Market Overview

| Study Period | 2017 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2017 - 2023 |

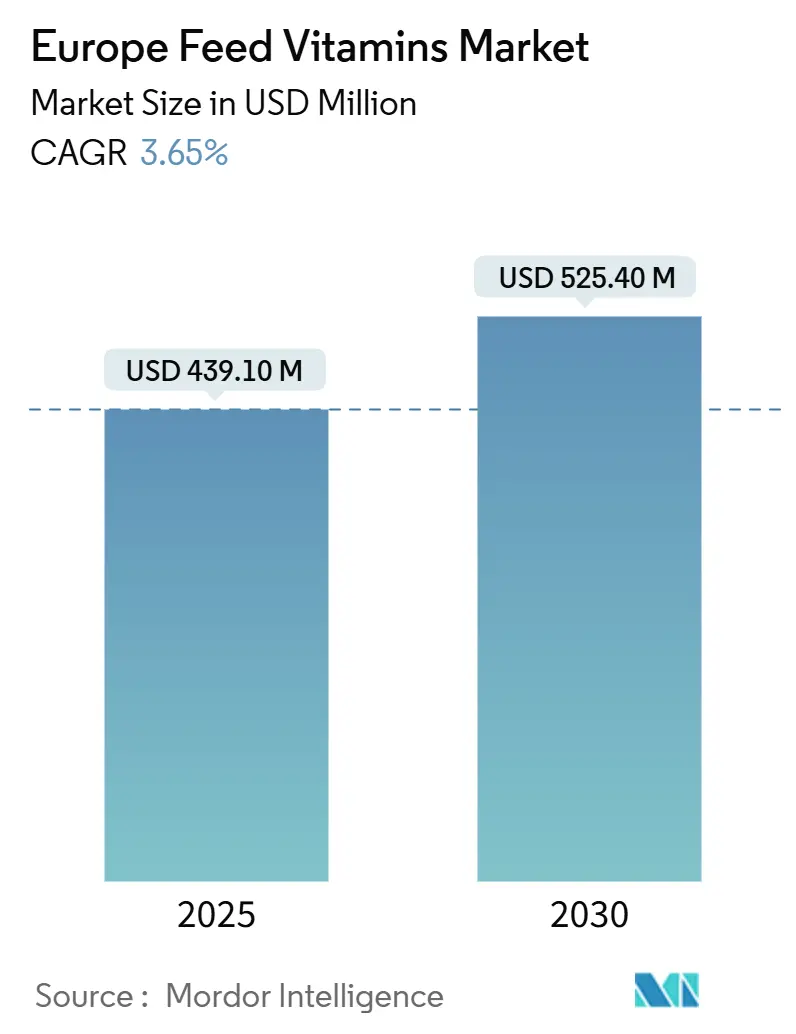

| Market Size (2025) | USD 439.10 Million |

| Market Size (2030) | USD 525.40 Million |

| Growth Rate (2025 - 2030) | 3.65% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Feed Vitamins Market Analysis by Mordor Intelligence

The Europe feed vitamins market size stands at USD 439.1 million in 2025 and is forecast to reach USD 525.4 million by 2030, expanding at a 3.65% CAGR during 2025-2030. Growth accelerates as stabilized vitamin E supply, mandatory fortification rules, and precision-nutrition adoption create steady demand across livestock sectors [1]Source: European Food Safety Authority, “Feed additives,” EFSA, efsa.europa.eu. Intensifying poultry and aquaculture production, especially in Eastern Europe and the United Kingdom, amplifies vitamin premix uptake, while synthetic biology advances lower production costs and carbon footprints. Ongoing regulatory tightening under EU Regulation 183/2005 favors established suppliers with robust dossiers and traceable supply chains, reinforcing moderate market concentration [2]Source: European Food Safety Authority, “Feed additives,” EFSA, efsa.europa.eu. The raw-material price volatility and vitamin A and D tolerance limits temper full-scale growth, nudging formulators toward efficiency-focused solutions that preserve animal performance.

Key Report Takeaways

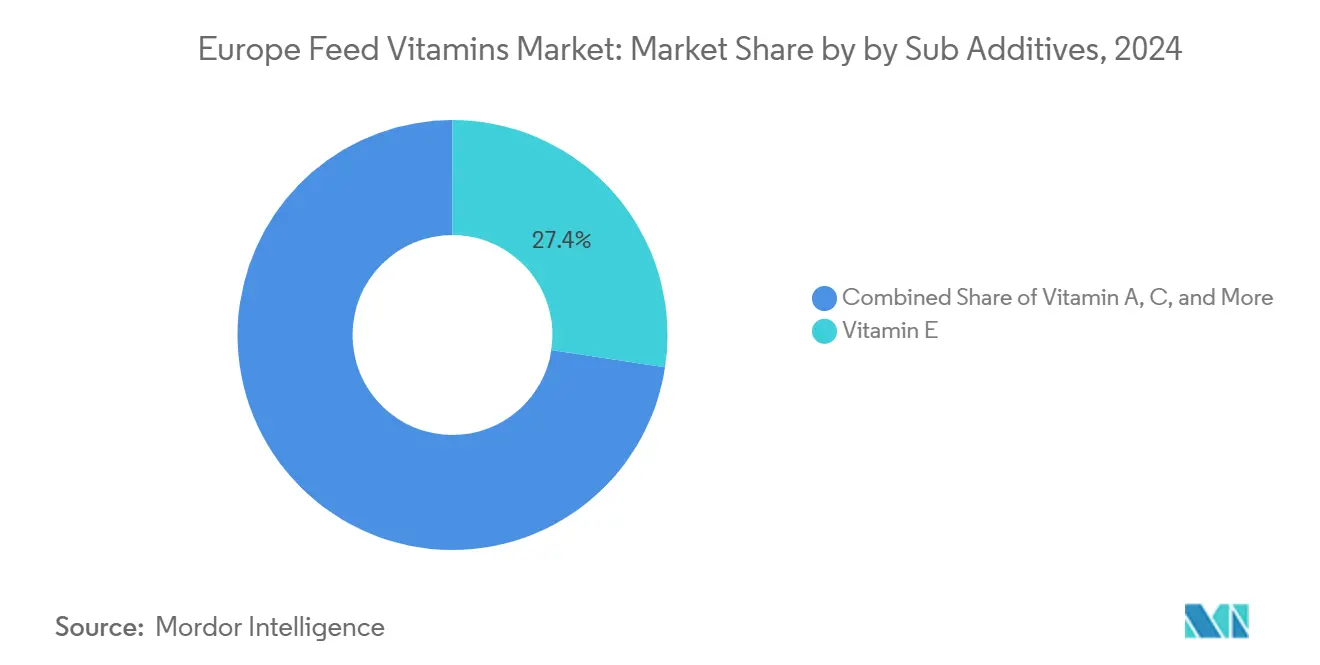

- By sub-additive, Vitamin E led with 27.4% of the European feed vitamins market share in 2024, while Vitamin C is projected to post the fastest 3.8% CAGR to 2030.

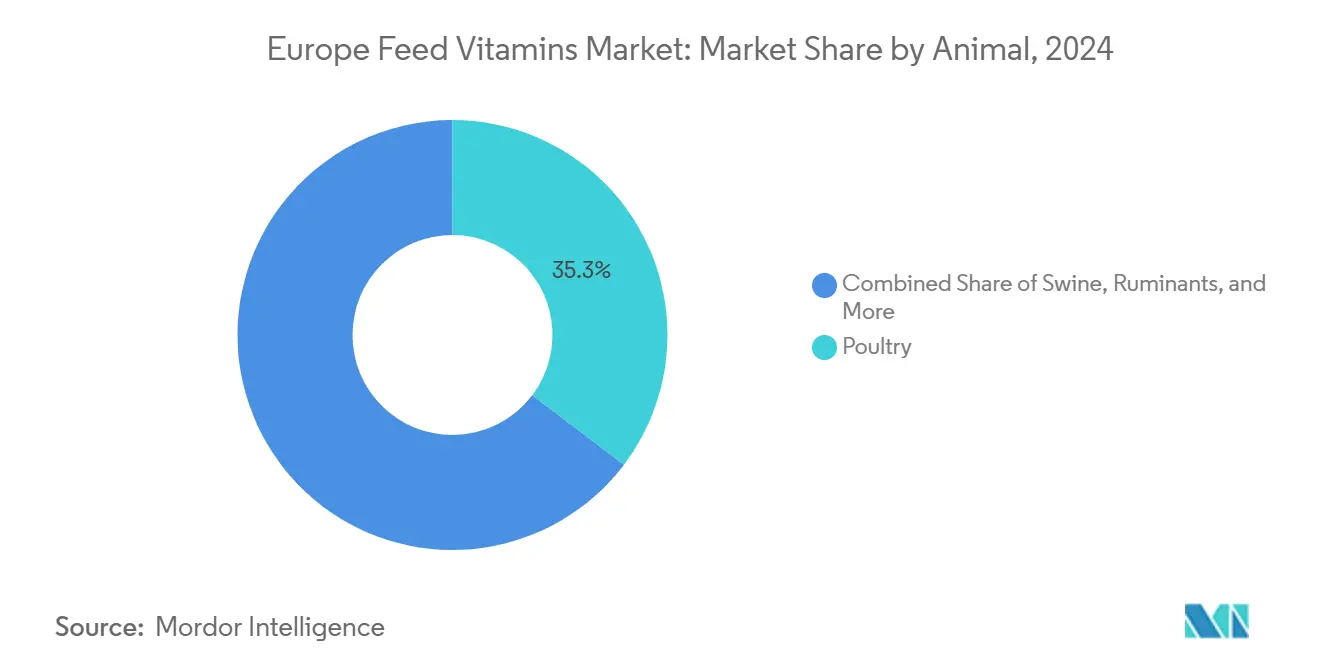

- By animal, poultry commanded 35.3% of the European feed vitamins market size in 2024, and Swine is advancing at a 4.0% CAGR through 2030.

- By geography, Spain dominated with 15.8% revenue in 2024, whereas the United Kingdom is set to grow at a 4.9% CAGR to 2030.

Europe Feed Vitamins Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising poultry meat demand in Eastern Europe | +0.8% | Poland, Hungary, Czech Republic, and Romania | Medium term (2-4 years) |

| Mandatory fortification under Regulation 183/2005 | +0.7% | European Union plus spill-over to United Kingdom and Turkey | Long term (≥4 years) |

| Recovery of vitamin E supply post-outages | +0.6% | Germany and Netherlands | Short term (≤2 years) |

| Precision-nutrition premix adoption | +0.5% | Western and Eastern Europe | Medium term (2-4 years) |

| Low-carbon vitamin synthesis via biotech | +0.4% | Denmark, Netherlands, and Germany | Long term (≥4 years) |

| Citrus-peel upcycling for vitamin C | +0.3% | Spain, Italy, and Southern France | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Poultry Meat Demand in Eastern Europe

Robust consumer preference for poultry drives broiler production up in Poland during 2024, with Hungary and the Czech Republic mirroring similar trajectories [3]Source: FEFAC, “Feed Production Statistics 2024,” European Feed Manufacturers’ Federation, fefac.eu. Larger integrators now operate vertically aligned supply chains, prompting feed mills to specify vitamin-dense premixes that boost feed-conversion ratios and meat quality. Producers increasingly rely on stabilized vitamins A, D3, and E to sustain bird health under intensive conditions, pushing procurement volumes upward. Importantly, EU animal-welfare standards extend to Eastern Europe, compelling formulators to adopt encapsulated vitamins that withstand pelleting temperatures. Cross-border trade of vitamin premixes rises as distributors serve multi-national poultry groups. The driver carries medium-term relevance because consumption patterns continue to shift from pork to poultry, but plateauing demand is projected beyond 2028 once per-capita consumption nears Western levels. Combined, these factors magnify the European feed vitamins market through larger base volumes and higher specification requirements.

Mandatory Fortification Under Regulation 183/2005

Regulation 183/2005 enforces vitamin inclusion rates and traceability in all commercial feed, guaranteeing a structural demand floor for quality-assured vitamins across Europe. Feed mills must validate potency retention, spurring uptake of coated and heat-stable forms that command premium pricing. The regulation’s scope extends to storage and transportation, requiring regular lab testing and documentation costs that smaller suppliers struggle to absorb. EFSA’s 2024 update tightened sampling frequencies and analytical methods, heightening compliance costs but reinforcing demand for certified products. As the United Kingdom realigns post-Brexit rules with European Union standards, fortification compliance broadens market depth. Over the long term, this driver ensures sustained buying cycles and positions trusted suppliers as indispensable partners, solidifying the European feed vitamins market.

Precision-Nutrition Premix Adoption

European producers deploy micro-dosing systems that tailor vitamin blends to species, genetics, and environmental data. Trouw Nutrition’s NutriOpt adjusts formulations on-farm, trimming vitamin oversupply while preserving performance. Early adopters report 15-20% vitamin savings and reduced nitrogen excretion, aligning with European Union Green Deal targets. Hardware-software integration supports real-time adjustments, enhancing vitamin bioavailability and minimizing feed wastage. The technology diffuses from Western hubs to Eastern Europe, encouraged by integrators seeking cost and sustainability gains. Medium-term uptake accelerates the European feed vitamins market’s shift from commodity volumes to value-added precision solutions.

Citrus-Peel Upcycling for Vitamin C

Southern European juice processors generate abundant citrus peels, now valorized through PeelPioneers’ enzymatic hydrolysis that yields feed-grade vitamin C concentrates at 25-30% lower costs [4]Source: PeelPioneers, “Citrus Peel Upcycling for Feed Ingredients,” PeelPioneers, peelpioneers.nl. Partnerships with Büfa Chemikalien extend distribution into Germany and Austria, shortening logistics distances and shrinking carbon footprints. The initiative fits circular-economy principles, converting waste into high-value additives. Medium-term commercialization strengthens local sourcing resiliency and lowers import dependence for vitamin C, expanding market access for price-sensitive feed mills and enhancing overall Europe feed vitamins market competitiveness.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile prices of petro-derived intermediates | −0.8% | Germany, the Netherlands, and broader global supply | Short term (≤2 years) |

| Tightening upper-tolerance limits for vitamins A and D | −0.7% | European Union and Union Kingdom | Long term (≥4 years) |

| Rapid substitution by functional probiotics | −0.5% | Western Europe, and expanding eastward | Medium term (2-4 years) |

| Chinese niacin supply crunch | −0.4% | Europe-wide premix manufacturers | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Tightening Upper-Tolerance Limits for Vitamins A and D

EFSA’s 2024 review retained strict adult upper limits and tightened pediatric thresholds for vitamins A and D, translating into lower permissible inclusion in animal feeds to avoid food-chain residues. Breeding and high-performance diets that once differentiated via elevated dosages now confront regulatory ceilings, curbing premium-segment volume expansion. Compliance enforcement necessitates costly analytical upgrades at feed mills and restricts marketing claims, tempering upside potential in the European feed vitamins market over the long term.

Rapid Substitution by Functional Probiotics

European poultry producers increasingly replace certain vitamin levels with probiotic solutions that enhance gut health and nutrient absorption. Kemin’s PROSIDIUM launch illustrates this trend, advertising improved vitamin uptake at lower inclusion rates. Early adopters report a 5-10% reduction in vitamin premix volumes, especially in broiler diets. As probiotic efficacy gains empirical validation, broader substitution threatens baseline vitamin demand, especially among price-sensitive integrators. Medium-term adoption thus restrains the European feed vitamins market volume growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sub-Additive: Vitamin E Dominance with Vitamin C on Fast Track

Vitamin E accounted for 27.4% of the European feed vitamins market share in 2024 due to its role in oxidative stability and immunity, especially in poultry and swine diets. Post-outage supply recovery normalized prices, prompting integrators to reinstate full dosages. Meanwhile, Vitamin C is projected to increase at the highest 3.8% CAGR, driven by aquaculture’s stress-mitigation protocols and citrus-waste upcycling that eases cost barriers. The European feed vitamins market size for vitamin C is projected to increase by 2030, reflecting this adoption curve. Fermentation-based processes for riboflavin, biotin, and other B-vitamins further recalibrate cost structures, with start-ups claiming 30-40% cost reductions that entice mid-tier premix blenders. Collectively, sub-additive diversification ensures stable market value despite dosage ceiling pressures.

Emerging biosynthetic technologies enable in situ vitamin activation, improving bioavailability while lowering inclusion rates. For example, BASF’s fermentation-derived riboflavin offers 30% lower CO₂ emissions, aligning with procurement criteria of eco-conscious feed mills across Germany and France. This synergy between sustainability and efficacy secures a long-term competitive position for biotech-driven sub-additives within the European feed vitamins market.

By Animal: Poultry Leads, Aquaculture Accelerates

Poultry remained the largest contributor, commanding 35.3% of Europe's feed vitamins market size in 2024, due to rapid production cycles and obligatory supplementation protocols. Optimized vitamin premixes enhance feed conversion and carcass quality, with vitamin A and E dosages tailored for climate stress factors across Southern Europe. The swine 4.0% CAGR through 2030, positioning it as the fastest-growing consumer of specialized vitamins. Aquaculture and ruminant segments sustain incremental gains through precision-nutrition adoption and fortified replacers, keeping the European feed vitamins market diversified against sector-specific shocks.

Precision-feeding software now integrates metabolic models for broilers, layers, salmon, and shrimp, recalculating vitamin requirements daily. Commercial deployments in Scotland indicate an increase in feed cost savings and improved fillet pigmentation, encouraging replication across European hatcheries. Consequently, aquaculture’s share of Europe's feed vitamins market is projected to increase by 2030, shrinking poultry’s dominance but enhancing total market resiliency.

Geography Analysis

Spain led the European feed vitamins market with 15.8% revenue in 2024, leveraging its concentrated poultry farms and extensive swine operations across Catalonia and Andalusia. Integrated feed giants such as Nanta employ stabilized vitamins that resist Mediterranean storage temperatures, ensuring potency during peak summers. Spain’s flourishing aquaculture clusters along the Galicia coast further diversify vitamin demand, particularly for vitamin C and B-complex blends tailored to cold-water species.

The United Kingdom exhibits the fastest 4.9% CAGR to 2030, driven by post-Brexit feed-security initiatives that prioritize domestic vitamin sourcing and Scottish salmon expansion. Research collaborations between universities and feed companies accelerate the adoption of encapsulated vitamins and real-time nutrient monitoring. With new land-based recirculating aquaculture systems planned in northern England, vitamin premix suppliers find fresh volume streams, injecting dynamism into the European feed vitamins market.

Germany, France, and the Netherlands collectively held a significant portion of regional revenue in 2024. Germany’s feed-production leadership and BASF’s fermentation innovations anchor vitamin supply reliability, while France’s dairy and poultry integrators deploy data-driven feeding protocols that standardize vitamin use across co-operatives. The Netherlands operates as a distribution and innovation hub, housing encapsulation specialists that license technology across the continent, thus facilitating sophisticated vitamin delivery and sustaining premium pricing. Eastern European countries such as Poland and Hungary, though smaller individually, collectively drive meaningful incremental demand, buoyed by rising meat consumption and modernization investments.

Competitive Landscape

The top five suppliers controlled a significant share of the European feed vitamins market in 2024, indicating a moderately concentrated landscape conducive to both global majors and agile niche players. DSM-Firmenich led with a significant share, leveraging vertically integrated production, multiple European plants, and strong regulatory dossiers. Brenntag and BASF together supplied 21.6%, using well-established logistics and technical services to defend their share.

Kemin’s 2024 acquisition of microbiome specialist Bactana highlights a strategic pivot toward combined vitamin-probiotic solutions that decrease reliance on antibiotics, echoing broader industry convergence. Emerging biotech firms capitalize on green credentials to penetrate high-margin segments, yet must navigate stringent EFSA authorization hurdles that advantage incumbents.

Strategic themes include capacity expansion to hedge supply shocks, sustainability-branded products, and integrated digital platforms for nutrient management. BASF’s Ludwigshafen restart at 70% capacity in early 2025 mitigates vitamin A and E tightness and re-establishes supply stability. Meanwhile, distributors enhance traceability platforms to meet customer ESG and regulatory reporting needs. This competitive interplay sustains innovation velocity and balances supply resilience in the European feed vitamins market.

Europe Feed Vitamins Industry Leaders

Adisseo

Archer Daniel Midland Co.

BASF SE

Brenntag SE

DSM-Firmenich

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Cargill completed the sale of 2 Romanian feed mills to Carmistin, streamlining its European operations while maintaining focus on premium vitamin premix manufacturing through its Provimi and Neolac brands. This strategic divestiture allows Cargill to concentrate resources on high-value nutritional solutions and precision feeding technologies across core European markets.

- February 2025: Nutreco received a Dutch government grant for developing nitrogen emission reduction solutions in animal nutrition, supporting research into vitamin supplementation strategies that optimize protein utilization and reduce environmental impact. The funding accelerates development of precision nutrition platforms that adjust vitamin inclusion based on real-time animal performance data.

- August 2024: Kemin Industries launched PROSIDIUM, a precision-dosed intestinal health solution that optimizes vitamin absorption efficiency in broiler diets. The product addresses growing demand for alternatives to antibiotic growth promoters while maintaining production performance through enhanced nutrient utilization.

Europe Feed Vitamins Market Report Scope

Vitamin A, Vitamin B, Vitamin C, Vitamin E are covered as segments by Sub Additive. Aquaculture, Poultry, Ruminants, Swine are covered as segments by Animal. France, Germany, Italy, Netherlands, Russia, Spain, Turkey, United Kingdom are covered as segments by Country.Sub Additive

| Vitamin A |

| Vitamin B |

| Vitamin C |

| Vitamin E |

| Other Vitamins |

Animal

| Aquaculture | Fish |

| Shrimp | |

| Other Aquaculture Species | |

| Poultry | Broiler |

| Layer | |

| Other Poultry Birds | |

| Ruminants | Beef Cattle |

| Dairy Cattle | |

| Other Ruminants | |

| Swine | |

| Other Animals |

Geography

| France |

| Germany |

| Italy |

| Netherlands |

| Russia |

| Spain |

| Turkey |

| United Kingdom |

| Rest of Europe |

| Sub Additive | Vitamin A | |

| Vitamin B | ||

| Vitamin C | ||

| Vitamin E | ||

| Other Vitamins | ||

| Animal | Aquaculture | Fish |

| Shrimp | ||

| Other Aquaculture Species | ||

| Poultry | Broiler | |

| Layer | ||

| Other Poultry Birds | ||

| Ruminants | Beef Cattle | |

| Dairy Cattle | ||

| Other Ruminants | ||

| Swine | ||

| Other Animals | ||

| Geography | France | |

| Germany | ||

| Italy | ||

| Netherlands | ||

| Russia | ||

| Spain | ||

| Turkey | ||

| United Kingdom | ||

| Rest of Europe | ||

Market Definition

- FUNCTIONS - For the study, feed additives are considered to be commercially manufactured products that are used to enhance characteristics such as weight gain, feed conversion ratio, and feed intake when fed in appropriate proportions.

- RESELLERS - Companies engaged in reselling feed additives without value addition have been excluded from the market scope, to avoid double counting.

- END CONSUMERS - Compound feed manufacturers are considered to be end-consumers in the market studied. The scope excludes farmers buying feed additives to be used directly as supplements or premixes.

- INTERNAL COMPANY CONSUMPTION - Companies engaged in the production of compound feed as well as the manufacturing of feed additives are part of the study. However, while estimating the market sizes, the internal consumption of feed additives by such companies has been excluded.

| Keyword | Definition |

|---|---|

| Feed additives | Feed additives are products used in animal nutrition for purposes of improving the quality of feed and the quality of food from animal origin, or to improve the animals’ performance and health. |

| Probiotics | Probiotics are microorganisms introduced into the body for their beneficial qualities. (It maintains or restores beneficial bacteria to the gut). |

| Antibiotics | Antibiotic is a drug that is specifically used to inhibit the growth of bacteria. |

| Prebiotics | A non-digestible food ingredient that promotes the growth of beneficial microorganisms in the intestines. |

| Antioxidants | Antioxidants are compounds that inhibit oxidation, a chemical reaction that produces free radicals. |

| Phytogenics | Phytogenics are a group of natural and non-antibiotic growth promoters derived from herbs, spices, essential oils, and oleoresins. |

| Vitamins | Vitamins are organic compounds, which are required for normal growth and maintenance of the body. |

| Metabolism | A chemical process that occurs within a living organism in order to maintain life. |

| Amino acids | Amino acids are the building blocks of proteins and play an important role in metabolic pathways. |

| Enzymes | Enzyme is a substance that acts as a catalyst to bring about a specific biochemical reaction. |

| Anti-microbial resistance | The ability of a microorganism to resist the effects of an antimicrobial agent. |

| Anti-microbial | Destroying or inhibiting the growth of microorganisms. |

| Osmotic balance | It is a process of maintaining salt and water balance across membranes within the body's fluids. |

| Bacteriocin | Bacteriocins are the toxins produced by bacteria to inhibit the growth of similar or closely related bacterial strains. |

| Biohydrogenation | It is a process that occurs in the rumen of an animal in which bacteria convert unsaturated fatty acids (USFA) to saturated fatty acids (SFA). |

| Oxidative rancidity | It is a reaction of fatty acids with oxygen, which generally causes unpleasant odors in animals. To prevent these, antioxidants were added. |

| Mycotoxicosis | Any condition or disease caused by fungal toxins, mainly due to contamination of animal feed with mycotoxins. |

| Mycotoxins | Mycotoxins are toxin compounds that are naturally produced by certain types of molds (fungi). |

| Feed Probiotics | Microbial feed supplements positively affect gastrointestinal microbial balance. |

| Probiotic yeast | Feed yeast (single-cell fungi) and other fungi used as probiotics. |

| Feed enzymes | They are used to supplement digestive enzymes in an animal’s stomach to break down food. Enzymes also ensure that meat and egg production is improved. |

| Mycotoxin detoxifiers | They are used to prevent fungal growth and to stop any harmful mold from being absorbed in the gut and blood. |

| Feed antibiotics | They are used both for the prevention and treatment of diseases but also for rapid growth and development. |

| Feed antioxidants | They are used to protect the deterioration of other feed nutrients in the feed such as fats, vitamins, pigments, and flavoring agents, thus providing nutrient security to the animals. |

| Feed phytogenics | Phytogenics are natural substances, added to livestock feed to promote growth, aid in digestion, and act as anti-microbial agents. |

| Feed vitamins | They are used to maintain the normal physiological function and normal growth and development of animals. |

| Feed flavors and sweetners | These flavors and sweeteners help to mask tastes and odors during changes in additives or medications and make them ideal for animal diets undergoing transition. |

| Feed acidifiers | Animal feed acidifiers are organic acids incorporated into the feed for nutritional or preservative purposes. Acidifiers enhance congestion and microbiological balance in the alimentary and digestive tracts of livestock. |

| Feed minerals | Feed minerals play an important role in the regular dietary requirements of animal feed. |

| Feed binders | Feed binders are the binding agents used in the manufacture of safe animal feed products. It enhances the taste of food and prolongs the storage period of the feed. |

| Key Terms | Abbreviation |

| LSDV | Lumpy Skin Disease Virus |

| ASF | African Swine Fever |

| GPA | Growth Promoter Antibiotics |

| NSP | Non-Starch Polysaccharides |

| PUFA | Polyunsaturated Fatty Acid |

| Afs | Aflatoxins |

| AGP | Antibiotic Growth Promoters |

| FAO | The Food And Agriculture Organization of the United Nations |

| USDA | The United States Department of Agriculture |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms