Europe Legal Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 257.87 Billion |

| Market Size (2026) | USD 267.5 Billion |

| Market Size (2031) | USD 321.29 Billion |

| Growth Rate (2026 - 2031) | 3.73% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Legal Services Market Analysis by Mordor Intelligence

The Europe Legal Services Market size is projected to be USD 257.87 billion in 2025, USD 267.5 billion in 2026, and reach USD 321.29 billion by 2031, growing at a CAGR of 3.73% from 2026 to 2031.

Organizations in highly regulated sectors are expanding compliance budgets as the EU rolls out new frameworks for AI, digital markets, data sharing, and financial resilience, which pushes steady demand for cross-practice advisory and investigations. Cross-border mandates continue to favor hubs with established infrastructure and international courts, which sustains premium demand for complex representation and arbitration across the Europe legal services market. The acceleration in digital court infrastructure, electronic identity, and e-signatures supports the rise of virtual advisory and remote proceedings while raising the bar for secure workflows. The Unified Patent Court has consolidated a significant portion of high-value patent litigation, which elevates the value of pan-European strategy, forum selection, and injunction practice for leading firms across the Europe legal services market. The cumulative effect of these shifts is a market where proactive risk management and specialized regulatory counsel replace reliance on organic litigation volume as the core growth driver across the Europe legal services market.

Key Report Takeaways

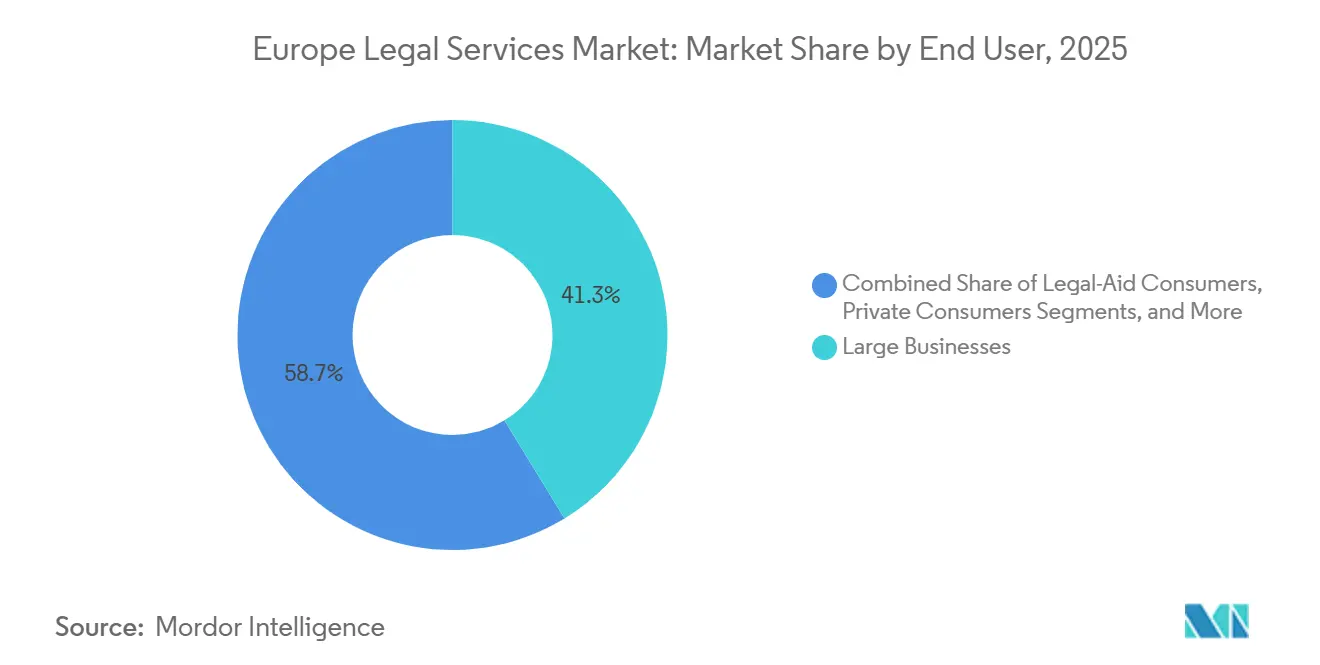

- By end user, large businesses held 41.28% of Europe legal services market share in 2025, and are poised for a 7.83% CAGR through 2031.

- By application, corporate, financial, and commercial law contributed 35.14% of Europe legal services market size in 2025, and employment law is poised for a 8.92% CAGR through 2031.

- By service, representation services held 44.36% of Europe legal services market share in 2025, while legal research and support services are projected to expand at a 10.74% CAGR.

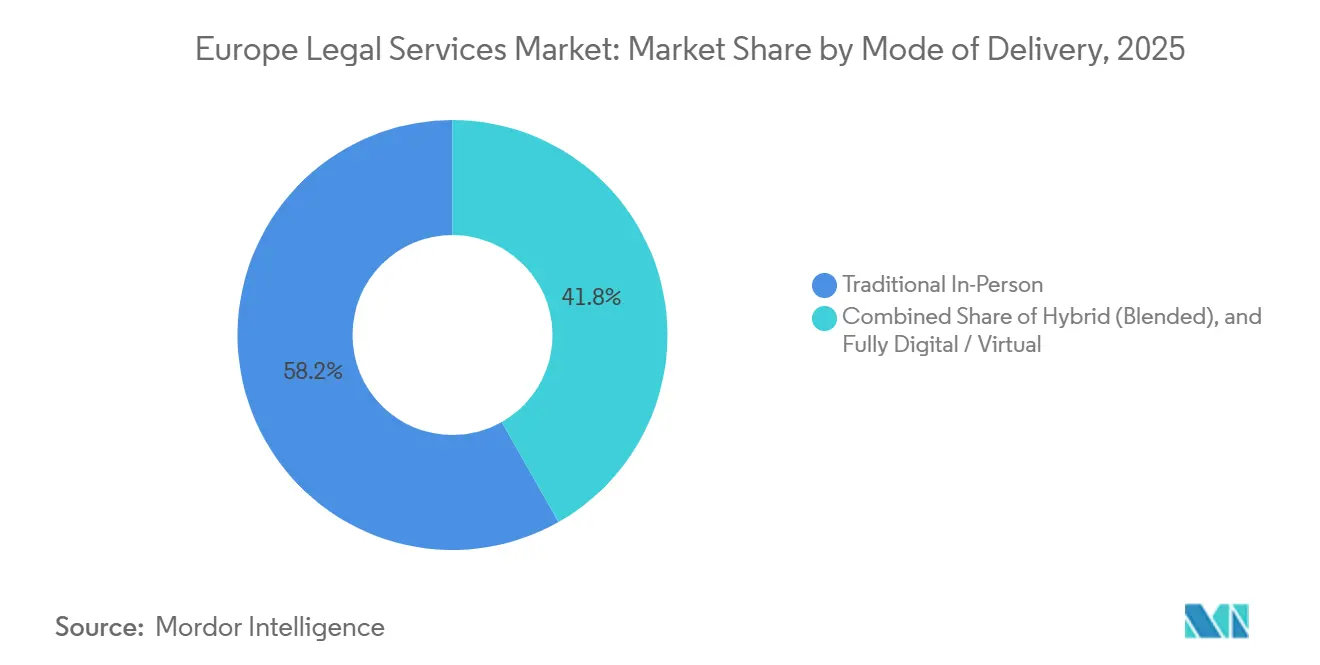

- By mode of delivery, traditional in-person work represented 58.21% of Europe legal services market share in 2025; fully digital or virtual services are expected to rise at a 11.48% CAGR.

- By firm size, large law firms accounted for 55.17% of Europe legal services market size in 2025; large law firms are expected to deliver 8.16% CAGR through 2031.

- By country, the United Kingdom retained a 34.62% stake in the Europe legal services market during 2025, and is projected to deliver the highest 6.04% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Legal Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| New EU digital and sustainability regimes expand compliance and investigations work | +2.8% | Global, strongest in Germany, France, the Netherlands, Nordics | Medium term (2-4 years) |

| FDI screening hardens across the EU, increasing M&A and PE counsel complexity | +1.2% | EU-wide, concentrated in Germany, France, Netherlands | Short term (≤ 2 years) |

| Collective redress rollout elevates mass-claims exposure and multi-country defense demand | +0.9% | Germany, the Netherlands, France, Belgium, expanding to CEE | Medium term (2-4 years) |

| The Unified Patent Court concentrates high-stakes pan-European patent litigation | +0.6% | Germany, The Hague, Paris, Milan | Short term (≤ 2 years) |

| eIDAS 2.0 and EU Digital Identity Wallet modernize identity, notarization, and e-signatures | +0.4% | EU-wide | Medium term (2-4 years) |

| EU Data Act drives cloud switching, IoT data access, and interoperability contracting | +0.5% | EU-wide with early impact in Germany, France, the Netherlands | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

New EU Digital and Sustainability Regimes Expand Compliance and Investigations Work.

The phased enforcement of the EU AI Act, which bans prohibited practices from February 2025 and applies high-risk system obligations from August 2026, has created immediate compliance roadmapping among financial institutions and technology providers. The regime sets penalties that can reach USD 38.9 million or 7% of global turnover for non-compliance, which elevates the need for specialized counsel to align technical controls with regulatory expectations[1]European Commission, “Artificial Intelligence Act,” European Commission, eur-lex.europa.eu. Adjustments to the Corporate Sustainability Reporting Directive and the Corporate Sustainability Due Diligence Directive shift the scope toward larger enterprises while requiring value-chain due diligence and climate transition planning that demand coordinated legal and ESG programs. Scope revisions to CSRD, including thresholds like USD 499.5 million in net turnover and over 1,000 employees, reduce the number of in-scope entities but increase program depth for large multinationals[2]Wilson Sonsini, “EU Rolls Back CSRD and CSDDD Obligations,” Wilson Sonsini, wsgr.com. Digital markets enforcement has intensified under the DSA and DMA, reflected in a USD 133.2 million penalty against Platform X for transparency violations in December 2025, which underscores the need for sustained counsel on platform obligations. The combined effect of AI Act, DSA, DMA, MiCA, DORA, NIS2, and the Data Act has institutionalized continuous advisory and investigations demand as companies operationalize compliance across products and services.

FDI Screening Hardens Across the EU, Increasing M&A and PE Counsel Complexity

The revised EU framework and national FDI rules embed multi-jurisdictional filing analysis into cross-border deals, which aligns sensitive-sector reviews with national security priorities and increases the demand for strategic legal planning . Transaction teams now map thresholds and mandatory filing sectors across Member States while planning for remedies and disclosures that can alter timelines and deal certainty. Expansion into areas such as semiconductors, quantum, AI research, and critical raw materials raises notification volume and counsel workload for transactional structuring. Private equity and corporate acquirers build early-stage FDI feasibility assessments into standard diligence to prevent sequencing bottlenecks and address closing risk. Sponsors also coordinate parallel antitrust and national security workstreams to handle information requests and mitigation terms efficiently . This environment sustains repeat advisory as corporates and investors develop standardized playbooks for FDI reviews across the Europe legal services market.

Collective Redress Rollout Elevates Mass-Claims Exposure and Defense Demand.

The transposition of the EU Representative Actions Directive and the maturing of national collective action regimes in Germany, France, the Netherlands, Belgium, and others expand both plaintiff and defense activity across consumer, competition, data, and product liability matters . Public registers and designated courts improve transparency and predictability, which also encourages coordinated filings across jurisdictions by qualified entities and litigation funders. Defense strategies now incorporate early case assessment, jurisdictional comparisons, and data analytics to manage exposure and inform settlement structures in high-volume claims. Opt-out and hybrid models expand claimant cohorts, creating procedural leverage points that shape negotiations and encourage efficient claims administration . This procedural evolution favors teams that combine civil procedure expertise with funding and insurance capabilities to steer outcomes and costs. The Europe legal services market sees durable demand as mass-claims infrastructure becomes embedded in national systems.

Unified Patent Court Concentrates High-Stakes Pan-European Patent Litigation.

The Unified Patent Court has aggregated infringement and revocation actions across local and central divisions, with early caseload concentration in Munich, Düsseldorf, The Hague, Paris, and Milan. Provisional measures and preliminary injunction activity validate the forum’s relevance for life sciences, telecom, and technology disputes where speed and injunctive relief are decisive. Divisional patterns on timelines, evidence, and remedies influence venue selection and litigation strategy as parties calibrate forum risk and relief prospects. Firms with integrated prosecution and litigation teams offer coordinated strategies for filings, evidence, and technical experts across divisions. The capacity to operate across multiple UPC locations has become a differentiator in pan-European disputes, especially for preliminary measures and cross-border enforcement. These features reinforce specialist capabilities as a core need in the Europe legal services market for patent risk management.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Panel consolidation and AFAs compress realizations in commoditized work | -1.1% | UK, Germany, France, Benelux | Short term (≤ 2 years) |

| Scarcity of AI, regulatory, cyber, and ESG specialists constrains capacity | -0.8% | EU-wide, most acute in smaller Member States | Medium term (2-4 years) |

| Fragmented ALSP and ABS rules slow scalable ALSP–law firm integrations | -0.4% | Germany, France, Italy, Spain | Long term (≥ 4 years) |

| Uneven court digitalization and backlogs prolong timelines and realization risk | -0.6% | Southern Europe and CEE | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Panel Consolidation and AFAs Compress Realizations in Commoditized Work.

Corporate legal departments have reduced external panels and favored fewer preferred providers for routine matters, which concentrates spend and intensifies fee pressure for high-volume work. The mix of fixed fees, capped arrangements, and success-based pricing narrows margins for tasks such as contract review, regulatory filings, and employment documentation. Firms respond with process improvement, legal project management, and technology enablement to preserve profitability and meet client expectations on budget adherence and reporting. Sole-supplier and managed service models channel recurring work to firms that can guarantee service levels and continuous efficiency gains through standardized workflows and dashboards. Generalist mid-market practices without scale or technology depth face sharper margin pressure as procurement demands predictability and transparency in spend. Price pressure limits upside in commoditized tasks in the Europe legal services market even as premium work for complex or uncertain mandates remains resilient.

Scarcity of AI, Regulatory, Cyber, and ESG Specialists Constrains Capacity.

Agencies, law firms, and in-house teams report shortages of senior specialists with cross-functional expertise in AI governance, GDPR interplay, cybersecurity, and sustainability reporting, which slows hiring and capacity expansion. Compensation gaps with private technology providers complicate recruitment for public bodies and mid-sized firms despite rising compliance demand under AI Act, DORA, NIS2, CSRD, and CSDDD. Salary premiums for ESG counsel reflect limited supply of professionals fluent in reporting standards, due diligence methods, and climate risk modeling, which pushes total program costs higher for corporates. Automation of junior tasks reduces traditional apprenticeship opportunities, which can slow skill development in deep legal reasoning and verification over time. Surveys show many firms view talent attraction and retention as a major challenge in the next planning cycle, which reinforces investment in training and technology to improve work experience. Capacity constraints act as a practical ceiling on growth in the Europe legal services market where demand for specialist teams outpaces supply.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End User: Enterprise Demand Drives Premium Services

Large Businesses held the largest share at 41.28% in 2025 and are also the fastest-growing segment at a 7.83% CAGR to 2031, supported by expanding mandates across AI governance, sustainability reporting, and investment screening that intensify cross-border advisory demand in the Europe legal services market. Regulatory thresholds such as CSRD’s USD 499.5 million net turnover and AI Act high-risk system requirements drive multi-year programs that require coordinated legal and ESG oversight. Implementation differences across 27 Member States push multinationals to deploy standardized controls for data protection, competition matters, sustainability, and transactions that align with local procedures. Legal operations teams scale regulatory intelligence and adopt contract lifecycle management, eDiscovery, and reporting tools to standardize workflows and track obligations across the enterprise. The United Kingdom attracts multinational mandates due to its institutional depth, while Germany and France expand with life sciences, industrial, and financial services programs tied to AI and automation within the Europe legal services market. These dynamics concentrate premium engagements on large enterprises as proactive compliance replaces reactive dispute spend across the Europe legal services market.

Public Sector and Government entities maintain meaningful spend in procurement, administrative litigation, and PPP structuring, though growth is moderated by budget constraints in parts of Southern and Eastern Europe. SMEs expand more slowly as digital tools handle routine needs in-house and external counsel is reserved for specialized risks and transactions, which shifts demand preferences. Consumer demand increasingly flows through digital platforms and fixed-fee services for family, property, and employment matters, while ALSPs support document and process-heavy workloads. Civil society organizations and NGOs expand strategic litigation under collective redress frameworks, which leverage funding models and cross-border procedural coordination. Legal-aid segments remain under pressure due to fiscal limits and court backlogs, despite digital access initiatives in several jurisdictions. These end-user differences allocate premium engagements to large enterprises while technology reshapes demand elasticity among smaller client groups within the Europe legal services market.

By Application: Employment Law Accelerates as Workforce Digitalization Reshapes Practice.

Corporate, Financial and Commercial Law maintained the largest application share at 35.14% in 2025, driven by cross-border M&A, corporate governance, securities rules, and banking regulation, while new FDI regimes broaden mandatory reviews that affect deal structuring across the Europe legal services market. Employment Law is the fastest-growing practice with an 8.92% CAGR as employers adapt to AI-supported HR processes, remote and hybrid work, and evolving rules for platform labor and algorithmic management. AI systems used for recruiting, performance evaluation, and allocation fall under high-risk categories that require conformity assessment and human oversight, which drives advisory demand for global employers. Procedures in major jurisdictions accelerate collective employment disputes and influence settlement strategies for large cohorts under representative mechanisms[3]BEUC, “From Collective Harm to Redress,” BEUC, beuc.eu. Digital identity, cross-border e-signatures, and electronic records reduce friction for workforce processes, which increases reliance on secure identity verification and standardized documentation. The Europe legal services market continues to pivot toward advisory at the intersection of technology, labor regulation, and data governance.

Personal Injury shows steady demand yet is shaped by ADR and fixed-fee mechanisms in some jurisdictions, while emerging liability theories around autonomous systems and digital health raise new questions for coverage and causation. Property transactions remain sensitive to rate cycles and balance sheet constraints, which tempers volumes even as notarization and conveyancing progress under eIDAS 2.0. Wills, Trusts, and Probate services benefit from demographic trends and expanded digital assets planning, which requires updates to fiduciary instruments and custodial arrangements. Family Law incorporates online dispute resolution for uncontested matters to reduce court congestion and speed outcomes where litigation is unnecessary. Criminal Law capacity reflects resource constraints in public defense for some regions, while white-collar enforcement and cyber incidents sustain demand for counsel with forensic and cross-border evidence expertise under new cooperation instruments. Other Applications including immigration, IP disputes, and environmental litigation gain from collective redress models and the Unified Patent Court, which broadens procedural and jurisdictional options across the Europe legal services market.

By Service: Legal Research and Support Services Surge Amid Automation and ALSP Growth.

Representation captured the largest share at 44.36% in 2025 across courtroom advocacy, arbitration, and regulatory proceedings, supported by the consolidation of patent disputes at the Unified Patent Court and the continued role of high-value hearings in Germany, the Netherlands, France, and Italy within the Europe legal services market. Settlement incentives in collective systems and ADR usage shape case trajectories, yet premium representation remains central when injunctions, precedent, and multi-forum strategy determine enterprise outcomes. Advisory and Consulting, at 28.7% share with steady growth, is buoyed by continuous regulatory interpretation across AI Act obligations, GDPR interface questions, and sector-specific digital resilience rules. Enterprises build continuous compliance models through audits and technical standard updates, which require sustained programmatic advisory. Legal Research and Support Services, while a smaller base, is posting the fastest growth at a 10.74% CAGR as firms adopt AI-enabled document analysis, drafting accelerators, and scalable delivery through ALSPs. These shifts move research and pre-production workflows to managed services while leading firms retain front-end strategy and advocacy in the Europe legal services market.

Notarial Services and formal attestation functions modernize through eIDAS 2.0 and the EU Digital Identity Wallet, which supports remote identity verification and cross-border e-signatures that reduce friction in corporate and property workflows. Collective redress growth elevates specialist claims administration and distribution capabilities often delivered by third-party administrators instead of in-house firm staff. Legal process outsourcing to cost-effective European locations calibrates staffing for document-heavy tasks while senior researchers focus on complex memoranda and briefings with client-facing teams. Technology investment blends build, buy, and partner models as firms balance security, usability, and time to value for workflow and knowledge systems. Clients reward providers that deliver predictability through dashboards, budget adherence, and well-governed knowledge bases. These dynamics shift share toward automated support tasks while reinforcing demand for nuanced advice and advocacy in the Europe legal services market.

By Mode of Delivery: Fully Digital Models Disrupt Traditional In-Person Service Provision.

Traditional In-Person delivery held 58.21% share in 2025, supported by complex deals, advocacy needs, and board-level engagements where in-person presence and courtroom practice are decisive across the Europe legal services market. Virtual delivery accelerates as courts and agencies adopt video hearings, e-filing, and digital service of process, which increases the scope of remote engagements in civil and commercial matters . Fully Digital or Virtual delivery is expanding at 11.48% CAGR, enabled by DigitalJustice programs and simplified identity and notarization mechanisms that standardize cross-border legal formalities. Hybrid models combine remote document review and research with selective in-person events like depositions and hearings to optimize resources and client convenience. Work patterns stabilize around flexible arrangements for lawyers and staff while firms invest in case management and cloud security to safeguard confidentiality and integrity. These mode-of-delivery shifts influence pricing, staffing, and litigation strategy in ways that benefit providers that can orchestrate both on-site and virtual operations consistently in the Europe legal services market.

Experience shows that adoption can lag where users face training gaps or complex interfaces, which underscores the importance of design and change management for litigants, counsel, and court staff. Jurisdictions that integrate filing tools with practice management systems and enforce standardized submissions achieve faster resolution cycles and better data for performance tracking. Investments in video infrastructure create cost savings and increased participation for rural and mobility-impaired users, for example an USD 8.9 million program yielding USD 2.4 million in annual savings in one EU initiative[4]European Commission, “Communication on DigitalJustice@2030,” European Commission, commission.europa.eu. Firms that configure browser-based workflows and encrypted collaboration improve client onboarding and associate engagement, which aids retention in a constrained talent market. Digital process scale requires balanced throughput and fairness objectives with procedural safeguards that evolve alongside new tools. These operational realities shape the adoption curve and drive continuous improvement across the Europe legal services market.

By Firm Size: Large Law Firms Consolidate Market Share Through Technology and Specialization.

Large Law Firms commanded a 55.17% share in 2025 and are growing at an 8.16% CAGR through 2031, driven by the capacity to invest in platforms for document automation, analytics, and matter management, plus the depth to staff cross-border mandates across the Europe legal services market. Magic Circle and leading global practices continue to win premium work where multi-disciplinary teams and global connectivity are differentiators in complex mandates. Mid-sized specialists in areas such as Unified Patent Court litigation, AI compliance, and collective redress stay competitive in niches that reward deep technical knowledge. SME firms with a generalist focus face fee pressure as panels consolidate and ALSPs capture document-heavy workflows, which leads to selective partnering and managed services. Small firm AI adoption is rising, which narrows the efficiency gap and supports fixed-fee offerings in defined work types. These dynamics favor providers that combine specialization with process maturity across the Europe legal services market.

Technology is embedded in pricing and delivery as clients ask for budget certainty and real-time visibility into matter progress and risk, which pushes firms to operationalize metrics and dashboards. Leading firms allocate a defined share of revenue to innovation and training for AI-assisted review, contract intelligence, and knowledge systems that accelerate production and reduce variance. Efficiency metrics show lower lawyer-hours for standardized due diligence and quicker turnaround on document-intensive tasks when teams combine automation with playbooks. Talent strategies emphasize structured development, international secondments, and exposure to complex matters to attract and retain graduates in competitive markets. Lateral hiring and flexible staffing supplement capacity for peak loads and fill skills gaps in areas like data privacy engineering and cyber incident response. As regulatory complexity expands, certification and advanced training in AI governance, cybersecurity, and ESG reporting become part of competitive positioning across the Europe legal services market.

Geography Analysis

The United Kingdom held 34.62% share in 2025 and is projected to grow at a 6.04% CAGR to 2031 as London retains its role in international disputes and transactions while collective action activity scales in the Competition Appeal Tribunal. UK legal services exports contributed foreign earnings estimated at USD 9.0 billion, reinforcing London’s cross-border reach for complex matters in the Europe Legal Services market. Divergent approaches on digital markets and AI governance from the EU create parallel compliance regimes for multinationals and a distinct advisory stream centered in London. Opt-out competition claims in the CAT raise exposure for platforms and intermediaries while setting procedural benchmarks that influence EU claim design. This combination of exports and complex domestic litigation keeps United Kingdom providers central to high-value counsel for multinationals operating under dual regimes.

Germany accounts for a significant revenue share and posts steady growth as the Unified Patent Court’s busiest local divisions sit in German cities, attracting technology and life sciences disputes that require fast preliminary measures. Representative actions under the Consumer Rights Enforcement Act introduce new claimant pathways for consumers and small businesses, which stimulates defense work and procedural strategy. The Federal Court of Justice has used leading case mechanisms that increase predictability for mass disputes, including a USD 111 lump sum standard for certain data scraping harms, which informs defense stances and settlement options. Investments in judicial digitization demonstrate improvements in processing mass claims and appeals, which affects litigation timelines and resource planning for counsel. Germany’s role in industrial automation and finance also concentrates advisory around AI Act controls, operational resilience, and data governance in the Europe legal services market.

France shows steady expansion following completion of its Representative Actions Directive transposition, which introduces a unified class action framework, late opt-in provisions, and a public registry for transparency. Sustainability advisory remains active for large enterprises as CSRD and CSDDD scope changes still require deep program design and governance structures for in-scope companies. Spain is moving toward formalizing collective mechanisms as draft legislation progresses, which positions the market for an uptick in mass claims once enacted. Italy gains traction as a life sciences patent hub through the Milan Central Division of the UPC, which boosts high-stakes litigation work that often requires preliminary measures and cross-border enforcement. The Benelux region leverages advanced digital infrastructure and mature collective action regimes to maintain high caseloads, while The Hague remains a leading UPC venue. The Nordics emphasize digital adoption and legal tech innovation in both private and public sectors, which creates opportunities for scalable virtual delivery models in the Europe legal services market. Rest of Europe faces uneven court capacity and adoption of digital processes, which suggests gradual improvements as DigitalJustice programs scale across Member States.

Competitive Landscape

The Europe legal services market exhibits moderate concentration at the top and fragmentation in regional tiers, as international firms compete with specialized boutiques on high-stakes mandates where cross-border capabilities and sector expertise matter most. Magic Circle and leading global platforms differentiate through multi-practice depth and institutional relationships that anchor premium engagements across corporate, regulatory, and disputes work. Strategy emphasizes multidisciplinary advisory for AI Act compliance and digital governance, legal operations, and integrated programs for data, cyber, and third-party risk. Firms deploy technology as a core component of positioning, including AI-enabled drafting, analytics, and knowledge systems that deliver predictable timelines and budget adherence. White-space opportunities include Unified Patent Court litigation, collective redress defense and settlement architecture, and ESG due diligence programs. The Europe legal services market rewards providers that align sector knowledge, procedural mastery, and technology adoption.

Geographic expansion and integration models vary, with some platforms extending coverage through verein structures while elite practices add targeted capability in select hubs to capture margin-dense work. ALSPs embed lawyers and process experts within corporate legal departments to flex capacity and optimize workflows, which redirects volume tasks from traditional leverage models. Law firms that integrate ALSP partnerships and managed service constructs offer scalable solutions without diluting focus on premium advisory and advocacy. Client procurement teams increasingly assess providers on demonstrable efficiency, data transparency, and outcomes in defined work types. These shifts drive investment in client portals, self-service templates, and metrics that track cycle time, budget adherence, and quality. As regulatory programs expand, firms invest in accreditation and specialized training to deepen credibility in AI governance, cybersecurity, and sustainability reporting.

Cross-disciplinary teams that combine lawyers, data scientists, and policy analysts are growing to meet complex advisory needs where legal interpretation depends on technical architectures and operational controls. Knowledge engineering and standardized playbooks improve repeatability and reduce variance without sacrificing nuance in complex programs. Providers that orchestrate multidisciplinary teams and platform-based delivery lead in system-level solutions for AI auditability, data controls, and sustainability performance. Firms that lag in technology adoption or cannot demonstrate value beyond hourly billing risk exclusion from panels and strategic projects. The Europe legal services market increasingly prizes transparent delivery, technology proficiency, and sustained capability building alongside legal judgment. This competitive dynamic aligns investment decisions with client outcomes and measurable performance across matters and portfolios.

Europe Legal Services Industry Leaders

Freshfields Bruckhaus Deringer LLP

Clifford Chance LLP

Allen Overy Shearman Sterling LLP

Linklaters LLP

DLA Piper

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Revised EU FDI Screening Regulation published with expanded sensitive sectors, which increases notification volume and cross-border counsel complexity.

- January 2026: The Unified Patent Court surpassed 880 cases filed since its inception, affirming its central role in European patent disputes.

- December 2025: The European Commission imposed a USD 133.2 million fine on Platform X under the Digital Services Act for transparency violations, signaling active enforcement.

- November 2025: Luxembourg completed transposition of the EU Representative Actions Directive, adding collective redress procedures with a consumer protection focus.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Europe legal services market as fee-based advisory, representation, transaction support, and dispute resolution delivered by licensed law firms and independent practitioners across corporate, civil, criminal, tax, and regulatory domains; revenues are captured at the point they are billed to external clients in constant 2024 dollars. Mordor Intelligence also counts alternative legal service units controlled by law firms but omits pure-play legal-tech vendors and court administration fees.

Scope exclusion: In-house counsel payroll, official notarization by state officers, and subscriptions to research platforms lie outside this scope.

Segmentation Overview

- By End User

- Legal-Aid Consumers

- Private Consumers

- SMEs

- Charities and NGOs

- Large Businesses

- Government and Public Sector

- By Application

- Corporate, Financial and Commercial Law

- Personal Injury

- Commercial and Residential Property

- Wills, Trusts and Probate

- Family Law

- Employment Law

- Criminal Law

- Other Applications

- By Service

- Representation

- Advisory and Consulting

- Notarial Services

- Legal Research and Support Services

- By Mode of Delivery

- Traditional In-Person

- Hybrid (Blended)

- Fully Digital / Virtual

- By Firm Size

- Large Law Firms

- SME Law Firms

- By Country

- United Kingdom

- Germany

- France

- Spain

- Italy

- Benelux (Belgium, Netherlands, and Luxembourg)

- Nordics (Sweden, Norway, Denmark, Finland, and Iceland)

- Rest of Europe

Detailed Research Methodology and Data Validation

Primary Research

Interviews with partners, practice managers, and finance heads across the United Kingdom, Germany, France, Spain, and the Nordics clarified utilization rates, average matter value, and technology uptake. Follow-up client polls tested billing elasticity assumptions and validated the growth outlook we derived from desk work.

Desk Research

We first mapped the addressable pool using open datasets such as Eurostat's professional services turnover series, OECD attorney employment matrices, the European Commission Justice Scoreboard, national bar association yearbooks, and the UK Ministry of Justice billing survey, which together outline historic demand drivers. Company filings, IPO prospectuses, and press coverage captured through Dow Jones Factiva, along with firm-level financials from D&B Hoovers, then refined billing rate ranges and service mix shifts. These examples are illustrative; many more records were screened to corroborate figures and language nuances.

Market-Sizing & Forecasting

A top-down reconstruction starts with professional services turnover and lawyer headcount, which are then multiplied by verified billable hours and blended hourly rates. Supplier roll-ups of leading firms, channel checks with mid-tier networks, and sampled ASP x volume calculations act as a bottom-up reasonableness screen. Key variables like GDP growth, cross-border M&A volume, corporate insolvency filings, digital court backlog clearance, and average ESG mandate count per client feed a multivariate regression that projects revenue through 2030. Missing firm data are bridged with regional averages adjusted for inflation and currency shifts.

Data Validation & Update Cycle

Outputs undergo a four-eye analyst review; variance triggers re-contact with sources, and every model is refreshed annually, with interim revisions for material regulatory or macro shocks so clients receive the freshest view.

Why Mordor's Europe Legal Services Baseline Stands Firm

Published estimates often diverge because providers mix different service buckets, client types, and currency treatments before applying distinct forecast styles. According to Mordor Intelligence, anchoring the baseline in audited turnover and refreshed interviews narrows error margins noticeably.

Key gap drivers include whether notarial and ALSP revenue are counted, how quickly post-Brexit pricing shifts are captured, the depth of firm sampling, and the cadence at which exchange rates are locked.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 257.48 Bn (2025) | Mordor Intelligence | |

| USD 271.0 Bn (2024) | Global Consultancy A | Counts notaries and ALSPs; holds 2022 exchange rates |

| USD 190.07 Bn (2024) | Regional Analyst B | Focuses on SME-centric firms; omits cross-border corporate matters |

| USD 177.9 Bn (2023) | Industry Dataset C | Uses historic court fee proxies and limited sampling |

Differences show that scope definitions and refresh cadence can swing totals widely; by rooting figures in audited turnover, timely interviews, and transparent variable choices, Mordor offers a dependable, decision-ready baseline.

Key Questions Answered in the Report

What is the current size and growth outlook for the Europe Legal Services market through 2031?

The Europe Legal Services market size is USD 267.50 billion in 2026 and is projected to reach USD 321.29 billion by 2031 at a 3.73% CAGR.

Which client segment drives the highest demand in Europe?

Large Businesses lead with a 41.28% share and are also the fastest growing at a 7.83% CAGR due to expanding EU regulatory programs that require sustained compliance and investigations support.

Which practice areas are expanding fastest in Europe?

Employment Law posts the fastest growth with an 8.92% CAGR, while Corporate, Financial and Commercial Law remains the largest by share within the Europe Legal Services market.

How is service delivery changing across Europe?

Traditional In-Person work still leads by share, but Fully Digital or Virtual delivery is expanding at 11.48% CAGR due to court digitalization, e-filing, and secure digital identity.

What factors most influence cross-border litigation in Europe?

The Unified Patent Court centralizes high-stakes patent disputes across several divisions while collective redress regimes expand mass claims and settlement strategies.

How are law firms differentiating in the Europe Legal Services market?

Leading firms invest in AI-enabled research, matter analytics, and multidisciplinary teams to deliver predictable outcomes, while niche practices specialize in UPC and collective redress mandates.

Page last updated on: