Ornithine Transcarbamylase (OTC) Deficiency Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

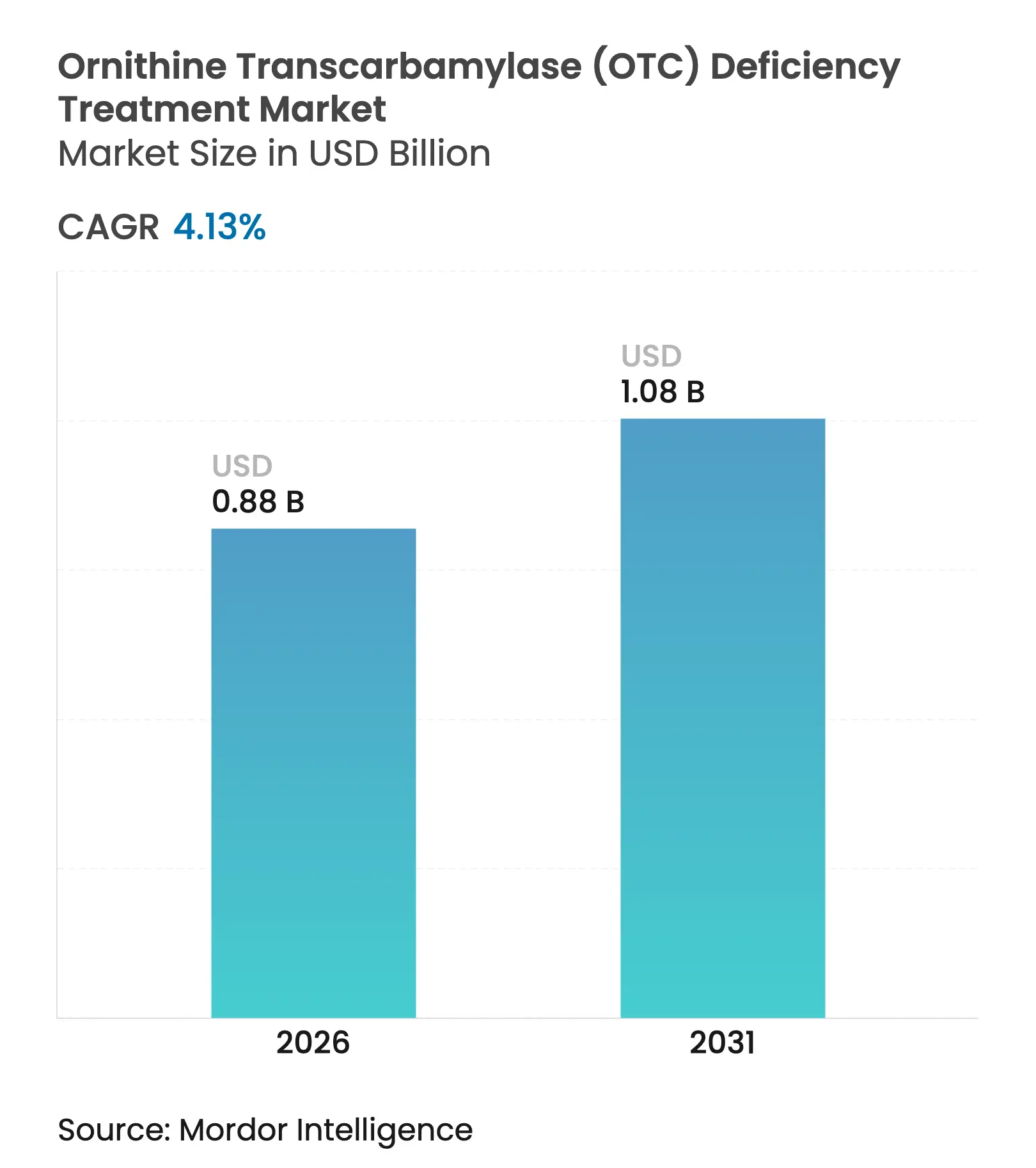

| Market Size (2026) | USD 0.88 Billion |

| Market Size (2031) | USD 1.08 Billion |

| Growth Rate (2026 - 2031) | 4.13 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Ornithine Transcarbamylase (OTC) Deficiency Treatment Market Analysis by Mordor Intelligence

The ornithine transcarbamylase deficiency treatment market size was valued at USD 0.849 billion in 2025 and estimated to grow from USD 0.88 billion in 2026 to reach USD 1.08 billion by 2031, at a CAGR of 4.13% during the forecast period (2026-2031). Growth follows rapid progress in gene‐replacement and gene‐editing technologies, wider newborn screening, and an active regulatory environment that prioritizes rare‐disease drug approvals. Small-molecule nitrogen scavengers still dominate prescriptions, yet curative therapies are moving from proof of concept toward commercialization as Ultragenyx, iECURE, and Moderna report pivotal-stage milestones. Payers and manufacturers are experimenting with value-based contracts to reconcile high one-time therapy prices with lifelong budget savings, while digital ammonia monitors and tele-metabolic clinics expand safe home management. Vector-manufacturing capacity remains the chief operational bottleneck, but new plants under construction in the United States and Europe are expected to alleviate supply constraints by 2027.

Key Report Takeaways

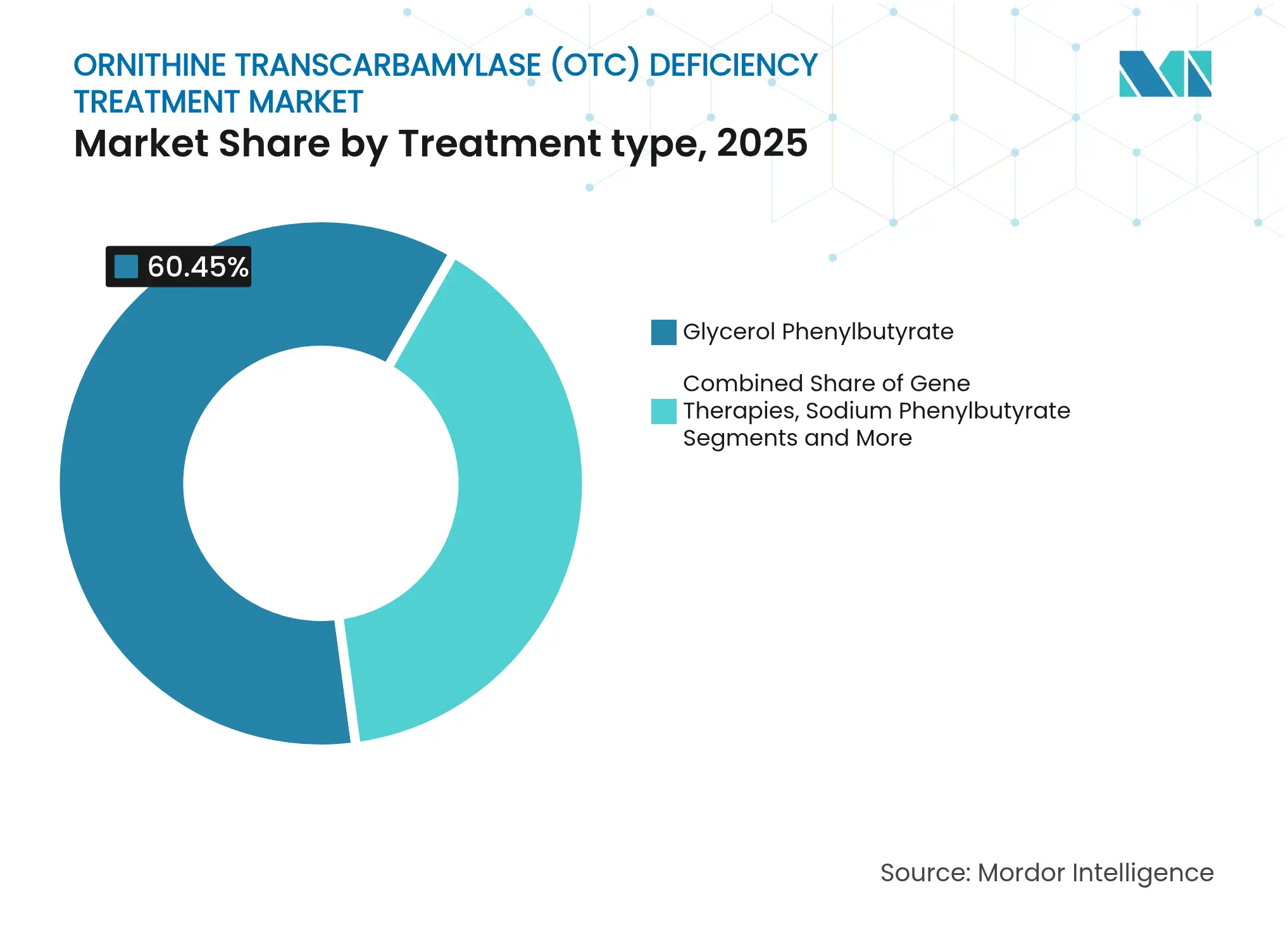

- By treatment type, glycerol phenylbutyrate led with 60.45% of ornithine transcarbamylase deficiency treatment market share in 2025; gene therapies are on track for the fastest 6.55% CAGR through 2031.

- By therapy modality, small-molecule nitrogen scavengers held 81.95% revenue in 2025, while gene replacement and editing are projected to grow at a 7.18% CAGR to 2031.

- By route of administration, oral products accounted for 80.60% of the ornithine transcarbamylase deficiency treatment market size in 2025; intravenous options will expand at a 5.62% CAGR as gene therapies launch.

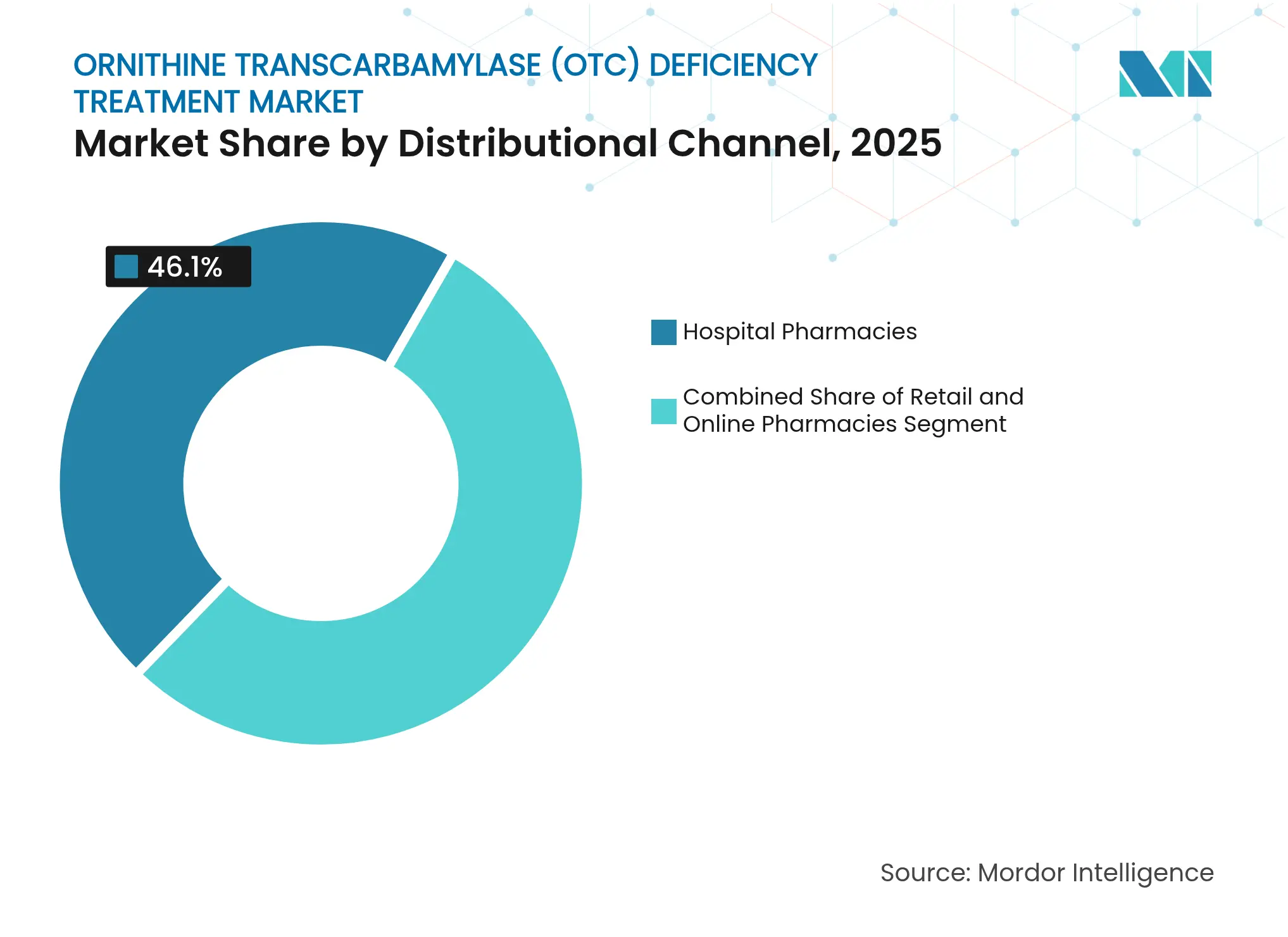

- By distribution channel, hospital pharmacies captured 46.10% revenue in 2025; online pharmacies post the highest 7.85% CAGR outlook to 2031.

- By patient age group, late-onset cases (≥28 days) comprised 67.80% share of the ornithine transcarbamylase deficiency treatment market size in 2025; neonatal-onset diagnoses are projected to rise at a 5.84% CAGR through 2031.

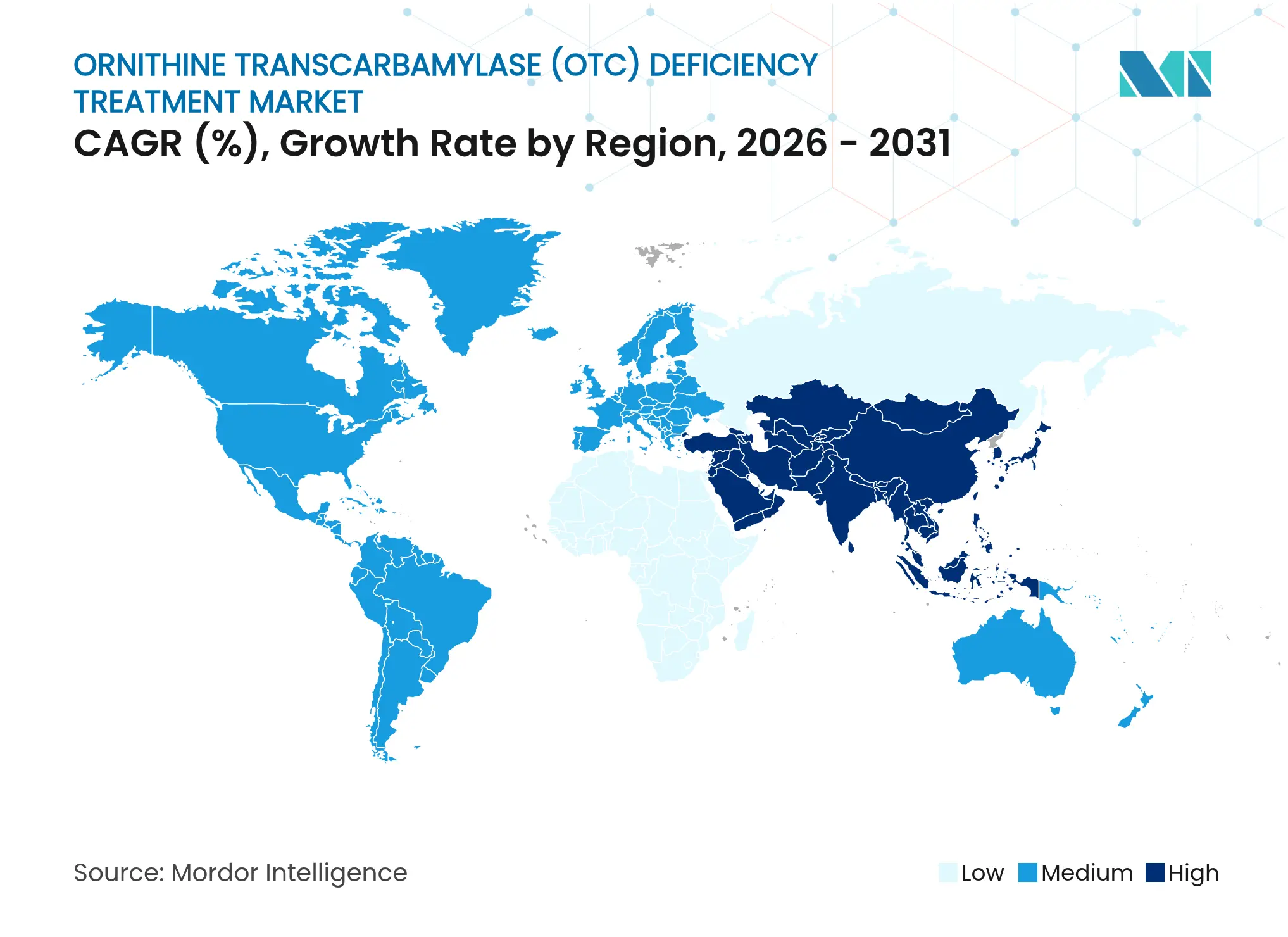

- Regionally, North America held a 43.90% revenue share in 2025; Asia-Pacific is the fastest-growing geography with a 6.33% CAGR expected to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ornithine Transcarbamylase (OTC) Deficiency Treatment Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising product approvals and richer

late-stage pipeline

Rising product approvals and richer

late-stage pipeline

| +1.2% | Global, North America leading | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:

+1.2%

|

Geographic Relevance

:

Global, North America leading

|

Impact Timeline

:

Medium term (2-4 years)

|

Growing reimbursement support and

patient-assistance programs

Growing reimbursement support and

patient-assistance programs

| +0.8% | North America & European Union | Short term (≤ 2 years) | |||

Intensifying public- and

private-sector awareness campaigns

Intensifying public- and

private-sector awareness campaigns

| +0.5% | Global | Long term (≥ 4 years) | |||

Breakthrough mRNA / gene-editing

platforms enabling once-and-done cures

Breakthrough mRNA / gene-editing

platforms enabling once-and-done cures

| +1.1% | North America & EU core, APAC emerging | Long term (≥ 4 years) | |||

Expansion of digital newborn

screening and AI-based phenotyping tools

Expansion of digital newborn

screening and AI-based phenotyping tools

| +0.6% | APAC core, spill-over global | Medium term (2-4 years) | |||

Increasing home ammonia monitoring

and tele-metabolic clinics

Increasing home ammonia monitoring

and tele-metabolic clinics

| +0.4% | Global | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Product Approvals and Richer Late-Stage Pipeline

Multiple breakthrough designations and pivotal completions are widening therapeutic choice sets. Ultragenyx finished Phase 3 enrollment of 37 patients in its Enh3ance study for DTX301, aiming to cut 24-hour ammonia exposure and end chronic scavenger use. In June 2024 the FDA cleared Acer Therapeutics’ Olpruva, the first oral suspension of sodium phenylbutyrate, offering easier dosing for pediatrics. iECURE recorded a complete clinical response in the first infant dosed with ECUR-506 gene editing therapy in January 2025, setting a new benchmark for neonatal interventions. Moderna’s mRNA-3705 entry into the FDA START pilot adds momentum to mRNA-based enzyme replacement. Precedent approvals such as Lenmeldy for metachromatic leukodystrophy show regulators are comfortable with complex gene therapies, indirectly smoothing the ornithine transcarbamylase deficiency treatment market pathway.

Breakthrough mRNA / Gene-Editing Platforms Enabling Once-And-Done Cures

Personalized CRISPR and lipid-nanoparticle mRNA platforms have produced curative-level signals. Children’s Hospital of Philadelphia documented the first customized base-editing rescue in a newborn with CPS1 deficiency, validating a template for future OTCD variants. High-throughput AAV manufacturing now reaches 8.14 × 10¹⁰ vg/mL with 85-95% recovery, driving down cost per dose.[1]Kevin J. Cirka, “Advanced Biomanufacturing and Evaluation of Adeno-Associated Virus Vectors,” Journal of Biological Engineering, springeropen.com Moderna’s LNP carrier restored ureagenesis in preclinical argininosuccinic aciduria, affirming cross-applicability within the urea-cycle cluster.[2]Maria L. Giovannini, “mRNA Therapy Corrects Defective Glutathione Metabolism and Restores Ureagenesis in Preclinical Argininosuccinic Aciduria,” Science Translational Medicine, science.org The N=1 Collaborative, launched in 2024, supplies regulatory and manufacturing scaffolds for single-patient antisense solutions. Despite progress, productive capacity for clinical-grade vectors remains tight, making manufacturing the gating factor for the ornithine transcarbamylase deficiency treatment market.

Expansion of Digital Newborn Screening & AI-Based Phenotyping Tools

Machine-learning classifiers achieved 93.42% sensitivity for inherited metabolic disease detection in neonatal dried-blood-spot data, promising broader early OTCD capture once adopted.[3]Xiaoyun Li, “Machine-Learning Classifiers Enhance Neonatal Screening Accuracy for Inherited Metabolic Diseases,” Frontiers in Pediatrics, frontiersin.org Only seven US states screen for OTCD today, but momentum is growing as digital filters prove low false-positive rates. Portable ammonia analyzers developed at Stanford deliver one-minute results from a single capillary drop, enabling home testing. UCLA’s tandem-reaction sensor tracks 800 metabolites continuously, allowing clinicians to pre-empt decompensation events. Regulatory frameworks for digital diagnostics are still evolving, yet real-time metabolite insight is expected to reduce hospitalization frequency and drug wastage.

Growing Reimbursement Support & Patient-Assistance Programs

The Centers for Medicare & Medicaid Services proposed a 6.4% CAR-T base-rate increase that signals willingness to recalibrate bundled payments for high-cost biologics, a move gene-therapy sponsors view as precedent for OTCD value-based payments. The American Society of Gene & Cell Therapy argues that rare-disease reimbursement must match FDA labels, noting that only 5% of disorders have approved therapies. Subscription and milestone-outcome models are under evaluation to smooth payer cash flow in North America and Europe. Amgen’s integrated support hub for RAVICTI and BUPHENYL simplifies benefit verification and co-pay assistance, helping maintain adherence.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High drug costs amid constrained

rare-disease budgets

High drug costs amid constrained

rare-disease budgets

| −0.9% | Global | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:

−0.9%

|

Geographic Relevance

:

Global

|

Impact Timeline

:

Short term (≤ 2 years)

|

Ultra-small patient pool limits

clinical-trial scalability

Ultra-small patient pool limits

clinical-trial scalability

| −0.6% | Global | Long term (≥ 4 years) | |||

Complex CMC and vector-manufacturing

bottlenecks

Complex CMC and vector-manufacturing

bottlenecks

| −0.8% | North America & EU | Medium term (2-4 years) | |||

Sparse long-term safety data dampens

payer uptake

Sparse long-term safety data dampens

payer uptake

| −0.5% | Global | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

High Drug Costs Amid Constrained Rare-Disease Budgets

Curative therapies price above USD 1 million, placing strain on public payers that operate within fixed annual envelopes. Specialist centers must invest in clean-room suites and post-therapy monitoring infrastructure, adding hidden costs that administrations often overlook. Prior authorization hurdles delay treatment starts, and in emerging markets reimbursement can be limited to salvage scenarios, widening geographic disparity. Risk-sharing deals that incorporate outcome triggers are being piloted but remain administratively heavy, slowing adoption.

Ultra-Small Patient Pool Limits Clinical-Trial Scalability

Ornithine transcarbamylase deficiency affects roughly 1 in 56,000 live births; site competition for eligible volunteers extends enrollment timelines and inflates per-patient costs. Cross-border master protocols and synthetic-control arms are being used to enlarge evaluable datasets, yet regulators still request multi-year follow-up, extending development spend. Sponsors are therefore selective about variant coverage, potentially leaving ultra-rare genotypes underserved.

Segment Analysis

By Treatment Type: Gene Therapies Drive Innovation Despite Nitrogen-Scavenger Dominance

Glycerol phenylbutyrate retained a 60.45% slice of ornithine transcarbamylase deficiency treatment market share in 2025 thanks to strong reimbursement, once-daily dosing, and tolerability data. Sodium phenylbutyrate’s new suspension formulation Olpruva widened pediatric uptake, while sodium phenylacetate + sodium benzoate remains indispensable for emergent decompensations. Gene therapies, although commercially nascent, are forecast to post a 6.55% CAGR as late-phase assets mature, underlining a shift toward curative intent within the ornithine transcarbamylase deficiency treatment market.

The ornithine transcarbamylase deficiency treatment market size for gene therapies could increase fivefold between 2026 and 2031 if just one candidate secures FDA approval and achieves 50% penetration of eligible neonates. Adjunct dietary supplements from Danone and Abbott offer protein-restricted formulations that complement pharmacologic regimens, particularly in regions where gene therapies remain unaffordable. Personalized antisense projects incubated by the N=1 Collaborative exemplify next-generation stratification that could eventually shrink the residual addressable pool for broad gene vectors.

Note: Segment shares of all individual segments available upon report purchase

By Therapy Modality: Small-Molecule Dominance Faces Gene Replacement Disruption

Small-molecule nitrogen scavengers commanded 81.95% of 2025 revenue, yet their CAGR outlook is half that of gene replacement platforms. Product familiarity, chronic dosing, and established safety records underpin current leadership. Nonetheless, proof-of-concept CRISPR successes and mRNA corrections suggest a meaningful transition toward once-and-done modalities.

Future uptake hinges on expanding vector manufacturing and real-world durability evidence. The ornithine transcarbamylase deficiency treatment market size attributable to gene replacement could reach USD 0.33 billion by 2031 at the projected CAGR, still below scavenger turnover but closing the gap. Nutrition-based adjuncts, though low value individually, create stickiness within multidisciplinary care bundles and reinforce dietary adherence.

By Route of Administration: Oral Convenience Versus Intravenous Innovation

Oral formulations captured 80.60% revenue in 2025, reflecting patient preference for at-home dosing and simplified logistics. Phenylbutyrate suspension has reduced pill burden, improving compliance in children. Intravenous delivery, currently reserved for acute crises and investigational gene therapies, carries a higher per-dose cost and requires specialized settings, but its share will expand to finance curative approaches.

As pipeline vectors migrate to outpatient infusion centers, the ornithine transcarbamylase deficiency treatment market will increasingly bifurcate: oral for chronic management, IV for definitive correction. Lipid-nanoparticle mRNA may eventually allow subcutaneous administration, but regulatory acceptance of newer routes remains several years away.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

By Distribution Channel: Hospital Pharmacies Lead Amid Online Growth

Hospital pharmacies realized 46.10% of 2025 sales, driven by emergency antidote stocking policies and inpatient gene therapy infusions. Retail outlets handle stable chronic scripts, yet online dispensaries are closing gaps in rural coverage by shipping temperature-controlled scavengers directly to homes. The 7.85% CAGR forecast for online channels aligns with tele-metabolic adoption and integrated digital monitoring platforms.

Regulatory tightening on internet pharmacies mandates pharmacist counseling for nitrogen scavengers, ensuring clinical oversight persists despite virtual fulfillment. When gene therapies move from single-site centers into regional hospitals, associated supporting medications will likely migrate to integrated health-system specialty pharmacies, preserving hospital dominance for complex products.

Note: Segment shares of all individual segments available upon report purchase

By Patient Age Group: Late-Onset Recognition Drives Market Expansion

Late-onset cases accounted for 67.80% revenue in 2025 as improved diagnostics uncovered symptomatic adults, especially heterozygous women. Neonatal-onset incidence appears steady, but screening expansion and earlier intervention push its CAGR to 5.84%, outperforming the overall ornithine transcarbamylase deficiency treatment market. Curative therapies target neonates because earlier enzyme restoration prevents irreversible neurologic damage, suggesting market composition will gradually rebalance toward the youngest cohort.

Adult carriers remain medically significant; psychiatric and cognitive manifestations drive healthcare utilization and necessitate monitoring. Treatment plans for late-onset patients increasingly integrate telehealth check-ins, digital ammonia sensors, and flexible scavenger regimens, maintaining a sizeable chronic-care revenue base even as gene therapies reshape pediatric management.

Geography Analysis

North America held 43.90% of global revenue in 2025, underpinned by robust insurance coverage, specialist centers, and early regulatory approvals. The FDA Rare Disease Innovation Hub streamlines coordination between drug-review divisions, shortening review times. Yet OTCD newborn screening remains uneven across states, restricting early identification.

Europe combines centralized EMA procedures with nationally heterogeneous funding. Western markets reimburse most scavengers, while Central and Eastern Europe encounter slower health technology assessment cycles that delay uptake. The EU-wide Joint Clinical Assessment initiative should harmonize evidence requirements post-2025, benefiting ornithine transcarbamylase deficiency treatment market access.

Asia-Pacific delivers the highest 6.33% CAGR outlook. Japan’s Orphan Drug Program grants premium pricing and 10-year exclusivity, incentivizing local trials. Australia and South Korea add to regional momentum through expanded newborn-screen mandates and technology-transfer partnerships. Budget constraints in Indonesia, Thailand, and India temper immediate volume, but multinational awareness campaigns and telemedicine are closing diagnostic gaps.

Competitive Landscape

Market Concentration

Market concentration is moderate. Amgen’s 2023 acquisition of Horizon secured control over the RAVICTI–BUPHENYL franchise, effectively locking in the chronic oral segment. Ultragenyx and iECURE front-run the gene-therapy race, with Moderna a credible mRNA challenger. Strategic moves highlight manufacturing: Roche’s new facility, Kyowa Kirin’s Orchard buyout, and smaller CDMOs scaling AAV lines.

Partnerships between innovators and payers test outcome-based reimbursement for curative therapies, while patient‐advocacy alliances influence policy change. Digital-health entrants collaborate with drug makers to bundle monitoring devices with prescriptions, creating ecosystem moats. As pivotal gene-therapy data matures, incumbents may acquire or license these assets to protect share, suggesting a fresh consolidation wave from 2026 onward.

Ornithine Transcarbamylase (OTC) Deficiency Treatment Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Arcturus Therapeutics announced positive Phase 2 interim data for ARCT-810, an mRNA candidate that restored OTC activity and reduced hyperammonemia episodes.

- January 2025: iECURE reported a complete clinical response in the first infant dosed with ECUR-506 gene-editing therapy for neonatal-onset OTCD.

- April 2024: iECURE received FDA IND clearance for the OTC-HOPE study evaluating ECUR-506 in newborn males with genetically confirmed OTCD.

Table of Contents for Ornithine Transcarbamylase (OTC) Deficiency Treatment Industry Report

1. Introduction

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising Product Approvals & Richer Late-Stage Pipeline

- 4.2.2Growing Reimbursement Support & Patient-Assistance Programs

- 4.2.3Intensifying Public- & Private-Sector Awareness Campaigns

- 4.2.4Breakthrough Mrna / Gene-Editing Platforms Enabling Once-And-Done Cures

- 4.2.5Expansion Of Digital Newborn Screening & AI-Based Phenotyping Tools

- 4.2.6Increasing Home Ammonia-Monitoring & Tele-Metabolic Clinics

- 4.3Market Restraints

- 4.3.1High Drug Costs Amid Constrained Rare-Disease Budgets

- 4.3.2Ultra-Small Patient Pool Limits Clinical-Trial Scalability

- 4.3.3Complex CMC & Vector-Manufacturing Bottlenecks For Gene Therapies

- 4.3.4Sparse Long-Term Safety Data Dampens Payer Uptake

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technology Outlook

- 4.7Porter’s Five Forces Analysis

- 4.7.1Bargaining Power of Suppliers

- 4.7.2Bargaining Power of Buyers

- 4.7.3Threat of New Entrants

- 4.7.4Threat of Substitutes

- 4.7.5Intensity of Competitive Rivalry

5. Market Size and Growth Forecasts (Value-USD)

- 5.1By Treatment Type

- 5.1.1Glycerol Phenylbutyrate

- 5.1.2Sodium Phenylbutyrate

- 5.1.3Sodium Phenylacetate + Sodium Benzoate

- 5.1.4Gene Therapies

- 5.1.5Dietary Supplements & Amino-acid Blends

- 5.2By Therapy Modality

- 5.2.1Small-molecule Nitrogen-Scavengers

- 5.2.2Gene Replacement / Editing

- 5.2.3Nutrition-based Adjuncts

- 5.3By Route of Administration

- 5.3.1Oral

- 5.3.2Intravenous

- 5.4By Distribution Channel

- 5.4.1Hospital Pharmacies

- 5.4.2Retail Pharmacies

- 5.4.3Online Pharmacies

- 5.5By Patient Age Group

- 5.5.1Neonatal-Onset (< 28 days)

- 5.5.2Late-Onset (≥ 28 days)

- 5.6By Geography

- 5.6.1North America

- 5.6.1.1United States

- 5.6.1.2Canada

- 5.6.1.3Mexico

- 5.6.2Europe

- 5.6.2.1Germany

- 5.6.2.2United Kingdom

- 5.6.2.3France

- 5.6.2.4Italy

- 5.6.2.5Spain

- 5.6.2.6Rest of Europe

- 5.6.3Asia-Pacific

- 5.6.3.1China

- 5.6.3.2Japan

- 5.6.3.3India

- 5.6.3.4Australia

- 5.6.3.5South Korea

- 5.6.3.6Rest of Asia-Pacific

- 5.6.4Middle East and Africa

- 5.6.4.1GCC

- 5.6.4.2South Africa

- 5.6.4.3Rest of Middle East and Africa

- 5.6.5South America

- 5.6.5.1Brazil

- 5.6.5.2Argentina

- 5.6.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1Amgen Inc.

- 6.3.2Bausch Health Companies Inc.

- 6.3.3Ultragenyx Pharmaceutical Inc.

- 6.3.4Zevra Therapeutics

- 6.3.5Arcturus Therapeutics Inc.

- 6.3.6iECURE

- 6.3.7Danone Group (Nutricia)

- 6.3.8Abbott Laboratories

- 6.3.9Nestlé Health Science

- 6.3.10Reckitt Benckiser

- 6.3.11Moderna Inc.

- 6.3.12Eurocept (Lucane Pharma)

- 6.3.13UniQure N.V.

- 6.3.14Astellas Gene Therapies

- 6.3.15AstraZeneca

- 6.3.16Asklepios BioPharmaceutical

- 6.3.17Generation Bio

- 6.3.18OrphanPacific Inc.

- 6.3.19Immedica Pharma AB

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-need Assessment

Global Ornithine Transcarbamylase (OTC) Deficiency Treatment Market Report Scope

Ornithine transcarbamylase deficiency is a rare genetic condition that results in ammonia building up in the blood. This condition is more prominently seen in boys than girls and tends to be more severe when symptoms emerge shortly after birth. Ornithine transcarbamylase deficiency is caused by changes in the OTC gene, which instructs the body to make the OTC enzyme. In OTC deficiency, the OTC gene is either damaged or missing.

The ornithine transcarbamylase (OTC) deficiency treatment market is segmented into treatment type, route of administration, distribution channel, and geography. The market is segmented by treatment type into glycerol phenylbutyrate, sodium phenylbutyrate, sodium phenylacetate and sodium benzoate, and other treatment types. By route of administration, the market is segmented into oral and intravenous. By distribution channel, the market is segmented into hospital pharmacies, retail pharmacies, online pharmacies, and other distribution channels. By geography, the market is segmented into North America, Europe, Asia-Pacific, and Rest of the World. The report also offers the market sizes and forecasts for 13 countries across the region. For each segment, the market size and forecast are provided in terms of value (USD).