Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

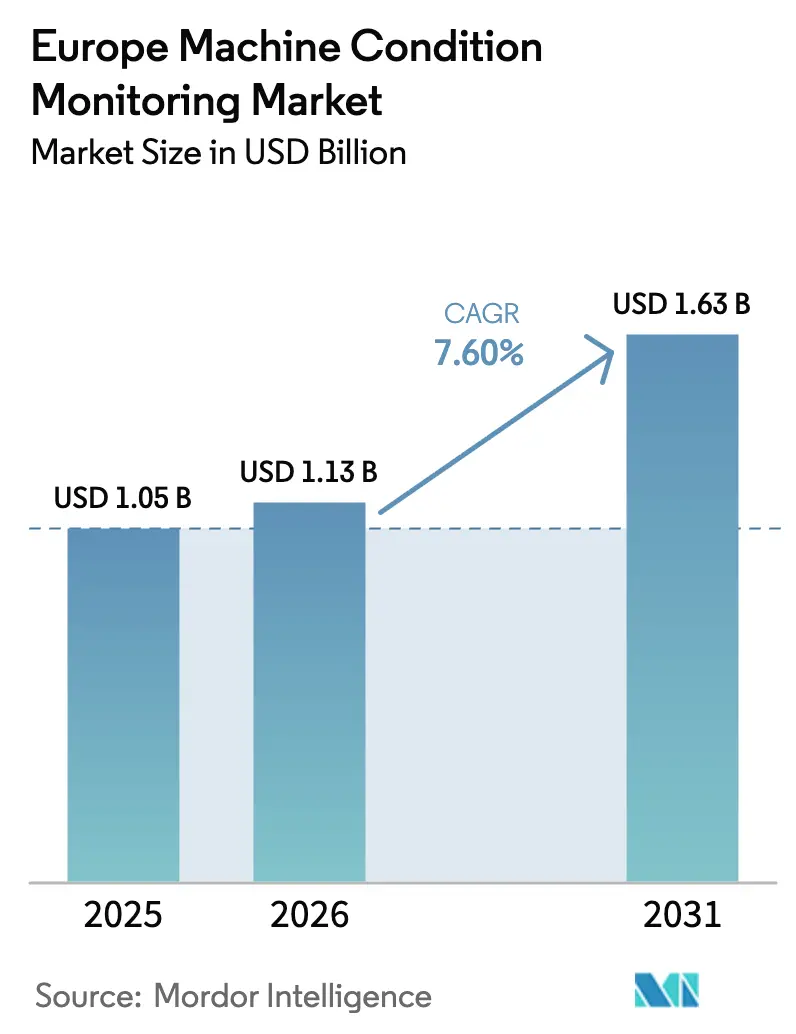

| Base Year Market Size (2025) | USD 1.05 Billion |

| Market Size (2026) | USD 1.13 Billion |

| Market Size (2031) | USD 1.63 Billion |

| Growth Rate (2026 - 2031) | 7.60% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Machine Condition Monitoring Market Analysis by Mordor Intelligence

Europe machine condition monitoring market size in 2026 is estimated at USD 1.13 billion, growing from 2025 value of USD 1.05 billion with 2031 projections showing USD 1.63 billion, growing at 7.60% CAGR over 2026-2031. This expansion aligns with accelerated Industry 4.0 programs, especially in German automotive plants and Spanish process lines, where edge-enabled diagnostics curtail downtime and avert costly line stoppages. Regulatory catalysts such as the NIS2 Directive elevate cybersecurity expectations for connected assets, prompting greater demand for secure, real-time monitoring platforms. Vendors that fuse legacy vibration analytics with artificial-intelligence-driven contextual insights gain competitive traction, while subscription pricing converts large capital outlays into manageable operating expenses. Meanwhile, Europe’s 5G rollout, together with rising labor shortages for skilled maintenance technicians, bolsters the business case for automated health-assessment solutions.

Key Report Takeaways

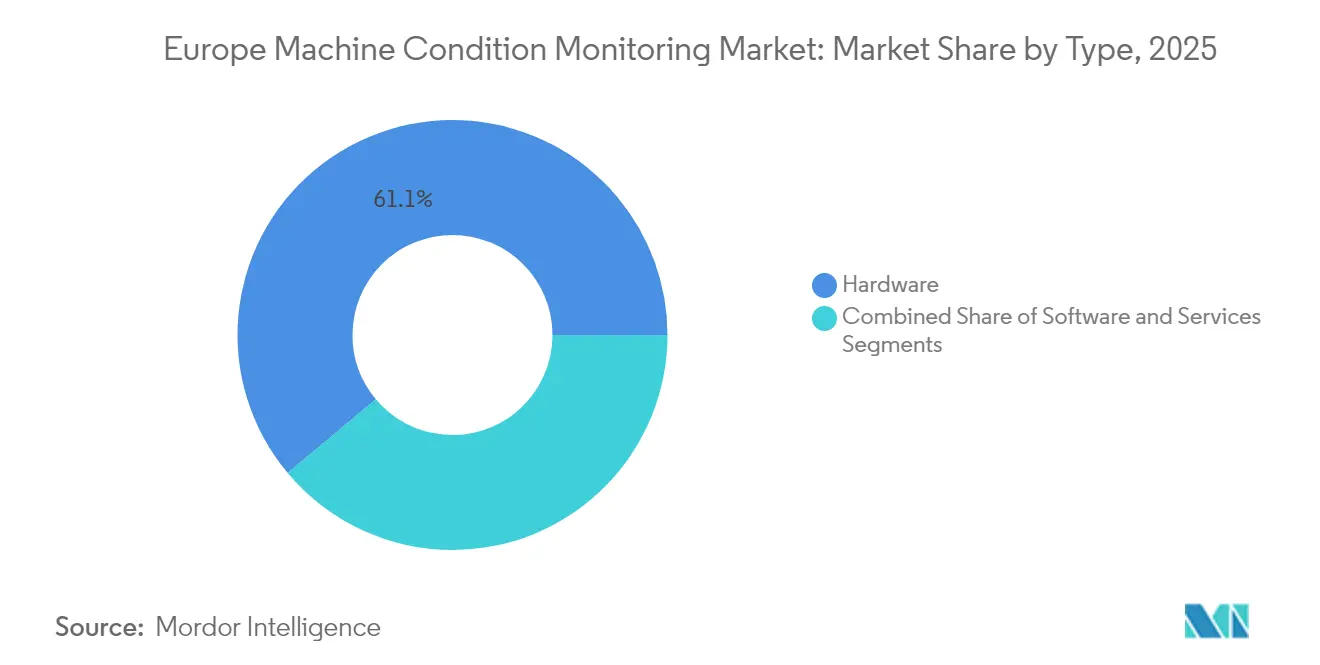

- By type, hardware led with 61.10% revenue share of the European machine condition monitoring market in 2025, whereas services are on track for the fastest 8.65% CAGR through 2031.

- By monitoring technique, online systems accounted for 56.20% of the European machine condition monitoring market share in 2025; edge-AI sensors posted the quickest 8.72% CAGR.

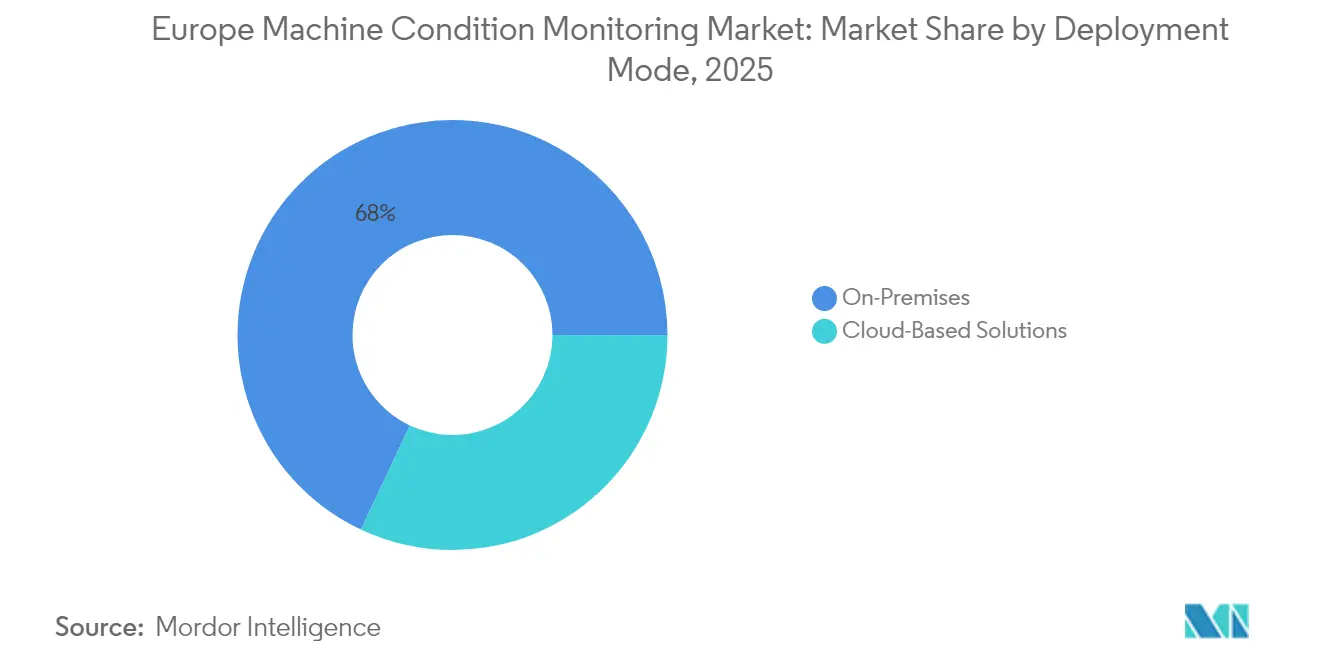

- By deployment mode, on-premises platforms dominated with a 68.00% share of the European machine condition monitoring market in 2025, while cloud solutions are set to expand at an 8.55% CAGR as security frameworks mature.

- By end-user vertical, oil and gas captured 29.90% of the European machine condition monitoring market size in 2025, and discrete manufacturing shows the strongest 9.05% CAGR to 2031.

- By country, Germany contributed 28.10% of the 2025 revenue of the European machine condition monitoring market, whereas Spain will accelerate at a 8.95% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Machine Condition Monitoring Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing equipment performance via predictive maintenance | +1.8% | Germany, France, Netherlands | Medium term (2-4 years) |

| Industry 4.0 expansion across manufacturing | +2.1% | Germany, Italy, Spain | Long term (≥ 4 years) |

| Shift toward remote operations and worker safety | +1.2% | United Kingdom, France, Germany | Short term (≤ 2 years) |

| Rising regulatory pressure on critical-infrastructure uptime | +0.9% | Germany, Netherlands, United Kingdom | Medium term (2-4 years) |

| Edge-AI smart sensors enabling real-time analytics | +1.4% | Germany, Spain, Netherlands | Long term (≥ 4 years) |

| Emergence of subscription-based monitoring platforms | +0.7% | United Kingdom, Germany, France | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Equipment Performance via Predictive Maintenance

German, French, and Dutch manufacturers now view reactive maintenance as a profit drain, with studies showing it can squander 70% of potential asset life. Germany’s Manufacturing-X consortium, backed by EUR 133 million (USD 150.5 million), blends machine-health data and production metrics to cut unplanned downtime 25-30% and stretch asset life 15-20%. Schaeffler’s online system across 58 drives at its European logistics hub delivered six-figure cost savings, validating ROI expectations.[1]Plant & Works Engineering, “Condition Monitoring Case Studies,” pwemag.co.uk Integrating vibration and electrical-signature insights uncovers root-cause faults sooner, reallocating maintenance labor toward continuous-improvement tasks. The resulting gains elevate plant availability and make predictive approaches standard practice across mid-sized factories.

Industry 4.0 Adoption Across Manufacturing and Process Industries

Europe’s transition toward data-centric production unifies plant-floor sensors with enterprise resource planning and manufacturing-execution applications. Strong 5G coverage in Germany, Italy, and Spain allows secure, high-speed data flow between machines and digital twins, unlocking continuous improvement loops. Siemens’ Digital Drivetrain (released in 2024) exemplifies how an automation incumbent embeds embedded analytics directly into motor drive packages.[2]Siemens AG, “Digital Drivetrain Launch,” siemens.com Process operators integrate temperature, pressure, and vibration streams into a single pane of glass, exposing correlations between asset health and product yield that once remained invisible. Standardization efforts under Manufacturing-X lower integration barriers, accelerating multi-plant rollouts, and fueling the European machine condition monitoring market.

Edge-AI Smart Sensors Enabling Real-Time Analytics

Embedding machine-learning cores within sensors eliminates latency and bandwidth obstacles. Fraunhofer IPMS’s multimodal platform trims data traffic 90% while issuing millisecond-level alarms for mission-critical gear. Analog Devices’ Voyager4 integrates MEMS accelerometers and on-board AI to spot bearing defects without a server or gateway. Such devices recalibrate sampling rates based on load, extending battery life in remote pumps and conveyors. TinyML algorithms foster pattern recognition once affordable only to Fortune 500 plants, democratizing advanced diagnostics to small and medium enterprises and widening the adoption corridor for the European machine condition monitoring market.

Rising Regulatory Pressure on Asset Uptime in Critical Infrastructure

The NIS2 Directive now captures manufacturing and essential infrastructure, penalizing inadequate resilience programs with fines up to EUR 10 million or 2% of global turnover.[3]Kaan Ozdogan, “Who Does NIS2 Apply To?,” Lexology, lexology.com ENISA’s 2024 NIS360 report highlights six sectors in a “risk zone,” pushing operators to justify proactive fault-detection schemes. Because operators must file incident reports within 24 hours, continuous monitoring has become a compliance requirement rather than an optional productivity tool. This shift directs fresh capital toward secure, always-on systems and lifts long-term spending projections in the European machine condition monitoring market.

Restraints Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost implications of retrofits and integration | -1.4% | Italy, Spain, Eastern Europe | Short term (≤ 2 years) |

| Macroeconomic and geopolitical uncertainties | -0.8% | Germany, United Kingdom, France | Medium term (2-4 years) |

| Cybersecurity and data-ownership concerns | -1.1% | Germany, Netherlands, France | Medium term (2-4 years) |

| Shortage of vibration analysts | -0.9% | Germany, United Kingdom, Spain | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cost Implications of Retrofits and Integration

Legacy pumps, turbines, and extruders often lack mounting points or digital interfaces for today’s multi-axis accelerometers. Integrating wireless networks with 1990-era programmable-logic controllers can inflate project expense by 30-40% over sensor costs alone. Hazard-area certifications in petrochemical plants further double the spending on explosion-proof hardware, particularly across mature facilities in Italy, Spain, and Eastern Europe. Diverse national electrical codes, CE-marking nuances, and ATEX rules extend project timelines and dilute ROI calculations, slowing adoption in price-sensitive segments within the European machine condition monitoring market.

Cybersecurity and Data-Ownership Concerns in Connected Assets

Adding thousands of radio-equipped nodes multiplies attack vectors. Manufacturers worry that a compromised sensor network could trigger NIS2 fines or force unplanned shutdowns. German automakers insist on zero-trust architectures with device-level encryption before allowing cloud connections. Data-sovereignty statutes demand that analytics servers reside in EU jurisdictions, complicating multi-country fleet management. Many mid-market plants lack in-house security talent, leaning on third-party managed security services that raise operating costs and elongate deployment cycles in the European machine condition monitoring industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Hardware Foundation Underpins Services Growth

Hardware retained a 61.10% revenue lead in 2025, supported by indispensable accelerometers, ultrasonic probes, and infrared cameras forming any monitoring program’s front line. Vibration instruments dominate because rotating machinery remains pervasive, while thermography devices gain traction for high-voltage switchgear audits. The European machine condition monitoring market size for hardware reached USD 641.55 million in 2025. Services, however, exhibit an 8.65% CAGR as subscription models surge. Vendors now bundle sensor leasing, data hosting, and monthly health reports, accepted by CFOs eager for cost certainty. Software, although a smaller slice, supplies the analytics engine that converts signal streams to actionable work orders. Machine-learning modules automate fault classification, closing a skill gap for scarce vibration experts.

Because hardware acts as the beachhead for follow-on service revenues, vendors pursue razor-and-blade strategies, offering low-cost wireless kits that later anchor multi-site service contracts. Hybrid solutions integrating lubrication analysis and electrical-signature monitoring enrich context for root-cause troubleshooting, strengthening cross-sell opportunities. Thermography and ultrasonic skids safeguard electrical assets and compressed-air systems, respectively, broadening wallet share within mature blue-chip accounts.

By Monitoring Technique: Online Systems Anchor, Edge-AI Sensors Excel

Online installations accounted for 56.20% of 2025 revenue as critical-asset owners refuse to rely on periodic checks. High-speed turbines, compressors, and rail switches now stream data nonstop, enabling degradations to be caught hours, not weeks, before failure. The European machine condition monitoring market share for online solutions rests on maturing wireless mesh protocols and long-life batteries that cut cabling labor. Portable devices still appear across non-critical conveyors, chosen for their flexibility and low upfront cost.

Edge-AI sensors capture headlines with a 8.72% CAGR forecast. By shifting pattern matching into the device, these nodes forward only condensed fault indicators, slashing bandwidth fees and enabling private-LTE deployments deep inside refineries. Deutsche Bahn’s KONUX rollout demonstrates how continuous rail-switch monitoring triggers preemptive field crews, shrinking network disruption minutes. Hybrid approaches emerge: technicians collect quick-route readings via Bluetooth handhelds, then upload to fleet dashboards for trend correlation, maximizing coverage while controlling spend.

By Deployment Mode: On-Premises Security Prevails, Cloud Gains Ground

On-premises platforms secured 68.00% of 2025 spend, reflecting European manufacturers’ insistence on local data custody amid evolving cybersecurity laws. Plants host servers in secure racks, ensuring sub-millisecond access to alarms and simplifying NIS2 audit trails. Yet cloud growth at 8.55% CAGR proves momentum toward scalable analytics. Hyperscalers now operate EU-only data centers with ISO 27001 controls, easing sovereignty fears and unlocking enterprise-wide benchmarking on gigabytes of vibration spectra.

Hybrid architectures combine the two: preprocessing occurs at the edge for real-time alarms, then trend features are upload to regional clouds for deeper machine-learning training. This topology offers a safety-by-design path for risk-averse sectors, especially pharmaceuticals and defense, where latency, privacy, and compliance intersect. As insurance carriers begin rewarding plants for documented predictive programs, CFOs accept subscription OPEX fees in lieu of unpredictable breakdown costs, nudging additional workloads to the cloud.

By End-User Vertical: Oil and Gas Leads, Discrete Manufacturing Accelerates

Oil and gas retained 29.90% of 2025 revenue; offshore platforms, pipelines, and downstream refineries rely on continuous diagnostics to mitigate environmental and safety risks. Aging compressors and pumps mandated under the EU Methane Regulation must prove mechanical integrity, fueling sensor retrofits. Yet discrete manufacturing shows a 9.05% CAGR through 2031. Automotive, electronics, and packaging lines embed smart diagnostics at each servo and gearbox, linking health metrics with just-in-time schedules.

Process manufacturing chemicals, food, and beverages remains a strong adopter where nonstop throughput demands high reliability. Aerospace, marine, and defense sectors require ruggedized, EMI-resistant gear and encrypted comms, positioning niche suppliers for premium margins. Power-generation utilities integrate condition data with energy-trading platforms, predicting plant availability for day-ahead markets.

Geography Analysis

Germany generated 28.10% of the Europe machine condition monitoring market in 2025, anchored by automotive, chemical, and machinery clusters. Government-funded Manufacturing-X bridges OT-IT data across 115 firms, creating fertile ground for sensor rollouts. Labor deficits estimated at 200,000 technicians by 2027 press companies to automate health checks. Despite robust 5G, patchy fiber access can slow cloud adoption in rural facilities, sustaining on-prem demand. The presence of Siemens, Schaeffler, and Bosch fosters a deep ecosystem of pilots and early-adopter case studies.

Spain represents the region’s fastest-growing locale: 8.95% CAGR. High AI-adoption rates (70% of firms seeing productivity gains) dovetail with Industry 4.0 subsidies. Renewable-energy expansion, particularly in wind-farm fleets scattered across harsh terrains, calls for wireless, solar-powered monitoring nodes. Lear’s acquisition of local integrator WIP Industrial Automation in 2024 highlights global confidence. Madrid’s push for digital upskilling further accelerates adoption, positioning Spain as a technology export hub to Latin America.

The United Kingdom, France, and Italy compose mature but opportunity-rich markets where asset replacement drives steady sensor refresh cycles. Post-Brexit customs complexity nudges U.K. plants to optimize uptime through predictive insights. The Netherlands leverages its petrochemical ports and logistics hubs, requiring ATEX-classified sensors and advanced lubrication analytics. Eastern Europe, grouped as Rest of Europe, shows promising greenfield projects in automotive and battery-manufacturing corridors, although budget limitations often steer buyers toward portable kits first.

Competitive Landscape

The European machine condition monitoring market balances between diversified automation conglomerates and agile sensor specialists. Siemens, Emerson, and Honeywell exploit installed-base leverage, bundling software, gateways, and professional services. Emerson’s USD 7.2 billion AspenTech buyout in 2025 signals an appetite to own high-margin analytics.[4]Emerson, “Emerson to Acquire AspenTech,” emerson.com SKF, Schaeffler, and NSK tighten grip on bearing-centric diagnostics, integrating smart lubricators and electro-mechanical drive data. Honeywell and Danfoss unite cybersecurity-hardened controllers with cloud dashboards, meeting stricter NIS2 clauses.

Edge analytics startups fill the white space. Samotics captured EUR 20 million EIB funding to refine electrical-signature analysis for submerged pumps. KONUX leverages AI to monitor rail turnout geometry, partnering with Deutsche Bahn on multi-year rollouts. Fraunhofer spin-offs commercialize ultralow-power neural networks, courting SMEs that lack data scientists. Meanwhile, distributors such as EU Automation publish implementation guides, easing adoption hurdles for mid-tier plants.

Pricing power favors vendors delivering closed-loop solutions and measurable ROI. As predictive programs cut warranty claims, OEM alliances emerge: ABB’s Födisch Group acquisition strengthens environmental compliance diagnostics. M&A momentum is poised to continue, as firms seek portfolio breadth spanning sensors, connectivity, AI, and services to satisfy end-users, consolidating supplier lists under cybersecurity procurement policies.

Europe Machine Condition Monitoring Industry Leaders

SKF AB

Schaeffler Technologies AG and Co. KG

Emerson Electric Co.

Honeywell International Inc.

General Electric Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: GEA has unveiled GEA InsightPartner EvoHDry, a cutting-edge digital service tool aimed at enhancing production reliability and operational efficiency in dairy and beverage facilities.

- January 2025: Samotics secured EUR 20 million (USD 22.6 million) EIB financing to commercialize AI-driven electrical-signature monitoring for motors.

- January 2025: Emerson fully acquired AspenTech for USD 7.2 billion, reinforcing its software-defined control roadmap.

- October 2024: Schaeffler completed its merger with Vitesco Technologies, expanding electric-mobility and intelligent-bearing offerings.

Europe Machine Condition Monitoring Market Report Scope

Machine condition monitoring is the process of monitoring the condition of a machine with the intent of predicting mechanical wear and failure.

The market is segmented by type (hardware (vibration condition monitoring equipment, thermography equipment, lubricating oil analysis), software, services), end-user vertical (oil and gas, power generation, process and manufacturing, aerospace and defense, automotive and transportation, other end-user verticals), and country (United Kingdom, Germany, France, Italy, Rest of Europe). The market sizes and forecasts are provided in terms of value in USD million for all the above segments.

By Type

| Hardware | Vibration Condition Monitoring Equipment |

| Thermography Equipment | |

| Ultrasonic Detection Systems | |

| Lubricating Oil Analysis | |

| Current Signature Analysis | |

| Acoustic Emission Monitoring | |

| Software | |

| Services |

By Monitoring Technique

| Online Condition Monitoring |

| Portable Condition Monitoring |

| Edge AI-enabled Sensors |

By Deployment Mode

| On-Premises |

| Cloud-Based Solutions |

By End-user Vertical

| Oil and Gas |

| Power Generation |

| Process Manufacturing |

| Discrete Manufacturing |

| Aerospace and Defense |

| Automotive and Transportation |

| Marine, Mining, and Metals |

| Other End-user Verticals |

By Country

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Netherlands |

| Rest of Europe |

| By Type | Hardware | Vibration Condition Monitoring Equipment |

| Thermography Equipment | ||

| Ultrasonic Detection Systems | ||

| Lubricating Oil Analysis | ||

| Current Signature Analysis | ||

| Acoustic Emission Monitoring | ||

| Software | ||

| Services | ||

| By Monitoring Technique | Online Condition Monitoring | |

| Portable Condition Monitoring | ||

| Edge AI-enabled Sensors | ||

| By Deployment Mode | On-Premises | |

| Cloud-Based Solutions | ||

| By End-user Vertical | Oil and Gas | |

| Power Generation | ||

| Process Manufacturing | ||

| Discrete Manufacturing | ||

| Aerospace and Defense | ||

| Automotive and Transportation | ||

| Marine, Mining, and Metals | ||

| Other End-user Verticals | ||

| By Country | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe machine condition monitoring market in 2026?

It is valued at USD 1.13 billion and is forecast to reach USD 1.63 billion by 2031 at a 7.60% CAGR.

Which country contributes the most revenue?

Germany leads with 28.10% of 2025 revenue, owing to its robust manufacturing base and early Industry 4.0 adoption.

Which monitoring technique is growing the fastest?

Edge-AI-enabled sensors are projected to expand at a 8.72% CAGR between 2026 and 2031.

Why are services outpacing hardware growth?

Subscription-based contracts that bundle analytics and maintenance convert CAPEX to OPEX and deliver predictable cost savings, driving an 8.65% CAGR for services.

What regulation is influencing investment decisions?

The NIS2 Directive imposes stringent cybersecurity and resilience requirements, making real-time monitoring essential for compliance.

Which vertical offers the highest growth opportunity beyond oil and gas?

Discrete manufacturing—particularly automotive and electronics—will grow at 9.05% CAGR as plants tie machine health to production-quality metrics.

Page last updated on: