Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

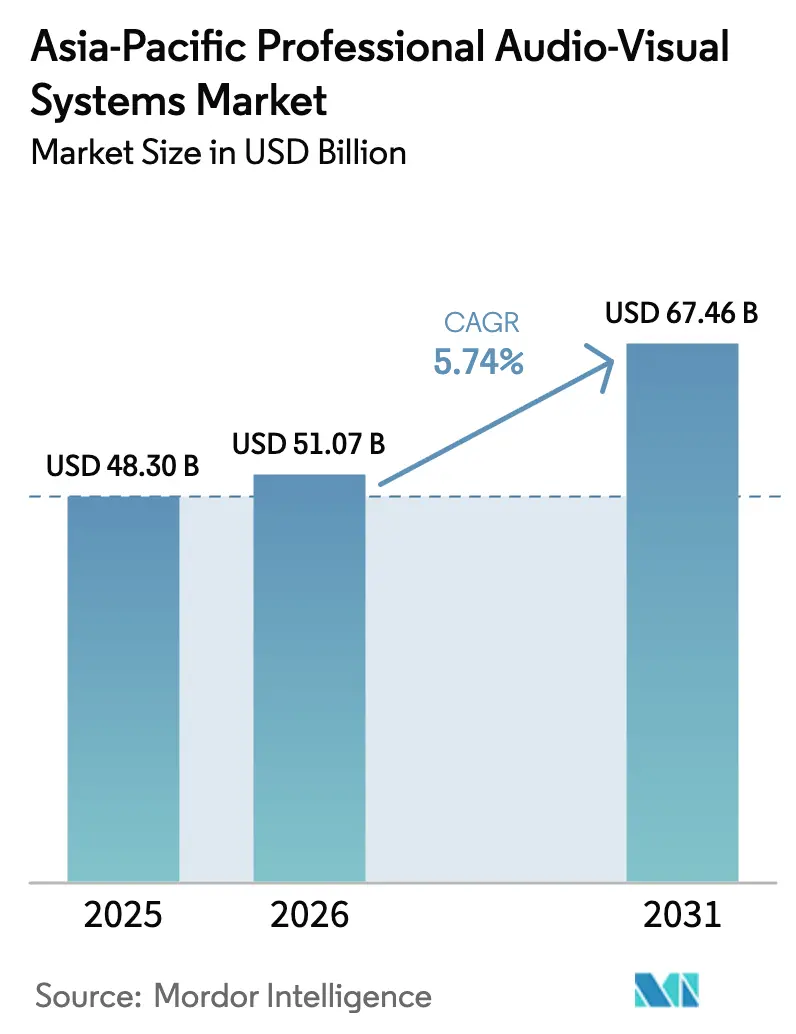

| Base Year Market Size (2025) | USD 48.3 Billion |

| Market Size (2026) | USD 51.07 Billion |

| Market Size (2031) | USD 67.46 Billion |

| Growth Rate (2026 - 2031) | 5.74% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Professional Audio-Visual Systems Market Analysis by Mordor Intelligence

The Asia-Pacific professional audio-visual system market size is expected to grow from USD 48.3 billion in 2025 to USD 51.07 billion in 2026 and is forecast to reach USD 67.46 billion by 2031 at 5.74% CAGR over 2026-2031. Rising digital-first business models, fast-tracking of cloud-native unified communications, and rapid 5G build-outs are reinforcing steady demand even as supply-chain friction persists. Hybrid work policies create sustained pull for platform-agnostic meeting spaces, while experiential retail and concert tourism encourage larger display footprints and immersive audio upgrades. Consolidation exemplified by Samsung’s 2025 purchase of Bowers & Wilkins, Denon, and Marantz, shows incumbents vertically integrating to manage component risk and own premium IP. Live-event recovery is energizing rental and staging refresh cycles, whereas government-funded “smart classroom” projects keep interactive learning hardware on a multi-year replacement curve.

Key Report Takeaways

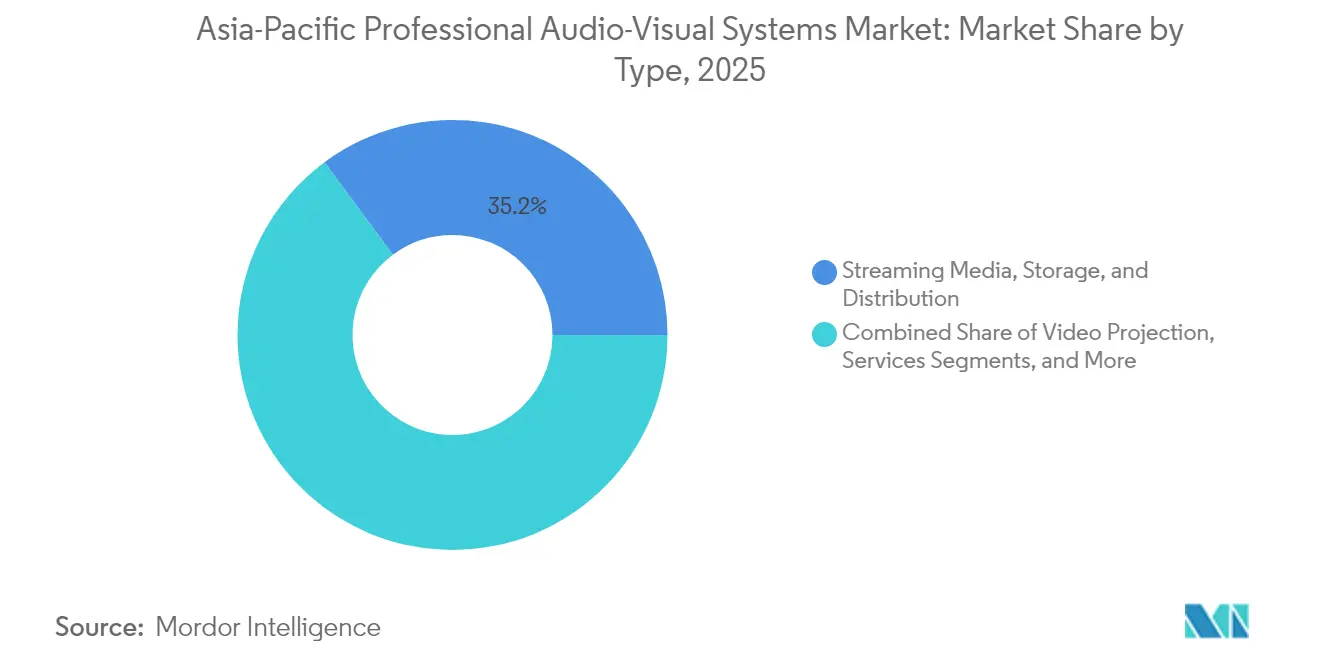

- By type, Streaming Media, Storage, and Distribution captured 35.15% of the Asia-Pacific professional audio-visual system market share in 2025, while Capture and Production Equipment is forecast to advance at a 6.62% CAGR through 2031.

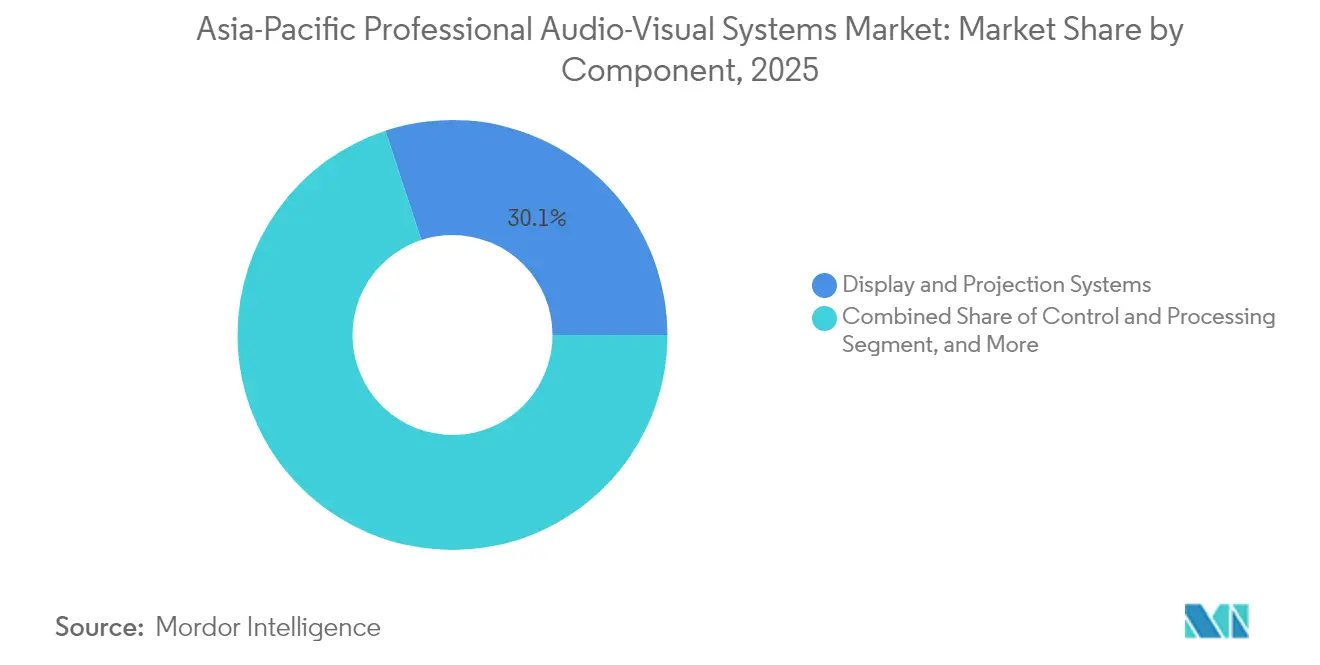

- By component, Display and Projection Systems accounted for a 30.05% share of the Asia-Pacific professional audio-visual system market size in 2025; Audio Equipment is projected to post a 7.01% CAGR from 2026-2031.

- By end-user vertical, Corporate offices held 29.35% revenue share in 2025, whereas Venues and Events is set to grow at 6.84% CAGR through 2031.

- By geography, China led with 38.35% of the Asia-Pacific professional audio-visual system market share in 2025; India is slated to register the fastest 7.22% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Professional Audio-Visual Systems Market Trends and Insights

Driver Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Hybrid-workplace demand for cloud-native UC suites | +1.2% | China, Japan, South Korea | Medium term (2-4 years) |

| Expansion of digital signage in experiential retail | +0.9% | Core Asia-Pacific, spillover to emerging markets | Short term (≤ 2 years) |

| Government-led “smart classroom” capex | +1.1% | India, Southeast Asia | Long term (≥ 4 years) |

| Live event rebound lifts rental and staging | +0.8% | Singapore, Hong Kong, Tokyo | Short term (≤ 2 years) |

| 5G-enabled remote production and AVoIP | +1.0% | China, Japan, South Korea | Medium term (2-4 years) |

| Carbon-neutral procurement mandates | +0.7% | Developed Asia-Pacific with Europe trade exposure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Hybrid-workplace demand for cloud-native UC suites

Enterprises across the Asia-Pacific professional audio-visual system market are standardizing on Microsoft Teams Rooms and similar platforms, prompting integrators to deliver turnkey packages that blend cameras, microphones, interactive displays, and AI-driven sound processing.[1]Source: Ashutosh Kumar, “Cloud communications industry bets on AI, hybrid working,” Economic Times, economictimes.indiatimes.com Spatial audio functions and automated framing make meetings more inclusive for distributed employees, a priority for Chinese and Japanese multinationals managing cross-border teams. Converged AV-IT networks also streamline managed services, cutting truck-roll costs for facility managers and helping corporations meet internal carbon-reduction goals through power-optimized device scheduling.

Expansion of digital signage in experiential retail

Interactive LED façades and 8K videowalls are transforming flagship stores, with regional retailers using large-format displays to bridge physical shopping and social-commerce engagement. The Asia-Pacific professional audio-visual system market benefits from falling pixel-pitch pricing and higher-efficiency micro-LED modules that meet sustainability regulations without sacrificing brightness. Post-pandemic safety messaging hastened display roll-outs, and content management software now integrates occupancy sensors to trigger real-time visual prompts, a feature retailers in Singapore and Seoul deploy to comply with local health codes.[2]Source: AVIXA, “Digital Signage Growth Forecast,” avixa.org

Government-led “smart classroom” capex

India’s Operation Digital Board catalyzed a leap from 20,000 interactive classrooms in 2009 to 581,000 in 2019, and installations are projected to hit 1.5 million by 2024, anchoring long-run growth in the Asia-Pacific professional audio-visual system market. ASEAN nations replicate this momentum, guided by Asian Development Bank frameworks that emphasize inclusive EdTech procurement. Demand concentrates on flat-panel displays, all-in-one soundbars, and cloud-hosted learning platforms capable of synchronous in-class and remote instruction, ensuring content continuity during weather-related school closures.

Live-event rebound lifts rental and staging

Concert tourism’s return sees Singapore underwriting exclusivity deals that generated an estimated SGD 500 million (USD 390.42 million) economic impact in 2024.[3]Source: Gary Bowerman, “Concert tourism takes centre stage across Asia,” asiamediacentre.org.nz New arenas in Hong Kong and Macau are specifying 120-frame-per-second projection, immersive 360° audio arrays, and low-latency fiber backbones to support esports, conferences, and televised award shows. Rental-house inventories thus tilt toward modular LED panels, weatherized line-array speakers, and IP-based signal routers that can be redeployed rapidly across multiple venues, compressing return-on-capital cycles.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High operating and compliance costs of complex AV | -0.8% | Global, heavier in tier-2 cities | Medium term (2-4 years) |

| Persistent chipset and optical-component bottlenecks | -1.1% | China, South Korea, Taiwan | Short term (≤ 2 years) |

| Shortage of certified AV technicians | -0.7% | Tier-2 cities in India, South East Asia China | Long term (≥ 4 years) |

| Carbon-border tariffs inflate export BOM costs | -0.6% | ASEAN suppliers to Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High operating and compliance costs of complex AV projects

Integrated solutions now blend video, audio, control, and cybersecurity safeguards, raising design hours and specialist wages, particularly outside primary metro areas. Training pipelines lag demand: fewer than 3,000 Asia-Pacific engineers hold advanced SDVoE certification, prompting firms to rely on freelancers who may not stay through warranty periods. AV-as-a-Service contracts transfer capex to opex but include SLA penalties tied to uptime and data-protection audits, making smaller integrators financially cautious.

Carbon-border tariffs inflate export BOM costs

The EU’s Carbon Border Adjustment Mechanism adds an estimated USD 40-60 per ton of embedded emissions on aluminum chassis and steel mounts exported from ASEAN suppliers.[4]Source: Melinda Martinus & Kanin Laopirun, “EU CBAM Implications for ASEAN,” iseas.edu.sg Manufacturers weigh localizing production within bloc markets or switching to recycled alloys, but both options demand capital and engineering redesigns, pushing up MSRP until economies of scale emerge.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Streaming Dominates Content Distribution Evolution

Streaming Media, Storage, and Distribution holds a 35.15% share of the Asia-Pacific professional audio-visual system market, underlining its role as the backbone for distance collaboration and direct-to-consumer entertainment. The wave of 5G private networks across factories further entrenches cloud gateways that ingest, transcode, and forward 4K content in under a second, unlocking remote quality-assurance reviews without on-site staff. Capture and Production Equipment, projected to clock a 6.62% CAGR, thrives on influencer-economy growth and affordable mirrorless cameras paired with AI auto-tracking tripods. Legacy video projection remains relevant for lecture halls and hotel ballrooms craving bright, lamp-free units able to run 24/7 with minimal maintenance.

Second-generation edge encoders compress HEVC streams at half the bit-rate, shrinking bandwidth fees for distance-learning providers. Managed-service vendors bundle them with content-delivery-network subscriptions, shifting the Asia-Pacific professional audio-visual system market from hardware sales toward recurring revenue models. Experimental holographic displays surface in surgical-planning labs, yet most enterprises still pilot them under research and development budgets rather than mainstream roll-outs.

By Component: Display Systems Lead Hardware Integration

Display and Projection Systems contributed 30.05% to the Asia-Pacific professional audio-visual system market size in 2025, buoyed by micro-LED cost declines and corporate appetite for bezel-less videowalls that double as digital backdrops for virtual production. LED manufacturers located in Shenzhen and Pyeongtaek race to reach sub-0.7-millimeter pixel pitches at competitive yields, compressing unit economics favorable to budget-sensitive education buyers. Audio Equipment enjoys a 7.01% CAGR outlook, catalyzed by Samsung’s integration of Bowers & Wilkins' psychoacoustic research into premium conferencing bars that replicate spatial attendance cues.

Control and Processing shift to software-defined cores that run on commercial off-the-shelf servers, enabling over-the-air updates that extend hardware cycles. Storage and Distribution Hardware sees traditional matrix switchers replaced by 10- and 25-gigabit network fabrics managed through browser dashboards. Power consumption remains a selling point as clients pursue green-building credits; hence, adaptive backlight dimming and class-D amplifier topologies become standard.

By End-user Vertical: Corporate Spending Drives Market Foundation

Corporate environments remained the largest revenue source, absorbing 29.35% of the Asia-Pacific professional audio-visual system market in 2025 as multinational tenants fitted flex-desking spaces with auto-calibrating beamforming arrays and dual-screen front-row configurations. Board approvals often hinge on carbon-payback models where occupancy sensors power down idle displays, aligning with ESG disclosures demanded by investors. Venues and Events, forecast at 6.84% CAGR, experience a renaissance in funding from city tourism boards courting international acts; venue managers demand modular gear capable of touring residencies one week and esports finals the next.

Education keeps rolling out interactive flat panels that bundle annotation software, thereby phasing out bulky chalkboards. Across India, state tenders increasingly require bilingual interface options, expanding addressable volume for regional OEMs integrating Hindi and Tamil fonts at the firmware layer. Healthcare adopts immersive visualization for tele-ICU monitoring and surgical rehearsals, a niche but high-margin pocket where latency tolerance is near zero and uptime SLAs exceed 99.99%.

Geography Analysis

China’s 38.35% slice of the Asia-Pacific professional audio-visual system market results from its dual position as OEM powerhouse and aggressive domestic adopter. Tier-2 smart-city pilots embed outdoor LED screens into traffic-management nodes, embedding AV feeds with urban IoT telemetry. Bulk purchasing rules often favor locally branded systems, prompting multinationals to form joint ventures or license IP to Chinese partners. Meanwhile, India’s 7.22% CAGR through 2031 rides on state-funded EdTech grants and corporate campus expansions around Bengaluru and Hyderabad that specify fully integrated huddle rooms with AI auto-translation overlays, boosting inclusion for a linguistically diverse workforce. Japan and South Korea remain innovation bellwethers: broadcasters in Tokyo test 8K/120 fps workflows ahead of global sports events, while Seoul’s electronics giants mold mini-LED supply chains resilient to raw-material tariffs. Southeast Asia, aided by the Thailand 4.0 blueprint, invests in digital-service corridors that bake immersive signage into transport hubs and logistics parks. Rest of Asia Pacific markets, from Pakistan to the Pacific Islands, start to pilot unified communication suites via subscription bundles as satellite broadband prices fall.

Competitive Landscape

The Asia-Pacific professional audio-visual system market features moderate fragmentation, yet top brands rely on scale to buffer supply shocks. Sony, Samsung, Panasonic, and LG map consumer-electronics IP into professional form factors, leveraging shared component pools to keep BOM costs predictable. Niche leaders Barco for visualization, Crestron for control, and Bose Professional for installed audio differentiate via software ecosystems and certified-partner programs. Consolidation accelerated with Samsung’s 2025 audio acquisitions and Acuity Brands’ 2024 purchase of QSC, moves that fold premium DSP and loudspeaker lines into broader building-technology stacks.

White-space revolves around AI orchestration layers that auto-detect occupancy and dynamically re-route signals based on application context. Sustainability credentials serve as a soft moat; Sony’s “Road to Zero” and Panasonic’s “Eco Vision 2050” shape sourcing policies toward recyclable plastics and halogen-free cables. Regional integrators like Vega Global win complex cross-border roll-outs by bundling multilingual helpdesks and in-country stock depots, whereas software start-ups craft SaaS dashboards that unify firmware updates across mixed-vendor fleets.

Future competition will likely pit vertically integrated giants against platform-agnostic consortia advocating open-standard APIs, with customers weighing lock-in risk against single-throat-to-choke convenience. Market positioning thus hinges on balancing proprietary codec advantages with interoperability commitments that reassure enterprise architects building long-run roadmaps.

Asia-Pacific Professional Audio-Visual Systems Industry Leaders

Sony Corporation

Samsung Electronics

Panasonic Corporation

LG Electronics

Epson

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Samsung’s Harman International acquired the audio division of Masimo for USD 350 million, adding Bowers & Wilkins, Denon, and Marantz to its portfolio.

- October 2024: Acuity Brands completed its USD 1.2 billion takeover of QSC to merge AV with smart-lighting controls.

- October 2024: Williams AV acquired TeachLogic, expanding classroom-audio offerings.

- September 2024: GSMA released case studies showing Thailand’s private 5G network delivered 15-20% efficiency gains at an appliance plant.

Asia-Pacific Professional Audio-Visual Systems Market Report Scope

Audio-visual technology is used in various applications, including entertainment, education, communication, presentations, conferences, and advertising. It involves using multiple devices and systems to create, enhance, and deliver audio and visual content. Advancements in high-definition display technologies are changing the way professional audio/visual or Pro AV; equipment is being used to communicate, broadcast, collaborate, interact, and advertise in commercial environments.

The Asia-Pacific professional audio-visual systems market is segmented by type (capture and production equipment, video projection, streaming media, storage, and distribution, and other types), end-user vertical (corporate, education, healthcare, hospitality, venues and events, retail, and other end-user verticals), and country (China, Japan, India, South Korea, and Rest of Asia-Pacific). The market sizes and forecasts are provided in terms of value in USD for all the above segments.

By Type

| Capture and Production Equipment |

| Video Projection |

| Streaming Media, Storage and Distribution |

| Services |

| Other Types |

By Component

| Audio Equipment (mics, mixers, amps) |

| Display and Projection Systems |

| Control and Processing |

| Storage and Distribution Hardware |

By End-user Vertical

| Corporate |

| Venues and Events |

| Retail |

| Media and Entertainment |

| Education |

| Government |

| Healthcare |

| Other End-user Vertical |

By Country

| China |

| Japan |

| India |

| South Korea |

| South-East Asia |

| Rest of Asia-Pacific |

| By Type | Capture and Production Equipment |

| Video Projection | |

| Streaming Media, Storage and Distribution | |

| Services | |

| Other Types | |

| By Component | Audio Equipment (mics, mixers, amps) |

| Display and Projection Systems | |

| Control and Processing | |

| Storage and Distribution Hardware | |

| By End-user Vertical | Corporate |

| Venues and Events | |

| Retail | |

| Media and Entertainment | |

| Education | |

| Government | |

| Healthcare | |

| Other End-user Vertical | |

| By Country | China |

| Japan | |

| India | |

| South Korea | |

| South-East Asia | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the current value of the Asia-Pacific professional audio-visual system market?

The market is valued at USD 51.07 billion in 2026, with a forecast to reach USD 67.46 billion by 2031.

Which segment holds the largest Asia-Pacific professional audio-visual system market share?

Streaming Media, Storage and Distribution leads with 35.15% share in 2025.

Which country is the fastest growing within the Asia-Pacific professional audio-visual system market?

India is projected to grow at a 7.22% CAGR between 2026 and 2031.

How is 5G influencing professional AV adoption in Asia-Pacific?

5G enables sub-10 ms latency AVoIP workflows, unlocking remote production and delivering 15-20% efficiency gains in manufacturing pilots.

Page last updated on: