Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

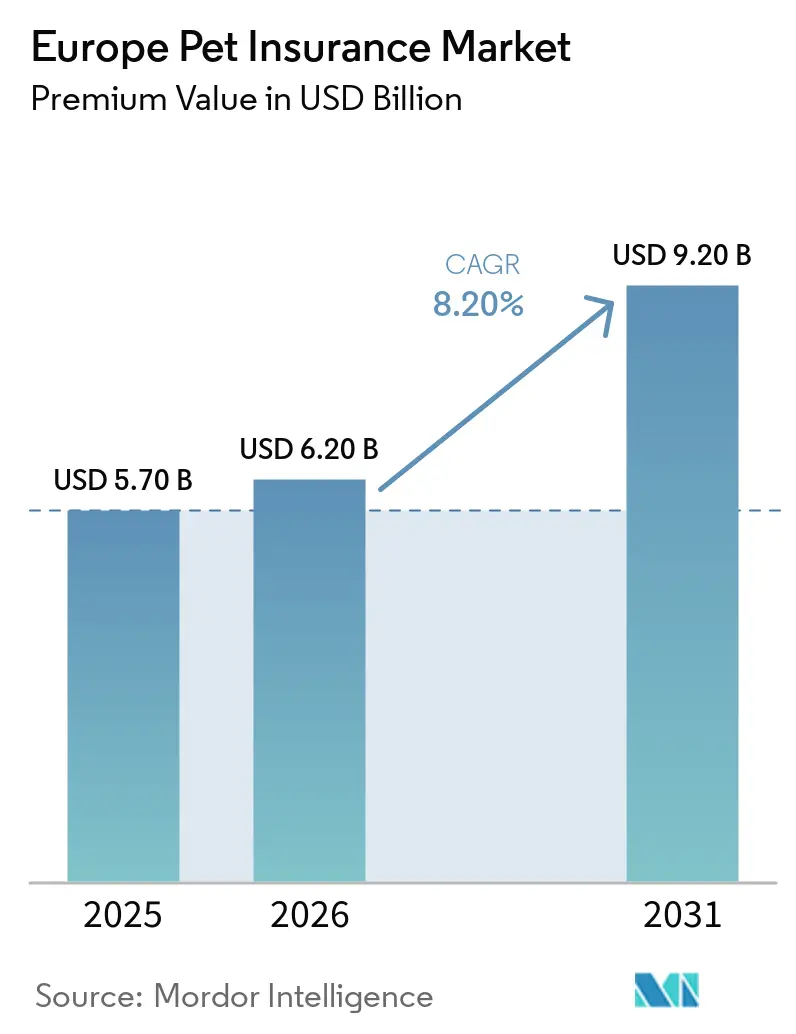

| Base Year Market Size (2025) | USD 5.70 Billion |

| Market Size (2026) | USD 6.20 Billion |

| Market Size (2031) | USD 9.20 Billion |

| Growth Rate (2026 - 2031) | 8.20% CAGR |

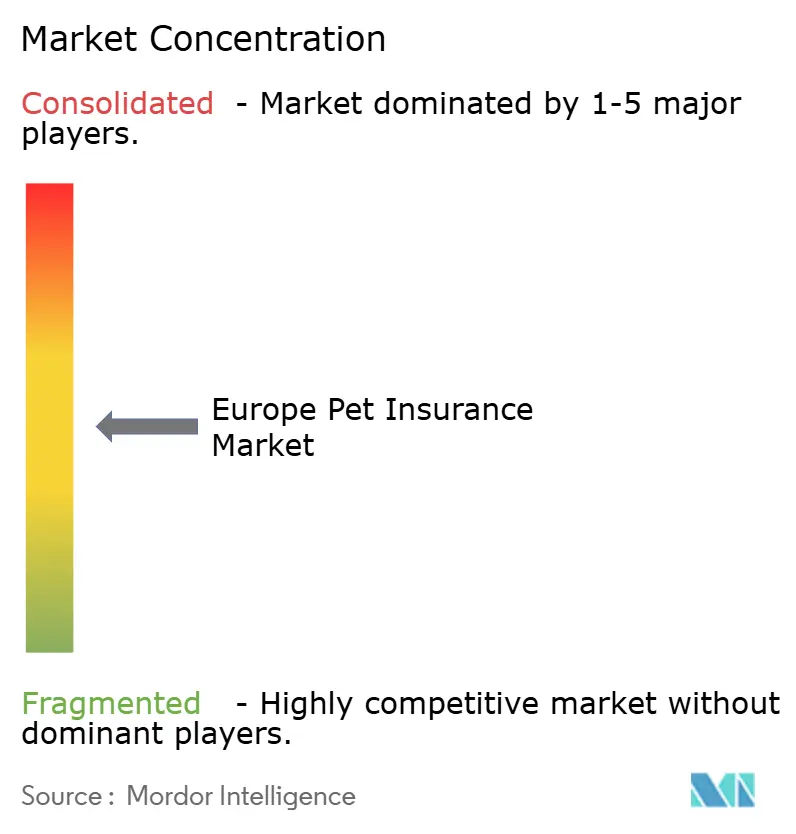

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Pet Insurance Market Analysis by Mordor Intelligence

The Europe Pet Insurance Market size in terms of premium value was valued at USD 5.70 billion in 2025 and is estimated to grow from USD 6.20 billion in 2026 to reach USD 9.20 billion by 2031, at a CAGR of 8.20% during the forecast period (2026-2031).

Growth in the Europe pet insurance market is supported by sustained veterinary fee inflation, with the UK’s veterinary services index at 177.1 in January 2026 on a 2015=100 base, a level that continues to outpace general consumer prices[1]Office for National Statistics, “CPI INDEX 09.3.5.0 Veterinary and other services for pets 2015=100,” Office for National Statistics, ons.gov.uk. The European Parliament’s 2025 approval of mandatory microchipping and interoperable national pet registries by 2027 enhances traceability and lowers fraud risk, which supports broader adoption of comprehensive policies across the region. Consolidation among corporate veterinary chains and multi-brand insurers has amplified pricing power and set higher care standards, with JAB’s pet platforms reaching over USD 3 billion in revenues in 2024. Digital distribution is accelerating as insurtechs streamline claims through automation and embedded partnerships, increasing conversion and retention across core markets such as the UK, Germany, France, and the Netherlands. Regulators in 2026 are scrutinizing price fairness and consumer understanding, shaping product transparency and service benchmarks for the Europe pet insurance market.

Key Report Takeaways

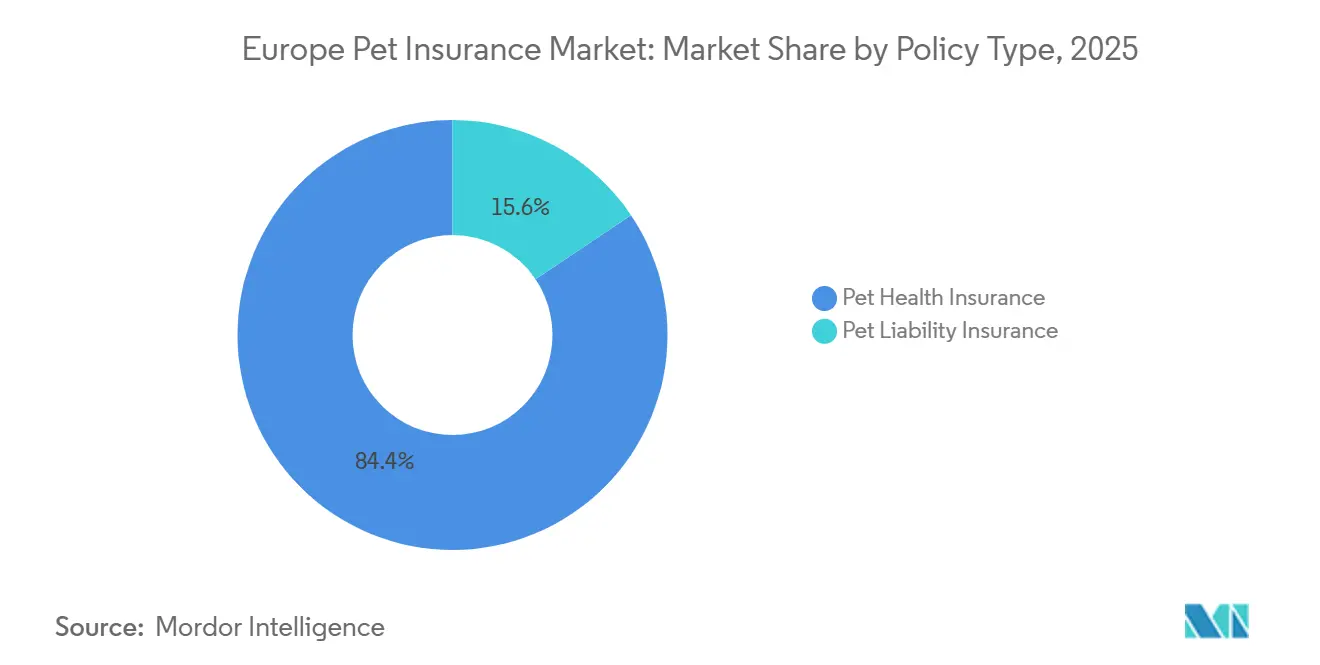

- By policy type, Pet Health Insurance led with 84.4% revenue share in 2025, and is projected to record the fastest 9.8% CAGR through 2031 within the Europe pet insurance market.

- By animal type, dogs commanded 68.8% revenue share in 2025, while cats are expected to grow at a 10.1% CAGR through 2031 within the Europe pet insurance market.

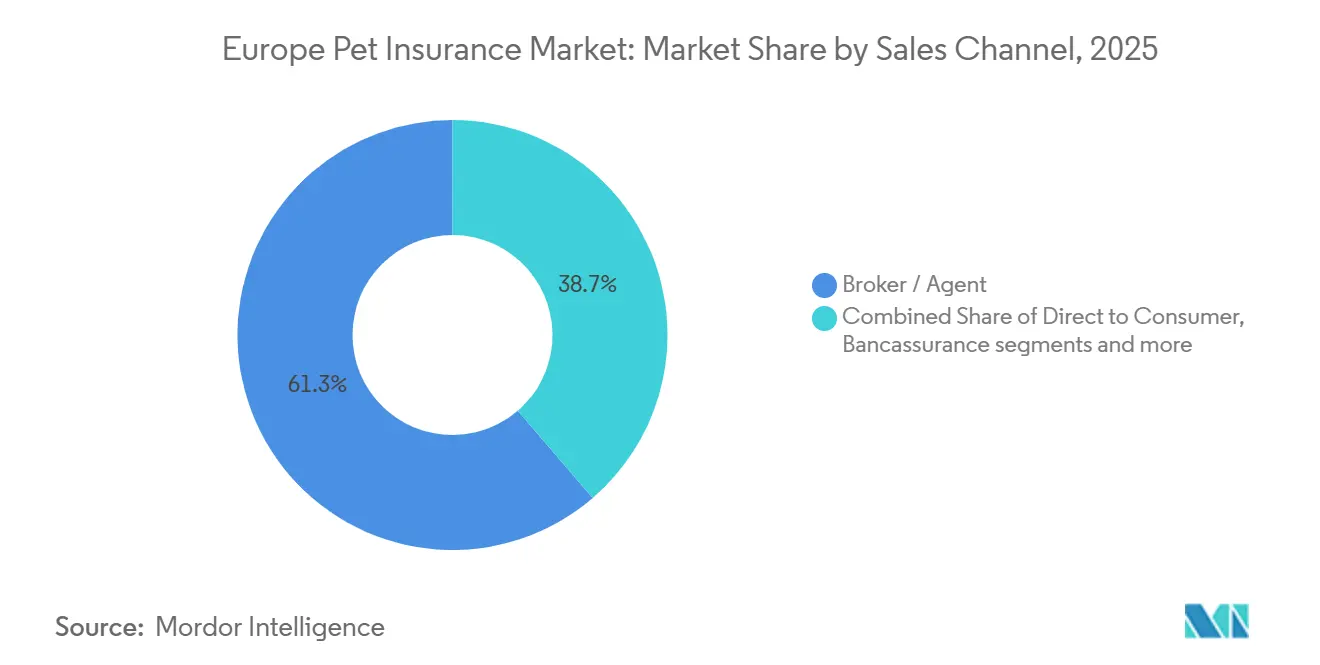

- By sales channel, broker/agent distribution held 61.3% revenue share in 2025, and online aggregators and insurtech platforms are set to expand at an 11.8% CAGR through 2031 within the Europe pet insurance market.

- By coverage level, Standard policies captured 52.4% revenue share in 2025, and Comprehensive is projected to be the fastest tier at a 10.5% CAGR through 2031 within the Europe pet insurance market.

- By geography, the United Kingdom accounted for 45.3% revenue share in 2025, while Italy is forecast to post the fastest 9.5% CAGR through 2031 within the Europe pet insurance market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Pet Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising veterinary treatment costs | +2.8% | Global, acute in UK, Nordics; UK veterinary CPI 177.1 in Jan 2026, Finland veterinary inflation 4.0% in 2025 | Medium term (2-4 years) |

| Growing humanisation of pets | +2.1% | Western Europe where a large majority view pets as family; high pet ownership and spending per FEDIAF | Long term (≥ 4 years) |

| High pet-ownership & pandemic adoption surge | +1.5% | EU-wide, 49% household penetration with 299 million pets per FEDIAF 2025 | Short term (≤ 2 years) |

| Digital distribution & insurtech expansion | +1.4% | Strongest in UK, Germany, Netherlands, France; nascent in Italy, Spain | Medium term (2-4 years) |

| Microchipping mandates lift uptake | +0.8% | EU Parliament directive June 2025, implementation by 2027; Spain and Belgium precedents | Long term (≥ 4 years) |

| Wearables-enabled usage-based pricing | +0.6% | Germany, Netherlands, UK early adopters; insurer–wearable partnerships expanding | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Veterinary Treatment Costs Drive Market Expansion

Veterinary fee inflation remained above general CPI across major European markets in 2025 and into 2026, with the UK’s veterinary services index reaching 177.1 in January 2026 on a 2015=100 base, reinforcing the need for broader fee coverage in the Europe pet insurance market. Investigations in the UK highlighted higher charging patterns among corporate chains, including findings of significant medicine markups and elevated procedure pricing, which contribute to cost pass-through into premiums. Peer-reviewed analysis from Sweden and Norway showed median price levels at corporate-affiliated clinics above those at independent practices, with higher claim costs over multi-year periods, signaling structural care inflation that insurers must price for. As owners confront larger invoices for diagnostics, surgery, and long-term therapies, demand tilts toward comprehensive lifetime cover despite rising premiums, particularly among risk-averse households in mature markets. Policymakers have responded by seeking greater pricing transparency and ownership disclosure in veterinary services, steps that can influence underwriting assumptions and claims management for the Europe pet insurance market.

Growing Humanization of Pets Elevates Willingness to Pay

Pet ownership in Europe is broad, with 299 million pets and household penetration near one in two homes, and spending patterns reflect a strong view of pets as family members who warrant comprehensive care[2]Federation of European Pet Food Manufacturers, “Facts & Figures 2025,” FEDIAF, fediaf.org. This outlook supports willingness to pay for lifetime policies that include wellness, dental, and behavioral benefits, which are now integrated by several leading carriers and insurtechs. Digital-first brands have reinforced this shift by bundling coaching, discounts for preventive actions, and fast claims resolution, all of which strengthen perceived value for consumers. Public policy trends such as France’s provisions for pet companionship for seniors add a social dimension that normalizes spending on pet well-being and support services. The behavioral and policy context together sustain demand for richer coverage and continuous service access across the Europe pet insurance market.

Digital Distribution & Insurtech Expansion Redefine Customer Acquisition

Insurtechs and online aggregators are expanding at a double-digit pace as they compress acquisition costs, personalize pricing, and resolve claims through automation, which is reshaping how the Europe pet insurance market acquires and serves customers. Leading examples include automated claims engines that process high volumes within minutes and deliver near instant payouts, which raise satisfaction and daily engagement. Carriers that consolidated policy administration on proprietary platforms have reported improved efficiency and financial performance alongside scaling AI enabled triage. Country launches that enable direct payment at checkout show how technology can reset expectations around cashless care and reduce friction for pet owners. Embedded routes with retailers, pharmacies, and wearables extend reach further, giving the Europe pet insurance market multiple high frequency touchpoints across the pet care journey.

Microchipping Mandates Lift Uptake by Boosting Traceability

The European Parliament’s 2025 approval of mandatory microchipping and interoperable national databases by 2027 builds a shared infrastructure that improves identification, cross-border traceability, and claims integrity. Microchip IDs link ownership to medical records more reliably, which helps insurers verify eligibility and reduce fraud risk during digital claims. Many policies already require microchip identification, and product designs that bundle preventive services with coverage are aligning with this regulatory trajectory across the Europe pet insurance market. Wearable and GPS-enabled offerings, when paired with microchipping, add a layer of safety and data, which can help validate care events and support proactive interventions. The cumulative effect is a more transparent, data-ready ecosystem that lowers administrative friction for carriers and for policyholders.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High premiums for older pets/breeds | -1.8% | UK, Nordics, Germany; steeper age multipliers and higher breed‑risk pricing | Medium term (2-4 years) |

| Low awareness outside UK & Nordics | -1.3% | Italy, Spain, Eastern Europe where penetration is low despite high ownership | Short term (≤ 2 years) |

| Veterinary fee inflation squeezes margins | -0.9% | UK, Sweden, Norway; elevated fee levels pressure underwriting | Medium term (2-4 years) |

| Fraudulent digital claims on the rise | -0.4% | UK, Germany, Netherlands; prompting AI fraud controls | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Premiums for Older Pets/Breeds Limit Addressable Demand

Age-linked premium increases and breed risk pricing can make comprehensive coverage expensive for seniors and large breeds, which narrows affordability at the point of renewal. Complaints data and consumer advocacy reported pressure around renewal hikes, noting that lifetime policies better match needs but can become harder to switch as pets age. Carriers that tightened risk selection in 2025 showed improved loss ratios, though that can also reduce access for high-risk profiles that often need cover the most[3]European Parliament, “MEPs propose stricter rules on dog and cat welfare and traceability,” European Parliament, europarl.europa.eu. Market responses include niche products tailored to older pets with lower benefit tiers that aim to keep premiums in reach for underserved owners. Supervisors in 2026 highlighted pet insurance for monitoring on price and consumer understanding, which may guide renewal practices and product clarity in the Europe pet insurance market.

Low Awareness Outside UK & Nordics Constrains Penetration

Penetration remains low in Southern and Eastern Europe, even where pet ownership is high, which reflects an awareness gap and limited distribution reach. New product launches by leading domestic health insurers and digitally native carriers in 2025 targeted Spain and Italy with app-based services, reimbursement benefits, and hotline access to address education and adoption hurdles. Insurtechs in France and Germany expanded with automation and transparent fee structures, reinforced by profitability milestones that validate the model[4] EU-Startups Staff, “Dalma raises €20M,” EU-Startups, eu-startups.com. Bancassurance distribution is emerging as a scale lever that brings pet cover to established customer bases through trusted channels, which can materially lift awareness in low penetration markets. Pharmacy and e-commerce partnerships add embedded routes to ensure large pools of pet owners online, broadening access across the Europe pet insurance market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Policy Type: Pet Health Dominates, Liability Scales with Regulation

Pet Health Insurance held 84.4% of revenue in 2025, and it is projected to grow at a 9.8% CAGR during 2026-2031 as owners prioritize comprehensive veterinary fee protection in the Europe pet insurance market. The Europe pet insurance industry has shifted toward richer lifetime benefits that cover accidents, illnesses, hereditary risks, and increasingly dental and behavioral care, as seen in product upgrades by leaders that improved claims approval rates and service levels. Insurtechs that process claims within minutes and integrate prevention features into the product experience are raising expectations for speed and transparency, which supports the adoption of broader tiers at renewal. Higher treatment costs for advanced surgery, imaging, and chronic care are the central reason owners step up from basic caps to lifetime configurations that reset annually. The result is a widening gap between standard and premium coverage preference, with health insurance expanding both through direct digital sales and bancassurance routes across core markets.

Pet Liability Insurance represents the balance of policies and grows in jurisdictions with mandatory or widely expected liability cover for dog owners, often as part of a modular bundle. Spanish and German regulatory frameworks have sustained demand for liability-led packages, while multi-line digital carriers provide high liability limits as part of streamlined app-based enrollment. The interplay between mandated liability and voluntary health cover creates cross-sell opportunities as owners discover the value of adding veterinary fee components. As more platforms standardize eligibility checks and real-time coverage verification for clinics, liability and health modules can be configured around use cases that match local laws and consumer expectations in the Europe pet insurance market.

By Animal Type: Dogs Lead, Cats Accelerate on Urban Living

Dogs accounted for 68.8% of revenue in 2025 as higher per-pet spend and complex treatments kept dog coverage central to the Europe pet insurance market. Cats are the fastest-growing segment with a projected 10.1% CAGR through 2031, supported by large, urban cat populations in leading markets that favor lower premium levels and digital service models. Feline-specific plans that calibrate benefits to indoor lifestyles and chronic condition profiles have seen strong traction among first-time policyholders. As more carriers integrate 24/7 tele vet access and preventive perks, cat owners see measurable service value beyond claims reimbursement alone, which supports improved retention in the Europe pet insurance market.

Dogs continue to anchor liability segments where coverage is mandated or expected, while comprehensive health packages for dogs normalize higher annual limits to match advanced care costs and breed-specific risks. Clinical pricing studies across the Nordics have documented sustained increases in surgical and diagnostic fees at larger groups, which sustains demand among dog owners for higher caps and lifetime resets. In parallel, the steady rise in total pet households in Western Europe ensures a deep base for both dog and cat policy expansion. Dogs held 68.8% of Europe's pet insurance market share in 2025, while the cat segment’s 10.1% projected CAGR signals a catch-up trajectory over the forecast period.

By Sales Channel: Brokers Hold Scale, Digital and Bancassurance Outpace

Broker and agent distribution represented 61.3% of revenue in 2025, reflecting the importance of advice-led journeys for complex policies within the Europe pet insurance market. Digital platforms are scaling fastest as insurtechs leverage automation, embedded offers, and mobile journeys to reach younger demographics at lower cost. Insurers that consolidated policy administration and deployed AI claims triage reported material operational gains that supported margin improvement in 2025. Clinic-facing verification tools that confirm coverage and remaining limits in real time strengthen the broker vet channel and improve customer experience at the point of care.

Bancassurance is emerging as a powerful route in mature and developing European markets by activating large installed customer bases and trusted brands for pet cover. Online pharmacy and retail ecosystems are also entering distribution with insurance partners to present pet cover at natural purchase points for care products, which broadens funnel reach in the Europe pet insurance market. In parallel, international launches that bring direct pay technology and lifetime protection to new countries are raising consumer expectations for frictionless claims experiences across channels. The Europe pet insurance market is therefore converging on an omnichannel model where advisory trust, digital speed, and embedded convenience coexist.

By Coverage Level: Standard Leads, Comprehensive Gains on Inflation

Standard policies, defined as plans with annual caps up to EUR 5,000, held 52.4% of revenue in 2025 as owners balanced affordability with meaningful clinical coverage in the Europe pet insurance market. Basic tiers with very low annual caps retain relevance in lower spend geographies, though their utility declines in high-cost markets that face steep procedure pricing. Comprehensive tiers are forecast to grow the fastest at a 10.5% CAGR through 2031 as owners respond to fee inflation by seeking higher annual limits and broader benefit sets. Leading brands strengthened claims service and product depth in 2025, which improved combined ratios and supported confidence in richer cover designs across the Europe pet insurance market.

Comprehensive tiers increasingly include dental, behavioral, and 24/7 tele vet access, while some entrants emphasize direct payment at checkout so owners avoid high upfront costs for complex care. Policy caps and reimbursement percentages were raised by select carriers in 2025 to keep pace with growing treatment intensity, reinforcing the overall shift toward premium tiers in the Europe pet insurance market. The Europe pet insurance market size tied to comprehensive tiers is thus expected to expand as owners make informed choices about cover levels that match real-world costs.

Geography Analysis

The United Kingdom led the region with 45.3% of revenue in 2025, underpinned by a mature product set, high claims incidence, and active competition among scale incumbents and agile insurtechs in the Europe pet insurance market. Market leaders reported solid performance in 2025, including combined ratios that improved year over year, supported by technical pricing and service enhancements. The UK’s regulatory focus in 2026 on price and consumer understanding, combined with proposals to cap prescription fees and mandate quotes for higher value treatments, is shaping a more transparent operating environment. The United Kingdom accounted for 45.34% of Europe's pet insurance market share in 2025, and this base continues to attract product innovation and partnership activity.

Germany, France, and the Nordics form the next tier of scale markets where digital carriers and established brands operate alongside strong veterinary networks. German digital insurers reported profitability milestones in 2024 and continued to scale in 2025, while Nordic carriers maintained premium strength amid elevated fee levels at clinics. France’s large cat population and strong pet food sector continue to support wellness-oriented coverage designs, where insurtechs have focused on transparency and fast claims analysis. In the Nordics, peer-reviewed evidence of higher prices at corporate groups in Sweden and Norway underscores the need for higher caps and careful underwriting discipline.

Italy and Spain are the fastest-improving larger markets, given low baselines and new product launches by leading national carriers and health insurers. Italy is forecast to post a 9.5% CAGR during 2026-2031, helped by urban demographics, policy enhancements by leading insurers, and incentives that support pet care adoption in cities. BENELUX shows momentum through e-commerce and pharmacy ecosystems that can embed pet cover within existing digital journeys at scale. Across these geographies, bancassurance and embedded retail partnerships are helping expand the Europe pet insurance market size to new owner segments that had limited awareness or access before 2025.

Competitive Landscape

The Europe pet insurance market features a blend of scale incumbents and high-growth insurgents. UK leaders maintained strong books in 2025, while Nordic specialists reported continued premium growth across multiple countries. Pan-regional platforms backed by diversified investors consolidated their share in 2024 and 2025, unifying brands and operating models across multiple countries to gain data and scale economies. Insurtechs improved loss ratios and cost positions through automation and proprietary claims technology, achieving profitability in selective markets.

Strategic moves in 2024 and 2026 reshaped the landscape. A UK FTSE 100 carrier purchased direct personal lines renewal rights from a major insurer, deepening its presence in pet through brand and employee transfers. A U.S.-listed pet medical insurer entered Germany and Switzerland with a direct pay model that authorizes vet payments at checkout, setting a new service bar for claim friction. Dutch market participants launched pharmacy and pet retail distribution for insurance, aligning embedded offers with recurring pet care purchases. These plays illustrate the region’s dual track of consolidation and digital expansion in the Europe pet insurance market.

Technology and channel innovation are core differentiators. Automated claims platforms in the Netherlands reached high straight-through processing rates with accuracy improvements, demonstrating the role of machine learning in cost control and customer satisfaction. In parallel, UK market leaders deployed real-time coverage verification tools for veterinary partners to reduce administrative latency and improve clinical workflow. Wearables partnerships extend into prevention-first experiences with GPS tracking and activity-based rewards integrated into insurance journeys, where new collaborations emerged in 2025 2026. Competitive intensity remains high, yet product breadth, distribution scale, and service speed are defining the leading positions across the Europe pet insurance market.

Europe Pet Insurance Industry Leaders

Agria Djurförsäkring

Petplan

RSA Group

ManyPets

Animal Friends Insurance

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Lassie (Stockholm-based insurtech) raised USD 75 million in Series C funding led by Balderton Capital, Felix Capital, Inventure, Passion Capital, and Stena Sessan, bringing total capital to USD 120 million to expand its prevention-first pet insurance platform across Europe, strengthen AI-driven claims processing (60% of German claims processed end-to-end in six minutes), and deepen partnerships with Lidl and Tractive, as the company surpassed USD 100 million in ARR while operating in Sweden, Germany, and France.

- February 2026: Musky (Spanish insurtech backed by GCO Ventures) became the first pet insurer to offer Tractive device and subscription reimbursement as a standard preventive care benefit for annually paying customers, integrating GPS tracking and health monitoring to enable early intervention and support usage-based pricing models.

- January 2026: Pet Service Holding N.V. (Netherlands) entered a multi-year partnership with Figo Pet Insurance to distribute pet insurance via B2C platforms including Dierenapotheek.nl and Pharmacy4Pets.nl, targeting one million plus pet-owning customers with an initial rollout in the Netherlands and expansion to Germany.

- January 2026: Clear Group (UK) acquired Shire Insurance Services Limited, a specialist veterinary sector broker with about GBP 7 million GWP, expanding its UK Retail division’s capabilities in veterinary insurance.

Europe Pet Insurance Market Report Scope

Pet insurance is an insurance policy bought by a pet owner which helps to lessen the overall costs of expensive veterinary bills. This coverage is similar to health insurance policies for humans. Pet insurance will cover, either entirely or in part, the often expensive veterinary procedures. The Europ pet insurance market is one of the most widely demanded in the world, as people are keen to adopt pets. A complete background analysis of the Europe Pet Insurance Market, which includes an assessment of the economy, a market overview, market size estimation for key segments, emerging trends in the market, market dynamics, and key company profiles, is covered in the report. The Europe Pet Insurance Market Report is Segmented by Policy Type (Pet Health Insurance, Pet Liability Insurance), Animal Type (Dogs, Cats), Sales Channel (Direct To Consumer, Broker/Agent, Bancassurance, and More), Coverage Level (Basic ≤EUR 1, 000, Standard ≤EUR 5, 000, and More), and Geography (United Kingdom, Germany, France, Spain, Italy, and more). The report offers market size and forecasts for the Europe Pet Insurance Market in value (USD) for all the above segments.

By Policy Type

| Pet Health Insurance |

| Pet Liability Insurance |

By Animal Type

| Dogs |

| Cats |

By Sales Channel

| Direct to Consumer |

| Broker / Agent |

| Bancassurance |

| Online Aggregators & Insurtech Platforms |

By Coverage Level

| Basic (≤ €1 000 annual cap) |

| Standard (≤ €5 000 annual cap) |

| Comprehensive (Unlimited / higher caps) |

By Country

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| BENELUX (Belgium, Netherlands, and Luxembourg) |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) |

| Rest of Europe |

| By Policy Type | Pet Health Insurance |

| Pet Liability Insurance | |

| By Animal Type | Dogs |

| Cats | |

| By Sales Channel | Direct to Consumer |

| Broker / Agent | |

| Bancassurance | |

| Online Aggregators & Insurtech Platforms | |

| By Coverage Level | Basic (≤ €1 000 annual cap) |

| Standard (≤ €5 000 annual cap) | |

| Comprehensive (Unlimited / higher caps) | |

| By Country | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe |

Key Questions Answered in the Report

What is the Europe pet insurance market size outlook to 2031?

The Europe pet insurance market size is USD 6.20 billion in 2026 and is forecast to reach USD 9.20 billion by 2031 at an 8.2% CAGR.

Which segments grow fastest in the Europe pet insurance market?

Pet Health Insurance is projected to post a 9.20% CAGR, cats are set to grow at 10.1% CAGR, online aggregators and insurtech platforms at 11.8%, and Comprehensive coverage at 10.5% over 2026?2031.

Which country leads and which is growing fastest in Europe?

The United Kingdom led with 45.3% share in 2025, while Italy is forecast to grow fastest at 9.5% CAGR during 2026?2031.

What is driving premium growth for the Europe pet insurance market in 2026?

Elevated veterinary fee indices, consolidation among clinics, and microchipping mandates are key drivers, alongside rapid expansion of digital distribution and automation?led claims.

How are regulators influencing the Europe pet insurance market in 2026?

The FCA identified pet insurance for monitoring on pricing and consumer understanding, while UK proposals seek more transparent veterinary pricing, shaping product terms and service.

What service innovations stand out in Europe pet insurance?

Direct pay to veterinarians at checkout, automated claims with high straight through rates, and real time coverage verification for clinics are setting new experience standards.

Page last updated on: