Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

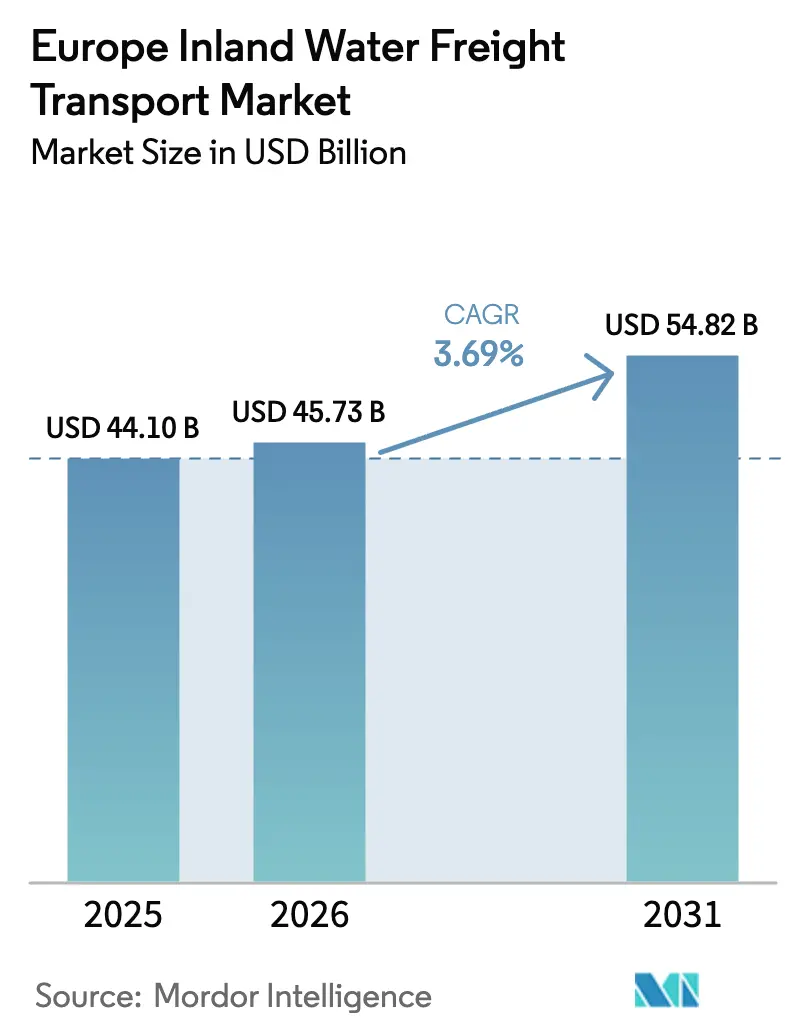

| Base Year Market Size (2025) | USD 44.10 Billion |

| Market Size (2026) | USD 45.73 Billion |

| Market Size (2031) | USD 54.82 Billion |

| Growth Rate (2026 - 2031) | 3.69% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Inland Water Freight Transport Market Analysis by Mordor Intelligence

The Europe Inland Water Freight Transport Market size was valued at USD 44.10 billion in 2025 and estimated to grow from USD 45.73 billion in 2026 to reach USD 54.82 billion by 2031, at a CAGR of 3.69% during the forecast period (2026-2031).

Demand is rising as shippers look for lower-carbon, cost-efficient corridors that fit the European Green Deal’s tight emissions timetable and the forthcoming expansion of carbon pricing. Policy clarity is encouraging operators to refresh aging barge fleets, alongside digital upgrades that tighten links with rail hubs and deep-sea ports. Large Western European networks already benefit from integrated river–sea gateways, while targeted Danube investments are unlocking new capacity in Central and Eastern Europe. Increasing container penetration, urban logistics pilots on city canals, and the widening fuel-cost gap with long-haul trucking together present clear opportunities for service differentiation and scale advantages.

Key Report Takeaways

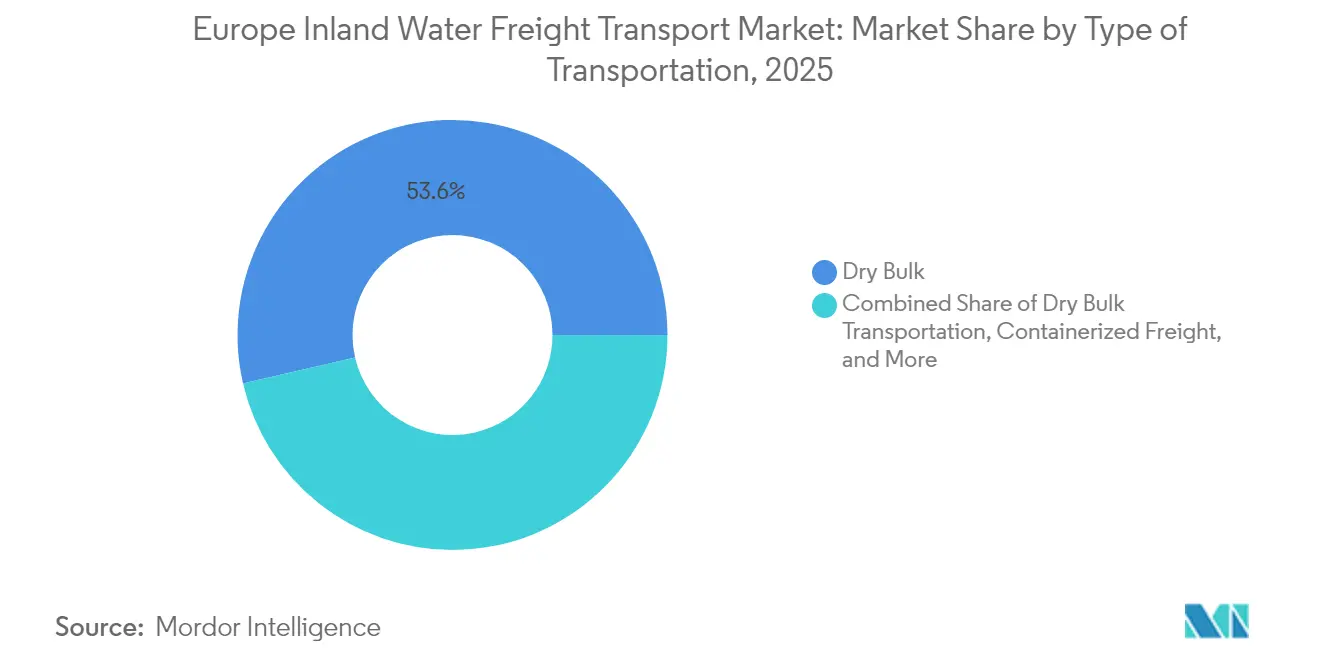

- By transportation type, dry bulk held the largest Europe inland water freight transport market share at 53.62 % in 2025, while containerized freight is projected to expand at a 6.98 % CAGR through 2031.

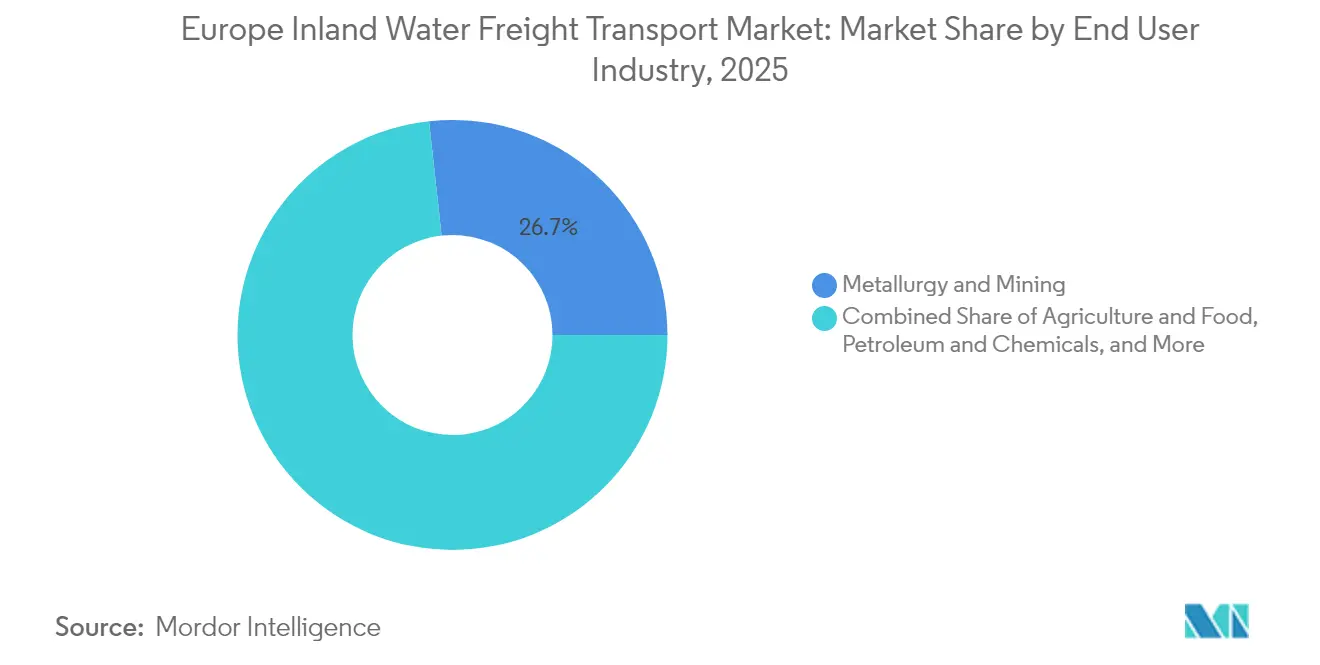

- By end-use industry, metallurgy and mining accounted for a 26.74 % share of the market size in 2025, whereas consumer goods and retail are advancing at an 7.93 % CAGR to 2031.

- By geography, the Netherlands dominated with a 32.70% market share in 2025, while Romania is set to grow the fastest at a 5.98 % CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Inland Water Freight Transport Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU Green Deal Driving Modal Shift to Waterways | +1.2% | EU-wide, Rhine–Scheldt delta strongest | Medium term (3-4 yrs) |

| Rhine-Danube Corridor Capacity Upgrades Accelerating Barge Demand | +0.9% | Central & Eastern Europe | Long term (≥ 5 yrs) |

| Tightening CO₂ / Pollutant Norms Favouring Low-Emission Barges | +0.6% | EU-wide, Western Europe strongest | Medium term (3-4 yrs) |

| Digitisation via RIS & DINA Improving Supply-Chain Visibility | +0.5% | EU-wide, Rhine corridor strongest | Short term (≤ 2 yrs) |

| Rise of Urban Logistics Pilots in Paris, Amsterdam & Antwerp | +0.3% | Major urban centres | Short term (≤ 2 yrs) |

| Fuel-Cost Differential vs. Road Transport Widening After ETS-II | +0.7% | EU-wide | Medium term (3-4 yrs) |

| Source: Mordor Intelligence | |||

EU Green Deal Driving Modal Shift to Waterways

The European Green Deal aims for a 90 % reduction in transport-related greenhouse-gas emissions by 2050, and its Sustainable and Smart Mobility Strategy calls for inland waterway freight volumes to climb 25 % by 2030 and 50 % by 2050. As ETS fees scale up for shipping emissions, the gap between the carbon cost of barges and trucks widens, strengthening the modal-shift argument in national freight strategies. Operators are already reporting stronger demand inquiries for container slots on the Rhine–Dutch delta, implying that the targets are influencing day-to-day routing decisions well before the 2030 milestone. An immediate inference is that modal-shift subsidies may taper sooner than expected because cost competitiveness alone progressively favours waterways.

Rhine–Danube Corridor Capacity Upgrades Accelerating Barge Demand

European Union investments to eliminate bottlenecks along the Rhine–Danube corridor include deeper draught sections, taller bridges, and modernised locks in Slovakia, Hungary, and Romania. Completion of these works raises baseline payloads during variable river conditions, thereby reducing the “empty kilometres” problem that once stifled profitability. Private operators such as Contargo have responded by enlarging their dedicated barge fleets and ordering hybrid-propulsion vessels to secure early mover advantages. From these patterns one can infer that barge charter rates along the Danube will trend upward as shippers compete for newly reliable capacity.

Tightening CO₂ / Pollutant Norms Favouring Low-Emission Barges

FuelEU Maritime rules effective January 2025 mandate a 2 % reduction in greenhouse-gas intensity for vessels, tightening to an 80 % cut by 2050 [1]European Commission, “Rhine-Danube Corridor,” transport.ec.europa.eu. The Central Commission for the Navigation of the Rhine (CCNR) complements this with a 35 % target by 2035 [2]Central Commission for the Navigation of the Rhine, “Study on the Energy Transition Towards a Zero-Emission Inland Navigation Sector,” ccr-zkr.org. Early adopters of Euro 6 truck-engine retrofits report reductions of up to 95 % in particulate matter, with payback periods shortened by lower fuel use and rising diesel surcharges. A logical inference is that secondary markets for retired but mechanically sound Euro 6 truck engines will strengthen, stimulating a niche refurbishment supply chain centred on inland shipyards.

Digitisation via RIS & DINA Improving Supply-Chain Visibility

River Information Services create unified electronic reporting and real-time traffic management, enabling skippers to pick optimal draught windows while ports pre-stage cranes and road feeders [3]International Hydrographic Organization, “The Digital Twin of the Navigable Waters: Paving the Way for E-Navigation,” iho.int. The forthcoming “digital twin” of navigable waters based on the IHO S-100 standard paves the way for seamless data exchange between maritime and inland systems. Research finds that RIS adoption can shorten route-planning times and cut administrative delays for interurban pallet flows. One immediate inference is that customs authorities gain earlier visibility over cargo manifests, potentially reducing inspection queues and favouring ports equipped with full RIS connectivity.

Restraints Impact Analysis*

| Restraint | (~) Impact on Market CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic Low-Water Events on Rhine & Danube Disrupting Load Factors | -0.8% | Rhine & Danube | Medium term (3-4 yrs) |

| Ageing Barge Fleet Facing Capex-Intensive Retrofit Mandates | -0.7% | EU-wide, Eastern Europe strongest | Medium term (3-4 yrs) |

| Port and Lock Bottlenecks Limiting Vessel Size on Secondary Canals | -0.5% | Secondary canals, Eastern Europe | Long term (≥ 5 yrs) |

| Competitive Pressure from Electrified Rail Freight in Central Europe | -0.4% | Central Europe | Medium term (3-4 yrs) |

| Source: Mordor Intelligence | |||

Chronic Low-Water Events on Rhine & Danube Disrupting Load Factors

Climate-driven low-water spells forced barges on the Rhine to sail at partial loads for several consecutive weeks in 2024, cutting German industrial output by roughly 1 % during the affected month. Similarly, parts of the Danube fell to 1.5 m depth, compelling convoys to idle or re-route. Operators mitigate with shallow-draught hull designs and dynamic cargo-allocation software, but residual uncertainty dents service reliability. From this evidence one can infer that risk-adjusted freight pricing will favour multi-hull vessels capable of continuing service at reduced draughts, even if capital costs are marginally higher.

Ageing Barge Fleet Facing Capex-Intensive Retrofit Mandates

The Rhine cargo fleet averages 1,500-tonne capacity, yet many hulls date back decades and lack pre-installed emission-control units. Retrofitting Euro 6 engines costs USD 175,000–290,000 and competes with owner plans for outright replacement by hybrid or LNG units. EU-funded programs such as MoVe IT! ease the burden, but family-owned operators with one or two barges still struggle to secure collateral for green loans. A new inference is that vertical collaboration with charterers—who may guarantee multi-year contracts in exchange for cleaner tonnage—will become a practical financing route for single-vessel entrepreneurs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

Type of Transportation: Dry Bulk Dominates While Containers Surge

Dry bulk commands the largest Europe Inland Water Freight Transport market share at 53.62 % in 2025, carrying commodities such as coal, steel inputs, and construction aggregates on high-capacity Rhine barges equivalent to 220 trucks. The segment benefits from low handling complexity, enabling steady utilisation even during economic lulls. A notable inference is that anticipated coal-phase-out policies will gradually shift barge tonne-kilometres toward biomass and recycled-metal flows, altering hold-cleaning protocols and port terminal equipment.

Containerised freight, while currently smaller, is forecast to grow at a 6.98 % CAGR from 2026-2031, significantly outpacing overall market expansion. Operators such as Contargo already field 13,498 TEU of barge capacity and plan to deploy electric-propulsion units in 2024. Liquid bulk retains stable volumes thanks to dedicated chemical park jetties, whereas roll-on/roll-off craft gain traction in city-distribution trials. An arising inference is that port planners will allocate more quay space to barge-mounted gantries capable of side-loading containers in tidal or variable river conditions.

End-Use Industry: Metallurgy Leads While Retail Accelerates

Metallurgy and mining account for the largest European Inland Water Freight Transport market size within end-use industries, holding 26.74 % share in 2025; iron ore flows on the Danube have risen 6.8 % on the back of higher steel output. The sector values barges for their high payloads and tolerance for longer transit times, turning rivers into rolling stockyards. A reasonable inference is that decarbonisation paths for steel, such as hydrogen-based direct-reduction, could introduce new upstream cargoes like iron-pellet additives, diversifying barge cargo mixes.

Consumer goods and retail, while representing a smaller base, are predicted to post an 7.93% CAGR through 2031 as e-commerce pushes parcel integrators to experiment with waterborne micro-fulfilment. Agriculture remains material, especially for grain exports from Central Europe, though the shrinking universe of small-capacity vessels strains seasonal peaks. Petrochemicals sustain solid demand via specialized tank barges equipped with inert-gas systems. A fresh inference is that the construction sector’s appetite for low-carbon cement may trigger an uptick in specialised silo-barge orders to meet urban project timelines.

Geography Analysis

The Netherlands leads the Europe Inland Water Freight Transport industry with a 32.70 % market share in 2025, underpinned by a dense canal matrix linking Rotterdam and Amsterdam with German and Belgian hinterlands. Around 35 % of intra-EU cargo tonnage transits the Dutch network, underscoring its gateway stature. Ongoing public-private programs channel capital into shore-power installations and hydrogen-ready refuelling, reinforcing environmental credentials. An inference derived here is that pilot-scale hydrogen barges may first achieve commercial viability on Dutch short-haul routes where bunkering infrastructure is densest.

Germany ranks second due to the Rhine artery feeding its industrial regions; planned upgrades will extend the “high-performance” network from 4,000 km to 9,000 km, integrating rail and river terminals. Low-water susceptibilities, however, expose manufacturers to supply chain shocks, prompting them to pre-book capacity during dry seasons. Federal subsidies for alternative-fuel retrofits have helped family operators modernise hulls, indirectly raising average fleet efficiency. A logical inference is that forward-looking shippers may negotiate index-linked freight contracts that adjust for draught-restricted payload penalties, spreading hydrological risk across supply partners.

Romania emerges as the fastest-growing geography, with a forecast CAGR of 5.98 % through 2031 as Rhine-Danube investments unlock navigation year-round. Romanian operators own the largest share of dry-cargo vessels in the Danube fleet, positioning them favourably for grain and steel inputs once corridor works finish. Nevertheless, episodic droughts lowered Danube flow to 2,900 m³/s in August 2024, below the 4,600 m³/s norm, temporarily curbing vessel draughts. EU cohesion funds earmarked for lock upgrades and dredging mitigate these constraints. An emergent inference is that Romanian logistics firms could leapfrog legacy Western European systems by adopting fully digital traffic-management from inception, avoiding incremental upgrades.

Competitive Landscape

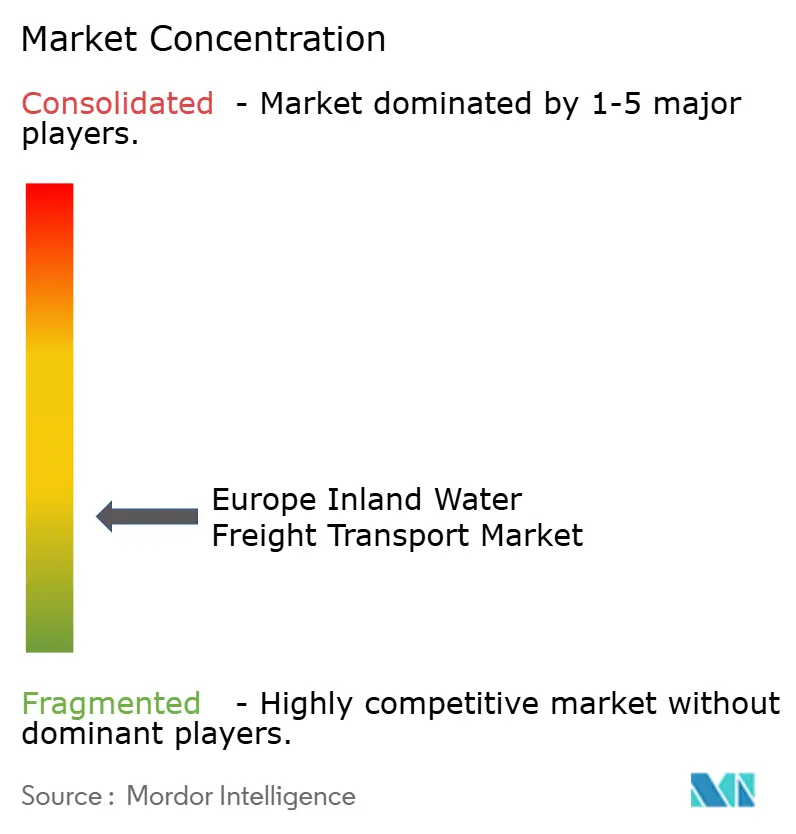

Europe Inland Water Freight Transport market competition is fragmented, with a mix of multinational integrators and region-specific family fleets. Rhenus Group has expanded via targeted acquisitions such as C. Hartwig Gdynia to reinforce its Air & Ocean divisions and cross-sell inland barge capacity to sea-freight customers. Scale allows such players to spread digital-platform costs and negotiate favourable energy contracts, pressuring smaller operators to form cooperatives. A direct inference is that software-as-a-service vendors focused on fleet-optimisation will find a ready client base among mid-tier barge owners looking to stay competitive without selling out.

Technological differentiation is becoming the new competitive lever. Contargo’s plan to introduce electric barges showcases how early deployment of zero-emission propulsion can capture environmentally conscious cargo flows and satisfy upcoming FuelEU Maritime thresholds. Parallel investments in RIS connectivity and automated mooring reduce turnaround times, amplifying asset utilisation. The logical inference is that productivity gains from digitalisation will widen profitability gaps between innovators and laggards faster than asset scale alone previously did.

Urban-logistics specialists represent a nascent but influential cohort. Firms piloting small electric or autonomous craft in Amsterdam or Paris focus on parcels and palletised goods that larger barges cannot deliver directly to quays in tight waterways. Collaboration with city councils is high because public authorities view waterborne micro-freight as a tool to meet congestion-reduction targets. From these initiatives one can infer that new licensing frameworks for urban waterways will likely emerge, potentially mirroring slot-allocation systems used in aviation.

Europe Inland Water Freight Transport Industry Leaders

Rhenus Group

HGK Shipping GmbH

Contargo GmbH & Co. KG

Danser Group

CMA CGM Inland Services

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2024: Contargo announced a major fleet expansion initiative, planning to introduce electric barges to its existing fleet of 38 barges and 18 push barges, representing a significant investment in zero-emission technology to enhance environmental performance and comply with upcoming EU regulations Contargo.

- April 2024: DP World Inland Europe formed a strategic partnership with Voies Navigables de France to develop autonomous vessel technology for urban logistics, building on the success of the 3D-printed autonomous ferry project in Paris Holland Shipyards Group.

- March 2024: Deutsche Binnenreederei AG, part of the Rhenus Group, invested EUR 45 million in fleet modernization, focusing on retrofitting existing vessels with Euro 6-compliant engines to meet stringent emission standards under the EU’s environmental regulations Rhenus DBR.

- February 2024: CMA CGM Inland Services announced a joint venture with Imperial Logistics International to develop integrated multimodal transport solutions across the Rhine-Danube corridor, targeting containerized freight growth in Central and Eastern Europe European Commission.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, the Europe inland water freight transport market covers all commercial movement of dry bulk, liquid bulk, containerized and roll-on/roll-off cargo along the continent's rivers, canals and associated inland ports. Revenues are captured at the point a licensed operator invoices for hauling a metric ton of freight over any distance, whether the vessel is self-propelled or pushed.

Scope Exclusions: Passenger cruises, dredging, offshore trans-shipment, cabotage at sea and pipeline flows fall outside our study.

Segmentation Overview

- By Type of Transportation

- Liquid Bulk Transportation

- Dry Bulk Transportation

- Containerised Freight

- Dry

- Reefer

- Roll-On / Roll-Off Cargo

- By End-Use Industry

- Agriculture & Food

- Metallurgy & Mining

- Petroleum & Chemicals

- Construction

- Energy (Biomass & Coal)

- Consumer Goods & Retail

- Others

- By Geography

- Netherlands

- Germany

- Belgium

- France

- Romania

- Bulgaria

- Rest of Europe

Detailed Research Methodology and Data Validation

Primary Research

We interviewed barge operators, river-port managers, grain exporters, petro-chemical shippers and modal-shift policy officials across the Rhine-Alpine, Danube and Seine basins. These conversations validated load-factor norms, seasonal surcharges and expected carbon-levy pass-throughs, giving us confidence to fine-tune model drivers surfaced in desk work.

Desk Research

We began by mapping the fleet, cargo mix and corridor economics through open datasets issued by Eurostat, the Central Commission for the Navigation of the Rhine, the European Commission's NAIADES dashboard and national waterway agencies. We then cross-checked traffic intensity with port authority statistics and customs filings. Our team also reviewed peer-reviewed journals on low-water impacts, trade association white papers from EBU/ESO, company 10-Ks and investor decks to benchmark average freight rates and cost structures.

Subscription resources such as D&B Hoovers for operator financials, Dow Jones Factiva for deal flow, and Questel for vessel technology patents helped us verify ownership concentration and innovation pace. The sources named illustrate our process and are not exhaustive; many additional references supported data capture and clarification.

Market-Sizing & Forecasting

A top-down reconstruction starts from Eurostat tonne-kilometer records, which we convert to revenue using corridor-specific average rates that we corroborate with sampled invoices. Supplier roll-ups on fleet capacity, bunker consumption and terminal handling charges provide a limited bottom-up lens that adjusts totals where under-reporting is suspected. Key variables like river draft days below 1.6 m, EU modal-shift incentive payout, diesel-LNG price spread, barge new-build deliveries and container penetration feed a multivariate regression to project demand to 2030. When gaps appear in operator disclosures, we interpolate using three-year moving averages anchored to verified traffic counts.

Data Validation & Update Cycle

Mordor analysts run variance checks between model outputs and independent port throughput, spot-rate indices and macro-freight elasticities. Results pass two levels of peer review before release. We refresh every twelve months and trigger interim revisions when floods, strikes or regulatory shocks materially alter traffic.

Why Mordor's Europe Inland Water Freight Transport Baseline Stays Dependable

Different publishers quote divergent values because they adopt unlike cargo scopes, pricing bases and refresh rhythms.

We acknowledge those gaps upfront and then show where our disciplined variable set leads to a sturdier midpoint.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 44.10 B (2025) | Mordor Intelligence | - |

| USD 14.48 B (2024) | Regional Consultancy A | Excludes contract charters and focuses on five core countries only |

| USD 22.70 B (2024) | Trade Journal B | Converts tonnes to value using fixed 2019 bunker prices and ignores container surcharge escalators |

The comparison shows that when scope breadth, variable realism and annual refresh are aligned, as in Mordor's approach, decision-makers gain a transparent, repeatable baseline they can trust for budgeting and strategy.

Key Questions Answered in the Report

What is the current Europe Inland Water Freight Transport market size?

The market is valued at USD 45.73 billion in 2026, with a forecast to reach USD 54.82 billion by 2031.

Which country holds the largest Europe Inland Water Freight Transport market share?

The Netherlands leads with roughly one-third of total cargo volumes due to its extensive canal system and connection to the Port of Rotterdam.

What is driving growth in containerised inland shipping?

Improved intermodal links, digital scheduling via RIS, and cost advantages under carbon pricing make containers the fastest-growing cargo type.

How are low-water events affecting the industry?

Extended droughts on the Rhine and Danube force barges to sail partially loaded or halt operations, prompting operators to invest in shallow-draught or multi-hull designs.

What regulations are influencing fleet modernisation?

FuelEU Maritime and the extension of the EU Emissions Trading System require progressive emission reductions, accelerating adoption of Euro 6, LNG, and electric propulsion technologies.

Are inland waterways being used for urban logistics?

Yes, pilot projects in Paris, Amsterdam, and Antwerp demonstrate how small electric or autonomous barges can alleviate road congestion and meet last-mile delivery needs.

Page last updated on: