Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

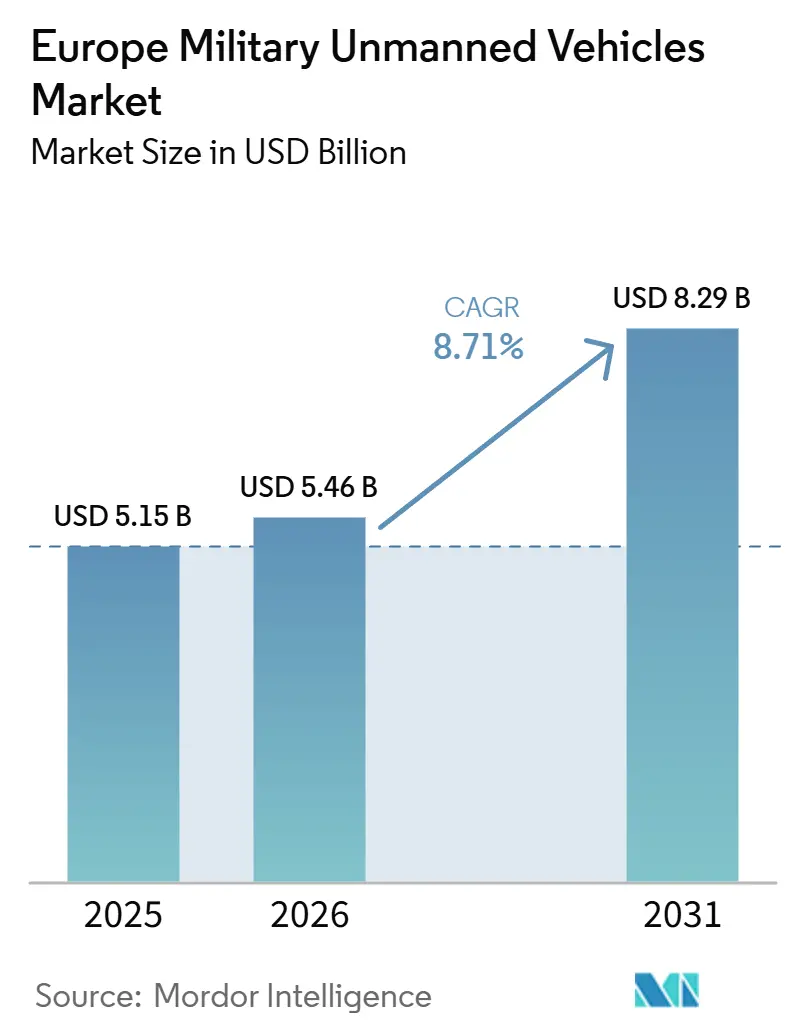

| Base Year Market Size (2025) | USD 5.15 Billion |

| Market Size (2026) | USD 5.46 Billion |

| Market Size (2031) | USD 8.29 Billion |

| Growth Rate (2026 - 2031) | 8.71% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Military Unmanned Vehicles Market Analysis by Mordor Intelligence

The Europe military unmanned vehicles market size is expected to grow from USD 5.15 billion in 2025 to USD 5.46 billion in 2026 and is forecast to reach USD 8.29 billion by 2031 at 8.71% CAGR over 2026-2031. The growth profile reflects accelerated procurement in core programs, rapid progress in AI-enabled autonomy, and the steady shift toward multi-domain unmanned concepts that reduce personnel risk in contested environments. Germany’s procurement cycle gains momentum in 2026 on loitering munitions and collaborative combat systems, while NATO mine-countermeasures and Baltic maritime security elevate undersea robotics to a strategic priority. The UK anchors capability in long-endurance ISR with Protector RG Mk1 and aligns regional adoption with NATO interoperability requirements. EU-wide policy, funding, and testbed expansion accelerate regulatory approval for counter-drone deployments and spur local supply chains in Germany, France, the Nordics, and Poland. The market is also shaped by persistent electronic warfare (EW) risks, fragmented certification requirements, and semiconductor supply considerations that reward resilient designs and dual-sourced components.

Key Report Takeaways

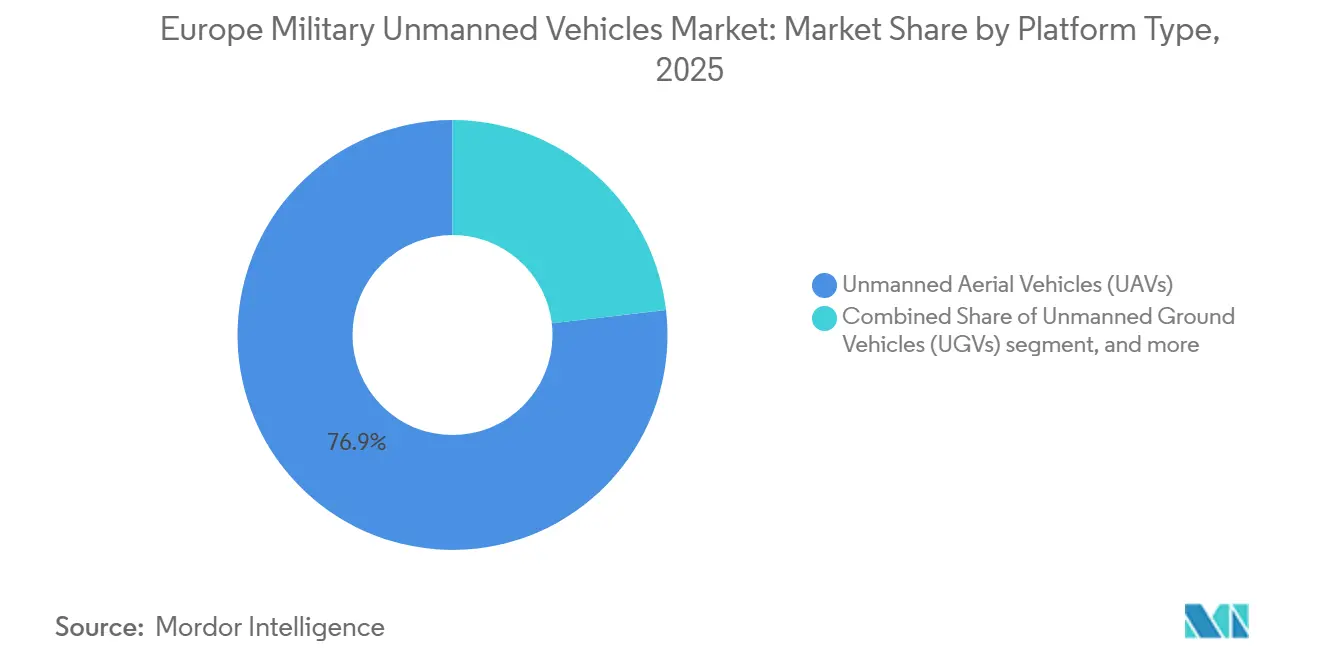

- By platform type, unmanned aerial vehicles (UAVs) led with 76.86% revenue share of the Europe military unmanned vehicles market in 2025, and unmanned marine vehicles (UMVs) are projected to expand at a 13.99% CAGR through 2031.

- By mode of operation, remotely piloted systems held a 46.24% share of the Europe military unmanned vehicles market in 2025, and fully autonomous platforms are projected to expand at a 11.24% CAGR through 2031.

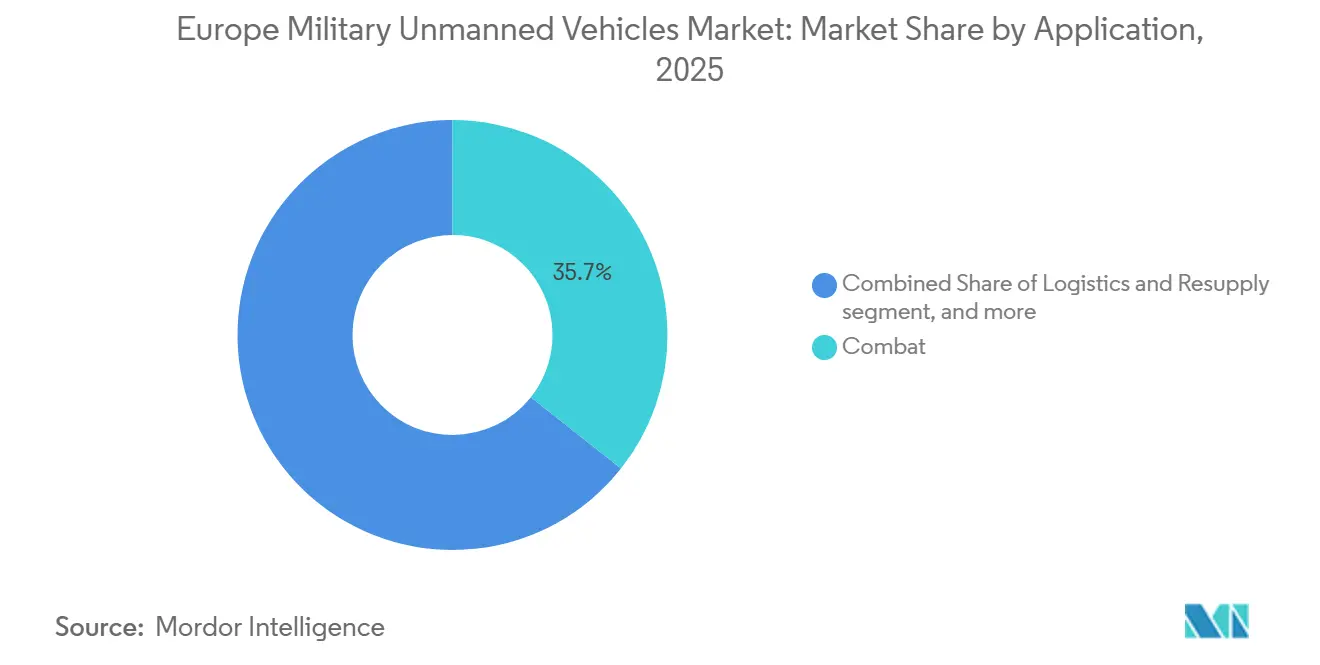

- By application, combat accounted for a 35.67% share of the Europe military unmanned vehicles market in 2025, while logistics and resupply are projected to expand at a 10.14% CAGR through 2031.

- By vehicle size, small platforms captured a 41.23% share of the Europe military unmanned vehicles market in 2025 and are advancing at a 9.87% CAGR through 2031.

- By geography, the United Kingdom led with a 28.45% share of the Europe military unmanned vehicles market in 2025, while Germany is projected to expand at a 9.56% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Military Unmanned Vehicles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Operational success of low-cost attritable drone swarms in Ukraine influencing European defense strategies | 2.30% | CEE and Nordics, spreading westward | Short term (≤ 2 years) |

| Large EU and NATO modernization programs driving adoption of autonomous and unmanned systems | 2.10% | EU+NATO members, focus in Germany, France, UK, Poland | Medium term (2-4 years) and Long term (≥ 4 years) |

| Rising defense budgets in Europe accelerating procurement of multi-domain unmanned platforms | 1.80% | EU core, Nordic, UK | Medium term (2-4 years) |

| Advancements in AI-enabled autonomy improving mission efficiency and reducing manpower risks | 1.60% | Global, early adoption in UK, Germany, France, Nordics | Medium term (2-4 years) |

| EU action plans on drone and counter-drone security unlocking new funding and development initiatives | 1.40% | EU-27, pilots in Poland, Romania, Baltic states | Short term (≤ 2 years) and Medium term (2-4 years) |

| Emergence of European tier-2 and tier-3 suppliers strengthening the regional unmanned systems ecosystem | 0.90% | Estonia, Germany, Portugal, France, VC hubs in Berlin, Paris, London | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Defense Budgets Accelerate Multi-Domain Unmanned Procurement

European defense spending increased in 2025 and continues to prioritize unmanned platforms in land, air, and maritime missions, supporting scale and recurring procurement cycles across the Europe military unmanned vehicles market. Germany allocated significant funding for unmanned capabilities, including a joint loitering-munition award planned for 2026, as part of efforts to develop hundreds of collaborative aircraft. Poland's defense spending emphasizes counter-UAS systems with high interception success rates and the expansion of domestic UAV production lines. France has committed substantial resources to unmanned systems through the next decade, with additional investments in AI-enabled drone development to advance domestic manufacturing and software-driven architectures, supporting long-term technological and operational objectives. These allocations target full-fleet modernization rather than incremental upgrades, which favors interoperable control systems and common payload standards across services.

EU And NATO Modernization Programs Expand Autonomous Adoption

The European Defence Fund committed EUR 7 billion (USD 8.14 billion) for 2021-2027 and has allocated a significant amount to AI and digital technologies, which underpin interoperable programs such as LEAP, launched by France, Germany, Italy, Poland, and the UK in February 2026. Sweden’s LUUV program, awarded in October 2025, integrates AI navigation for GPS-denied maritime missions and is set to move to summer 2026 trials, signaling near-term operationalization in cold-water environments. The LEAP initiative accelerates the adoption of common data-link standards to reduce duplication across national fleets and enable combined operations. The Europe military unmanned vehicles market benefits from aligned standards that ease integration into NATO task groups and facilitate cross-border readiness for ISR, logistics, and counter-mine missions.

AI-Enabled Autonomy Improves Mission Efficiency and Reduces Risk

In September 2025, Germany's Helsing introduced the AI-enabled CA-1 Europa UCAV, targeting 2029 deployment, integrating sensor fusion and real-time threat prioritization to optimize operator efficiency and accelerate decision-making processes. The UK's Protector RG Mk1, delivered in June 2025, brought AI-assisted mission planning that compresses planning activities and enables persistent ISR over extended durations. France's recent funding to scale AI-enabled drones supports supervised autonomy, which holds human authorization while delegating routine maneuvers to onboard algorithms to improve safety and tempo. Sweden demonstrated swarm control of 100 UAS in January 2025, proving that a single operator can supervise tasks that conventional workflows required multiple pilots to coordinate, with direct implications for manpower planning.[1]Defense News, “Sweden Unveils Drone Swarm to Be Paired With Ground Troops,” defensenews.com The market emphasizes software-defined payloads and autonomy stacks that shorten kill chains and lower manpower risks in high-threat air defense environments.

EU Action Plans on Drone and Counter-Drone Security Unlock New Programs

The European Commission’s Action Plan, published in February 2026, aims to accelerate regulatory harmonization to support cross-border deployments for detect-and-defeat programs. NATO’s Counter-Small UAS framework supports common testing standards and joint evaluation of jammers, interceptors, and integrated radars to guide procurement scaling. Countries in Central and Eastern Europe deploy counter-drone systems to protect bases and energy nodes, and early pilots inform larger procurements within NATO exercises. Gaps remain, as not all member states have transposed relevant annexes into national law, which sustains timing and documentation differences that complicate regional rollouts in the Europe military unmanned vehicles market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cybersecurity and EW vulnerabilities in C2 links and GNSS-dependent platforms | -1.90% | Poland, Baltic states, Finland; cascading NATO risk | Short to Medium term (1-3 years) |

| Fragmented procurement regulations and airworthiness certification across EU member states | -1.30% | EU-27, acute friction in Germany-France-Poland-Italy corridors | Medium term (2-4 years) |

| Dependence on non-European semiconductor and RF component supply chains subject to export controls | -1.20% | Global, particularly acute for Germany, France, UK defense primes | Medium to Long term (3-5 years) |

| Rising lifecycle and sustainment costs of advanced autonomous unmanned systems | -0.80% | EU-wide, most acute for MALE/HALE operators (UK, France, Germany, Italy) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented Procurement Regulations and Airworthiness Certification Across EU Member States

Certification pathways vary by country and category, introducing friction that slows cross-border deployments in the Europe military unmanned vehicles market. National testing requirements, including electromagnetic compatibility and collision-avoidance in segregated airspace, increase supplier costs across jurisdictions. These variations increase lifecycle costs and complicate sustainment planning for mixed fleets in multinational brigades, thereby impacting operational efficiency and long-term resource allocation. NATO’s STANAG 4586 harmonization is not yet comprehensive for ground and maritime controllers, which leaves multi-vendor teams to handle interface work themselves during integration. The EU Cybersecurity Act drives IEC 62443 certification for industrial controls, and many platforms still need retrofits to meet required assurance levels for connectivity and autonomy components.

Cybersecurity and EW Vulnerabilities In C2 Links And GNSS-Dependent Platforms

Persistent jamming and spoofing in Eastern Europe expose command links and navigation channels that many unmanned systems still depend on, affecting sortie reliability in the Europe military unmanned vehicles market. Poland recorded 2,732 GNSS jamming incidents in January 2025 along the Belarus and Kaliningrad borders, signaling near-continuous EW pressure in critical corridors. Programs now emphasize inertial and visual odometry as backups and seek to encrypt telemetry, but integration lags vary across legacy fleets and new procurement lots. NATO guidance and national CERTs advise layered defenses, including hardened ground stations, segmented networks, and firmware integrity checks for fielded autonomy stacks. Demand has shifted toward modular EW protection that can be updated over the air, to keep pace with adversary techniques without pulling vehicles from service. Galileo’s PRS maturation remains a policy and implementation focus, and operators maintain diversified navigation strategies for mission-critical sorties in the interim.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform Type: Marine Systems Surge on Mine-Warfare Imperatives

UAVs led with a 76.86% share in 2025, while UMVs are projected to expand at a 13.99% CAGR through 2031 as NATO prioritizes mine countermeasures and undersea security in the North Sea and Baltic theaters. The Belgian-Dutch rMCM program, valued at EUR 2.2 billion (USD 2.56 billion), delivered the first vessels in March 2026 and aims to cut per-mission costs by 50-60% by shifting high-risk clearance tasks from crewed hulls to unmanned surface and underwater vehicles. Sweden’s LUUV contract for SEK 60 million (USD 6.3 million) targets GPS-denied environments with AI-based sonar classification, and third-quarter 2026 trials will test longer patrol durations and low-latency operator oversight in cold waters.[2]Janes, “Sweden’s FMV Awards Saab Development and Demonstration Contract for LUUV,” janes.com UGVs hold a mid-teen share, with growth in logistics and EOD roles, as units field standardized platforms that integrate payloads via open interfaces to reduce maintenance and training burdens. The Europe military unmanned vehicles market continues to see UAVs as the volume driver because Group 1 and Group 2 systems scale quickly with commercial components and dual-use supply chains, especially where BVLOS is not required. Unmanned marine systems benefit from NATO-certified mission packages for mine detection and neutralization, and now receive a larger share of capital budgets as maritime choke points elevate risk profiles.

UMV adoption reshapes fleet composition by combining unmanned mother ships with autonomous mine-hunting vehicles to expand coverage without exposing crews to more IEDs. In the air domain, the United Kingdom’s Protector RG Mk1 anchors ISR modernization through AI-assisted planning, multi-sensor ensembles, and STANAG 4586 compatibility, enabling collaboration with NATO assets. Ground robotics remains essential for base logistics and EOD, and European programs now favor autonomy kits that can be refitted across multiple chassis to protect investment and avoid lock-in. The Europe military unmanned vehicles market supports common command-and-control and control station standards so teams can reallocate vehicles between ISR, logistics, and engineering missions as needed NATO. Procurement teams seek platform-agnostic autonomy layers because long-term cost savings derive from software reuse and shared training across formations in the Europe military unmanned vehicles market.

By Mode of Operation: Fully Autonomous Gains as Bandwidth Scarcity Bites

Remotely piloted systems held a 46.24% share in 2025, while fully autonomous platforms are projected to expand at a 11.24% CAGR through 2031 as contested EW environments increase the need for on-board decision loops that do not depend on constant control links. Helsing’s CA-1 Europa demonstrates coordinated multi-platform engagements with faster cycle times, aligning with NATO’s push for resilient kill chains. Sweden’s 100-UAS swarm demonstration showed that one operator can supervise complex search-and-allocation patterns across large areas, reducing manpower requirements per sortie. Semi-autonomous modes hold a mid-30s share because they allow pre-programmed routes with human authorization for key steps, balancing speed and oversight in the Europe military unmanned vehicles market. Fully autonomous growth focuses on ISR and logistics, where rules of engagement do not require immediate human authority, and autonomy supports tight timelines and sparse communications. The EU AI Act exempts military applications, but militaries continue to define operational guardrails while awaiting NATO-level guidance to standardize ethical and safety practices.

Suppliers build autonomy stacks around supervised modes that ensure an operator can intervene, thereby improving acceptance among commanders and procurement authorities in the European unmanned vehicles industry. Standardized handoff of control from remote to autonomous modes is becoming a design requirement in RF-contested areas, and airworthiness authorities continue to address safety cases for multi-vehicle operations. Training pipelines include human-machine team drills so operators can safely supervise more safely, and doctrine aligns with meaningful human control standards for engagement decisions. Over the forecast period, autonomy adoption is likely to expand from ISR and logistics to engineering and mine-countermeasure roles where on-board processing and deterministic behaviors improve mission timing in the Europe military unmanned vehicles market.

By Application: Logistics Missions Outpace Combat on Last-Mile Urgency

Combat applications led with a 35.67% share in 2025, while logistics and resupply are projected to expand at a 10.14% CAGR through 2031 as forces reduce risk on the last mile and compress delivery timelines in contested areas. Germany continues to field UGV logistics concepts for moving loads of 500 to 1,000 kilograms per sortie in support areas, reducing driver demand and speeding resupply. ISR remains a mid-20s share pillar as the United Kingdom fields Protector RG Mk1 for persistent surveillance, multi-sensor intelligence collection, and intelligence, surveillance, and reconnaissance tasking. EOD and MCM jointly secure a mid-to-high teens share, taking advantage of policy clarity to deploy autonomous systems in minefields and hazardous zones where personnel risk is highest. The Europe military unmanned vehicles market prioritizes applications that deliver measurable time savings, reduced risk, and high sustainment value, favoring logistics, ISR, and counter-mine roles as early adopters of autonomy.

As autonomy reliability improves, the Europe military unmanned vehicles market will integrate mission libraries and task packages so that logistics drones can dynamically reroute and coordinate with ISR assets to avoid threats. Combined arms concepts link ground UGVs carrying loads to aerial escorts and overwatch vehicles that apply real-time sensing to suggest safer paths. Mine-countermeasures missions see increased procurement of autonomous vehicles, which reduce crewed exposure and offer predictable cost-per-clearance for budget planning. Logistics growth is expected to be most significant in border areas and regions with critical infrastructure that require rapid replenishment under EW pressure. Additionally, growth will be supported in areas where dedicated drone corridors or waivers reduce clearance cycles under EASA frameworks.

By Vehicle Size: Small Platforms Dominate on Attritable Economics

Small vehicles captured 41.23% of the Europe military unmanned vehicles market in 2025 and are advancing at a 9.87% CAGR through 2031, as mass production, commercial components, and short training cycles favor scale. Ukraine’s 2026 target of 7 million drones illustrates how high-volume, small systems saturate defenses and create persistent tactical pressure, shaping European views on cost imposition and attrition tolerance. Medium vehicles range hold a high-20s share for hybrid missions that mix ISR, logistics, and precision effects. Large platforms such as MALE and HALE systems remain vital for strategic ISR but face capital scrutiny due to unit costs and extended airworthiness cases. The Europe military unmanned vehicles market now rewards designs that can be adapted across payloads and sizes to share autonomy, spares, and training.

Regulatory processes also shape the mix, because SORA-based authorizations add time for BVLOS and complex operations. At the same time, many small drones below 120 meters face lighter requirements or clearer waivers, depending on the mission and the airspace. Operators prefer to combine small UAS for local ISR and target handoff with medium UAS carrying heavier payloads, which enables flexible sequencing of mission tasks. The Europe military unmanned vehicle industry is seeing increased interest in common controllers and visual interfaces across platforms, enabling operators to transition quickly between platforms. Programs include hardened communications modules for small drones to maintain connectivity under jamming, helping increase sortie completion rates in contested zones.

Geography Analysis

The United Kingdom accounted for 28.45% of the Europe military unmanned vehicles market in 2025, supported by the Protector RG Mk1 program and consistent NATO interoperability requirements, while Germany is projected to lead expansion at a 9.56% CAGR through 2031, driven by loitering munitions and collaborative aircraft initiatives. The UK’s fleet modernization emphasizes AI-enabled ISR with long endurance and STANAG 4586 compliance, supporting joint missions. Germany’s February 2026 award of EUR 540 million (USD 629.10 million) for loitering munitions adds momentum to the rapid fielding of autonomous teaming.[3]Army Recognition, “Germany Approves EUR 540 Million Medium-Range Loitering Munition Procurement from Helsing and Stark Defence Firms,” armyrecognition.com Poland’s 4.7% GDP defense outlay funds counter-UAS and indigenous lines that shorten supply chains and support mass production. Spain invests in domestic drone plants and prepares for programs such as SIRTAP with 2026 flight targets to build sovereign capability in medium-class UAVs.

Nordic countries continue to pioneer autonomy in maritime and Arctic domains through robust research and testing. Sweden’s LUUV integrates AI navigation and sonar classification with trials slated for summer 2026 to validate long-duration missions in GPS-denied waters. Finland’s AI-WASP project allocates EUR 45 million (USD 52.40 million) to enhance autonomous systems in harsh climates and strengthen inter-service collaboration on unmanned capabilities. Central and Eastern Europe emphasize counter-UAS and tactical drones in national strategies, with deployments along borders and coastal areas informing program requirements and training. The Europe military unmanned vehicles market recognizes that Nordic and Benelux lessons on maritime autonomy and counter-mine packages are being incorporated into procurement templates for broader EU fleets.

Industrial policy and supply chain resilience feature prominently in continental planning. The EU Chips Act supports advanced semiconductor capacity to lower external dependencies, while a new fab in Germany by a leading global foundry signals future mitigation for defense electronics programs. Italy advances domestic UAV production through joint ventures aligned with European partners, strengthening sovereign capacity and export potential. As interoperability improves, the Europe military unmanned vehicles market aims to reduce cross-border friction and increase sortie generation rates across air, land, and sea missions.

Competitive Landscape

The Europe military unmanned vehicles market is moderately fragmented. Legacy primes such as Leonardo S.p.A., BAE Systems plc, Thales Group, Saab AB, and Airbus SE hold a substantial combined share due to integration track records and certification depth across air, land, and maritime domains. Software-native entrants expand influence with AI-enabled autonomy, modular kits, and update pipelines that reduce time to capability and sustainment costs. Airbus advanced manned-unmanned teaming with Mindshare AI to fuse multi-sensor feeds into a unified operating picture for faster decision-making by operators. Leonardo’s 2025-2029 industrial plan allocates significant capital to autonomy and collaborative systems, including a cross-border JV to scale domestic UAV production. Suppliers that can demonstrate secured telemetry, resilient PNT, and certified software pipelines are best placed to win long-duration contracts in the Europe military unmanned vehicles market.

Helsing’s momentum includes a major German contract awarded in February 2026 for loitering munitions that align with collaborative air combat concepts, which underscores the importance of over-the-air updates and rapid AI iteration for frontline readiness. Thales Group expanded its EW integration by acquiring autonomous devices in September 2025, combining sensing, classification, and jamming within these platforms. Rheinmetall AG accelerated the development of PATH autonomy kits across Germany, the Nordics, and the UK in March 2025 to adapt existing platforms more rapidly for logistics and engineering missions. BAE Systems plc signed a memorandum of understanding with Turkish Aerospace in November 2025 to explore interoperable UCAV and support NATO-aligned teaming concepts in contested airspace. The Europe military unmanned vehicles market trends favor vendors that align program baselines with NATO frameworks to streamline cross-country deployments.

Saab AB’s LUUV program validates maritime autonomy claims and places pressure on competitors to match endurance and classification performance in GPS-denied conditions. The market rewards modular payloads and common controllers that standardize training and reduce sustainment costs across fleets in the Europe military unmanned vehicles market. Suppliers who demonstrate compliance with IEC 62443 and related cybersecurity baselines strengthen bids on programs that require hardened links and authenticated updates in the field.

Europe Military Unmanned Vehicles Industry Leaders

Thales Group

BAE Systems plc

Leonardo S.p.A.

Rheinmetall AG

Saab AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: The German parliament's budgetary committee approved EUR 540 million (USD 623.40 million) for the procurement of kamikaze drones from German manufacturers Helsing and Stark Defence, ensuring advanced defense capabilities.

- January 2026: The French defense procurement agency (DGA) awarded contracts to Naval Group and Airbus Helicopters under the SDAM program to develop and supply VTOL UAVs for the French Navy's operational needs.

- January 2026: French Army tests hydrogen-powered Hermione UGV to advance AI-led combat unit development by 2027, emphasizing autonomy, energy efficiency, and seamless unit-level integration through rigorous trials supporting operational and technological readiness.

Europe Military Unmanned Vehicles Market Report Scope

Unmanned vehicles are platforms that can be remotely controlled by a human operator or navigated autonomously by a programmed onboard computer. This report examines platforms used by the armed forces for various missions.

The Europe military unmanned vehicles market is segmented based on platform type, mode of operation, application, vehicle size, and geography. By platform type, the market is segmented into unmanned aerial vehicles (UAVs), unmanned ground vehicles (UGVs), and unmanned marine vehicles (UMVs). By mode of operation, the market is segmented into remotely piloted, semi-autonomous, and fully autonomous. By application, the market is segmented into intelligence, surveillance, and reconnaissance (ISR), combat, logistics and resupply, explosive ordnance disposal (EOD), mine counter-measures (MCM), and others. By vehicle size, the market is segmented into small, medium, and large. The report also covers the market sizes and forecasts for the Europe military unmanned vehicles market in major countries across the region. For each segment, the market size is provided in terms of value (USD).

By Platform Type

| Unmanned Aerial Vehicles (UAVs) |

| Unmanned Ground Vehicles (UGVs) |

| Unmanned Marine Vehicles (UMVs) |

By Mode of Operation

| Remotely Piloted |

| Semi-Autonomous |

| Fully Autonomous |

By Application

| Intelligence, Surveillance, and Reconnaissance (ISR) |

| Combat |

| Logistics and Resupply |

| Explosive Ordnance Disposal (EOD) |

| Mine Counter-Measures (MCM) |

| Others |

By Vehicle Size

| Small |

| Medium |

| Large |

By Geography

| United Kingdom |

| Germany |

| Spain |

| Italy |

| France |

| Russia |

| Norway |

| Poland |

| Sweden |

| Rest of Europe |

| By Platform Type | Unmanned Aerial Vehicles (UAVs) |

| Unmanned Ground Vehicles (UGVs) | |

| Unmanned Marine Vehicles (UMVs) | |

| By Mode of Operation | Remotely Piloted |

| Semi-Autonomous | |

| Fully Autonomous | |

| By Application | Intelligence, Surveillance, and Reconnaissance (ISR) |

| Combat | |

| Logistics and Resupply | |

| Explosive Ordnance Disposal (EOD) | |

| Mine Counter-Measures (MCM) | |

| Others | |

| By Vehicle Size | Small |

| Medium | |

| Large | |

| By Geography | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Norway | |

| Poland | |

| Sweden | |

| Rest of Europe |

Key Questions Answered in the Report

What is the Europe military unmanned vehicles market size in 2025 and its growth outlook to 2031?

The Europe military unmanned vehicles market size is USD 5.15 billion in 2025 and is projected to reach USD 8.29 billion by 2031 at an 8.71% CAGR over 2026-2031.

Which country leads the Europe military unmanned vehicles market and which grows fastest?

The United Kingdom leads with 28.45% in 2025, while Germany records the fastest expansion with a projected 9.56% CAGR through 2031.

Which platform segment leads and which is the fastest growing across Europe?

UAVs lead with 76.86% in 2025, and UMVs are the fastest growing with a projected 13.99% CAGR through 2031, driven by mine-countermeasure programs.

What applications are expanding fastest within European defense programs?

Logistics and resupply is the fastest growing application with a projected 10.14% CAGR through 2031, while combat remains the largest at 35.67% in 2025.

How is autonomy adoption evolving in European unmanned systems?

Fully autonomous platforms are projected to grow at 11.24% CAGR as EW conditions and bandwidth limits increase the need for on-board decision loops, while remotely piloted systems retain a leading share.

What are the main risks facing the Europe military unmanned vehicles market?

Fragmented certification and cybersecurity vulnerabilities in C2 and GNSS links are the primary constraints, which increase timelines and require hardened architectures and layered EW defenses.

Page last updated on: