Europe Professional Audio Video (ProAV) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

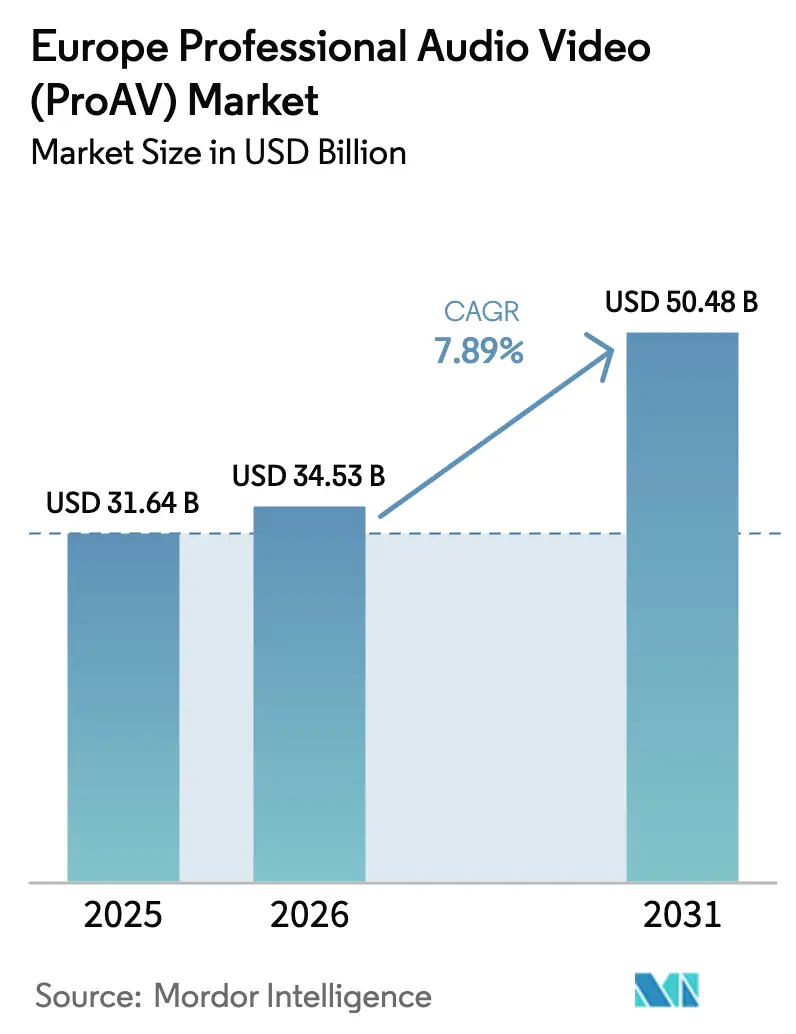

| Base Year Market Size (2025) | USD 31.64 Billion |

| Market Size (2026) | USD 34.53 Billion |

| Market Size (2031) | USD 50.48 Billion |

| Growth Rate (2026 - 2031) | 7.89% CAGR |

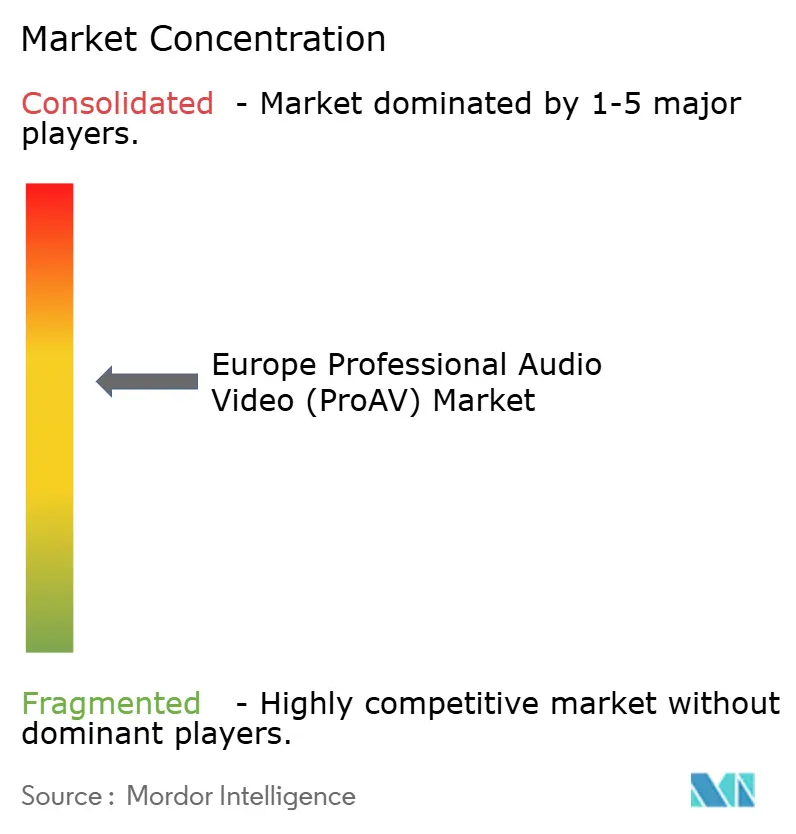

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Professional Audio Video (ProAV) Market Analysis by Mordor Intelligence

The Europe Professional Audio Video Market size is projected to expand from USD 31.64 billion in 2025 and USD 34.53 billion in 2026 to USD 50.48 billion by 2031, registering a CAGR of 7.89% between 2026 to 2031. The expansion is underpinned by hybrid-work mandates that concentrate technology budgets on fewer yet higher-specification collaboration rooms, an accelerated rollout of networked digital signage across retail and transit hubs, and the transition from analog or proprietary signal chains to IP-based architectures that lower vendor lock-in while enabling remote device management. Enterprises are retiring power-intensive legacy gear ahead of the usual replacement cycle because EU ecodesign regulations favor low-consumption displays and amplifiers, while integrated AI functions, such as real-time transcription, speaker tracking, and spatial audio, are shifting value from standalone processors to smart endpoints. At the same time, channel dynamics are evolving: systems integrators remain influential in complex, multi-site deployments, yet e-commerce portals are gaining traction for commoditized cameras, video bars, and AV-over-IP switches as buyers prioritize transparent pricing and rapid delivery. Heightened cybersecurity scrutiny under the NIS2 Directive is prompting integrators to bundle managed security services with firmware updates and vulnerability audits, supporting the premium that services command over hardware in new contracts.

Key Report Takeaways

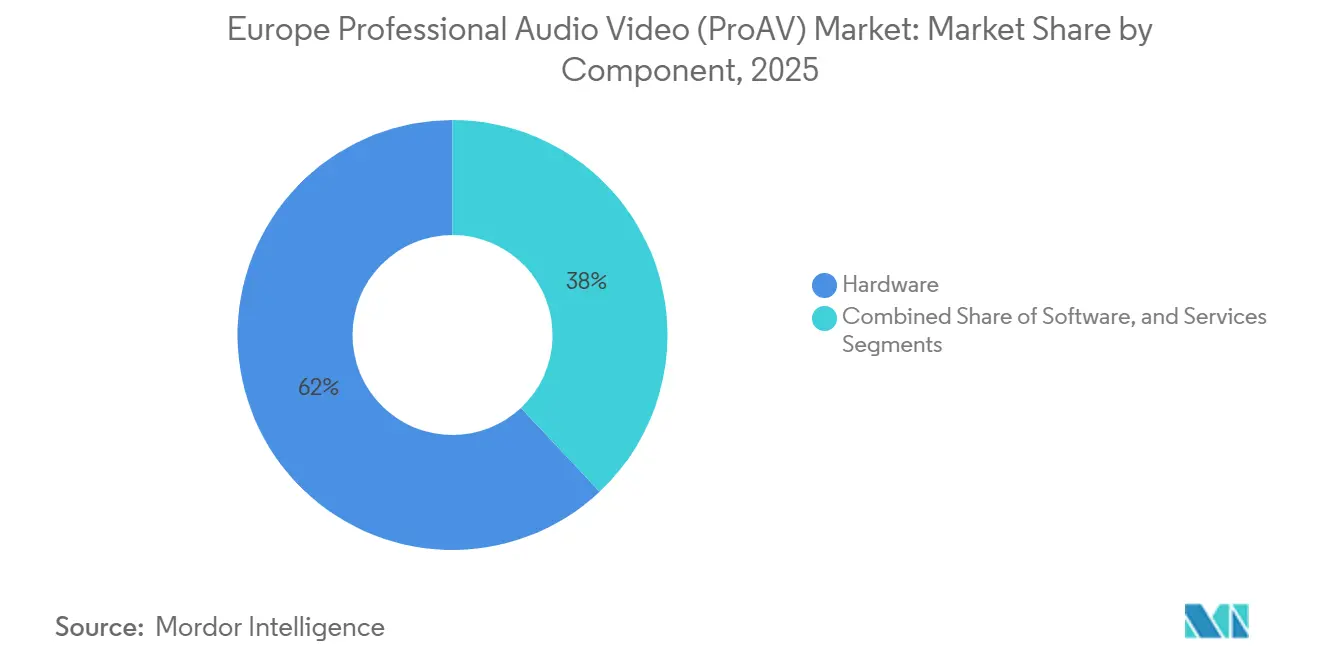

- By component, hardware commanded 62% of revenue in 2025, and services are accelerating at a 10.40% CAGR through 2031.

- By solution category, video displays and projection held 28.50% of the Europe professional audio-video market share in 2025, and unified communication and collaboration solutions are advancing at a 12.90% CAGR to 2031.

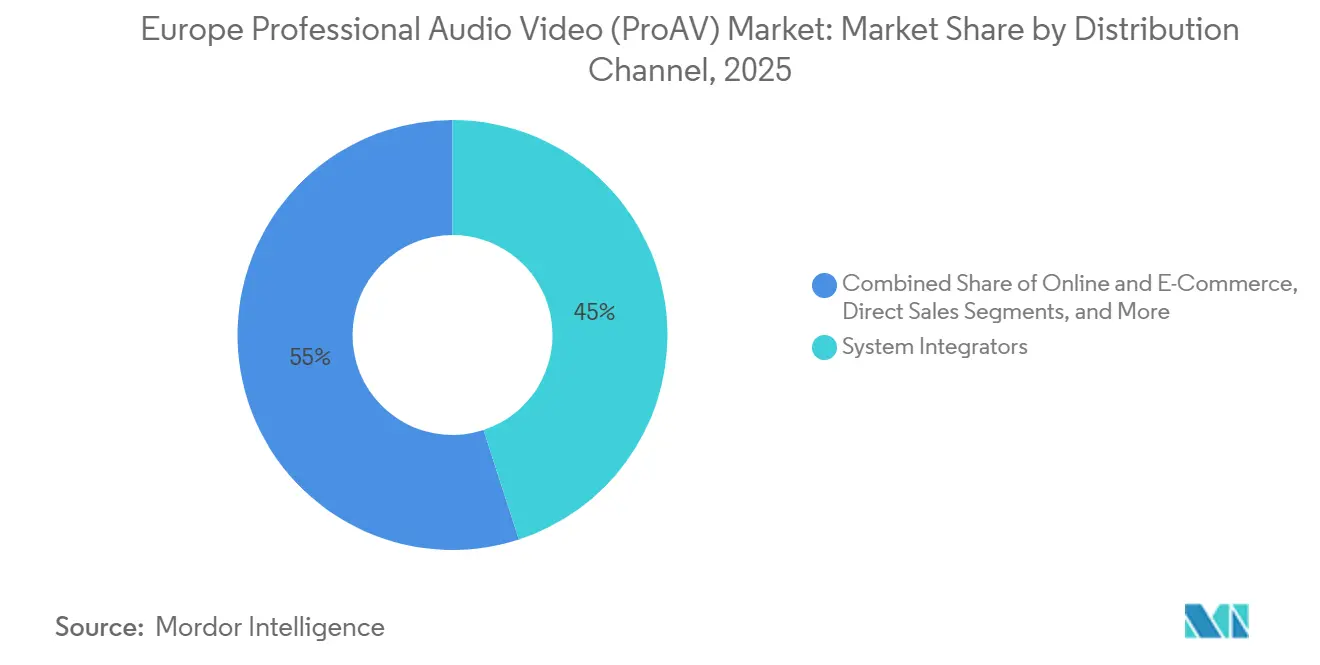

- By Distribution Channel, Direct Sales held 41.04% of the Europe ProAV market share in 2025, and Online and E-Commerce is advancing at an 11.5% CAGR to 2031.

- By end-user industry, corporate buyers accounted for 30.40% of demand in 2025 in the Europe ProAV market, and education is expanding at an 11.70% CAGR through 2031.

- By geography, Germany led with 25.10% revenue share in 2025, and Italy is forecast to achieve an 8.60% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Professional Audio Video (ProAV) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Hybrid Work and Collaboration Ecosystems Across Enterprises | +2.10% | Germany, France, United Kingdom, Benelux, Southern Europe | Medium term (2-4 years) |

| Rapid Proliferation of Digital Signage in Retail and Transportation Hubs | +1.50% | Germany, France, Spain, Italy (metro areas and airports) | Short term (≤ 2 years) |

| UHD Content Consumption Fuelling Upgrade Cycle for Projection and Display Hardware | +1.30% | United Kingdom, Germany, France | Medium term (2-4 years) |

| Transition to Open Standards Like AV-over-IP Reducing Vendor Lock-in | +1.20% | Germany, United Kingdom, Netherlands | Long term (≥ 4 years) |

| Rising Adoption of Immersive Audio for Esports Arenas and Virtual Event Venues | +0.80% | France, Spain, Germany | Medium term (2-4 years) |

| EU Energy-Efficiency Directives Accelerating Replacement of Legacy AV Gear With Low-Power Solutions | +0.90% | EU-wide, strongest in Germany, France, Netherlands | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Hybrid Work and Collaboration Ecosystems Across Enterprises

More than one-half of EU companies supported remote meeting capabilities in 2024, up from less than one-third before 2020, signaling a structural redesign of real-estate footprints toward technology-rich collaboration rooms. Organizations are reallocating budgets from large office leases to unified communication suites that combine 4K cameras, beamforming microphones, and AI transcription tools, elevating employee experience and productivity. Investment momentum is visible in vendor performance: Logitech’s video collaboration revenue grew 9% year-over-year to USD 614 million during its October-December 2024 quarter, and continued device certification for Microsoft Teams Rooms and Zoom Rooms is lowering integration risk for buyers. Hybrid work thus acts as a flywheel, boosting endpoint refresh cycles, software subscriptions, and remote management services in the Europe professional audio video market.

Rapid Proliferation of Digital Signage in Retail and Transportation Hubs

European retailers and transit authorities are swapping static posters for networked LED walls that deliver targeted promotions, real-time wayfinding, and higher advertising yields. LG demonstrated transparent OLED storefront panels at CES 2024, enabling immersive overlays without blocking sightlines.[1]LG Electronics, “Transparent OLED at CES 2024,” LG.COM Samsung’s modular MicroLED Wall All-in-One, launched in January 2024, integrates onboard processing to simplify installation where space or cooling limits conventional video walls.[2]Samsung Electronics, “The Wall All-in-One IAW 2024,” SAMSUNG.COM Centralized, cloud-based content management lets operators schedule campaigns across hundreds of locations, cutting labor costs and permitting data-driven A/B tests. Airports, metro systems, and shopping centers use the same infrastructure for safety messaging, generating recurring demand for ruggedized screens, media players, and analytics software across the Europe professional audio video market.

UHD Content Consumption Fueling Upgrade Cycle for Projection and Display Hardware

Streaming platforms, live sports, and enterprise e-learning assets are increasingly produced in 4K or 8K, rendering older HD-only systems obsolete in visually intensive workflows. Sony released its BVM-HX1710 4K OLED monitor for live production in September 2024 to satisfy broadcasters’ color-critical needs. Barco added HDR-capable cinema projectors in April 2024, raising the bar on brightness and dynamic range for premium auditoriums. Corporate meeting rooms and university lecture theaters now specify 4K flat panels to display dense spreadsheets or medical imagery without zooming, accelerating replacement demand for high-resolution displays and compatible distribution hardware in the Europe ProAV market.

Transition to Open Standards Like AV-over-IP Reducing Vendor Lock-in

IPMX, Dante, and SMPTE ST 2110 allow audio, video, and control data to traverse standard Ethernet, eliminating expensive matrix switchers and proprietary cabling. Audinate reports more than 4,000 Dante-enabled product models as of 2024, expanding buyers’ ability to mix and match brands without compromising functionality. Interoperability improves price transparency, and built-in remote management aligns AV assets with IT service practices. As a result, procurement teams increasingly consider total cost of ownership rather than headline hardware price, reinforcing the migration toward IP workflows across the Europe ProAV market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cybersecurity and Privacy Threats in Networked AV Systems | -1.10% | Germany, France, Netherlands (NIS2 high scrutiny) | Short term (≤ 2 years) |

| High Initial Capital Expenditure Amid Macroeconomic Uncertainty | -0.90% | Southern Europe, United Kingdom | Short term (≤ 2 years) |

| Semiconductor Supply Instability Curbing Hardware Availability | -0.60% | Germany, France (manufacturing hubs) | Medium term (2-4 years) |

| Growing Environmental Scrutiny of E-Waste in AV Hardware Lifecycle | -0.50% | EU-wide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cybersecurity and Privacy Threats in Networked AV Systems

Embedding AV devices on corporate LANs exposes cameras, microphones, and control processors to ransomware, eavesdropping, and unauthorized access, risks heightened by the NIS2 Directive’s mandatory cybersecurity controls for large enterprises.[3]European Union Agency for Cybersecurity, “Threat Landscape 2024,” ENISA.EUROPA.EU ENISA’s 2024 threat-landscape report flagged compromised video-conferencing endpoints as a vector for corporate espionage, prompting IT teams to enforce network segmentation, certificate authentication, and timely patching. System integrators now wrap projects with managed detection and response services, but the added 15%-25% cost strains price-sensitive public-sector and SME budgets, tempering uptake in parts of the Europe professional audio video market.

High Initial Capital Expenditure Amid Macroeconomic Uncertainty

A fully equipped 4K hybrid meeting room can exceed USD 25,000, while large auditoriums require six-figure investments that many organizations defer amid inflation and rising interest rates. Although Italy’s National Recovery and Resilience Plan allocates EUR 191.5 billion (USD 206.8 billion) to digital transformation, competing healthcare and energy priorities dilute immediate AV outlays, especially for municipalities and smaller universities. Subscription-based AV-as-a-service offers smoother cash flow, but adoption is slow because lessors are cautious about technology obsolescence risk, keeping some demand sidelined in the Europe ProAV market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Outpace Hardware on Managed-Offering Shift

Hardware delivered 62% of 2025 revenue due to the cost of displays, projectors, cameras, microphones, and control processors that form the backbone of ProAV installations. Services revenue is rising at a 10.40% CAGR as enterprises prefer predictable operating expenses and end-to-end accountability for uptime. System integrators bundle remote monitoring, firmware updates, and cybersecurity audits into multi-year contracts, monetizing network operations centers that predict failures before they disrupt meetings. Software platforms, from content management to analytics dashboards, add stickiness by measuring room utilization and device health, supporting incremental upsells. The hardware mix is polarizing: commoditized USB peripherals compete on price, while premium endpoints integrate AI auto-framing or beamforming that justify longer replacement cycles and higher margins. Managed offerings resonate in verticals with scarce in-house expertise such as healthcare, hospitality, and retail, driving sustained growth in the services slice of the Europe ProAV market.

Services also mitigate supply-chain volatility by decoupling customer satisfaction from pure hardware availability. Integrators can swap functionally equivalent devices when chip shortages delay specific models, maintaining SLA compliance. Meanwhile, software subscriptions expand their role in environmental sustainability by triggering automated power-down or lighting adjustments via links to building-management systems. These efficiencies reinforce the business case for services, which are forecast to narrow the revenue gap with hardware beyond 2030 within the Europe professional audio video market.

By Solution Category: Unified Communication Platforms Eclipse Traditional Displays

Video displays and projection accounted for a 28.50% share in 2025, anchored by the omnipresence of large-format screens in meeting rooms, lecture halls, and retail venues. However, unified communication and collaboration kits are advancing at a 12.90% CAGR as pre-certified bundles reduce integration risk and accelerate deployment. Manufacturers ship 4K cameras, microphone arrays, and compute modules as a single SKU that IT teams can deploy in under an hour, shrinking labor costs and downtime. Capture and production equipment is also benefitting from hybrid-event demand; PTZ cameras with NDI or SRT support slot directly into streaming workflows without external encoders, boosting margin-rich sales to venues and broadcasters.

Streaming, storage, and distribution tools enable on-demand access to recorded meetings and training sessions, cultivating secondary revenue through corporate learning platforms. Audio innovations remain central: Dante-enabled ceiling microphones auto-calibrate to room acoustics, while full-range line-array speakers deliver intelligibility in acoustically challenging halls. Software-defined control systems leverage commodity tablets rather than proprietary touch panels, extending flexibility. As buyers gravitate toward integrated user experiences, modular LED walls and immersive audio rigs increasingly anchor flagship deployments, creating a hierarchy of premium showcases that lift the Europe professional audio video market size associated with experiential solutions.

By Distribution Channel: E-Commerce Disrupts Integrator Dominance

System integrators retained 45% of distribution in 2025, reflecting their value in multi-room design, certification, and commissioning. Yet online marketplaces are expanding at an 11.5% CAGR, particularly among SMEs that purchase video bars, USB DSPs, and HDMI extenders directly after reviewing peer feedback. Amazon Business, CDW, and specialist portals publish spec comparisons and compatibility guides, eroding information asymmetry. Value-added resellers occupy the middle ground, bundling hardware with software keys and light configuration for clients requiring more support than pure e-commerce but less complexity than enterprise-scale integration.

Direct sales remain essential for strategic accounts seeking volume pricing, extended warranties, or co-designed firmware features. Retail outlets serve prosumers equipping home studios and very small businesses. Subscription-based AV-as-a-service blurs channel lines: integrators, resellers, and even manufacturers now offer monthly bundles, aligning incentives around uptime rather than one-off margins. As price transparency rises, integrators differentiate through vertical expertise, managed services, and compliance consulting, preserving their share in highly regulated sectors across the Europe professional audio video market.

By End-User Industry: Education Modernization Outpaces Corporate Refresh

Corporate buyers generated 30.40% of demand in 2025 in the Europe ProAV market as hybrid-work policies embedded collaboration technology into workplace design. Education, however, is the fastest-growing vertical, expanding at an 11.70% CAGR on the back of Italy’s School 4.0 allocation of EUR 2.1 billion (USD 2.27 billion) for approximately 100,000 classrooms and 40,000 buildings. EU connectivity grants totaling EUR 323 million (USD 348.8 million) in 2024 further underpin bandwidth-intensive applications such as live streaming of lectures. Universities install 4K PTZ cameras and interactive flat panels to serve blended cohorts, while K-12 institutions prioritize all-in-one displays that displace projector-plus-whiteboard combos.

Venues and events follow closely, with esports arenas and corporate conventions embracing modular LED walls and immersive sound systems that promise rapid scene changes. Media and entertainment facilities transition to IP production pipelines supporting remote contribution, while retail focuses on experiential signage. Healthcare adopts telemedicine carts and surgical displays, though long procurement cycles temper near-term volumes. Government agencies retrofit council chambers with streaming-ready AV to satisfy transparency mandates. Transportation hubs deploy passenger-information displays integrated with public-address audio. Collectively, these segments illustrate how vertical-specific drivers tilt investment timing and technology mix within the Europe professional audio video market.

Geography Analysis

Germany secured 25.10% of 2025 revenue, leveraging its manufacturing base, dense integrator network, and stringent quality standards. Federal and regional governments fund Industry 4.0 projects and public-sector hybrid-meeting upgrades, sustaining demand even amid macro headwinds. Data privacy and cybersecurity priorities encourage on-premises management and encrypted transport solutions, favoring premium vendors with robust security stacks. France, the United Kingdom, and Spain each contribute sizable volumes. France draws on the EUR 54 billion (USD 58.3 billion) France 2030 investment plan to digitize public services and industry. The United Kingdom navigates post-Brexit customs and standards divergence, stimulating opportunities for domestic integrators and challenges for EU manufacturers crossing new trade barriers. Spain channels Digital Spain 2026 funds toward rural connectivity, unlocking fresh AV demand in schools and municipal buildings.

Italy represents the fastest growth trajectory, catalyzed by School 4.0 and the broader National Recovery and Resilience Plan’s EUR 191.5 billion (USD 206.8 billion) envelope. Classroom modernization involves interactive displays, lecture-capture rigs, and wireless presentation hubs, creating sustained pull through 2031. Universities align with the European Higher Education Area’s interoperability frameworks, further fueling investment. Corporate adoption of hybrid-meeting suites and hotel conference-room upgrades for international events also contribute.

The Rest of Europe displays heterogeneous patterns. Benelux and Nordic countries emphasize sustainability, procuring low-power displays and circular-economy service models. Central and Eastern Europe focus on bridging the digital divide via EU cohesion funds, prioritizing essential functionality over premium features. EU-wide regulations such as the Ecodesign Directive, WEEE, and RoHS harmonize environmental criteria, accelerating retirement of non-compliant analog gear. Collectively, regulatory alignment and stimulus funding shape both baseline demand and technology preferences in the Europe professional audio video market across the region.

Competitive Landscape

Competition is moderately fragmented, as global display giants, audio specialists, UC-platform vendors, and regional integrators vie for share. Sony, Samsung, LG, and Panasonic defend display and camera franchises through vertical integration and channel breadth. Audio expertise remains the differentiator for Shure, Sennheiser, and Harman, who leverage acoustic research and artist endorsements to justify premium pricing. Control-system incumbents Crestron and Barco face pressure from software-defined alternatives that run on tablets and offer cloud management at lower cost. Open networking standards such as Dante and IPMX erode proprietary ecosystems, allowing smaller players to compete on interoperability.

Integrator consolidation intensifies, targeting geographic coverage and vertical specialization in healthcare, education, or government. Managed services and AV-as-a-service models elevate operational excellence over product margins, tying revenue to uptime and customer satisfaction. White-space growth areas include AI analytics for meeting effectiveness, immersive audio for esports, and modular LED walls for retail storytelling. Cloud-native collaboration suites embedded within productivity platforms pose a disruptive threat by abstracting hardware layers.

Semiconductor supply volatility and cybersecurity compliance create dual stresses. Vendors with resilient supply chains and credible security roadmaps win procurement cycles in finance, healthcare, and public administration. Meanwhile, the embrace of sustainability, from low-power chipsets to recyclable enclosures, differentiates suppliers in environmentally conscious Nordic and Benelux markets. Overall, vendor success hinges on balancing innovation velocity, open-standards adoption, and lifecycle service capabilities in the Europe professional audio video market.

Europe Professional Audio Video (ProAV) Industry Leaders

Barco NV

Crestron Electronics, Inc.

Bosch Security Systems GmbH

Harman International Industries, Inc.

Sony Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Zoom Video Communications partnered with Mitel to blend cloud collaboration with Mitel’s on-premises PBX, easing migration for enterprises retaining legacy telephony.

- September 2024: Sony began shipping the BRC-AM7 4K PTZ camera with AI-based auto-framing for corporate, education, and broadcast users.

- September 2024: Sony introduced the BRAVIA VPL-XW8100ES and VPL-XW6100ES 4K laser projectors with HDR10 and HLG support for small commercial venues.

- September 2024: Sony announced the BVM-HX1710 and BVM-HX1710N 4K OLED monitors for live production, shipping summer 2025.

Europe Professional Audio Video (ProAV) Market Report Scope

Professional audio visual (AV) is a sophisticated interaction system for commercial sharing, advertising, and marketing. It is used in private and public complexes for electronic displays to deliver videos, web content, graphics, and texts. Lighting and sound devices, digital signage, video conferencing systems, companion whiteboard recording equipment, and projector systems are all part of it. These components help to improve overall user communication and connectivity and are also used in classrooms, presentations, and on-site product demonstrations.

The Europe Professional Audio Video Market Report is Segmented by Component (Hardware, Software, Services), Solution Category (Streaming Media, Capture Equipment, Displays, Audio, Control, UC Solutions, Others), Distribution Channel (Direct, Integrators, Resellers, E-Commerce, Retail, Others), End-User (Corporate, Venues, Media, Retail, Education, Hospitality, Government, Healthcare, Transport, Others), and Geography (Germany, France, UK, Italy, Spain, Rest of Europe). The Market Forecasts are provided in Terms of Value (USD).

| Hardware |

| Software |

| Services |

| Streaming Media, Storage and Distribution |

| Video Displays and Projection |

| Audio Equipment |

| Unified Communication and Collaboration Solutions |

| Others Solution Category (Control Systems, Capture and Production Equipment,and others) |

| Direct Sales |

| Online and E-Commerce |

| System integrators |

| Others Distribution Channel ( Value-Added Resellers, Retail Stores, and Others) |

| Corporate |

| Venues and Events |

| Media and Entertainment |

| Education |

| Hospitality |

| Others End-User Industry |

| Germany |

| France |

| United Kingdom |

| Italy |

| Spain |

| Rest of Europe |

| By Component | Hardware |

| Software | |

| Services | |

| By Solution Category | Streaming Media, Storage and Distribution |

| Video Displays and Projection | |

| Audio Equipment | |

| Unified Communication and Collaboration Solutions | |

| Others Solution Category (Control Systems, Capture and Production Equipment,and others) | |

| By Distribution Channel | Direct Sales |

| Online and E-Commerce | |

| System integrators | |

| Others Distribution Channel ( Value-Added Resellers, Retail Stores, and Others) | |

| By End-User Industry | Corporate |

| Venues and Events | |

| Media and Entertainment | |

| Education | |

| Hospitality | |

| Others End-User Industry | |

| By Country | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe professional audio video market in 2026 and what is its growth forecast?

The market was valued at USD 34.53 billion in 2026 and is expected to reach USD 50.48 billion by 2031, expanding at a 7.89% CAGR.

Which component category is expanding fastest in Europe?

Services are rising at a 10.40% CAGR as enterprises shift from one-time installations to managed offerings covering monitoring, cybersecurity, and firmware updates.

Why is education investment accelerating across the region?

National programs such as Italy’s School 4.0 and EU connectivity grants are funding interactive displays, lecture-capture systems, and broadband infrastructure, driving an 11.70% CAGR in the education segment.

What technology trend is reshaping procurement decisions?

The move to open, IP-based standards like Dante and IPMX is lowering vendor lock-in and enabling central device management, influencing hardware refresh cycles and supplier selection.

How do EU energy-efficiency rules influence AV upgrades?

Ecodesign and WEEE regulations push organizations to retire power-hungry legacy gear in favor of low-consumption equipment.

Page last updated on: