Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

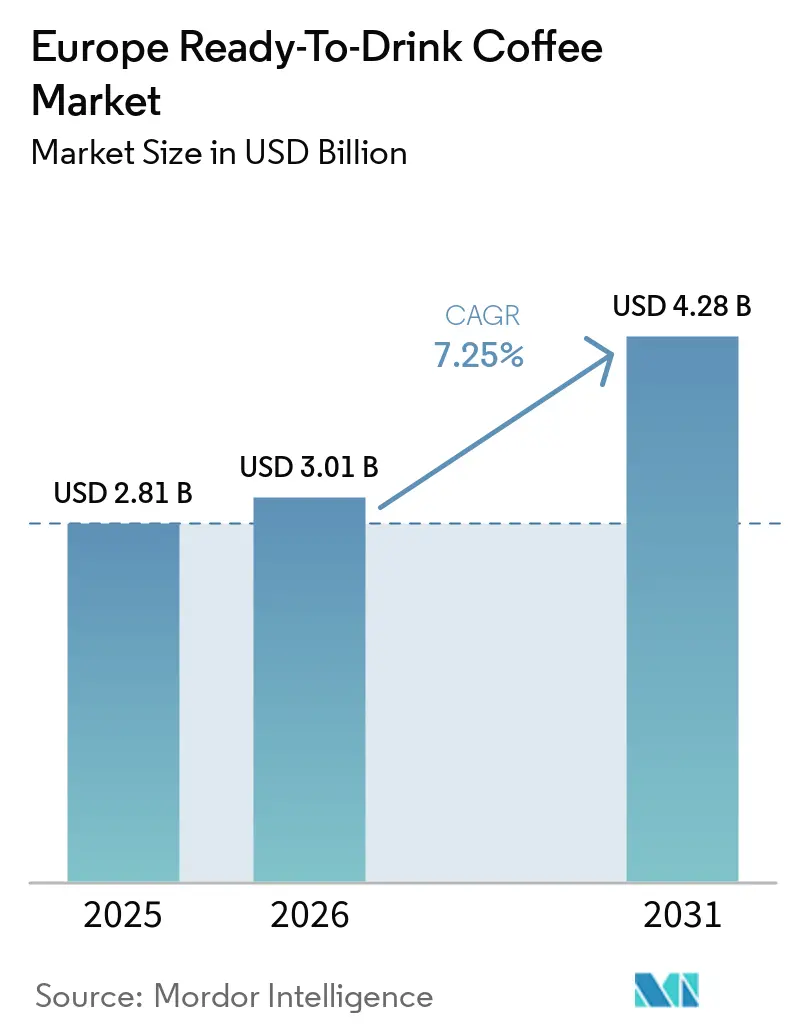

| Base Year Market Size (2025) | USD 2.81 Billion |

| Market Size (2026) | USD 3.01 Billion |

| Market Size (2031) | USD 4.28 Billion |

| Growth Rate (2026 - 2031) | 7.25% CAGR |

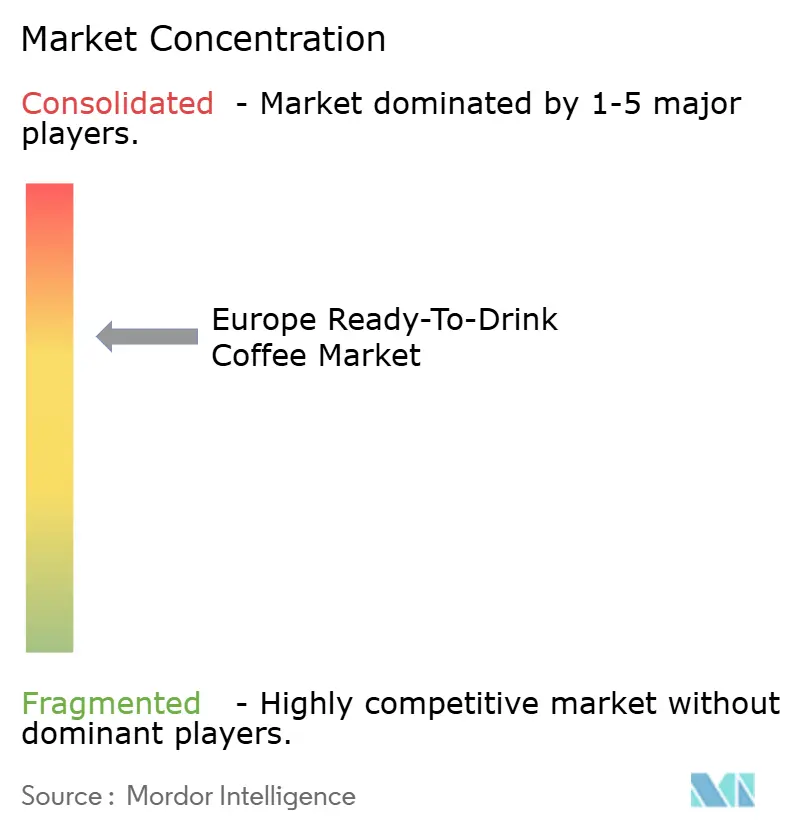

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Ready-To-Drink Coffee Market Analysis by Mordor Intelligence

The Europe Ready-To-Drink Coffee market size is expected to grow from USD 2.81 billion in 2025 to USD 3.01 billion in 2026 and is forecast to reach USD 4.28 billion by 2031 at 7.25% CAGR over 2026-2031. Demand from Gen Z and Millennials for on-the-go solutions, coupled with the EU's sustainability push and fluctuating arabica prices, is driving this value surge, even as traditional at-home brewing sees a slowdown. The market is witnessing a transformation, with rising private-label prominence, new traceability mandates from the EU Deforestation Regulation, and a shift towards energy-boosted formulations influencing sourcing and channel strategies. The café culture's premiumisation trend, swift flavour innovations, and a shift to lightweight PET are further propelling the market's growth. However, challenges like limited aseptic-filling capacity and ongoing green-coffee price fluctuations pose constraints. Major beverage players are diversifying across categories, and with Keurig Dr Pepper eyeing JDE Peet’s for acquisition, a wave of consolidation looms. This could sharpen competitive edges, emphasizing brand narratives, functional nutrition, and eco-friendly packaging.

Key Report Takeaways

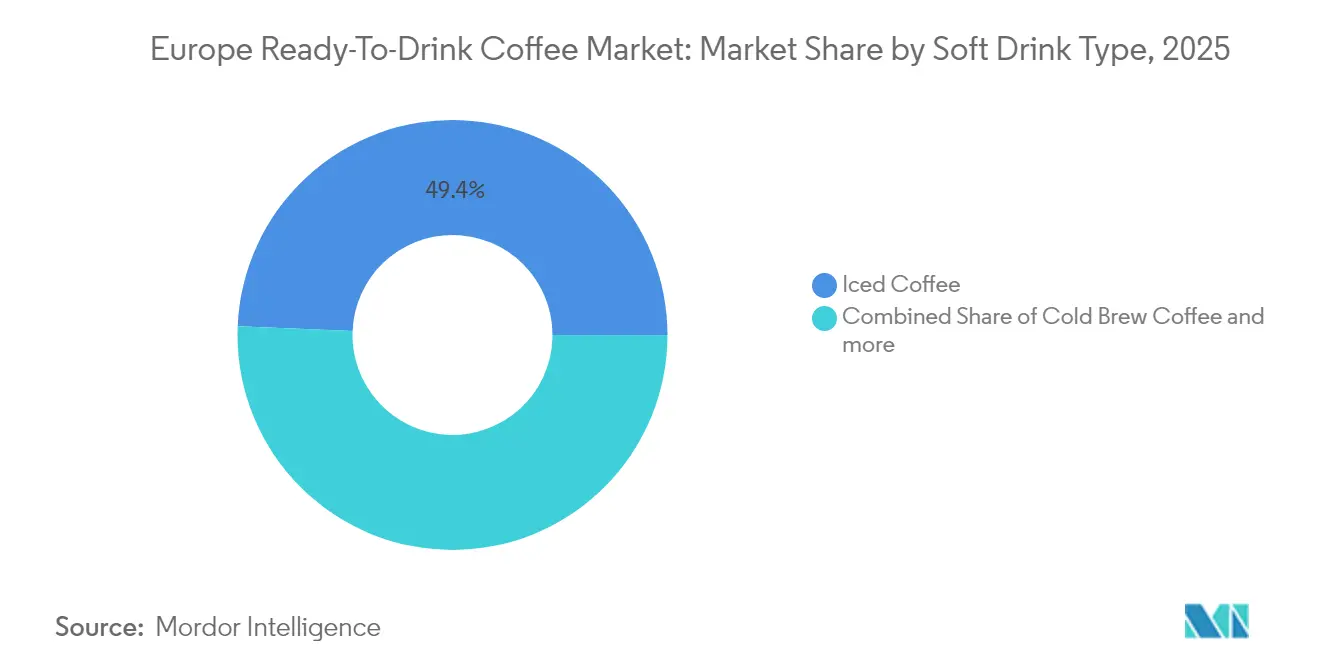

- By soft drink type, iced coffee led with 49.35% of the Europe Ready-To-Drink Coffee market share in 2025; cold brew is forecast to expand at an 7.82% CAGR through 2031.

- By packaging, glass bottles captured 35.10% share of the Europe Ready-To-Drink Coffee market size in 2025, and PET bottles are advancing at a 7.65% CAGR to 2031.

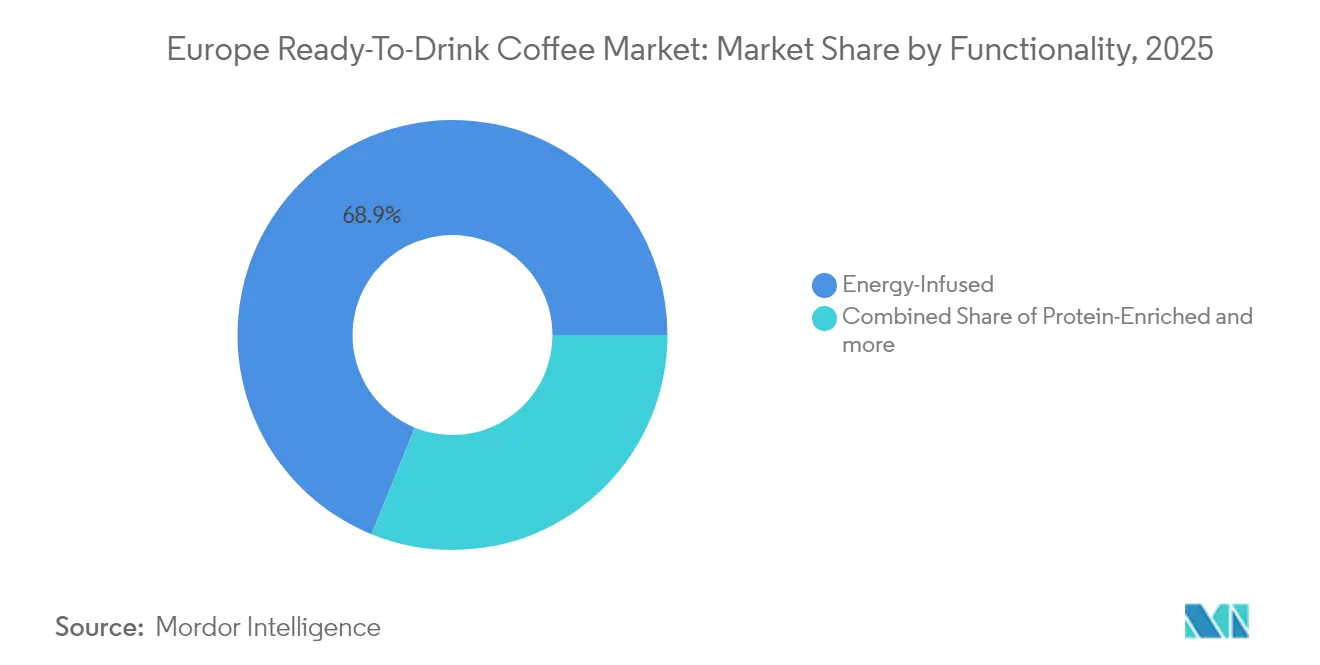

- By functionality, energy-infused products accounted for 68.85% of the Europe Ready-To-Drink Coffee market size in 2025 and are progressing at an 7.88% CAGR through 2031.

- By distribution, off-trade held 62.30% of the Europe Ready-To-Drink Coffee market share in 2025, while on-trade is expanding at an 8.54% CAGR to 2031.

- By geography, the United Kingdom generated 37.10% of demand in 2025; Italy records the fastest 7.03% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Ready-To-Drink Coffee Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| On-the-go consumption trend among Gen Z and Millennials | +1.8% | The United Kingdom, Germany, France, Netherlands; urban centers across Europe | Short term (≤ 2 years) |

| Premiumisation and cafe-culture influence | +1.5% | Italy, Spain, the United Kingdom, and France, spreading to Poland and Belgium | Medium term (2-4 years) |

| Flavour and format innovation | +1.3% | Pan-European, led by Germany, the United Kingdom, Netherlands | Medium term (2-4 years) |

| Expansion of supermarket private-label RTD portfolios | +1.2% | Spain, Germany, United Kingdom, France, and accelerating in Poland | Short term (≤ 2 years) |

| Sustainability-driven switch to recyclable carton formats | +0.9% | Germany, Netherlands, Sweden, Belgium; Europe-wide regulatory push | Long term (≥ 4 years) |

| EU deforestation-free sourcing rules spurring traceable offerings | +0.6% | EU-wide, compliance-driven across all member states | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

On-the-go consumption trend among gen Z and millennials

Gen Z and Millennials, driven by fast-paced urban lifestyles and a preference for convenience, are fueling the European Ready-To-Drink (RTD) coffee market. These demographics view RTD coffee as a time-saving caffeine fix, with Gen Z favoring experimental, flavored, and iced varieties over traditional hot coffee. Government initiatives, such as Germany's focus on diabetes management, have increased demand for low-sugar products, prompting manufacturers to innovate with healthier formulations. In January 2024, Nestlé's Nescafé launched plant-based RTD coffee in Europe, targeting health-conscious consumers. By July 2024, Starbucks introduced RTD protein coffee drinks in flavors like caffe latte and caramel hazelnut, appealing to young adults seeking functional benefits. In February 2025, Emmi released Caffè Latte Zero in the UK, a no-added-sugar line made using sustainable processes, aligning with Gen Z's eco-conscious values. Innovations like these, coupled with sustainable packaging such as recyclable aluminum cans, reinforce the on-the-go trend as a key growth driver for the European RTD coffee market.

Premiumization and cafe culture influence

In Europe, especially in Italy and Spain, consumers are increasingly associating coffee with artisanal quality and a narrative of origin. This trend is now making its way into ready-to-drink (RTD) formats. Italy, with its deep-rooted espresso culture, where most adults indulge in daily coffee rituals and cafe prices have steadily climbed over the past three years, has cultivated a consumer base willing to pay a premium for authenticity. Seizing this opportunity, brands are rolling out offerings like single-origin cold brews, nitro-infused lattes, and specialty blends, closely resembling those found in third-wave cafes. In 2024, JDE Peet's capitalized on this trend, launching 'L'OR Iced Coffee', banking on the premium equity of its L'OR brand to set higher shelf prices. This push for premiumisation isn't just limited to the product but extends to packaging as well. Glass bottles and aluminum cans, adorned with high-resolution prints, exude a sense of craft, while aseptic cartons, boasting 360-degree branding, tell a story on a larger canvas. However, the appetite for premium pricing isn't universal. While Spain showcases a 43% share for private labels, hinting at a price-sensitive market in southern Europe, urban millennials in cities like Milan, Madrid, and Paris are increasingly viewing RTD coffee as a palatable luxury.

Flavour and format innovation

In a bid to capture niche preferences and broaden consumption occasions, manufacturers are expanding their offerings beyond the traditional latte and cappuccino. In March 2025, Nescafé unveiled Iced Lattes in multi-serve cartons, aiming at moments of at-home sharing. Meanwhile, in June 2024, Starbucks rolled out a trio of protein-infused coffee drinks, each boasting 20 grams of protein and no added sugar, catering to health-conscious consumers. Lavazza, in June 2024, introduced three iced coffee cans, one of which is protein-enriched, highlighting the merging worlds of functional beverages and coffee. Flavor experimentation is on the rise: Alpro infused caramel into its Barista drink range in September 2024, and Oatly debuted two new ready-to-drink iced coffees in November 2025, both proudly showcasing their plant-based credentials. These innovations cater to diverse demands: decaf for evening sips, protein for post-workout recovery, and plant-based options for lactose-intolerant or vegan shoppers, allowing brands to secure prime shelf space across various retail categories.

Expansion of supermarket private label RTD portfolios

Retailers are harnessing their scale and consumer insights to introduce proprietary ready-to-drink (RTD) coffee lines, pricing them 20% to 30% lower than national brands, thereby securing both margins and customer loyalty. A case in point is Spain, where private-label coffee accounts for 43% of retail sales. Supermarkets, such as Mercadona with a 26.8% market share and Carrefour at 10%, are not just dominant in the coffee sector but are also pushing into the RTD coffee arena, as highlighted by CBI, a government agency from the Netherlands. In the UK, supermarkets are mirroring this trend. Marks & Spencer rolled out cold-brew oat lattes in 2025, while Tesco, Morrisons, and Sainsbury's are promoting Alpro and Starbucks RTD lines at enticing price points. The surge in private-label popularity can be attributed to enhanced quality, retailers are now sourcing from the same co-packers as established brands, and a shift in consumer behavior. During inflationary times, shoppers are more inclined to prioritize value over brand loyalty. This evolving landscape presents a challenge for multinational manufacturers: they can either engage in price competition, risking their margins, or they can pivot towards premiumization and innovation, seeking to validate their brand's higher price tag.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile coffee-bean prices are squeezing manufacturer margins | -1.4% | Pan-European, acute in Spain, Italy, Eastern Europe | Short term (≤ 2 years) |

| Intensifying private-label and discounter competition | -1.1% | Germany, Spain, the United Kingdom, and Poland, spreading to France | Medium term (2-4 years) |

| EU deforestation-free traceability compliance costs | -0.7% | EU-wide, disproportionate burden on small importers | Short term (≤ 2 years) |

| Limited aseptic-filling capacity for small entrants | -0.5% | Germany, Netherlands, United Kingdom; capacity-constrained markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile coffee-bean prices squeezing manufacturer margins

In December 2024, Arabica prices soared to USD 3.44 per pound, marking an 80% year-over-year surge. This spike was largely attributed to frost damage in Brazil, drought conditions in Vietnam, and speculative trading activities. Robusta prices mirrored this trend, hitting record highs. This surge in prices intensified input-cost pressures for manufacturers who typically blend both Arabica and Robusta to achieve a desired flavor profile while managing costs. In its October 2025 update, JDE Peet's highlighted the challenges, noting that green-coffee prices are "significantly elevated and increasingly volatile." This volatility has compelled the company to adopt disciplined pricing and productivity measures to safeguard its adjusted EBIT. Meanwhile, Nestlé's coffee category in Zone Europe implemented double-digit price increases in the first half of 2025 to counteract inflationary pressures. However, despite these hikes, the real internal growth remained stagnant, underscoring the sensitivity of volumes to price adjustments. Smaller coffee brands, lacking the hedging tools and purchasing clout of their multinational counterparts, find themselves at a disadvantage. They're more susceptible to margin squeezes or compelled retail price hikes, which can diminish their competitiveness against private-label options. Given the ongoing climate volatility, this cautious approach seems set to continue. The International Coffee Organization has even forecasted persistent supply deficits extending through 2026.

EU deforestation free traceability compliance costs

To comply with EUDR regulations, operators must invest in digital traceability platforms, third-party audits, and supplier training. These costs, ranging from EUR 50,000 to EUR 200,000 per operator based on supply-chain complexity and origin diversity, disproportionately impact smaller importers and roasters, as highlighted by a 2024 industry survey and the European Commission[1]Source: European Commission, “Deforestation-Free Supply Chains Brief,” europa.eu . For ready-to-drink (RTD) manufacturers blending flavors from diverse origins, the administrative challenges intensify. Take Spain, for instance: in 2023, it imported coffee from a diverse set of countries, including Vietnam, Brazil, and Colombia, showcasing the complexities of compliance, as noted by CBI, the Government of the Netherlands. In response, smaller brands might either steer clear of high-risk origins or streamline their suppliers, simplifying blends but risking a loss in taste differentiation. On the other hand, industry giants like Nestlé and JDE Peet's, who are already on the path to sourcing 100% responsibly, with JDE Peet's hitting 83.8% in 2023, are better positioned. They can absorb these compliance costs and leverage certification as a strategic advantage.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Soft Drink Type: Cold Brew Outpaces Iced Coffee Despite Smaller Base

In 2025, iced coffee captured 49.35% of the market, underscoring its widespread appeal and resonance with Europe's traditional preference for milk-forward, sweetened brews. Cold brew coffee, while a smaller player, is set to grow at an 7.82% CAGR through 2031, bolstered by its specialty positioning and the smoothness attributed to its low-acidity extraction. Nestlé debuted Nescafé Iced Lattes in multi-serve cartons in March 2025, aiming squarely at the at-home consumption market. Meanwhile, Lavazza rolled out a trio of iced coffee cans in June 2024, featuring a protein variant to tap into the growing functional demand. Cold brew's premium pricing, typically 20% to 30% higher than iced coffee, finds favor with urban millennials, who are willing to pay a premium for its craft credentials and reduced bitterness. Grind, a specialty roaster from the UK, broadened its cold-brew concentrate line in 2024-2025, focusing on single-origin offerings for cafes and retail.

While other ready-to-drink (RTD) coffee formats like nitro coffee, espresso shots, and flavored lattes cater to niche occasions, they collectively command a significant market share. In 2025, Emmi introduced a 230 ml decaffeinated CAFFÈ LATTE and a 650 ml resealable "Mr. Huge" variant, catering to late-evening consumers and those seeking multi-serve convenience. JDE Peet's inaugurated a Modular Innovation Lab in Utrecht in October 2025, equipped with dedicated RTD cold-brew production capabilities, signaling a clear intent to fast-track format innovation. The market segmentation reveals a clear divide: while mass-market iced coffee drives volume, it's the cold brew and specialty formats that are fueling value and margin growth. Brands face the challenge of balancing their portfolios, offering entry-level iced lattes to entice trials, while also featuring premium cold-brew SKUs that command higher retail prices and fend off private-label competition.

By Packaging Type: PET Gains on Glass as Sustainability and Convenience Converge

In 2025, glass bottles commanded a 35.10% market share, lauded for their premium appeal, inert nature, and perceived quality. Meanwhile, PET bottles are set to expand at a 7.65% CAGR through 2031, driven by trends like lightweighting, recyclability mandates, and consumer convenience. European Union regulations are pushing for a 30% recycled PET content by 2030 and ramping up to 65% by 2040. This has led brands to swiftly adopt food-grade rPET. Notably, Coca-Cola European Partners reached an impressive 63.2% rPET usage in Europe in 2024. Reusable PET bottles, designed for 15 to 25 cycles, are gaining traction as a circular substitute to single-use glass, boasting advantages like reduced weight and diminished transport emissions. Metal cans, though holding a smaller market share, enjoy stability thanks to Europe's impressive recycling rates, surpassing 70%. Additionally, innovations like new water-based, BPA-free coatings, as highlighted by Canmakers UK, are alleviating food-safety concerns.

Aseptic packages, predominantly Tetra Pak and SIG cartons, are revolutionizing distribution. They allow for ambient storage and extended shelf life sans preservatives, a boon for convenience stores and vending machines. Tetra Pak's 2024 foray into paper-based barriers and certified recycled polymers underscores a commitment to circularity. Their push for 360-degree printability further elevates premium branding. However, disposable cups, a staple in on-trade settings, are grappling with regulatory challenges. The EU Packaging Regulation is steering the industry: it mandates that by 2030, 10% of on-premise consumption should utilize reusable packaging, escalating to 40% by 2040. This shift is nudging cafes and restaurants towards refillable systems. As the industry pivots, PET and aseptic formats emerge as frontrunners, striking a balance between sustainability, cost, and consumer convenience. Meanwhile, glass bottles carve out a niche, remaining the go-to for specialty items and gifting occasions.

By Functionality: Energy-Infused Dominates, Protein-Enriched Carves Niche

In 2025, energy-infused RTD coffee dominated the functionality segment, capturing 68.85% market share and projecting an 7.88% CAGR. This growth mirrors a crossover trend, with energy-drink aficionados gravitating towards coffee-based alternatives, drawn by the familiar caffeine kick. Partnerships between Monster Beverage and PepsiCo, alongside Celsius's foray into Europe, have mainstreamed functional beverages, casting a favorable light on coffee-centric energy drinks. Brands are emphasizing caffeine transparency, often spotlighting 150 to 200 mg per serving, and bolstering their energy claims with additions like B vitamins, taurine, or guarana. This segment resonates with shift workers, students, and fitness buffs, who prioritize effectiveness over subtle taste variations.

While protein-enriched RTD coffee occupies a smaller niche, it's on the rise as brands zero in on post-workout recovery and meal-replacement scenarios. In June 2024, Starbucks unveiled three protein-packed coffee drinks, each boasting 20 grams of protein and no added sugar, with distribution through Asda, Tesco, and Morrisons. Lavazza followed suit, launching its protein-infused iced coffee can in June 2024, merging the realms of coffee and functional nutrition. In July 2024, Arla Foods poured USD 29 million into its Esbjerg, Denmark facility, ramping up protein-beverage production to cater to brands like Starbucks and Cocio Stack3d. The "Others" category in functionality encompasses decaffeinated, low-calorie, and adaptogen-infused variants, catering to evening drinkers, weight watchers, and wellness enthusiasts. Notably, decaffeinated coffee made up 20% of Spain's total coffee consumption in 2021, hinting at a burgeoning appetite for decaf RTD options, as highlighted by CBI, a Dutch government agency. While functionality segmentation allows brands to command premium prices and secure multiple shelf spaces, it necessitates clear on-pack messaging to rationalize the price difference from standard RTD coffee.

By Distribution Channel: On-Trade Gains as Operators Seek Labor Efficiency

In 2025, off-trade channels, including supermarkets, hypermarkets, convenience stores, specialty stores, and online retail, captured a 62.30% market share, buoyed by impulse buys, promotional efforts, and the allure of private labels. Supermarkets and hypermarkets lead the charge, with Spain's top five chains, Mercadona, Carrefour, Lidl, Eroski, and DIA, jointly accounting for over half of the nation's grocery sales. In the UK and the Netherlands, convenience stores cater to commuters and urban dwellers, pushing high-margin single-serve SKUs. Meanwhile, online retail, boasting a global growth rate of 16% CAGR, entices with subscription and bulk-purchase deals. Notably, Nestlé highlighted the significance of e-commerce, attributing 20.2% of its Group sales in H1 2025 to this channel.

On-trade channels, encompassing cafes, restaurants, hotels, and foodservice, are set to grow at the fastest pace among distribution segments, with an anticipated CAGR of 8.54% through 2031. In a strategic move, Coca-Cola Hellenic Bottling Company expanded its reach by adding 5,000 outlets in 2023, bringing its total to 13,000, by providing ready-to-drink (RTD) coffee to cafes aiming to streamline labor and ensure consistent quality. Coca-Cola European Partners, catering to over 4 million customers outside the home, is bolstering its RTD coffee ambitions by investing in aseptic filling lines. Looking ahead, EU HORECA's refill and reuse mandates, set to kick in between 2027 and 2028, will push operators to provide reusable packaging for a tenth of on-premise consumption by 2030. This shift could tilt the scales in favor of RTD formats, especially in returnable glass or refillable PET. The on-trade's expansion signals a broader transformation: operators are opting for the predictability of RTD costs over the unpredictability of barista wages and equipment upkeep. In turn, consumers are embracing the convenience of RTDs, finding them more wallet-friendly than traditional handcrafted espresso drinks. While specialty stores and other channels, like vending and travel retail, cater to niche demands, their collective contribution to volume is significant.

Geography Analysis

The UK accounted for 37.10% of Europe's demand for ready-to-drink (RTD) coffee. This dominance is driven by the UK's mature adoption of cold brews, a dense network of convenience stores, and a strong presence of private-label brands. In the three months leading up to 2024, 16% of UK consumers bought RTD coffee, primarily driven by convenience. Major brands, including Starbucks, Lavazza, Alpro, and Marks & Spencer, launched new products like protein drinks and cold-brew oat lattes, predominantly in the UK, showcasing retailers' commitment to innovative offerings. Nestlé's investment of GBP 28 million (USD 35 million) in its Dalston, Cumbria factory in 2024, aimed at boosting frothy coffee sachet production, underscores its confidence in the UK's coffee demand. While Germany, France, and the Netherlands boast significant volumes, their growth is hindered by established home-brewing traditions and a competitive landscape dominated by price-sensitive private labels, especially in Germany's discount-driven grocery market.

Italy is set to spearhead geographic growth with a projected 7.03% CAGR through 2031. This surge is fueled by Italy's rich espresso culture, 75% of adults indulge in daily coffee, and a 15% hike in cafe prices over three years, nudging consumers towards more portable coffee formats. As Europe's second-largest green coffee importer and home to major roasters like Lavazza and Illy, Italy enjoys inherent supply-chain advantages and brand credibility for its RTD launches. A 2024 joint venture between Coca-Cola and Illy aims at the premium RTD coffee segment, capitalizing on Illy's esteemed Italian legacy and Coca-Cola's expansive distribution. While 95% of Spanish adults consume coffee, and 20% opt for decaffeinated, the country's 43% retail share of private labels pressures branded pricing. Yet, this landscape hints at a burgeoning demand for functional and decaf RTD formats. Meanwhile, Poland, Belgium, and Sweden, though smaller markets, are experimenting with cold brews and expanding specialty cafes. Eastern markets, where instant coffee reigns supreme but disposable incomes are on the rise, remain fragmented but promising.

Spain's coffee eCommerce market, forecasted to hit USD 93.9 million in 2025 and expand at a 12.2% CAGR through 2029, highlights the digital potential for RTD subscriptions and bulk buys. The country's 59% share of Robusta imports, outpacing the EU's 36% average, underscores a cost sensitivity that leans towards value-priced RTD offerings. A closer look at geographic segmentation reveals distinct opportunities: the UK and Germany maintain their volume through established retail channels and rapid innovation, while Italy and Spain, rooted in a rich coffee culture, are poised for premiumization and growth. Emerging markets like Poland and Belgium present a golden opportunity for early entrants to cultivate brand loyalty before the competition heats up.

Competitive Landscape

The Europe ready-to-drink coffee market is moderately consolidated, with multinational giants like Nestlé, PepsiCo, Coca-Cola, JDE Peet's, and Danone leveraging their brand portfolios, expansive distribution networks, and co-packing partnerships to secure a dominant foothold. In H1 2025, Nestlé celebrated "very strong growth" in its European RTD coffee segment, buoyed by double-digit price hikes and a marketing push that saw investments soar to 8.6% of sales. JDE Peet's, grappling with surging green-coffee prices, funneled EUR 5 million into its Kostinbrod plant in Bulgaria in 2024, boosting roasting and packaging capacity by 25% to cater to 18 European markets. Keurig Dr Pepper's ambitious USD 18 billion bid for JDE Peet's, unveiled in August 2025 and set to finalize in H1 2026, promises to redefine Europe's distribution landscape and brand lineup, with a spotlight on consolidating RTD innovations under flagship labels like L'Oréal, Jacobs, and Peet's. In a strategic move, Coca-Cola and Illy have joined forces, harnessing Illy's esteemed Italian legacy and Coca-Cola's vast distribution prowess to carve a niche in the premium RTD coffee arena.

There's a burgeoning demand for functional RTD variants, think decaffeinated, protein-boosted, or adaptogen-infused options, catering to evening drinkers, post-workout enthusiasts, and wellness aficionados, yet these remain largely untapped by mainstream iced coffee and cold brew offerings. Smaller players, such as the UK's Grind and GoodBrew, fresh off a crowdfunding boost for their UK expansion in December 2024, are sidestepping traditional supermarket hurdles. They're doing this by forging direct-to-consumer pathways, subscription services, and cafe collaborations. Technology is rapidly reshaping the landscape: JDE Peet's inaugurated a Modular Innovation Lab in Utrecht in October 2025, equipped with cold-brew production, freeze-drying tech, and eco-friendly packaging trials, all aimed at speeding up market entry and swift SKU adjustments.

Aseptic-filling capabilities have emerged as a key competitive edge, underscored by Tetra Pak's hefty EUR 100 million investment in European Centres of Excellence in 2024, bolstering the stronghold of established players. Meanwhile, supermarket chains like Mercadona, Carrefour, and Lidl are ramping up their private-label offerings, intensifying market competition. This surge pushes branded entities into a tight spot: either they align their prices, risking profit margins, or they channel resources into premiumization and innovation, seeking to validate their brand's premium pricing.

Europe Ready-To-Drink Coffee Industry Leaders

Nestlé SA

Starbucks Corp.

The Coca-Cola Company

Arla Foods amba

PepsiCo Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Kerry acquired a manufacturing facility in Bethlehem, Pennsylvania, specializing in coffee roasting and extraction, upgrading assets to support natural, high-quality coffee flavors and ingredients across beverage, dairy, and foodservice applications. The investment advances coffee extraction technology and accelerates innovation pipelines, with implications for RTD coffee ingredient supply in Europe and North America.

- October 2025: JDE Peet's opened a fully renovated Modular Innovation Lab in Utrecht, Netherlands, a global research and development center with RTD cold-brew production capabilities, capsule filling machines, freeze-drying systems, and sustainable packaging prototypes. The EUR 8 million investment (including a separate Joure facility) aims to accelerate product development and rapid deployment across JDE Peet's manufacturing network.

- August 2025: Keurig Dr Pepper announced a USD 18 billion acquisition of JDE Peet's, creating a global coffee powerhouse. The transaction, expected to close in H1 2026, subject to regulatory approvals, will consolidate RTD coffee innovation, distribution, and brand portfolios across North America and Europe.

Europe Ready-To-Drink Coffee Market Report Scope

Cold Brew Coffee, Iced coffee are covered as segments by Soft Drink Type. Aseptic packages, Glass Bottles, Metal Can, PET Bottles are covered as segments by Packaging Type. Off-trade, On-trade are covered as segments by Distribution Channel. Belgium, France, Germany, Italy, Netherlands, Russia, Spain, Turkey, United Kingdom are covered as segments by Country.Soft Drink Type

| Cold Brew Coffee |

| Iced Coffee |

| Other RTD Coffee |

Packaging Type

| PET Bottles |

| Glass Bottles |

| Metal Can |

| Aseptic packages |

| Disposable Cups |

Functionality

| Protein-Enriched |

| Energy-Infused |

| Others |

Distribution Channel

| On-Trade | |

| Off-Trade | Supermarket/Hypermarket |

| Convenience Stores | |

| Specialty Stores | |

| Online Retail | |

| Other Distribution Channels |

Geography

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Netherlands |

| Poland |

| Belgium |

| Sweden |

| Rest of Europe |

| Soft Drink Type | Cold Brew Coffee | |

| Iced Coffee | ||

| Other RTD Coffee | ||

| Packaging Type | PET Bottles | |

| Glass Bottles | ||

| Metal Can | ||

| Aseptic packages | ||

| Disposable Cups | ||

| Functionality | Protein-Enriched | |

| Energy-Infused | ||

| Others | ||

| Distribution Channel | On-Trade | |

| Off-Trade | Supermarket/Hypermarket | |

| Convenience Stores | ||

| Specialty Stores | ||

| Online Retail | ||

| Other Distribution Channels | ||

| Geography | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

Market Definition

- Carbonated Soft Drinks (CSDs) - Carbonated soft drinks (CSDs) refer to non-alcoholic beverages that are carbonated and typically flavored, containing dissolved carbon dioxide to create effervescence. These beverages commonly include cola, lemon-lime, orange, and various fruit-flavored sodas. Marketed in cans, bottles, or fountain dispense.

- Juices - We have considered packaged juices which encompass non-alcoholic beverages derived from fruits, vegetables, or a combination thereof, processed and sealed in various packaging formats such as bottles, cartons, or pouches. Excluding fresh juices, this market segment involves commercially prepared and preserved juices, often with added preservatives and flavors.

- Ready-to-Drink (RTD) Tea and RTD Coffee - Ready-to-Drink (RTD) tea and RTD coffee are pre-packaged, non-alcoholic beverages that are brewed and prepared for consumption without further dilution. RTD tea typically includes various tea varieties, infused with flavors and sweeteners, and comes in bottles, cans, or cartons. Similarly, RTD coffee involves pre-brewed coffee formulations, often mixed with milk, sugar, or flavorings, and is conveniently packaged for on-the-go consumption.

- Energy Drinks - Energy drinks are non-alcoholic beverages formulated to provide a quick boost of energy and alertness. Whereas, sports drinks are beverages designed to hydrate and replenish electrolytes, particularly after physical exertion, exercise, or intense activity

| Keyword | Definition |

|---|---|

| Carbonated Soft Drinks | Carbonated soft drinks (CSDs) are a combination of carbonated water and flavouring, sweetened by sugar or a non-sugar sweeteners. |

| Standard Cola | Standard Cola is defined as the original flavor of cola soda. |

| Diet Cola | A cola-based soft drink containing no or low amounts of sugar |

| Fruit Flavored Carbonates | A carbonated beverage prepared from fruit juice/fruit flavor with carbonated water and containing sugar, dextrose, invert sugar or liquid glucose either singly or in combination. It may contain peel oil and fruit essences. |

| Juice | Juice is a drink made from the extraction or pressing of the natural liquid contained in fruit and vegetables. |

| 100% Juice | Fruit/vegetable juice made from fruit in the form of its juice with no water added to make up the volume. It is not permitted to add sugars, sweeteners, preservatives, flavourings or colourings to fruit juice. |

| Juice Drinks (up to 24% Juice) | Fruit/vegetable juice drinks with up to 24% fruits/vegetable extract. |

| Nectars (25-99% Juice) | Juices that can have between 25 and 99% of fruit, with the minimum legal limits defined depending on the type of fruit |

| Juice concentrates | Juice Concentrates are those form of juices when most of this liquid is removed resulting in a thick, syrupy product known as juice concentrate. |

| RTD Coffee | Packaged coffee beverages that are sold in a prepared form and are ready for consumption at the time of purchase. |

| Iced Coffee | An iced coffee is a cold version of coffee, usually a combination of hot espresso and milk with ice added to it. |

| Cold Brew Coffee | Cold brew also called cold water extraction or cold pressing is made by steeping ground coffee in room-temperature water for several hours. |

| RTD Tea | Ready-to-drink (RTD) tea is a packaged tea product ready for immediate consumption without brewing or preparation |

| Iced Tea | Ice tea or iced tea is a drink made from tea without milk but with sugar and sometimes fruit flavourings, drunk cold. |

| Green Tea | Green tea is a tea beverage which promotes mental alertness, relieving digestive symptoms and promoting weight loss. |

| Herbal Tea | Herbal tea beverages are made from the infusion or decoction of herbs, spices, or other plant material in hot water. |

| Energy Drink | A type of drink containing stimulant compounds, usually caffeine, which is marketed as providing mental and physical stimulation. They may or may not be carbonated and may also contain sugar, other sweeteners, or herbal extracts, among numerous possible ingredients. |

| Sugar-free or Low-calories Energy Drinks | Sugar-free or Low-calories Energy Drinks are sugar-free, artificially sweetened energy drinks with few or no calories. |

| Traditional Energy Drink | Traditional Energy Drinks are functional soft drinks containing ingredients designed to boost the consumer's energy. |

| Natural/Oraganic Energy Drinks | Natural/Organic energy drinks are energy drinks free of artificial sweeteners and synthetic colorings. Instead, they contain naturally derived ingredients such as green tea, yerba mate, and botanical extracts. |

| Energy Shots | A small but highly concentrated energy drink that contains large amounts of caffeine and/or other stimulants. The quantity is comparatively smaller compared to energy drinks. |

| Sports Drink | Sports drinks are beverages designed specifically for the rapid supply of fluid, carbohydrates, and electrolytes before, during or after exercise. |

| Isotonic | Isotonic drinks contain similar concentrations of salt and sugar as in the human body, and are designed to quickly replace fluids lost during exercise but with an increase of carbohydrate. |

| Hypertonic | Hypertonic drinks have a higher concentration of salt and sugar than the human body. They are best drunk after exercise as it is important to replace glycogen levels quickly after exercise. |

| Hypotonic | Hypotonic drinks are designed to quickly replace fluids lost during exercise. They have very low carbohydrate content and a lower concentration of salt and sugar than the human body. |

| Electrolyte-Enhanced Water | Electrolyte water is water infused with electrically-charged minerals, such as sodium, potassium, calcium, and magnesium. |

| Protein-based Sport Drinks | Protein-based sports drinks are those sports drinks which has added protein in it that will improve performance and reduce muscle protein breakdown. |

| On-Trade | The on-trade refers to places that sell beverages for immediate consumption on the premises like bars, restaurants, and pubs |

| Off-Trade | Off-trade usually means places like liquor stores, supermarkets and other places where you don't consume the beverage right away. |

| Convenience Store | A retail business that provides the public with a convenient location to quickly purchase a wide variety of consumable products and services, generally food and gasoline. |

| Specialty store | A specialty store is a shop/store that carries a deep assortment of brands, styles, or models within a relatively narrow category of goods |

| Online Retail | Online retail is a type of eCommerce whereby a business sells goods or services directly to consumers from a website. |

| Aseptic Packaging | Aseptic packaging refers to the filling of a cold, commercially sterile product under sterile conditions into a presterilized container and closure under sterile conditions to form a seal that effectively excludes microorganisms. These includes tetra packs, cartons, pouches etc. |

| PET Bottle | PET bottle means a bottle made of polyethylene terephthalate. |

| Metal Cans | Metal containers made of aluminum or tin- plated or zinc-plated steel, which are commonly used for packaging food, beverages or other products. |

| Disposable Cups | Disposable Cup means a cup or other container designed for single use to serve beverages, such as water, cold drinks, hot drinks and alcoholic beverages. |

| Gen Z | A way of referring to the group of people who were born in the late 1990s and early 2000s. |

| Millenial | Anyone born between 1981 and 1996 (ages 23 to 38 in 2019) is considered a Millennial |

| Taurine | Taurine is an amino acid that supports immune health and nervous system function. |

| Bars & Pubs | It is a drinking establishment licensed to serve alcoholic drinks for consumption on the premises. |

| Café | It is a foodservice establishment serving refreshments (mainly coffee) and light meals. |

| On the go | It means doing / dealing with while busily engaged with something and not diverting plans in order to accommodate. |

| Internet Penetration | The Internet Penetration Rate corresponds to the percentage of the total population of a given country or region that uses the Internet. |

| Vending Machine | A machine that dispenses small articles such as food, drinks, or cigarettes when a coin or token is inserted |

| Discount store | A discount store or discounter offers a retail format in which products are sold at prices that are in principle lower than an actual or supposed "full retail price". Discounters rely on bulk purchasing and efficient distribution to keep down costs. |

| Clean Label | Clean label on the beverage market are drinks that are made from few ingredients of natural origin and are not or only slightly processed. |

| Caffeine | An alkaloid compound which is a stimulant of the central nervous system. It is mainly used recreationally, as a mild cognitive enhancer to increase alertness and attentional performance. |

| Extreme sport | Action sports, adventure sports or extreme sports are activities perceived as involving a high degree of risk. |

| High-intensity interval training | It incorporates several rounds that alternate between several minutes of high intensity movements to significantly increase the heart rate to at least 80% of one's maximum heart rate, followed by short periods of lower intensity movements. |

| Shelf life | The length of time for which an item remains usable, fit for consumption, or saleable. |

| Cream Soda | Cream soda is a sweet soft drink. Generally flavored with vanilla and based on the taste of an ice cream float |

| Root Beer | Root beer is a sweet North American soft drink traditionally made using the root bark of the sassafras tree Sassafras albidum or the vine of Smilax ornata as the primary flavor. Root beer is typically, but not exclusively, non-alcoholic, caffeine-free, sweet, and carbonated. |

| Vanilla Soda | A carbonated soft drink flavoured with vanilla. |

| Dairy-Free | A product that does not contain any milk or milk products from cows, sheep or goats. |

| Caffeine-Free Energy Drinks | Caffeine-free energy drinks rely on other ingredients to boost the energy. Popular choices include amino acids, B vitamins, and electrolytes. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated reports, custom consulting assignments, databases & subscription platforms