026 - 2031) | 5.68% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Soy Beverages Market Analysis by Mordor Intelligence

The Europe soy beverages market size is expected to grow from USD 1.93 billion in 2025 to USD 2.04 billion in 2026 and is forecast to reach USD 2.69 billion by 2031 at 5.68% CAGR over 2026-2031. This growth is buoyed by soy's unparalleled protein density of 2.0-3.4 g/100 ml, outpacing other plant-based milks, and heightened visibility in both mainstream supermarkets and niche vegan stores. Multinationals are streamlining their portfolios, responding to the EU Deforestation Regulation by sidelining Brazilian soy, and embracing aluminum-free aseptic packaging, all bolstering supply-chain resilience and sustainability. Yet, challenges loom: the rise of oat and almond alternatives, concerns over GMOs, and varying national labeling regulations pose hurdles. Promotions aligning prices in Germany, Spain, and Austria, coupled with initiatives like the Netherlands' 50-50 animal-to-vegetable protein policy, are expanding household adoption and raising standards for functional fortification.

Key Report Takeaways

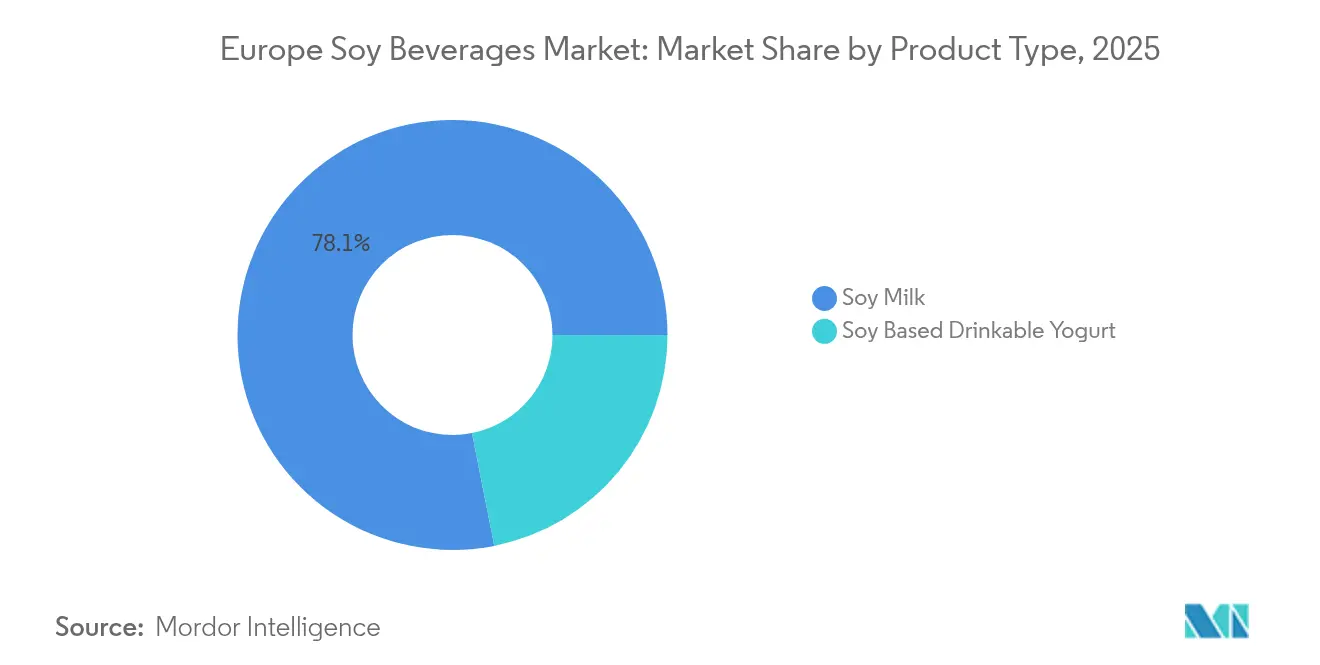

- By product type, soy milk led with 78.12% of the Europe soy beverages market share in 2025; soy-based drinkable yogurt is expanding at an 7.83% CAGR through 2031.

- By flavor, flavoured variants accounted for 61.02% share of the Europe soy beverages market in 2025, while un-flavoured options are forecast to grow at 7.55% CAGR to 2031.

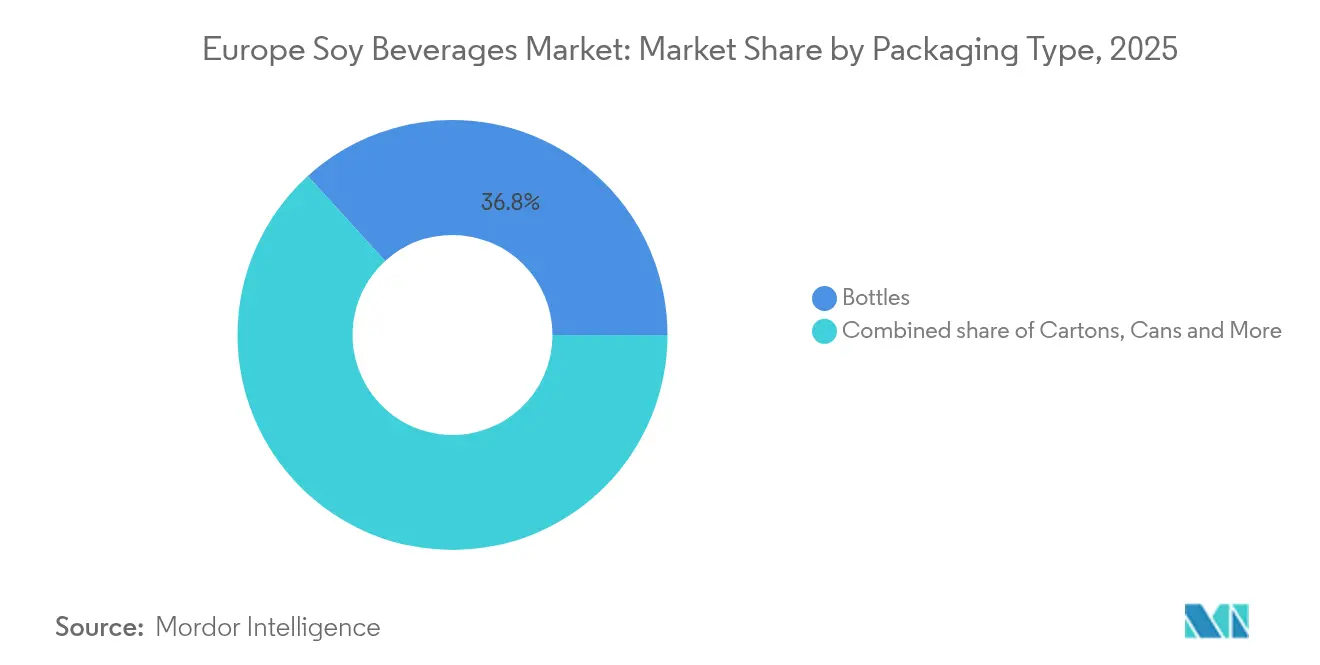

- By packaging type, bottles captured 36.75% share of the Europe soy beverages market in 2025, whereas cans are advancing at a 6.68% CAGR through 2031.

- By distribution channel, supermarkets and hypermarkets held 40.25% share of the Europe soy beverages market in 2025; pharmacies and drugstores record the highest projected CAGR at 6.74% during 2026-2031.

- By geography, Germany commanded 28.35% of the Europe soy beverages market in 2025, and Spain is projected to post the fastest growth at a 7.21% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Soy Beverages Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing consumer shift towards plant-based diets | +1.8% | Germany, Spain, UK, Netherlands; spillover to France and Italy | Medium term (2-4 years) |

| Rising popularity of fortified and functional beverages | +1.3% | Germany, UK, Netherlands; emerging in Spain and France | Short term (≤ 2 years) |

| Rising demand for natural and clean-label products | +1.1% | Germany, France, Netherlands; growing in UK and Spain | Medium term (2-4 years) |

| Expanding availability in retail outlets | +0.9% | Germany, Spain, UK; gradual penetration in Italy and Rest of Europe | Short term (≤ 2 years) |

| Innovation in flavors and formats | +0.7% | Spain, UK, Germany; niche adoption in France and Italy | Medium term (2-4 years) |

| Sustainability and environmental concerns | +0.6% | Netherlands, Germany, France; emerging in Spain and UK | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Consumer Shift Towards Plant-Based Diets

By 2023, 27% of European consumers identified as flexitarians, while 51% of meat-eaters actively reduced their meat consumption[1]CBI Ministry of Foreign Affairs Netherlands, "Plant-Based Market Trends." cbi.eu. This shift is not just driven by ethical reasons. For instance, plant-based milk has become a household staple, with over 40% of households in Spain and more than 33% in Germany and the UK purchasing it, reflecting its move into the mainstream. The Netherlands has set a goal to achieve a 50:50 balance between animal and vegetable protein consumption by 2030, highlighting the role of government policies in driving demand. In Austria, the BILLA supermarket chain reported a 33% increase in plant-based milk sales after reducing its price premium over dairy to single digits. Among protein-conscious consumers, soy beverages stand out. Unlike oat milk, which contains about 1.0 g of protein per 100ml, soy milk provides 2.0-3.4 g per 100ml, making it the only plant-based milk that naturally matches cow's milk in protein content without requiring fortification.

Rising Popularity of Fortified and Functional Beverages

Fortification is a key differentiator in the market, but its application is inconsistent. In the UK, only 28% of plant-based dairy alternatives are fortified with iodine, essential for thyroid health. A Swiss study found just four iodine-fortified products, all oat-based, highlighting an opportunity for soy products to offer better nutrient profiles. The British Dietetic Association recommends fortifying plant-based milk alternatives with calcium, vitamin D, B12, B2, and iodine. Studies show calcium carbonate in soy milk absorbs as well as dairy, while tricalcium phosphate absorbs 25% less. The European Commission aims to standardize fortification levels by 2025, which could benefit large players like Danone and Nestlé due to compliance costs. Probiotic soy yogurts, using encapsulated Lactobacillus acidophilus and Bifidobacterium strains, now achieve a 30-day shelf life, combining gut-health benefits with plant-based appeal for consumers wary of "overly processed" foods.

Rising Demand for Natural and Clean-Label Products

Clean-label trends are reshaping the food industry by driving changes in formulation strategies. Although 41% of European consumers cite price as the main barrier to adopting sustainable products, many are willing to pay a 24% premium for products labeled "all natural" and a 16% premium for those with organic certification. France stands out as a leader in organic product availability, with 26% of food items on digital shelves featuring organic claims. This reflects the country’s strict regulatory standards and the increasing demand from informed consumers. The new EU Organic Regulation (EU 2018/848), which mandates full compliance by January 1, 2025, is expected to raise adaptation and certification costs by 50-200%[2]Research Institute of Organic Agriculture (FiBL), "New EU Organic Regulation Impact Study.", fibl.org. These rising costs are likely to reduce supply and further increase premiums for certified organic products.

Innovation in Flavors and Formats

Alpro's 2024 UK launches, including a caramel barista line, protein-enriched drinks, and 500ml convenience packs, highlight how flavor and packaging innovations drive growth. Flavored products dominate with a 61.34% share in 2024, but the unflavored segment is set to grow at a 7.92% CAGR through 2030, reflecting two distinct consumer groups: mainstream buyers prefer sweetened options, while health-conscious and culinary users choose unsweetened bases for cooking and coffee. Cans, growing at a 6.93% CAGR, benefit from sustainability and on-the-go trends. SIG's aluminum-free aseptic carton, launching in July 2025 and already used by ALDI Germany for Rio d'oro grape juice, offers a greener alternative with up to 61% lower CO2 emissions when paired with forest-based polymers. Soy-based drinkable yogurt, with an 8.17% CAGR, is gaining traction due to probiotics and a shelf life exceeding 30 days, enabling wider distribution without cold-chain logistics and positioning it as a versatile snack beyond breakfast.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from alternative plant-based beverages | -1.4% | Germany, UK, France; moderate in Spain and Italy | Short term (≤ 2 years) |

| Soy allergies and GMO perceptions | -0.8% | Germany, France, UK; emerging in Spain and Netherlands | Medium term (2-4 years) |

| Regulatory restrictions on labeling | -0.5% | UK (post-Brexit), France; limited in Germany and Spain | Medium term (2-4 years) |

| Supply chain traceability challenges | -0.4% | Germany, Netherlands, France; emerging in Spain and Italy | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Competition from Alternative Plant-Based Beverages

Oat milk has significantly changed the competitive landscape of plant-based milk. By early 2024, it dominated Germany's plant-based milk market. However, its growth is slowing down. In the UK, Oatly's sales growth dropped to just 0.3%, a sharp decline from its earlier triple-digit growth rates. Additionally, 81% of Europeans aged 18-35 still consume cow's milk at least once a week. This indicates that while plant-based milk options are growing, they have not replaced dairy but have instead diversified the market. Concerns about oat milk's nutrition are also emerging. For instance, maltose in oat milk has a glycemic index of 105, much higher than lactose's 46. Beta-glucan fiber in oat milk can cause digestive issues, and its classification as an ultra-processed product raises health concerns. These factors are creating opportunities for soy milk to regain popularity among protein-focused consumers. The market is also seeing more fragmentation with almond and pea protein alternatives. Almond milk attracts calorie-conscious consumers, while pea protein appeals to those focused on sports nutrition. However, neither matches soy milk's high protein content or its versatility in fortification.

Soy Allergies and GMO Perceptions

Europe’s soy beverages market continues to face complex perception challenges, particularly as many consumers still associate soy with large-scale industrial farming and genetically modified crops, even though the region relies predominantly on certified non-GMO supply chains. This disconnect between perception and reality shapes purchasing behavior, contributing to a preference for alternatives such as oat and almond beverages, which are viewed as more natural and less allergenic. At the same time, mandatory allergen labeling adds to hesitancy around soy, even though actual allergy prevalence is comparatively low. Market dynamics are also influenced by fluctuations in non-GMO soy availability and pricing, driven by shifts in regional cultivation patterns and changes in global export flows. Variability in production and trade continues to shape procurement strategies for European manufacturers, who must balance cost pressures with consumer expectations for clean-label, sustainably sourced ingredients. Although yields and supply conditions may improve periodically, the category still faces a cost disadvantage relative to commodity soy, reinforcing the need for efficient sourcing and long-term supplier partnerships.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Drinkable Yogurt Drives Functional Shift

In 2025, soy milk captured a commanding 78.12% of the product-type segment, solidifying its status as the go-to soy beverage. This dominance is a result of decades of category evolution, extensive retail reach, and its adaptability—from enhancing coffee to diverse cooking uses. With a protein density of 2.0-3.4 g/100ml, soy milk closely mirrors cow's milk, a fact underscored by the German Nutrition Society, which recognizes soy drinks as the top nutritionally-aligned alternative. While fortifying with calcium carbonate ensures a dairy-comparable bioavailability, sedimentation challenges necessitate consumer education on shaking before use for optimal nutrient absorption. Alpro's 2024 UK launches, featuring a caramel barista line and 500ml protein-enriched convenience packs, highlight how subtle innovations in flavor and format can safeguard market share against the rising oat-milk trend.

Soy-based drinkable yogurt, projected to grow at an 7.83% CAGR through 2031, is charting the category's functional frontier. By fortifying with encapsulated Lactobacillus acidophilus and Bifidobacterium probiotics, shelf life has been extended to over 30 days. This advancement allows for ambient distribution, rebranding the yogurt as a portable, gut-health-centric snack, moving away from its traditional refrigerated breakfast role. This shift directly addresses the 29% of consumers deterred by perceptions of "overly processed" plant-based products. The fermentation process bestows a health halo absent in ultra-filtered beverages. Additionally, the yogurt's growth taps into the pharmacy and drugstore channel's 6.74% CAGR, where its functional appeal commands premium pricing, bolstered by endorsements from health professionals. Notably, Germany's dm drugstore chain, witnessing a surge in food purchases during customer visits, underscores the expanding footprint of health-and-wellness retail in the plant-based beverage arena, moving beyond conventional grocery boundaries.

By Flavor: Simplicity Gains Among Clean-Label Seekers

In 2025, flavoured soy beverages hold a significant 61.02% share of the segment. This growth is driven by consumer preferences for sweetened, vanilla, chocolate, and fruit-infused options. These flavors help mask soy's natural beany taste and compete directly with the flavor profile of dairy milk. However, widespread adoption depends on improving taste and texture. Many European consumers cite these factors as barriers to trying plant-based dairy products. Flavoring helps overcome these challenges, especially for first-time buyers, as noted by Roland Berger. Alpro's caramel barista line targets premium coffee shops, where its rich flavors and excellent frothing ability justify higher prices and attract latte drinkers. New flavors like matcha, turmeric, and coffee-infused options are gaining attention among health-conscious consumers looking for added functional benefits. However, these emerging flavors remain niche compared to the more popular vanilla and chocolate options.

Un-flavoured soy milk, while holding a smaller market share, is expected to grow at a 7.55% CAGR through 2031. This growth reflects a shift in consumer preferences. Clean-label advocates and culinary users prefer unsweetened, unflavoured soy milk for cooking, baking, and coffee, as added sugars and flavors can interfere with recipes. A February 2025 OECD study found that products with "all natural" claims can command a 24% premium in consumer willingness-to-pay. Un-flavoured soy milk aligns with this trend by offering simple ingredient lists. In France, 26% of organic products on digital food shelves highlight a consumer base that values transparency and carefully examines labels. The growth of un-flavoured soy milk in this market shows that educated buyers prioritize transparency over masking taste. Additionally, the barista channel is driving demand for unsweetened soy milk. Its high protein content provides better frothing performance compared to oat milk, giving specialty coffee shops a way to differentiate their plant-based offerings.

By Packaging Type: Cans Capture Sustainability and Portability

In 2025, bottles hold a 36.75% share of the packaging market, driven by PET's affordability, clear design that highlights product quality, and compatibility with retail refrigeration systems. This packaging format is especially popular in Germany and the UK, where 1-liter bottles suit household consumption needs and align with private-label strategies focused on cost-effectiveness rather than premium branding. However, bottles face challenges due to their environmental impact. PET relies on fossil-based materials, and recycling infrastructure in Southern and Eastern Europe remains underdeveloped, making bottles vulnerable as sustainability regulations become stricter. Cartons, while not the fastest-growing segment, are gaining traction with SIG's introduction of aluminum-free aseptic technology in July 2025. This innovation reduces CO2 emissions by 18-29% compared to traditional cartons and by up to 61% when combined with forest-based polymers.

Cans are projected to grow at a 6.68% CAGR through 2031, benefiting from two major trends: sustainability and the rise of on-the-go consumption. Aluminum's infinite recyclability and Europe's high 76% recycling rate for cans (compared to PET's 42%) align with the EU's Circular Economy Action Plan and growing consumer demand for sustainable packaging. Cans are also portable and stable at room temperature, allowing them to be sold in convenience stores, vending machines, and travel retail outlets, expanding the occasions for soy beverage consumption. Spain, with a 7.21% geographic CAGR, reflects this growth. The country's strong tourism industry and outdoor lifestyle drive demand for single-serve, portable packaging. Aseptic pouches, though a niche option, are used in institutional food services and emerging markets with limited cold-chain infrastructure. They offer a cost-effective alternative to cartons for bulk applications.

By Distribution Channel: Health Retail Elevates Functional Positioning

In 2025, supermarkets and hypermarkets account for 40.25% of the distribution share, driven by their ability to scale operations, run impactful promotions, and expand private-label offerings. In April 2024, REWE opened Berlin's first fully plant-based supermarket, featuring over 2,700 vegan products. This initiative highlights how mainstream retailers are creating dedicated plant-based sections to grow this category while maintaining dairy sales. Austria's BILLA chain reported a 33% rise in plant-based milk sales after introducing price-parity measures that reduced the cost difference with dairy to single digits. This demonstrates that affordability, identified by 41% of consumers as the main barrier, is key to driving mass-market adoption. The dominance of supermarkets and hypermarkets in Germany and Spain reflects the retail structure in these countries, where hypermarkets cater to weekly shopping habits and promote large-format packaging through regular promotional cycles.

Pharmacies and drugstores are growing at a 6.74% CAGR through 2031, repositioning soy beverages as functional wellness products rather than basic commodities. Germany's dm chain, where 42% of customers now purchase food items, has expanded its organic and plant-based product range to leverage the health-focused image of pharmacy retail. Pharmacies typically charge 15-25% more than supermarkets, justified by smaller packaging, fortified formulations, and the perceived endorsement of health professionals. The 7.83% CAGR of soy-based drinkable yogurt aligns with this channel's growth, as its probiotic benefits and gut-health claims appeal to health-conscious shoppers. In the Netherlands, the National Protein Strategy aims for a 50:50 balance between animal and plant-based proteins by 2030. This goal is encouraging pharmacies and health-food retailers to increase their plant-based product offerings, supporting public health initiatives.

Geography Analysis

In 2025, Germany holds a 28.35% market share, supported by strong household adoption and government policies, including significant public funding for alternative protein research announced in 2023. In April 2024, REWE launched Berlin's first fully plant-based supermarket, offering over 2,700 vegan products, signaling a strong commitment from mainstream retailers to grow the category. However, the rise of private-label products is putting pressure on branded product margins. In August 2025, Danone decided to discontinue its Provamel brand in Germany to focus resources on Alpro, highlighting the need for companies to streamline their portfolios in a market where scale is critical for promotional opportunities. Germany consumed approximately 850,000 tonnes of non-GMO soy in 2023, the highest in the EU. This soy is used for both feed and food, with food applications benefiting from strict traceability under VLOG certification.

Spain is projected to be Europe’s fastest-growing soy beverage market, with a 7.21% CAGR through 2031, driven by increasing consumer preference for plant-based dairy. By 2023, household penetration reached 40%, surpassing Germany and the UK. National brands like Vivesoy and Yosoy enjoy strong regional loyalty. In July 2024, Refresco announced its acquisition of Frías Nutrición, a Burgos-based private-label producer of plant-based drinks, including soy. This acquisition is expected to strengthen Spain’s contract-manufacturing capabilities and boost exports to France and Italy. Spain’s Mediterranean diet, which emphasizes legumes and plant proteins, provides a cultural advantage over northern European markets. Additionally, the growing tourism sector is driving demand for portable, single-serve formats like cans, which are growing at a 6.68% CAGR.

The UK, France, Italy, and the Netherlands show diverse market trends. In the UK, plant-based milk household penetration exceeded 33% in 2023, with one in three consumers purchasing plant-based dairy. However, post-Brexit regulatory changes, including draft guidelines restricting plant-based dairy terminology, are creating compliance challenges for brands operating across Europe. Italy consumed 350,000 tonnes of non-GMO soy in 2023 and accounted for 10% of the EU’s organic soy cultivation. This reflects its use in both feed and food, with domestic production led by regional players like Valsoia and Granarolo. In the Netherlands, the National Protein Strategy aims to achieve a 50:50 balance between animal and vegetable protein by 2030. Wageningen University is driving innovation in functional beverages, although oat and pea alternatives currently receive more R&D investment than soy. Despite this, soy remains an important part of the market.

Competitive Landscape

The Europe soy beverages market is moderately consolidated, with a handful of established multinational brands and strong regional players shaping competition through broad distribution networks and deep category expertise. Companies such as Danone S.A., Vitasoy International Holdings Limited, Hain Celestial Group Inc., Valsoia S.p.A., SunOpta Inc. and prominent private-label lines from leading retailers maintain significant market presence by leveraging their scale, strong brand portfolios, and consistent product innovation. Their ability to offer a wide range of soy-based drinks—including fortified, organic, unsweetened, barista-ready, and flavored variants—allows them to cater to both mainstream consumers and those seeking functional or health-oriented options.

Alongside these major players, several regional producers and newer plant-based start-ups contribute to market diversity by introducing clean-label, non-GMO, and sustainably sourced soy beverages tailored to local consumer preferences. These companies often focus on origin transparency, shorter ingredient lists, and environmentally responsible sourcing, positioning themselves as appealing alternatives within the broader plant-based segment. This dynamic creates a competitive environment in which agility and differentiation are key, as smaller brands leverage niche positioning while larger companies rely on scale and marketing strength.

Consolidation in the market is further reinforced by Europe’s stringent regulatory framework related to food safety, labeling, sustainability, and nutritional claims, which tends to favor companies with strong R&D capabilities and established compliance systems. Meanwhile, rising adoption of plant-based diets, increased protein awareness, and continued interest in dairy alternatives support steady demand for soy beverages. As competition intensifies from oat, almond, and other plant-based drinks, leading soy beverage manufacturers are expected to focus on taste improvements, cleaner formulations, and sustainability messaging to preserve their share in an evolving marketplace.

Europe Soy Beverages Industry Leaders

-

Danone S.A.

-

Vitasoy International Holdings Limited

-

Hain Celestial Group Inc.

-

Valsoia S.p.A.

-

SunOpta Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Danone's dairy-free Alpro brand has introduced a new Alpro Kids product range in the United Kingdom. The range features a soya-based strawberry drink available in 200 ml cartons with paper straws.

- April 2025: Rude Health introduced a new Super Clean Soya Milk with Calcium. This dairy-free milk alternative is made with only four ingredients: spring water, sustainably sourced soya beans, calcium carbonate, and sea salt. It is high in protein and gluten-free.

- July 2024: Dutch drinks group Refresco has acquired Spanish plant-based beverage maker Frías Nutrición from its private-equity owner. Frías produces private-label plant-based drinks, including almond, rice, hazelnut, and soy drinks, for several Spanish retailers.

Europe Soy Beverages Market Report Scope

Europe soy beverage market is segmented by product type which includes soy milk and soy-based drinkable yogurt. The market is divided based on flavor including flavored and plain/unflavored. Based on the distribution channel, the market is segmented into supermarkets/hypermarkets, pharmacy, convenience stores, online retail stores, and others. The study also involves the analysis in regions such as the United Kingdom, Germany, France, Spain, Italy, Russia and Rest of Europe.

Product Type

| Soy Milk |

| Soy Based Drinkable Yogurt |

Flavour

| Flavoured |

| Un-flavoured |

Packaging Type

| Bottles |

| Cartons |

| Cans |

| Aseptic Pouches |

Distribution Channel

| Supermarkets and Hypermarkets |

| Convenience Stores |

| Pharmacies/ Drug stores |

| Online Retail Stores |

| Others |

Country

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| Netherlands |

| Rest of Europe |

| Product Type | Soy Milk |

| Soy Based Drinkable Yogurt | |

| Flavour | Flavoured |

| Un-flavoured | |

| Packaging Type | Bottles |

| Cartons | |

| Cans | |

| Aseptic Pouches | |

| Distribution Channel | Supermarkets and Hypermarkets |

| Convenience Stores | |

| Pharmacies/ Drug stores | |

| Online Retail Stores | |

| Others | |

| Country | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| Netherlands | |

| Rest of Europe |

Key Questions Answered in the Report

How big is the Europe soy beverages market in 2026?

The Europe soy beverages market size is USD 2.04 billion in 2026 and is projected to reach USD 2.69 billion by 2031.

Which country leads soy beverage sales in Europe?

Germany holds the largest share at 28.35% of regional value, supported by strong household penetration and robust retail distribution.

What is driving growth of soy-based drinkable yogurt?

Probiotic fortification, 30-day ambient shelf life, and rising pharmacy-channel placement are pushing drinkable yogurt ahead with an 7.83% CAGR.

What is the fastest growing distribution channel for soy beverages?

Pharmacies and drugstores are expanding at a 6.74% CAGR as shoppers seek fortified, functional drinks with a health-professional halo.

Page last updated on: