Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

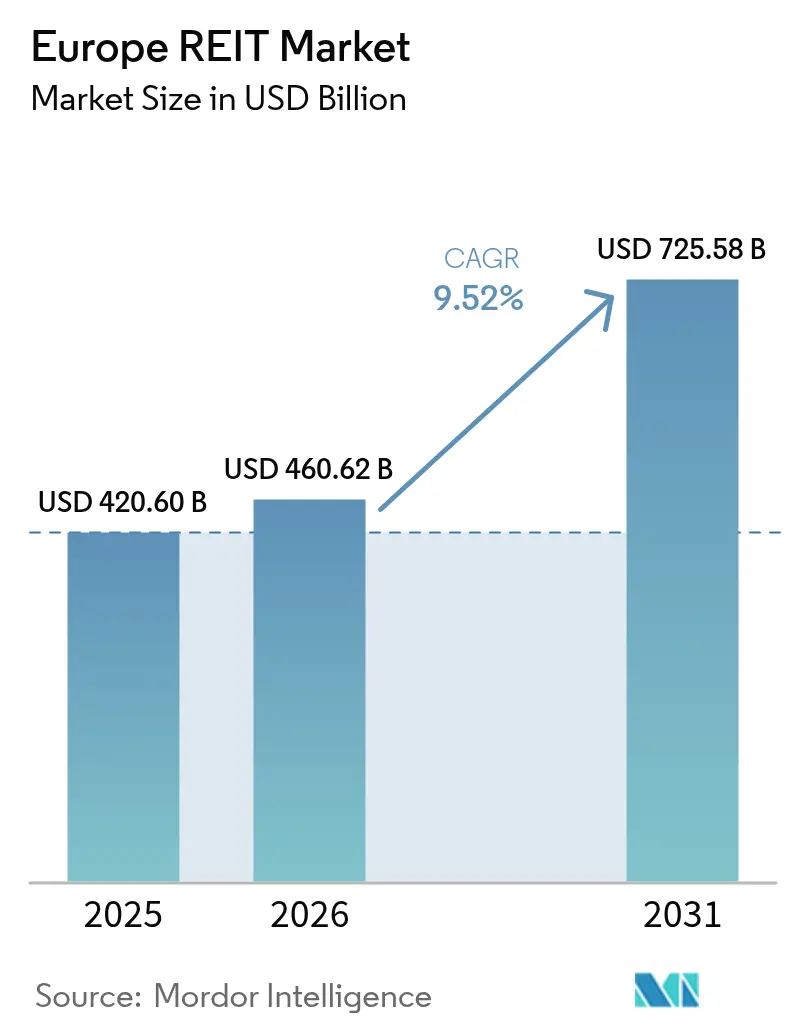

| Base Year Market Size (2025) | USD 420.60 Billion |

| Market Size (2026) | USD 460.62 Billion |

| Market Size (2031) | USD 725.58 Billion |

| Growth Rate (2026 - 2031) | 9.52% CAGR |

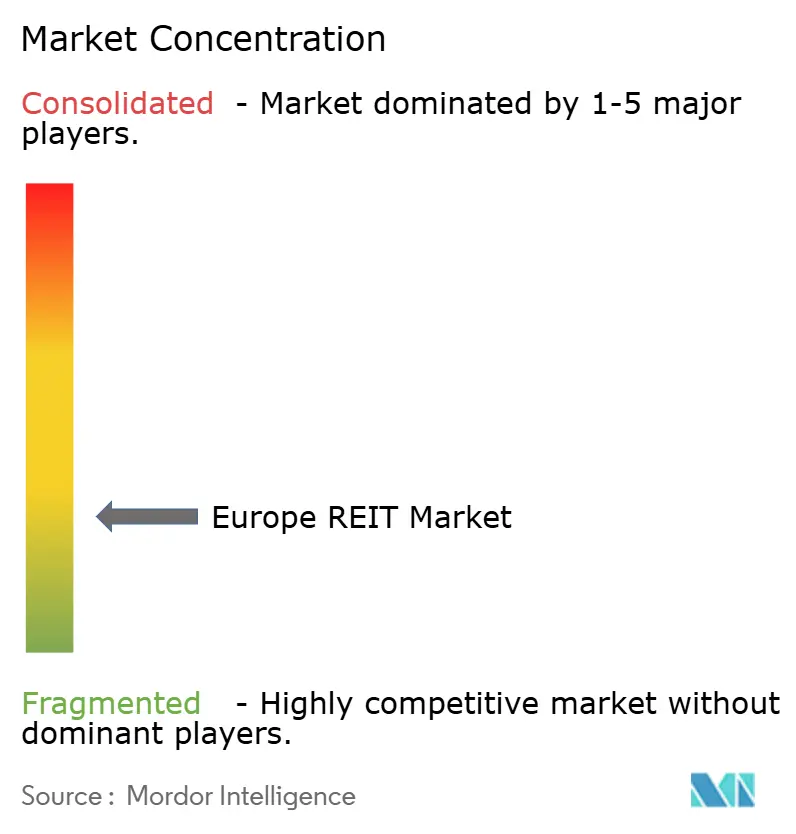

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe REIT Market Analysis by Mordor Intelligence

The Europe REIT market size is expected to grow from USD 420.60 billion in 2025 to USD 460.62 billion in 2026 and is forecast to reach USD 725.58 billion by 2031 at 9.52% CAGR over 2026-2031. Six interrelated forces sustain this momentum: moderated borrowing costs under the European Central Bank’s (ECB) carefully sequenced rate-cutting cycle, deep institutional appetite for inflation-adjusted yields, enduring e-commerce logistics demand, rising data-center build-outs, expanding municipal partnerships for affordable housing, and supportive EU-wide capital-markets reforms such as ELTIF 2.0. Rising refinancing costs after 2024 created near-term volatility, yet well-capitalized vehicles refinanced at spreads still below the twenty-year average, protecting cash-flow coverage and preserving distribution visibility. Sector rotation into industrial and data-center assets compresses cap rates faster than in retail and secondary office segments, which now price in meaningful hybrid-working vacancy risk. Listed vehicles increasingly rely on sustainability-linked debt to fund green retrofits, turning energy-performance regulations from a cost overhang into a competitive differentiator with tenants and investors alike. The landscape remains fragmented—top-five players control only 31% of capitalization—which leaves ample room for consolidation plays by sponsors that can shoulder stricter covenant packages.

Key Report Takeaways

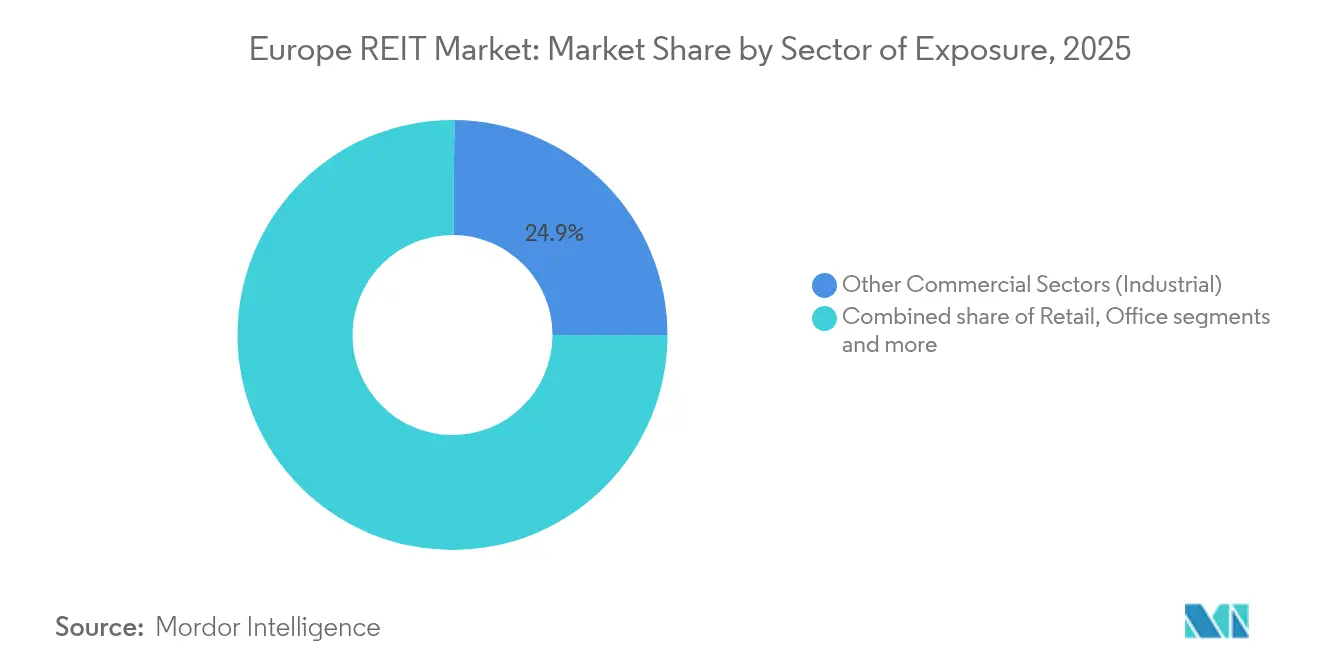

- By sector, industrial properties (under the other commercial sectors) led with a 24.86% Europe REIT market share in 2025, while data centers (under the other commercial sectors) are forecast to post a 10.18% CAGR to 2031.

- By market capitalization, large-cap vehicles held 46.92% of the Europe REIT market size in 2025, and small-cap platforms are projected to expand at a 9.78% CAGR through 2031.

- By geography, the United Kingdom captured 40.21% of the Europe REIT market share in 2025, whereas the Nordics are on track for an 8.11% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe REIT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Measured ECB rate-cutting cycle | +1.8% | Eurozone core, spill-over to UK | Medium term (2-4 years) |

| E-commerce-led logistics absorption | +2.1% | Germany, Netherlands, UK corridors | Long term (≥ 4 years) |

| Inflation-hedged institutional inflows | +1.4% | France, Germany, pan-regional pension funds | Short term (≤ 2 years) |

| EU ELTIF 2.0 retail-capital gateway | +0.9% | All EU-27 member states | Medium term (2-4 years) |

| Municipal affordable-housing programs | +0.7% | Germany, Netherlands, Nordic capitals | Long term (≥ 4 years) |

| Tokenized real estate secondary markets | +0.3% | Luxembourg, Netherlands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Sustained ECB Rate Moderation

The central bank cut policy rates by 50 basis points across 2024-2025, allowing well-rated REITs to roll maturities at sub-4% coupons while still attracting overseas capital seeking positive real yields[1]European Central Bank, “ECB Lowers Key Interest Rates by 25 Basis Points,” ecb.europa.eu. Liability management now extends weighted-average debt maturities beyond five years, shielding cash flows during forecast tightening cycles. Transatlantic rate divergence added relative-value appeal, prompting U.S. pension plans to raise strategic allocations. Germany’s Vonovia exemplified the trend by closing USD 1.60 billion in syndicated loans at favorable spreads, preserving its investment-grade status. If inflation expectations re-anchor lower, the carry trade could narrow and reduce incremental fund inflows, but base-case forecasts still assume credit spreads remain below the 20-year mean. Consequently, financing visibility continues to underpin dividend stability across the Europe REIT market.

E-Commerce-Driven Logistics Expansion

European online sales penetration rose to 16% of retail turnover in 2024, tripling warehouse needs relative to brick-and-mortar formats[2]CBRE, “European Logistics and Industrial Outlook 2024,” cbre.com. Grade-A facilities within 50 kilometres of dense population clusters now command rental uplifts exceeding 8% annually, outpacing headline CPI. Segro accelerated this pattern by accumulating 15 infill plots in Germany and the Netherlands that shorten delivery radii to less than 20 minutes. Development pipelines remain disciplined because land constraints and zoning hurdles cap speculative supply, protecting occupancy north of 97%. Cross-border fulfillment standards under the EU customs union further stimulate demand for pan-regional hubs with advanced automation. As a result, logistics remains the anchor growth pillar of the Europe REIT market for the foreseeable horizon.

Institutional Inflows Looking for Inflation Hedges

Large pension funds rotated USD 50 billion into listed real estate during 2024, drawn by CPI-linked leases unavailable in sovereign-bond portfolios[3]EPRA, “EPRA Annual Report 2024,” epra.com. Cash-flow indexation clauses safeguard real returns when consumer prices exceed 2.5% thresholds. Dutch asset owner APG lifted its allocation to 4.2% of AUM, citing superior correlation benefits. The long-duration nature of these mandates lowers unit-share volatility because redemptions track actuarial projections rather than market sentiment. These sticky flows have cushioned price swings during sudden rate repricings, supporting liquidity and tightening bid-ask spreads. Over time, structural pension de-risking into real assets will likely deepen, reinforcing the asset-class premium enjoyed by the Europe REIT market.

ELTIF 2.0 Retail Capital Access

The 2024 overhaul of the European Long-Term Investment Fund regime abolished high entry minima and simplified passporting, opening doors for mass-affluent savers to buy listed property funds via bancassurance channels. French managers launched the first compliant REIT wrappers in 2025, targeting USD 2.14 billion in subscriptions. Retail flows tend to be more stable than institutional rebalancing, extending valuation support during periods of market stress. Compliance, however, entails granular disclosure and liquidity-buffer obligations that smaller issuers may find onerous. Those electing not to adopt the framework could forfeit growing retail demand, accelerating scale-driven consolidation. Net-net, ELTIF 2.0 increases the breadth of the Europe REIT market’s investor universe.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Refinancing costs after 2024 rate hikes | -2.3% | Eurozone, UK, Switzerland | Short term (≤ 2 years) |

| Hybrid working reduces office demand | -1.7% | London, Paris, Frankfurt CBDs | Medium term (2-4 years) |

| EPC C-rating retrofit capex cliff | -1.1% | All EU-27 commercial stock | Medium term (2-4 years) |

| Tightening ESG-linked debt covenants | -0.8% | Northern Europe, global lenders | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Hybrid Work Shakes Office Utilization

Average office attendance settled near 65% of 2019 baselines by 2025, yet occupancy divergence between prime CBD towers and suburban stock has widened[4]JLL, “Office Market Clock,” jll.com. Land Securities’ West End assets maintain waiting lists, whereas secondary London periphery blocks face structural vacancy above 15%. Tenants prioritize wellness amenities and high-efficiency ventilation, forcing landlords to offer capital-intensive fit-outs that dilute initial yields. Flexible-lease providers absorb some footprint risk, but their month-to-month contracts introduce revenue volatility for host REITs. Office-heavy vehicles now pivot to mixed-use or life-science conversions to preserve relevance. Without adaptive strategies, office exposure will continue to weigh on the Europe REIT market’s blended growth.

Stricter ESG-Linked Debt Covenants

Lenders now embed sustainability-performance targets into revolving credit facilities, tying margin ratchets to annual emission-intensity reductions. Northern European banks lead adoption, pushing spreads 25-30 basis points wider for borrowers that miss milestones. Digital Realty Trust’s 2025 green bond raised USD 1.07 billion at 35 35-basis-point discount, proving that compliance pays when executed credibly. Smaller borrowers struggle with data-collection requirements and may pay higher all-in coupons. Over time, covenant convergence will crowd out laggards, effectively raising the baseline cost of capital for non-aligned portfolios. As reporting rigor increases, credibility around ESG delivery will become integral to valuation within the Europe REIT market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sector of Exposure: Industrial Leadership Anchors Growth

Industrial assets (under the other commercial sectors) delivered 24.86 of % Europe REIT market share in 2025, underscoring irreplaceable e-commerce fulfillment needs close to consumption nodes. Rental escalations averaged 8% year-on-year across Germany’s Rhine-Ruhr corridor, sustaining cap-rate compression to sub-4% levels. Data centers (under the other commercial sectors) posted the fastest growth, with a forecast 10.18% CAGR to 2031 underpinned by hyperscale and edge deployments requiring high-density power envelopes. Diversified vehicles now bundle last-mile warehouses with micro-data-hubs, creating blended income resilient to consumer-spending cycles. Residential REITs hold an enduring 24.73% share, leveraging urban housing undersupply and index-linked leases that hedge inflation. Meanwhile, retail footprints continue to rationalize, as experiential malls outperform vanilla shopping centers by capturing spill-over footfall from leisure anchors. This sectoral hierarchy illustrates how technological shifts and demographic constraints shape capital allocation inside the Europe REIT market.

Industrial dominance persists because brownfield availability near major ports is scarce, limiting disruptive oversupply. Segro’s cross-docking design cuts average delivery windows by 22 minutes, a tangible economic advantage for tenants facing tight consumer-delivery promises. In data centers, Digital Realty expanded inter-connect nodes in Brussels and Vienna, monetizing cross-connect fees that enhance EBITDA margins above 60%. Healthcare REITs register 8.21% CAGR on aging-population fundamentals, with Aedifica’s merger with Cofinimmo creating a USD 12.84 billion (EUR 12 billion) pan-regional champion. Office exposure bifurcates: prime CBD towers enjoy pricing power, whereas secondary blocks seek alternate uses. Each subsector’s distinct cash-flow cadence allows portfolio managers to engineer risk-adjusted performance that meets rising dividend expectations in the Europe REIT market.

By Market Capitalization: Small-Cap Agility versus Large-Cap Scale

Large-cap issuers represented 46.92% of the Europe REIT market size in 2025, benefiting from AAA tenant rosters and granular refinancing menus. Their weighted-average debt cost sits 60 basis points below small-cap peers, cushioning net interest margins. Yet growth momentum skews toward smaller platforms projected at 9.78% CAGR to 2031, as niche managers incubate specialized strategies overlooked by bigger rivals. Mid-caps occupy a 32.84% share, balancing diversification with opportunity capture. Institutional investors increasingly mix large-cap stability with small-cap torque, constructing barbell exposures that outperform passive benchmarks. Capitalization dispersion, therefore, fuels healthy liquidity across the Europe REIT market’s listing tiers.

Tritax Big Box illustrates small-cap outperformance: H1 2025 adjusted EPS climbed to 4.63 pence, a 6.4% lift, on occupancy levels topping 98%. Conversely, refinancing fragility surfaced when Brookfield stepped in to buy Tritax EuroBox, validating the thesis that balance-sheet resilience matters more than headline growth. Large-caps deploy balance-sheet firepower for bolt-on acquisitions, accelerating sector consolidation. Mid-caps remain takeover targets, especially diversified vehicles trading at persistent NAV discounts. The interplay across size bands ensures continuous M&A optionality, a defining trait of the Europe REIT market’s competitive evolution.

Geography Analysis

The United Kingdom anchored 40.21% Europe REIT market share in 2025, leveraging transparent governance and a deep capital-market infrastructure that global investors prize. London’s West End offices average headline rents of GBP 140 per square foot, yet hybrid-work adaptation compels landlord incentives such as turnkey fitouts and shorter lease commitments. Logistics nodes around the “Golden Triangle” accommodate 35% of UK e-commerce parcels, sustaining low single-digit vacancy despite speculative supply. Brexit red tape shifted some banking functions to Dublin and Amsterdam, but listed REITs retained overseas interest through London Stock Exchange liquidity. ESG retrofits now dominate capex budgets, aligning with the City of London’s 2040 net-zero roadmap. These dynamics collectively underpin resilient distributable earnings that reinforce the UK’s outsized weight in the Europe REIT market.

Germany captured 21.57% of market value by focusing on residential ceilings constrained by chronic housing shortages in Munich, Berlin, and Hamburg. Vonovia and LEG Immobilien leverage municipal land collaborations to secure pipelines at implied land costs 30% below private-market benchmarks. Regulatory rent brakes temper near-term upside but guarantee occupancy exceeding 95%, supporting bond-like income qualities. Industrial corridors along the Rhine-Ruhr also attract logistics REITs, given proximity to Benelux ports. Meanwhile, France holds a 13.42% share centered on Parisian commercial landmarks owned by Unibail-Rodamco-Westfield, which pivots toward experience-led retail to counter pure online substitution. Spain’s 7.34% slice benefits from tourism-driven hospitality rebounds, aiding Merlin Properties’ diversified tilt. Each continental block contributes unique demand levers that diversify the Europe REIT market.

Nordic countries present the fastest trajectory with an 8.11% CAGR out to 2031, catalyzed by Stockholm’s office-to-residential conversions and Copenhagen’s stringent green-building codes. Swedish sponsors exploit flexible planning regimes allowing mixed-use overlays that spread operational risk across daytime and nighttime economies. Denmark’s energy-positive construction mandates push capex but reward compliant assets with green-bond pricing benefits. The BENELUX region, although with only 3.05% of capitalization, enjoys post-Brexit financial-services migration that lifts office and residential absorption in Amsterdam and Brussels. Cross-border passporting smooths expansion for pan-regional operators that can navigate multilingual tenant bases.

Competitive Landscape

The Europe REIT market remains moderately fragmented, with the largest entities holding a notable but not dominant share of total market capitalization. This fragmentation leaves room for further consolidation, which could unlock scale-driven operating efficiencies and competitive advantages. Specialization is the reigning strategy: Segro dominates logistics, Vonovia leads residential, Digital Realty spearheads data centers, and Aedifica-Cofinimmo forges healthcare supremacy. Technology adoption differentiates winners; Digital Realty’s predictive-maintenance AI reduced unplanned outages by 40%, enhancing tenant retention. Green-bond issuance also shapes capital-cost hierarchies as lenders favor verifiable energy-efficiency programs. Emerging proptech-enabled platforms, while small, introduce disruptive leasing models such as subscription-based co-living, potentially reshaping occupancy economics.

Strategic M&A punctuates the narrative. In 2024, Brookfield acquired Tritax EuroBox, signaling private equity's keen interest in high-barrier subsectors, especially those with depressed valuations. Aedifica and Cofinimmo merged in 2025, forming a pan-European healthcare landlord boasting a book value of USD 12.84 billion (EUR 12 billion), and unlocking benefits in fit-out equipment purchases. Digital Realty, buoyed by leasing surges in Frankfurt and Amsterdam, twice raised its 2025 FFO guidance, underscoring its growth-through-development strategy. Segro's focus on brown-field reclamations positions it advantageously in land-scarce corridors. As refinancing costs trend upward, capital discipline and asset recycling stand out as key differentiators in the landscape.

Competitive intensity varies by segment. Industrial enjoys oligopolistic traits given scarce land, while retail remains fragmented with many sub-scale owners. Office portfolios face existential strategy reviews amid hybrid occupancy pressures, driving selective divestments into mixed-use conversions. Residential consolidation continues, but regulatory rent caps slow mega-deals. Data-center portfolios attract infrastructure-fund bids that re-price the segment at utility-like multiples. Overall, managers capable of agile capital-allocation and ESG compliance solidify leadership, shaping the future trajectory of the Europe REIT market.

Europe REIT Industry Leaders

Unibail-Rodamco-Westfield

Segro plc

Vonovia SE

Land Securities Group plc

Klepierre SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Aedifica and Cofinimmo shareholders approved their proposed merger to create a EUR 12 billion (USD 12.84 billion) pan-European healthcare real estate platform, combining complementary geographic footprints across Belgium, the Netherlands, Germany, and France with specialized expertise in senior housing and medical facilities.

- July 2025: Digital Realty Trust raised its 2025 funds from operations forecast for the second time, citing stronger-than-expected demand for hyperscale data center capacity and edge computing infrastructure across European markets, with strength in Frankfurt and Amsterdam facilities.

- June 2025: Unibail-Rodamco-Westfield completed a USD 732.95 million (EUR 685 million) hybrid notes placement to refinance maturing debt and fund development projects, while announcing a strategic partnership with Saudi Arabia's Cenomi Centers for Middle East expansion opportunities.

- April 2025: Castellum AB announced plans to convert 15 Stockholm office properties to residential use, targeting USD 428 million (EUR 400 million) in development investments to address Sweden's housing shortage while repositioning assets away from hybrid-working-pressured office markets.

Europe REIT Market Report Scope

A real estate investment trust is a company that owns and, in most cases, operates income-producing real estate.

The European REITs market is segmented by sector of exposure (retail, industrial, office, residential, diversified, and other sectors of exposure) and country (the United Kingdom, France, Belgium, the Netherlands, Spain, and Rest of Europe). The report offers market sizes and forecasts in terms of value (USD) for all the above segments.

By Sector

| Commercial | Office |

| Retail | |

| Hospitality | |

| Healthcare | |

| Other Commercial Sector | |

| Residential |

By Market Capitalization

| Large-Cap (more than USD 10 billion) |

| Mid-Cap (USD 2–10 billion) |

| Small-Cap (less than USD 2 billion) |

By Geography

| United Kingdom | |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX | Belgium |

| Netherlands | |

| Luxembourg | |

| NORDICS | Denmark |

| Finland | |

| Iceland | |

| Norway | |

| Sweden | |

| Rest of Europe |

| By Sector | Commercial | Office |

| Retail | ||

| Hospitality | ||

| Healthcare | ||

| Other Commercial Sector | ||

| Residential | ||

| By Market Capitalization | Large-Cap (more than USD 10 billion) | |

| Mid-Cap (USD 2–10 billion) | ||

| Small-Cap (less than USD 2 billion) | ||

| By Geography | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX | Belgium | |

| Netherlands | ||

| Luxembourg | ||

| NORDICS | Denmark | |

| Finland | ||

| Iceland | ||

| Norway | ||

| Sweden | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the current value of the Europe REIT market and its expected growth?

The Europe REIT market size stands at USD 460.62 billion in 2026 and is projected to reach USD 725.58 billion by 2031, reflecting a 9.52% CAGR over 2026-2031.

Which sector leads European REIT allocations?

Industrial logistics assets lead with 24.86% of the Europe REIT market share due to sustained e-commerce demand.

Why are data-center REITs gaining prominence in Europe?

Hyperscale cloud and edge-computing expansions drive a 10.18% CAGR for data-center REITs, making them the fastest-growing segment.

How does hybrid work affect office-focused European REITs?

Office attendance stabilizing at 65% of 2019 levels pressures secondary assets, prompting conversions and flexible-lease strategies to maintain cash flows.

What role does ELTIF 2.0 play in REIT fundraising?

ELTIF 2.0 widens retail access to listed property funds, adding a new, stable capital channel that could expand the investor base by up to 40%.

Which geographic region is the fastest growing within European REITs?

Nordic markets are forecast to expand at an 8.11% CAGR through 2031 due to office-to-residential conversions and stringent green-building codes.

Page last updated on: